Hong Kong Mortgage Default Model - NYUpages.stern.nyu.edu/~igiddy/ABS/hkmortgage.pdfHong Kong...

12

Hong Kong Mortgage Default Model Hong Kong New York Sovereign Chris Chau Jill M. Zelter C. Mia Koo Gabriel Torres 852 2522-9581 (212) 908-0774 (212) 908-0651 (212) 908-0705 [email protected] [email protected] [email protected] [email protected] Summary Fitch IBCA has developed a new model for evaluating credit loss levels on securities backed by Hong Kong Special Administrative Region (HKSAR) residential mortgage loans (MBS). The model, developed from an analysis of approximately 20 years of historical residential home market value data, calculates credit enhancement requirements to support ratings on investment-grade classes of MBS. The past 20 years of data include several stressful periods in Hong Kong, such as the 1989 Tiananmen Square student protest and the 1994–1995 rise in domestic interest rates of the People’s Republic of China (PRC). The model incorporates a loan-by-loan analysis that takes into account the characteristics of each individual property, borrower, and loan. To determine rating guidelines that reflect the unique characteristics of mortgages and lending practices in the Hong Kong market, Fitch IBCA conducted a study of the residential mortgage market. The study included an examination of the residential mortgage portfolio from several leading originators of Hong Kong residen- tial mortgages. In addition, Fitch IBCA analysed data and research obtained from the Rating and Valuation Department of the HKSAR government (HKRV), Cen- sus and Statistics Department of the HKSAR govern- ment (HKCS), and the Hong Kong Monetary Authority (HKMA). Fitch IBCA’s Hong Kong mortgage default model cal- culates credit losses for MBS based on the probability of borrower default and loss severity. The model fo- cuses on the interaction of three factors that serve as the primary determinants of default: ➢ The financial resilience of a borrower as evidenced by the debt-to-income ratio (DTI). ➢ Effects of an unexpected downturn in the borrower’s financial standing, such as unemployment or divorce. ➢ The amount of equity the borrower has invested in the home (or loan-to-value ratio [LTV]). Structured Finance International Special Report www.fitchibca.com 11 June 1998 Collateral Information Checklist Loan Attributes ❑ Loan balances (current and original). ❑ Property appraisals (original and current). ❑ Origination and paid-through date. ❑ Loan type (fixed versus variable tenor). ❑ Loan term (original, remaining, and sea- soning). ❑ Loan purpose. ❑ Loan status (if in arrears, number of months and balance). Borrower Attributes ❑ Profile (e.g. first-time homebuyer). ❑ Status (e.g. self-employed). ❑ Debt-to-income ratio (original and cur- rent). Housing Attributes ❑ Class type (A, B, C, D, or E). ❑ Home type. ❑ Owner-occupied or investment property. ❑ Regional dispersion. ❑ Duration of lease. ❑ Age of property. Pool Concentration ❑ Geographic location (by region). ❑ Building, development, and insurance provider.

Transcript of Hong Kong Mortgage Default Model - NYUpages.stern.nyu.edu/~igiddy/ABS/hkmortgage.pdfHong Kong...

Hong Kong Mortgage Default ModelHong Kong New York SovereignChris Chau Jill M. Zelter C. Mia Koo Gabriel Torres852 2522-9581 (212) 908-0774 (212) 908-0651 (212) [email protected] [email protected] [email protected] [email protected]

SummaryFitch IBCA has developed a new model for evaluatingcredit loss levels on securities backed by Hong KongSpecial Administrative Region (HKSAR) residential

mortgage loans (MBS). The model, developed from ananalysis of approximately 20 years of historical residentialhome market value data, calculates credit enhancementrequirements to support ratings on investment-gradeclasses of MBS. The past 20 years of data includeseveral stressful periods in Hong Kong, such as the 1989Tiananmen Square student protest and the 1994–1995rise in domestic interest rates of the People’s Republicof China (PRC). The model incorporates a loan-by-loananalysis that takes into account the characteristics ofeach individual property, borrower, and loan.

To determine rating guidelines that reflect the uniquecharacteristics of mortgages and lending practices in theHong Kong market, Fitch IBCA conducted a study ofthe residential mortgage market. The study includedan examination of the residential mortgage portfoliofrom several leading originators of Hong Kong residen-tial mortgages. In addition, Fitch IBCA analysed dataand research obtained from the Rating and ValuationDepartment of the HKSAR government (HKRV), Cen-sus and Statistics Department of the HKSAR govern-ment (HKCS), and the Hong Kong Monetary Authority(HKMA).

Fitch IBCA’s Hong Kong mortgage default model cal-culates credit losses for MBS based on the probabilityof borrower default and loss severity. The model fo-cuses on the interaction of three factors that serve as theprimary determinants of default:➢ The financial resilience of a borrower as evidenced

by the debt-to-income ratio (DTI).➢ Effects of an unexpected downturn in the borrower’s

financial standing, such as unemployment or divorce.➢ The amount of equity the borrower has invested in

the home (or loan-to-value ratio [LTV]).

Structured Finance

International Special Report

www.fitchibca.com

11 June 1998

Collateral Information Checklist

Loan Attributes❑ Loan balances (current and original).❑ Property appraisals (original and current).❑ Origination and paid-through date.❑ Loan type (fixed versus variable tenor).❑ Loan term (original, remaining, and sea-

soning).❑ Loan purpose.❑ Loan status (if in arrears, number of

months and balance).

