HMS Group 6m 2012 resultsgrouphms.com/upload/grouphms/pdf/Roadshow_12m.pdfHMS at a Glance 4 HMS...

45

HMS Group Investor Presentation, Non-Deal Road-show May, 2013

Transcript of HMS Group 6m 2012 resultsgrouphms.com/upload/grouphms/pdf/Roadshow_12m.pdfHMS at a Glance 4 HMS...

HMS Group

Investor Presentation, Non-Deal Road-show

May, 2013

Agenda

2

WHO WE ARE 3

HMS at a Glance 4

Unique business model 5

INVESTMENT HIGHLIGHTS 6

1. Supportive Industry Fundamentals 7

2. The Leading Provider of Flow Control Solutions 8

2.1 New Milestone projects in the O&G sector 9

3. Focus on Value-added Integrated Solutions 10

4. Operations on Protected Markets in Russia 11

5. Advanced R&D Capabilities 12

6. Well-established Top-tier Customer Base 13

7. Shareholders Run the Business 14

Key Investment Highlights 15

FINANCIAL PERFORMANCE 16

2012 FY Financial Highlights 17

Revenue & EBITDA by Segments 18

Compressor Business Segment 19

Cost analysis 20

Capex & Working Capital 21

Financial Position 22

STRATEGY & OUTLOOK 23

Achievements 2012: Strategy Update 24

Most of 2012 target contracts were signed 25

Backlog development: new record high 26

Selected End-Markets projects for mid-term 27

CONTACTS AND HMS GROUP KEY DETAILS 31

APPENDIX 32

WHO WE ARE

3

HMS at a Glance

4

HMS Group is the leading pump manufacturer and provider of flow control solutions and related services to oil and gas (~80% of revenue), nuclear and thermal power generation and water utility sectors in Russia and the CIS

19 operating facilities in Russia and the CIS with 6 research & development centres, one of the largest pump testing facilities

Growing markets driven by strong investments in oil & gas, power generation and water supply sectors

Unique integrated management, sales and R&D team

The story of resilient financial growth on the back of moderate debt position

Key financials for 2007-2012 Overview

Source: Company data

EPC Oil & gas equipment Industrial pumps

Pump station of the Baltic pipeline system,

Transneft

Example of Oil Pumping Station Oil Pump Station “Tayezhnaya”, Transneft

Design, engineering,

manufacturing, delivery and

installation of pumps and pump

related products

Manufacturing and installation of oil & gas equipment, including modular (pump stations, metering equipment, oil, gas and water processing and preparation units, tanks & vessels, etc.)

Project & design, oil&gas fields infrastructure construction, turn-key projects

Compressors

Twin modular compressor unit

since July 2012

Design, engineering,

manufacturing, delivery and

installation of compressors,

compressor packages and

compressor stations

50% Revenue 68% EBITDA

23% Revenue 22% EBITDA

22% Revenue 8% EBITDA

4% Revenue 1.4% EBITDA

Way of the market consolidator – from pumps to integrated solutions based on advanced R&D capabilities

Significant demand on the key market Leading installed base in Russia Exposure to key growth markets

CAPEX of Russian oil majors 2012-2020F of more than $50 bn Revenue breakdown by industries, 2012 Installed pumps and units

upstream

7%

9%

11%

9%

2% 2% 2%

-1%

1%2%

1%0% 0% 0%

1% 1%

0% 0% 0% 0%

0

100

200

300

400

500

600

2000 2002 2004 2006 2008 2010 2012F 2014F 2016F 2018F 2020F

mn

to

nn

es

Greenfield, 2009-2020F

Traditional oil regions, 2009-2020F

Total production, 2000-2008

Production growth, % YoY

2009–2012

Pump-based Integrated Solutions

2007–2008

Construction

2004–2006

Modular Equipment Design

&

Manufacturing

2003

Pump Design

&

Manufacturing

1993–2002

Pump Trading

Unique Business Model

5

Water Thermal energy midstream

Nuclear energy

Source: Company data Source: Company data Source: REnergyCo, Rosstat

2012 Revenue

Rub 33.7 bn

Pump- and Compressor-based Integrated Solutions

2012–Today

Oil industry

INVESTMENT HIGHLIGHTS

6

Modernization of basic industries, backed by state development programs leads to expenditure on equipment, including specialized pumps

Pumps for water injection, oil refineries and municipal water are expected to demonstrate the highest growth rate

Modest growth in surface pumps for oil and gas industry is largely explained by diminished growth in the segment of pumps for oil transportation due to the completion of major pipeline project (ESPO), after an explosive expansion over 2008-2012

Oil and gas equipment is expected to grow with double-digit rate driven by modernization of the current and development of new oilfields, increase of associated gas utilization ratio, installation of modern metering units

Compressors are expected to grow with CAGR of 16.6% thanks to a number of new pipelines development programs, increase of associated gas utilization ratio

CAGR 11.0%

4,768

1,395

CAGR 17.8%

Supportive Industry Fundamentals

7

4,393

2,727

Pump market revenues in Russia, US mln

Source: Frost & Sullivan research

1

2,137

CAGR 10,0%

1,581

784

O&G equipment market revenues, US mln

CAGR 6.3%

Comments

CAGR

2008-12

CAGR

2012-17E

O&G surface

includes:

Water injection -4,2% 13,6%

Oil transportation 59,5% -12,6%

Oil downstream 12,4% 15,6%

Municipal water -1,6% 16,5%

Power generation 15,0% 10,3%

Total 6,3% 10,0%

940

CAGR

2008-12

CAGR

2012-17E

Pump Stations 1,2% 11,0%

AGMUs 1,0% 10,8%

Associated Gas

Processing &

Transport Units 15,3% 12,2%

Total 4,6% 11,0%

2,215

CAGR

2008-12

CAGR

2012-17E

Oil & Gas

Production and

Transportation 14,4% 17,8%

Gas Processing 11,8% 13,2%

General Service 4,7% 11,4%

Refrigeration -8,1% 16,2%

Total 12,4% 16,6%

Compressor market revenues, US mln

1 575 2 128 2 193

865 1013 1314

2010 2011 2012

HMS Group revenue, Rub mln

Other players Revenue, Rub mln

2,748 2,785 2,664

1,301 1,813 2,009

2010 2011 2012

HMS Group revenue, Rub mln

Other players Revenue, Rub mln

7,395

12,601 14,504

10,057

13,931

15,374

2010 2011 2012

HMS Group revenue, Rub mln

Other players Revenue, Rub mln

Pumps and Oil & gas equipment

Oil and gas industry

The Leading Provider of Flow Control Solutions

Leading market share in key markets

HMS Group has leading positions in almost every key target markets, while over 2012 the Group managed to fruther expand its market share

The Group’s market share in the pumps and equipment for the oil & gas industry the remained flat, with overall growth on par with the market

In the pumps for water utilities and power generation applications, the Group’s managed to outperform market growth thanks to higher revenue from pumps for nuclear application (contracts signed in the previous years) and strong demand for water utilities pumps

