HM Treasury Labour Market Conference October 14 2013uctp39a/Blundell HMT Presentation October 14...

50

© Institute for Fiscal Studies What has been driving living standards? Richard Blundell University College London and Institute for Fiscal Studies Thanks to Jonathan Cribb, Wenchao Jin, Robert Joyce and Cormac O’Dea. This research is funded by the ERSC Centre (CPP) at IFS. HM Treasury Labour Market Conference October 14 th 2013

Transcript of HM Treasury Labour Market Conference October 14 2013uctp39a/Blundell HMT Presentation October 14...

© Institute for Fiscal Studies

What has been driving living standards?

Richard Blundell University College London and Institute for Fiscal Studies

Thanks to Jonathan Cribb, Wenchao Jin, Robert Joyce and Cormac O’Dea.

This research is funded by the ERSC Centre (CPP) at IFS.

HM Treasury Labour Market Conference October 14th 2013

Outline I will look (briefly) at Incomes, Earnings and Consumption

All three measures have something important to say.

1. Incomes: Working-age and Pensioners 2. Earnings: Wage Changes, Employment and Productivity 3. Consumption: Durable and Non-durable Expenditures 4. Prospects

Under each heading some summary points and supporting evidence.

Draw on three references to recent IFS research: Ø Living Standards, Poverty and Inequality in the UK.

– IFS Report R81, http://www.ifs.org.uk/comms/r81.pdf

Ø What Can Wages Tell Us about the Productivity Puzzle? – IFS Working Paper, W13/11; forthcoming Economic Journal, http://www.ifs.org.uk/wps/

wp201311.pdf

Ø Household Consumption through Recent Recessions. – Fiscal Studies, 34(2), June 2013,

http://onlinelibrary.wiley.com/doi/10.1111/j.1475-5890.2013.12003.x/abstract

© Ins&tute for Fiscal Studies

1. Incomes • Leading up the recession:

• income growth had slowed in early 2000s. • pensioners/ working-age childless were doing relatively well/

badly

• During recession and immediately afterwards: • real earnings for those in work fell; benefits/tax credit

incomes were robust. • employment rates fell for young adults but not for older

ones. • As a result:

a) income inequality fell (despite rise in earnings inequality among workers)

b) young adults did worst; pensioners did best (again)