Borrower Attributes❑ Profile (e.g. first-time homebuyer).❑ Status (e.g. self-employed).❑ Debt-to-income ratio (original and cur-

rent).

Housing Attributes❑ Class type (A, B, C, D, or E).❑ Home type.❑ Owner-occupied or investment property.❑ Regional dispersion.❑ Duration of lease.❑ Age of property.

Pool Concentration❑ Geographic location (by region).❑ Building, development, and insurance

provider.

Loss severity is determined by consid-ering regional market value trends, thecosts involved once a borrower has de-faulted (carrying costs and legal ex-penses, among others), and LTV. FitchIBCA’s market value assumptions arebased not only on traditional determi-nants but also on historical home pricevolatility by region, home classification(class A, B, C, D, or E), and projectedsteady sustainable growth. The estima-tion of costs used in Fitch IBCA’smodel are representative of actual costdata supplied to Fitch IBCA by HongKong residential mortgage originators.

Sovereign CeilingFitch IBCA rates the HKSAR’s foreigncurrency obligations ‘A+’ and local cur-rency obligations ‘AA+’, reflecting theregion’s extremely solid fiscal andmacroeconomic position while ac-knowledging the political uncertaintiesresulting from its return to Chinesesovereignty (see Fitch IBCA 1998 Re-search on “Hong Kong Special Administra-tive Region”).

Country risk can enter the ratings equa-tion in several ways. The general eco-nomic and business environment, whichcan determine underlying creditworthi-

ness, is directly affected by governmentmacroeconomic polices. In addition,changes in relevant legislation may affectan issuer’s debt-paying capacity.

More importantly, country risk affectsratings by limiting them to the “sover-eign ceiling.” The government’s for-eign currency rating normally acts as aceiling for resident issuers, since thereis ample empirical evidence that coun-tries, when in a default situation, haveimposed exchange controls and othermeasures that precluded otherwisecreditworthy issuers from servicingtheir foreign currency debt. The localcurrency rating, on the other hand, isnot usually a cap, as governments havefew incentives to limit access to theirown currency. Fitch IBCA will rate HongKong dollar transactions as high as ‘AAA’given the appropriate structure.

Breaching the foreign currency ceilingrequires structural provisions that iso-late relevant cash flows from any gov-ernment interventions. These include,but are not limited to, offshore reserveaccounts, currency swaps, and alterna-tive mechanisms to access foreign cur-rency. Offshore reserve accounts willallow a deal to continue to be serviced

even in the event of foreign exchangecontrols. Currency swaps, if set up cor-rectly, can take care of transfer and con-vertibility risk by having an appropriatelyrated swap counterparty pay foreigncurrency abroad as long as Hong Kongdollars are paid in a local account. Whenassessing different factors that can di-minish sovereign risk, even if no singlefactor by itself is enough to eliminate it,Fitch IBCA takes a probability ap-proach combining all relevant aspects.This process allows for two or moremitigating factors to be used to breachthe foreign currency ceiling, even ifnone of them by itself would beenough. Fitch IBCA utilised this ap-proach to rate an Argentine mortgage-backed securities deal two notchesabove Argentina’s sovereign rating (seeFitch IBCA Research on “BHN III MortgageTrust, Series 1997-2,” dated Nov. 3, 1997).

Hong Kong Mortgage MarketThe individual characteristics of theHong Kong economy and legal system,as well as those of the Hong Kong mort-gage market, played an important rolein the development of Fitch IBCA’smortgage model and the assumptionsbehind it, as each factor influences bor-rower, loan, and property behaviour.

Comparison of the 1994 and 1997 Hong Kong Monetary Authority Survey FindingsSeptember 1994 September 1997

Average Outstanding Amount (HK$ Mil.) 0.8 1.3Outstanding Loan-to-Value Ratio (%)* 53.3 52.0Properties < 10 Years Old 68.2 56.4Contractual Life (Months) 183 221Seasoning (Months) 23 19Remaining Contractual Life (Months) 160 202Owner Occupied (%) 97.0 92.9Interest Payment Method (%) Floating-Rate 96.0 92.0 Fixed-Rate — 0.1 Staff Mortgages/Hybrid Interest Rates — 7.9Spread of Floating-Rate Mortgages over BLR (bps)** 129 (Average) 59 (Average)Delinquency Ratio (%) > 60 Days 0.43 0.20 > 90 Days 0.13 0.10

*Valuation refers to appraisal value at origination or refinancing. **Hong Kong Prime rate. BLR – Best lending rate.