Summary

2

Market growth +12% yoy

Source: Company data

Water utilities Power generation

Market growth +1% yoy

Market growth +12% yoy

HMS +11% yoy

HMS +11% yoy

HMS +30% yoy

Industrial pumps only Industrial pumps only

17,452

26,532

4,049 4,598

3,141 2,440

8

4,673

29,878

3,507

Source: Frost & Sullivan report 2009, Transneft website (www.transneft.ru)

Novorossiysk

Moscow

Unecha

Primorsk

Kozmino

Skovorodino

Verkhnechonskoye

Tengiz

Timano-Pechora basin

Caspian Pipeline Consortium expansion (35 MMt, 1,510 km)

Baltic Pipeline System-II (50 MMt, 1,000 km)

ESPO-I and ESPO-I capacity expansion (50 MMt, 2,694 km)

Russia

ESPO-II and ESPO-II capacity expansion (47 MMt, 2,046 km)

Talakanskoye

Purpe-Samotlor (25 MMt, 430 km)

Vankor

Salymskoye

Samotlor

Nizhnevartovsk

Priobskoye

Purpe

Tyamkinskoye

Russkoye

Taishet

Zapolyarnoye-Purpe (45 MMt, 536 km)

Syzran

Tikhoretsk-Tuapse 2 (12 MMt, 295 km)

Haryaga Yuzhny

Khylchuyu

Haryaga-Yuzhny Khylchuyu (8 MMt, 160 km)

Yurubcheno-Tokhomskoe

Yurubcheno-Tokhomskoe-Taishet (18 MMt, 600 km)

Tuapse

Tikhoretsk

Komsomolsky NPZ -port De-Kastry (9 MMt, 313 km)

Oil pipeline projects

Mature oil producing regions

Underdeveloped oil producing regions

Developing oil fields

HMS participation confirmed

Oil products pipeline projects

Komsomolsky NPZ

De-Kastri

“Yug” (South) (9 MMt, 1,465 km)

Komsomolsky NPZ -De-Kastry (n.d., 300 km)

New Milestone Projects in the Oil&Gas sector

Zapolyarnoye

> 3 bn tons of oil reserves to be

developed in the next several

years

Oil production development

> 10,000 km of pipelines to be constructed or

replaced

> 140 of pump stations to be constructed or

reconstructed

> 550 reservoirs with total capacity of almost 10

mln m3 to be reconstructed

Transneft investment program 2010-2017

Iraq

Significant installed base of HMS pumps from Soviet and post Soviet periods

Currently undertaking projects for Oil Ministry and BP

Export markets

26 oil refineries to be

reconstructed & modernized

Oil refining development

9

Trebs & Titov (140 MMt, 2,151 km)

Prirazlomnoye

Taas-Yuryakh

Verkhne-Shapshinskoe

Oil & gas production and oil transportation

Stronger share of integrated solutions in revenue

Focus on Value-added Integrated Solutions

Source: Company data

Advanced R&D is the basis for value-added integrated solutions

10

Standard equipment Integrated solutions & customized pumps

Size Numerous small-size contracts Single large-scale project

Impact of R&D Medium Critical

Technical entry-barriers Medium High

Competition type Price R&D and references

Competition level High Limited

Revenue growth potential Limited High

Revenue downside potential Limited Visibility for at least 1.5 years

Repeat business Very significant Possible

Aftermarket demand Average High

EBITDA margin 10-15% 25-30%

3

Super-blocks X-9001, X-9004 for Vankor oilfield, Rosneft ESPO-1 oil transportation station, Transneft

Examples of successful integrated solutions

25%

30%

1. Project & design works 2. Project management 3. Production of key elements (pump units,

auxiliary equipment) 4. Assembling 5. Testing 6. Disassembling, transportation and

assembling on customer site 7. Supervision, start-up and commissioning 8. Aftermarket services

Industry HMS IGSS Eurasia

Drilling Weir

Flow

serve

Dresser

Rand Sulzer KSB Grundfos Technip Shlumberger

Baker

Hughes

Gea

Grasso

Above

ground

Pum

ps Power generation

Oil and Gas

Water

Oil

&

gas

equip

-

ment Equipment

Repair

EP

C

Project & design

Construction

Com

pre

sso

r

s

Oil up and

midstream

Natural gas

Metals and mining

Under

ground

Serv

ice

Seismic research

Well service

Drilling

Oil product

increase

Operations on Protected Markets in Russia

Source: Company data

4

11

Where we compete…

Russian International

Limited R&D

Small scale of operations

Pump manufacturing is a non-core business for many players (Votkinsk Plant, Uralhydromash, Katasky Plant)

Products are often not in direct competition with HMS product line

Not well-positioned in terms of operational efficiency due to limited scale of operations

No single competitor in all key segments

Global players Lack of local engineering expertise (Weir, KSB, Sulzer, Grundfos, Flowserve)

Lack of references with Russian clients

Not well-positioned in terms of price of products

Chinese players Lack of relevant technologies to produce customized pumps

Lack of references

Inapplicable for mission-critical applications

No brand names

No established relationships with Russian clients

Customized Equipment Standard Equipment

Russian players

Apollo Goessnitz (acquired in 2012) is a center of innovative technologies complying with API standards in pumps for off-shore and oil refinery applications

3. Foreign innovative centers

2. Project and design institutes

Leading project and design facility in Tyumen GTNG - OIL One of the leading Russian institute for water utilities Rostov Vodokanalproekt – WATER One of the leading Russian project and design institute for compressor technologies –

OIL&GAS

12

1. Research & development and engineering centres

Leading pump R&D centers in Russia and CIS: Design office in Livny: advanced R&D works focused on pumps Research Institute VNIIAEN in Sumy: focus on high-speed centrifugal pumps Specialized R&D center in Moscow focused on design of demanding complex

solutions for energy efficient pump systems Neftemash (Tyumen): oil and gas equipment and complex solutions for oil and gas

processing Kazankomressormash (Kazan): compressors and gas processing units with improved

efficiency for natural and associated gas

Tender, pricing and

contract negotiation

1–3 months

Design and production

1–24 months

Delivery and installation

1 month

After-market services

HMS ability to participate in pre-tender preparation stage creates unique competitive advantage

Pre-tender project

preparation

up to 24 months

Advanced R&D Capabilities 5

2011 Revenue

Rub 27.5 bn

2012 Revenue

Rub 33.7 bn

Well-diversified client base of 4,000-6,000 names, stable

growth of revenue coming from small-to-mid clients with

annual purchases below Rub 200 mn

Strong and stable base of “Blue-chip” clients, which includes

the largest oil & gas and energy companies in Russia

HMS Group may have different Top-3 customers for each

period, depending on the particular project mix

Prevailing installed base in the key segments ensures

recurring business growth

Source: Company data * Large client - a client that brings revenue more than Rub 200 mn per period

13

Well-established Top-tier Customer Base 6

Revenue contribution by clients*, 2011-2012 Comments

In 2012, HMS Group sold products and services to

more than 6,000 unique clients, including VOIC,

trade companies, dealers and individual

enterpreneurs

Vladimir Lukyanenko Non-executive Director

Shareholder In company since 2005

Artem Molchanov Managing Director (CEO)

