HOMESNOW! LEASE TO PURCHASE CASH FLOW INVESTMENT PROGRAM HomesNow Lease Purchase Program is...

61

HOMESNOW! LEASE TO PURCHASE CASH FLOW INVESTMENT PROGRAM HomesNow Lease Purchase Program is Copyrighted by First Horizon Consulting, Inc. Copyrighted 2007

-

Upload

corinne-elliott -

Category

Documents

-

view

218 -

download

0

Transcript of HOMESNOW! LEASE TO PURCHASE CASH FLOW INVESTMENT PROGRAM HomesNow Lease Purchase Program is...

HOMESNOW!LEASE TO PURCHASE

CASH FLOW INVESTMENT PROGRAM

HomesNow Lease Purchase Program is Copyrighted by First Horizon Consulting, Inc. Copyrighted 2007

“Rent a home to a man and he has shelter.

Give a man the option to buy it, and he has direction.”

FIRST HORIZON CONSULTING LEASE TO PURCHASE

INVESTING

Buy, Sell and InvestSafer and Easier

WHAT IS LEASE TO PURCHASE?

“The main idea of the lease purchase contract is to control properties, not own them.”

“Lease Purchase” is known by several other names: “rent-to-own,” “lease option,” and “lease with option to buy.”

Association of Progressive Rental Organizations• rent-to-own business is more than forty years old• generates about $4.4 billion in annual revenues • serves nearly three million customers • indications that revenues will increase in the years to come.

What is a Lease Purchase Contract?

A lease purchase contract combines a basic lease contract with an option-to-purchase contract. The tenant/buyer pays to the landlord/seller a nonrefundable option deposit that is applied to the purchase price of the home.

The tenant/buyer then pays to the landlord/seller rent to compensate the landlord/seller for the tenant/buyer’s use of the property. Rent payments are usually made on a monthly basis. A portion of that monthly payment is often applied to the purchase price and/or the down payment of the home.

During the term of the lease, but before the option expires, the tenant/buyer has exclusive right to buy the home under the terms to which both parties have previously agreed.

Lease Purchase agreements, since they combine the terms of a real estate purchaseagreement with a residential lease, must contain all the required elements for real estate contracts, as well as the following provisions:

1. Option Price: For an option contract to be enforceable, the buyer must pay for the option. The amount paid for the option is not refundable, and is applied to the purchase price of the property if the buyer elects to exercise the option, or is forfeited to the seller if the buyer does not exercise the option to purchase the property.

2. Option Term: The contract should contain a specific date by which the buyer must exercise the option.

3. Buyer’s Credits: If a portion of the rent payments are to be applied to the purchase price of the home, this should be stated clearly in the contract.

4. Method of Exercising the Option: The contract should specify what actions the buyer must take to exercise the option. This is often simply a letter to the seller stating the buyer’s intent to purchase the property.

FEATURES & BENEFITS

INVESTOR

“You miss 100% of the shots you don’t take.”~ Wayne Gretzky ~

• Top Sales Price, Even If Demand Is Low

You attract more tenant/buyers who are willing to pay a premium because of the terms and value you are offering.

Since you are flexible on your terms and are offering value, you can demand a HIGHER THAN USUAL RENT.

• Higher than Usual Rent

• Positive Cash Flow

Since you can demand a higher than usual rent, this will increase your cash flow.

• Non-Refundable Option Consideration Up Front/Minimum Risk

When a tenant/buyer executes (signs) a lease purchase contract, you receive an option deposit that is yours to keep if they default or decide not to buy.

• Realtor Commissions

Since you are selling your home yourself, you will avoid paying a Realtor commission.

• Time to Save for a Good Down Payment

Since the closing is delayed, there is time for your tenant/buyer to save for a good payment.

•Tax Shelter Is Maintained

Since you own the home, you remain on the deed until the option is exercised, therefore, you maintain all of the tax benefits of ownership, i.e. Taxes, Depreciation, Insurance,

• Attraction of the Highest Quality Tenants

You are dealing with tenant/buyers who have a vested interest in the home. So, they think of themselves as a homeowner and tend to take better care of it. (PRIDE OF OWNERSHIP)

• No Maintenance, No Land lording

Tenants/Buyers have a vested interest and believe they are homeowners feeling a “pride in ownership” that encourages them to pay on time, perform maintenance and make improvements to your home. Additionally, you may delegate maintenance to the tenant in your agreement.

• Market of Buyers

You are marketing your home not only to buyers, but also to renters and investors.

These three groups make up 95% of those seeking to acquire real estate.

• No Long Vacancies

Your phone will ring off the hook when you advertise that your home offers a lease purchase opportunity. Typical turnover time is days or weeks rather than months.

• Peace of Mind

It is safer than conventional rentals because of the quality of the tenant/buyers and their vested interest in your home. It also means that someone is living onsite who will watch and guard your investment against vandalism, fire, etc.

