Hostile Takeover Defenses: Decisionsmedia.straffordpub.com/.../presentation.pdf · 6/23/2011 ·...

45

Presenting a live 90‐minute webinar with interactive Q&A Hostile Takeover Defenses: Recent Decisions Evaluating and Structuring Anti‐Takeover Strategies T d ’ f l f 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific THURSDAY, JUNE 23, 2011 T oday’ s faculty features: Joseph J. Basile, Partner, Weil Gotshal & Manges, Boston Adam H. Offenhartz, Partner, Gibson Dunn & Crutcher, New York Eduardo Gallardo, Partner, Gibson Dunn & Crutcher, New York The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Transcript of Hostile Takeover Defenses: Decisionsmedia.straffordpub.com/.../presentation.pdf · 6/23/2011 ·...

Presenting a live 90‐minute webinar with interactive Q&A

Hostile Takeover Defenses: Recent DecisionsEvaluating and Structuring Anti‐Takeover Strategies

T d ’ f l f

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, JUNE 23, 2011

Today’s faculty features:

Joseph J. Basile, Partner, Weil Gotshal & Manges, Boston

Adam H. Offenhartz, Partner, Gibson Dunn & Crutcher, New York

Eduardo Gallardo, Partner, Gibson Dunn & Crutcher, New York

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the blue icon beside the box to send

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-869-6667 and enter your PIN when prompted Otherwise please send us a chat or e mail when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Hostile Takeover DefensesHostile Takeover Defenses

Joseph J. Basile

Adam H. Offenhartz

5

Eduardo Gallardo

OverviewOverview

I IntroductionI. IntroductionII. Takeover DefensesIII Wh t W C L F R tIII. What We Can Learn From Recent

Takeover Decisions and State Statutory F kFrameworks

IV. Best Practice Strategies

6

I IntroductionI. Introduction

7

Overview of U.S. M&A EnvironmentEnvironment

• 2010 public large-cap (>$1 billion) M&A activity increased following the end of the economic downturn

• In 2011, upward trend has continued

8 8

Source: Thompson Financial; Year-to-Date Numbers as of June 14, 2011

Overview of U.S. M&A Environment (cont )Environment (cont.)

• Large cap hostile and unsolicited takeover attempts on the rise

9 9

Source: Thompson Financial; Year-to-Date Numbers as of June 14, 2011

II Takeover DefensesII. Takeover Defenses

10

Stockholder Rights Plans

• Mechanics– Issuance to existing stockholders of rights to acquire common g g q

stock at a 50% discount in the event a potential acquiroraccumulates a specified percentage of voting shares (typically 10%-20%)H til i th t t i th i ht l i t itt d t– Hostile acquiror that triggers the rights plan is not permitted to exercise the rights, resulting in significant dilution

• Benefits of a Rights Plan– Provides Boards with adequate time to consider and respond to

unsolicited takeover proposals– Prevents the acquisition of a controlling interest that would

preempt Board consideration of alternativespreempt Board consideration of alternatives– Limits the use of abusive takeover tactics

11

Stockholder Rights Plans (cont’d)

• Opposed by many institutional investors, stockholder activists and proxy advisor firms

I d f i t t i t th i i ht l• Increased pressure for companies to terminate their rights plans• Implementation of rights plan with a term of more than 12 months

may lead to “withhold vote” recommendation by ISS

Stockholder Rights Plans – Changes from 2002-2011

60.00%

70.00%

30.00%

40.00%

50.00%

0.00%

10.00%

20.00%

12

Percentage of S&P 500*Source: 2002-2011 SharkRepellent.net

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Stockholder Rights Plans (cont’d)

• Recent DevelopmentsMany companies have decided to follow an “on the shelf” strategy– Many companies have decided to follow an on-the-shelf strategy

• Rights plan is kept ready for implementations at such time as the Company faces the actual threat of a hostile bid

– Definition of “Beneficial Ownership” expanded in some rights plans to include derivatives (e.g. cash-settled equity swaps)swaps)

– Use against controlling stockholder (e.g. iBasis/KPN)