Shareholder In company since 1993

Shareholders Run the Business

The Board is comprised of professionals with significant

experience in flow control and oil and gas industries

It includes founders, who has led HMS since its

inception

HMS is the core business of the largest shareholders

Dividend policy: pay out not less than 25% of profit for

the year

Source: Company data as of May 8, 2012

7

Board of Directors Comments

Shareholders Structure

Kirill Molchanov First Deputy CEO (CFO)

Shareholder In company since 1993

German Tsoy Chairman of the Board

Shareholder In company since 1993

Yury Skrynnik Head of Compressors Business

segment Shareholder

In company since 2005

Nikolay Yamburenko Head of Industrial Pumps

Shareholder In company since 2003

Philippe Delpal Independent

Chairman Audit Committee

Andreas Petrou Non-executive

Gary Yamamoto Independent

Chairman Remuneration Committee

14

Free-f loat28.5%

Vladimir Lukyanenko

27.4%

Managers24.4%

German Tsoy

19.8%

Through H.M.S. Technologies Ltd. (Cyprus)

Key Investment Highlights

15

Supportive Industry Fundamentals 1

The Leading Provide of Flow Control Solutions 2

Operating on Protected Markets in Russia 4

Advanced Research & Development Capabilities 5

Shareholders Run the Business 7

Well-established Top-tier Customer Base 6

Focus on Value-added Integrated Solutions 3

FINANCIAL PERFORMANCE

16

Key financials

4Q’11 4Q’12 chg, qoq 2011 2012 chg, yoy

6,935 10,093 +46% Revenue 27,496 33,656 +22%

2,055 3,279 +60% Gross profit 8,365 10,010 +20%

1,111 2,210 +99% EBITDA 1 5,509 6,231 +13%

665 1,465 +120% Operating profit 4,547 4,237 -7%

434 808 +86% Net income 1 3,377 2,301 -32%

6,408 13,410 +109% Total debt 6,408 13,410 +109%

4,809 12,064 +151% Net debt 2 4,809 12,064 +151%

0.9 1.9 Net debt to EBITDA 0.9 1.9

29.6% 32.5% +286 bps Gross margin 30.4% 29.7% -70 bps

16.0% 21.9% +588 bps EBITDA margin 1 20.0% 18.5% -152 bps

9.6% 14.5% +493 bps Operating margin 16.5% 12.6% -395 bps

6.3% 8.0% +175 bps Net income margin 12.3% 6.8% -544 bps

ROCE 3 32.4% 18.7%

ROE 4 40.9% 18.0%

1 268 1 588 1 545 1 265 1 111 1 367 1 103 1 551 2 210

18,4%

22,5% 22,7%

18,9%

16,0%

18,7%

14,5%

18,0%

21,9%

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

EBITDA, Rub mn EBITDA margin

Financial Highlights

Source: Company data 1 Hereinafter, read EBITDA as EBITDA adjusted, Net income as Profit for the period / year, EBITDA margin as EBITDA adjusted margin 2 Net debt = Total debt – Cash & cash equivalents 3 ROCE = EBIT LTM / average capital employed 4 ROE = total equity period average / profit for the year

17 Source: Company data

6 912 7 051 6 806 6 703 6 935 7 307 7 632 8 624 10 093

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Revenue, Rub mn

Financial highlights, Rub mn

15,64617,066

4,399 4,278

28.1%

25.1%

2011 2012

Revenue Pumps, Rub mn EBITDA Pumps, Rub mn

EBITDA margin Pumps, %

Oil & gas equipment Pumps

Revenue & EBITDA by Segments

Source: Company data

Inflow of small and medium orders as well as a number of large-scale projects resulted in Pumps segment revenue growth

Smaller sales share of high-margin contracts lowered FY 2012 EBITDA and EBITDA margin

18

Revenue +9% EBITDA -3%

Revenue +33% EBITDA +101%

Revenue +23% EBITDA -16%

EPC Compressors

5,900

7,828

6971,397

11.8%17.8%

2011 2012

Revenue OG equipment, Rub mn EBITDA OG equipment, Rub mn

EBITDA margin OG equipment, %

Revenue grew by 33% and EBITDA by 101% compared to 2011, primarily driven by the Vankor project and consolidation of Sibneftemash, acquired in 2011

As a result, EBITDA margin reached 17.8% vs. 11.8% last year

New business segment for HMS Group. In July 2012, HMS Group acquired Kazankompressormash, consolidated in 2H 2012 financial results

Previously KKM hasn’t applied IFRS for it’s financial reporting, and that makes impossible to compare results on yoy basis

1,426

86

6.0%

2011 2012

Revenue Compressors, Rub mn EBITDA Compressors, Rub mn

EBITDA margin Compressors, %

5,946

7,336

563 475

9.5% 6.5%

2011 2012

Revenue EPC, Rub mn EBITDA EPC, Rub mn

EBITDA margin EPC, %

Revenue growth by 23% was driven by new contracts for oilfield infrastructure construction

EBITDA contraction by 16% yoy resulted in lower EBITDA margin, mainly because of GTNG’s margin drop and operating losses caused by challenges with the EPC project at the Srednebotuobinskoye oilfield

Financial results

Since the date of acquisition Revenue of Rub 1,426 mn and EBITDA of Rub 86 mn are included in HMS’ consolidated statement for FY 2012

Year-on-year and quarter-on-quarter comparison is not relevant as HMS applied IFRS accounting principles for KKM reporting since Q3 2012

Operating results

Signed 2 contracts totaled Rub 2 bn for compressor stations (integrated solutions)

Record high 2012 backlog of Rub 2.3 bn and expected strong inflow of new contracts for compressors and based on them integrated solutions

KKM: Half-year with HMS Group

Compressors business segment

19

Main factors of revenue and profitability growth in compressors segment

Acquisition of a compressor design center in April 2013

In April 2013, HMS acquired 61.75% of NIITurbokompressor

Integrated with KKM: the R&D center holds 15.77% of KKM

The largest applied center for compressor technology in Russia and the CIS: 35 testing units, 300 patents, 310 specialist where 3 with doctor degrees and 10 with PhD

80% of KKM’s innovative production is based on design documentation prepared by the institute

Client base consists of Russian major companies, including Gazprom, Lukoil, Rosneft, Sibur, Nizhnekamskneftekhim, NLMK, etc.

Annual revenue of the institute in 2012 was approx. Rub 290 mn

1. Capability to secure large contracts for compressor-based integrated solutions

Current status:

HMS has a strong track record with Russian majors

Contracts signed in August 2012, right following the acquisition of KKM

2. Competences in project & design of a compressor-based integrated solution

– Technical solutions, more profitable for a producer – Strong negotiation power towards suppliers

Current status:

The compressor design center acquired recently

3. Competences in large flow control project management

Current status:

ESPO, Vankor, Turkmenistan

All 3 factors, brought together, should lead to revenue and EBITDA growth in 2014

2011 2012 chg, yoy

Cost of sales 19,131 23,645 +24%

% of revenue 69.6% 70.3%

Supplies and raw materials 9,603 11,767 +23%

% of revenue 34.9% 35.0%

Labour costs 4,045 5,727 +42%

% of revenue 14.7% 17.0%

Cost of goods sold 2,714 2,222 -18%

% of revenue 9.9% 6.6%

Other expenses 2,770 3,930 +42%

% of revenue 10.1% 11.7%

G&A costs grew by 58% mainly due to: Labour costs growth driven by:

1. Rub 200 mn ESPO-linked bonuses paid to the staff related to the project execution (from key managers to sales, engineering and support personnel)

2. Labor related expenses of companies acquired in 2012 3. Planned increase of all personnel salaries

New initiatives in the corporate development – IT-systems unification and export infrastructure development.