Hong Kong Mortgage Default Model

2 Fitch IBCA, Inc.

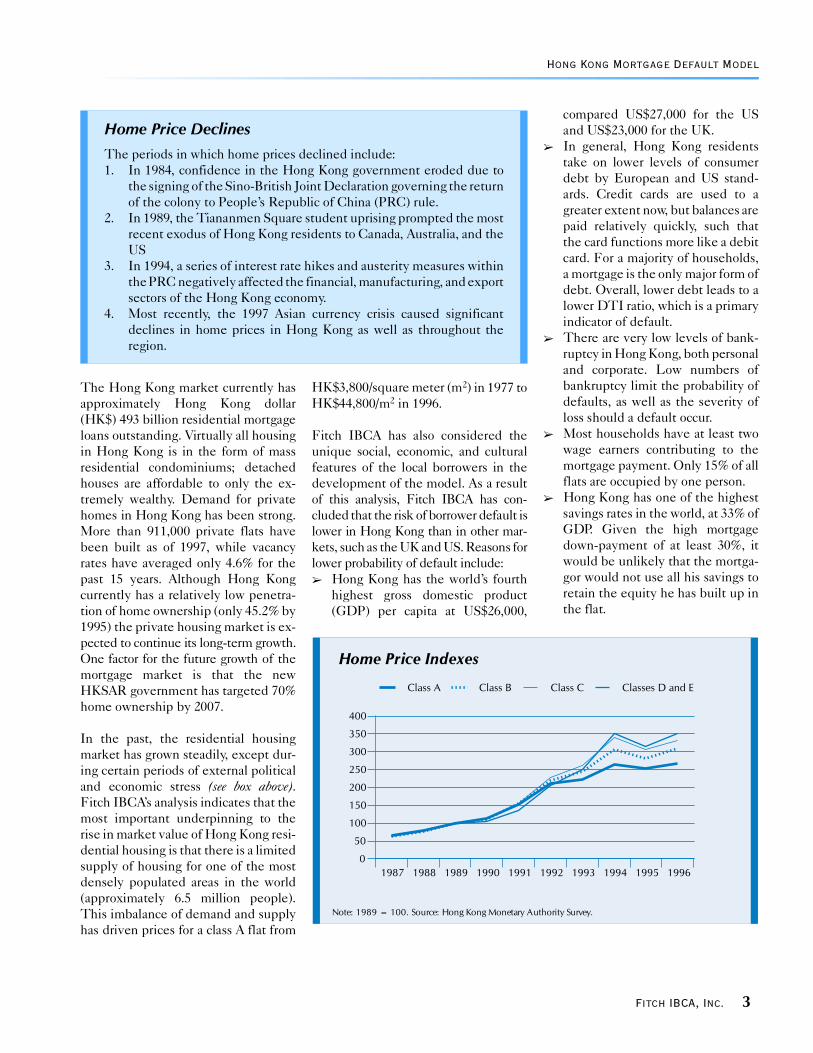

The Hong Kong market currently hasapproximately Hong Kong dollar(HK$) 493 billion residential mortgageloans outstanding. Virtually all housingin Hong Kong is in the form of massresidential condominiums; detachedhouses are affordable to only the ex-tremely wealthy. Demand for privatehomes in Hong Kong has been strong.More than 911,000 private flats havebeen built as of 1997, while vacancyrates have averaged only 4.6% for thepast 15 years. Although Hong Kongcurrently has a relatively low penetra-tion of home ownership (only 45.2% by1995) the private housing market is ex-pected to continue its long-term growth.One factor for the future growth of themortgage market is that the newHKSAR government has targeted 70%home ownership by 2007.

In the past, the residential housingmarket has grown steadily, except dur-ing certain periods of external politicaland economic stress (see box above).Fitch IBCA’s analysis indicates that themost important underpinning to therise in market value of Hong Kong resi-dential housing is that there is a limitedsupply of housing for one of the mostdensely populated areas in the world(approximately 6.5 million people).This imbalance of demand and supplyhas driven prices for a class A flat from

HK$3,800/square meter (m2) in 1977 toHK$44,800/m2 in 1996.

Fitch IBCA has also considered theunique social, economic, and culturalfeatures of the local borrowers in thedevelopment of the model. As a resultof this analysis, Fitch IBCA has con-cluded that the risk of borrower default islower in Hong Kong than in other mar-kets, such as the UK and US. Reasons forlower probability of default include:➢ Hong Kong has the world’s fourth

highest gross domestic product(GDP) per capita at US$26,000,

compared US$27,000 for the USand US$23,000 for the UK.

➢ In general, Hong Kong residentstake on lower levels of consumerdebt by European and US stand-ards. Credit cards are used to agreater extent now, but balances arepaid relatively quickly, such thatthe card functions more like a debitcard. For a majority of households,a mortgage is the only major form ofdebt. Overall, lower debt leads to alower DTI ratio, which is a primaryindicator of default.

➢ There are very low levels of bank-ruptcy in Hong Kong, both personaland corporate. Low numbers ofbankruptcy limit the probability ofdefaults, as well as the severity ofloss should a default occur.

➢ Most households have at least twowage earners contributing to themortgage payment. Only 15% of allflats are occupied by one person.

➢ Hong Kong has one of the highestsavings rates in the world, at 33% ofGDP. Given the high mortgagedown-payment of at least 30%, itwould be unlikely that the mortga-gor would not use all his savings toretain the equity he has built up inthe flat.

Home Price Declines

The periods in which home prices declined include:1. In 1984, confidence in the Hong Kong government eroded due to

the signing of the Sino-British Joint Declaration governing the returnof the colony to People’s Republic of China (PRC) rule.

2. In 1989, the Tiananmen Square student uprising prompted the mostrecent exodus of Hong Kong residents to Canada, Australia, and theUS

3. In 1994, a series of interest rate hikes and austerity measures withinthe PRC negatively affected the financial, manufacturing, and exportsectors of the Hong Kong economy.