13

Rights Plan and Takeover Strategy

• Since rights plans make it economically impracticable for a hostile bidder to close on an unsolicited tender offer, the end game in most h til t k i t t k t l f th t t b dhostile takeovers is to take control of the target board– If hostile bidder’s nominees take control of the board new

directors could deactivate pill and permit bidder to complete tender offertender offer

• A target’s ultimate vulnerability will depend on a hostile bidder’s ability to take control of the board within a reasonable timeframe

• This highlights the importance of classified boards

14

Classified Boards

• A classified board is one in which directors are divided into separate classes– Usually three classes, with directors in each class serving

three-year terms and only one class elected annually• Staggering directors’ terms makes it more difficult for raidersStaggering directors terms makes it more difficult for raiders

or dissidents to use proxy contest to take control of target immediately

• Under Delaware law if you have a classified board your• Under Delaware law, if you have a classified board, your directors can be removed only for cause

• The use of classified boards have come under pressure from corporate governance groups and activist stockholderscorporate governance groups and activist stockholders.

15

Action by Written Consent and Special MeetingsMeetings• What is “action by written consent”?

– Stockholders can take corporate action in writing, as opposed to at annual or special meetingspecial meeting

– Provision denying stockholders ability to act by written consent must be in Charter in Delaware

• Provisions regarding calling special meetings also may vary– Some permit stockholders owning over a specified percentage to call a special

meeting– Some permit only management and/or board to call special meetings

• Stockholders’ ability to act by written consent and/or call a specialStockholders ability to act by written consent and/or call a special meeting can significantly impact the vulnerability of a company with a declassified board

– Window to react to a hostile bidder is reduced from up to 13 months to 2-3 thmonths

• Corporate governance groups and activist investors have increased pressure on public companies to allow for action by written consent and give stockholders ability to call special meetings.

16

and give stockholders ability to call special meetings.

State Takeover Statutes• Come in many varieties

– Control Share Acquisition StatutesC S ( )– Business Combination Statutes (e.g. Delaware 203)

– Business Combination with Fair Price Provisions

• Most of these statutes will play a secondary role in the takeover context, as rights plan will typically be the main deterrent that a hostile bidder will face

• However, parties to a hostile bid must play close attention to these o e e , pa t es to a ost e b d ust p ay c ose atte t o to t eseprovisions, as they can be a trap for the unwary (e.g. inadvertent triggering of “beneficial ownership” definition under state statutes)

17

III. What We Can Learn From R t T k D i iRecent Takeover Decisions

and State Statutoryand State Statutory Frameworks

18

Selectica, Inc. v. Versata Enterprises, Inc.(Del Ch 2010)(Del. Ch. 2010)• Selectica and Versata had a tumultuous relationship in prior years, including

multiple lawsuits and takeover attemptsmultiple lawsuits and takeover attempts.

• In 2006, Selectica enlisted the help of outside experts to evaluate its net-operating loss (“NOL”) assets.

• Versata’s parent company began acquiring Selectica stock in 2008, and quickly bought over 5% of the company.

• Selectica lowered the trigger from its pre-existing shareholder rights plan from 15% to 4.99%.

– The rights plan was amended to grandfather in entities that already owned more than 4.99%, including Versata, but provided that the rights plan would be triggered if any grandfathered entity increased its holdings by .5% of Selecticatriggered if any grandfathered entity increased its holdings by .5% of Selecticacommon stock.

• Versata then intentionally triggered the rights plan, and litigation followed.

19

Selectica, Inc. v. Versata Enterprises, Inc.(Del Ch 2010)(Del. Ch. 2010)• The Court of Chancery upheld Selectica’s use of an NOL rights plan • Background on NOLs.

Federal tax law permits corporations to carry forward NOLs in order to offset– Federal tax law permits corporations to carry forward NOLs in order to offset taxes on future profits.

– However, a company may lose its ability to use NOLs if it experiences an “ownership change,” as that term is defined by federal tax law, which may be t i d b t k t Sh h ld h h ld l th 5% f thtriggered by stock turnover. Shareholders who hold less than 5% of the company are not counted.