© Ins&tute for Fiscal Studies

-‐1.0%

-‐0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

10 20 30 40 50 60 70 80 90 Average an

nual re

al income chan

ge Parents and children

Working-age without children

Pensioners

Percentile point

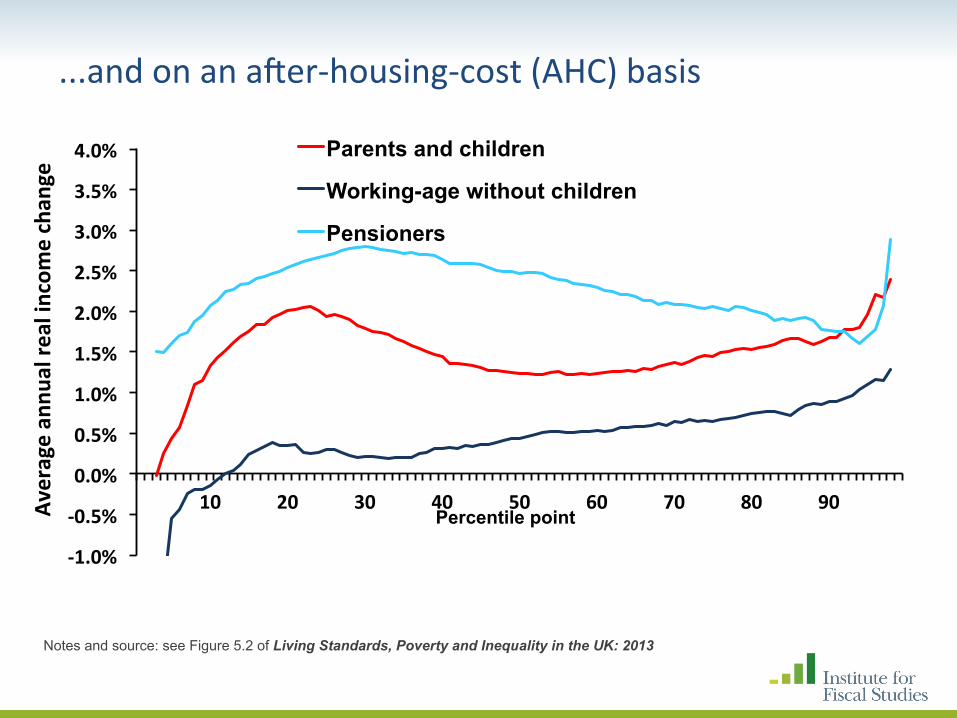

1996-‐97 to 2011-‐12: pensioners did rela&vely well; working-‐age childless rela&vely badly

Notes and source: see Figure 5.2 of Living Standards, Poverty and Inequality in the UK: 2013

-‐1.0%

-‐0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

10 20 30 40 50 60 70 80 90 Average an

nual re

al income chan

ge Parents and children

Working-age without children

Pensioners

Percentile point

...and on an aFer-‐housing-‐cost (AHC) basis

Notes and source: see Figure 5.2 of Living Standards, Poverty and Inequality in the UK: 2013

