Hospitality investments and developments, lessons … · Asia-Pacific countries (main cities) offer...

56

Presented by: Robert McIntosh, Executive Director, CBRE Hotels, Asia Pacific. Hospitality investments and developments, lessons from Asia- Pacific for Vietnam’s future strategy Sheraton Saigon 21 July, 2010

Transcript of Hospitality investments and developments, lessons … · Asia-Pacific countries (main cities) offer...

Presented by:

Robert McIntosh, Executive Director, CBRE Hotels, Asia Pacific.

Hospitality investments and developments, lessons from Asia-Pacific for Vietnam’s future strategy

Sheraton Saigon 21 July, 2010

CB Richard Ellis | Page 2

Hotel Performances

Hotel Investors

New Developments

Investment Strategies

Condo-Hotel

Mixed Use Hotel

Economy/Budget Sector

Villa-Resort

SUMMARY

Hotel Performances

CB Richard Ellis | Page 4

Vietnam has still the third highest Average Daily Rate (ADR) in Asia Pacific due the remarkable increase from March to Dec 2008 (similar to Singapore)

Singapore has experienced the highest correction in ADR due to the decline in business clients during the economic slowdown

Indonesia is the only country where the rates have constantly increased.

Hotel Performance in the Region (Upper-Upscale-Luxury)

CB Richard Ellis | Page 5

HK and Singapore still lead the market in term of occupancy rates.

Vietnam had the largest drop in occupancy (25 percentage points from its highest), followed by Thailand (20 percentage points) and Singapore (15 percentage points)

Hotel Performance in the Region (Upper-Upscale-Luxury)

CB Richard Ellis | Page 6

The RevPAR levels in Asia-Pacific are currently segmented in two groups.

In every area the RevPAR shows indications of gradual improvement as economies recover.

Hotel Performance in the Region (Upper-Upscale-Luxury)

CB Richard Ellis | Page 7

Hotel Performance in the RegionSome keys points:

Singapore is still a very attractive market due to the demand drivers and recovering economy

Thailand is on the way to recover from the drop in occupancies due to the recent political instability.

Vietnam has a higher volatility due to the relative immaturity of the market

China has had a strong economic trend but substantial oversupply in some markets

HK has recovered strongly with limited new supply

CB Richard Ellis | Page 8

$0$50

$100$150$200$250

ADR Rates Countries (selected cities)

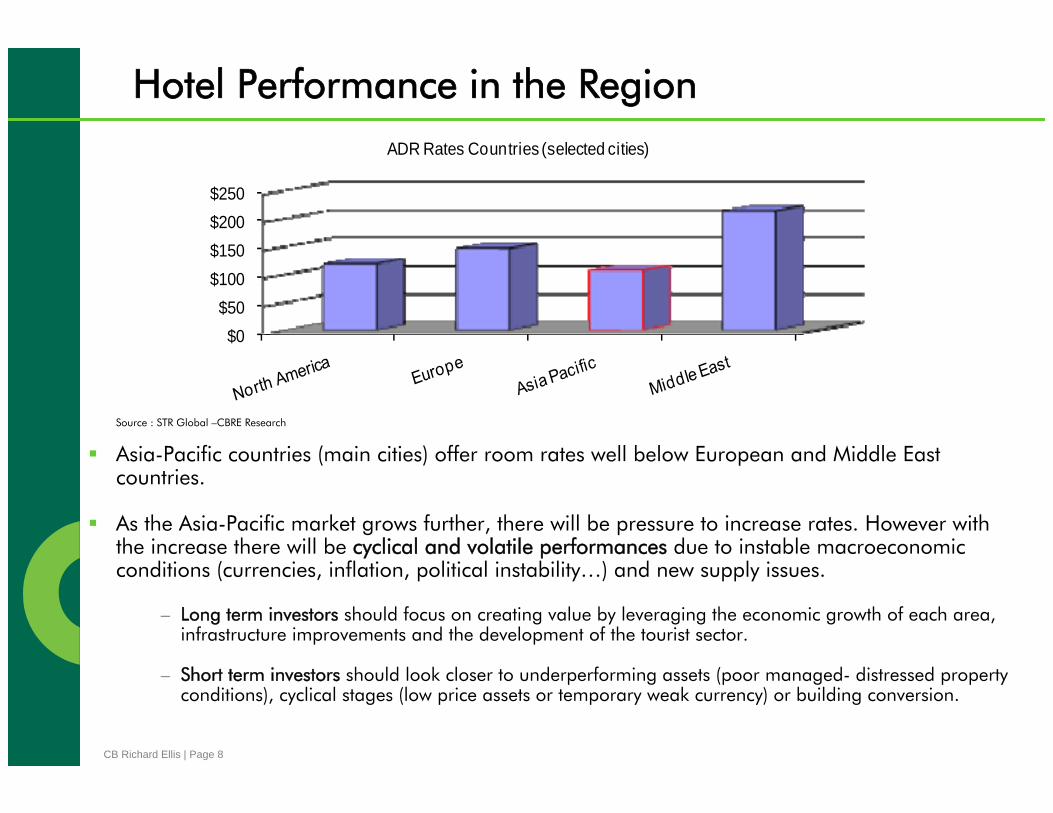

Hotel Performance in the Region

Asia-Pacific countries (main cities) offer room rates well below European and Middle East countries.