4. Most recently, the 1997 Asian currency crisis caused significantdeclines in home prices in Hong Kong as well as throughout theregion.

Hong Kong Mortgage Default Model

Fitch IBCA, Inc. 3

➢ As a result of Chinese cultural influ-ence, a significant social status isattached to home ownership inHong Kong. Property is also seen asthe principal source of long-terminvestment for many Hong Kongresidents.

➢ The divorce rate in Hong Kong,like the rest of Asia, continues to below. Only 1.3% of the total popula-tion is divorced. Divorce is typicallyone of the primary causes of bor-rower default.

➢ Unemployment is extremely low inHong Kong, averaging only 2.58%for the past 15 years. This is a func-tion of free market economics, asopposed to “lifetime employment”found in other Asian economies.Hong Kong has very little in the

form of government-sponsored so-cial subsidies.

➢ Hong Kong has a free market-orientedtax structure, whereby the maximumpersonal income tax rate is 15%. Only2% of Hong Kong residents have topay this maximum level. Capitalgains on stock and real estate trans-actions are not taxed. Additionally,to promote home ownership, amortgage interest deduction ofHK$100,000 is allowed. This taxstructure results in higher dispos-able income for savings and debtservicing.

Fitch IBCA has reflected the lowerlikelihood of borrower default in its de-fault probability matrix as shown in thetable below.

Guidelines and ModelDevelopment

Model ApproachTo determine loss coverage for residen-tial MBS, Fitch IBCA’s Hong Kong de-fault model employs a loan-by-loanreview, examining numerous loan-,borrower-, and property-specific factorsthat influence default probability andloss severity. Fitch IBCA’s base defaultprobability analysis focuses primarilyon the borrower’s DTI ratio, in con-junction with the loan’s LTV. Theseexpected default rates then are ad-justed further by loan, borrower, andproperty attributes.

A large component of Fitch IBCA’s re-covery value analysis is market valuetrends. (Recovery value is the inverseof loss severity.) Fitch IBCA’s marketvalue assumptions focus on historicaldeclines, regional volatility, and sustain-able growth. The base market value pro-jections then are adjusted by loan andproperty attributes, including propertysize and ownership status. Fitch IBCA’sHong Kong mortgage default modelcan be characterised as a worst-case,loss-driven model, which calculates in-vestment-grade credit enhancementrequirements for residential mortgagesecuritisations.

Default Probability

Determinants of Default: Fitch IBCAbelieves the primary indicators of de-

‘AAA’ Default Matrix(%)

–––––––––––––––––––– Debt-to-Income Ratio ––––––––––––––––––––Loan-to-Value Ratio Class 1 Class 2 Class 3 Class 4 Class 5 Debt-to-Income Ratio

≤ 30 6 7 7 8 9 Class 1 > 20.0030.01–40.00 7 8 9 10 11 Class 2 20.00–29.9940.01–50.00 9 10 11 12 14 Class 3 30.00–39.9950.01–60.00 10 11 13 14 16 Class 4 40.00–49.9960.01–65.00 11 12 14 15 17 Class 5 ≥ 50.0065.01–70.00 12 13 15 16 18

Hong Kong Mortgage Default Model

4 Fitch IBCA, Inc.

linquency and default are a combina-tion of the following factors:➢ The financial resilience of the bor-

rower, as evidenced by his DTI ratio.➢ The effect of unexpected financial

stress on the borrower, such as un-employment or divorce.

➢ The amount of equity invested inthe home (LTV).

Fitch IBCA incorporates the two basictheories of mortgage default in itsmodel, namely the borrower’s abilityand willingness to make monthly pay-ments. A borrower’s ability to pay islargely dictated by his income in rela-tion to his debts — the more income,the better. In Hong Kong, the total

DTI is calculated by dividing totalmonthly debt obligations by monthlygross income. Total monthly debt obli-gations are defined as all financial obli-gations of a borrower with a maturity ofmore than 12 months. DTIs in HongKong are more conservative than DTIsin the US because personal income taxand social security tax in the US aremuch higher. The maximum personaltax rate in the US, including federal,state, and local, can be 36% or greater,while the maximum tax rate in HongKong is 15%. Therefore, by US stand-ards, net income available for debt serv-icing in Hong Kong is greater than whatthe DTI would imply.

Lower DTIs also allow for the greaterabsorption by the borrower of financialshocks. In many countries, unemploy-ment and divorce are the two mostcommon reasons for borrower default.Contributing to the lower probability ofborrower default in the Hong Kongmarket are the very low rates of divorceand unemployment, averaging approxi-mately 1.3% and 2.58%, respectively.Historical Hong Kong unemploymentrates are set out in the chart on page 4.

The equity or willingness-to-pay the-ory states that the borrower’s perceivedequity in the property dominates thedecision to default if the borrower is in

financial distress. Additionally, the eq-uity theory assumes that a large initialdown-payment reflects a borrower ofhigher financial means. Fitch IBCA be-lieves a borrower is more willing to pay ifhe has made a substantial down-paymentat origination, regardless of declines inhome prices that might cause the ero-sion of equity over time. Consequently,lower LTV loans (less than 60%) areexpected to have low default rates. Thecurrent Hong Kong maximum LTV atthe time of origination on a mass residen-tial housing mortgage is 70%, as en-dorsed by the HKMA through guidelinesto authorised lending institutions (AI).According to a survey conducted by theHKMA in 1997, the average HongKong outstanding mortgage has an out-standing LTV of 52%. This is very lowcompared to the US and parts of Europe;low LTVs also limit loss severity.

