Homeowners Friendly Society Group annual report & … report & accounts ... strategic marketing...

49

annual report & accounts for the year ended 31 December 2005 Homeowners Friendly Society Group

-

Upload

nguyenduong -

Category

Documents

-

view

212 -

download

0

Transcript of Homeowners Friendly Society Group annual report & … report & accounts ... strategic marketing...

annual report & accountsfor the year ended 31 December 2005

Homeowners Friendly Society Group

society information

2

engage Mutual Assurance is a trading name of Homeowners Friendly Society Limited.

registered officeHornbeam Park Avenue, Harrogate HG2 8XE

telephone: 01423 855 000

e-mail: [email protected]

websites: www.engagemutual.com

www.theukgroup.com

Registered and Incorporated under the

Friendly Societies Act 1992

Registered No: 964F

Authorised and regulated by the

Financial Services Authority

board of directorsRaymond F Pierce BA FRSA

David G Hargrave BCom MSc FIA

Andrew S Haigh BSc

Kevin D Chidwick BSc FCCA MBA

(resigned 26 August 2005)

Rt. Hon. Lord Clark of Windermere BA MSc PhD

Penelope J Hemming

W Graham Henderson B Comm CA FRSA

(appointed 23 February 2006)

C Christopher F Lazenby BSc(Eng) CEng MBCS

Peter W Mason BSc Hons. FIA

(appointed 9 December 2005)

Christina M McComb BA Hons. MBA

(appointed 11 May 2005)

Gordon A Murison MBE (retired 12 May 2005)

secretary

Andrew J Horsley MSI FCIS

actuarial function holder

Trevor M Batten FIA

auditors

KPMG Audit Plc

Registered Auditor

solicitors

Addleshaw Goddard

bankers

Barclays Bank Plc

board committeesaudit

Peter W Mason

(appointed as Chairman 1January 2006)

Rt. Hon. Lord Clark of Windermere

David G Hargrave (resigned as Chairman 31 December 2005)

Christina M McComb

finance & risk

David G Hargrave (Chairman)

Trevor M Batten

Graham Henderson

Peter W Mason

nominations

Raymond F Pierce (Chairman)

Andrew S Haigh

David G Hargrave

remuneration

Christina M McComb (appointed as Chairman 9 December 2005)

Rt. Hon. Lord Clark of Windermere

Penelope J Hemming

Raymond F Pierce (resigned as Chairman 9 December 2005)

3

our mission isto enable people to protect their welfare.

We will do this by providing our customers

with accessible, simple, value for money

protection and savings products.

contents

society information 2

mission 3

your board of directors 4 - 5

chairman’s report 6 - 7

chief executive’s business review 8 - 13

directors’ report 14 - 16

corporate governance report 17 - 22

statement of the directors’ responsibilities 23

report of the directors on remuneration 24 - 25

independent auditor’s report 26 - 27

group income and expenditure 28

group balance sheet 29 - 30

society income and expenditure 31

society balance sheet 32 - 33

notes to the accounts 34 - 48

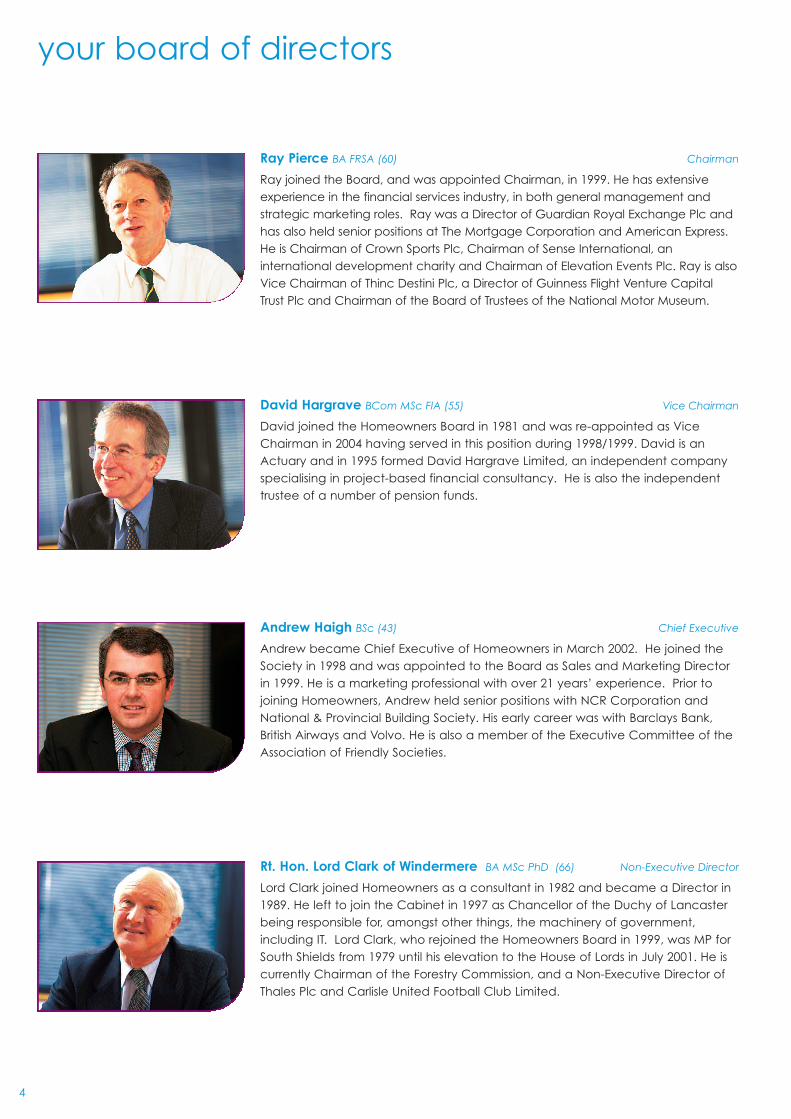

Ray Pierce BA FRSA (60) Chairman

Ray joined the Board, and was appointed Chairman, in 1999. He has extensiveexperience in the financial services industry, in both general management andstrategic marketing roles. Ray was a Director of Guardian Royal Exchange Plc andhas also held senior positions at The Mortgage Corporation and American Express.He is Chairman of Crown Sports Plc, Chairman of Sense International, aninternational development charity and Chairman of Elevation Events Plc. Ray is alsoVice Chairman of Thinc Destini Plc, a Director of Guinness Flight Venture CapitalTrust Plc and Chairman of the Board of Trustees of the National Motor Museum.

your board of directors

David Hargrave BCom MSc FIA (55) Vice Chairman

David joined the Homeowners Board in 1981 and was re-appointed as ViceChairman in 2004 having served in this position during 1998/1999. David is anActuary and in 1995 formed David Hargrave Limited, an independent companyspecialising in project-based financial consultancy. He is also the independenttrustee of a number of pension funds.

Andrew Haigh BSc (43) Chief Executive

Andrew became Chief Executive of Homeowners in March 2002. He joined theSociety in 1998 and was appointed to the Board as Sales and Marketing Directorin 1999. He is a marketing professional with over 21 years’ experience. Prior tojoining Homeowners, Andrew held senior positions with NCR Corporation andNational & Provincial Building Society. His early career was with Barclays Bank,British Airways and Volvo. He is also a member of the Executive Committee of theAssociation of Friendly Societies.

Rt. Hon. Lord Clark of Windermere BA MSc PhD (66) Non-Executive Director

Lord Clark joined Homeowners as a consultant in 1982 and became a Director in1989. He left to join the Cabinet in 1997 as Chancellor of the Duchy of Lancasterbeing responsible for, amongst other things, the machinery of government,including IT. Lord Clark, who rejoined the Homeowners Board in 1999, was MP forSouth Shields from 1979 until his elevation to the House of Lords in July 2001. He iscurrently Chairman of the Forestry Commission, and a Non-Executive Director ofThales Plc and Carlisle United Football Club Limited.

4

Penny Hemming (58) Non-Executive Director

Penny joined the Homeowners Board in October 2004 having served as CBI RegionalDirector for Yorkshire and the Humber since 1995, giving her a wide understanding ofall issues confronting businesses today. She also spent 16 years in the city as astockbroker and currency broker. Penny is a Trustee of Eureka, the Museum forChildren, a member of the Advisory Board of the University of Bradford School ofManagement and was appointed a Deputy Lieutenant of West Yorkshire in 2000.

Graham Henderson B Comm CA FRSA (51) Finance Director

Graham joined the Board in February 2006 as Finance Director. He is a CharteredAccountant with over 20 years’ experience in senior financial roles in financialservices companies. His last role was as Programme Director responsible for theimplementation of new reporting regulations for the life and pensions operations ofAbbey Plc. He has operated as Finance Director and Head of Finance at BritanniaLife and at Royal Life and has extensive experience of change management,corporate finance and business planning.

Chris Lazenby BSc(Eng) CEng MBCS (55) Operations Director

Chris joined Homeowners in August 2003 and was appointed to the Board asOperations Director in January 2004. He has extensive experience of leadingbusiness-wide change having been responsible for projects as diverse asdeveloping strategy, setting up a customer contact centre, cost reduction andmany technology-based initiatives. Chris’s previous roles have included Head ofBusiness Improvement in the mutual sector with Britannia Building Society, IT Directorfor Lunn Poly as well as senior positions at Ladbrokes and Massey Ferguson.

Peter Mason BSc Hons FIA (55) Non-Executive Director

Peter joined the Board in December 2005. He is a Fellow of the Institute of Actuaries withover 30 years’ experience of Financial Services businesses. He is Investment Directorand Actuary at the Neville James Group, an investment management company, andholds Non-Executive Directorships at Countrywide Plc and Chesnara Plc.

Christina McComb BA Hons MBA (49) Non-Executive Director

Christina joined the Board in May 2005. She has extensive experience of investing in anddeveloping smaller companies, including 14 years working at 3i where she wasresponsible for 3i's investment portfolio in London and the South East and latterly 3i's UKtechnology portfolio. She is currently a Director of the Shareholder Executive, adepartment based within the DTI which manages the Government's financial andshareholder interests in a number of public-owned enterprises. Christina is also a Non-Executive Director of Partnerships-UK and a member of the Investors AdvisoryBoard of the London Technology Fund. She is a Governor of Richmond Upon ThamesCollege, a leading tertiary college in south-west London.