As the Asia-Pacific market grows further, there will be pressure to increase rates. However with the increase there will be cyclical and volatile performances due to instable macroeconomic conditions (currencies, inflation, political instability…) and new supply issues.

– Long term investors should focus on creating value by leveraging the economic growth of each area, infrastructure improvements and the development of the tourist sector.

– Short term investors should look closer to underperforming assets (poor managed- distressed property conditions), cyclical stages (low price assets or temporary weak currency) or building conversion.

Source : STR Global –CBRE Research

Hotel Investors

CB Richard Ellis | Page 10

Investment main points

Economic recovery

Overhang of investment capital

Rapidly rising visitor numbers

New demand drivers

Increases in supply

Repositioning Asia-Pacific as a tourism destination (including Singapore, Vietnam, Cambodia and China)

Major local investors are looking globally

Little local distress

CB Richard Ellis | Page 11

Hotel Sales by country

2009 more properties were transacted but at lower volume compared to 2010 (except Australia and Vietnam). This is smaller properties being sold, lower prices or some distressed asset.

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

0

5

10

15

20

25

30

35

Australia Japan China Hong Kong Vietnam Malaysia Singapore Thailand

Mill

ions

Hotel Sales Activity in Asia Pacific

No. Transactions 2009

No. Transactions 2010(td)

Volume (US$ )2009

Volume (US$ )2010(td)

Source : RCA and Cbre Research

CB Richard Ellis | Page 12

Investments Activities in the RegionIn 2010 lower number of transactions due to the different risk perception from buyer/seller (divergence from “asking price” to “offered price”)

In 2010 some deals were done on Greenfield Projects. This is a positive sign of restored optimistic expectations for the long term development of the sector.

……Future ?

CB Richard Ellis | Page 13

Who is investing now in Hotels and Resorts ?

On a global scale, few of the largest buyers in 2006-07 are still active in 2009-10.

REITs and funds investment capacity - diminished

International Operators – rarely invest

Current categories of investors are:

• Public Companies

• High Net Worth Individuals

• Sovereign Wealth Funds

Looking for :• Diversity

• Trophy assets

• Discounts to previous figures

• Clear turnaround potential

• Operator and asset management skills

• Security and risk minimization

CB Richard Ellis | Page 14

Investment Vehicles Main Target Risk ToleranceLuxury Segment-Large Developments Plan HighOperating Properties-Strong Historical Performance-Central Locations LowOperating Hotels Med-HighDevelopment Sites-Mixed Use Development High

Operating Hotel-Under construction-Branded-Dev sites MedOperating Upper Upscale Hotel with strong historical LowHighly Strategic Properties-Good Location-150 rooms min Low-MedBranded Operating Hotel Med-HighLocal Properties HighDevelopment Sites High

Investment Vehicles Investment rational Exit StrategyDiversification- Hold-Operate(outsource operator)Operative Income-ROI Hold-Capital Gain-SellDiversification-Operative Income Hold-OperateCapital Gain-Operative Income Build-SellROI Build or Buy-Operate Short time-SellDiversification-Operative Income Hold-Operate(outsource operator)Brand Expansion-Operative Income Hold-OperateTrophy Asset- Diversification-Operative Income Hold-Operate(outsource operator)Diversification-Status Hold-OperateROI-Trophy Asset Build-Operate-Sell

GovernmentDevelopers

Investment FundInstitutional Investor

Hotel OperatorHNW

Sovereign Wealth Fund

REITPublic CompanyProperty Company

Sovereign Wealth FundREITPublic CompanyProperty Company

GovernmentDevelopers

Investment FundInstitutional InvestorHotel OperatorHNW

Investment Vehicles

In hotel investments there are wider categories of Investors with different characteristics and modus operandi :

Different Risk tolerances (high-low)

Different Investment rational (not only ROI)

Different management strategy (International operator or self operated ?)

CB Richard Ellis | Page 15

Construction costs "100 room Hotel"

$-

$5

$10

$15

$20

$25

$30

Toki

o

Mac

au

Hon

g K

ong

Sing

apor

e

Seul

Bru

nei

KL

BK

Viet

nam

Bei

jing

Shan

ghai

Man

ila

Gua

ngzh

ou

Jaka

rta

Milli

ons

Upscale Mid-Scale

Construction costs in the Region…..If cannot buy, where can I build it ?

Construction costs in Tokyo are roughly three times Jakarta, Guangzhou and Manila.

Vietnam is singly more expensive in the Mid-Scale level than Thailand or China.

On average there is a 40% increase in costs is building Upscale compare to Mid-Scale(on GFA basis). …what would be the difference in profit … ?

Source Davis&Langdon. Note :excluding FF&E and land costs, indicating international quality building

Adoptions :

Upscale (32m2room-50% total eff)

Mid-Scale(28m2room-60% total eff)

CB Richard Ellis | Page 16

$0

$40

$80

$120

$160

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

Construction Costs(sqm/GFA) VS 2010 RevPar

Upscale REVPAR

Construction costs and Performances

The REVPAR is the single most important indicator of the value in an operating asset.

In countries where REVPAR is relatively higher compared to construction costs, there could be more pressure on Land Price increases to fill the gap.

Other fundamental costs to consider will be : (1) Land Price (2) approvals process (3) Operating costs

Indicative REVPAR as at 2010, subject to changes .Source Davis&Langdon. Note :excluding FF&E

and land costs, indicating international quality building

CB Richard Ellis | Page 17

Investment summary

Economic recovery to continue?

