Hotel Industry Trends & Predictions 1 - Presented by Stephen Rushmore Jr., MAI, CRE, FRICS President...

24

-1- Presented by Stephen Rushmore Jr., MAI, CRE, FRICS President and CEO of HVS Hotel Industry Trends & Predictions

Transcript of Hotel Industry Trends & Predictions 1 - Presented by Stephen Rushmore Jr., MAI, CRE, FRICS President...

- 1 -

Presented by Stephen Rushmore Jr., MAI, CRE, FRICS

President and CEO of HVS

Hotel Industry Trends & Predictions

- 2 -

The Last Ten Years

- 3 -

The Next Four Years

- 4 -

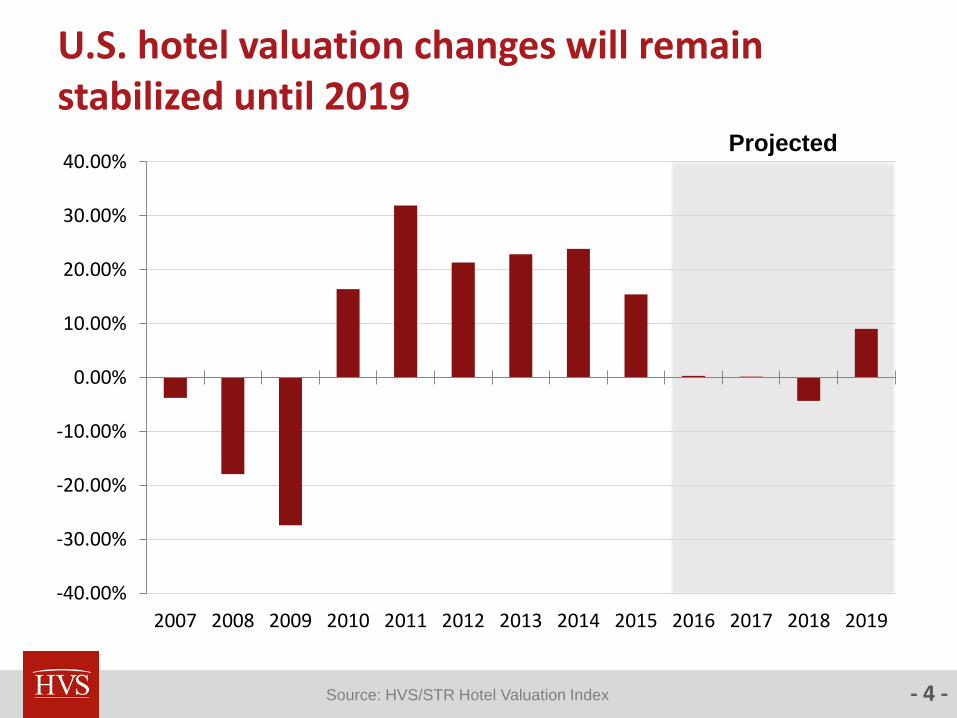

U.S. hotel valuation changes will remain stabilized until 2019

Projected

Source: HVS/STR Hotel Valuation Index

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

- 5 -

The HVI measures changes in value and provides a tool for identifying hotel acquisition and disposition opportunities

The 2016 HVS-STR Hotel Valuation Index (HVI)