5

Of particular importance to manycustomers last year was the continuedrise of the stock market, which resultedin considerable improvement inmaturity values for many unit linkedsavings plans as equities returned tolevels of early 1998. We hope forcontinued growth this year and aconsequent further improvement ininvestment returns.

As well as bringing the welcomeimprovement in stock market growth,2005 also proved to be a verysignificant year in the Society’sdevelopment. After several years ofpreparation and consultation, ChildTrust Funds became a reality and I amdelighted to report that your Societyplayed one of the leading roles in theirsuccess during the year.

We have supported the concept of theChild Trust Fund since it was first raised,and have been keen to approach it ina manner which would be as inclusiveas possible and would encourage moreyoung parents to save regularly. Webelieve we have made good progresstowards this goal as researchundertaken last year suggested thattwice as many of our Child Trust Fundcustomers were making regularpayments into their Child Trust Fund,compared to the experience of otherproviders.

As explained in last year’s AnnualReport, we launched our new tradingidentity, engage Mutual Assurance, inApril 2005. Our new name has given theorganisation a contemporary look andfeel while retaining our traditionalmutual values and welfare orientation.

We have also made changes to thenames of our subsidiary companies tofeature the new engage identity. Thisenables us to make best use of the newname, while avoiding complex orconfusing caveats or footnotes in ourliterature to explain the differentrelationships between new tradingstyles and old company names. The firstof these was the OEIC manager –which is used to provide the Child TrustFund and our equity ISA product –which is now called engage MutualFunds Limited.

The more significant decision will bewhether to change the name of theSociety itself. To date, the engagetrading style has been a huge successand provides an excellent base onwhich to develop the Society further.We would like to see how this yearunfolds, but our current thinking is that itwould be appropriate to change thename of the Society next year. If we dodecide to go ahead, we willcommunicate our plans and seek yoursupport in the normal way by putting

forward a formal resolution for memberapproval.

With so much change happening inthe organisation and the industry atlarge, it would be all too easy tobecome focused on the present, dayto day issues of running the organisationand lose sight of our long term strategy.I am pleased to be able to informmembers that we have addressed thesignificant opportunities presented inthe last 12 months in the context ofwhere we need to take theorganisation in the long term. In hisBusiness Review, the Chief Executiveoutlines how we have made the mostof the opportunity to build newstrategic partnerships, build awarenessof our new name and develop theinternet as one of the most importantchannels by which we communicatewith people.

Some of the main responsibilities of yourBoard are, of course, to carefully reviewstrategy, progress and the changingrisks that the organisation faces. Wecontinue to develop both themembership of the Board and thereporting and control processes toensure that these responsibilities aredelivered effectively.

In my report last year, I referred to theMyners Review on “The Governance of

chairman’s report for the year ended 31 December 2005

6

Life Mutuals” and the likely proposals forimprovement in governance processes.These proposals have now crystallisedinto formal guidance which wasdeveloped by a joint Committee fromthe two trade bodies, the Association ofFriendly Societies and the Association ofMutual Insurers. The Society is amember of both organisations andplays an active role on the Committee.We support the changes and havealready implemented a number ofdetailed improvements to our ownprocesses, although we were pleasedto note that in the majority of cases wealready met the proposed standard.You can read about some of thechanges in the Corporate GovernanceSection of the Annual Report.

We were pleased to welcome two newNon-Executive Directors to the Societyin the course of 2005. ChristinaMcComb joined the Board in May.Christina is a Director of the ShareholderExecutive within the Cabinet Office,prior to which she had a longassociation with the venture capitalgroup 3i. She has much experience inthe workings of government and theproblems and challenges faced bygrowing organisations.

Peter Mason was appointed to theBoard in December, having had earlierinvolvement as an independentmember of the Finance & Risk

Committee. He is an Actuary andbrings a wealth of experience of lifecompany financial operations. Petertook on the Chairmanship of the AuditCommittee on 1 January 2006.

Graham Henderson joined the Board inFebruary 2006 for an eighteen monthfixed term in the Finance Director role,having worked with us on an interimbasis since October 2005. Graham is aqualified Chartered Accountant andhas extensive experience gained insenior roles in the life insurance industry,which has already been put to verygood effect. We look forward toworking with Graham in the months tocome.

Two members of the Board steppeddown in 2005.

Kevin Chidwick, Finance Director, leftthe Society in August to pursue otherinterests. We thank Kevin for hiscontribution and wish him well for thefuture.

Gordon Murison retired as a Non-Executive Director in May 2005.Gordon had given tremendous service,over 27 years, to the Board of theformer UK Civil Service Benefit Societywhich transferred its engagements to usin 2003. He remained on the Board ofthe merged organisation to ensure asmooth transition and to provide

continuity in the representation of theUK members at Board level. On behalfof all members we thank Gordon for hisservice over so many years and inparticular for the support and advicehe offered to make the integration ofthe Societies such an effective process.We wish Gordon an enjoyableretirement.

I closed my report last year with theexpectation that 2005 would beimportant for us. That certainly provedto be the case. I have no doubt that2006 will be just as important, as weseek to make the very most of theexcellent progress we made last year.

The Board, Management and Staff ofthe Society continue to focus onbuilding a successful future for theorganisation and delivering good valueand excellent service for all ourcustomers. We thank you for yoursupport.

Ray PierceChairman23 February 2006

7

chief executive’s business reviewfor the year ended 31 December 2005

8

As always, our priority last year was tocontinue to provide customers with agood value, high quality service fortheir savings and protection needs. In what proved to be a very eventfulyear, we were successful in that aimand were able to deliver our productsto a far wider audience than everbefore. The number of new policiesprocessed in the year rose by threeand a half times the number for 2004to nearly 80,000 and our customerbase grew by 24%.

a new look and a new name2005 was our first year of operationsunder our new trading style of engage Mutual Assurance. We areproud of the success we have beenable to make of Child Trust Fund (CTF),through our subsidiary engage MutualFunds Limited, and the impressive list ofnew distribution partners weattracted. These results wereunderpinned by our new tradingstyle, which provided a far morecontemporary and relevantfoundation on which to buildawareness and new customerrelationships.

The new style was launched tocustomers with the AGM Notice ofMeeting for 2005 and the first annualstatements under the new brandwere issued in January 2006.

Part of the challenge we faced inlaunching the new identity was howto make people aware of our newname. We were delighted to securea sponsorship arrangement with theRugby Football League which hasprovided extensive exposure in bothbroadcast and print media as titlesponsors of the engage SuperLeague. The sponsorship coveragewe received last year wasindependently assessed and wasestimated to have an equivalentmedia value worth significantly morethan the cost of the sponsorship. Welook forward to another successfulyear as sponsors in 2006 and haveextended the relationship to coverthe 2007 and 2008 seasons. Wefurther reinforced awareness ofengage, with the sponsorship of theengage International Open, a WorldBowls Tour event held in November2005. These initiatives have served toraise awareness and the profile of theorganisation amongst our customerbase, and have supported our salesand marketing activity during 2005.

results and key performanceindicators for 2005In my 2004 report, I aimed to providecustomers with more informationabout the progress of the Society. Wehave developed this report further tomeet new requirements for reportingunder an amendment (Section 71A)to the Friendly Societies Act.

The change of trading style fromHomeowners to engage MutualAssurance in April 2005 provided theideal platform from which to launchour CTF campaign. The CTF is theGovernment’s initiative to provideevery child born after 1 September2002 with a savings account. TheGovernment provides a voucher foreither £250 or, for lower incomefamilies, £500 to pay into the CTF atbirth and a further top up will beprovided at age 7. Families andfriends can add up to £1200 a yearto the CTF, tax free. The CTF waslaunched in April 2005 when morethan 2.7 million vouchers weredistributed. The initial wave ofvouchers included babies bornbetween September 2002 andJanuary 2005, and now goes to thechild benefit claimant of all new bornchildren in the UK.

In order to ensure that no child isexcluded, parents who do notchoose a CTF within twelve months ofreceiving their voucher will have theirCTF allocated to one of a number ofregistered providers. engage will beone of the providers registered toreceive government allocated CTFs.

We ended 2005 as one of the leadingproviders of CTFs. Our success in CTFwas the result of more than three years’preparation. In addition to extensiveresearch and involvement in theconsultation process, we developedoperating systems and procedures toensure the smooth and efficientadministration of these new accounts.

We provide CTFs direct to the publicthrough our website,www.engagemutual.com and alsothrough a range of high qualitypartners who provide additionalaccess for distribution. Early researchsuggests that we have beenparticularly successful in internetdistribution of CTFs and we believewe are the leading provider of webbased equity stakeholder CTFaccounts, with over 60% of allapplicants using the internet.

The positive impact of CTF on newbusiness volumes has been significant,as shown in the chart below.

We do not wish to become reliant onCTF as our sole source of newbusiness and have been working tomaintain sales in our traditional lifeassurance products such as the Over50s plan, Tax Exempt Savings Planand With Profits policies. Our lifebased new business volumeremained stable with only a veryslight decrease in volume and a slightincrease in the level of new businesspremiums in 2005.

For life assurance policies we shownew regular premiums and one tenthof the new single premiums for theyear. Under normal financial reportingconventions we would show the OEICinvestment sales in terms of the totalpremiums received, however for easeof comparison, we have adoptedthe same convention as for lifepolicies in this chart. The total figurefor new OEIC subscriptions was inexcess of £18m for the year.

9

new business volume

0

10

20

30

40

50

60

70

80

2001 2002 2003 2004 2005Year

k

Life

c

ctf

eMFL Subscription

Life policy API

new business performance

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2001 2002 2003 2004 2005Year

£m

chief executive’s business review (cont.)

The Group continues to be financiallyrobust. The Fund For FutureAppropriations (FFA) has continued toincrease as shown on our BalanceSheet on page 30.

The FFA is a measure of the Group’ssurplus assets over liabilities, usingaccounting conventions for lifecompanies. The improved positionreflects a strengthening of the WithProfits sub fund, with a proportion ofthese assets being required for futureterminal bonuses.

Continued investment in long-term,low charge business such as the CTFis likely to result in a reduction in theFFA as with this type of product, ittakes several years to recover theinitial costs, or ‘strain’, of selling andsetting up an account. Managing ourfinancial strain will be an importantfeature of our activities in the coming

years as we seek to grow theorganisation and maintain asatisfactory level of capital bykeeping costs under control.

The success of the CTF has broughtmany new customers to engage ascan be seen in the chart below. Itshould be noted that we always aimto offer all our customers the samestandard of value and service,regardless of which type of policythey hold or which subsidiary providestheir product.