As managers of investment capital gain confidence they will spend

Rapidly rising visitor numbers to continue in the region

Increases in supply may make investors cautious

Focus on secure, low risk, locations

Major investors will focus on distress

Prices will rise and more transactions occur

Financing

CB Richard Ellis | Page 19

Financing

Reduction in the number of banks willing to finance hospitality projects due to : – Lower liquidity-higher risk in the sector– Long payback period– Lack of capabilities (bank) in the sector (in case of asset repossession

banks will require support from operators…)

Intra-regional lending– Banks tend to not provide financing in foreign countries (relative to the country

where they are based). Currency issues and ownership issues are among the mains reasons.

What do they finance ?– Operating assets with strong historical financials are, by far, the preferred assets. – International Operator and a Brand is an advantage for a number of banks.– Villa/Resort projects are well perceived because of the pre-sale structure.– Valuation Reports done by independent companies are a fundamental document

for obtaining a banking loan.

New Developments

CB Richard Ellis | Page 21

Current and Future Supply in Asia Pacific 2010

14%20%

66%

0

200

400

600

800

1,000

1,200

1,400

Upscale-Luxury Economy-MidScale Independentsqm

(000

)

0 %

1 0 %

2 0 %

3 0 %

4 0 %

5 0 %

6 0 %

7 0 %

Existing Supply Active Pipeline % of new supply(on total)

New Developments

The majority of the new developments in the Region are concentrated in Upscale to Luxury segment.

A large part of new supply will make use of International Operators, whilst in the past the majority were unaffiliated properties (no international operator)

Source : HNN and STR

Investment Strategies

CB Richard Ellis | Page 23

What is your investment strategy ?

Build and Sell upon completionBuild – Operate - SellBuy-renovate/repositioning-SellBuilding ConversionLand Acquisition-Presale Villas-Operate the ResortResort as value addedBuild and long term lease

CB Richard Ellis | Page 24

Strategy 1 - Build and Sell

Typical Investment strategy of Developers, Property Companies or Funds not specialized in hospitality sector

Frequently the hotel component is part of a major complex and the developer wants to shorten the payback period with the sale of the asset.

Typical cycle :

The achievable ROI largely depend on (1) land price and (2) stage of the hotel cycle (at the moment of sale) (3) construction costs (4) hotel market conditions in the area.

Also important factors influencing the value of the under construction asset are : • Hotel Design• Size (minimum number of rooms)• Facilities provided• Operator commitment• Hotel Market performances in the area

2-6 Months yLand Acquisition OpeningLand clearance Basement Superstr-Fitout Pre- OpeOut Flow Out Flow Selling period In-FlowBank Financing Equity

1.5-2.5Years

Contruction Stage

Income from sale

3-6 Month 1-2 years

CB Richard Ellis | Page 25

…..Design matters …. The asset characteristic will affect the number of investors available.

International investors want assets of an International standard (any conversion costs or adjustments after completion could be quite expensive)

Build and Sell

Common Mistakes Reasons Consequence Consequence in your investment

Incorrect Design/LayoutPoor planning stage- architects with no experience in hotel operation

Low Efficiency-Higher Operating Costs

Less Attractive building-Lower number of investors-Lower Achievable Sale Price

Incorrect Room Size (too small)Poor planning stage- attempt to maximize the efficiency ratio

Decreased Achievable Room Rates and achievable property rating

Lower number of investors available-Lower number of operators Available- Lower value per room

Incorrect Room Size (too large)Poor planning stage-inexperienced developers-Building conversion

Increased the fit-out costs, waste of useful space, decreased building efficiency.

Lower Hotel performance(lower number of rooms)-

Incorrect facilities (F&B, Meeting rooms, Karaoke…) too many

Poor planning stage( preliminary market analysis)

Lower building efficiency-waste of useful space-Higher Operating costs

Less Attractive building-Lower number of investors-Lower Hotel performance(lower number of rooms)

Incorrect facilities (F&B, Meeting rooms, Karaoke…) scarce

Poor planning stage( preliminary market analysis) Lack of necessary services

Less Attractive building-Lower number of Operator available-Lower Achievable Sale Price

CB Richard Ellis | Page 26

Good locations but … not easy to sell…

Build and Sell -design issues

CB Richard Ellis | Page 27

Typical Investment strategy of REIT, Hospitality Funds with experience in hospitality.

The ROI largely depends on (1) hotel income (2) land costs/construction costs.

International Operator needed? …maybe yes .. or… maybe not ..

Do you have the capabilities to manage hotels ?

Poor management can lead to:

• Lower RevPAR (Rate and Occ)

• Higher costs

• Poor property maintenance

Strategy 2 - Build, Operate ….and …Sell

3 months 6 Months-1 YearLand Acquisition OpeningLand preparation Basm-Superstr Superstr-Fitout Pre- Ope Start-up period Operating PeriodOut Flow Out Flow Out Flow Inflow (high fixed costs) Operating income SaleBank Financing Operating income Income from sale

2-3 yearsTotal Period 4-6 years

Contruction Stage Operative Asset

Equity Refinancing

3-6 Month 1-2 years

CB Richard Ellis | Page 28

A number of hotel owners in Asia are not using the full potential of the property. Some of them they only target operating costs.

In some cases developers are also the original owners of the land. The investment is limited to construction costs. Those costs can be easily repaid by mediocre performances. That discourages hotel owner from seeking better performance. ….ask yourself, is your profit good enough ?