- 6 -

Oakland and San Jose markets appreciated the most in value during 2015

Source: HVS/STR Hotel Valuation Index

0% 5% 10% 15% 20% 25% 30%

Oakland

San Jose

Tampa

Phoenix

Salt Lake City

Richmond

Portland

San Diego

Sacramento

Savannah

United States

- 7 -

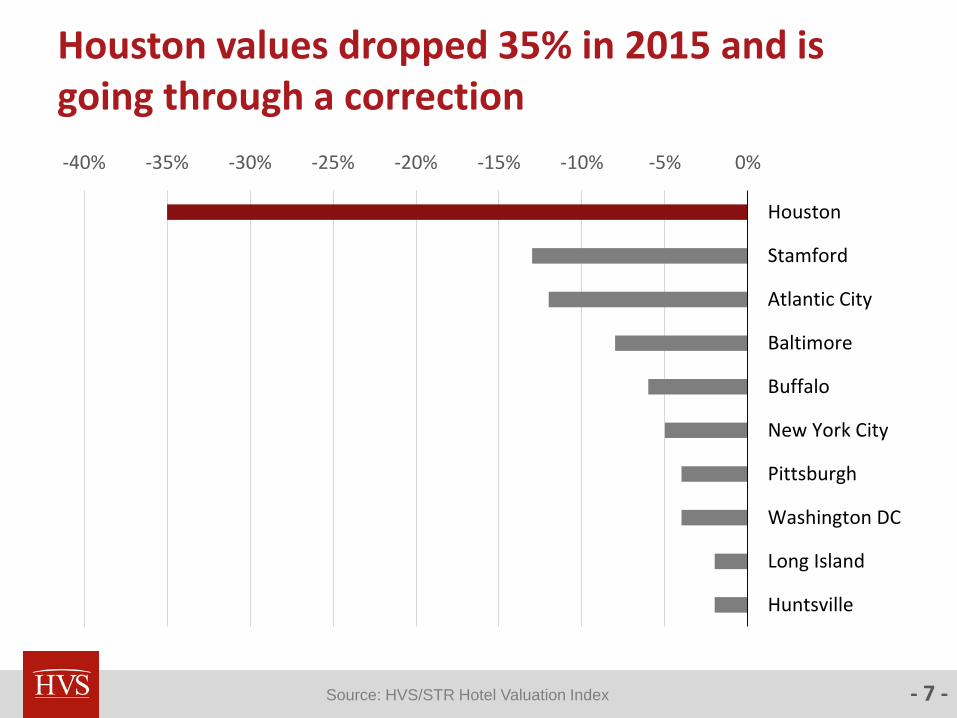

Houston values dropped 35% in 2015 and is going through a correction

Source: HVS/STR Hotel Valuation Index

-40% -35% -30% -25% -20% -15% -10% -5% 0%

Houston

Stamford

Atlantic City

Baltimore

Buffalo

New York City

Pittsburgh

Washington DC

Long Island

Huntsville

- 8 -

Huntsville and San Francisco predicted to show largest value appreciation through 2019