It was a successful year for the WithProfits sub fund and the UK brands.We have continued to promote theUK Civil Service Benefit Society brandfollowing the transfer ofengagements in 2003, and welaunched the UK Armed ForcesBenefit Society brand in 2004 tosupport our activities with NAAFI

Financial. We saw good new businessgrowth in 2005 from new and existingcustomers with maturing polices.

investment performance In general, 2005 proved to be a verystable environment for UK basedsavings and investments.

It proved a successful period for theUK stock market and by the end ofthe year the FTSE All Share index hadrisen by more than 18%,predominantly driven by energycompanies benefiting from higher oilprices and significant returns for thosecompanies who serve the rapidlygrowing Chinese economy.

10

FTSE All Share index

1,000

1,500

2,000

2,500

3,000

3,500

2001 2002 20052003 2004

fund for future appropriations (FFA)

0

5

10

15

20

25

30

35

40

45

50

2001 2002 2003 2004 2005Year

£m

Year

£

group customers

0

50,000

100,000

150,000

200,000

250,000

300,000

2001 2002 2003 2004 2005Year

Life Policy holders

O

OEIC Customers

11

Stock market based investmentsshould be regarded with a mediumto long-term time frame, i.e. five toten years. As customers you shouldalso be aware that the value of stockmarket based investments can fall orrise and in some circumstancesinvestors may not get back all theyhave invested.

The Bank of England kept base ratesunchanged at 4.75% until August 2005,when economic indicators led themto lower rates to 4.50%, this being theonly movement during the year.

Many engage customers have theirpolicies invested in deposits. Theaverage tax-free return for ourdeposit-based policies in 2005 rose to4.85% before charges.

achieving our long termobjectivesThe long term goals for the Societycontinue to focus on an increase inthe scale of our operations andsustaining that scale with anincreased flow of new business. Inthat way, we will be able to achieve

a cost of operation that enables us todeliver simple, good value savingsand protection products to agrowing customer base.

It is pleasing to note that in a yearwhen we completely rebranded ouroperations and attracted three anda half times the volume of newbusiness in the previous year, ouroperating expenses remained withinour planned budgets.

Keeping control of expenses willcontinue to be a priority as we investto grow the organisation and buildan increasingly efficient operatingmodel and continued quality servicefor customers.

society administrative expenses

0

5

2001 2002 2003 2004 2005Year

£m

2

3

4

5

6

7

8

chief executive’s business review (cont.)

12

increase in scaleOrganic growth through initiativessuch as CTF is one aspect of our longterm plans. Another is to achievegrowth through third partyadministration and transfer ofengagement. We are proud of thesuccessful transfer of the UK CivilService Benefit Society in 2003 and,two years on, we can clearlydemonstrate how we upheld theprinciples of the transfer to the overallbenefit of the combined membershipof both organisations. The UK brandcontinues to thrive and is an importantpart of our continued operations. Weare keen to build on that success andmaintain an open dialogue with otherSocieties who may have an interest inpursuing a similar initiative.

We have maintained a strongrelationship with Pension AnnuityFriendly Society, who demutualisedlast year and changed their name toPartnership Assurance and for whomwe provide administration servicesthrough our subsidiary engage MutualAdministration Limited. Again, we arealways keen to speak to organisationswho are interested in pursuing asimilar initiative.

our productsWe aim to offer our customers arange of products rather thanspecialise in just one specific type ofproduct. CTF has been a welcomeaddition to our range and upholdsour principles of simple, good valueproduct design. But we do not justprovide for children, our productrange includes unit linked and withprofits savings plans, term assurance,guaranteed acceptance Over 50sLife Insurance, OEICs and equity ISAs.In 2006 we will look to furtherenhance our savings products to allgenerations to make them relevant,ensuring that all our customers haveaccess to the best service and valuewe can provide in protecting theirfamilies’ welfare.

new business partnerships

Our most significant new partner in2005 was ASDA. Through ASDA weare able to reach millions of potentialcustomers each week in over 300stores across the country. We havequickly developed a strong workingrelationship with ASDA which hasmade them an important nationaldistributor of the Child Trust Fund. Welook forward to developing therelationship further in 2006.

We have a tradition of buildingeffective distribution relationships withthird parties. Our partnership withNAAFI Financial has enabled us tooffer a range of savings andinvestment products to young soldierswho perhaps would not saveotherwise. It has also filled animportant gap in CTF distribution,making the CTF readily accessible tomembers of the Armed Forces.

We also welcomed a dozen buildingsocieties, including Yorkshire, Skipton,Leeds, Scarborough and Darlington,together with a number of friendlysocieties. In 2006 we are very pleasedto have been appointed to provideCTFs to customers of Legal & Generaland will look to develop a successfulrelationship with our most recentpartner, Debenhams, whilst looking toadd new partners during the year.

engage products are now availablethrough more channels and outletsthan ever before.

13

social and environmentalissuesThe very nature of our organisationmeans that we do not have asignificant environmental impact in theway that industrial companies do.However, we take our responsibilitiesseriously and have, for example,introduced a recycling scheme withinthe business. Within our basic mission ofencouraging people to save, weacknowledge the fact that theorganisation can have a significantsocial impact. We are keen to developinitiatives which enable us to serve theless well off and last year, for example,we developed a project with housingassociations to provide CTF literature totheir tenants, many of whom wouldnot have been approached by otherfinancial organisations.

We support local welfare orientedcharities and encourage our staff todo the same. We seek feedback fromstaff across many issues in theworkplace and completed abenchmark survey in 2005 againstwhich I will be able to report progressnext year.

customer feedbackWe always welcome customerfeedback, particularly if it helpsidentify a weakness or strength in ourservice that we can seek to improve,or where there is good news, domore of. Market Research has beena useful technique through which wehave understood customers’ productand service requirements. It alsoplayed an essential role in helping usto make the right choices in ourrecent change of trading style.

We have now decided to add morestructure to our feedback processesand have established a customerpanel which will be consulted onissues such as changes to service orproduct design. We are keen to hearfrom any customer who wishes to beavailable for such consultation, eitherthrough the Customer Panel page onour website www.engagemutual.comor by writing to the CompanySecretary at the Society’s address.

outlook for 2006Our main challenge will be tocontinue to grow so that we achievethe efficiencies required to run the

organisation effectively, whilemanaging our capital and expensescarefully to preserve our long termstability. A great deal was achievedin 2005 towards that goal and weexpect 2006 to be a year when thebenefits of that hard work will reallybecome evident. We have anincreasingly strong brand, excellentdistribution partners and a relevant,good value product range. We willcontinue to work hard in 2006 toensure we provide customers with thevalue and quality of financial servicesproducts that they require andexpect from us.

thanksWe made great progress last year butit would not have been possiblewithout the commitment of the staffand the continued loyalty of ourcustomers. Thank you all. We lookforward to a very successful 2006.

Andrew HaighChief Executive23 February 2006

directors’ report for the year ended 31 December 2005

14

The Directors present theirannual report, together withthe financial statementsand Auditor’s report for theyear ended 31 December2005.

business objectivesThe mission of engage is to enablepeople to protect their welfare. Wewill do this by providing our customerswith accessible, simple, value formoney protection and savingsproducts.

Our major subsidiaries are playing anincreasingly important role in meetingthe mission:

• engage Mutual Funds Limited is theprovider of our stakeholder ChildTrust Fund, along with our equity ISAproduct. Homeowners InvestmentFund Managers Limited changed itsname to engage Mutual FundsLimited on 25 January 2006.

• engage Mutual AdministrationLimited, our administration servicessubsidiary, provides services toother organisations, creating anincome which can be used tooffset our operating expenses. Thesubsidiary also employs all of thestaff of engage. HomeownersFinancial Administration Limitedresolved to change its name toengage Mutual AdministrationLimited on 23 February 2006.

The role of the subsidiaries and theimpact on the finances of the Societyis such that we present consolidatedaccounts for the Group.

The Board is committed to theongoing development of engage asa leading Friendly Society, deliveringa range of good value, welfareproducts to a wide audience throughdirect, worksite and partnershipdistribution.

The Directors are of the opinion thatall activities performed during theyear by the Society and itssubsidiaries have been carried outwithin their respective powers.

development of businessKey business developments and thefuture outlook for the business of theSociety and its subsidiaries aredetailed in the Chief Executive’sBusiness Review on pages 8 to 13.

15

board of directorsA list of Directors who held officeduring the year appears within the‘society information’ on page 2.

Christina McComb was appointed asa Director on 11 May 2005 and PeterMason on 9 December 2005 and,being eligible, offer themselves forelection to the Board of Directors.Gordon Murison retired on 12 May2005. The Board wishes toacknowledge his contribution, inparticular, for the successful transitionof the ex UK Civil Service BenefitSociety (UKCSBS) business into theSociety. Kevin Chidwick resigned on26 August 2005. Graham Hendersonwas appointed as Finance Directoron 23 February 2006.

Lord Clark and Andrew Haigh retire inaccordance with the Society’s rulesand the Friendly Societies Act 1992and, being eligible, offer themselvesfor re-election.

As at the year end, no Director of theSociety had any interest in the sharesof the Society’s subsidiary companies.

The Society maintains Directors’ andOfficers’ Insurance for the Board ofDirectors in respect of their duties asmembers of the Board.

statement of solvencyAs at 31 December 2005, theSociety’s capital resources for eachclass of relevant business exceededthe minimum capital resourcesrequirements prescribed by theFinancial Services Authority’s“Integrated Prudential Sourcebook”.

membershipMembership of the Society as at 31 December 2005 stood at 234,015(2004: 239,056).

complaints policyWe aim to deliver the highest possiblelevel of service to our customers. Ifany customer believes that we havefailed in this aim, they have recourseto our complaints procedures.

We have documented proceduresfor the handling and recording ofcomplaints. We deal with allcomplaints with due care, ensuringthat they are thoroughly investigated.The Board of Directors regularlyreviews the number and type ofcomplaints received to monitor thatcomplaints are properly dealt withand corrective action has beentaken to prevent recurrence.

Senior management deals withserious complaints. In the unlikelyevent that a complaint cannot beresolved to the customer’s satisfaction,the customer will be made aware ofthe option to appeal to the FinancialOmbudsman Service.

employeesThe average number of Directors andstaff employed by the Group, in eachweek of the year, totalled 192. Theaggregate remuneration paid toDirectors and staff employed by theGroup, during the year, amounted to £5,161,000. All of the staff areemployed by our third partyadministration subsidiary, engageMutual Administration Limited.