Trends not uniform: slower growth from early 2000s

100

105

110

115

120

125

1997–98=100

Mean income Median Income

© Ins&tute for Fiscal Studies

Source: Family Resources Survey, various years

Trends not uniform: slower growth from early 2000s

100

105

110

115

120

125

1997–98=100

Mean income Median Income

© Ins&tute for Fiscal Studies

Source: Family Resources Survey, various years

... and large falls aFer the recession

100

105

110

115

120

125

1997–98=100

Mean income Median Income

© Ins&tute for Fiscal Studies

Source: Family Resources Survey, various years

© Ins&tute for Fiscal Studies

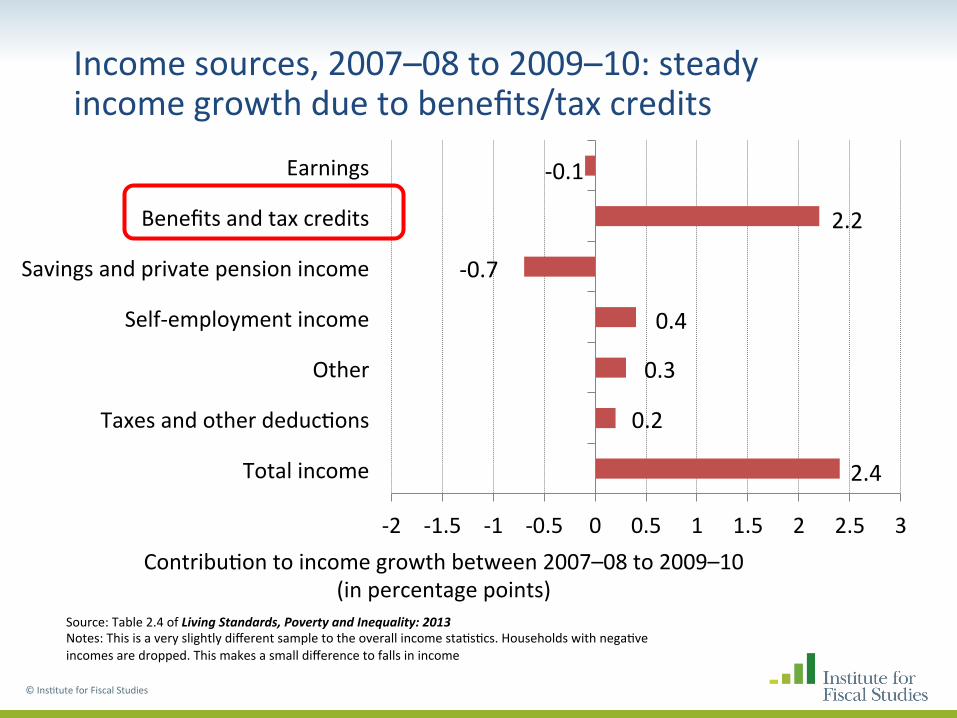

Source: Table 2.4 of Living Standards, Poverty and Inequality: 2013 Notes: This is a very slightly different sample to the overall income sta&s&cs. Households with nega&ve incomes are dropped. This makes a small difference to falls in income

Income sources, 2007–08 to 2009–10: steady income growth due to benefits/tax credits

-‐2 -‐1.5 -‐1 -‐0.5 0 0.5 1 1.5 2 2.5 3

Total income

Taxes and other deduc&ons

Other

Self-‐employment income

Savings and private pension income

Benefits and tax credits

Earnings

Contribu&on to income growth between 2007–08 to 2009–10 (in percentage points)

-‐0.1

0.4

0.3

0.2

2.4

2.2

-‐0.7

© Ins&tute for Fiscal Studies

Source: Table 2.4 of Living Standards, Poverty and Inequality: 2013 Notes: This is a very slightly different sample to the overall income sta&s&cs. Households with nega&ve incomes are dropped. This makes a small difference to falls in income

Income sources, 2009–10 to 2011–12: large income falls due to falling earnings

-‐10 -‐8 -‐6 -‐4 -‐2 0 2 4

Total income

Taxes and other deduc&ons

Other

Self-‐employment income

Savings and private pension income

Benefits and tax credits

Earnings

Contribu&on to income growth between 2009–10 to 2011–12 (in percentage points)

-‐5.7

-‐2.0

-‐0.4

2.4

-‐7.5

-‐1.0

-‐0.7

© Ins&tute for Fiscal Studies

Source: Table 2.4 of Living Standards, Poverty and Inequality: 2013 Notes: This is a very slightly different sample to the overall income sta&s&cs. Households with nega&ve incomes are dropped. This makes a small difference to falls in income

Income sources: 2007–08 to 2011–12

-‐10 -‐8 -‐6 -‐4 -‐2 0 2 4

Total income

Taxes and other deduc&ons

Other

Self-‐employment income

Savings and private pension income

Benefits and tax credits

Earnings

Contribu&on to income growth between 2007–08 to 2011–12 (in percentage points)

-‐5.9

-‐1.6

-‐0.1

2.7

-‐5.3

1.2

-‐1.5

-‐12.0%

-‐11.0%

-‐10.0%

-‐9.0%

-‐8.0%

-‐7.0%

-‐6.0%

-‐5.0%

-‐4.0%

-‐3.0%

-‐2.0%

-‐1.0%

0.0% 10 20 30 40 50 60 70 80 90

Cumula>

ve re

al cha

nge Percentile point

Weekly earnings inequality (among workers) rose between 2007-‐08 to 2011-‐12...

Notes and source: see Figure 3.10 of Living Standards, Poverty and Inequality in the UK: 2013

Note: towards bottom, much driven by falls in hours worked

(not falls in hourly wages)

...but net result was s&ll a fall in income inequality

© Ins&tute for Fiscal Studies

-12%

-8%

-4%

0%

4%

8%

10 20 30 40 50 60 70 80 90

Inco

me

chan

ge

2007–08 to 2009–10 2009–10 to 2011–12 2007–08 to 2011–12

Percentile point

Source: Figure 3.5 of Living Standards, Poverty and Inequality: 2013

Median income changes by age (BHC, GB)

Notes and source: see Figure 5.7 of Living Standards, Poverty and Inequality in the UK: 2013

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

0s 10s 20s 30s 40s 50s 60s 70s

Aver

age

annu

al g

row

th

2007–08 to 2011–12 2001–02 to 2007–08

Age

2. Earnings: Wages and Employment

• Average real hourly wages fallen since this recession began. – Why and will the trend continue?