G&A costs growth must be assessed together with order intake and backlog performance, which not only hit record high, but also became more diversified

Cost analysis

Source: Company data 20

Cost of sales grew 24% yoy, that is in line with Revenue

Supplies and raw materials up 23% yoy, in line with revenue growth

Labor costs grew by 42% yoy, mainly because of consolidation of acquired in 2012 companies

Increase in expenses, related to construction subcontractors as well as depreciation and amortization, influenced other expenses, resulted in their growth

Distribution and transportation costs grew by 16% in line with revenue

Distribution and transportation expenses hold less share in revenue, 3.7% vs. 3.9% in 2011

The company decreased transportation expenses by 11% yoy thanks to better logistics

Cost of sales Comments

2011 2012 chg, yoy

Distribution & transportation expenses 1,070 1,241 +16%

% of revenue 3.9% 3.7%

Transportation expenses 469 419 -11%

% of revenue 1.7% 1.2%

Labour costs 335 461 +38%

% of revenue 1.2% 1.4%

Insurance 35 36 +2%

% of revenue 0.1% 0.1%

Other expenses 231 325 +41%

% of revenue 0.8% 1.0%

Distribution & transportation expenses

2011 2012 chg, yoy

General & administrative expenses 2,525 3,977 +58%

% of revenue 9.2% 11.8%

Labour costs 1,616 2,619 +62%

% of revenue 5.9% 7.8%

Depreciation & amortization 142 179 +26%

% of revenue 0.5% 0.5%

Audit & consultancy services 133 140 +5%

% of revenue 0.5% 0.4%

Other expenses 633 1,039 +64%

% of revenue 2.3% 3.1%

General & administrative expenses

1 598

+5,725

-174

-2,368

3 184

-8,303

+4,864

1 346

Cash as of Jan 1, 2012

Operating cash flow

before WC changes

WC changes & others

Income tax & interest

paid

Net cash used in

operating activities

Net cash used in

investing activities

Net cash from

financing activities & some adj.

Cash as of Jan 1, 2013

Comments Working capital as of 1 Jan 2013, Rub mn

Cash flow performance in 2012, Rub mn Capital expenditures2 in 2012 vs. 2011

6 029

+2,181

+197 +50

-1,673

6 784

WC 2011 Inventories change

Receivables change & other adj.

Deposits change

Payables & other adj.

WC 2012

Operating cash flow before working capital changes increased to Rub 5.7 bn, compared to Rub 5.2 bn in 2011

Working capital1 amounted to 20% of total revenue, compared to 22% last year

Net working capital decrease led to cash inflow from operating activities of Rub 3.2 bn, compared to net cash outflow of Rub 1.6 bn last year

Organic capex increased to Rub 1.6 bn from Rub 1.2 bn last year, but Capex to D&A ratio decreased to 1.6x

Payments for acquisitions of KKM and Apollo, net of cash acquired, totaled Rub 6.7 bn

CAPEX & Working Capital

Source: Company data

Source: Company data

21

6%

28%

9M 2010 9M 2011

Working capital to Revenue LTM

20%

1 Working capital formals see slide 19 2 Capital expenditures here equals Organic capex = Purchase of PPE + Purchase of intangible assets

Source: Company data

+ +

=

Organic capex (1,623) Rub mn

M&A Capex (6,690) Rub mn

+

1 194 1 623 614 1 026

1,9x

1,6x

2011 2012

Organic capex, Rub mn Depreciation & amortization, Rub mn Capex to D&A ratio, x

6%

28%

9M 2010 9M 2011

Working capital to Revenue LTM

22%

6%

28%

9M 2010 9M 2011

Working capital to Revenue LTM

Working capital to revenue LTM

2 042 3 510 5 753 3 211 208 2 708

2013E 2014E 2015E 2016E 2017E

Debt to be repaid, Rub mn Undrawn credit lines, Rub mn

Short-term debt 13.5%

Net debt grew by 151% yoy, mainly because of HMS’ M&A activities. Also debt was used for working capital needs under execution of current projects

Net Debt to EBITDA LTM ratio reached 1.94x, but this level is much lower than banks’ covenants

Company constantly works on its debt, that led to steady repayment schedule with negligible currency risk and prudent maturity structure

Euro loan was raised to finance the acquisition of Apollo

Successful 10.75% 3-year and 10.1% 5-year Ruble bonds placements, which are cheaper than proposed loans from main Russian banks

Available liquidity of Rub 4.1 bn fully covers 2013E debt repayments

2012 Interest coverage ratio1 equals 3.5

9.4% average interest rate, as of 1 April 2013

In April 2013, Sberbank approved 3 unsecured revolving credit lines, where 2 of them refinance current Rub 2.5 bn credit lines, and 1 is a new Rub 0.7 bn line. HMS plans to sign credit contracts by June 2013

Currency and maturity risks are low Comments

Comfortable repayment schedule

Cash 1,377

S&P corporate credit rating : B+ Outlook: Stable Upgrade on 31 Jan 2013

22 Source: Company data as of 01 April, 2013

Financial position

Source: Company data Source: Company data as of 01 April, 2013

Maturity payment of 3 Rub bn bonds 03

Available liquidity 4.1 Rub bn

Maturity payment of 3 Rub bn bonds 02

Net debt to EBITDA ratio less than 2.00x

2 638 3 455 4 550 4 288 4 809 12 064

1,85

2,10

2,41

1,22

0,87

1,94

2007 2008 2009 2010 2011 2012

Net Debt, Rub mn Net Debt to EBITDA LTM ratio

Fixed rate 99.7%

Floating rate 0.3%

Long-term debt 86.5%

Credits in Rub 89.2%

Euro 8.4%

Others 2.5%

STRATEGY & OUTLOOK

23

Higher margin than stand-alone products and services HMS Group’s largest customers more often prefer to work

with manufacturers that can offer integrated and customized solutions

Creates strong ties with customers, pull-through demand for aftermarket services

Take advantage of positive market trends in existing core markets

Organic expansion into attractive market segments Increase of aftermarket services component to generate

higher-margin and regular cash flows Core export opportunities: water projects in Central Asia,

Rosatom nuclear contracts, O&G in Kazakhstan and Iraq

Leverage leading R&D capabilities in order to develop next-generation customized pumps, technological upgrades and integrated pump systems

Work closely with customers to develop technical policies and standards

Commitment to integration and optimization of current production assets and commitment to increase synergies between acquired businesses

Standardization and continuous improvement of operations and business processes (e.g. ERP, budgeting and reporting methodology and software development, etc.)