The Society’s management meetsemployee representatives regularly to discuss a wide range of topics,through its staff forum.Communication with and betweenall employees is subject to regularreview and includes staff satisfactionsurveys, team briefings and informalmeetings with the Chief Executive.

engage has an equal opportunitiespolicy for recruitment and iscommitted to the ongoingdevelopment of its staff. The Societyhas been officially recognised as an‘Investor in People’ since 2001.

directors’ report for the year ended 31 December 2005 (cont.)

16

pensions arrangementsWe are committed to assisting ourstaff to make adequate provision fortheir retirement, and to this end theaccounts show a small surplus on ourdefined benefit scheme. This schemeclosed to new members on 29 March2001. The Directors are working withthe trustees to seek to manage thepension scheme investment policy toensure that the scheme remains in aposition to meet its obligations goingforward in a manner which shouldnot place a material financial strainon the Society.

For employees joining the Societysince April 2001 we have a definedcontribution arrangement in placewhereby the Society matches theemployee’s contributions with amaximum corporate contribution of 10% of salary.

charitable donationsIn 2005 we donated £9,191 tocharities, which included donationsto local charities, St Michael’sHospice and Martin House Hospice aswell as donations to SCOPE, BritishHeart Foundation, Children in Needand the Breast Cancer and TsunamiAppeals. We met all the costs ofmaintaining the grounds that weshare with our local Hospice.

Our staff fully support charities andhave donated £1,589 to Children inNeed, Cancer Research, SCOPE andthe Breast Cancer Appeal as well asdonations to local charities, St Michael’s Hospice, Martin HouseHospice, Harrogate Hospital and theJake Burgess Appeal.

More recently, engage has beenofficially recognised as having one ofthe country's most successful Give asYou Earn schemes and was awardedthe Payroll Giving Gold Award. Thishonour recognised the number of ouremployees who had enrolled on thescheme and was presented to theSociety in February 2006.

re-appointment of auditorsA resolution to re-appoint KPMGAudit Plc as Auditor will be proposedat the forthcoming Annual GeneralMeeting. Auditors are rotated at leastonce every seven years with a fullreview process being conductedevery three years.

By Order of the BoardAndrew HorsleySecretary23 February 2006

17

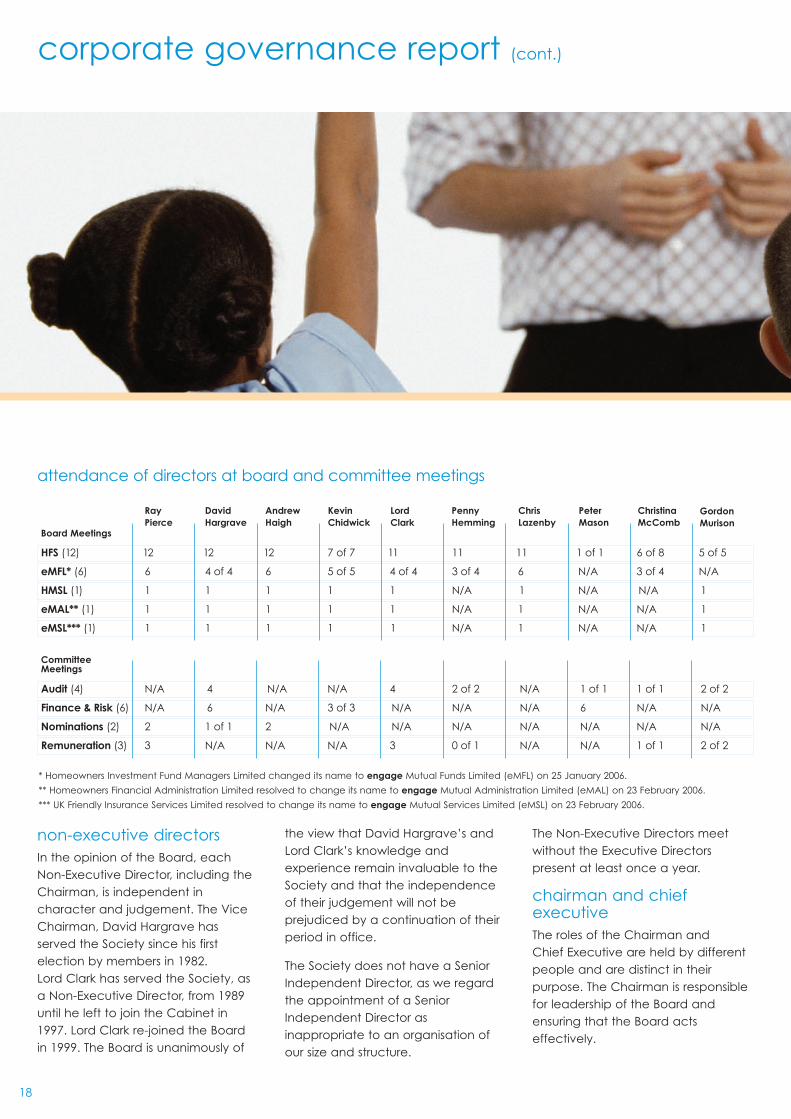

corporate governance report

The Board is accountable to theSociety’s members for the operationof the Society and regards goodcorporate governance as beingfundamental to this responsibility. It hasbeen the Society’s policy to follow theprinciples of the Combined Code onCorporate Governance matters for anumber of years. As a result, the Boardhas welcomed the recommendationsof the Myners Review and theintroduction of the AnnotatedCombined Code. The Board is firmly ofthe view that, to comply with bestpractice in corporate governance, itshould aim to adhere to the principlesand provisions of the Combined Codeon Corporate Governance annotatedby the Association of Mutual Insurersand the Association of FriendlySocieties to cover mutual insurers (“theCode”).

It will be our policy to observe theCode wherever appropriate for anorganisation of our size, status andaspiration or to clearly explain whywe feel any deviation from the Codeis acceptable or necessary. TheBoard considers that it complies withall aspects of the Code unless thecontrary is stated within this Report.

The Board applies principles of goodgovernance by adopting thefollowing procedures:

• the Board meets a minimum of sixtimes a year for Board meetingsand, in addition, meets at leasttwice a year for a detailed reviewof the Society’s strategy;

• the Board’s principal role is to focuson the Society’s strategy andensure that the necessary resourcesare in place for the Group to meetits objectives and that financialcontrol and risk managementprocedures are robust. In particular,its role is to provide generaldirection to the organisation and tosafeguard the interests of members;

• the Board maintains a schedule ofretained powers relating to approvalof the strategic aims of the Group aswell as approval of policies andmatters which must be approved bythe Board under legislation and theSociety’s rules;

• to ensure that the Board functionseffectively, all Directors receiveaccurate, timely and clear informationand it is the responsibility of theChairman to ensure that this isperiodically reviewed;

• the Chairman also ensures that, onappointment, Non-Executive Directorsreceive a comprehensive tailoredinduction programme on the Group’sbusiness and regulatory environment.All Non-Executive Directors update

their skills, knowledge and familiaritywith the Group through meetings withthe Executive of the Society and itsemployees and relevant externalcourses. Individual trainingrequirements for Non-Executives arediscussed during the performanceevaluation process;

• the Board has access toindependent professional advice atthe Society’s expense, where theyjudge it necessary to dischargetheir responsibilities as Directors;

• all Directors have access to theadvice and services of the GroupSecretary who is responsible forensuring the Board procedures arecomplied with and advising theBoard, through the Chairman, ongovernance matters;

• the Board currently consists of threeExecutive Directors and six Non-Executive Directors. The size andcomposition of the Board is keptunder review to ensure that there isadequate succession planning forExecutive and Non-ExecutiveDirectors and that there aresufficient skills and experiencerepresented on the Board for thedirection of the Group’s activities.The Board is of the opinion that thecomposition of the Board isappropriate for the business.

corporate governance report (cont.)

18

HFS (12) 12 12 12 7 of 7 11 11 11 1 of 1 6 of 8 5 of 5

eMFL* (6) 6 4 of 4 6 5 of 5 4 of 4 3 of 4 6 N/A 3 of 4 N/A

HMSL (1) 1 1 1 1 1 N/A 1 N/A N/A 1

eMAL** (1) 1 1 1 1 1 N/A 1 N/A N/A 1

eMSL*** (1) 1 1 1 1 1 N/A 1 N/A N/A 1

Board Meetings

RayPierce

DavidHargrave

AndrewHaigh

KevinChidwick

LordClark

PennyHemming

ChrisLazenby

PeterMason

ChristinaMcComb

attendance of directors at board and committee meetings

Audit (4) N/A 4 N/A N/A 4 2 of 2 N/A 1 of 1 1 of 1 2 of 2

Finance & Risk (6) N/A 6 N/A 3 of 3 N/A N/A N/A 6 N/A N/A

Nominations (2) 2 1 of 1 2 N/A N/A N/A N/A N/A N/A N/A

Remuneration (3) 3 N/A N/A N/A 3 0 of 1 N/A N/A 1 of 1 2 of 2

Committee Meetings

GordonMurison

* Homeowners Investment Fund Managers Limited changed its name to engage Mutual Funds Limited (eMFL) on 25 January 2006.

** Homeowners Financial Administration Limited resolved to change its name to engage Mutual Administration Limited (eMAL) on 23 February 2006.

*** UK Friendly Insurance Services Limited resolved to change its name to engage Mutual Services Limited (eMSL) on 23 February 2006.

non-executive directors In the opinion of the Board, eachNon-Executive Director, including theChairman, is independent incharacter and judgement. The ViceChairman, David Hargrave hasserved the Society since his firstelection by members in 1982. Lord Clark has served the Society, asa Non-Executive Director, from 1989until he left to join the Cabinet in1997. Lord Clark re-joined the Boardin 1999. The Board is unanimously of

the view that David Hargrave’s andLord Clark’s knowledge andexperience remain invaluable to theSociety and that the independenceof their judgement will not beprejudiced by a continuation of theirperiod in office.

The Society does not have a SeniorIndependent Director, as we regardthe appointment of a SeniorIndependent Director asinappropriate to an organisation ofour size and structure.