• ‘Effective labour supply’ is higher now than during previous recessions, due (perhaps) to welfare policy changes and wealth shocks, – increasing in the long-run (due to social and policy changes) and in the

short-run (due to wealth shocks and long term real wage declines).

• Workforce composition has shifted towards more productive types, – as in previous recessions, yet real wages have fallen.

• These real wage falls have occurred within individuals: – unprecedentedly high proportions of employees experienced nominal

wage freezes, – especially in the lower-middle of the wage distribution and in the

absence of collective agreements.

© Ins&tute for Fiscal Studies

In contrast to previous recessions, real output per hour has at best been stagnant since 2008: why?

90

95

100

105

110

115

120

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Quarter since the labelled one

Real output per hour

1979Q4 1990Q2 2008Q1 Linear trend (90Q2-‐08Q1)

Average real hourly wages have also been stagnant

95

100

105

110

115

120

0 1 2 3 4 5 6

Real hou

rly wage (first y

ear o

f recession = 100)

Years since the year in which the recession began

Average real male hourly wage (using GDP deflator)

1979 1990 2008 Linear trend 1990-‐2008

The UK is different.....

0.85

0.9

0.95

1

1.05

1.1

1.15

2007 2008 2009 2010 2011 2012

UK, GDP per hour

US, GDP per hour

France, GDP per hour

Germany, GDP per hour

UK, average wage

US, average wage

France, average wage

Germany, average wage

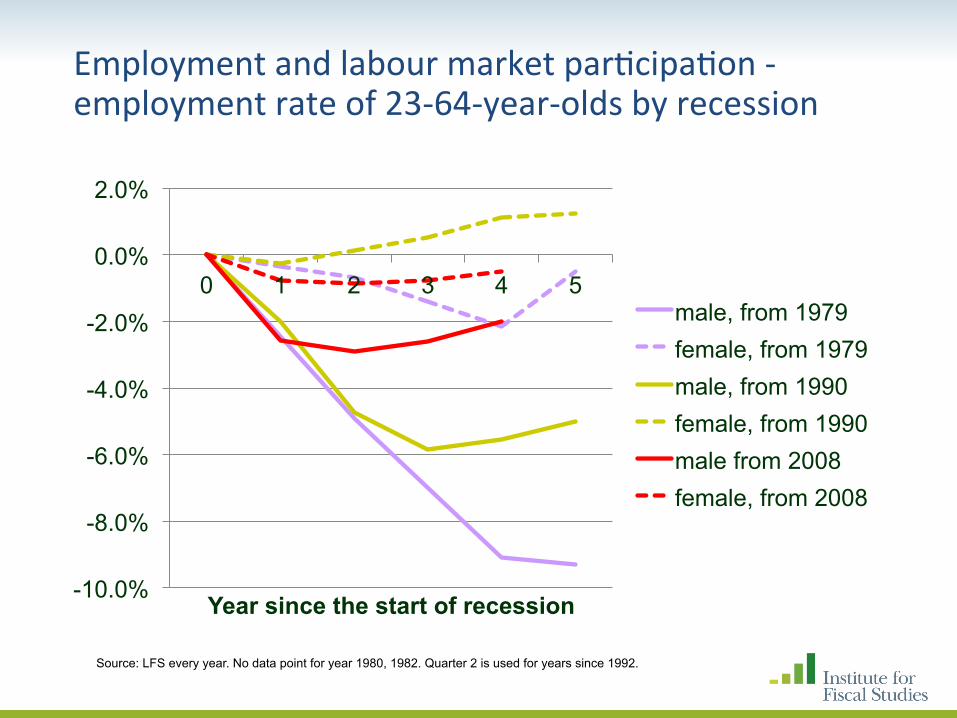

Employment and labour market par&cipa&on

• Labour market par&cipa&on has held up beier during this recession than previous ones. For example: – Employment rates fell less (and unemployment rates increased

less)

Employment and labour market par&cipa&on -‐ employment rate of 23-‐64-‐year-‐olds by recession

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

0 1 2 3 4 5

Year since the start of recession

male, from 1979 female, from 1979 male, from 1990 female, from 1990 male from 2008 female, from 2008

Source: LFS every year. No data point for year 1980, 1982. Quarter 2 is used for years since 1992.