Fitch IBCA uses all the aforemen-tioned factors in the Hong Kong mort-gage default model to determine basedefault rates, as outlined in the table onpage 4.

Default Probability Adjustments: FitchIBCA adjusts the base default rates ona loan-by-loan basis to account for indi-vidual loan characteristics of the collat-eral across all rating levels. Defaultrates may be adjusted for product type,

Delinquent Loans/Total Outstanding Loans in Hong Kong(%)

Number of Days from Payment Due Date September 1994 Year-End 1995 Year-End 1996 September 1997

31–60 Days N.A. 0.59 0.48 0.040*61–90 Days 0.30 0.20 0.13 0.1091–120 Days 0.05 0.08 0.10 0.04>120 Days 0.08 0.12 0.11 0.06

Loan Delinquency Ratio (Amount of Loans Overdue)> 60 Days 0.43 0.40 0.34 0.20> 90 Days 0.13 0.20 0.21 0.10

Number of Reporting Authorised Institutions 32 29 35 39

*Only 38 authorised institutions have submitted data. N.A. – Not available. Note: The delinquent loans reported as of September 1997 were sea-soned on average 22 months. The average loan-to-value ratio of these loans was 62.8%; the market average was 52.0%. Mortgagee actions (in theform of repossession of the property) generally took place about 12 months after the loans were overdue for one month. In all default cases, the loanamount was fully recovered. Source: Hong Kong Monetary Authority Survey.

Hong Kong Mortgage Default Model

Fitch IBCA, Inc. 5

loan purpose, second home/investmentproperty, arrears status, borrower pro-file, seasoning, age, and underwritingquality.

Product Type: Approximately 92% ofmortgages originated in Hong Kong arefloating rate, 99.9% of which is indexedagainst the prime rate, formerly theBest Lending Rate (see chart, page 5).The prime rate is set and reviewed bythe Hong Kong Bankers’ Associationduring a weekly meeting. Hong Kongmortgage lenders offer floating-ratemortgages with maturities ranging from10-40 years, with the most popular be-ing the 15-year mortgage. Recently, theHKMA has taken steps to increase thepercentage of fixed-rate mortgageloans (pilot program launched duringthe first quarter of 1998); however,there continues to be resistance by theAIs. One of the factors behind the re-sistance is the inability of these entitiesto economically hedge the asset/liabil-ity mismatch of long-term fixed-rateHong Kong dollar loans. There are nointerest rate caps or floors in HongKong mortgages.

Unique to the Hong Kong market is thefeature of fixed tenor versus variabletenor. The fixed tenor structure adjuststhe monthly payment amount when-

ever the prime rate fluctuates, so thatthe mortgage amortises within the setterms of the maturity. The variable-tenor structure keeps the monthly pay-ment amount the same and extends theamortisation schedule to the maximummaturity date, usually 30 years, afterwhich, the monthly payments will ad-just like fixed-tenor mortgages. Notethat the AI has the option to extend thematurity date and not the mortgagor.Approximately 70.9% of all floating-rate mortgages are fixed tenor and29.1% are variable tenor or a combina-tion of the two options.

All mortgages have prepayment penal-ties should mortgagors completely repaythe loan during the first year and someinclude penalties for partial prepaymentsduring the first year. Penalties range fromtwo to five months of interest or 3% of theoriginal loan balance.

Fitch IBCA’s base probabilities of defaulttake into consideration the product typesdescribed earlier and, therefore, no addi-tional adjustment is made for defaultprobability with respect to these loans.To the extent additional product typesare offered and securitised, depending onthe product characteristics, default prob-ability may be adjusted.

Loan Purpose: Most loans advanced inHong Kong are for the purchase ofowner-occupied flats and not for refi-nancing or investment. Refinancingonly accounts for 8.3% of all mortgages(see chart below). Fitch IBCA does notpenalise mortgage loans advanced topurchase a home or those advanced torefinance existing loans. However,Fitch IBCA views mortgage loans ad-vanced to release equity in the home(equity refinance mortgages) as riskybecause the homeowner is essentiallyborrowing back his equity based on thehome’s price appreciation. Because theloan is advanced on the basis of the

Hong Kong Mortgage Default Model

6 Fitch IBCA, Inc.

home’s appreciated value, appraisals onrefinancings are critical to the under-writing process. Fitch IBCA reviewsthe issuer’s appraisal process, as well asall underwriting guidelines, whenmeeting with the originator’s manage-ment. On completion of this review, ifFitch IBCA believes these loans havean increased likelihood of default, thebase default probability will be ad-justed by 10%–25%. For loans ad-vanced to construct homes, Fitch IBCAexpects construction to be completedprior to the loan being included in thepool for securitisation.

Mortgages Up to 90 Days in Arrears:When rating a portfolio combining currentand arrears mortgages, Fitch IBCA in-creases base default rates for mortgages inarrears up to 90 days by 25%–75%.