The Non-Executive Directors meetwithout the Executive Directorspresent at least once a year.

chairman and chiefexecutiveThe roles of the Chairman and Chief Executive are held by differentpeople and are distinct in theirpurpose. The Chairman is responsiblefor leadership of the Board andensuring that the Board actseffectively.

19

The Chief Executive has overallresponsibility for managing theSociety and its subsidiaries and forimplementing the strategies andpolicies agreed by the Board.

performance evaluationThe Group has a formal performanceevaluation system for all members ofstaff including the Executive Directors.The Chief Executive appraises theExecutive Directors on theirperformance and the Chairmanundertakes an appraisal of the Chief Executive.

A performance evaluation system forNon-Executive Directors, including theChairman, has been established. TheChairman meets each Non-ExecutiveDirector annually to discuss individualperformance. A meeting of the Non-Executive Directors is also held,without the Executive Directors present,to discuss collectively the performanceof the Executive Directors.

In 2005 the appraisal of Non-ExecutiveDirectors took the format of anappraisal of each individual Directorby the Chairman through the

completion of a questionnaire. TheChairman reviewed the output of allquestionnaires and used this as abasis for an evaluation interview witheach Non-Executive Director. Thisprocedure identifies any individualand Board training requirements andprovides the evidence for the Boardto decide whether to recommend tomembers that a Director should bere-elected.

appointments to the boardThe appointment of new Directors isconsidered by the NominationsCommittee (see page 21) whichmakes recommendations to theBoard. All Directors are subject toelection by members at the AnnualGeneral Meeting (AGM) followingtheir appointment. In addition, allDirectors must receive approval fromthe Financial Services Authority as anApproved Person in order to fulfil theircontrolled function as a Director.Under the Society’s Rules, Directorshave to submit themselves for re-election at least once every three years.

At the AGM to be held in 2006,members will be asked to electChristina McComb, Peter Mason andGraham Henderson, and re-electAndrew Haigh and Lord Clark.

Given their particular individualexpertise and experience andperformance to date, the Boardrecommends that Christina McComb,Peter Mason and Graham Hendersonbe put forward for election andAndrew Haigh and Lord Clark be putforward for re-election by members.

The terms and conditions ofappointment of Non-ExecutiveDirectors are available for inspectionat our Head Office and can beviewed by contacting the Secretary.

board committeesThe Board has established a numberof Committees which have their ownterms of reference. Details of theprincipal Board Committees,including their membership during2005, are set out overleaf.

corporate governance report (cont.)

20

audit committeeThe Audit Committee consists of fourNon-Executive Directors which, witheffect from 1 January 2006, falls underthe Chairmanship of Peter Mason.Three of the Committee members,Peter Mason, Christina McComb andDavid Hargrave, have relevantfinancial sector experience. The otherCommittee member is Lord Clark. Theresponsibilities of the Committee arein line with the provisions of the SmithGuidance on Audit Committees. Themain function of the Committee is toassist the Board in fulfilling its oversightresponsibilities, specifically theongoing review, monitoring andassessment of:

• the integrity of the financialstatements and reviewingsignificant financial reportingjudgements contained in them;

• the effectiveness of systems ofinternal control and riskmanagement processes;

• the internal and external auditprocesses;

• compliance with applicable lawsand regulations;

• the recommendation to the Boardon the appointment, re-appointmentand removal of External Auditors.

During 2005 the Committee met fourtimes in the execution of itsresponsibilities. During the meetingsthe Committee considered reports on:

• the system of internal control;

• the integrity of financial statements;

• high level risks and associatedcontrols;

• compliance with laws andregulations, including adherence to Money Laundering and Health & Safety regulations; and

• the activities of internal audit and ofthe External Auditors on the audit.

Reports were provided by the InternalAudit, Risk and Compliance functionsand the External Auditors. TheChairman of the Audit Committeemeets regularly with the Internal Auditorto discuss issues of internal control.

The Committee considers that it hasmet its responsibilities and performedits duties with appropriate levels ofcare and expertise during 2005.

finance & risk committeeThe Finance & Risk Committeeconsists of Peter Mason, GrahamHenderson, the Finance Director, andTrevor Batten, the Actuarial FunctionHolder and With Profits Actuary,under the Chairmanship of DavidHargrave. The Committee met sixtimes during 2005 to review theGroup’s financial management ingreater detail than is possible atregular Board meetings. In particular,the Board has charged theCommittee with providing directionand recommending strategy in theareas of management of theSociety’s with profit business,management of the Group’sinvestment strategy and monitoringof the Group’s investmentperformance. In September 2005, thepurposes of the Committee wereexpanded to include a review of theprinciples underlying capitalmanagement of the Group, productpricing for all Group products, theexpense analysis and FSA returns.

21

nominations committeeThe Nominations Committee consistsof the Chairman, the Vice Chairmanand the Chief Executive. It meets asappropriate to review the structure,size and composition of the Boardand to make recommendations to theBoard with regard to any adjustmentsthat are deemed necessary. It is alsoresponsible for identifying andnominating for the approval of theBoard, candidates to fill Boardvacancies as and when they arise.

We appointed professionalrecruitment consultants to ensure thatvacancies were brought to theattention of as wide an audience aspossible. All applicants wereindependently appraised by externalconsultants and a short list was drawnup, prior to interview by the Boardand appointment.

remuneration committeeThe Remuneration Committeecurrently consists of the Chairman ofthe Society and three independentNon-Executive Directors, under theChairmanship of Christina McComb.Christina McComb took overChairmanship of the RemunerationCommittee from the Chairman of theSociety on 9 December 2005. TheCommittee meets as appropriate todetermine the policy for executive

remuneration. The objective of theCommittee is to give ExecutiveDirectors encouragement to enhancethe Society’s performance by ensuringthat they are fairly and responsiblyrewarded for their individual andcollective contributions. Further detailsof the Committee and theremuneration policy can be found inthe Report of the Directors onRemuneration on pages 24 to 25.

Where the Society appointsremuneration consultants, they haveno other connection with the Society.

The full terms of reference of theAudit, Finance & Risk, Nominationsand Remuneration Committees areavailable on request from the GroupSecretary or by viewing our websiteat www.engagemutual.com.

relations with customersThe customers of the engage Groupare made up of the Friendly Society’slife fund members and non-lifecustomers of its open endedinvestment subsidiary company.engage applies the same principlesof value and service to all customersand encourages feedback on anyaspect of the Group’s activities.

The engage Group has recentlyestablished a customers’ panel,consisting of around 200 customers,

who are invited to comment on avariety of issues. It is the intention of theSociety that members of the Board willattend meetings of the panel and usethis as an opportunity to understandcustomers’ issues and concerns.

All members of the Friendly Societywho are eligible to vote areencouraged to exercise their vote atthe AGM by sending to them a proxyvoting form and pre-paid replyenvelope. A separate resolution isproposed on each separate issueincluding a resolution on the AnnualReport and Accounts.

system of internal controlThe Board has delegatedresponsibility for managing the systemof internal control to seniormanagement. The Internal Auditfunction provides independentassurance to the Board on theeffectiveness of the system of internalcontrol through the Audit Committee.

The information received andconsidered by the Committeeprovided reasonable assurance thatduring 2005 there were no materialbreaches of control or regulatorystandards and that, overall, theGroup maintained an adequatesystem of internal control.

corporate governance report (cont.)

22

auditorThe Group has a policy on the use ofthe External Auditor for non-auditwork which is implemented by theAudit Committee. The purpose of thepolicy is to ensure the continuedindependence and objectivity of theExternal Auditor. The External Auditor,KPMG Audit Plc, undertook a numberof non-audit assignments during 2005and these were conducted withinthe limits set out in the policy and areconsidered to be consistent with theprofessional and ethical standardsexpected of the External Auditor inthis regard.

role as an institutionalshareholderThe Group has appointed State StreetGlobal Advisers and more recently in2006 Legal & General InvestmentManagement to undertake its fundmanagement. Both fund managerscomply with the principles set out in“The responsibilities of institutionalshareholders and agents – statementof principles” published by theInstitutional Shareholders Committee.

The Group has requested State Streetand Legal & General to considercarefully the explanations given bycompanies in which they haveinvested for any departure from theCombined Code and to makereasoned judgements in each case.Our fund managers use the ABI andResearch, Recommendations &Electronic Voting (RREV) services toanalyse resolutions for compliancewith the Combined Code. Where thefund manager does not accept theexplanation for any major departurefrom the Combined Code, the fundmanager will enter into dialoguedirectly with the company inquestion. Arrangements are currentlybeing made to ensure that the Boardis made aware, through the quarterlyreport of any issues of significance.

Our fund managers have proceduresto check that proxy votes have beenreceived. Arrangements are currentlybeing made to ensure that the Boardis made aware, through the quarterlyreport, of the total number ofresolutions and the number ofcompany resolutions that the fundmanager voted against or abstained.

Our fund managers also attendAGMs of companies in which theyhave invested, on behalf of theSociety, where it is appropriate andpracticable to do so.

creditor payment policyIt is the Society's policy to settleinvoices in accordance with suppliers'standard terms, unless specificallyagreed otherwise in advance.

23

statement of the directors’ responsibilities

The Directors are responsible forpreparing the Directors’ Report andthe financial statements inaccordance with applicable law and regulations. Friendly Society lawrequires the Directors to preparefinancial statements for eachfinancial year. Under that law theDirectors have elected to preparethe financial statements inaccordance with UK AccountingStandards. The financial statementsare required by law to give a trueand fair view of the state of affairs of the Society and of the income and expenditure of the Society forthat period. In preparing thesefinancial statements, the Directors are required to:

• select suitable accounting policiesand then apply them consistently;

• make judgements and estimatesthat are reasonable and prudent;

• state whether applicable UKAccounting Standards have beenfollowed, subject to any materialdepartures disclosed and explainedin the financial statements; and

• prepare the financial statements onthe going concern basis, unless it isinappropriate to presume that theGroup will continue in business.