• Applying Unocal, the Court held that Selectica’s Board had reasonable grounds for considering Versata a threat.

– Although the value of NOLs are, ex ante, inherently unknowable, and “by their very nature, have the potential of ultimately providing zero value to the company,” a board might properly conclude that a company's NOLs are worth protecting where it does so reasonably and in reliance upon expert advice.

• The Board’s use of the NOL rights plan was a reasonable response to the threat.

– The rights plan did not preclude the possibility of a successful proxy contest, even though there was a staggered board

20

even though there was a staggered board.– The Board consulted with experts in order evaluate its response to Versata.

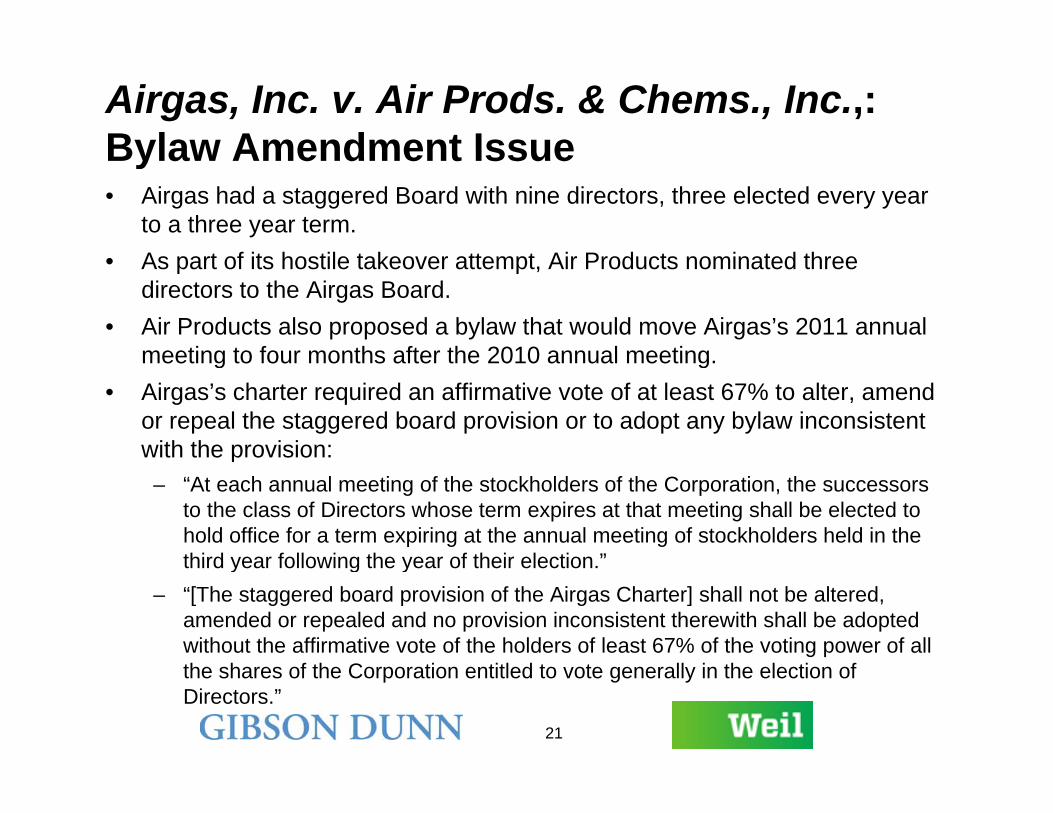

Airgas, Inc. v. Air Prods. & Chems., Inc.,: Bylaw Amendment IssueBylaw Amendment Issue• Airgas had a staggered Board with nine directors, three elected every year

to a three year term.A t f it h til t k tt t Ai P d t i t d th• As part of its hostile takeover attempt, Air Products nominated three directors to the Airgas Board.

• Air Products also proposed a bylaw that would move Airgas’s 2011 annual meeting to four months after the 2010 annual meetingmeeting to four months after the 2010 annual meeting.