Second Homes and Investment Prop-erties: While information about mort-gage performance for second homesand investor properties is limited, FitchIBCA assumes that these properties areconsiderably more susceptible to de-fault. Accordingly, Fitch IBCA in-creases base default rates by 10%–25%.

Furthermore, Fitch IBCA’s analysis hasindicated that one of the factors driving

the market value volatility experiencedin the Hong Kong market may be anunreported number of cases where themortgage loans were originated not forowner occupation but for investment.Fitch IBCA’s default model has incor-porated the probability that someowner-occupied flats are leased and fi-nanced for investment purposes, (forinformation on occupancy status in HongKong, see chart at the bottom of page 6).

Borrower Profile: Fitch IBCA believesthat self-employed borrowers have agreater probability of default than borrow-ers who are paid a salary, depending on thenature of their business. Fitch IBCA in-creases default probability on loans to self-employed borrowers by a factor of 30%.

Underwriting Quality: When apply-ing the default probability matrix,Fitch IBCA also considers a lender’sunderwriting guidelines. Fitch IBCAviews a lender favourably if he limitsloan amounts based on borrower in-come and debt and if a thorough bor-rower evaluation is carried out, includingchecks for negative credit information.However, since there are no majorcredit bureaus in Hong Kong, the checksshould include an analysis of employ-

ment statistics, historical performanceon other credit facilities provided bythe lender (including credit cards andpersonal or business loans).

Fitch IBCA’s review and analysis of theoriginator of this process determineswhether Fitch IBCA decreases defaultrates by up to 25% or increases them by0%–200%. The areas of focus for FitchIBCA’s review of an originator and serv-icer are summarised on page 11.

Loss Severity

Components of Loss Severity: It has longbeen recognised in the mortgage indus-try that mortgage performance is affectedby changes in economic conditions.The risk created by serious economicdownturns can be severe. Home pricesand repossession rates can fluctuatedramatically with bank losses escalat-ing if a surge in foreclosure rates coin-cides with a downturn in home prices.Fitch IBCA’s Hong Kong default modelquantifies loss severity (or, conversely,recovery value) using several factors,including market value trends, costs(such as foreclosure and carrying costs),and LTV.

Hong Kong Mortgage Default Model

Fitch IBCA, Inc. 7

To capture true market value movementsfor Hong Kong, Fitch IBCA dividedHong Kong into three regions and,within each region, examined changes inhome price by class from 1977 until thepresent. The three major regions areHong Kong, Kowloon, and New Territo-ries. The four classes of flats (as estab-lished by the HKRV and endorsed by theHKMA for mortgage lending purposes)are A, B, C, and D/E; the classificationindicates the size of the flat (see tableabove). Fitch IBCA focused on the worst-case historical price decline and volatilityto develop base market value decline(MVD) assumptions for the Hong Kongresidential default model. These worse-case regional declines were then stressedincreasingly to formulate MVDs from ‘BBB’to ‘AAA’. The resulting regional declinesare depicted in the table below right andrepresent Fitch IBCA’s base MVD as-sumptions for properties classified as A or B.

Market Value Adjustments: Fitch IBCAadjusts the base market value assump-tions on a loan-by-loan basis to accountfor individual loan characteristics of thecollateral across all rating levels. Mar-ket values may be adjusted for propertysize and ownership status.

High-Value Properties: Homes with rela-tively high market values within a re-gion (those classified as C or D/E) aregenerally subject to higher MVDs in adeteriorating market than homes withaverage or below-average market val-ues due to limited demand for suchproperties. Imprecise pricing informa-tion, caused by the lack of comparablebenchmark homes, also influences the

amount of price volatility during a mar-ket downturn. Fitch IBCA will increasebase MVD assumptions to account forthis increased risk.

Property Ownership: Flat owners usu-ally possess their land on a leaseholdbasis. This ownership status representsa higher credit risk; as the lease ap-proaches expiration, it tends to depreci-ate the value of the leasehold property asa new lease will have to be renogtiated atthe homeowner’s expense. For this rea-son, Fitch IBCA requires that leases ex-pire in a reasonable period of timebeyond the life of the loan (see HongKong Property Law, page 9).

Age: Approximately 56.4% of theproperties in Hong Kong are less than10 years old, approximately 35.7% aremore than 20 years old, and 7.9% areunknown (see chart at the top of page 6).Fitch IBCA may increase loss severityproperties or may require their removalfrom the collateral pool if propertyvalue is limited due to age.

Building and Development Concentra-tion: Many banks have relationshipswith particular property developers,whereby the bank or a consortium ofbanks have exclusive right to providemortgage financing for a particularhousing development. Many housingdevelopments have 15 towers. Eachtower may have 30 plus floors. Depend-ing on the target market, each floor mayhave two to eight flats of various sizes.The more upscale the target market,the larger the apartment and the lowerthe number of flats per floor. FitchIBCA may increase the loss severity if

there are concentrations greater than5% by development and/or building.

Insurance: There are several optionsin obtaining insurance for residentialmortgages, including master, block,and individual policies. Most bankshave a relationship with specific insur-ance companies, whereby such insur-ance companies underwrite the firstyear of coverage, a master policy. Blockpolicies are used when the buildingmanagement company has relation-ships with specific insurance compa-nies and requires all tenants to obtaininsurance from these providers. In anindividual policy, the mortgagor can ap-proach a different insurance providerfor coverage, usually from the bank’slist of authorised insurance companies.According to current market practice,only fire insurance is required. Otherforms of insurance may be requested orprovided, depending on the bank.Fitch IBCA will verify that the insur-ance policy provides coverage for dam-age from fire in an amount at least equalto the mortgage loan and includes a mort-gagee payee clause regarding the distri-bution of payments to the mortgagee.

