HMDA: WHAT TO - UBA Conference/Hamilton_HMDA… · 16 ‹# › A D RCE W ORKSHEET. 17 ... When you...

19

© 2015 Temenos USA, Inc. All rights reserved. HMDA: WHAT’S TO COME Leah M. Hamilton Chief Compliance Officer TriComply Services

-

Upload

truongcong -

Category

Documents

-

view

213 -

download

0

Transcript of HMDA: WHAT TO - UBA Conference/Hamilton_HMDA… · 16 ‹# › A D RCE W ORKSHEET. 17 ... When you...

© 2015 Temenos USA, Inc.

All rights reserved.

HMDA: WHAT’S TO COME

Leah M. Hamilton

Chief Compliance Officer TriComply Services

2

WHAT YOU WILL LEARN

Overview of proposed changes

A quick run down

Other proposed changes

You mean there is more?

What do these changes mean to you?

Data collection

Tools to get you started

3

WHERE DO WE STAND?

Is the wait over?

If final rule published by March 31, 2016, earliest

possible effective date is January 1, 2017

Minimum 9-month implementation period

Data submission under new rule earliest date

March 1, 2018

4

OVERVIEW OF PROPOSED CHANGES

Change reporting threshold for all financial institutions

Make 25 or more loans in calendar year required to report

Change transactions subject to reporting

Include all home-secured loans

Include HELOCs, reverse mortgages and business LOCs

Exempt home improvement loans not secured by a dwelling

Require certain large institutions to file reports quarterly

Report at least 75,000 loans annually

Align HMDA data points with other industry data points

Mortgage Industry Standards Maintenance Organization (MISMO)

Change submission of HMDA-LAR info

Web-based data submission

5

OVERVIEW OF NEW INFORMATION TO BE

COLLECTED

Applicant/borrower information

Age, credit score, debt-to-income ratio, reasons for denial, application channel and automated underwriting system results

Property information Construction method, property value, lien priority, number of

individual dwelling units in the property and information about manufactured and multifamily housing

Loan features Pricing information, loan term, interest rate, introductory rate period,

non-amortizing features and type of loan

Unique identifiers Such as loan identifier, property address, loan originator identifier

and legal entity identifier

6

KEY INDUSTRY CONCERN

Privacy

Masked data may not be sufficient

So many personal data fields to release to the public

age

property address

debt-to-income

credit score

mortgage interest rate

7

OTHER PROPOSED CHANGES

Loan purpose

ALL dwelling secured

“Covered Loan”

Open and closed end mortgages

HELOCs, LOCs, reverse mortgages

Dwelling

Clarify when dwelling no longer used as a residence

No RVs or houseboats, even if located in US region that considers them homes

Mobile homes will only be referred to as manufactured homes (consistent with HUD)

5 or more residential units in a mixed use property = residential regardless of allocations for commercial/residential

8

OTHER PROPOSED CHANGES

Financial institution

Non-depository

Home or branch office in MSA

Originated at least (25) closed-end, covered loans

Depository institution

$43 million in assets (adjusted annually)

Home or branch in MSA

Originated at least (1) home purchase or refinance secured by a first lien on a 1-4 dwelling

Federally insured or regulated

Originated at least (25) closed-end, covered loans

9

OTHER PROPOSED CHANGES

Home improvement loan

Must be secured by a dwelling

No more unsecured home improvement loans

Home purchase loans

Assumptions with written agreement that lender accepts

as new borrower obligated on the loan

Manufactured home

References to mobile home will go away

Consistent with HUD definition

10

OTHER PROPOSED CHANGES

Multifamily dwellings

New definition - 5 or more individual dwelling units

Additional information will also be required

Open-end credit

New definition based on Regulation Z

Applies regardless of consumer or commercial borrower or loan purpose

All HELOCs and dwelling secured commercial LOCs

Refinancing

Not limited to prior purchase refinance

One dwelling secured loan satisfying and replacing another dwelling secured loan

Modifications without satisfaction would not be HMDA reportable

11

OTHER PROPOSED CHANGES

Reverse mortgage

Currently reportable if home purchase, home improvement or refinancing

Optional if LOC

Mandatory inclusion

Use definition under Regulation Z

Temporary financing

Designed to be replaced by permanent financing

Except construction loan > 2 years is not temporary

Unimproved land

Vacant land under RESPA is deemed a lien secured by unimproved land under HMDA

12

WHAT DO THESE CHANGES MEAN TO YOU

Small banks – Finally a break!