The Directors are responsible forkeeping proper accounting recordsthat disclose with reasonableaccuracy at any time the financialposition of the Society and enablethem to ensure that its FinancialStatements comply with the FriendlySocieties Act 1992. They have generalresponsibility for taking such steps asare reasonably open to them tosafeguard the assets of the Societyand to prevent and detect fraud andother irregularities. Under applicablelaw the Directors are also responsiblefor preparing a Directors’ Report thatcomplies with that law.

report of the directors on remuneration

24

2005 2004salary bonus benefits sub-total contributions total total

£’000 £’000 £’000 £’000 £’000 £’000 £’000

Executive Directors

Andrew Haigh (Chief Executive) 174 40 1 215 24 239 200

Kevin Chidwick (resigned 26 August 05) 82 - 1 83 8 91 141

Chris Lazenby 109 9 1 119 10 129 127

Total 365 49 3 417 42 459 468

2005 2004salary bonus benefits sub-total contributions total total

£’000 £’000 £’000 £’000 £’000 £’000 £’000

Non-Executive Directors

Ray Pierce (Chairman) 60 - 1 61 - 61 58

Lord Clark of Windermere 26 - 1 27 - 27 18

David Hargrave 36 - 1 37 - 37 50

Penny Hemming 24 - - 24 - 24 5

Peter Mason (appointed 9 December 05) 1 - - 1 - 1 -

Christina McComb (appointed 11 May 05) 14 - - 14 - 14 -

Gordon Murison (retired 12 May 05) 10 - 1 11 - 11 24

Total 171 - 4 175 - 175 155

pension

pension

the total emoluments of the Directors, comprise:

The composition and responsibilities ofthe Society’s Remuneration Committeeare set out on page 3 and 21respectively. The RemunerationCommittee is responsible for the Group’sExecutive remuneration policy. Theobjective of the Committee is to giveExecutive Directors encouragement toenhance the Society’s performanceby ensuring that they are fairly andresponsibly rewarded for their individual

contributions. Where possible theCommittee seeks to meet thestandards set out in the CombinedCode applicable to listed companies.

The level of remuneration is set byreference to jobs carrying similarresponsibilities in similar organisations.There is a performance-related elementwithin the remuneration, which is linkedto the achievement of objectives.

Proper regard is paid to the need toretain good quality, highly motivatedstaff and the remuneration beingpaid by competitors of the Society istaken into consideration. In thisrespect the Committee receivesinformation inter alia from a leadingfirm of remuneration consultants, Hay,and also receives benchmarking datawhere required.

The remuneration of our Non-Executive Directors is recommended by the Chairman and the Chief Executive for theRemuneration Committee to agree annually at the year end. The remuneration is calculated on the basis of an agreedminimum number of days committed to Society business, and is paid at a rate, which has been confirmed as competitive,when compared with other similar sized financial services organisations.

25

service contractsAndrew Haigh and Chris Lazenbyhave service contracts with a twelve-month notice period. The standardterms for Executive Directors includea contractual notice period of 12months. Graham Henderson isemployed on an 18 month fixed termcontract from 1 January 2006.

No Non-Executive Director has aservice contract.

non-executive directors’remunerationNon-Executive Directors’remuneration comprises a specifiedfee, which includes extra amounts forspecific additional responsibilities, asset out on page 2.

executive bonusentitlementsThe Society operates an annualdiscretionary bonus scheme forExecutive Directors. The Society’spolicy is to ensure that ExecutiveDirectors are appropriatelyincentivised to meet the objectives ofthe business.

The Chief Executive is awarded amaximum of 66% of basic salary forachievement of Society objectives.The Operations Director is awarded a

maximum of 15% of basic salary forthe achievement of individualobjectives with a further maximum of15% awarded for the achievement ofSociety objectives.

long-term benefitsThe Executive Directors participate ina long-term bonus scheme, based onthe long-term performance of theGroup. This has been provided for inthe financial statements ofHomeowners Financial AdministrationLimited, but is not payable to theDirectors until January 2006. The longterm bonus scheme ran from 1January 2002 to 31 December 2005,at its conclusion Andrew Haigh wasawarded £70,000. Kevin Chidwick leftthe Group in August 2005, accordinglyno payment was made under thelong term bonus scheme. It isanticipated a further long term benefitscheme for the Executive Directors willrun for the period 2006 to the end of 2008, subject to the approval of theRemuneration Committee.

directors’ pensionentitlementThe company operates a definedbenefit pension scheme for itsemployees. This scheme was closedto new entrants on 29 March 2001.

A stakeholder pension scheme is inplace for all new employees. ChrisLazenby is a member of thestakeholder pension scheme andAndrew Haigh is a member of thedefined benefit pension scheme. Thetransfer value of Andrew Haigh’spension at 31 December 2005 was£167,610 (2004: £115,113).

other benefitsAlso paid in respect of 2005 for formerDirectors and their spouses was£3,000 pension (2004: £3,000). Therewere no payments relating to loss ofoffice in 2005 (2004: £Nil).

independent auditor’s report

26

independent auditor’sreport to the members of Homeowners FriendlySociety LimitedWe have audited the Group andSociety financial statements ofHomeowners Friendly Society Limitedfor the year ended 31 December2005 which comprise the Group andSociety Income and ExpenditureAccounts, the Group and SocietyBalance Sheets and the relatednotes. These financial statementshave been prepared under theaccounting policies set out therein.We are also required to report on theReport of the Directors for the yearended 31 December 2005.

This report is made solely to theSociety’s members, as a body, inaccordance with section 73 of theFriendly Societies Act 1992. Our auditwork has been undertaken so thatwe might state to the Society’smembers those matters we arerequired to state to them in anauditors’ report and for no otherpurpose. To the fullest extentpermitted by law, we do not acceptor assume responsibility to anyone

other than the Society and theSociety’s members as a body, for ouraudit work, for this report, or for theopinions we have formed.

respective responsibilities ofthe directors and auditors

The Directors’ responsibilities forpreparing the financial statements inaccordance with applicable law andUK accounting standards (UK GenerallyAccepted Accounting Practice) areset out in the Statement of Directors’Responsibilities on page 23.

Our responsibility is to audit thefinancial statements in accordancewith relevant legal and regulatoryrequirements and InternationalStandards on Auditing (UK andIreland).

We report to you our opinion as towhether the financial statements givea true and fair view and are properlyprepared in accordance with theFriendly Societies Act 1992 and theregulations made under it. In additionwe report to you if, in our opinion, theSociety has not kept proper accountingrecords, or if we have not received all

the information, explanations andaccess to documents that we requirefor our audit.

We also report to you our opinion asto whether the Report of the Directorshas been prepared in accordancewith the Friendly Societies Act 1992and the regulations made under it,and as to whether the informationgiven therein is consistent with thefinancial statements.

We read other information containedin the Annual Report & Accounts andconsider whether it is consistent withthe audited financial statements. Weconsider the implications for ourreport if we become aware of anyapparent misstatements or materialinconsistencies with the financialstatements. Our responsibilities do notextend to any other information.

independent auditor’s report

27

basis of audit opinionWe conducted our audit inaccordance with InternationalStandards on Auditing (UK andIreland) issued by the AuditingPractices Board. An audit includesexamination, on a test basis, ofevidence relevant to the amountsand disclosures in the financialstatements. It also includes anassessment of the significantestimates and judgments made bythe Directors in the preparation of thefinancial statements, and of whetherthe accounting policies areappropriate to the Group’s andSociety's circumstances, consistentlyapplied and adequately disclosed.

We planned and performed ouraudit so as to obtain all theinformation and explanations whichwe considered necessary in order toprovide us with sufficient evidence togive reasonable assurance that thefinancial statements are free frommaterial misstatement, whethercaused by fraud or other irregularityor error. In forming our opinion wealso evaluated the overall adequacyof the presentation of information inthe financial statements.

opinionIn our opinion the financialstatements give a true and fair view,in accordance with UK GenerallyAccepted Accounting Practice, ofthe state of affairs of the Group andof the Society as at 31 December2005 and of the income andexpenditure of the Group and of theSociety for the year then ended.

In our opinion the financialstatements have been properlyprepared in accordance with theFriendly Societies Act 1992 and theregulations made under it.

In our opinion the Report of theDirectors has been prepared inaccordance with the FriendlySocieties Act 1992 and theregulations made under it and theinformation given therein is consistentwith the financial statements.

KPMG Audit PlcRegistered AuditorChartered AccountantsLeeds23 February 2006

.

28

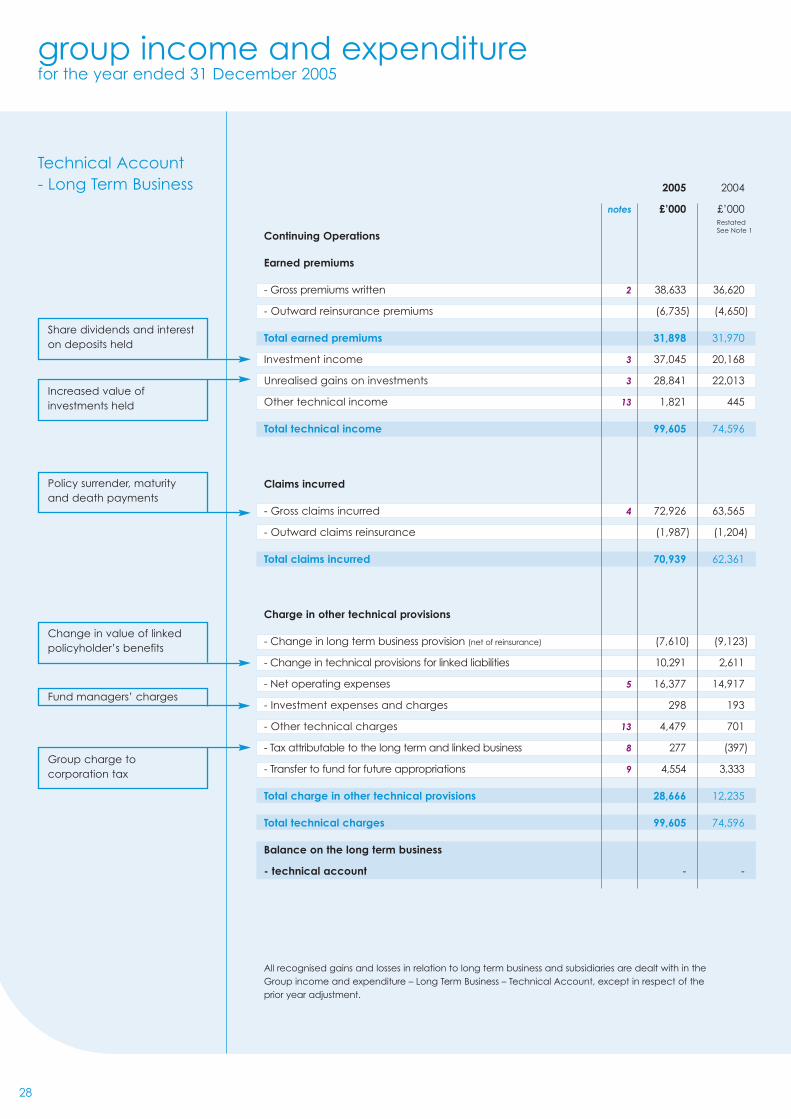

group income and expenditure for the year ended 31 December 2005

Technical Account - Long Term Business

Share dividends and intereston deposits held

Policy surrender, maturityand death payments

Change in value of linkedpolicyholder’s benefits

Increased value ofinvestments held

Group charge tocorporation tax

Fund managers’ charges

2005 2004

notes £’000 £’000

Continuing Operations

Earned premiums

- Gross premiums written 2 38,633 36,620

- Outward reinsurance premiums (6,735) (4,650)