Fitch IBCA will analyse the concentra-tion of insurance providers within abuilding and development as well asthe claims-paying ability of these insur-ance companies. Fitch IBCA may adjustthe loss severity should the insurance cov-erage prove to be weak or certain legallanguage is not included in the contract.

Foreclosure and Carrying Costs: Whencalculating recovery value, Fitch IBCA’smodel reduces the property valuation

Market Value Declines (%)

Region ’BBB’ ’A’ ’AA’ ’AAA’

Hong Kong 40 45 50 55Kowloon 46 51 56 61New Territories 49 54 59 64

Property ClassificationsClass Size Ranges (m2)

A Up to 39.9B 40.0–69.9C 70.0–99.9D 100.0–159.9E 160.0–279.9

m2 – Square meter.

Hong Kong Mortgage Default Model

8 Fitch IBCA, Inc.

by foreclosure costs and the cost to theadministrator of carrying the loan fromdelinquency through to default. Fore-closure costs include administrative ex-penses of approximately HK$100,000,selling costs of approximately 1% ofmarket value, and legal costs of 4% ofloan balance at the time of possession.This estimate is based on actual costdata supplied to Fitch IBCA and maybe adjusted as costs structures changein the industry.

To calculate carrying costs, Fitch IBCAassumes the borrower does not pay in-terest for 18 months and that the inter-est rate is 15% on all loans during thistime. The 18-month time frame isbased on worst-case estimates obtainedfrom several leading Hong Kong mort-gage originators. The 15% interest rateis based on worst-case historical mort-gage interest rates plus a spread.

Credit EnhancementFitch IBCA calculates credit enhance-ment for each loan in a mortgage poolby multiplying default probability byloss severity. An example of this calcu-lation is set out in the table on page 10.

Liquidity CoverageMBS transactions require liquidity tocover short-term delinquencies as wellas long-term shortfalls. Assumptionsregarding liquidity requirements canvary dramatically because the timing ofdelinquencies and shortfalls is difficultto predict. For this reason, Fitch IBCAuses a worst-case methodology to de-termine the level of liquidity requiredto cover delinquencies and defaultsand takes the weighted average defaultprobability for a given pool of mort-gages as the base indicator. Becauseliquidity coverage is closely related tothe quality and efficiency of mortgageadministration, as well as the quality ofthe collateral, Fitch IBCA tailors the cal-culation of liquidity to the particular dy-namics of each transaction that it rates.

For short-term delinquencies, FitchIBCA assumes that payment will be re-ceived within a maximum of 12 monthsand that interest will accrue during thisperiod at 15%. Fitch IBCA also as-sumes that no more than half of theseloans are likely to become delinquentat any one time, working on the as-sumption that monthly delinquenciesat any given time will represent half thelevel of cumulative defaults.

For long-term payment shortfalls,Fitch IBCA typically assumes that pay-ment will be received within a maxi-mum of 18 months from the point ofdefault and that interest will accrue at15%. Fitch IBCA then adjusts weightedaverage default probability to reflect itsestimation of the number of loans likelyto be in default at any one time.

Operations ReviewA key factor in evaluating and rating apool of mortgage loans is the quality ofthe operations and procedures of the un-derlying mortgage originator/administra-tor. There is a direct correlation betweenthe origination and servicing functionsand the performance of a collateral pool.Fitch IBCA may increase or reduce creditenhancement based on the quality andexperience of the originator and adminis-trator. Underwriting guidelines, apprais-als, and collection procedures are ofparticular importance.

Fitch IBCA reviews the operations ofthe originator/administrator, determin-ing whether the company’s procedures,controls, and performance are accept-able. Interviews, procedural reviews, andloan level analysis are performed, notonly to determine if operations complywith industry and investor guidelines,but to ensure that the proper controls arein place for a given transaction.

Fitch IBCA tailors its review to therequirements of each issuer and inves-tor, as well as the nature of the transac-

tion involved. However, the key aspectsof its approach are summarised in thechecklists on page 11.

Hong Kong Property LawPrior to the transfer of Hong Kong fromthe British Crown to the PRC on July 1,1997, it was the practice of the HongKong government, being the ultimateholder of land, to grant only leaseholdinterests to land purchasers. Since thehandover, it continues to be the casethat all existing government leases willcontinue to be recognised and pro-tected under the laws of the HKSAR.Accordingly, land tenure in Hong Kongcontinues to be leasehold, and ownersof property in Hong Kong are effec-tively long leaseholders.

Most land is sold by the government atpublic auction to the highest bidder,subject to the purchaser paying a pre-mium and government rent and signingcertain terms and conditions of sale,upon which the purchaser is entitled tolease and develop the land. The termsof government leases and sale condi-tions vary. Historically, Crown leases weregranted for periods of 75, 99, or 999 years,with or without the right of renewal. Cur-rently, Crown leases are granted for astandard term of 75 years, with the rightof renewal in Kowloon and Hong Kong.In the New Territories, Crown leaseswere extended (at the time of the han-dover) until June 2047.

