Hostile Takeovers and Defenses - FKI

66

© 2006 Cleary Gottlieb Steen & Hamilton LLP. All rights reserved. Hostile Takeovers and Defenses June 22, 2006

Transcript of Hostile Takeovers and Defenses - FKI

© 2006 Cleary Gottlieb Steen & Hamilton LLP. All rights reserved.

Hostile Takeovers and Defenses

June 22, 2006

2

Table of Contents

1. Global Takeover Activity

2. Shareholder and Hedge Fund Activism

3. Are Korean Companies Susceptible to Hostile Activity?

4. Hostile Strategies and Tactics

5. U.S.-Style Structural Defenses: Can They Work in Korea?

6. Other Measures to Minimize Hostile Risk

7. Practical Guidelines for Preparation

8. Selected Speaker Biographies

Annex A: Recent Hostile Activities in Korea

3

Hostile Takeovers and Defenses

Speakers– Paul J. Shim, Partner, Cleary Gottlieb Steen & Hamilton LLP

(New York)– Neil Q. Whoriskey, Partner, Cleary Gottlieb Steen & Hamilton LLP

(New York)– Sang Jin Han, Partner, Cleary Gottlieb Steen & Hamilton LLP

(New York)– Hee Chul Kang, Partner, 법무법인율촌

Moderator– Yong Guk Lee, Partner, Cleary Gottlieb Steen & Hamilton LLP

(Hong Kong)

Global Takeover Activity

5

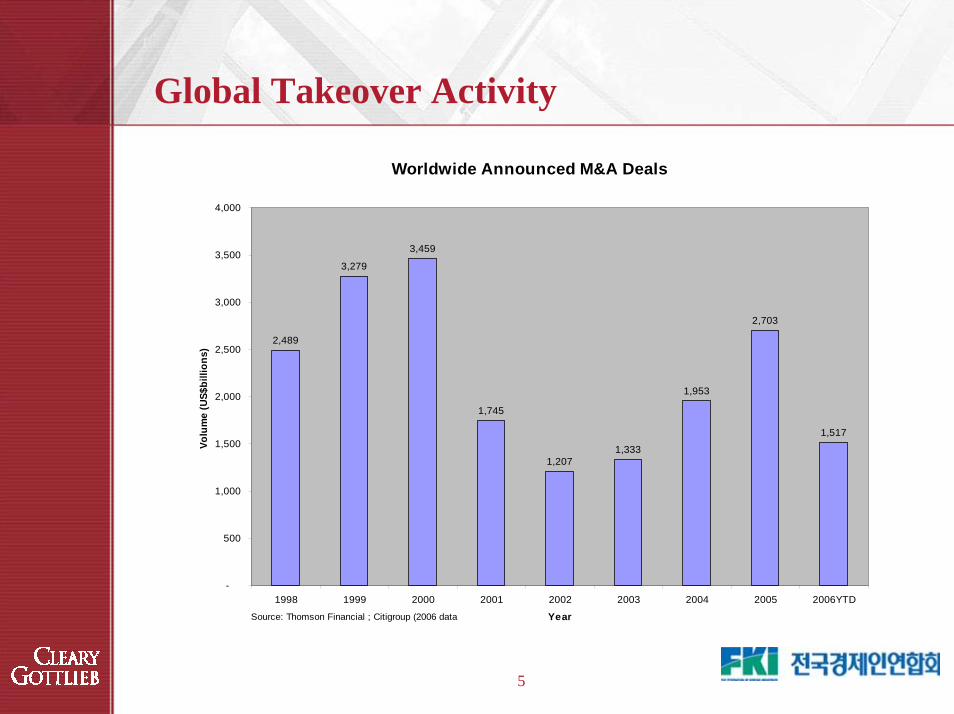

Global Takeover Activity

Worldwide Announced M&A Deals

2,489

3,279

3,459

1,745

1,2071,333

1,953

2,703

1,517

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1998 1999 2000 2001 2002 2003 2004 2005 2006YTD

Year

Volu

me

(US$

billi

ons)

Source: Thomson Financial ; Citigroup (2006 data

6

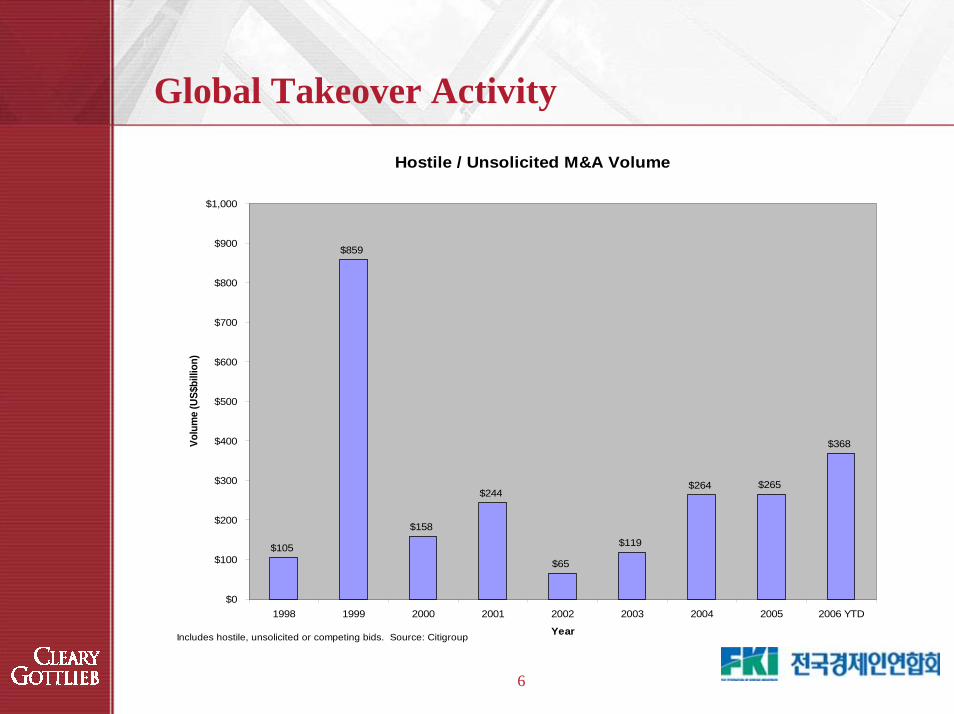

Global Takeover Activity

Hostile / Unsolicited M&A Volume

$105

$859

$158

$244

$65

$119

$264 $265

$368

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 YTD

Year

Volu

me

(US$

billi

on)

Includes hostile, unsolicited or competing bids. Source: Citigroup

7

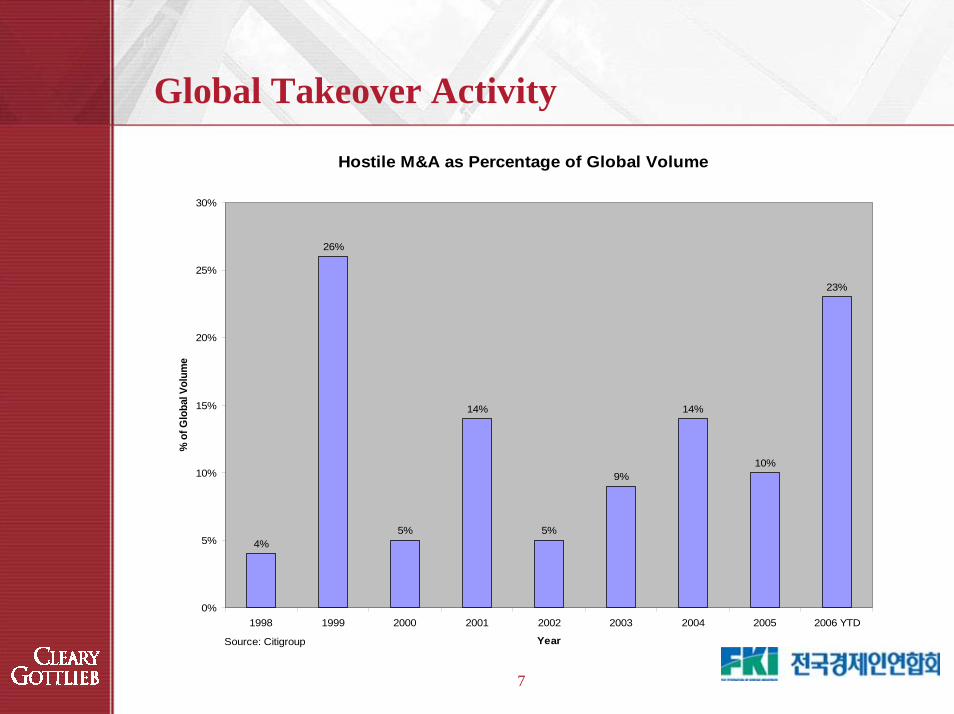

Global Takeover Activity

Hostile M&A as Percentage of Global Volume

4%

26%

5%

14%

5%

9%

14%

10%

23%

0%

5%

10%

15%

20%

25%

30%

1998 1999 2000 2001 2002 2003 2004 2005 2006 YTD

Year

% o

f Glo

bal V

olum

e

Source: Citigroup

8

Global Takeover Activity

Growth in Contested Activity– There were 38 hostile bids announced globally in the first quarter of 2006 with

a total value of $236 billion (including BASF – Engelhard and Mittal Steel –Arcelor). 2006 YTD hostile M&A volume increased to $368 billion

Reasons for Growth in Contested Activity– Strong economies and cash flow– Popularity of hedge funds– Environment of increased shareholder activism– Low interest rates– Globalization and worldwide consolidation of key industries– Globalization of capital markets– Newfound focus on corporate governance and valuation penalty for poor

behavior– The “stigma” that strategic buyers once associated with hostile transactions is

gone given the increase in unsolicited transactions initiated by blue-chip companies

9

Global Takeover Activity

Are There Benefits to Hostile Activity?– Can replace entrenched management and lead to improved corporate

governance and transparency– Can help to maximize corporate value at underperforming companies – The threat of a hostile takeover gives incumbent managers an incentive to

increase corporate value/meet market expectations

What’s Bad About Hostile Takeovers?– Very costly to launch and defend hostile takeovers– Defense of hostile takeovers may entail short-term measures (such as

payment of dividends, share repurchase to boost stock price or payment of “greenmail” to acquirers) that may erode the target’s long-term competitiveness

– Companies could potentially become “overly-responsive” to market expectations

Shareholder and Hedge Fund Activism

11

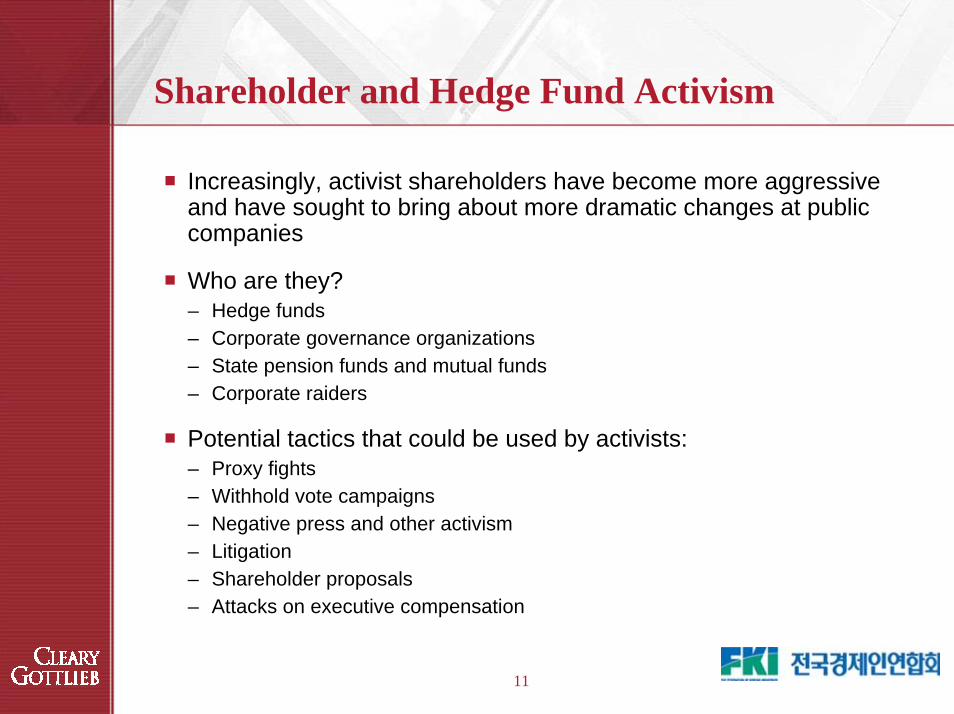

Shareholder and Hedge Fund Activism

Increasingly, activist shareholders have become more aggressive and have sought to bring about more dramatic changes at public companies

Who are they? – Hedge funds– Corporate governance organizations– State pension funds and mutual funds– Corporate raiders