Our targets are technology and R&D facilities Pursue acquisition opportunities in high-growth sectors

where HMS has limited presence Search for cost and revenue synergies

Achievements 2012: strategy update

24

Focus on high value-added products

Strengthen position in core markets

Expand R&D capabilities

Improve operational efficiency

Pursue selective and value enhancing acquisitions

2012 EBITDA margin 18.5% on the back of 24%

share of integrated solutions in revenue New contracts for integrated solutions: Vankor

(second stage), ESPO-1 extension, 3 water stations in Turkmenistan, Nuclear contracts.

A number of new material contracts signed thanks to successful delivery on the previous stages, including the follow-up ESPO, Vankor, water stations in Turkmenistan, nuclear pumps for China Nuclear Energy Industry Corporation

Entrance into gas condensate and associated petroleum gas markets (project&design)

Entrance into compressor market

Continued working on new models of pumps and equipment, including high efficiency D-type pump, high-tech feed pump PA 1840-80, innovative measuring equipment Mera MFR, etc.

Start of KKM and Apollo integration Completed integration of Sibneftemash and

Bobruisk Continued Oracle HFM implementation; Continued Infor LN (ERP) installation

Acquisitions of Kazankompressormash: new promising compressor market

Acquisition of Apollo: obtaining a unique engineering expertise and strong product portfolio of pumps for oil refineries and off-shore applications

Strategic Goals Strategic Targets Development in 2012

Project Brief description

Rosneft

Vankor 2 stage Further development. Capex for 2011 US$ 2.6 bn

Yurubcheno-Tokhomsk oilfield Start of oil production in 2016. Oil reserves & resources 513mt

Komsomolskoe, Priobskoe oilfields Achievement of 95% level of associated gas utilization

Bashneft

Trebs and Titov fields JV with Lukoil. Project development stage. Reserves 141 mt. Start of production is expected in 2013. Max capacity 6 mtpa

Transneft

Tikhorestk-Tuapse-2 pipeline Increase of the oil volume delivered to the Tuapse oil refining plant. Length of 247 km and capacity of 12 mtpa. 2 OPSs to be reconstructed

ESPO expansion OPS to be constructed to deliver oil to Khabarovsk and Komsomolsk refineries

Zapolyarye – Pur-pe pipeline Oil transportation from YANAO and Northern Krasnoyarsk region to ESPO pipeline

Yurubcheno-Takhomskoe-Taishet pipeline Oil transportation from Yurubcheno-Tokhomsk and Kuyumbinsk oilfields to ESPO-1. Length ~703 km. Capacity ~15mtpa

TNK-BP

Russkoe oilfield Giant oilfield in YANAO with specific oil. Project production 20 mtpa

Samotlor Further development of an active oilfield in Nizhnevartovsk

Uvat 21 oilfields in Tyumen region

East- and Novo- Urengoy gas & condensate fields

Planned production for 2011 is 3.2bcm

Verkhnechonsk oilfield Oilfield located in the Eastern Siberia, Irkutsk region. Development was stimulated by close proximity of the ESPO pipeline

Gazprom

Shtokman gas and condensate field The field will become a resource base for Russian pipeline gas and liquefied natural gas (LNG) exports to the Atlantic Basin markets

Gazprom neft

Priobskoe oilfield Western Siberia. Recoverable reserves ~600 mt

Kuyumbinskoe oilfield 50/50 w TNK-BP thru Slavneft. Reserves C1 65 mt, C2 151 mt

Sberbank Capital

Dulisma oilfield Irkutsk region. Further development. 3rd resource base for ESPO

Taas-Yuriah oilfield Sakha region. Further development. Total reserves ~130 mt

Refineries Refineries located in Central and Privolzhskiy Federal district

Iraq

Rumaila brownfield Consortium headed by BP

Az Zubair Consortium headed by Eni

Water utilities

Central Asia Irrigation stations for Uzbekistan and Turkmenia

Nuclear

Rosatom Inflow of several contracts for delivery of pumps and pump equipment

CNEIC Pumps for 2 block of Chinese nuclear power plant (China Nuclear Energy Industry Corporation)

Most of 2012 target contracts were signed or won

Priorities for 2012 (filled pink)

25 Sources: Public information, Company’s data Prioritized projects

signed

signed

postponed

signed

signed

signed

signed

signed

postponed

signed

partially postponed

Backlog dynamics in 2010-2012

Backlog development: New Record High

Source: Company data, Management accounts

26

Order intake dynamics in 2010-2012

In Q1 2013, the Group added Rub 9.2 bn (vs. Rub 7.8 bn in Q1 2012, +17% yoy) of orders, mainly consisted of small and mid-size regular orders across different business segment

62 476 646

1 289 1 146 1 387

2 653

4 379 3 780 301

546 2 287

1 373

4 694

4 031

4 519

1 293

7 650

8 910 5 242

1 731 19 106

17 777

21 513

2010 2011 2012

ESPO pumps 8 910 5 242 1 731

Pumps excl ESPO 4 519 1 293 7 650

Oil & Gas equipment 1 373 4 694 4 031

Compressors 301 546 2 287

EPC: Construction 2 653 4 379 3 780

EPC: Project & Design 1 289 1 146 1 387

Others 62 476 646

Total 19 106 17 777 21 513

Total without ESPO 10 196 12 535 19 781

ESPO pumps: old 8 910 5 242 76

ESPO pumps: new 1 655

1 637 611

1 955

1 366 2 198

2 086

2 637

5 533

5 450

450

2 361

3 897

7 832

8 135

7 376

6 597

11 497

12 404

4 626

29 318

23 222

36 110

2010 2011 2012

ESPO pumps 12 404 4 626

Pumps excl ESPO 7 376 6 597 11 497

Oil & Gas equipment 3 897 7 832 8 135

Compressors 450 2 361

EPC: Construction 2 637 5 533 5 450

EPC: Project & Design 1 366 2 198 2 086

Others 1 637 611 1 955

Total 29 318 23 222 36 110

Total without ESPO 16 913 23 222 31 484

ESPO pumps: old 12 404

ESPO pumps: new 4 626

-41% -67%

-71% +491%

+242% -14%

+81% +319%

+65% -14%

-11% +21%

+671% +36%

-7% +21%

+23% +58%

-41% -99%

n/a

n/a n/a

-11% +74%

+101% +4%

n/a +425%

+110% -1%

61% -5%

-63% +220%

-21% +56%

+37% +36%

n/a

n/a

Project Brief description

Rosneft

Komsomolskiy refinery Oil product pipeline from the refinery to De-Kastri harbor. Delivery of pumps and pump units

Yurubcheno-Tokhomsk oilfield Start of oil production in 2016. Oil reserves & resources 513mt. Delivery of pumps and oil&gas equipment

TNK-BP

Russkoe, Tagulskoe and Suzunskoe oilfields Oilfields in Yamal region with specific oil. Assets of TNK-BP. Can be developed using Vankor’s infrastructure. Production start is planned in 2015-2016

Lodochnoe oil-gas condensate field Discovered in Eastern Siberia in 1985. Recoverable oil reserves C1 10.5mt, C2 32.6mt. Next to Vankor. Production engineering in 2013

Uvat 22 oilfields in Tyumen region , including Protozanovskoe and Tyamkinskoe fields. Production 7mtpa in 2012. Planned production 7.5mtpa in 2015