Costs

Changes to your software systems

Training

Time

Data collection

Data verification/scrub

More room for error

More data = more potential for mistakes

Resubmissions

HMDA Violations

Fair Lending Violations

Public Enforcement Orders

13

DATA COLLECTION

Create a HMDA Worksheet (Handout)

List each data field required to be inputted

Record the information to be inputted in the exact form it is to be inputted (e.g. Purpose of Loan – 1; Action Taken – 3; Reasons for Denial – 3)

Attach any copies from FFIEC Calculator or FFIEC Geocoding (or other vendor)

Benefits

Inputting

Accountability

14 ‹#›

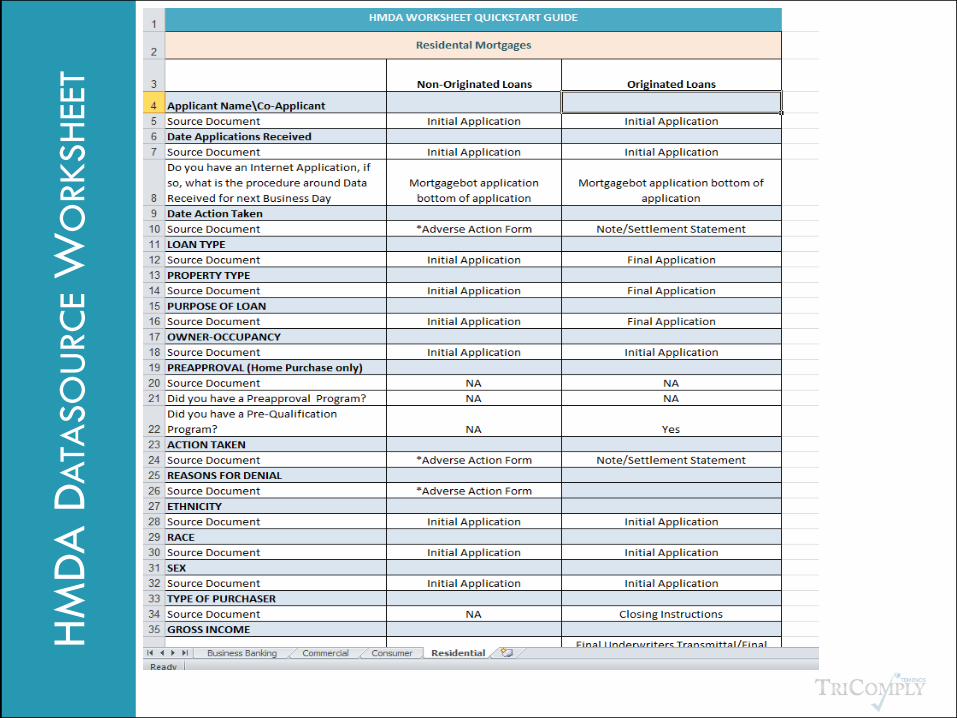

DA

TA C

OLL

ECTI

ON:

HM

DA

WO

RK

SH

EET

15

DATA COLLECTION

Create a HMDA Data Source Worksheet – (Handout)

What are your actual source documents for each data element that must

be captured for HMDA reporting ?

For example: Residential mortgage loan, you use the 1003; GMI information

is located on page 4 of 5

Next, add a column to indicate what source documents have the correct

(and consistent) information

Complete this for each type of application

Residential Mortgage Loans: 1003, GMI, Page 4 of 5

Commercial loans: separate GMI form

16 ‹#›

HM

DA

DA

TASO

URC

E W

ORKSH

EET

17

DATA COLLECTION

Key factors to address in procedures

Who collects the data?

When is it collected?

Where is it stored?

How will it be captured electronically?

Benefits

Minimize errors

Consistency

Examiners

Training

18

DATA COLLECTION

When you downloaded your materials, there was also (1) editable Excel worksheet file for your convenience

HMDA_Excel.xls (filename in downloads)

You will have (5) tabs

(one HMDA data worksheet and four examples of DataSource Worksheets)

HMDA_NewData

DSWks_Consumer

DSWks_Commercial

DSWks_Residential

DSWks_Business Banking

Questions?

![Linear actuators UBA Series and UAL Series · Linear actuators UBA Series SIZE UBA 1 UBA 2 UBA 3 UBA 4 UBA 5 Push rod diameter [mm] 25 30 35 40 50 Outer tube diameter [mm] 36 45 55](https://static.fdocuments.us/doc/165x107/5f11f8c668ca0d412533dd3d/linear-actuators-uba-series-and-ual-series-linear-actuators-uba-series-size-uba.jpg)