Potential tactics that could be used by activists:– Proxy fights– Withhold vote campaigns– Negative press and other activism– Litigation– Shareholder proposals– Attacks on executive compensation

12

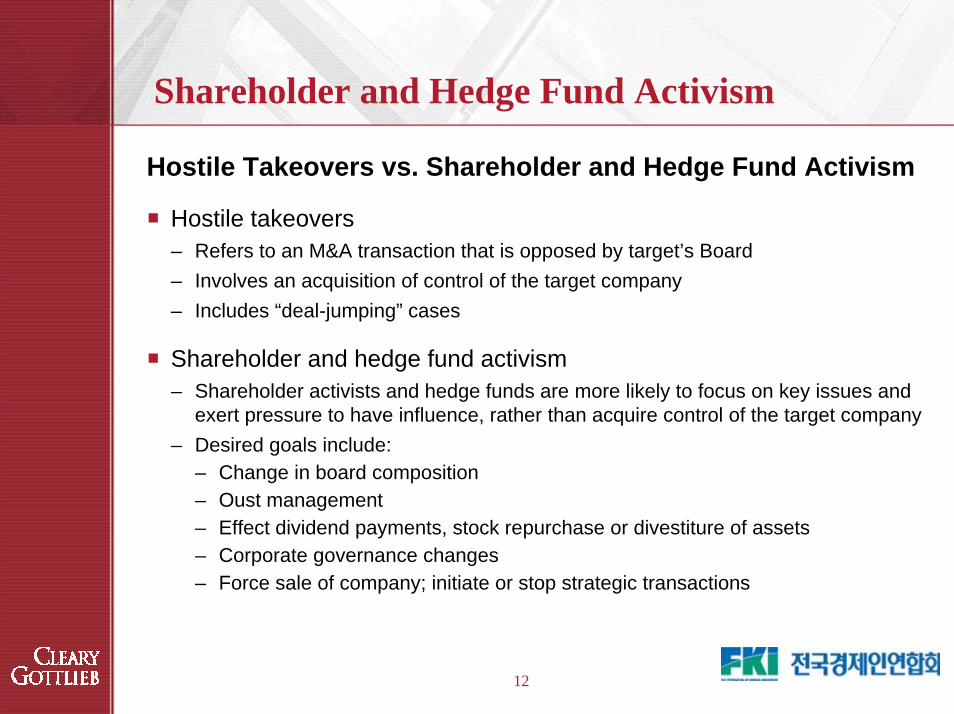

Shareholder and Hedge Fund Activism

Hostile Takeovers vs. Shareholder and Hedge Fund Activism

Hostile takeovers– Refers to an M&A transaction that is opposed by target’s Board– Involves an acquisition of control of the target company– Includes “deal-jumping” cases

Shareholder and hedge fund activism– Shareholder activists and hedge funds are more likely to focus on key issues and

exert pressure to have influence, rather than acquire control of the target company– Desired goals include:

– Change in board composition– Oust management– Effect dividend payments, stock repurchase or divestiture of assets– Corporate governance changes– Force sale of company; initiate or stop strategic transactions

13

Shareholder and Hedge Fund Activism

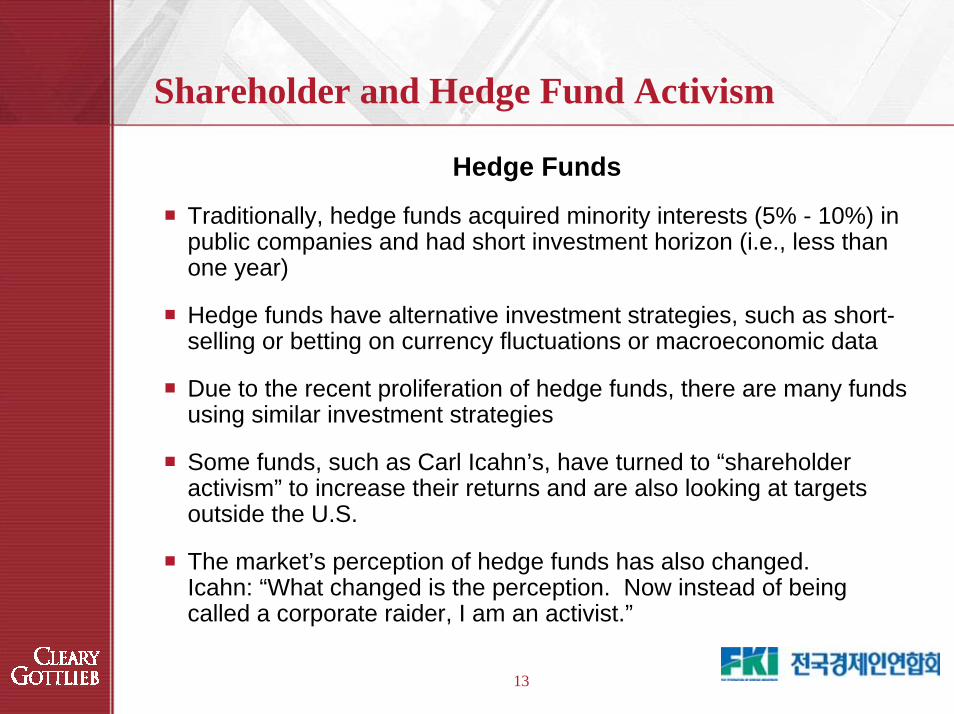

Hedge Funds

Traditionally, hedge funds acquired minority interests (5% - 10%) in public companies and had short investment horizon (i.e., less than one year)

Hedge funds have alternative investment strategies, such as short-selling or betting on currency fluctuations or macroeconomic data

Due to the recent proliferation of hedge funds, there are many funds using similar investment strategies

Some funds, such as Carl Icahn’s, have turned to “shareholder activism” to increase their returns and are also looking at targets outside the U.S.

The market’s perception of hedge funds has also changed. Icahn: “What changed is the perception. Now instead of being called a corporate raider, I am an activist.”

14

Shareholder and Hedge Fund Activism

Hedge Funds (continued)

Common features of hedge fund activism– Often no credible takeover proposal to acquire target– Use of derivatives and trading strategies to acquire significant positions, quietly

and with stealth– Exhaustive review of target’s strengths and vulnerabilities, including

shareholder sentiment, business, capital structure, corporate governance and takeover defenses

– Coordination with other shareholders (especially other hedge funds)– Willingness to pursue aggressive tactics

Common targets of hedge fund activism– Diversified companies– Underperforming companies – Overcapitalized companies (companies with significant cash balances) – Companies in consolidating industries

15

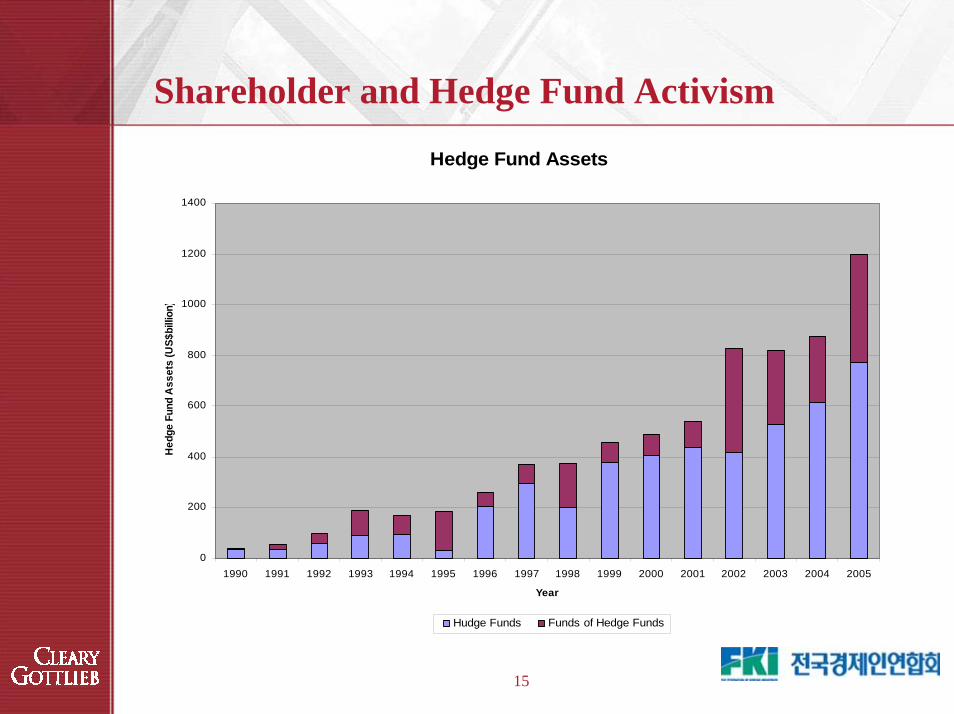

Shareholder and Hedge Fund Activism

Hedge Fund Assets

0

200

400

600

800

1000

1200

1400

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Year

Hed

ge F

und

Ass

ets

(US$

billi

on)

Hudge Funds Funds of Hedge Funds

Are Korean Companies Susceptible to Hostile Activity?

17

Are Korean Companies Susceptible to Hostile Activity?

Two recent cases involving SK Corp. (Sovereign) and KT&G (Carl Icahn / Steel Partners) have raised awareness of hostile activities inKorea

Foreign ownership of Korean companies has increased

Controlling Shareholder Group Foreign Ownership KT&G 15.5% 62.4% Samsung Electronics 27.7% 53.9% SK 15.2% 53.8% SK Telecom 34.6% 48.3% KT 29.6% 47.0% Hyundai Motor 30.4% 46.1% Shinsegae 29.6% 46.0% LG Electronics 36.6% 38.8% Kia Motor 44.9% 30.9% KEPCO 55.7% 29.3% Hyundai Heavy 38.2% 22.0% Hynix Semiconductor 9.6% 18.6%As of November 10, 2005; Source: Korea Exchange (November 2005)

18

Are Korean Companies Susceptible to Hostile Activity?

For structural reasons, an outright hostile takeover of a Koreancompany may be difficult– Mandatory tender offer rule

– Korean law requires a mandatory public tender offer if a person, together with any related persons, intends to make an acquisition outside the Korea Exchange that will result in such person holding 5% or more of target’s shares during a 6-month period

– Failure to comply with the tender offer rule may result in criminal sanctions and loss of voting rights

– Limited closing conditions, such as minimum tender condition– Supermajority voting requirement for business combination– Dissenting shareholders’ appraisal rights based on market price formula– Dissenting creditors’ rights– Strong labor unions– Public sentiment against hostile M&A

19

Are Korean Companies Susceptible to Hostile Activity?

It is more likely that Korean companies could be subject to following types of shareholder/hedge fund activism:– Private activism: phone calls, meetings, letters, questions on conference calls– Public activism: political press releases and interviews with the press, contact

with other shareholders– Proxy fight: hostile PR campaign, contact with all shareholders– Filing petitions with Korean regulatory authorities such as the Fair Trade

Commission, the Financial Supervisory Service and/or prosecutors office.– Recent examples include SK Corp (Sovereign) and KT&G (C. Icahn/Steel

Partners) (See Annex A)

Hostile Strategies and Tactics

21

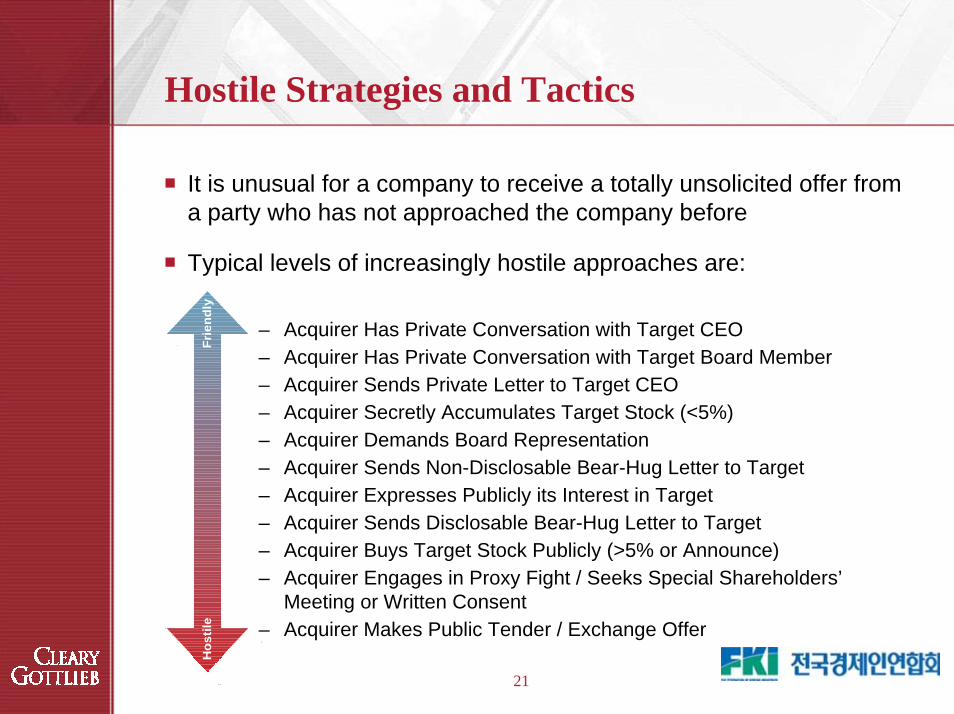

Hostile Strategies and Tactics

It is unusual for a company to receive a totally unsolicited offer from a party who has not approached the company before