• Airgas’s charter required an affirmative vote of at least 67% to alter, amend or repeal the staggered board provision or to adopt any bylaw inconsistent with the provision:p

– “At each annual meeting of the stockholders of the Corporation, the successors to the class of Directors whose term expires at that meeting shall be elected to hold office for a term expiring at the annual meeting of stockholders held in the third year following the year of their election ”third year following the year of their election.

– “[The staggered board provision of the Airgas Charter] shall not be altered, amended or repealed and no provision inconsistent therewith shall be adopted without the affirmative vote of the holders of least 67% of the voting power of all h h f h C i i l d ll i h l i f

21

the shares of the Corporation entitled to vote generally in the election of Directors.”

Airgas, Inc. v. Air Prods. & Chems., Inc., Bylaw Amendment Issue(Delaware Chancery Court)• At the 2010 annual meeting, Air Products successfully passed its requested

bylaw and elected its slate to Airgas’s Board.

• Airgas sued Air Products, arguing that the bylaw was inconsistent with the Airgas charter’s requirement of a 67% vote to amend the staggered board g q ggprovision.

• The Chancery Court upheld the bylaw.The charter pro ides that the ann al meeting m st be “held in the third ear– The charter provides that the annual meeting must be “held in the third year following the year of their election.”

– The bylaw moves the 2011 annual meeting to January, only four months after the 2010 meeting.

– But January is still 2011, the “third year” of the directors’ terms.

22

Airgas, Inc. v. Air Prods. & Chems., Inc.,Bylaw Amendment Issue(Delaware Supreme Court)• The Supreme Court reversed the Chancery Court, striking down the

bylawbylaw.

• Like the Chancery Court, the Supreme Court found the charter’s language ambiguous because it does not define “annual,” “year,” or “full term ”term.

• But extrinsic evidence indicated that directors should serve three full years:

Other Delaware state and federal court precedents “reflect[] the understanding– Other Delaware state and federal court precedents reflect[] the understanding . . . that directors of staggered boards serve a three year term.”

– As practiced, most companies with staggered boards provide that their directors serve three year terms.

– Academic commentary indicates that directors on staggered boards serve three year terms.

– The Court declined to state “with exactitude” how much of a deviation from a precise three years is acceptable but a third year that lasts only four months is

23

precise three years is acceptable, but a third year that lasts only four months is certainly unacceptable.

Air Products & Chemicals, Inc. v. Airgas, Inc.Rights PlanRights Plan

• Issue Presented – How long can a public company board of directors keep a rights plan in place to effectively prevent shareholders from tendering their shares into a premium offer when the shareholders are fully informed and the tender offer is fully financed and non-coercive?

– Or, in other words, under what circumstances can a board “just say no”?

• Holding: A board cannot “just say no” unless it can justify its refusal to pull• Holding: A board cannot just say no unless it can justify its refusal to pull the rights plan under Unocal.

– That is, the board must be able to show that (i) it reasonably perceived a threat to corporate policy and effectiveness and (ii) its response (here the rights plan)to corporate policy and effectiveness and (ii) its response (here, the rights plan) was reasonable in relation to the threat posed.

– Airgas makes clear that process matters.

24

A Prolonged Fight: The Airgas Timeline• 10/15/09 – Air Products & Chemicals, Inc. makes a private offer to acquire Airgas,

Inc. for $60 per share in stock.11/ /09 Th f ll Ai b d d id h ff l i i– 11/5-7/09 – The full Airgas board meets and considers the offer; relying in part on an internal stock price analysis and Airgas’s five year plan, it decides to reject the offer.

– 11/11/09 – Airgas calls Air Products to reject the offer.g j– 11/20/09 – Air Products sends Airgas a letter that puts its offer in writing.– 12/7/09 – Airgas board again considers the offer, along with legal and financial

analyses from outside advisors.– 12/8/09 – Airgas formally rejects the proposal via letter to Air Products.