East- and Novo- Urengoy gas & condensate fields

Rospan International project. Total reserves of 2 deposits 890bcm of gas and 133mt of gas condensate. Total development investments US$ 6bn. Current production 3.5bcm. Planned production 8.6bcm in 2015, and 16bcm in 2017

Bashneft

Trebs and Titov fields JV with Lukoil. Project development stage. Reserves C1 142mt. Oil production in 2013 Transneft

ESPO Capacity expansion of ESPO-1 and ESPO-2

Zapolyarye – Pur-pe pipeline Oil transportation from YANAO and Northern Krasnoyarsk region to ESPO pipeline

Modernization of the current pipelines Ongoing inflow of contracts

Yurubcheno-Takhomskoe-Taishet pipeline Oil transportation from Yurubcheno-Tokhomsk and Kuyumbinsk oilfields to ESPO-1. Length ~703 km. Capacity ~15mtpa

Gazprom

Kovyktinskoe gas field Total reserves of gas 1.5trncm and gas condensate 77mt. Currently in exploration program development stage. By 2016 Gazprom plans to shoot 1,300m2 and drill 10 exploration wells

Chayandinskoe oil-gas condensate field Base for creation of Yakutsk gas production center. Reserves of gas 1.2trncm and oil & gas condensate 79mt. Next to Kovyktinskoe field. Commencement planned in 2014 for oil and 2017 for gas. Field infrastructure development 2014-2017

Urengoy oil-gas condensate field The 3rd world largest with gas reserves over 10trncm, located in Tyumen region. Development of oil rims. Production plans in 2015

Mylzhinskoe OGF – Kazan OGCF – Kuybyshev trunk oil product pipeline

Pipeline construction in 2013-2014

South Stream (KMPO) Gas pipeline, which is planned to be laid on the seafloor of the Black sea from Russia to Italy and Austria thru Bulgaria, Balkan Peninsula, and other countries. Construction started in Dec 2012, completion in 2015. Total investments €16bn

Gazprom neft

Novoport (Novy port) field Recoverable reserves C1+C2 230mt of oil and 270bcm of gas. First oil in 2012. Start of year-round production in 2014 at 400-500ktpa. Planned production 6-9mtpa in 2020.

Etypurovskoe field Further development of the field

Iraq

Rumania brownfield Consortium headed by BP

Projects with South Oil Company of Iraq International oil majors

Water utilities

Central Asia Irrigation stations for Uzbekistan and Turkmenia

Russia & the CIS Modernization of outdated equipment

Nuclear

Rosatom Pumps and other equipment for new nuclear power plants and modernization of the old ones

Selected end-market projects for mid-term Our current priorities for 2013 (filled pink)

27 Sources: Public information, Company’s data Prioritized projects

Contacts and HMS Group Key Details

28

Company address:

7 Chayanova Str.

Moscow 125047

Russia

Investor Relations

Phone +7 (495) 730-66-01

http://grouphms.com/shareholders_and_investors/

Twitter HMSGroup and HMSGroup_Rus

Sergey Klinkov, Head of Investor Relations

HMS Hydraulic Machines & Systems Group Plc is listed on the London Stock Exchange (Main market, IOB):

Identifier Number Number of shares outstanding

ISIN US40425X2099 117,163,427

Ticker HMSG

Bloomberg HMSG LI

Reuters HMSGq.L

APPENDIX

29

Consolidated statement of financial position FY 2012

30

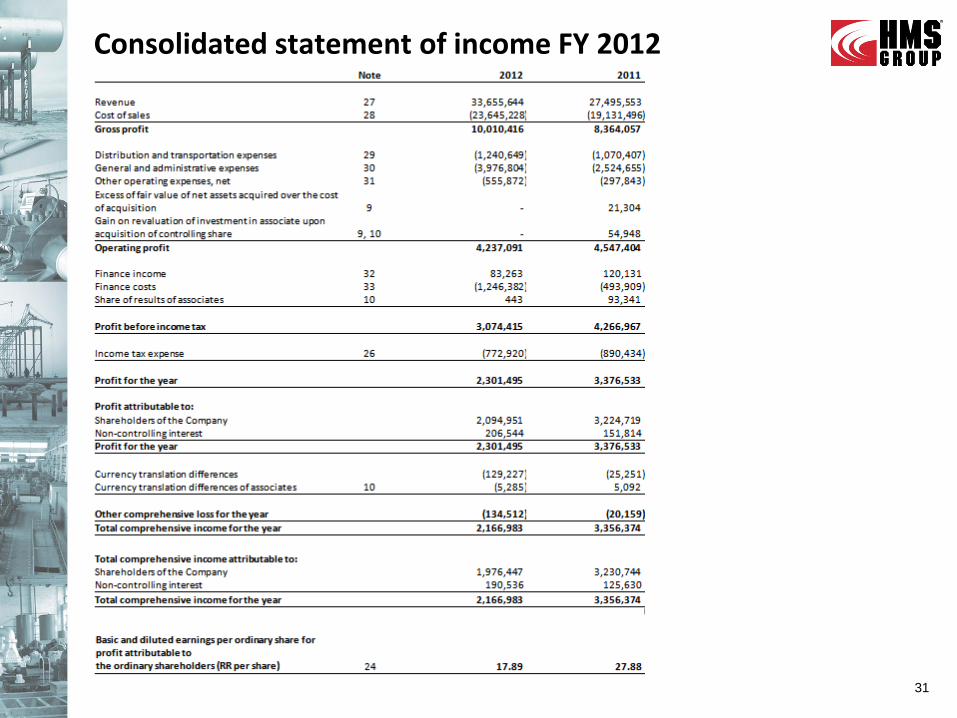

Consolidated statement of income FY 2012

31

Consolidated statement of cash flows FY 2012

32

New Projects

33

34

Russia

China

Kazakhstan

Belarus

Ukraine

India

UAE

Uzbekistan

Turkmenistan

Iraq

Vietnam

Kyrgyzstan

Tajikistan

Export Markets

Central Asia

Recently undertook turnkey construction of pumping station on Amu Darya river in Turkmenistan and construction of pumping station on water-storage basin Arnasai in Uzbekistan

Rapidly growing sales of modular equipment to oil and gas sector in Kazakhstan

Presence in water markets of Tajikistan and Kyrgyzstan

Offices in Ashkhabad (Turkmenistan) and Tashkent (Uzbekistan)

Europe

Office in Milan

Iraq

Significant installed base of HMS pumps, particularly in oil and gas, from Soviet and post Soviet periods

Office in Baghdad diversifies customer base, currently undertakes projects for Oil Ministry and BP

The UAE

Office in Dubai *

Nuclear Exports

Long history of HMS involvement in Rosatom’s foreign as well as domestic projects

International agreements in place for the construction of 19 reactors in China, India, Belarus, Turkey, Ukraine, Armenia, Slovakia, Bulgaria and Vietnam using Russian technology