Typical levels of increasingly hostile approaches are:

– Acquirer Has Private Conversation with Target CEO– Acquirer Has Private Conversation with Target Board Member– Acquirer Sends Private Letter to Target CEO– Acquirer Secretly Accumulates Target Stock (<5%)– Acquirer Demands Board Representation – Acquirer Sends Non-Disclosable Bear-Hug Letter to Target– Acquirer Expresses Publicly its Interest in Target– Acquirer Sends Disclosable Bear-Hug Letter to Target– Acquirer Buys Target Stock Publicly (>5% or Announce)– Acquirer Engages in Proxy Fight / Seeks Special Shareholders’

Meeting or Written Consent – Acquirer Makes Public Tender / Exchange Offer

ostil

eFr

iend

lyH

22

Hostile Strategies and Tactics

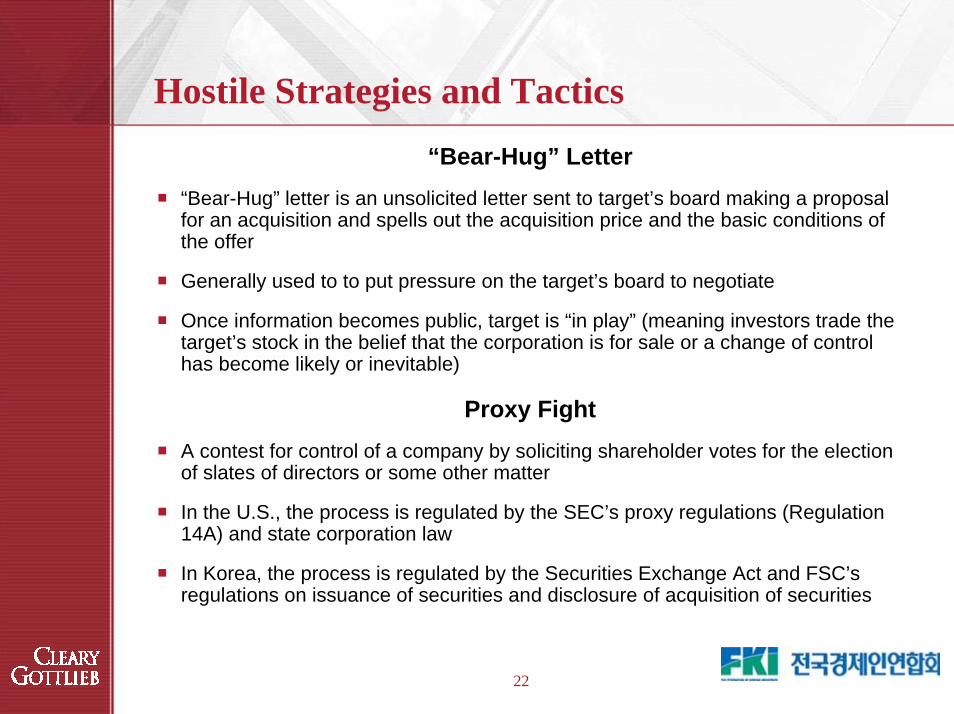

“Bear-Hug” Letter“Bear-Hug” letter is an unsolicited letter sent to target’s board making a proposal for an acquisition and spells out the acquisition price and the basic conditions of the offer

Generally used to to put pressure on the target’s board to negotiate

Once information becomes public, target is “in play” (meaning investors trade the target’s stock in the belief that the corporation is for sale or a change of control has become likely or inevitable)

Proxy FightA contest for control of a company by soliciting shareholder votes for the election of slates of directors or some other matter

In the U.S., the process is regulated by the SEC’s proxy regulations (Regulation 14A) and state corporation law

In Korea, the process is regulated by the Securities Exchange Act and FSC’sregulations on issuance of securities and disclosure of acquisition of securities

23

Hostile Strategies and Tactics

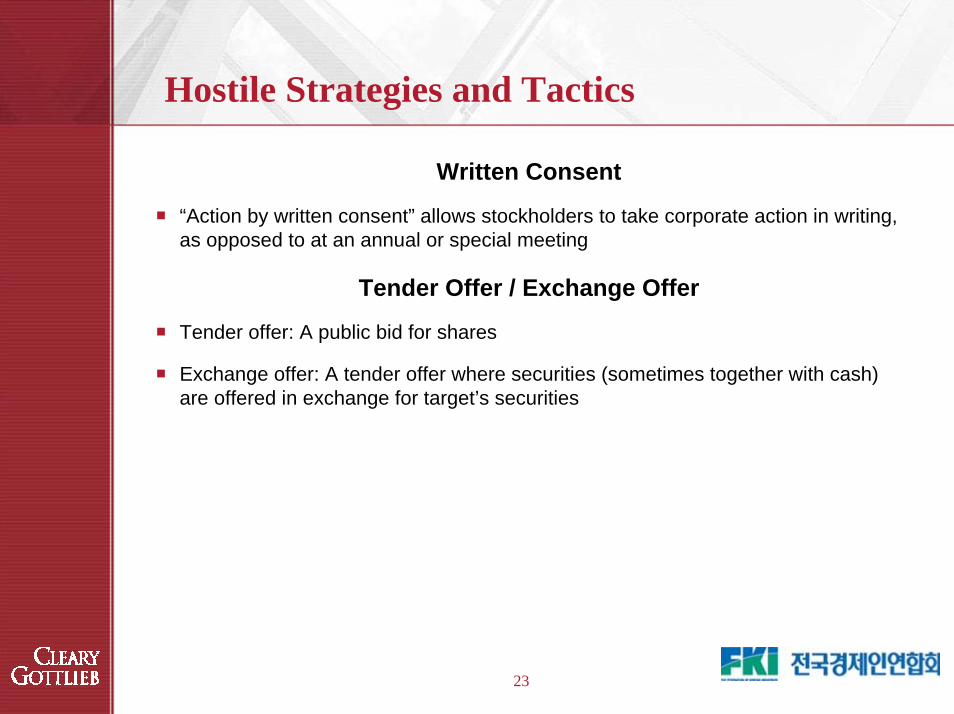

Written Consent

“Action by written consent” allows stockholders to take corporate action in writing, as opposed to at an annual or special meeting

Tender Offer / Exchange Offer

Tender offer: A public bid for shares

Exchange offer: A tender offer where securities (sometimes together with cash) are offered in exchange for target’s securities

24

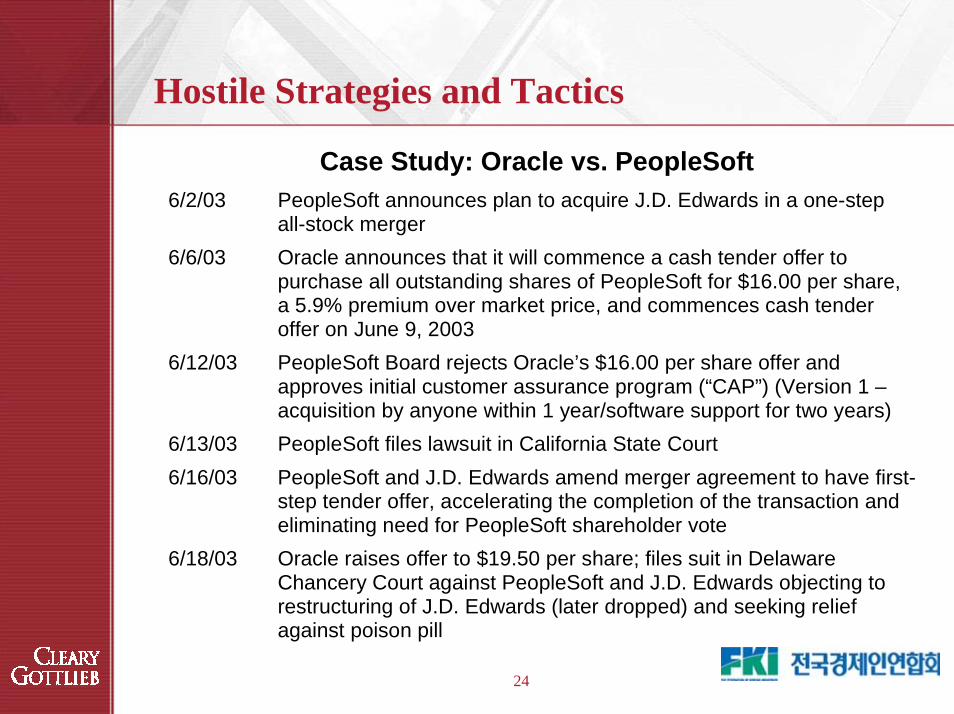

Hostile Strategies and Tactics

Case Study: Oracle vs. PeopleSoft6/2/03 PeopleSoft announces plan to acquire J.D. Edwards in a one-step

all-stock merger 6/6/03 Oracle announces that it will commence a cash tender offer to

purchase all outstanding shares of PeopleSoft for $16.00 per share, a 5.9% premium over market price, and commences cash tender offer on June 9, 2003

6/12/03 PeopleSoft Board rejects Oracle’s $16.00 per share offer and approves initial customer assurance program (“CAP”) (Version 1 – acquisition by anyone within 1 year/software support for two years)

6/13/03 PeopleSoft files lawsuit in California State Court 6/16/03 PeopleSoft and J.D. Edwards amend merger agreement to have first-

step tender offer, accelerating the completion of the transaction and eliminating need for PeopleSoft shareholder vote

6/18/03 Oracle raises offer to $19.50 per share; files suit in Delaware Chancery Court against PeopleSoft and J.D. Edwards objecting to restructuring of J.D. Edwards (later dropped) and seeking relief against poison pill

25

Hostile Strategies and Tactics

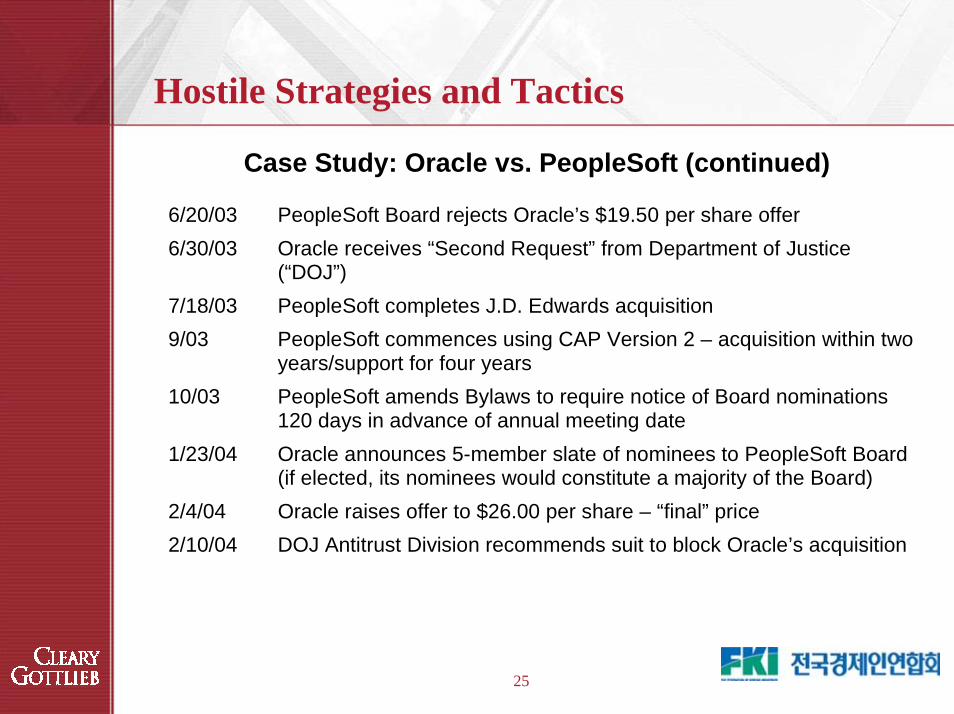

Case Study: Oracle vs. PeopleSoft (continued)

6/20/03 PeopleSoft Board rejects Oracle’s $19.50 per share offer 6/30/03 Oracle receives “Second Request” from Department of Justice

(“DOJ”) 7/18/03 PeopleSoft completes J.D. Edwards acquisition 9/03 PeopleSoft commences using CAP Version 2 – acquisition within two

years/support for four years 10/03 PeopleSoft amends Bylaws to require notice of Board nominations