• 12/17/09 – Air Products sends Airgas a revised proposal, which raises its offer to $62 per share in cash and stock

– 12/21/09 – The Airgas board holds a telephonic meeting to consider the offer.– 1/4/10 – On another teleconference the board resumes its meeting, including the

review of financial analyses provided by Airgas’s investment bankers; Airgas writes Air Products that the offer “grossly undervalues Airgas ”

25

writes Air Products that the offer grossly undervalues Airgas.

A Prolonged Fight: The Airgas Timeline• 2/4/10 – Air Products sends a public letter to the Airgas board announcing its

intention to launch a tender offer for $60 per share, all-cash, all-shares.2/8 9/10 Ai b d d h i f G ld S h– 2/8-9/10 – Airgas board meets and hears presentations from Goldman Sachs and Bank of America Merrill Lynch, which indicate that the offer is inadequate; the board unanimously agrees that $60 is too low.

– 2/10/10 – Airgas rejects the offer.g j

• 10/15/09 – Air Products & Chemicals, Inc. makes a private offer to acquire Airgas, Inc. for $60 per share in stock.

– 11/5-7/09 – The full Airgas board meets and considers the offer; relying in part11/5 7/09 The full Airgas board meets and considers the offer; relying in part on an internal stock price analysis and Airgas’s five year plan, it decides to reject the offer.

– 11/11/09 – Airgas calls Air Products to reject the offer.11/20/09 Air Products sends Airgas a letter that puts its offer in writing– 11/20/09 – Air Products sends Airgas a letter that puts its offer in writing.

– 12/7/09 – Airgas board again considers the offer, along with legal and financial analyses from outside advisors.

– 12/8/09 – Airgas formally rejects the proposal via letter to Air Products.

26

A Prolonged Fight: The Airgas Timeline• 12/17/09 – Air Products sends Airgas a revised proposal, which raises its offer to $62

per share in cash and stock12/21/09 Th Ai b d h ld l h i i id h ff– 12/21/09 – The Airgas board holds a telephonic meeting to consider the offer.

– 1/4/10 – On another teleconference the board resumes its meeting, including the review of financial analyses provided by Airgas’s investment bankers; Airgas writes Air Products that the offer “grossly undervalues Airgas.”g y g

• 2/4/10 – Air Products sends a public letter to the Airgas board announcing its intention to launch a tender offer for $60 per share, all-cash, all-shares.

– 2/8-9/10 – Airgas board meets and hears presentations from Goldman Sachs2/8 9/10 Airgas board meets and hears presentations from Goldman Sachs and Bank of America Merrill Lynch, which indicate that the offer is inadequate; the board unanimously agrees that $60 is too low.

– 2/10/10 – Airgas rejects the offer.

27

A Prolonged Fight: The Airgas Timeline• 2/11/10 – Air Products launches a $60 per share all-cash, all-shares tender offer.

– 2/20/10 – The Airgas board holds a telephonic meeting to discuss the tender ff G ld S h d B k f A i i d i d i ioffer; Goldman Sachs and Bank of America again render inadequacy opinions.

– 2/22/10 – Airgas files a Form 14D-9 with the SEC in which it recommends against tendering shares.

• 3/13/10 – Air Products nominates a slate of three candidates for election to the Airgas board and proposes amendments to Airgas’s bylaws.

• 7/8/10 – Air Products raises its bid to $63.50.– 7/9/10 – Air Products writes Airgas to reiterate its willingness to negotiate.– 7/15 and 20/10 – The Airgas board meets and its financial advisors again render

inadequacy opinions.– 7/21/10 – In a public letter, Airgas rejects Air Products’ revised offer and its

invitation to meet; Airgas also files an amendment to its 14D-9 rejecting the $63.50 offer as “grossly inadequate” and recommending against tendering.

28

A Prolonged Fight: The Airgas Timeline• 9/6/10 – Air Products again increases its offer, to $65.50 per share.

– 9/7/10 – The Airgas board meets to consider the revised offer; it receives d d i d i i d i j h ffupdated inadequacy opinions and again rejects the offer.

– 9/8/10 – Airgas again amends its 14D-9 and recommends against tendering.

• 9/15/10 – Airgas annual meeting at which the Air Products nominees are elected to g gthe Airgas board and the Air Products-backed bylaw amendments are adopted.