Change to the propor&on of 23-‐64-‐year-‐olds who are unemployed by recession

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0 1 2 3 4 5

male, from 1979

female, from 1979

male, from 1990

female, from 1990

male from 2008

female, from 2008

Source: LFS every year. No data point for year 1980, 1982. Quarter 2 is used for years since 1992.

Employment and labour market par&cipa&on

• Some increase of par&cipa&on can be aiributed policy changes, e.g. : – Labour supply has increased among lone parents as a result of

job search condi&ons aiached to benefit claims

– Older workers are re&ring later as a result of increased SPA for women

Change to lone mothers’ par&cipa&on rate since policy change

-‐8% -‐6% -‐4% -‐2% 0% 2% 4% 6% 8% 10% 12% 14%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Quarter since the last quarter before policy change

youngest kid 12-‐15, 2008Q3 youngest kid10-‐11, 2009Q3

youngest kid 7-‐9, 2010Q3 youngest kid 5-‐6, 2011Q3

Impact of SPA increase for women on employment

30%

35%

40%

45%

50%

55%

60%

Counterfactual male 60-‐64 employment rate

LFS employment rate 60-‐64 men

Counterfactual female 60-‐64 employment rate

LFS employment rate 60-‐64 year old women

Note: counterfactual employment rates are estimated. See Cribb et al (2013) “Incentives, shocks or signals: labour supply effects of increasing the female state pension age in the UK”

Employment and self-‐employment rate of older people

-‐10%

-‐8%

-‐6%

-‐4%

-‐2%

0%

2%

4%

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

2011Q3

2012Q1

2012Q3

2007Q4 = 0

employment rate 60-‐74 male self-‐employment rate 60-‐74 male

employment rate 60-‐74 female self-‐employment rate 60-‐74 female

Employment status of 16-‐22-‐year-‐olds

0%

10%

20%

30%

40%

50%

60%

70%

80% % in work % unemployed

Source: LFS 2nd

quarter every year

Employment and labour market par&cipa&on

• There is also some (weak) evidence that par&cipa&on amongst older people has increased as a result of shocks to housing or financial wealth § But probably a response to falling expected real wages too.

Can changes in the composi&on of the workforce explain the fall in real hourly wages?

• Short answer: no – unlike, to an extent, in other countries.

• As in previous recessions, the composi&on of the workforce shiFed towards more produc&ve workers, – hence we would have expected the average real wage to increase

(other things being equal).

• What has been different in this recession is that the returns to those characteris&cs have fallen substan&ally.

• This is true even amongst workers who keep their jobs, who have experienced nominal wage freezes/real wage falls, – May have been facilitated by the reduced power of labour market

ins&tu&ons (e.g. unions) since previous recessions.

Average real hourly wage by age group (RPI deflated)

0

2

4

6

8

10

12

14

16

18

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

16-‐17

18-‐25

26-‐35

36-‐45

46-‐55

56-‐64

65+

Average real hourly wage by qualifica&on among young people

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

18-‐21, GCSEs or above

18-‐21, no GCSEs or equilvants

22-‐24, degree or above

22-‐24, GCSEs, no degrees

22-‐24, no GCSEs

NEET rate among young people

0%

10%

20%

30%

40%

50%

60%

18-‐21, GCSEs or above

18-‐21, no GCSEs or equilvants

22-‐24, degree or above

22-‐24, GCSEs, no degrees

22-‐24, no GCSEs

%change to real hourly wage since last year, by period

% facing nominal wage freeze in the coming year by current wage quintile

0%

2%

4%

6%

8%

10%

12%

14%

16% 1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Lowest-‐paid 20% 2nd quin&le 3rd quin&le 4th quin&le Highest-‐paid 20%

Source: New Earnings Survey Panel Dataset 1975-‐2011. There are 20,000-‐30,000 observa&ons underlying each data point.