120 days in advance of annual meeting date 1/23/04 Oracle announces 5-member slate of nominees to PeopleSoft Board

(if elected, its nominees would constitute a majority of the Board) 2/4/04 Oracle raises offer to $26.00 per share – “final” price 2/10/04 DOJ Antitrust Division recommends suit to block Oracle’s acquisition

26

Hostile Strategies and Tactics

Case Study: Oracle vs. PeopleSoft (continued)

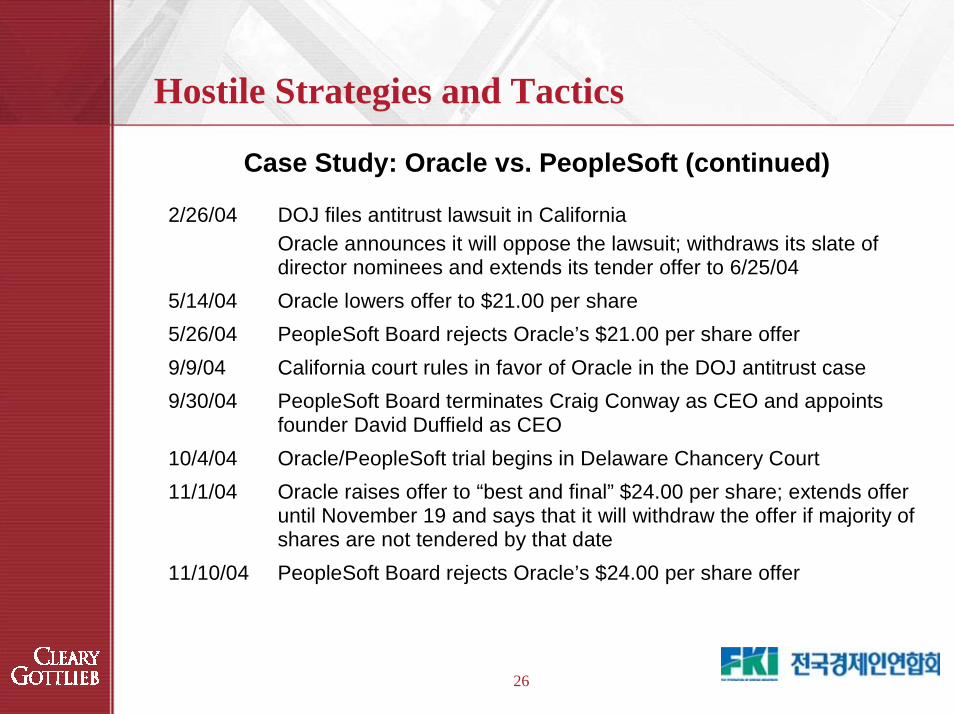

2/26/04 DOJ files antitrust lawsuit in California Oracle announces it will oppose the lawsuit; withdraws its slate of director nominees and extends its tender offer to 6/25/04

5/14/04 Oracle lowers offer to $21.00 per share 5/26/04 PeopleSoft Board rejects Oracle’s $21.00 per share offer 9/9/04 California court rules in favor of Oracle in the DOJ antitrust case 9/30/04 PeopleSoft Board terminates Craig Conway as CEO and appoints

founder David Duffield as CEO 10/4/04 Oracle/PeopleSoft trial begins in Delaware Chancery Court 11/1/04 Oracle raises offer to “best and final” $24.00 per share; extends offer

until November 19 and says that it will withdraw the offer if majority of shares are not tendered by that date

11/10/04 PeopleSoft Board rejects Oracle’s $24.00 per share offer

27

Hostile Strategies and Tactics

Case Study: Oracle vs. PeopleSoft (continued)

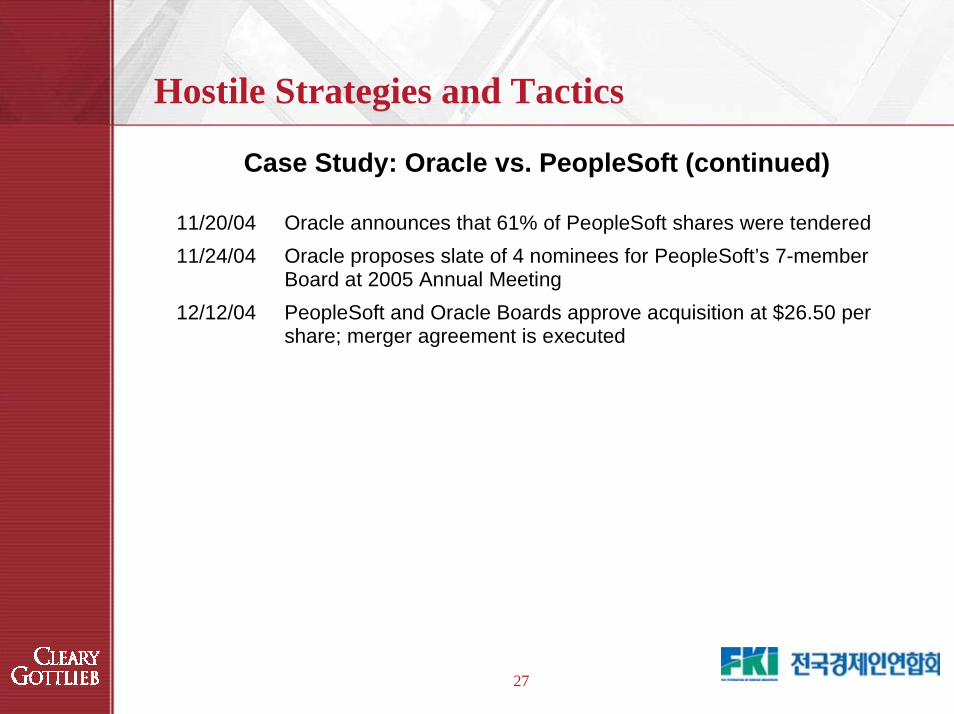

11/20/04 Oracle announces that 61% of PeopleSoft shares were tendered 11/24/04 Oracle proposes slate of 4 nominees for PeopleSoft’s 7-member

Board at 2005 Annual Meeting 12/12/04 PeopleSoft and Oracle Boards approve acquisition at $26.50 per

share; merger agreement is executed

U.S.-Style Structural Defenses: Can They Work in Korea?

29

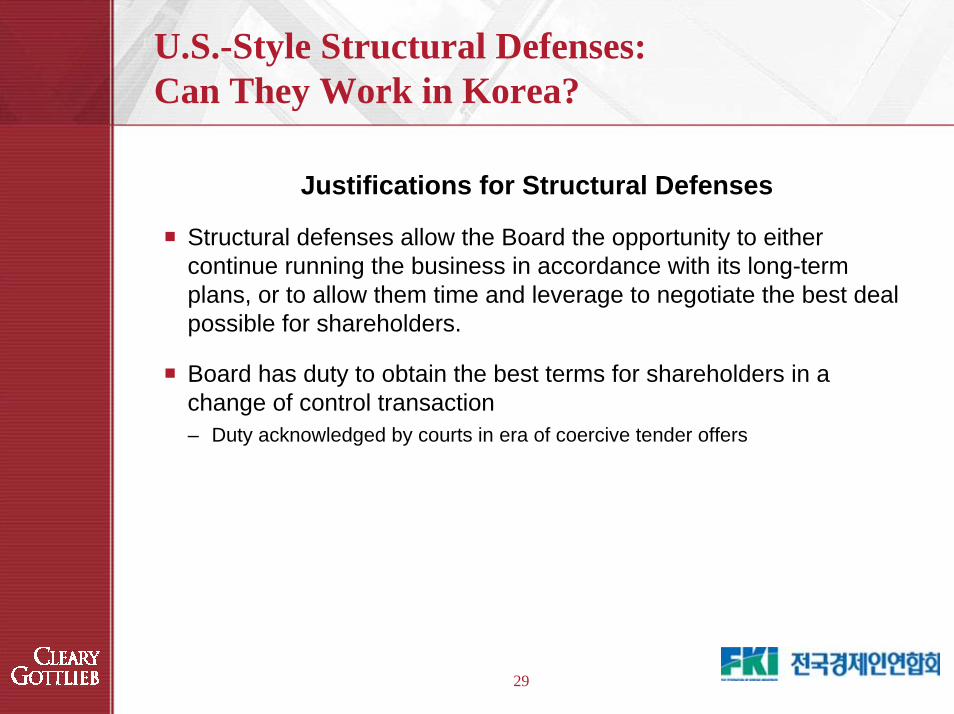

U.S.-Style Structural Defenses: Can They Work in Korea?

Justifications for Structural Defenses

Structural defenses allow the Board the opportunity to either continue running the business in accordance with its long-term plans, or to allow them time and leverage to negotiate the best deal possible for shareholders.

Board has duty to obtain the best terms for shareholders in a change of control transaction– Duty acknowledged by courts in era of coercive tender offers

30

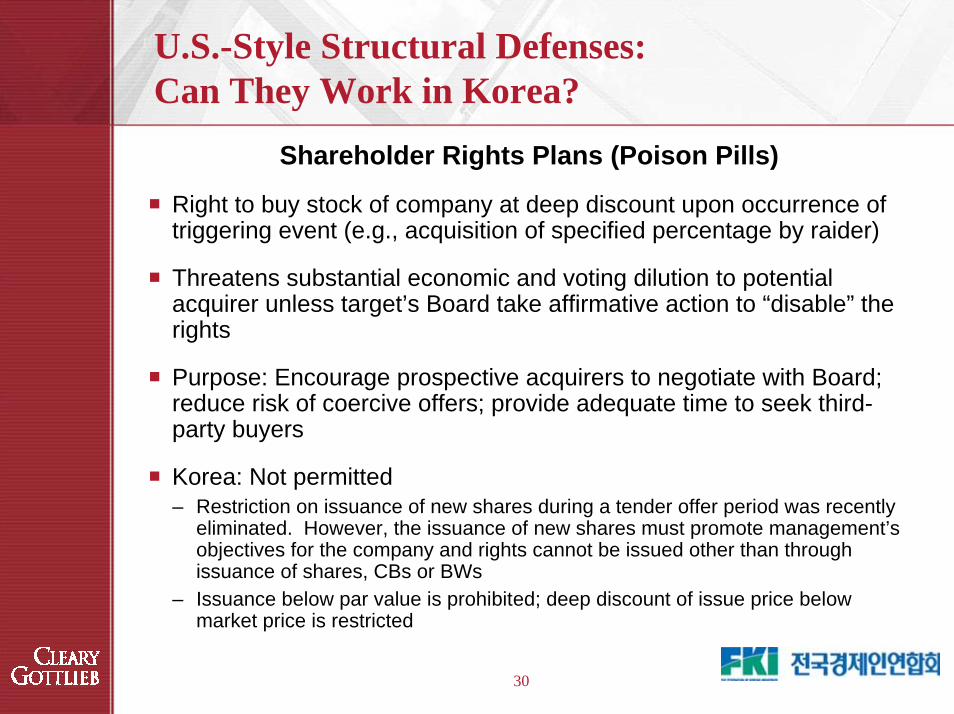

U.S.-Style Structural Defenses: Can They Work in Korea?

Shareholder Rights Plans (Poison Pills)

Right to buy stock of company at deep discount upon occurrence of triggering event (e.g., acquisition of specified percentage by raider)

Threatens substantial economic and voting dilution to potential acquirer unless target’s Board take affirmative action to “disable” the rights

Purpose: Encourage prospective acquirers to negotiate with Board; reduce risk of coercive offers; provide adequate time to seek third-party buyers

Korea: Not permitted– Restriction on issuance of new shares during a tender offer period was recently

eliminated. However, the issuance of new shares must promote management’s objectives for the company and rights cannot be issued other than through issuance of shares, CBs or BWs

– Issuance below par value is prohibited; deep discount of issue price below market price is restricted

31

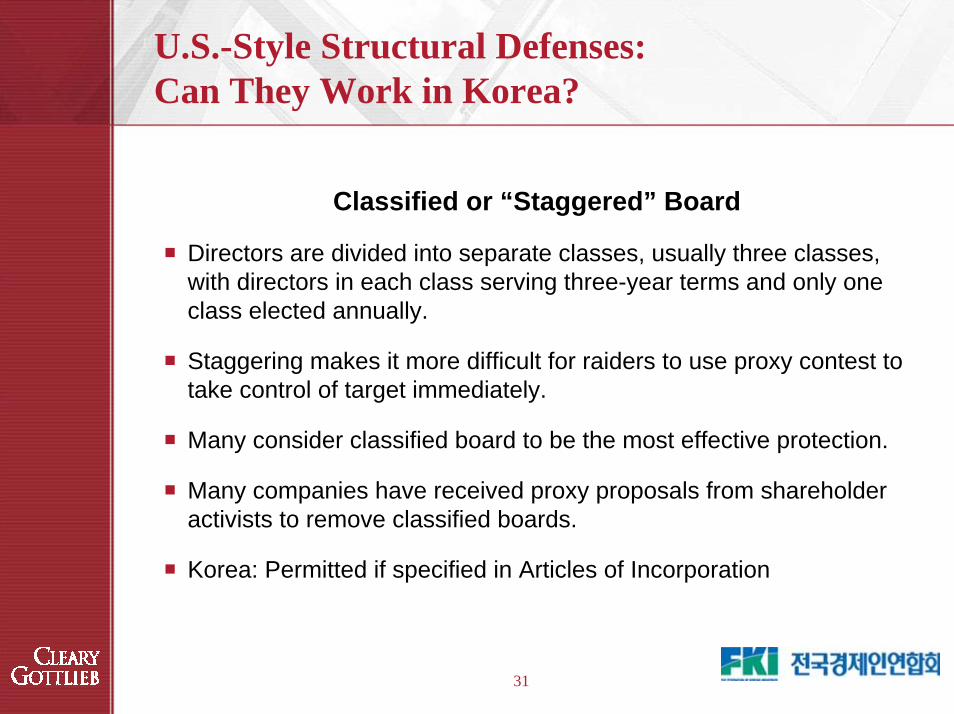

U.S.-Style Structural Defenses: Can They Work in Korea?