“Success is the sum of small efforts,repeated day in and day out.”~ Robert Collier ~

FEATURES & BENEFITS

RENTER/BUYER

• Faster Equity Growth

Equity can accumulate much faster than with conventional financing

• Sales Price Is Locked In

The sales price will be stated in the lease purchase agreement.

• Closing Costs Are Delayed

Closing costs will be delayed (not avoided) until BUYER actually close on the home. • Profits from Appreciation

Since the sales price is locked in before closing, any increase in property value will mean that your equity is increasing in the home.

• Minimum Cash Out of Pocket

When you purchase a home conventionally, you must pay closing costs, pre-paids and a down payment. With a lease purchase contract, you pay only first month’s rent and an option deposit. This will save you between 25% and 85%.

• Rent Money is Working Towards the Purchase of the Home

Each month that you pay rent, a portion of that payment will be credited towards your down payment or off of the sales price

• Option Consideration Is Credited Towards the Purchase of the Home

When tenant/Buyer executes (signs) a lease purchase contract, they must pay the landlord/seller an option deposit. This money is their vested interest in the home and will be fully credited (100%) to either the down payment or the sales price.

• Problems Will Not Hold You Back

Qualification restrictions are not as strict as conventional financing. Tenant/Buyer will be approved at the sole discretion of the landlord/seller.

Profits from Appreciation

Since the sales price is locked in beforeclosing, any increase in property valuewill mean that the Tenant/Buyer’s equity is increasing in the home.

Buying PowerTenant/Buyer’s buying power is drasticallyincreased. They can get into a leasepurchase home for as little as $5,000.Compare that to a lender who requires 5- 20% down plus closing costs and Pre-paids.

No Taxes, Less Liability

Since Tenant/Buyer does not own the homeyet, they will not have to pay property taxesAnd their liability exposure will be drastically reduced.

Privacy

Since Tenant/Buyer is leasing, there will be no public record of where they live.

Maximum Leverage

Tenant/Buyer is spending very little money to control a very expensive and potentially veryprofitable investment.

TimeBefore Tenant/Buyer actually buys the home,they will have time to repair their credit andfind the best financing available.

*We will assist you with credit repair at no cost.

No Lengthy Escrows or Mortgage Approvals

The decision to lease purchase to will be made

at the sole discretion of a landlord/seller rather than by a lender who can take up to a month (or longer) to render a decision.

Peace of Mind

As long as the Tenant/Buyer lives up to the contract, they will have full control of thehome and can maintain it or improve it as

theywish (improvements will require the permission of the landlord/seller).

LANDLORD/SELLERIf it looks like a sale and acts like a sale, it’s probably a sale. In the unfortunate event that you need to

evicta tenant/buyer, he or she could go kicking andscreaming to court claiming “equitable title.” If aCourt rules in favor of the tenant/buyer on these grounds, as the landlord/seller you will have to foreclose on the person. Why? Because in the eyes ofthe court, you are actually selling your home.

Managing the Risks

This is the best way to close a deal with a tenant/buyer and greatly reduce the risk of “Equitable Title”• Use a separate lease agreement in conjunction with an option to purchase agreement. • Do not refer to the option to buy agreement in your lease agreement.• Treat any tenant/buyer the same as you would treat any normal tenant.• Never use the terms “credit,” “seller,” or “buyer” in your lease contracts.

• Always get a security deposit. Sellers don’t take security deposits, landlords do.• Do not give your tenant/buyer more than a one-year lease term. Give a one-year lease with rights to renew. Draft a new Lease• Pay the taxes and insurance. Tenants don’t pay taxes and insurance, landlords do.

• Do not give monthly rent credits at all. Instead have the tenant/buyer pay a monthly option consideration in addition to the rent.• Keep in mind that all written evidence and conversations are admissible to court, and the court will judge you on your intent to sell or not sell.• You do not want your tenant/buyer to record the option in the public real estate records until it is a sale, because in the eyes of the court, it will look like a sale.

Why Lease/Purchase Buyers Buy• The lack of a down payment• Credit problems• Not being able to qualify for a mortgage• Needing more time

“Do what you love, love what you do,and deliver more than you promised.” ~ Harvey MacKay ~

As the landlord/seller, the two

major concerns that you will face

are:

1. Collecting rent on time.

2. Destruction of your property.

Minimize Your RiskThese risks can be reduced greatly with a little research:1. Have the tenant/buyer fill out a detailed rental application.2. Check the tenant/buyer’s credit history. 3. Make an unannounced visit to the tenant/buyer at their current residence to see how well they maintain it. What you see there is what you will see at your home.

4. Call previous landlords to verify payment history, quality of tenants, etc. 5. Verify the tenant/buyer’s employment.6. Ask for many references and check them.7. Get a large option deposit to create value in the home for the tenant/buyer.8. Make the tenant/buyer responsible for the maintenance.

Tips and Recommendations

1.Encourage tenant/buyers to allow automatic transfer from their account to yours.

2. Coincide rent due dates with tenant/buyer’s paydays.

3. Send your tenant/buyer a holiday, birthday, or better yet, a Thanksgiving card. How often do you receive Thanksgiving cards? They will definitely remember it.