Common Mistakes in Operation stage Reasons Consequence Consequence in your investment

Not prepared "pre-opening"First Hotel project-No pre-opening budget-disregard for this stage-

Low occupancy-Very low rates (opening discount…!)-Disappointed clients… Negative impact on the future operation

Poor distribution system/rev management.

Not experience in Hotel business-No brand-No marketing or sale systems

High discount to travel agents-failure in price parity.

Lower achieved Rates(even if high published rates)

Inaccurate rooms' pricing

Poor planning stage(market analysis)-No sale system- Unrealistic expectations(Ego driven) Lower Occupancy-Disappointed clients Lower RevPar-Repositioning costs

Not adequate services/staff

Not experience in Hotel business-Poor planning stage(market analysis)- Inaccurate costs allocation.

Disappointed Clients-Lower Rates-Image damaged Lower RevPar-Higher costs (% of rev)

Scarce Property Mainanenace system Short term cost saving Deteriorating property conditions

Lower property value-fast deteriorating condition-higher capex future expenditure

Build, Operate ….and …Sell

…..Performance matters …. The asset value will be directly affected by the performance achieved.

CB Richard Ellis | Page 29

If decided to select an Operator, “Performance test” in the Management Contract and “Incentive fee” are a tools to motivate higher performances. But make sure to have also the right “termination clause”.

Hotel Consultants can support the Planning stages, Technical Support, Pre-Opening, Operations but they will not bring any benefit in terms of “Brand Name”.

Build, Operate ….and …Sell

Brand is extremely important in the hospitality business. Being associated with the wrong brand or wrong operator could dramatically affect the performance of your property….

CB Richard Ellis | Page 30

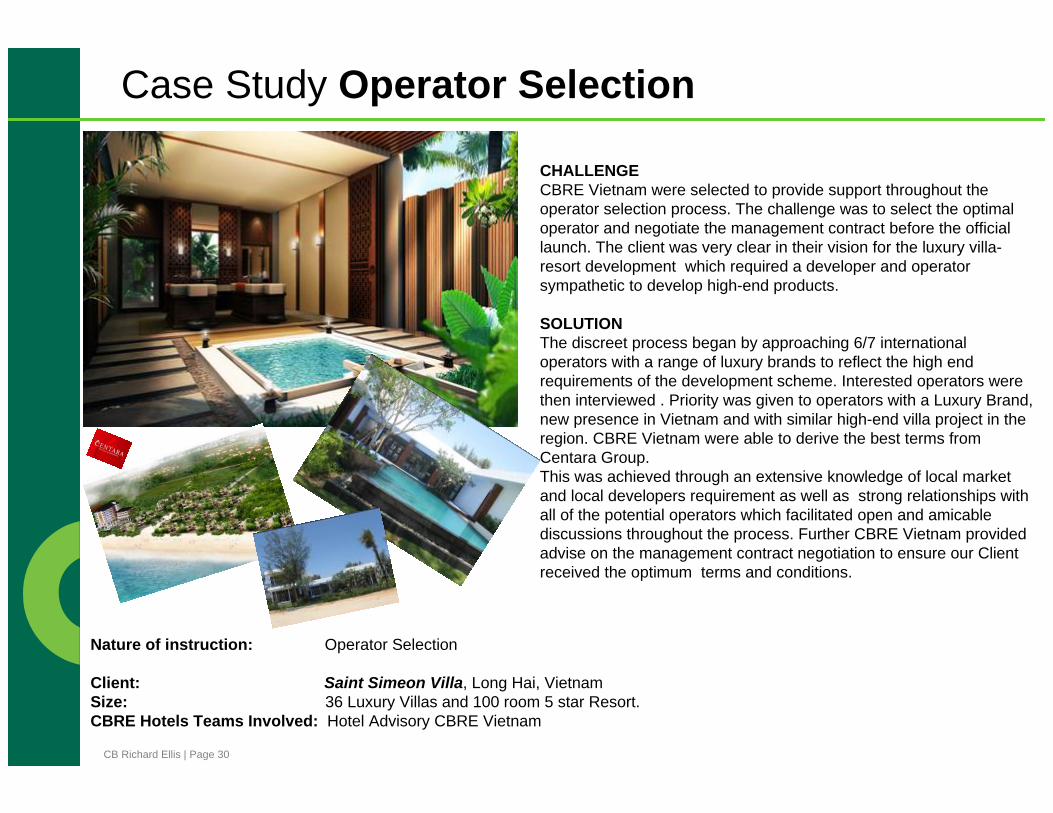

Case Study Operator Selection

CHALLENGECBRE Vietnam were selected to provide support throughout the operator selection process. The challenge was to select the optimal operator and negotiate the management contract before the official launch. The client was very clear in their vision for the luxury villa-resort development which required a developer and operator sympathetic to develop high-end products.

SOLUTIONThe discreet process began by approaching 6/7 international operators with a range of luxury brands to reflect the high end requirements of the development scheme. Interested operators were then interviewed . Priority was given to operators with a Luxury Brand, new presence in Vietnam and with similar high-end villa project in the region. CBRE Vietnam were able to derive the best terms from Centara Group. This was achieved through an extensive knowledge of local marketand local developers requirement as well as strong relationships with all of the potential operators which facilitated open and amicable discussions throughout the process. Further CBRE Vietnam provided advise on the management contract negotiation to ensure our Client received the optimum terms and conditions.