More nominal pay freezes in the absence of collec&ve agreement since 2008

3. Consumption

• Expenditure falls have been deeper than in previous recessions. – Note that the start of the fall is coincident with the fall in GDP (not

income).

• Unusually expenditure on consumer nondurables has fallen most – Especially among the young and to some extent among the middle

aged. Less for the old.

– Temporary VAT reduc&on?

© Ins&tute for Fiscal Studies

Non-‐ and semi-‐durables

© Ins&tute for Fiscal Studies

90

92

94

96

98

100

102

104

106

108

110

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Chan

ge since be

ginn

ing of re

cessions (q

uarter

prior to recession = 100)

Quarters since beginning of recession

1980

1990

2008

Durables

© Ins&tute for Fiscal Studies

80

85

90

95

100

105

110

115

120

125

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Chan

ge since be

ginn

ing of re

cessions (q

uarter

prior to recession = 100)

Quarters since beginning of recession

1980

1990

2008

Components of GDP

© Ins&tute for Fiscal Studies

-‐20

-‐15

-‐10

-‐5

0

5

10

15

Chan

ge since 2008 Q1 (£b) Net exports

Govt. purchases

Consumer durables

Nondurable consump&on

Corporate investment

Propor&onate Fall in Each Component

© Ins&tute for Fiscal Studies

65

70

75

80

85

90

95

100

105

110

Chan

ge since 2008 Q1 (2008 Q1 = 100)

Govt. purchases

Consumer durables

Nondurable consump&on

Corporate investment

Consumption

• Homeowners have made the largest cuts. – In past recessions there was liile difference between owners and renters.

• Saving ra&os are lower than during the early 1980s and early 1990s – but haven risen drama&cally since 2008 (and pension contribu&ons higher).

• The data points to an expecta&on of a permanent fall in living standards, – especially among the young and middle-‐aged.

© Ins&tute for Fiscal Studies

4. Summary and … Prospects …

• What has driven living standards?

• Changes in the labour market are a key factor behind the changes, – especially for younger families/singles rela&ve to pensioners.

• Real wages and employment tell much of the story. Benefit changes have also been important drivers. – the poor employment and earnings performance of young adults

maps into big falls in their incomes rela&ve to older workers.

• The con&nued catch-‐up of pensioners rela&ve to working-‐age adults is in large part due to the sharp falls in real earnings and rela&vely robust benefit rates.

© Ins&tute for Fiscal Studies

Simula&ons up to 2015–16

© Ins&tute for Fiscal Studies

-8%

-6%

-4%

-2%

0%

2%

10 20 30 40 50 60 70 80 90

Inco

me

chan

ge

2007–08 to 2011–12 2011–12 to 2015–16 2007–08 to 2015–16

Percentile point

Note: Figure taken from Brewer et. al. (2013), Fiscal Studies, Vol. 34, No. 2, June 2013, Vol. 34, No. 2, pp. 179–201. Published before the latest HBAI release. The 2011–12 income distribu&on is therefore a simula&on, but is extremely similar to the actual data.