Classified or “Staggered” Board

Directors are divided into separate classes, usually three classes, with directors in each class serving three-year terms and only one class elected annually.

Staggering makes it more difficult for raiders to use proxy contest to take control of target immediately.

Many consider classified board to be the most effective protection.

Many companies have received proxy proposals from shareholder activists to remove classified boards.

Korea: Permitted if specified in Articles of Incorporation

32

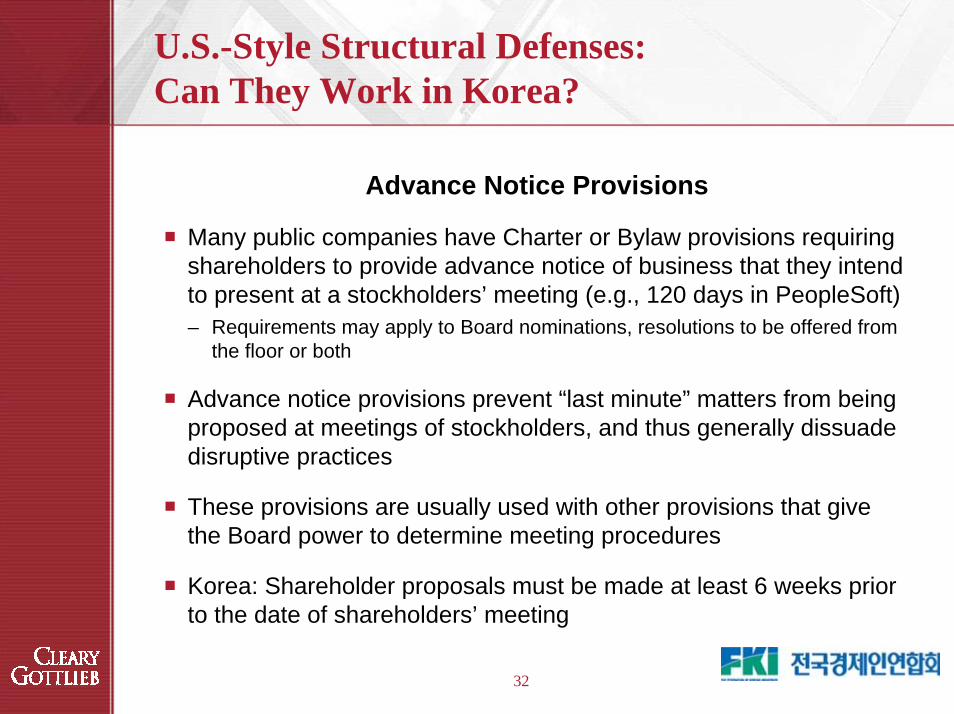

U.S.-Style Structural Defenses: Can They Work in Korea?

Advance Notice Provisions

Many public companies have Charter or Bylaw provisions requiringshareholders to provide advance notice of business that they intend to present at a stockholders’ meeting (e.g., 120 days in PeopleSoft)– Requirements may apply to Board nominations, resolutions to be offered from

the floor or both

Advance notice provisions prevent “last minute” matters from being proposed at meetings of stockholders, and thus generally dissuade disruptive practices

These provisions are usually used with other provisions that give the Board power to determine meeting procedures

Korea: Shareholder proposals must be made at least 6 weeks priorto the date of shareholders’ meeting

33

U.S.-Style Structural Defenses: Can They Work in Korea?

Stockholder Limitations

Bar action by written consent– “Action by written consent” allows stockholder to take corporate action in

writing, as opposed to at annual or special meeting– Limiting action by written consent prohibits removal of director without

stockholder meeting– Korea: Shareholder action by written consent is not permitted

Bar on stockholder ability to call a special meeting– Confines all business to annual meeting, thereby limiting Board’s “window of

vulnerability” to a proxy contest to one meeting per year– Variations on provisions regarding special meetings

– Some permit stockholders owning over a specified percentage to call special meetings

– Some permit only management and/or board to call special meetings– Korea: Shareholders of more than 3% of outstanding shares or 3% (1.5%

in the case of companies with paid-in capital of 100 billion won or more) of voting shares held for at least 6 months are permitted to call special meetings

34

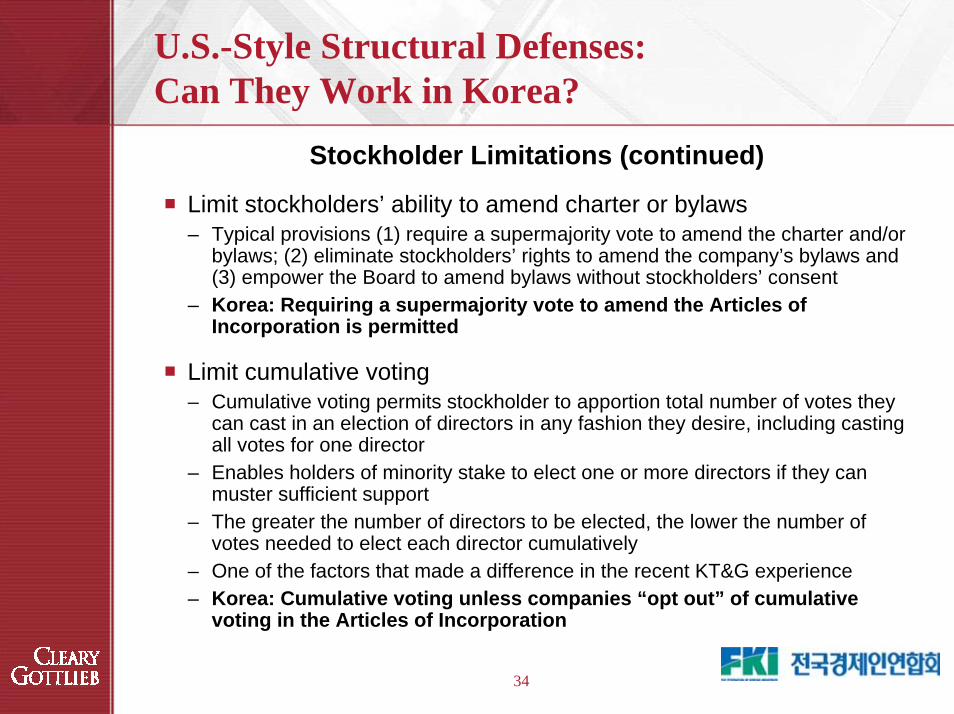

U.S.-Style Structural Defenses: Can They Work in Korea?

Stockholder Limitations (continued)

Limit stockholders’ ability to amend charter or bylaws– Typical provisions (1) require a supermajority vote to amend the charter and/or

bylaws; (2) eliminate stockholders’ rights to amend the company’s bylaws and (3) empower the Board to amend bylaws without stockholders’ consent

– Korea: Requiring a supermajority vote to amend the Articles of Incorporation is permitted

Limit cumulative voting– Cumulative voting permits stockholder to apportion total number of votes they

can cast in an election of directors in any fashion they desire, including casting all votes for one director

– Enables holders of minority stake to elect one or more directors if they can muster sufficient support

– The greater the number of directors to be elected, the lower the number of votes needed to elect each director cumulatively

– One of the factors that made a difference in the recent KT&G experience– Korea: Cumulative voting unless companies “opt out” of cumulative

voting in the Articles of Incorporation

35

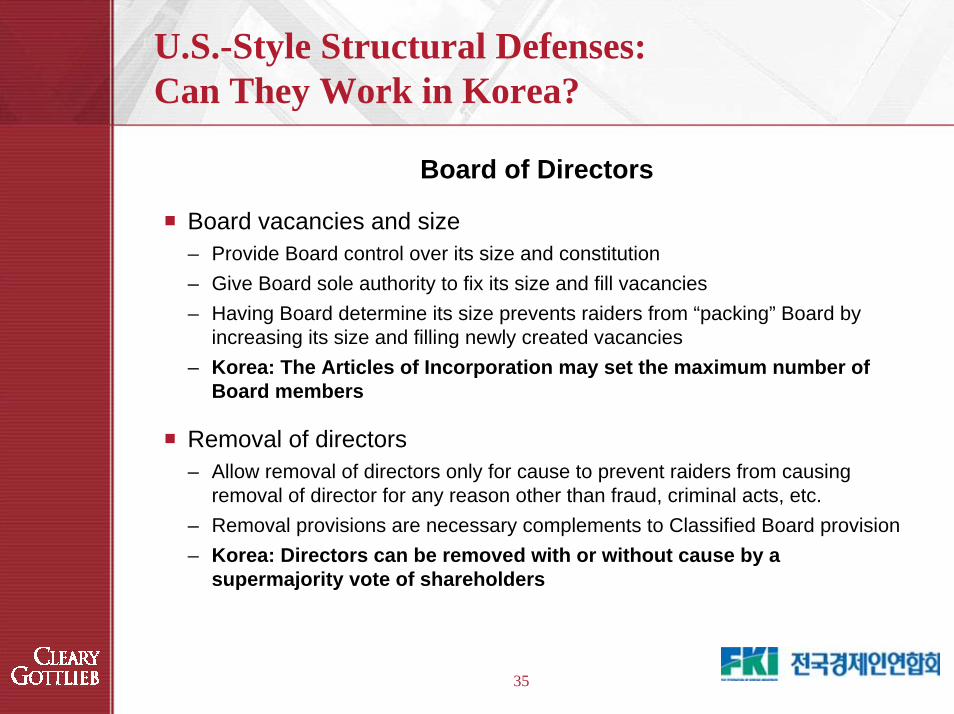

U.S.-Style Structural Defenses: Can They Work in Korea?

Board of Directors

Board vacancies and size– Provide Board control over its size and constitution – Give Board sole authority to fix its size and fill vacancies– Having Board determine its size prevents raiders from “packing” Board by

increasing its size and filling newly created vacancies– Korea: The Articles of Incorporation may set the maximum number of

Board members

Removal of directors– Allow removal of directors only for cause to prevent raiders from causing

removal of director for any reason other than fraud, criminal acts, etc. – Removal provisions are necessary complements to Classified Board provision– Korea: Directors can be removed with or without cause by a

supermajority vote of shareholders

36

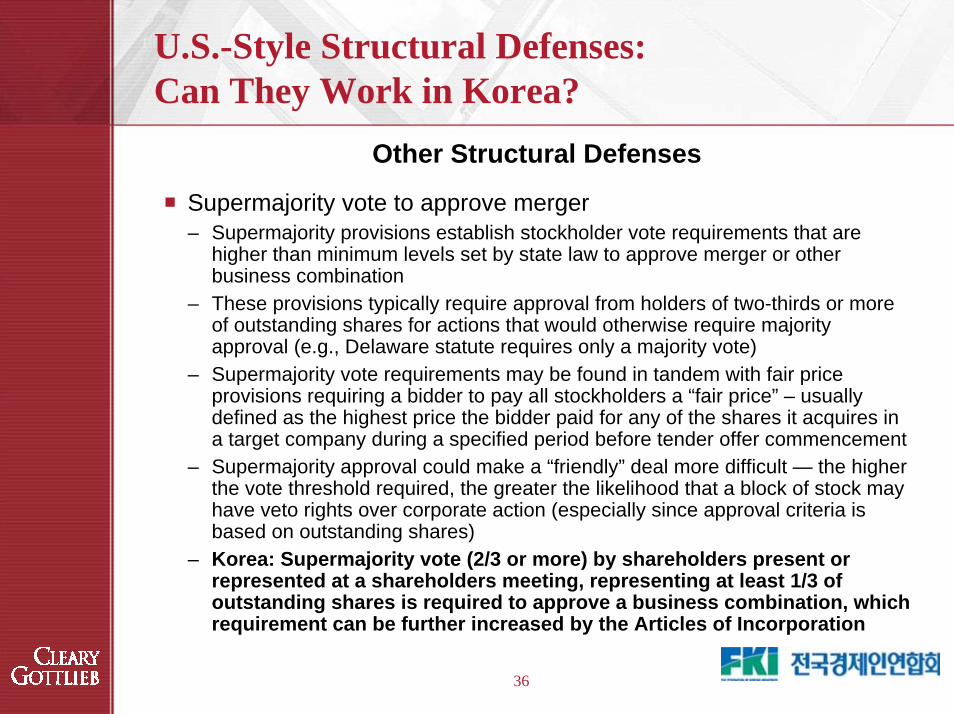

U.S.-Style Structural Defenses: Can They Work in Korea?