Total earned premiums 31,898 31,970

Investment income 3 37,045 20,168

Unrealised gains on investments 3 28,841 22,013

Other technical income 13 1,821 445

Total technical income 99,605 74,596

Claims incurred

- Gross claims incurred 4 72,926 63,565

- Outward claims reinsurance (1,987) (1,204)

Total claims incurred 70,939 62,361

Charge in other technical provisions

- Change in long term business provision (net of reinsurance) (7,610) (9,123)

- Change in technical provisions for linked liabilities 10,291 2,611

- Net operating expenses 5 16,377 14,917

- Investment expenses and charges 298 193

- Other technical charges 13 4,479 701

- Tax attributable to the long term and linked business 8 277 (397)

- Transfer to fund for future appropriations 9 4,554 3,333

Total charge in other technical provisions 28,666 12,235

Total technical charges 99,605 74,596

Balance on the long term business

- technical account - -

All recognised gains and losses in relation to long term business and subsidiaries are dealt with in the Group income and expenditure – Long Term Business – Technical Account, except in respect of the prior year adjustment.

Restated See Note 1

29

group balance sheet as at 31 December 2005

Assets

Harrogate head office andKew Gardens property

Fixtures, fittings andcomputer hardware

With Profits fund and surplusinvestments

Value of unit linkedinvestments

Accumulated sales coststhat are associated withacquiring new policies and are spread over several years

RestatedSee Note 1

2005 2004

notes £’000 £’000

Investments

- Investment in land and buildings 10 6,300 6,175

- Financial investments 10 134,359 134,975

Total investments 140,659 141,150

Assets held to cover linked liabilities 11 456,561 446,270

Reinsurers’ share of technical provisions

- Long term business provision 4,604 2,795

Debtors

- Other debtors 530 453

Other assets

- Tangible assets 12 805 689

- Cash at bank 3,255 1,332

- Pension asset 17 546 413

Total other assets 4,606 2,434

Prepayments and accrued Income

- Accrued interest and rent 5,772 5,934

- Deferred acquisition costs 859 2,371

- Other prepayments and accrued income 977 1,883

Total prepayments and accrued income 7,608 10,188

Total assets 614,568 603,290

30

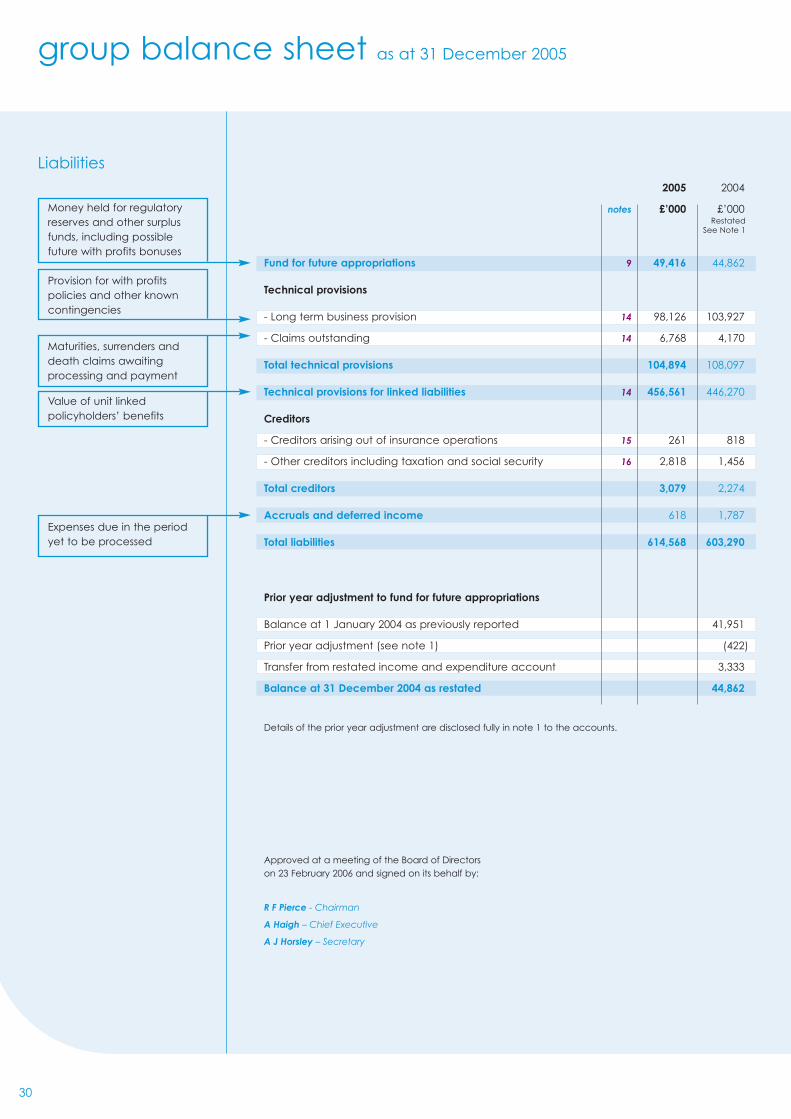

group balance sheet as at 31 December 2005

Liabilities

Provision for with profitspolicies and other knowncontingencies

Money held for regulatoryreserves and other surplusfunds, including possiblefuture with profits bonuses

Expenses due in the periodyet to be processed

Value of unit linkedpolicyholders’ benefits

2005 2004

notes £’000 £’000

Fund for future appropriations 9 49,416 44,862

Technical provisions

- Long term business provision 14 98,126 103,927

- Claims outstanding 14 6,768 4,170

Total technical provisions 104,894 108,097

Technical provisions for linked liabilities 14 456,561 446,270

Creditors

- Creditors arising out of insurance operations 15 261 818

- Other creditors including taxation and social security 16 2,818 1,456

Total creditors 3,079 2,274

Accruals and deferred income 618 1,787

Total liabilities 614,568 603,290

Prior year adjustment to fund for future appropriations

Balance at 1 January 2004 as previously reported 41,951

Prior year adjustment (see note 1) (422)

Transfer from restated income and expenditure account 3,333

Balance at 31 December 2004 as restated 44,862

RestatedSee Note 1

Maturities, surrenders anddeath claims awaitingprocessing and payment

Details of the prior year adjustment are disclosed fully in note 1 to the accounts.

Approved at a meeting of the Board of Directors on 23 February 2006 and signed on its behalf by:

R F Pierce - Chairman

A Haigh – Chief Executive

A J Horsley – Secretary

31

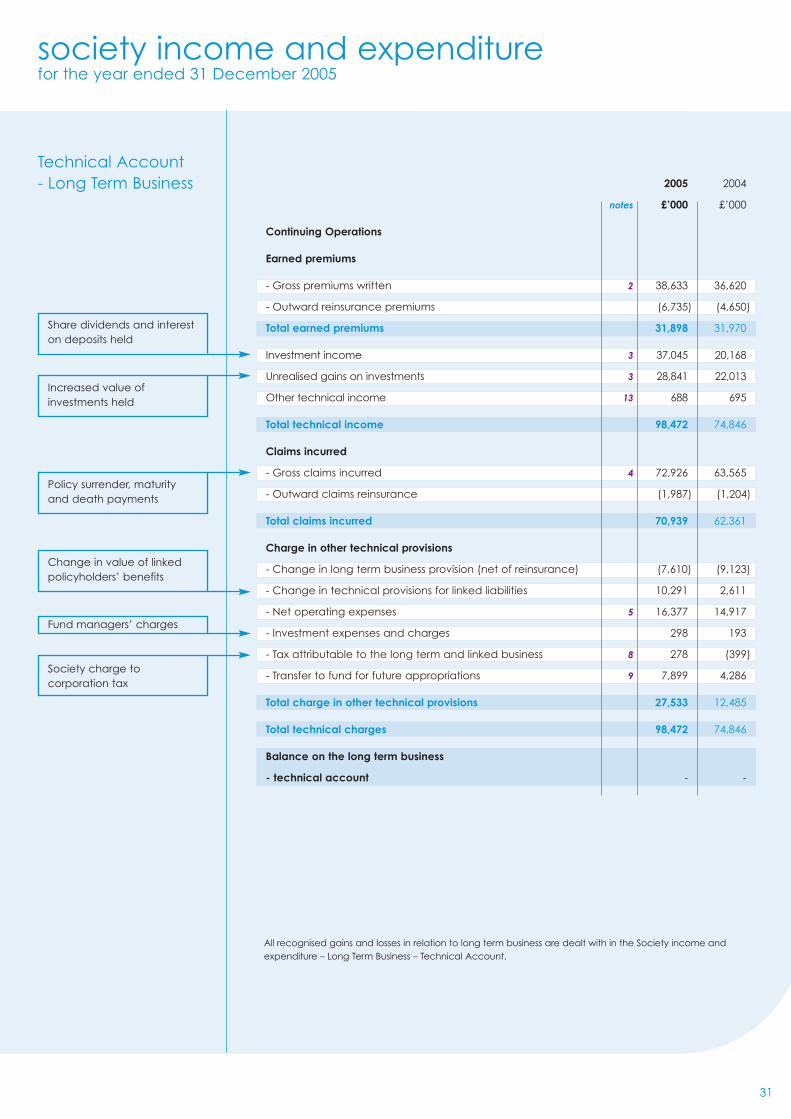

society income and expenditure for the year ended 31 December 2005

Technical Account - Long Term Business

Share dividends and intereston deposits held

Change in value of linkedpolicyholders’ benefits

Society charge tocorporation tax

Policy surrender, maturityand death payments

Increased value ofinvestments held

Fund managers’ charges

2005 2004

notes £’000 £’000

Continuing Operations

Earned premiums

- Gross premiums written 2 38,633 36,620

- Outward reinsurance premiums (6,735) (4,650)

Total earned premiums 31,898 31,970

Investment income 3 37,045 20,168

Unrealised gains on investments 3 28,841 22,013

Other technical income 13 688 695

Total technical income 98,472 74,846

Claims incurred

- Gross claims incurred 4 72,926 63,565

- Outward claims reinsurance (1,987) (1,204)

Total claims incurred 70,939 62,361

Charge in other technical provisions

- Change in long term business provision (net of reinsurance) (7,610) (9,123)

- Change in technical provisions for linked liabilities 10,291 2,611

- Net operating expenses 5 16,377 14,917

- Investment expenses and charges 298 193

- Tax attributable to the long term and linked business 8 278 (399)

- Transfer to fund for future appropriations 9 7,899 4,286

Total charge in other technical provisions 27,533 12,485

Total technical charges 98,472 74,846

Balance on the long term business

- technical account - -

All recognised gains and losses in relation to long term business are dealt with in the Society income andexpenditure – Long Term Business – Technical Account.