Nature of instruction: Operator Selection

Client: Saint Simeon Villa, Long Hai, VietnamSize: 36 Luxury Villas and 100 room 5 star Resort.CBRE Hotels Teams Involved: Hotel Advisory CBRE Vietnam

CB Richard Ellis | Page 31

Typical Investment strategy of expert Hotel Investors

The ROI largely depend on (1) property price/condition and (2) increase in hotel performance (success in the repositioning operation)

In some cases the asset must be demolished and built again

Vietnam and China have an enormous potential.

Typical rooms refurbishment costs (4-5 star ) $10,000-$20,000 per room

Strategy 3 - Buy, Reposition, Sell

Property Acqusition SaleValuation/Negotiation Refusbisment/RebrandingCost Cost ExitBank Financing Equity

12-24 Months

Selling periodIncome from sale

1-6 Months 6-12 MonthsRepositioning

Re Opening

CB Richard Ellis | Page 32

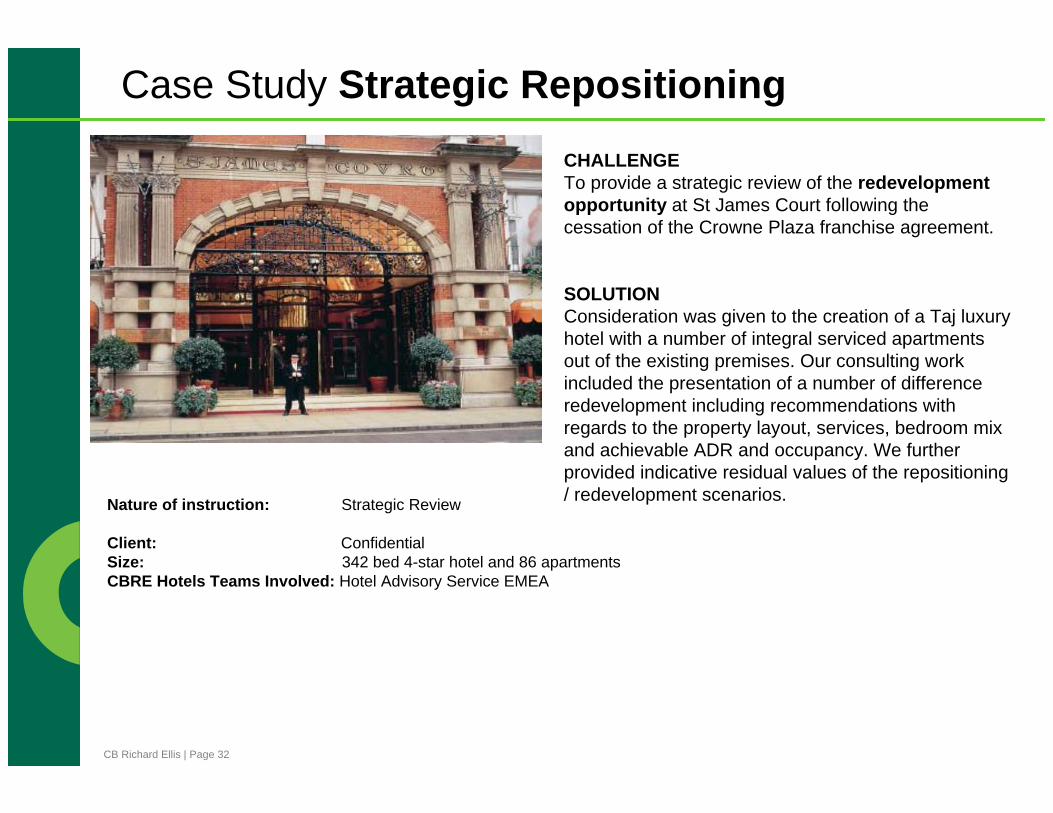

Case Study Strategic RepositioningCHALLENGETo provide a strategic review of the redevelopment opportunity at St James Court following the cessation of the Crowne Plaza franchise agreement.

SOLUTIONConsideration was given to the creation of a Taj luxury hotel with a number of integral serviced apartments out of the existing premises. Our consulting work included the presentation of a number of difference redevelopment including recommendations with regards to the property layout, services, bedroom mix and achievable ADR and occupancy. We further provided indicative residual values of the repositioning / redevelopment scenarios.Nature of instruction: Strategic Review

Client: ConfidentialSize: 342 bed 4-star hotel and 86 apartmentsCBRE Hotels Teams Involved: Hotel Advisory Service EMEA

CB Richard Ellis | Page 33

Case Study Valuation for Acquisition

CHALLENGECBRE Vietnam were selected to provide a valuation service for the potential acquisition of an international five star hotel located in the CBD of HCMC. The challenge was to accurately assess the current value of the property taking into consideration the changeable market conditions, the weak but recovering market situation and the potential threats of new supply in HCMC. The finding of the valuation works would have been critical for the purchasing decision of the foreign investor.

SOLUTIONThrough their in-depth knowledge of the hotel market in Vietnam and the extensive database of information including operating costs,competitor data, transaction evidences, current and future supply information, CBRE Vietnam were able to assess the fair market value based on six (6) different methodologies of valuation. Further an extensive rational of input data used in the Cash Flow we provided to the investor to aid the negotiation process.