Other Structural Defenses

Supermajority vote to approve merger– Supermajority provisions establish stockholder vote requirements that are

higher than minimum levels set by state law to approve merger or other business combination

– These provisions typically require approval from holders of two-thirds or more of outstanding shares for actions that would otherwise require majority approval (e.g., Delaware statute requires only a majority vote)

– Supermajority vote requirements may be found in tandem with fair price provisions requiring a bidder to pay all stockholders a “fair price” – usually defined as the highest price the bidder paid for any of the shares it acquires in a target company during a specified period before tender offer commencement

– Supermajority approval could make a “friendly” deal more difficult — the higher the vote threshold required, the greater the likelihood that a block of stock may have veto rights over corporate action (especially since approval criteria is based on outstanding shares)

– Korea: Supermajority vote (2/3 or more) by shareholders present or represented at a shareholders meeting, representing at least 1/3 of outstanding shares is required to approve a business combination, which requirement can be further increased by the Articles of Incorporation

37

U.S.-Style Structural Defenses: Can They Work in Korea?

Other Structural Defenses (continued)

Golden parachute and other employee agreements– Lump-sum payments to senior management or vesting of options and

restricted stock units after change of control– Two types of triggers: Change of control or change of control and change of

circumstances (i.e. termination of employment))– Compensation usually determined by annual compensation and years of

service– Korea: Permitted if specified in the Articles of Incorporation or approved

by the shareholders

Consider nonfinancial effects of merger– Provisions that require or allow directors to evaluate the impact that a

proposed change in control could have on employees, host communities, suppliers and other constituencies.

– Korea: Board can consider the impact a proposed change in control could have on other constituencies without specific provision in the Articles of Incorporation

38

U.S.-Style Structural Defenses: Can They Work in Korea?

Other Structural Defenses (continued)

Blank Check Preferred Stock– “Blank check preferred stock” describes provisions that gives the Board of

Directors broad discretion to establish voting, dividend, conversion and other rights for preferred stock

– Provides the Board with flexibility to meet changing financial conditions by setting preferred stock terms and grants the Board authority to issue preferred stock necessary to implement certain defenses, including a poison pill or stockholder rights plan

– Blank check preferred stock can be placed with an employee stock ownership plan or a friendly investor

– These parties may control enough voting power to block a takeover attempt– Korea: Types and number of authorized shares must be specified in the

Articles of Incorporation. Issuance of shares to third parties without giving shareholders pre-emptive rights is strictly regulated

Dual class common stock– Two or more classes of common stock with different voting rights– Korea: Not permitted

39

U.S.-Style Structural Defenses: Can They Work in Korea?

Other Structural Defenses (continued)

Antigreenmail provisions– Greenmail refers to the practice of accumulating a sizeable block of stock in a

company and then selling the stock back to the company in a private transaction, at an above market price. Often accompanied by a standstill agreement, which limits the recipient’s ability to seek control of the company for a certain period

– Some companies have adopted charter and bylaw amendments that prohibit such above-market purchases unless the same offer is made to all shareholders or shareholders approve the transaction by a majority or supermajority vote

– Korea: Not permitted because of strict regulation of share repurchases

Change of control provisions– Change of control provisions contained in loan agreements and indentures,

intellectual property agreements, joint venture agreements and customer support agreements make hostile takeovers more difficult

40

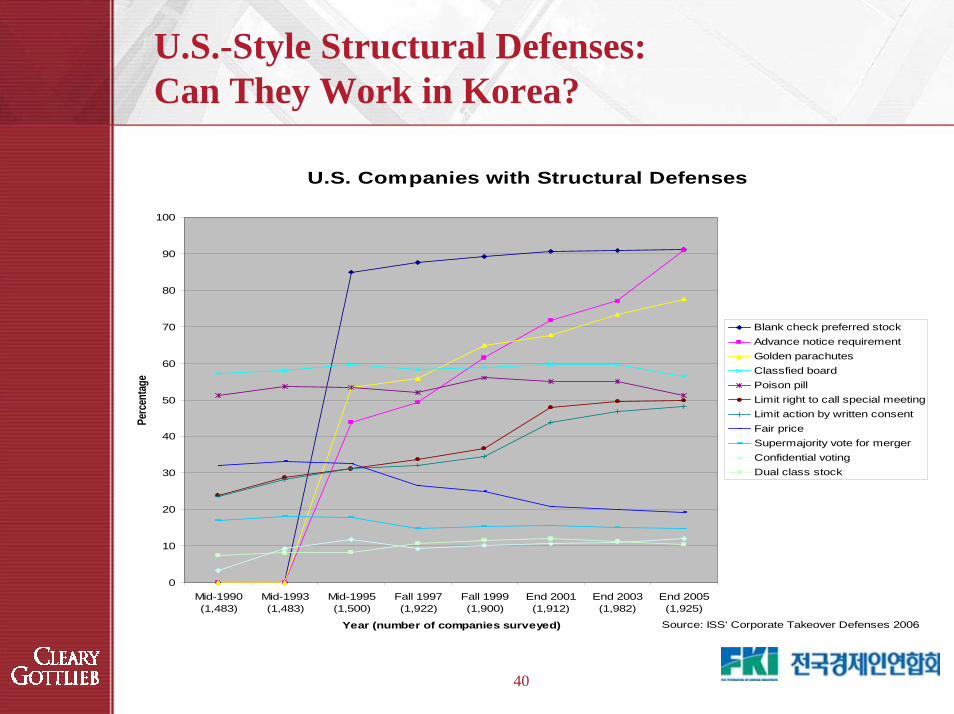

U.S.-Style Structural Defenses: Can They Work in Korea?

U.S. Companies with Structural Defenses

0

10

20

30

40

50

60

70

80

90

100

Mid-1990(1,483)

Mid-1993(1,483)

Mid-1995(1,500)

Fall 1997(1,922)

Fall 1999(1,900)

End 2001(1,912)

End 2003(1,982)

End 2005(1,925)

Year (number of companies surveyed)

Perc

entag

e

Blank check preferred stockAdvance notice requirementGolden parachutesClassfied boardPoison pillLimit right to call special meetingLimit action by written consentFair priceSupermajority vote for mergerConfidential votingDual class stock

Source: ISS' Corporate Takeover Defenses 2006

Other Measures to Minimize Hostile Risk

42

Other Measures to Minimize Hostile Risk

Improvements to corporate governance structure

Increased transparency

Enhanced public and investor relations

Proactive business planning

Superior operating and share price performance

Practical Guidelines for Preparation

44

Practical Guidelines for Preparation

Create Team to Deal with Takeovers

Create a small group (2-5) of key officers, lawyers, investment bankers, proxy soliciting firms and public relations firm

Periodic review company’s defensive profiles

Ensure ability to convene special meeting of board within 24 to 48 hours– Continuing contact and periodic meetings by board are important

Provide periodic updates to the board

45

Practical Guidelines for Preparation

Communications in Response to Hostile Approach

Press

Stock exchange

Directors

Employees and unions

Customers/suppliers/banks

Institutional investors and analysts

Public officials and government contacts

46

Practical Guidelines for Preparation

Consider Additional Advance Preparation

Advance preparation of earnings projections and liquidation values for evaluation of takeover bid and alternative transactions

White knight/white squire and other arrangements– White knight: a friendly bidder who agrees to buy the company as an

alternative to a pending or anticipated hostile bid– White squire: someone who purchases a large position in the stock of a

company as a takeover defense– Identify potential strategic partners and assess interest level– Private equity firms can be helpful– Employee Stock Ownership Associations can be helpful

47

Practical Guidelines for Preparation

Consider Additional Advance Preparation (continued)

Restructuring: divestiture, spin-off, recapitalization, stock repurchases– Identify businesses or subsidiaries for potential divestiture or spin-off– Evaluate potential recapitalizations, increases or decreases in leverage, cash

distributions or stock repurchases– Evaluate antitrust and other regulatory issues in potential business

combinations

48

Practical Guidelines for Preparation

Shareholder Relations

Review dividend policy, analyst presentations and other financial public relations

Monitor changes in institutional holdings on a regular basis

Plan contacts with institutional investors (including maintenance of an up-to-date list of holdings and contact information), analysts, media, regulatory agencies and political bodies

Remain informed about activist institutional investors and aboutcorporate governance and proxy issues

49

Practical Guidelines for Preparation

Prepare Board to Deal with Takeovers

Maintain a unified board consensus on key strategic issues

Schedule periodic presentations by lawyers and investment bankers to familiarize directors with their advisors and with the takeover scene and the law

Directors must guard against subversion by raider and should refer all approaches to the CEO

Avoid being put “in play”; psychological and perception factors may be more important than legal and financial factors in avoiding being singled out as a takeover target

50

Practical Guidelines for Preparation

Duties and Role of Board of Directors

In the United States:– No duty to accept or reject proposal – can “just say no”– Subject to Unocal two-prong test:

– Reasonable grounds for believing that a danger exists; and– Defensive actions must be reasonable in relation to threat – cannot be

“preclusive” or “coercive”– Board may consider adequacy of price, notice and timing of proposal, antitrust

and other regulatory considerations, impact on constituents other than shareholders and nature and terms of securities being offered, if any

– Two guiding principles:– Procedural guarantees for consideration of alternative proposals; and– Maximization of shareholder interest

– In Delaware, it is possible to limit directors’ liabilities; D&O insurance is widely used

51

Practical Guidelines for Preparation

Duties and Role of Board of Directors (continued)

In Korea:– No duty to respond to a tender offer– Lack of sufficient court precedents – no precedent in the context of tender offer– Conflicting lower court decisions on sale of treasury shares – recent decision

required equal opportunity to all shareholders– A lower court recently held that a defense against hostile M&A by way of

issuance of new shares is permitted if:– Such measures protect the company or the shareholders or such measures

are in furtherance of public interest; and– Reasonable procedures are followed, such as obtaining opinion from

independent experts– It is not possible to limit directors’ liabilities; D&O insurance is not widely used

52

Practical Guidelines for Preparation

Prepare CEO to Deal with Takeover Approaches

The CEO should be the sole spokesperson for the Company on independence, merger and takeover

The CEO handles casual passes (bear hugs), offers, and communications with officers and board of directors

Company may have policy of not commenting on takeover discussions and rumors

53

Practical Guidelines for Preparation

Responses to Accumulations in the Market

Monitor trading

Monitor/combat disruption of executives, personnel, customers, suppliers, etc.