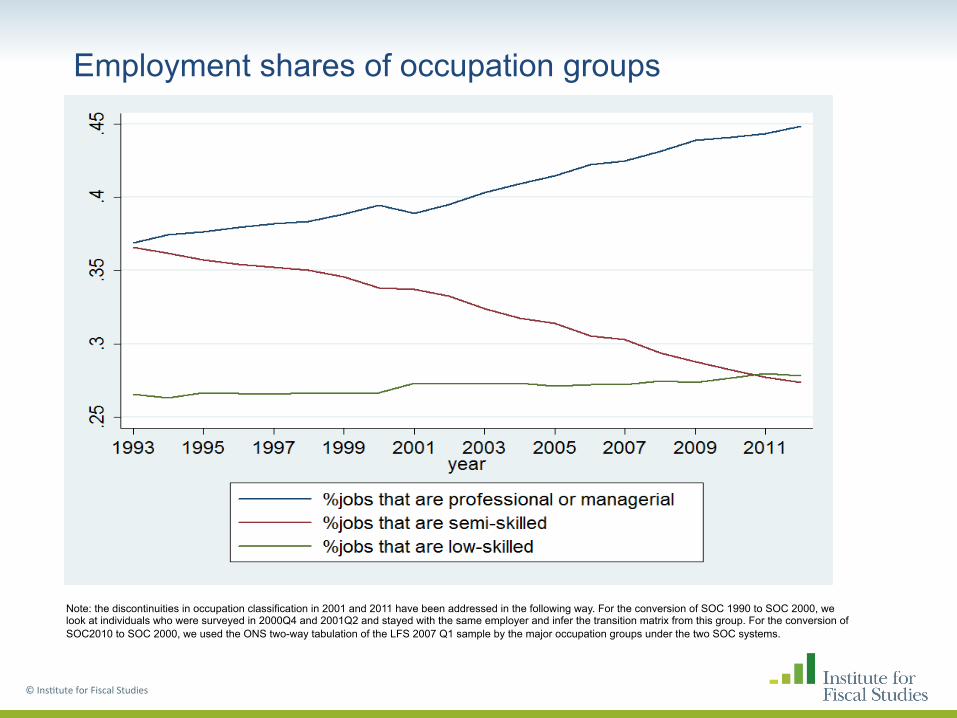

Employment shares of occupation groups

© Ins&tute for Fiscal Studies

Note: the discontinuities in occupation classification in 2001 and 2011 have been addressed in the following way. For the conversion of SOC 1990 to SOC 2000, we look at individuals who were surveyed in 2000Q4 and 2001Q2 and stayed with the same employer and infer the transition matrix from this group. For the conversion of SOC2010 to SOC 2000, we used the ONS two-way tabulation of the LFS 2007 Q1 sample by the major occupation groups under the two SOC systems.

(RPI deflated) Real wages by occupation group since 1993

© Ins&tute for Fiscal Studies

Note: the low-skilled wage would end up around the 1993 level if we use CPI instead of RPI. Each log wage series is normalized to 0 in 1993.

Prospects - I • Younger workers and families are ac&ng as if they expect a long-‐run fall

in rela&ve living standards – evidence from consump&on and saving.

• Real wages, produc&vity and capital investment have slow to pick up – we can expect the paiern of lower real wages to con&nue, but with fairly

buoyant employment due to increased supply.

• Most falls in real earnings have happened (but low/no real growth) – fiscal contrac&on implies >£20 bn year of benefit cuts by end of this parliament

– trends by age maybe more durable, e.g. pensioner benefits protected

• The number of rou&ne jobs near the middle of the earnings distribu&on has declined steadily &ll 2009 – more jobs are now professional or managerial. In the late 90s to early 2000s, wages

grew fast for high (and mid-‐skilled) occupa&ons, but this slowed down around 2003 and real wages fell since 2009.

• Suggests longer term earnings growth will mostly come from high-‐skilled occupa&ons, with some at the very boiom.

Prospects - II • But s&ll much to do in focussing on older workers in general, on return

to work for parents/mothers, and on entry into work.

• There are s&ll some poten&al big gains here, – for example, as (higher skilled) women age in the workforce.

• Tax/welfare reforms to enhance earnings (from Mirrlees): – refocus incen&ves towards transi&on to work, return to work for lower

skilled mothers and on enhancing incen&ves among older workers.

• Produc&vity is s&ll the key, – (financial) capital misalloca&on and poten&al investment returns.