• 10/4-8/10 – Week-long trial in the Delaware Chancery Court relating to Airgas’s rejection of the $65.50 offer and the board’s decision to keep the company’s takeover defenses in place in response to that offer.

• 10/8/10 – Chancellor Chandler upholds the January Bylaw.

/ / f• 11/4/10 – Principals from both sides meet to discuss the proposed transaction, but the meeting does not yield any results.

• 11/23/10 – The Delaware Supreme Court unanimously reverses Chancellor Chandler d h ld th t th J B l i i lid (S N 29 2010 Cli t Al t)

29

and holds that the January Bylaw is invalid (See Nov. 29, 2010 Client Alert).

A Prolonged Fight: The Airgas Timeline• 12/2/10 – In light of the Supreme Court’s decision concerning the January Bylaw,

Chancellor Chandler issues a Letter Order asking each side to answer a number of questions and submit supplemental post trial briefingquestions and submit supplemental post-trial briefing.

• 12/8/10 – In response to a letter from the Air Products-nominated directors, Airgas agrees to the retention of a third financial advisor to advise the board.

• 12/9/10 – Just before the supplemental briefing is due, Air Products announces its “best and final” offer of $70 per share in cash.

• 12/10/10 – Airgas’s independent directors retain Credit Suisse and the Air Products-12/10/10 Airgas s independent directors retain Credit Suisse and the Air Productsnominated directors retain Skadden, with expenses to be paid by Airgas.

• 12/10/10 – Responses to Chancellor Chandler’s December 2 Letter Order due.

• 12/21/10 – The Airgas board meets, and, after considering its five-year plan and inadequacy opinions from three financial advisors, it unanimously rejects Air Products’ final offer.

– 12/22/10 – Airgas amends its 14D-9 to announce the board’s rejection of the $70

30

– 12/22/10 – Airgas amends its 14D-9 to announce the board s rejection of the $70 offer.

A Prolonged Fight: The Airgas Timeline

• 12/23/10 – Chancellor Chandler issues a Letter Order that rejects Air Products’ request for a new trial in light of the $70 offer; however, Chancellor Chandler does permit additional discovery and a supplemental evidentiary hearing related to the $70permit additional discovery and a supplemental evidentiary hearing related to the $70 offer.

• 1/25-27/11 – Supplemental evidentiary hearing in order to complete the record on the $70 offer$70 offer.

• 2/15/11 – The Chancery Court upholds the Airgas rights plan; Air Products rescinds its offer.

31

Airgas Stock Price

$70 00

$75.00Sept. 6: $65.50 Dec. 9: $70

$65.00

$70.00

Feb 11: $60

July 8: $63.50

$60.00

Feb. 11: $60

$50.00

$55.00 Stock Price

Tender Offer Price

$45.00 Oct-

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul-

Aug

Sep

Oct-

Nov

Dec

Jan

Feb

Mar

32

-09

v-09

c-09

-10

b-10

r-10

-10

y-10

-10

-10

g-10

p-10

-10

v-10

c-10

-11

b-11

r-11

Chancellor Chandler Credited Airgas’s Process of Evaluating the OffersProcess of Evaluating the Offers• Airgas regularly updated its five year plan.

• Airgas retained Wachtell, Goldman Sachs and Bank of America Merrill Lynch.Airgas retained Wachtell, Goldman Sachs and Bank of America Merrill Lynch. The Board received updated analysis from its financial advisors each time Air Products increased its offer.

• After Air Products waged a successful proxy contest and installed 3 g yindependent directors on the Airgas board, Airgas held a new director orientation session. The new directors challenged the board’s economic assumptions underlying the five year plan, yet left the meeting convinced that the five year plan was conservative.the five year plan was conservative.

• Airgas retained independent outside legal counsel for the three Air Products nominated-directors, and at the request of these directors, retained Credit Suisse to conduct an independent financial analysis. When Air Products made p yits best & final $70 offer, management presented an updated five year plan, Goldman & BOA made updated financial presentations, and Credit Suisse presented its independent analysis, explaining its evaluation and how its methodology differed from Goldman & BOA.