Monitor uncertainty in the market; change in shareholder profile

Consider immediate responses to accumulation– In the U.S., poison pill can be structured so that it takes effect at 10% to 15%

threshold; in Korea, poison pill response is not permitted– Monitor potential violations of securities law and other regulations including the

“5% rule” (which may restrict the raider’s voting rights for a certain period of time)

54

Practical Guidelines for Preparation

Responses to Casual Passes or Non-Public Bear Hugs

No duty to discuss or negotiate

No duty to disclose unless leak comes from within

Response to any particular approach must be specially structured; team should confer to decide proper response

Keep the Board advised

55

Practical Guidelines for Preparation

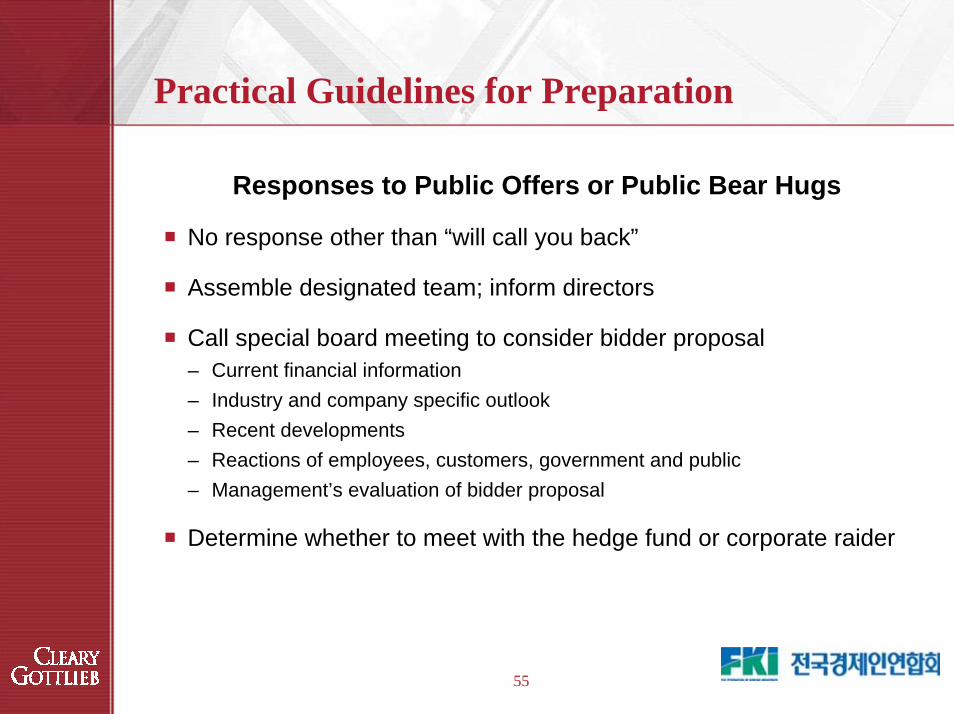

Responses to Public Offers or Public Bear Hugs

No response other than “will call you back”

Assemble designated team; inform directors

Call special board meeting to consider bidder proposal– Current financial information– Industry and company specific outlook– Recent developments– Reactions of employees, customers, government and public– Management’s evaluation of bidder proposal

Determine whether to meet with the hedge fund or corporate raider

56

Practical Guidelines for Preparation

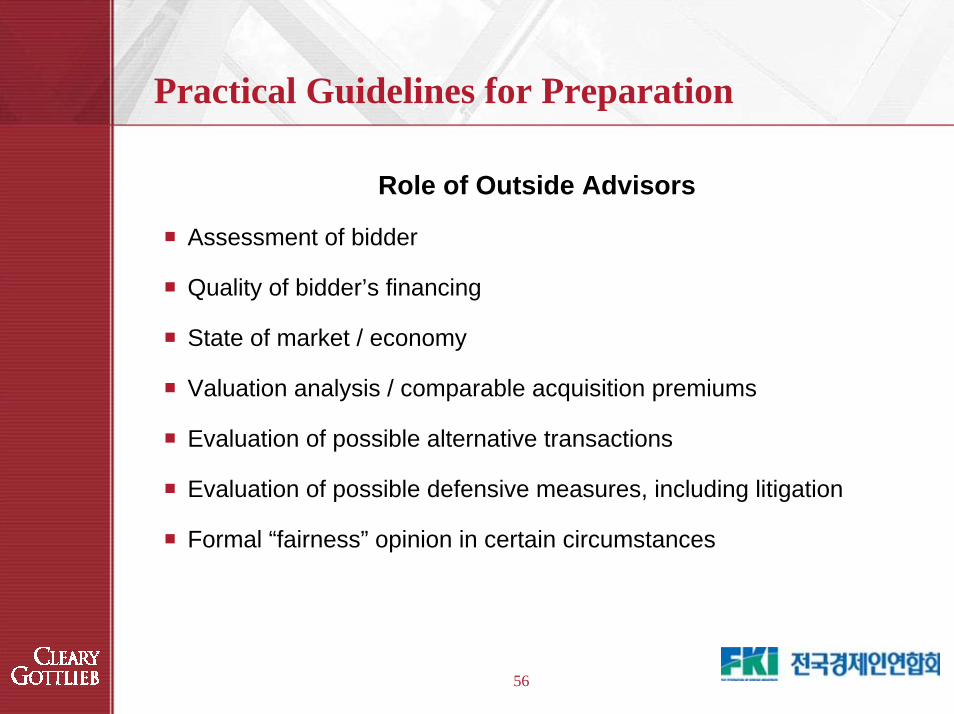

Role of Outside Advisors

Assessment of bidder

Quality of bidder’s financing

State of market / economy

Valuation analysis / comparable acquisition premiums

Evaluation of possible alternative transactions

Evaluation of possible defensive measures, including litigation

Formal “fairness” opinion in certain circumstances

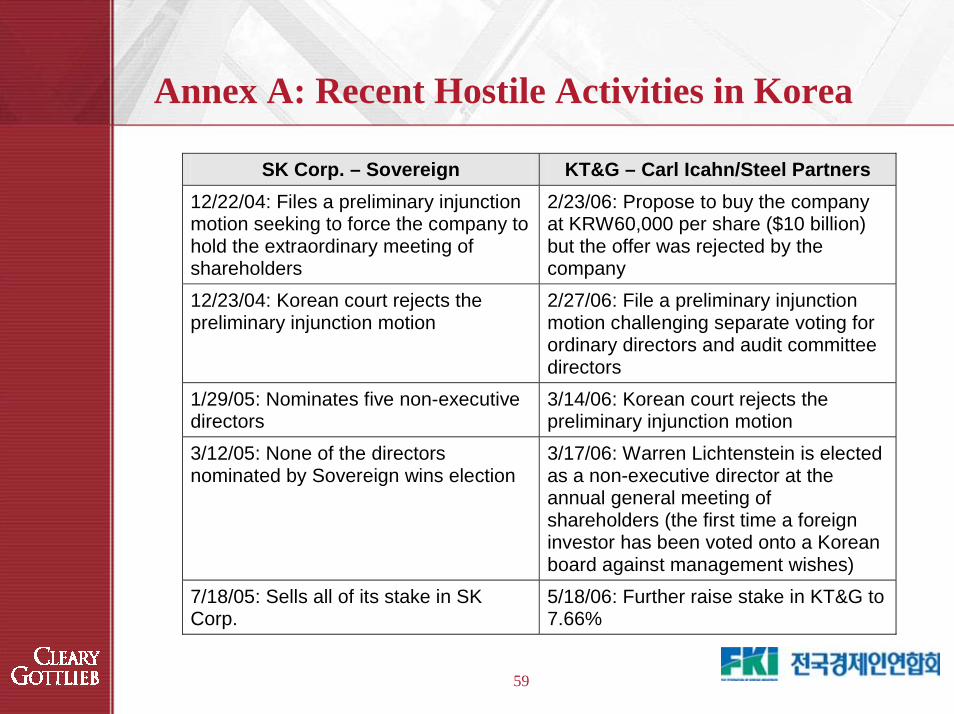

Annex A: Recent Hostile Activities in Korea

58

Annex A: Recent Hostile Activities in Korea

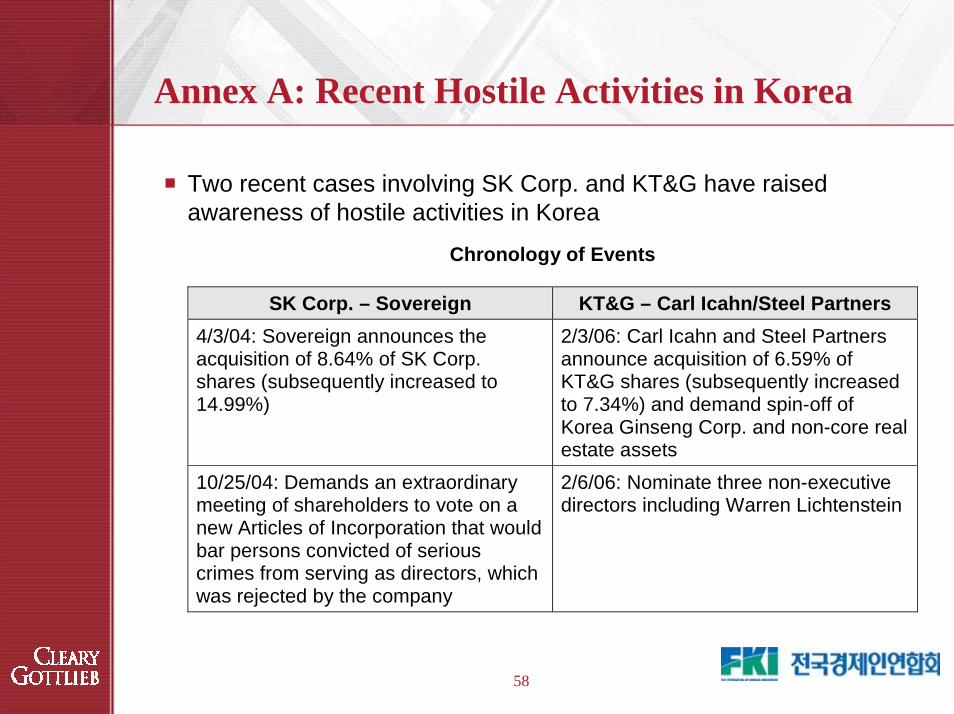

Two recent cases involving SK Corp. and KT&G have raised awareness of hostile activities in Korea

Chronology of Events

SK Corp. – Sovereign KT&G – Carl Icahn/Steel Partners 4/3/04: Sovereign announces the acquisition of 8.64% of SK Corp. shares (subsequently increased to 14.99%)

2/3/06: Carl Icahn and Steel Partners announce acquisition of 6.59% of KT&G shares (subsequently increased to 7.34%) and demand spin-off of Korea Ginseng Corp. and non-core real estate assets

10/25/04: Demands an extraordinary meeting of shareholders to vote on a new Articles of Incorporation that would bar persons convicted of serious crimes from serving as directors, which was rejected by the company

2/6/06: Nominate three non-executive directors including Warren Lichtenstein

59

Annex A: Recent Hostile Activities in Korea

SK Corp. – Sovereign KT&G – Carl Icahn/Steel Partners 12/22/04: Files a preliminary injunction motion seeking to force the company to hold the extraordinary meeting of shareholders

2/23/06: Propose to buy the company at KRW60,000 per share ($10 billion) but the offer was rejected by the company

12/23/04: Korean court rejects the preliminary injunction motion

2/27/06: File a preliminary injunction motion challenging separate voting for ordinary directors and audit committee directors

1/29/05: Nominates five non-executive directors

3/14/06: Korean court rejects the preliminary injunction motion

3/12/05: None of the directors nominated by Sovereign wins election

3/17/06: Warren Lichtenstein is elected as a non-executive director at the annual general meeting of shareholders (the first time a foreign investor has been voted onto a Korean board against management wishes)

7/18/05: Sells all of its stake in SK Corp.

5/18/06: Further raise stake in KT&G to 7.66%

Selected Speaker Biographies

61

Speakers

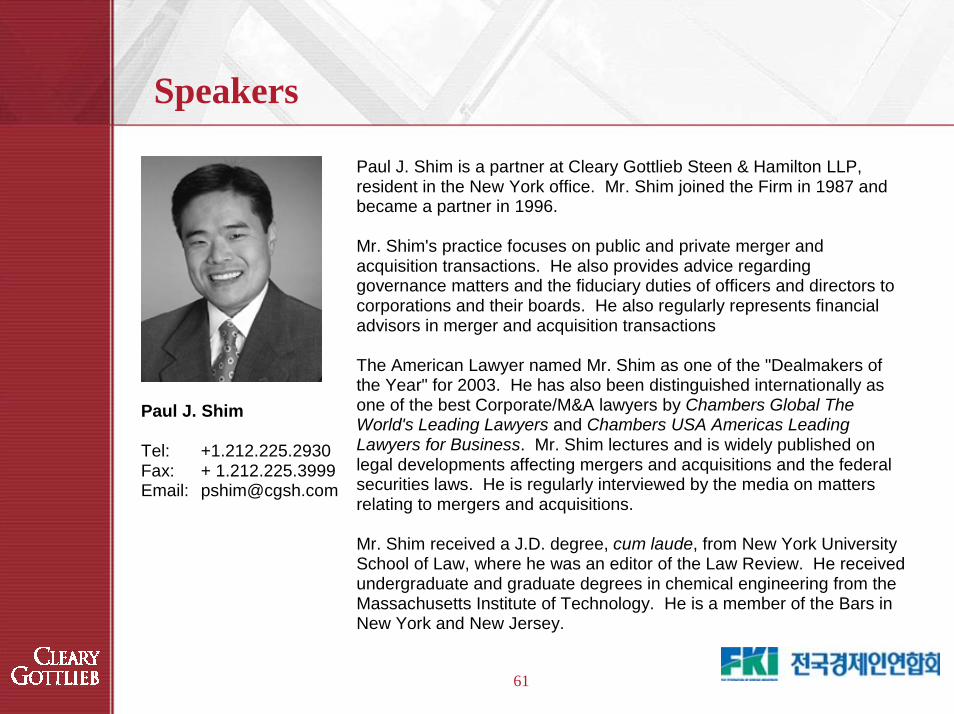

Paul J. Shim Tel: +1.212.225.2930 Fax: + 1.212.225.3999 Email: [email protected]

Paul J. Shim is a partner at Cleary Gottlieb Steen & Hamilton LLP, resident in the New York office. Mr. Shim joined the Firm in 1987 and became a partner in 1996. Mr. Shim's practice focuses on public and private merger and acquisition transactions. He also provides advice regarding governance matters and the fiduciary duties of officers and directors to corporations and their boards. He also regularly represents financial advisors in merger and acquisition transactions The American Lawyer named Mr. Shim as one of the "Dealmakers of the Year" for 2003. He has also been distinguished internationally as one of the best Corporate/M&A lawyers by Chambers Global The World's Leading Lawyers and Chambers USA Americas Leading Lawyers for Business. Mr. Shim lectures and is widely published on legal developments affecting mergers and acquisitions and the federal securities laws. He is regularly interviewed by the media on matters relating to mergers and acquisitions. Mr. Shim received a J.D. degree, cum laude, from New York University School of Law, where he was an editor of the Law Review. He received undergraduate and graduate degrees in chemical engineering from the Massachusetts Institute of Technology. He is a member of the Bars in New York and New Jersey.