― Current tenders for development of 16 other reactors worldwide

Source: Company data, media sources Note: * To be opened at 2012

HMS office

Italy Bulgaria

Turkey

TGC-13 (Enisei) Investments 2010-2015: RUB 10 bn

TGC-9 Investments 2010-2015: RUB 28 bn

TGC-8 Investments 2010-2015: RUB 18 bn

TGC-7 (Volga) Investments 2010-2015: RUB 11 bn

TGC-6 Investments 2010-2015: RUB 16 bn

TGC-5 Investments 2010-2015: RUB 14 bn

TGC-3 (Mosenergo) Investments 2010-2015: RUB 39 bn

TGC-14 Investments 2010-2015: RUB 8 bn

TGC-12 (Kuzbas) Investments 2010-2015: RUB 21 bn

TGC-11 Investments 2010-2015: RUB 26 bn

TGC-10 (Fortum) Investments 2010-2015: RUB 47 bn

TGC-4 Investments 2010-2015: RUB 21 bn

TGC-2 Investments 2010-2015: RUB 28 bn

TGC-1 Investments 2010-2015: RUB 73 bn

Source: Frost & Sullivan report 2009

Nuclear Power Plants HMS participation confirmed Projects under construction Planned projects

Leningradskaya-II

Kalininskaya

Rostovskaya

Novovoronezhskaya-II

Beloyarskaya

Kurskaya Smolenskaya

Kolskaya

New Milestone Projects

Rostovskaya

Summary of total investments in power generating capacity

Selected nuclear power plant projects abroad using Russian technology

Number of power units to be

constructed or reconstructed

Additional generation

capacity, MW

Investments 2010-

2015 (RUB bn)

TGC n/a 13,627 359

OGC n/a 11,962 467

Nuclear plants

(Russia) 41 21,500 808

Nuclear plants

(Foreign) 17 17,880 1,940

Name Country No of power units /

Unit capacity (MW)

Investments 2010-

2015 (RUB bn)

Tianwan NPP China 2 / 1,000 86

Kudankulam

NPP India 2 / 1,000 65

Mokhovtse NPP Slovakia 2 / 440 53

Akkuyu NPP Turkey 4 / 1,200 27

Other projects

Ukraine 2 / 1,200

1,581 Belarus 2 / 1,200

Armenia 1 / 1,200

Vietnam 1 / 1,200

35

Baltic

Berezovskaya SDPP

Thermal and nuclear power utilities

Zapolyarnoe-Pur-pe pipeline

Projected Zapolyarnoe–Pur-pe pipeline

Inlet pipelines from main perspective oilfields (with production level over 2mln tons in 2020)

New OPS

Maximum level of pumping capacity by 2020, mtpa

Main OPS – main oil-pumping station of the future Zapolyarnoe-Pur-per pipeline

OPS – oil-pumping station

Legend

Inlet pipelines

Inlet point Oilfield License holder Max capacity in

2020, mt

Main OPS 1 Vostochno-Messoyakhinskoe Slavneft * 10.9

Main OPS 1 Zapadno-Messoyakhinskoe Slvaneft 2.4

Total Main OPS 1 13.3

OPS 2 Russkoe TNK-BP 6.8

OPS 2 Zapolyarnoe Gazprom 2.3

OPS 2 Tazovskoe Gazprom 1.0

OPS 2 Northern Urengoyskoe Gazprom n/a

OPS 2 Salekaptskoe Lukoil 0.3

Total OPS 2 10.9

OPS 3 Urengoyskoe Gazprom 7.4

OPS 3 Pestsovoe Gazprom n/a

OPS 3 En-Yakhinskoe Gazprom n/a

OPS 3 Samburgskoe SeverEnergiya ** 0.2

OPS 3 Yaro-Yakhinskoe SeverEnergiya 0.5

OPS 3 License plot of Western Urengoyskoe TNK-BP 1.1

Total OPS 3 9.7

Total capacity to Pur-pe 34.0-45.0

* TNK-BP and Gazprom Neft have per 50% share ** Gazprom holds 51%; this shareholding should be sold to Novatek

Source: Public sources, Transneft site

Capacity, mtpa up to 45

Total length, km 488

Projected cost, RUB bn 120

Total length of inlet pipelines, km 1,200

Project figures Construction period 2012-2016

1st stage 2014

2nd stage 2015

3rd stage 2016

Implementation

1st stage

2nd stage

3rd stage

36

Kuyumba - Taishet pipeline

Main OPS: Kuyumba

37

OPS 3

OPS 4

OPS 2

Main OPS: Taishet

Capacity, mtpa 15

Total length, km 703

Projected cost, RUB bn 97

Start of project implementation 2012

Completion 2016

Project figures

Krasnoyarsk region

1 2

3 4

ESPO

8

10

5

6

7

11

9

12 13 14

4

3

2

Verkhnechonskoe oil field

Danilovskoe oil field

Dulisminskoe oil field

Talakanskoe oil field

Srednebotuobinskoe oil field

Taas-Yuryakhskoe oil field

Kuyumbinskoe oil field

Yurubcheno-Tokhomskoe oil field 1

Kuyumba - Taishet

Number of new pumping stations for increasing capacity 21

New stations contracted by HMS 3

New station contracted by Turbonasos 1

New stations to be contracted 16

Number of contracted pumping stations 20

Pumping stations under construction by HMS 12

Pumping stations constructed by Sulzer 7

Pumping stations under construction by Turbonasos 2

East Siberia – Pacific Ocean pipeline

Source: Company data, Transneft

Krasnoyarsk region

1 2

3 4 5

6 7

8

9

10

11

12 13 14 15

16 17

18

19

20

23 24

25

26 27

28 29 30

31 32 33

34

35

36

37

38

39

40

41

Buryat region

Chita region

RUSSIA

MONGOLIA

Irkutsk Chita

Ust’-Kut

Yakutsk

Skovorodino

Blagoveschensk

Vladivostok

Taishet

Irkutsk region

Khabarovsk region

Sea of Okhotsk

CHINA

Total number of pumping stations: 41

22 21

38

M&A Policy

39

How we expand acquired businesses

Main rationale: M&A approach

M&A Strategy

40 Source: Company data (RAS accounts)

Sectors: pumps, compressors, oil & gas equipment, project & design

Region: Russia and the CIS

Target revenue within $ 20-100 mn

Strong business model

Friendly management

PUMP PRODUCERS

Broadening of HMS Group’s product portfolio with complementary equipment

Potential growth of revenues and EBITDA margin of acquired companies:

– Sales power and R&D capability of HMS Group

– Well-known brands and/or technical equipment base of acquired companies

Potential growth of revenues and EBITDA margin of the whole Group through integrated solutions

Year

of

acq

uis

itio

n

O&G EQUIPMENT PRODUCERS

Trading Company, established in 2002, is a profit center that represents the Group in a number of large-scale contracts, which are executed by production facilities afterwards

42%

5%

17%

16%

17%

11%

30%

59%

23%

21%

14%

18%

14%

9%

23%

37%

HMS Neftemash

Sibneftemash

Sibna

HMS Pumps

Nasosenergomash

Livnynasos

DGHM

HMS Trading company

2004

2011

2009

2003

2005

2006

2007

2002

Revenue, CAGR %

EBITDA CAGR %

Comments:

• Proven track record of a market consolidator with 21 completed acquisition in Russia, CIS and abroad

• HMS Group expands to adjacent segments seeking complimentary technologies and R&D facilities