Since most sales and purchases andmortgages relate to units within a hous-ing complex, the HKSAR does not is-sue a separate lease for each unit.Instead, each flat is equated with sev-eral undivided shares according to adeed of mutual consent (DMC) thatwill provide for exclusive use and pos-session of the purchased unit. A DMCis binding on all original and futureowners of the flats.

Hong Kong Mortgage Default Model

Fitch IBCA, Inc. 9

The land registration ordinance pro-vides for registration of all instrumentsaffecting land in the relevant land reg-istry. Although the sale conditions mayrequire the registration of all mortgagesand assignments, there is no statutoryrequirement that such documents mustbe registered. Non-registration of anyinstrument that is registerable does notmake such instrument invalid. How-ever, registration insures protection oftitle.

Foreclosure ProcessGenerally, a mortgagee can enforce itssecurity by applying to the court forforeclosure, taking possession of theproperty, exercising its power of sale of

the property, or appointing a receiver tomanage and take control of the prop-erty or its income. A mortgagee mayalso take an action in debt against themortgagor if the mortgagor fails to payor is in breach of any other covenants.

A foreclosure order is made by the courtupon the application of the mortgageeif a mortgagor fails to repay the loan onthe payment date or if there is a breachof any term of the mortgage. A foreclo-sure order extinguishes the mortgagor’spersonal covenant to pay and vests theownership of the property in the mort-gagee. Upon default by the mortgagor,the mortgagee may exercise its powerto take possession of the property. Pos-

session of the mortgaged property canbe obtained by means of a court order.

A power of sale cannot be exerciseduntil notice requiring payment of themortgage has been served on the mort-gagor and the default has lasted for onemonth after service of the notice, interestis in arrears and unpaid for one monthafter the due date, or there has been abreach of other covenants. The mortga-gee, in exercising its power of sale, doesnot require an order of the court to pro-ceed with the sale of the property.

Mortgage actions (in the form of repos-session of the property) generally takeabout 12 months from first delinquency.

Loan-Level Credit Enhancement Calculation

Desired Rating ’AAA’

Property Value (HK$) 2,000,000Region Hong KongLoan Balance (HK$) 1,400,000Loan-to-Value Ratio (%) 70Debt-to-Income Ratio (%) 35Property Purpose Investment

Default Probability Calculation (%)‘AAA’ Base Default Probability 15Investment Property 25Default Probability (DP) 18.75

Loss Severity Calculation (HK$)Loan Balance 1,400,000Property Value 2,000,000Less Market Value Decline (55%) 1,100,000Less Foreclosure Costs 165,000Less Carrying Costs (15% for 18 months) 315,000Equals Recovery Value 420,000Loss Severity: (LS) = (Loan Balance – Recovery Value)/ (Loan Balance) = 70.0% Credit Enhancement Required = DP x LS = 13.3%

*Example assumes no mortgage insurance.

Hong Kong Mortgage Default Model

10 Fitch IBCA, Inc.

Hong Kong Mortgage Default Model

Fitch IBCA, Inc. 11

Copyright © 1998 by Fitch IBCA, Inc., One State Street Plaza, NY, NY 10004 Telephone: New York, 1-800-753-4824, (212) 908-0500, Fax (212) 480-4435; Chicago, IL, 1-800-483-4824, (312) 214-3434, Fax (312) 214-3110;London, 011 44 171 638 3800, Fax 011 44 171 374 0103; San Francisco, CA, 1-800-953-4824, (415) 955-0529, Fax (415) 955-0549Barbara A. Besen, Publisher; John Forde, Editor-in-Chief; Madeline O’Connell, Director, Subscriber Services; Jason H. Kantor, Manager, Publishing Technology;Nicholas T. Tresniowski, Senior Managing Editor; Diane Lupi, Managing Editor; Jennifer Hickey, Andrew Simpson, Editors; Jay Davis, Martin E. Guzman, PaulaSirard, Senior Publishing Specialists; Harvey Aronson, Publishing Specialist; Robert Rivadeneira, Publishing Assistant. Printed by American Direct Mail Co., Inc.NY, NY 10014. Reproduction in whole or in part prohibited except by permission.Fitch IBCA ratings are based on information obtained from issuers, other obligors, underwriters, their experts, and other sources Fitch IBCA believes to be reliable.Fitch IBCA does not audit or verify the truth or accuracy of such information. Ratings may be changed, suspended, or withdrawn as a result of changes in, or theunavailability of, information or for other reasons. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacyof market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. FitchIBCA receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. Such fees generally vary from $1,000 to $750,000 perissue. In certain cases, Fitch IBCA will rate all or a number of issues issued by a particular issuer, or insured or guaranteed by a particular insurer or guarantor,for a single annual fee. Such fees are expected to vary from $10,000 to $1,500,000. The assignment, publication, or dissemination of a rating by Fitch IBCA shallnot constitute a consent by Fitch IBCA to use its name as an expert in connection with any registration statement filed under the federal securities laws. Due tothe relative efficiency of electronic publishing and distribution, Fitch IBCA Research may be available to electronic subscribers up to three days earlier than printsubscribers.

Hong Kong Mortgage Default Model

12 Fitch IBCA, Inc.