Nature of instruction: Valuation for acquisition

Client: Foreign InvestorSize: 5 star hotel- ConfidentialCBRE Hotels Teams Involved: Hotel Advisory VAS CBRE Vietnam

CB Richard Ellis | Page 34

Typical Investment strategy of property developer or building owners.

The ROI largely depend on (1) conversion costs and (2) hotel market condition

Efficient strategy in emerging markets where the demand/supply characteristic in some sector changes rapidly….

Must comply with local regulation in term of zoning and licenses

In some properties need structural changes (high costs)

Another alternative is the long lease of the building (the investors will pay conversion costs)

Strategy 4 - Building Conversion

Property Acqusition Sale SaleValuation/Negotiation Tenants relocation Costruction Fit-out OpeningCost Cost ExitBank Financing Equity Operating income

Selling periodIncome from sale

1-6 Months 6-18 MonthsConversion

12-24 Months

CB Richard Ellis | Page 35

CHALLENGEOur client owns a grade B office building in the Hong Kong’s CBD. They received a proposal from a potential investment partner to take up part ownership of the property, which the potential partner wanted to convert into a boutique hotel and then manage under their own independent brand.

CBRE Hotels were asked to provide a strategic review of the conversion proposal, to provide financial feasibility and a hotel industry overview, and make recommendations on the conversion feasibility.

SOLUTIONThe existing office building was fully leased, and CBRE Hotels had to take into account the cost of obtaining vacant possession and conversion costs, to evaluate whether a hotel option for the site would be financially better than an office building. The market positioning of the hotel was proposed at the 4-star market, and CBRE Hotels made recommendations on the optimal positioning, which was suggested to target the luxury end of the market.The client took our recommendations to negotiate better terms with the potential investment partner and the proposal is under negotiation.

Client: ConfidentialSize: 70 rooms, high end hotelCBRE Hotels Teams Involved: CBRE Hotels Hong Kong office Nature of instruction: Financial Feasibility and Hotel Advisory

Case Study Grade B Office Conversion

Condo-Hotel

CB Richard Ellis | Page 37

Condo-Hotel

Condo hotels are usually high-rise condominium buildings operated as hotel property.

Hotel facilities such as swimming pools, restaurants or bars, Spa and business centers are included in the upscale/luxury complex but not necessarily in lower categories.

Parties involved are typically developer, operators and unit owner.

CB Richard Ellis | Page 38

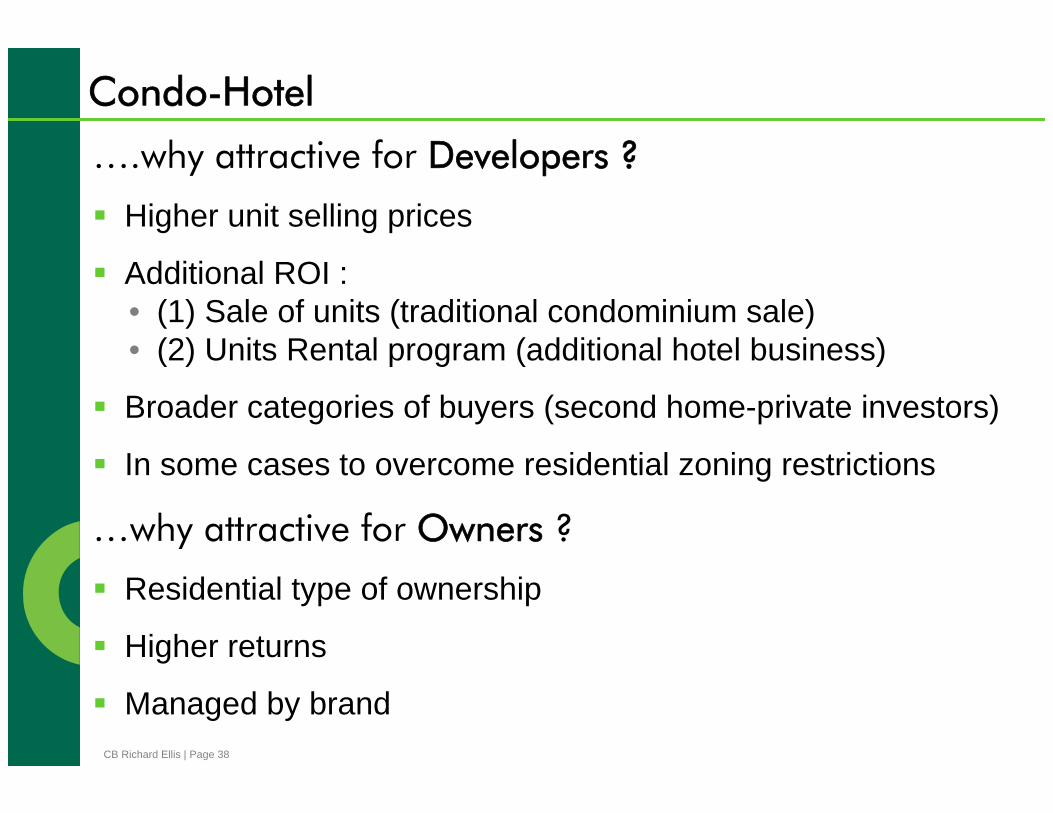

….why attractive for Developers ?

Higher unit selling prices

Additional ROI : • (1) Sale of units (traditional condominium sale)• (2) Units Rental program (additional hotel business)

Broader categories of buyers (second home-private investors)

In some cases to overcome residential zoning restrictions

…why attractive for Owners ?