0% 5% 10% 15% 20% 25% 30%

Huntsville

San Francisco

Sacramento

Boston

San Diego

Los Angeles

Las Vegas

Winston-Salem

Oakland

Charlotte

United States

Source: HVS/STR Hotel Valuation Index

- 9 -

New York City and Tallahassee expected to decline in value by 12% through 2019

Source: HVS/STR Hotel Valuation Index

-14% -12% -10% -8% -6% -4% -2% 0% 2% 4% 6%

New York City

Tallahassee

Miami

Hartford

Salt Lake City

Cleveland

Denver

Minneapolis

Milwaukee

Atlantic City

- 10 -

Nashville and NYC will see the largest supply increases by 2019

0.00% 5.00% 10.00% 15.00% 20.00% 25.00%

Nashville

NYC

Charleston

Milwaukee

Cleveland

New Orleans

Indianapolis

Columbus

Houston

Dallas

United States

Source: HVS/STR Hotel Valuation Index

- 12 -

Transactions

- 13 -

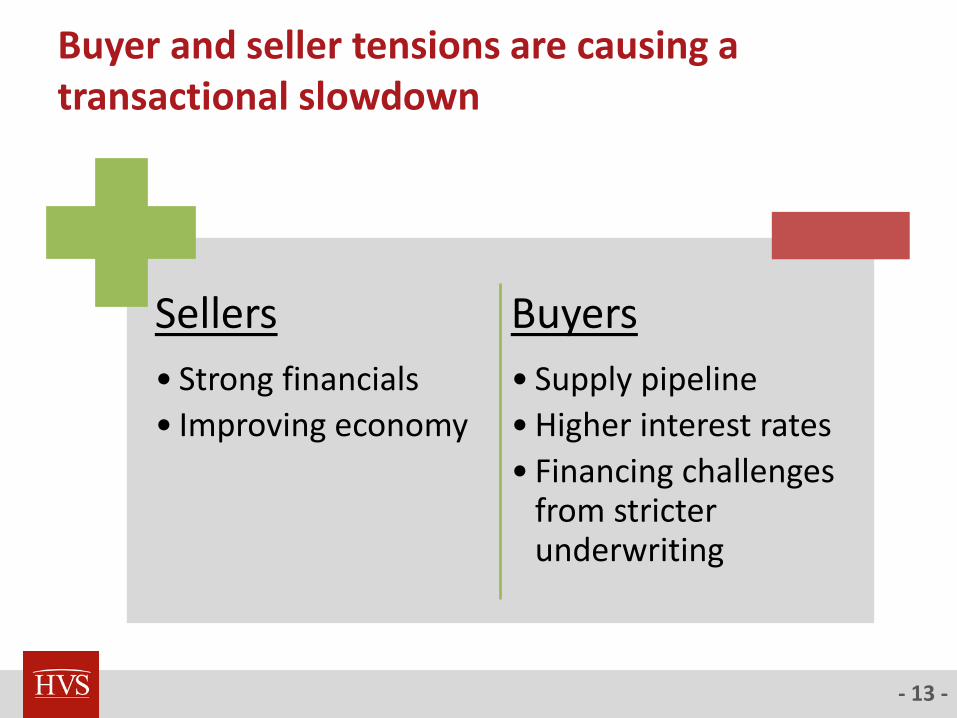

Buyer and seller tensions are causing a transactional slowdown

Sellers

• Strong financials

• Improving economy

Buyers

• Supply pipeline

•Higher interest rates

• Financing challenges from stricter underwriting

- 14 -

Transactional slowdown won’t rebound for a couple more years

0

100

200

300

400

500

6002

01

4 Q

1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

Source: RCA

- 15 -

Average cap rates have increased an average of 50 basis points from last year

9.50%

8.50%

7.50%

5.0% 6.0% 7.0% 8.0% 9.0% 10.0%

Limited Service

Select Service

Full Service

Source: HVS

- 16 -

In summary…

Most markets Values will be stabilized and will rebound in 2019 due to newsupply financing constraints

Nashville Significant supply increase through 2019

New York City Significant supply increase through 2019. Values will decline slightly over next four years.

San Francisco High valuation appreciation through 2019

Huntsville Long-term opportunity for value growth

Houston Going through a correction, but it will recover over the next four years

- 17 -

Miami

- 18 -

New supply will impact Miami’s performance over the next four years

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Supply Demand

Projected

Source: HVS & STR

- 19 -

Hotel values projected to decrease Miami through 2018 and rebounding in 2019

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Projected

Source: HVS/STR Hotel Valuation Index

- 20 -

2016 Q4 Reservations on the books showing decline from previous year

Source: TravelClick

-2.5% ADR

-4.2% Occupancy

- 21 -

REVPAR is expected to decline through 2018 as new supply is absorbed and dollar remains strong

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Projected

Source: HVS & STR

- 22 -

Median cap rate 7.9% 2016 YTD

Transactions for YTD 2016 Price/Room

The Sagamore, Miami Beach $677,419

The Confidante, Miami Beach 603,718

Marriott Vacation Club, Miami Beach 462,184

Viceroy, Brickell (conversion to W) 435,811

Sadigo Court, Miami Beach 432,833

Holiday Inn, Coral Gables 283,871

Staybridge Suites Miami, Doral 187,500

Holiday Inn Miami, Doral 155,039

Best Western on the Bay 118,110

Source: HVS & RCA

- 23 -

Opportunities still exist in Miami, but be cautious

Threats

New supply, especially in upscale tier

New supply in Brickell and Downtown submarkets

Strong dollar impact on rate

Opportunities

Development of convention-oriented hotels in Downtown or Miami Beach

Development opportunities in the Airport and the Design District

Globally, the price per room is relatively inexpensive

- 24 -

Stephen Rushmore Jr., MAI, CRE, FRICS

+1 617-868-6840@HVS_Consulting