32

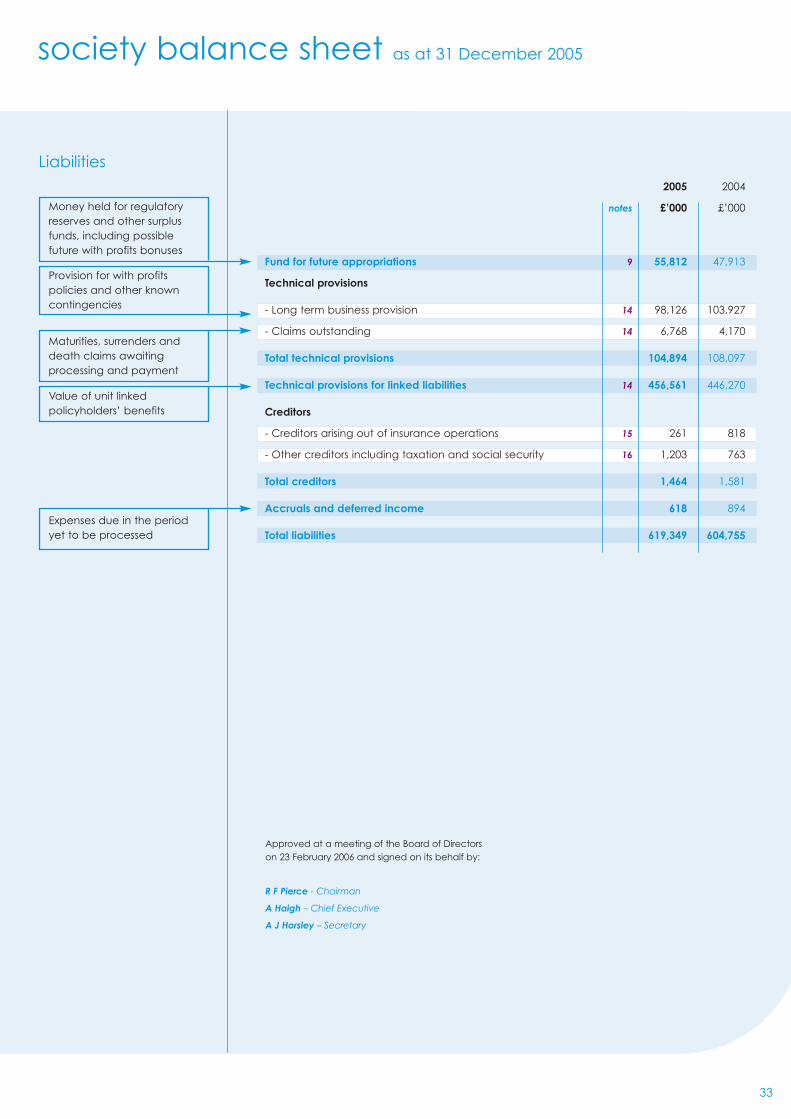

society balance sheet as at 31 December 2005

Assets2005 2004

notes £’000 £’000

Investments

- Investment in land and buildings 10 6,300 6,175

- Financial investments 10 134,359 134,975

Total investments 140,659 141,150

Assets held to cover linked liabilities 11 456,561 446,270

Reinsurers’ share of technical provisions

- Long term business provision 4,604 2,795

Debtors

- Other debtors 7,204 4,072

Other assets

- Cash at bank 3,006 669

Total other assets 3,006 669

Prepayments and accrued income

- Accrued interest and rent 5,772 5,934

- Deferred acquisition costs 859 2,371

- Other prepayments and accrued income 684 1,494

Total prepayments and accrued Income 7,315 9,799

Total assets 619,349 604,755

Harrogate head office andKew Gardens property

With Profits fund and surplusinvestments

Value of unit linkedinvestments

Accumulated sales coststhat are associated withacquiring new policies and are spread over several years

33

society balance sheet as at 31 December 2005

Provision for with profitspolicies and other knowncontingencies

Money held for regulatoryreserves and other surplusfunds, including possiblefuture with profits bonuses

Expenses due in the periodyet to be processed

Value of unit linkedpolicyholders’ benefits

Maturities, surrenders anddeath claims awaitingprocessing and payment

Approved at a meeting of the Board of Directors on 23 February 2006 and signed on its behalf by:

R F Pierce - Chairman

A Haigh – Chief Executive

A J Horsley – Secretary

2005 2004

notes £’000 £’000

Fund for future appropriations 9 55,812 47,913

Technical provisions

- Long term business provision 14 98,126 103,927

- Claims outstanding 14 6,768 4,170

Total technical provisions 104,894 108,097

Technical provisions for linked liabilities 14 456,561 446,270

Creditors

- Creditors arising out of insurance operations 15 261 818

- Other creditors including taxation and social security 16 1,203 763

Total creditors 1,464 1,581

Accruals and deferred income 618 894

Total liabilities 619,349 604,755

Liabilities

notes to the accounts at 31 December 2005

34

basis of presentation The Accounts are prepared on the basis of the accounting policies set out below.The Accounts have been prepared in compliance with the Friendly Societies(Accounts and Related Provisions) Regulations 1994 and with the Association ofBritish Insurers’ Statement of Recommended Practice on Accounting for InsuranceBusiness (“ABI SORP”), dated December 2005. In implementing the requirements ofthese regulations, the Society has adopted a modified statutory solvency basis fordetermining technical provisions. The true and fair override provisions of theCompanies Act 1985 have been invoked in relation to investment properties (seeaccounting policies on Investments below).

The Accounts comply with applicable accounting standards.

basis of consolidationThe Group Accounts comprise the assets, liabilities, and income and expenditureaccount transactions of the Society and its subsidiary undertakings. The ongoingresults of subsidiary undertakings are included within Other Technical Income andOther Technical Charges. The net results are included in the Fund for FutureAppropriations for the Group. The activities of the Society and Group are accountedfor in the income and expenditure – Technical Account.

change of accounting policyFinancial Reporting Standard 17 ‘Retirement Benefits’ (‘FRS 17’) supersedesStatement of Standard Accounting Practice 24 ‘Pension Costs’ (‘SSAP 24’). All thedisclosure requirements of FRS 17 were adopted by the Company in the 2003Accounts. In November 2002, the Accounting Standards Board deferred theeffective date of the recognition and measurement elements of the standard toaccounting periods beginning on or after 1 January 2005. As such the Company hasimplemented the recognition and measurement provisions of FRS 17 in 2005 and hasrestated 2004 comparatives to reflect this.

FRS 17 requires assets in a defined benefit scheme to be measured at their fair valueat the balance sheet date. Scheme liabilities are measured using the projected unitmethod, which takes account of projected earnings increases that are mutuallycompatible and lead to the best estimate of future cash flows. These cash flows arediscounted at the interest rate applicable to high quality corporate bonds of thesame currency and term as the liabilities. The surplus (deficit) in a defined benefitscheme is the excess (shortfall) of the value of the assets in the scheme over(below) the value of the scheme liabilities.

A surplus is recognised as an asset to the extent that the employer is able to recoverthe surplus either through reduced contributions in the future or through refundsfrom the scheme. A deficit is recognised as a liability to the extent of the employer’slegal or constructive obligation to fund it. The current service cost (the increase inthe scheme liabilities arising from employee service in the current period), any pastservice costs (the cost of improvements to benefits for service relating to priorperiods), interest cost (the unwinding of the discount on scheme liabilities) net of theexpected return on scheme assets and actuarial gains and losses (changes in thesurpluses or deficits due to experience of gains and losses) are charged to thetechnical account in other technical income and other technical charges.

1.accounting policies

35

notes to the accounts at 31 December 2005

Under SSAP 24 the income and expenditure charge comprised the cost of accruingbenefits for active employees offset by a credit for the amortisation of the schemesurplus as measured at the last triennial valuation in 2005. A SSAP 24 debtor wasincluded in the balance sheet, relating to contributions in excess of the charge.

The effect of this change of policy on the technical account has been an increasein other technical charges of £132,000 (2004: £194,000). An FRS 17 pension asset of£546,000 (2004: £413,000) has been recognised on the balance sheet and the 2004opening SSAP 24 debtor of £805,000 has been eliminated. The total prior yearadjustment £422,000 reduced the funds for future appropriation as shown in note 9.

premiumsPremiums are credited when they become due. Reinsurance premiums arecharged when they become payable.

claimsDeath claims are recorded on the basis of notifications received. Annuity paymentsare recorded when due. Maturities and surrenders are recorded on the earlier ofthe date when paid or when the policy ceases to be included within the long-termbusiness provision and / or the technical provision for linked liabilities. Reinsurancerecoveries are credited to match the relevant gross amounts.

investment income and expenses

Investment income and expenses include dividends, interest, rents, gains and losseson the realisation of investments and related expenses. Dividends are included asinvestment income on the date that shares become quoted ex-dividend. Interest,rents and expenses are included on an accruals basis.

Realised gains and losses on investments are calculated as the difference betweennet sales proceeds and original cost. Unrealised gains and losses are calculated asthe difference between the valuation of investments at the balance sheet date andtheir original purchase price, or if they have been previously valued, their valuationat the last balance sheet date.

The movement in unrealised gains and losses recognised in the year also includesthe reversal of unrealised gains and losses recognised in earlier years in respect ofinvestment disposals in the current period.