Residential type of ownership

Higher returns

Managed by brand

Condo-Hotel

CB Richard Ellis | Page 39

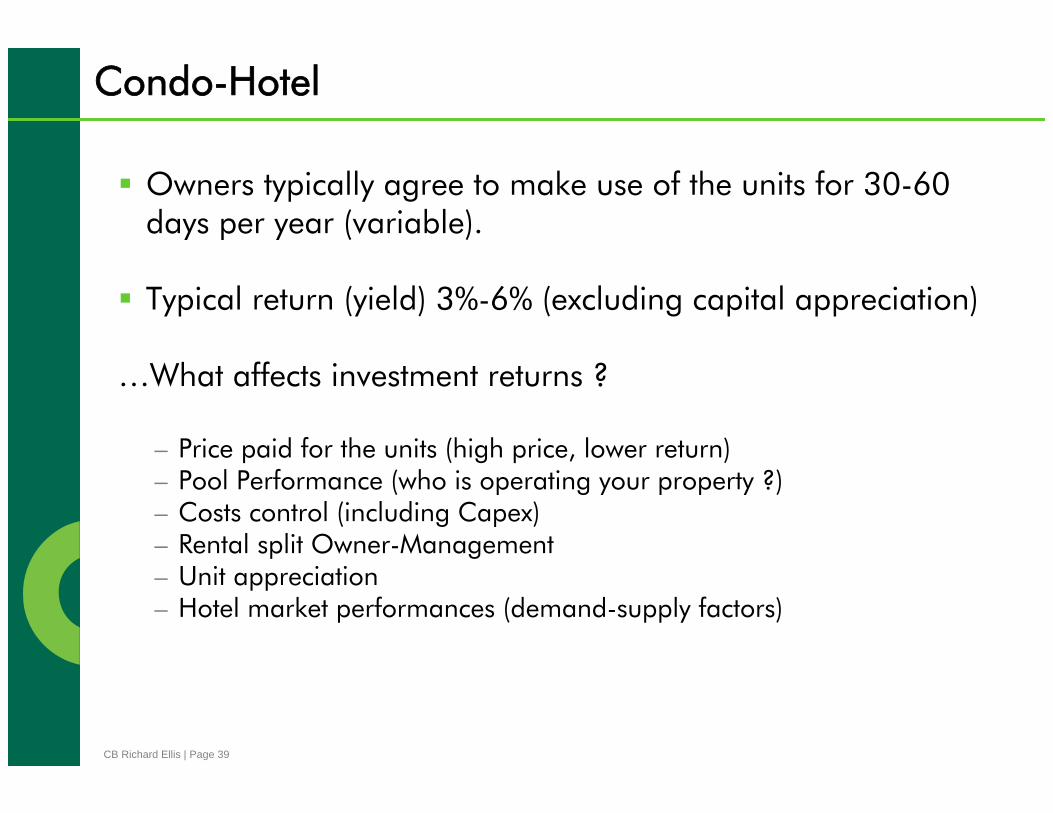

Owners typically agree to make use of the units for 30-60 days per year (variable).

Typical return (yield) 3%-6% (excluding capital appreciation)

…What affects investment returns ?

– Price paid for the units (high price, lower return)– Pool Performance (who is operating your property ?)– Costs control (including Capex)– Rental split Owner-Management – Unit appreciation– Hotel market performances (demand-supply factors)