33

methodology differed from Goldman & BOA.

Air Prod. & Chem., Inc. v. Airgas, Inc. –Emerging LawEmerging Law • Applied Unocal in analyzing Airgas’s rights plan.

Prong 1: Target board had reasonable ground to believe a danger to corporate– Prong 1: Target board had reasonable ground to believe a danger to corporate policy and effectiveness existed.

– Prong 2: The defensive measures were reasonable in relation to the threat posed.

• Recognized inadequate price as a possible threat under Unocal Prong 1.

– Board must reasonably believe that the tender offer price is inadequate.

• Recognized the reasonableness of the defensive measures under Unocal Prong 2.

– Rights Plan not preclusive.

• Upheld the Rights Plan but suggested that the Delaware Supreme Court might want to revisit the law regarding Rights Plans.

34

Air Prod. & Chem., Inc. v. Airgas, Inc. –Unocal Prong 1Unocal Prong 1• Chancellor Chandler emphasized the Airgas Board’s process in

investigating the threat of Air Product’s offer, the reasonableness of the process used in its investigation and the reasonableness of the results theprocess used in its investigation and the reasonableness of the results the Board reached.

• Three types of threats implicitly recognized in Paramount Commc’ns, Inc. v. Ti I (“Ti ”)Time, Inc. (“Time”):

– Structural Coercion–Risk that disparate treatment of non-tendering shareholders might distort shareholders’ tender decisions.

– Opportunity Loss—Dilemma that hostile offer might deprive target shareholdersOpportunity Loss Dilemma that hostile offer might deprive target shareholders of the opportunity to select a superior alternative offered by target management.

– Substantive Coercion—Risk that shareholders will mistakenly accept an underpriced offer because they disbelieve management’s representations of intrinsic valueintrinsic value.

35

Airgas - Substantive Coercion, Inadequate PricePrice• Delaware Court of Chancery has attempted to cut back on a broad

conception of substantive coercion: – Key issue is whether inadequate price alone is sufficient to be a threat.

• Inadequate price was the only threat alleged by Airgas board.

• Airgas argued that merger arbitrageurs/short term investors threatened the• Airgas argued that merger arbitrageurs/short-term investors threatened the long-term goals of the company and long-term investors.

– Merger arbitrageurs – bought stock when Air Products announced its interest in acquiring Airgas and would be willing to tender an inadequate offer because they q g g g q yare focused on short term returns.

• Chancellor Chandler: Found Airgas acted in good faith and relied on advice of its financial and legal advisers.

• BUT Chancellor Chandler arguably did not go all the way and say that inadequate price alone is sufficient to justify defensive measures.

– Included notion that there must be a fear that shareholders will actually tender

36

yinto the offer.

Airgas - Reasonableness of Defensive Measures – Unocal Prong 2Measures – Unocal Prong 2• Airgas defensive measures were not preclusive “if they delay Air Products

from obtaining control of the Airgas board (even if that delay is significant) l bt i i t l t i t i th f t i li ti llso long as obtaining control at some point in the future is realistically

attainable.” – Chancellor Chandler: “an Air Products victory at the next annual meeting is very

realistically attainable.” y

• “The board’s actions do not forever preclude Air Products, or any bidder, from acquiring Airgas or from getting around Airgas's defensive measures if the price is right. In the meantime, the board is preventing a change of control from occurring at an inadequate price.”

– Airgas’s defensive measures were within the range of reasonable responses to the perceived threat of the inadequate bid by Air Productsthe perceived threat of the inadequate bid by Air Products.

37

Delaware Alternatives: Nevada• Nevada corporate code grants greater deference to directors in the takeover

contest: Th b i j d t l i h i d i th N d d (NRS 78 138)– The business judgment rule is enshrined in the Nevada code. (NRS 78.138)

– Directors may consider “other constituencies” in exercising their fiduciary duties. (NRS 78.139)

– Directors may schedule an annual meeting within 18 months of the prior annual meeting. (NRS 78.330; 78.345)

– Directors do not automatically consent to personal jurisdiction in Nevada by virtue of their board membership. (compare 8 Del. C. 3114)

Di t l th i d b t t t t i l t i ht l i• Directors are expressly authorized by statute to implement a rights plan in response to a takeover attempt (NRS 78.139; 78.195; 78.350).