62

Speakers

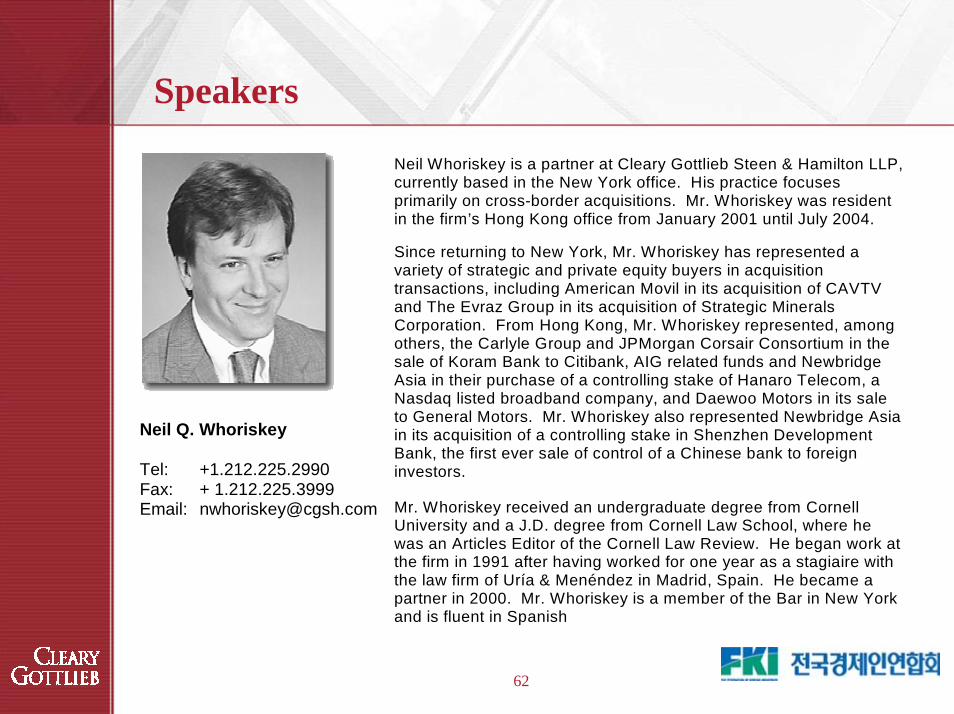

Neil Q. Whoriskey Tel: +1.212.225.2990 Fax: + 1.212.225.3999 Email: [email protected]

Neil Whoriskey is a partner at Cleary Gottlieb Steen & Hamilton LLP, currently based in the New York office. His practice focuses primarily on cross-border acquisitions. Mr. Whoriskey was resident in the firm’s Hong Kong office from January 2001 until July 2004.

Since returning to New York, Mr. Whoriskey has represented a variety of strategic and private equity buyers in acquisition transactions, including American Movil in its acquisition of CAVTV and The Evraz Group in its acquisition of Strategic Minerals Corporation. From Hong Kong, Mr. Whoriskey represented, among others, the Carlyle Group and JPMorgan Corsair Consortium in the sale of Koram Bank to Citibank, AIG related funds and Newbridge Asia in their purchase of a controlling stake of Hanaro Telecom, a Nasdaq listed broadband company, and Daewoo Motors in its sale to General Motors. Mr. Whoriskey also represented Newbridge Asia in its acquisition of a controlling stake in Shenzhen Development Bank, the first ever sale of control of a Chinese bank to foreign investors.

Mr. Whoriskey received an undergraduate degree from Cornell University and a J.D. degree from Cornell Law School, where he was an Articles Editor of the Cornell Law Review. He began work at the firm in 1991 after having worked for one year as a stagiaire with the law firm of Uría & Menéndez in Madrid, Spain. He became a partner in 2000. Mr. Whoriskey is a member of the Bar in New York and is fluent in Spanish

63

Speakers

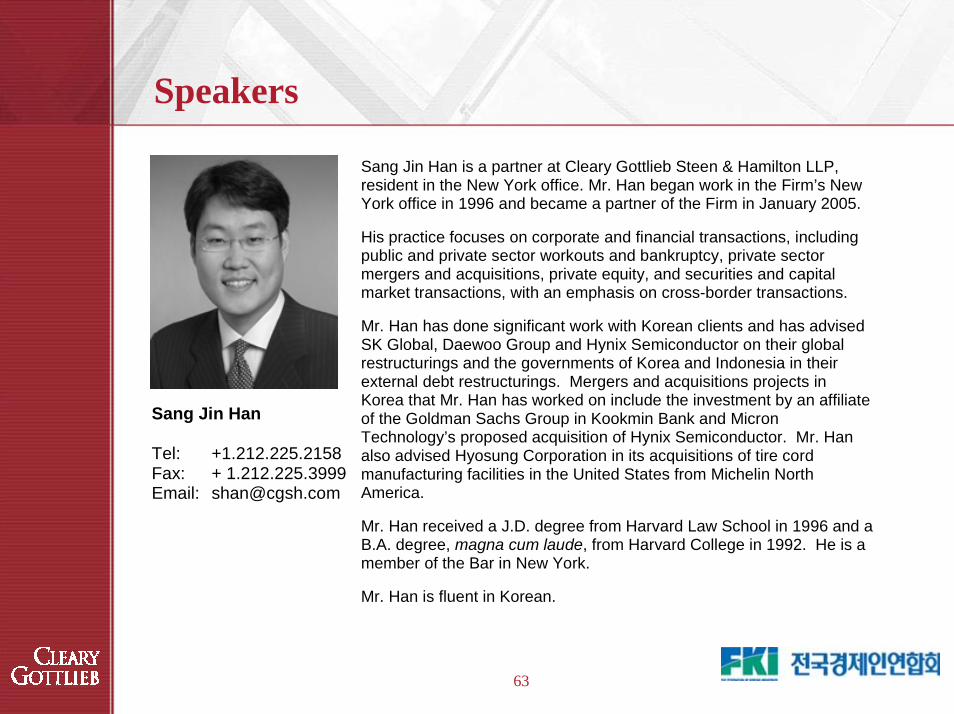

Sang Jin Han Tel: +1.212.225.2158 Fax: + 1.212.225.3999 Email: [email protected]

Sang Jin Han is a partner at Cleary Gottlieb Steen & Hamilton LLP, resident in the New York office. Mr. Han began work in the Firm’s New York office in 1996 and became a partner of the Firm in January 2005.

His practice focuses on corporate and financial transactions, including public and private sector workouts and bankruptcy, private sector mergers and acquisitions, private equity, and securities and capital market transactions, with an emphasis on cross-border transactions.

Mr. Han has done significant work with Korean clients and has advised SK Global, Daewoo Group and Hynix Semiconductor on their global restructurings and the governments of Korea and Indonesia in their external debt restructurings. Mergers and acquisitions projects in Korea that Mr. Han has worked on include the investment by an affiliate of the Goldman Sachs Group in Kookmin Bank and Micron Technology’s proposed acquisition of Hynix Semiconductor. Mr. Han also advised Hyosung Corporation in its acquisitions of tire cord manufacturing facilities in the United States from Michelin North America.

Mr. Han received a J.D. degree from Harvard Law School in 1996 and a B.A. degree, magna cum laude, from Harvard College in 1992. He is a member of the Bar in New York.

Mr. Han is fluent in Korean.

64

Speakers

Hee Chul Kang Tel: 02.528.5203 Fax: 02.528.5300/5228 Email: [email protected]

Hee Chul Kang is a partner at Woo Yun Kang Jeong & Han (Korean name: Yulchon). He had worked for Kim & Chang (1984-1996) before he became one of the founding partners of the current firm. His primary practice areas are corporate (general, mergers & acquisitions and labor & employment) and banking and finance. He is licensed to practice in Korea and the State of New York. He was selected as a leading lawyer by the International Financial Law Review in the field of M&A, Capital Markets and Corporate Governance. He was also selected as a recommended lawyer by Chambers Global in the filed of Corporate/M&A and Banking Finance. He is a member of Korea’s Accounting Supervision Committee of the Financial Supervisory Service. Mr. Kang received his education at Seoul National University (LL.B. 1979) and Harvard Law School (LL.M. 1990).

65

Moderator

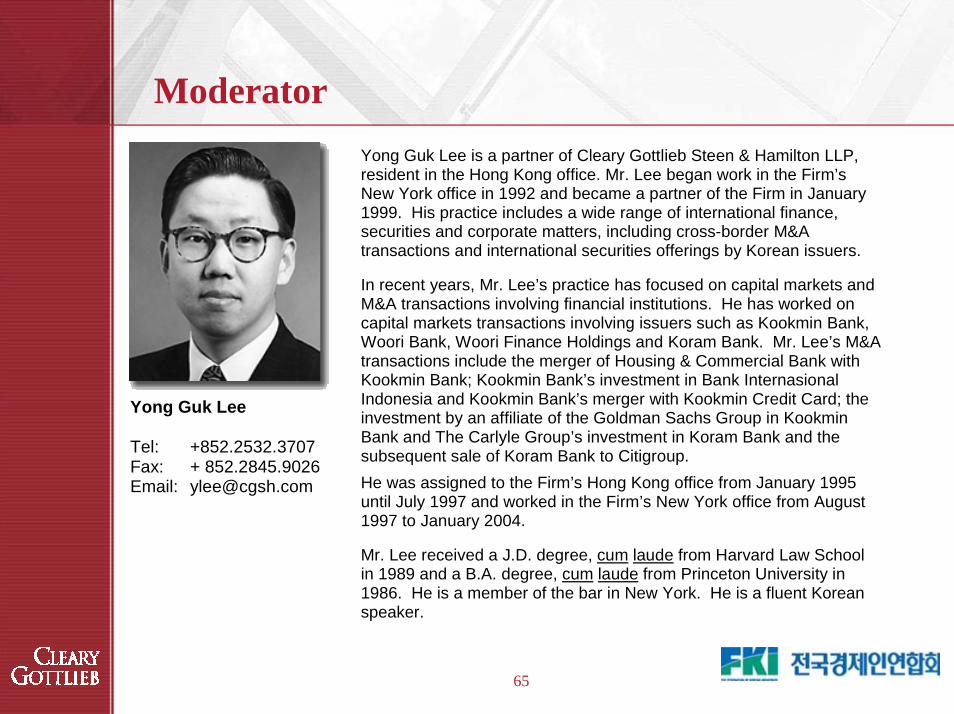

Yong Guk Lee Tel: +852.2532.3707 Fax: + 852.2845.9026 Email: [email protected]

Yong Guk Lee is a partner of Cleary Gottlieb Steen & Hamilton LLP, resident in the Hong Kong office. Mr. Lee began work in the Firm’s New York office in 1992 and became a partner of the Firm in January 1999. His practice includes a wide range of international finance, securities and corporate matters, including cross-border M&A transactions and international securities offerings by Korean issuers.

In recent years, Mr. Lee’s practice has focused on capital markets and M&A transactions involving financial institutions. He has worked on capital markets transactions involving issuers such as Kookmin Bank, Woori Bank, Woori Finance Holdings and Koram Bank. Mr. Lee’s M&A transactions include the merger of Housing & Commercial Bank with Kookmin Bank; Kookmin Bank’s investment in Bank Internasional Indonesia and Kookmin Bank’s merger with Kookmin Credit Card; the investment by an affiliate of the Goldman Sachs Group in Kookmin Bank and The Carlyle Group’s investment in Koram Bank and the subsequent sale of Koram Bank to Citigroup. He was assigned to the Firm’s Hong Kong office from January 1995 until July 1997 and worked in the Firm’s New York office from August 1997 to January 2004.

Mr. Lee received a J.D. degree, cum laude from Harvard Law School in 1989 and a B.A. degree, cum laude from Princeton University in 1986. He is a member of the bar in New York. He is a fluent Korean speaker.