• High-growth sectors where HMS has limited presence are the Groups’ focus area

• M&A experience converts to synergies - strong and sustainable double digit annual EBITDA growth after acquisition

CAGR since the acquisition year to 2012

up to

Rub 50 mn

up to

Rub 500 mn

Rub 1-3 bn

Located in Kazan, Russia (~ 800 km from Moscow)

Overall area 420 ‘000 m2, production floor ~127 ‘000 m2

Developed infrastructure near railway and dense in & outbound roads network

Focuses on a gas flow control products and technologies: centrifugal and screw compressors, refrigeration and cooling units (centrifugal compressor-based), couplings, gearboxes, multipliers

Service top Russian players in the basic industries:

In April, the Group additionally acquired the Russian project and design institute ZAO “NIITurbokompressor” (Turbokompressor) located in Kazan, which focuses on centrifugal, rotarary and screw compressors and designs 10-12 of new compressor samples annually

Recent M&A: KazanKomressorMash (KKM)

41

Company description…

Focus shifts to integrated solutions to expand the business

Shift in the strategy: key points of concept 1. One gas pumping station (integrated solution) for the trunk gas pipeline is similar to current annual revenue of KKM in 2011 (around Rub 3bn) 2. There is no “one-stop shop” providers of integrated solutions in Russia with experience similar to HMS (ESPO-1, ESPO-2, Vankor) 3. Revenue of KKM can double based on several successful contracts for compressor stations

Product offering for associated gas, natural gas and basic industries in Russia and CIS…

Revenue 2012 and expectations for 2013

Compressor

Compressor unit

Compressor station

Plan 2013: +32% YoY based on the

current and expected backlog

2 contracts for compressor stations totaled Rub 2 bn were already signed, while HMS keep working on several potential ones

*- Had the acquisition occurred on 1 January 2012, the revenue of KKM would have been Rub 3,066 mn

*

Production Assets

42

Livny

Russia Ukraine

Tomsk

Nizhnevartovsk

Tyumen

Dimitrovgrad

Nizhnevartovskremservice (NRS)

Services: Maintenance and repair of pump equipment, drilling and other oil and gas field equipment

HMS Neftemash

Products: Modular equipment for oil and gas and water industries

Sibneftavtomatika (SibNA)

Products: High-precision measuring equipment for oil, gas and water flow rates

Tomskgazstroy (TGS)

Services: Trunk oil and gas pipeline and auxiliary facilities construction

Sibkomplektmontazhnaladka (SKMN)

Services: Design, construction and commissioning of oil and gas field projects

Rostov Vodokanalproekt (RVKP)

Services: Project design for water utilities

Rostov

Sumy

43

HMS Household pumps

Products: Household vibration pumps

HMS Group

Headquarters

Promburvod (PBV)

Products: Water well submersible pumps

Livnynasos (LN)

Products: Water well submersible pumps

Nasosenergomash (NEM)

Products: Pumps for thermal and nuclear power generation and oil & gas industry

VNIIAEN, associate 47%

Description: R&D center for pumps used in nuclear, thermal power generation, oil and gas industry

Dimitrovgradhimmash (DGHM)

Products: Equipment for oil and chemical industries and pumps for oil refining

HMS Pumps

Products: Industrial pumps for oil and gas, power generation

Giprotyumenneftegaz (GTNG)

Services: Project and construction design of oil and gas facilities

Belarus

Minsk

Moscow Bavleny

Industrial pumps Modular equipment EPC (Construction and Project & design) Compressors

Source: Company data

HMS’ Production Assets

Bobruisk Machine Building Plant (BMBP)

Products: Pumps for oil refining and metals & mining

Bobruisk

Sibneftemash

Products: Tanks and vessels for oil and oilfield service companies

Products: Compressors

Kazan

Kazankompressormash (KKM)

Apollo Goessnitz GmbH

Products: Centrifugal pumps and systems for oil refining

Germany Goessnitz (Thuringia)

Description: R&D center for centrifugal, rotary and screw compressors

NIITK (Turbokompressor)

Calculations

All figures in millions of Russian Rubles, unless otherwise stated

Management of the Group assesses the performance of operating segments based on a measure of adjusted EBITDA, which is derived

from the consolidated financial statements prepared in accordance with IFRS

EBITDA is defined as operating profit/loss adjusted for other operating income/expenses, depreciation and amortization, impairment of

assets, provision for obsolete inventory, provision for impairment of accounts receivable, unused vacation allowance, defined benefits

scheme expense, warranty provision, provision for legal claims, provision for VAT and other taxes receivable, other provisions, excess of

fair value of net assets acquired over the cost of acquisition. This measurement basis excludes the effects of non-recurring income and

expenses on the results of the operating segments

EBIT is calculated as Gross margin minus Distribution & transportation expenses minus General & administrative expenses

Total debt is calculated as Long-term borrowings plus Long-term financial lease liabilities plus Short-term borrowings plus Short-term

financial lease liabilities

Net debt is calculated as Total debt minus Cash & cash equivalents at the end of the period

Working capital is calculated as Inventories plus Trade and other receivables minus Trade and other payables

ROCE is calculated as EBIT LTM divided by Average Capital Employed (total debt + total equity), where EBIT equals Gross profit minus

SG&A, and Total debt equals the above formula

Backlog is calculated as the preceding backlog plus new or additional customer orders booked during the reporting period, less amounts of

contract value booked as revenue under ‘‘Russian GAAP’’ on an unconsolidated basis under the relevant contracts, plus or minus

adjustments made in the judgment of the Group’s management. The Group may also make certain adjustments to bookings to reflect

amendment, expiry or termination of contracts, cancellation of orders, changes in price terms under contracts or orders, or other factors

affecting the amount of potential revenue which the Group believes may be recognized under such contracts. The Group’s backlog

estimates are not an indication of potential revenues. Actual revenues and other measures of financial performance under IFRS may differ

materially from any estimate of backlog, and changes in backlog between periods may have limited or no correlation to changes in revenue

or any other measure of financial performance under IFRS

Notes to the presentation and formulas used for some figures’ calculations

44

The information contained herein has been prepared using information available to HMS Group (“HMS” or

“Group” or “Company”) at the time of preparation of the presentation. External or other factors may have

impacted on the business of HMS Group and the content of this presentation, since its preparation. In addition all

relevant information about HMS Group may not be included in this presentation. No representation or warranty,

expressed or implied, is made as to the accuracy, completeness or reliability of the information.

Any forward looking information herein has been prepared on the basis of a number of assumptions which may

prove to be incorrect. Forward looking statements, by the nature, involve risk and uncertainty and HMS Group

cautions that actual results may differ materially from those expressed or implied in such statements. Reference

should be made to the most recent Annual Report for a description of the major risk factors. This presentation

should not be relied upon as a recommendation or forecast by HMS Group, which does not undertake an

obligation to release any revision to these statements.

This presentation does not constitute or form part of any advertisement of securities, any offer or invitation to

sell or issue or any solicitation of any offer to purchase or subscribe for, any shares in HMS Group, nor shall it or

any part of it nor the fact of its presentation or distribution form the basis of, or be relied on in connection with,

any contract or investment decision.

Disclaimer

45