– In Delaware, most rights plans are evaluated under a Unocal-like, but takeover defenses that disenfranchise shareholders must have a “compelling justification” under Blasius.

– In Nevada, most rights plans are evaluated with the business judgment rule, but takeover defenses that disenfranchise shareholders are evaluated under Unocal.

M b d d l l ti d t i ht l i lt l ?

38

• May a board delay an annual meeting and enact a rights plan simultaneously?

Delaware Alternatives: Georgia• Invacare Corp. v. Healthdyne Techs., Inc., 968 F. Supp. 1578 (N.D. Ga.

1997).• Healthdyne’s Board adopted a “dead hand” rights plan• Healthdyne s Board adopted a dead hand rights plan.

– A dead hand rights plan restricts the ability of future boards to redeem the plan.– In this case, Healthdyne was facing a proxy contest, and therefore designed the

rights plan so that only “continuing directors,” i.e., the directors who voted for the plan, could redeem it.

• The Court refused to enjoin the plan, holding that Georgia corporate law embraces continuing director provisions as part of a takeover response.

• O.C.G.A. 14-2-624(c) (board has the “authority to determine, in its sole discretion, the terms and conditions of the rights, options, or warrants” it issues)

• Note: no other court has allowed dead hand rights plans• Note: no other court has allowed dead hand rights plans.• See Carmody v. Roll Bros., Inc., 723 A.2d 1180 (Del. Ch. 1998) (invalidating

dead hand rights plan on the grounds that any differential voting power of directors is void unless provided for in the certificate of incorporation per 8

39

directors is void unless provided for in the certificate of incorporation per 8 Del. C. § 141(d)).

IV Best PracticesIV. Best Practices

40

Suggested Best Practice Strategies

• Develop, Review and Manage Execution of Long-Term Business/Strategic Plan– Key assumptions– Projections– Benchmark performance against peers– Regular Board updates

• Assemble the TeamKey officers– Key officers

– Counsel– Investment banker

PR fi– PR firm– Proxy solicitor

41

Suggested Best Practice Strategies (continued)Suggested est act ce St ateg es (co t ued)

• Review Defensive Profile– Charter– By-laws– State anti-takeover statutesState anti takeover statutes– “Change of control” provisions in employment

agreements and key contracts• Regular Team Meetings• Regular Team Meetings

– Review recent developments– Consider potential hostile acquirers, activist

stockholders “white knights”stockholders, white knights– Consider issues that a potential hostile acquirer may

face

42

Suggested Best Practice Strategies (continued)Suggested est act ce St ateg es (co t ued)

• Attention to Relationships with Stockholdersp– Maintain current list– Monitor trading activity– Develop plan for meeting with key stockholders and

proxy advisory services

43

Suggested Best Practice Strategies (continued)Suggested est act ce St ateg es (co t ued)

• Develop Communications Planp– Designate one spokesman– Identify and develop messages for key constituencies

Monitor news stories blogs message boards etc– Monitor news stories, blogs, message boards, etc.

• Regular Board Discussions– Usually no need for a special committee– Important to maintain a good record

44

PanelistsPanelists

Joseph J. Basile, PartnerJosep J as e, a t eWeil, Gotshal & Manges LLP100 Federal Street, Floor 34Boston, MA 02110 Tel: +1 617 772 8334Fax: +1 617 772 8333joseph basile@weil [email protected]

Eduardo Gallardo, PartnerGibson, Dunn & Crutcher LLP200 Park AvenueNew York, New York 10166Tel: +1 212.351.3847Fax: +1 [email protected]

Adam H. Ofenhartz, PartnerGibson, Dunn & Crutcher LLP200 Park AvenueNew York, New York 10166T l 1 212 351 3808

45

Tel: +1 212 351 3808Fax: +1 212 351 [email protected]