• Human capital and ‘on the job’ wage/produc&vity complementarity – note the rela&ve importance of mismatch of entry skills in the recession.

• Produc&vity and wages are closely related but note recent growth in the wedge between labour costs and hourly wages, – the growing importance of pensions and NI in the UK,

– what will the trends in this wedge look like?

Employer contribu&ons to pension funds – in constant prices terms

Source: Office for National Statistics Notes: Data for Q4 2012 is not yet published so has been estimated based on Q4 2011 to Q3 2012 data

Prospects - II • But s&ll much to do in focussing on older workers in general, on return

to work for parents/mothers, and on entry into work.

• There are s&ll some poten&al big gains here, – for example, as (higher skilled) women age in the workforce.

• Tax/welfare reforms to enhance earnings (from Mirrlees): – refocus incen&ves towards transi&on to work, return to work for lower

skilled mothers and on enhancing incen&ves among older workers.

• Produc&vity is s&ll the key, – (financial) capital misalloca&on and poten&al investment returns.

• Human capital and ‘on the job’ wage/produc&vity complementarity – note the rela&ve importance of mismatch of entry skills in the recession.

• Produc&vity and wages are closely related but note recent growth in the wedge between labour costs and hourly wages, – the growing importance of pensions and NI in the UK,

– what will the trends in this wedge look like?

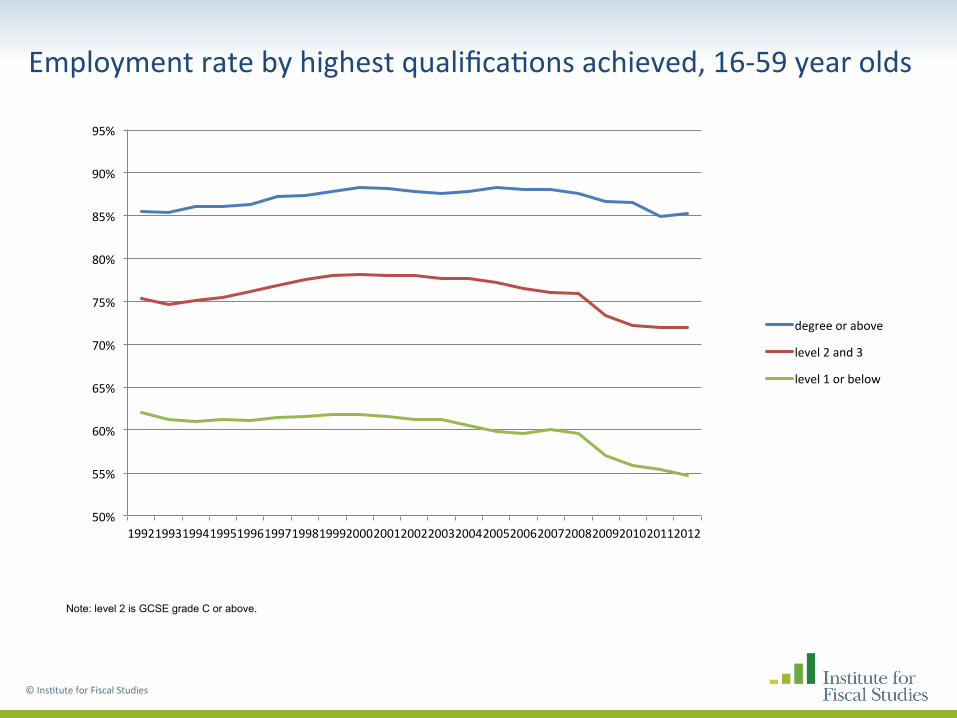

Employment rate by highest qualifica&ons achieved, 16-‐59 year olds

© Ins&tute for Fiscal Studies

Note: level 2 is GCSE grade C or above.

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

degree or above

level 2 and 3

level 1 or below

Par&cipa&on rates over &me

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0%

100.0%

23-64, male 23-64, female 65-84, male 65-84, female