4. To encourage them to actually become homeowners, send them a monthly statement that shows their current amount due, due date, late payment fees and any notes you want to include. Tenant/Buyers who think like homebuyers act in the following:• They take better care of your home.• They pay rent on time and fulfill other obligations.• They handle repairs and other maintenance items.• They improve or upgrade your home.

5. When signing a lease, give the tenant/buyer twelve labels pre-printed with your address. All they need to do is peel off one each month, place it on the envelope with a stamp and mail it.

6. To encourage timely rental payments, attach an addendum to the option to buy stating that the tenant/buyer will receive an option consideration bonus (maybe $1,500) if they make all of their monthly rental payments in a timely fashion. If they don’t make their payments on time, declare the option consideration bonus void by sending a written statement to that effect.

7. In the first month, welcome the tenant/buyer as a “future home buyer” and use that term in both oral and written communications (Note: This would strengthen the tenant/buyer’s defense of equitable title

8. Send an “on-time thank you voucher”, valued at either $25 or $50 good toward the purchase of the home. If they are ever late, any vouchers received up to that point are considered null and void (Note: this would strengthen the tenant/buyer’s defense of equitable title

9. While lease purchasing a home to a tenant/buyer, it would be to your benefit to give them a periodical check-up to see what progress they are making towards purchasing your home. You want them to be ready to buy when the time comes.

“The reason a lot of people do not recognize opportunity is because it usually goes around wearing overalls looking like hard work.” ~ Thomas A. Edison ~

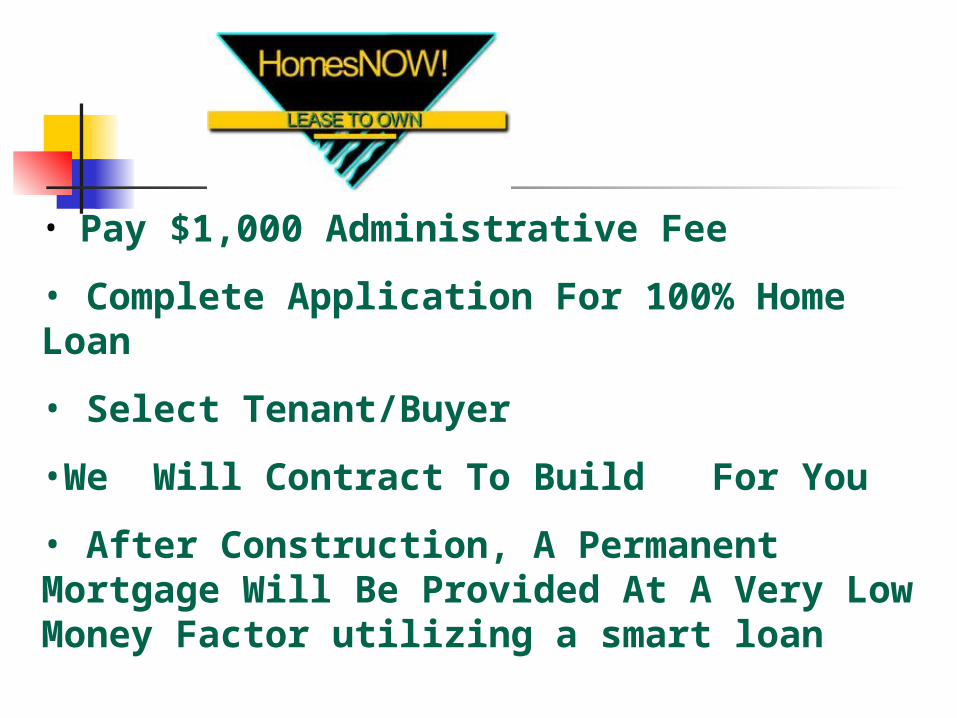

HOW DO I INVEST IN A PROJECT?

• Pay $1,000 Administrative Fee

• Complete Application For 100% Home Loan

• Select Tenant/Buyer

•We Will Contract To Build For You

• After Construction, A Permanent Mortgage Will Be Provided At A Very Low Money Factor utilizing a smart loan

THE INVESTMENT ANALYSIS

INVESTOR/LANDLORD

THE INVESTMENT ANALYSIS

TENANT/BUYER

THE LEASE

THE OPTION TO PURCHASE

IRA BUSINESS SYSTEM

IRA BUSINESS SYSTEM

This entity structure is a robust redesign and upgrade from the IRA Wealth System that allows an even greater level of tax minimization and wealth building. With it, you will be able to operate a business that might be investing in real estate, tax liens, or trust deeds, directly from your IRA funds, WITHOUT penalities.

IRA BUSINESS SYSTEM

Here are just some of the benefits Significant asset protection Checkbook Control Over Your Money! Fully self-directed for total flexibility. Complete access to your retirement funds in a

tax-free environment for investment purposes. This structure provides the ability to realize unlimited wealth growth.

A complete business can operate inside of this entity!

Group coaching for the utilization of the system