Condo-Hotel

CB Richard Ellis | Page 40

Condo-Hotel considerations

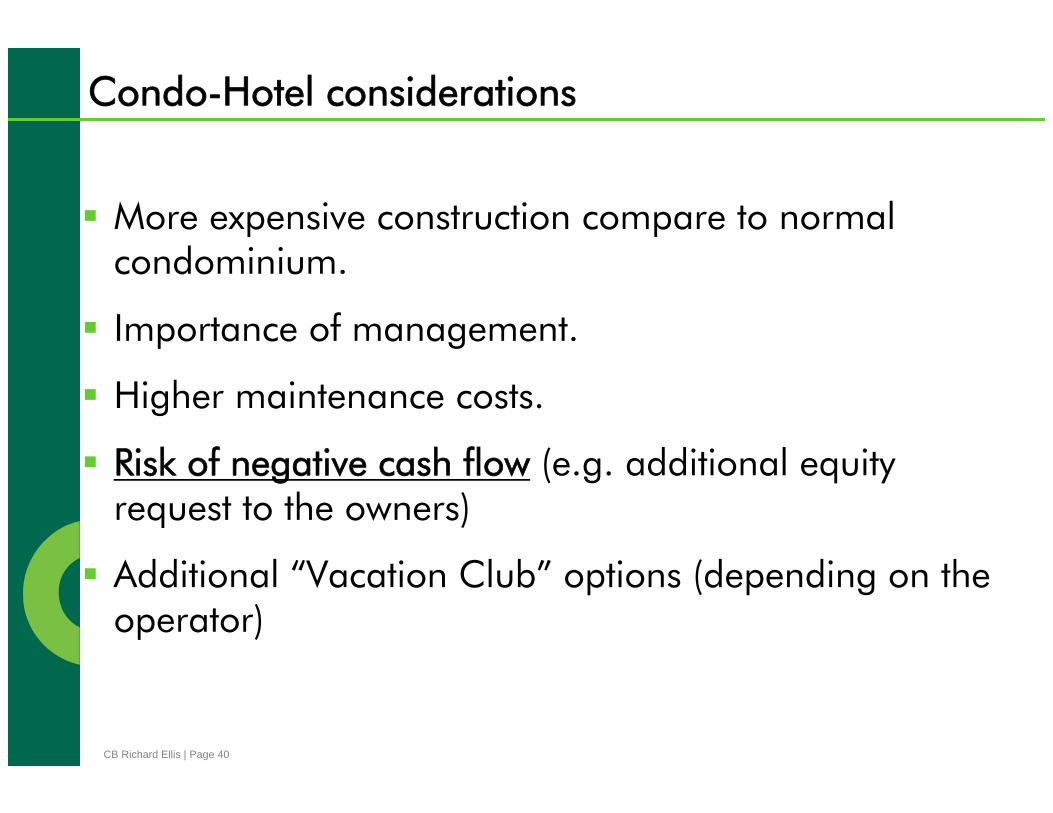

More expensive construction compare to normal condominium.

Importance of management.

Higher maintenance costs.

Risk of negative cash flow (e.g. additional equity request to the owners)

Additional “Vacation Club” options (depending on the operator)

CB Richard Ellis | Page 41

Best Western Nha Trang

Hilton Conrad Condo-Hotel Miami

Condo-Hotel

Mixed-Use complex

CB Richard Ellis | Page 43

Mixed Use Complex

Synergies -Retail-Hotel-Office

More complexity : (co-developers, co-architects, different operators/property managers, different type of clients…)

The projects have to suit each sector

Large scale projects are important for relocation of urban centers and can define the new urban areas.

CB Richard Ellis | Page 44

Benefit in cost sharing

Benefits of cross branding

Competition between facilities

Hotel operators are very defensive on their brand image

Mixed Use Complex considerations

CB Richard Ellis | Page 45

Mixed Use Complexes Asia

Marina Bay Sands Singapore

Park Hyatt Tokyo

Central world

Centara Bangkok

JW Marriot Shanghai

CB Richard Ellis | Page 46

Mixed Use Complexes Vietnam

Windsor Plaza, HCMC

Daewoo Complex HanoiKumho Asiana Plaza

Economy and Budget hotels

CB Richard Ellis | Page 48

Economy and Budget hotels

In developed markets the key issue is pricing strategy

In emerging markets the key issues are cost control, branding and distribution system, and economies of scale

Only few operators active in Asia in those category : – Economy Holiday Inn (IHG)-Ibis (Accor)-– Budget Tune Hotels-Formula 1(Accor)

Key Success Factors : – Rooms and facilities standardization– Land Price/Construction Costs– Economies of scale achievable– Operational Costs( high cost efficiency)– Design (high space efficiency)

CB Richard Ellis | Page 49

Economy and Budget hotelsHome Inn China

Home Inn is a leading economy hotel chain in China

From 10 hotels in 2003 to 616 in 2010.. Target 1000 hotels…

Two models : • Lease the building (390 hotels), typical building lease 15 years• Franchise the brand to hotel owners (226 hotels), typical Franchise concession 8 years

(69 hotels under construction)• Typical hotel 80-160 rooms

Performances (2009)• Average occupancy 91% • Average daily rate $25• Cumulative revenue $380MilSource : MorningStar Document Research

CB Richard Ellis | Page 50

Tune Hotels Typical rooms (economy)

1 Bed (of course…. )(107 x 190 x 24cm)

1 En-suite shower/bathroom

Hot water

One pillow, pillowcase, bed sheet

Toilet roll

1 power socket on the wallSource Tune Hotels website

Economy and Budget hotelsTune Hotels

Standardized rooms is a key success factor

Villa Projects

CB Richard Ellis | Page 52

Villa/Resort projects

A “villa” is a common term referring to landed properties, often a one or two-storey structure built on a private ground.

Banyan tree villas, Phuket

Alila villa, Bali

Shangri-La , Maldives

CB Richard Ellis | Page 53

Villa/Resort projectsType of Villas :

• Semi-detached Houses & Townhouses• Luxury Villas• Prime Location Luxury Villas• Branded Hotel Villas

Purchasing options• Re-sale villas• Completed villas• Off-plan villas• Investment Villas

Other considerations :• Rental guarantee offers ? Typically in the market 3%-6%

for 1-6 years• Off-plan villa importance of reputable developer

Songsaa Island Resort, Cambodia

CB Richard Ellis | Page 54

Hotel Performances

Hotel Investors

New Developments

Investment Strategies

Condo-Hotel

Mixed Use Hotel

Economy/Budget Sector

Villa-Resort

SUMMARY

CB Richard Ellis | Page 55

CBRE Vietnam Hotel Services

• Brokerage

• Operator Selection

• Operator Finding

• Management Contract Negotiation

• Investment Advisory

• Valuation

• Development Consultancy

• Market Research

CB Richard Ellis | Page 56

Mauro Gasparotti

Hotel Services - CBRE Vietnam

M 84 903 028 722

Email: [email protected]

©2010 CB Richard Ellis (Vietnam) Co., Ltd.

Robert McIntosh

Executive Director - CBRE Hotels Asia Pacific

M 65 8123 0208

Email: [email protected]

KEY CONTACTS

Thank you

Pham Thanh Duong

Valuation & Advisory Service - HCMC

M 84 983 426 175

Email: [email protected]

Tran Thi To Thanh

Research and Consulting Hanoi

M 84 912 360 263

Email: [email protected]