Highlights of amendments to Schedule III and CARO

24

Highlights of amendments to Schedule III and CARO CA Ruta Chitale 14.07.2021

Transcript of Highlights of amendments to Schedule III and CARO

Highlights of amendments to Schedule III and CAROCA Ruta Chitale

14.07.2021

Schedule III of CA Act, 2013

Schedule III – General Instructions For Preparation of BalanceSheet and Statement of Profit & Loss of the Company (Format!)

In addition to the disclosure requirements of AS and not assubstitution

Amendments : in three parts Division I : FS where AS are need to be complied with

Division II: FS where Ind-AS are need to be complied with

Division III: Specific to NBFC’s

Purpose of these amendments is ‘Alignment to CARO’

Applicability: FY 2021-22 but comparative figures of FY 2020-21

Division I

26 areas of change

General disclosure:

- Round Off

- Shareholding of Promoter (!) to be disclosed

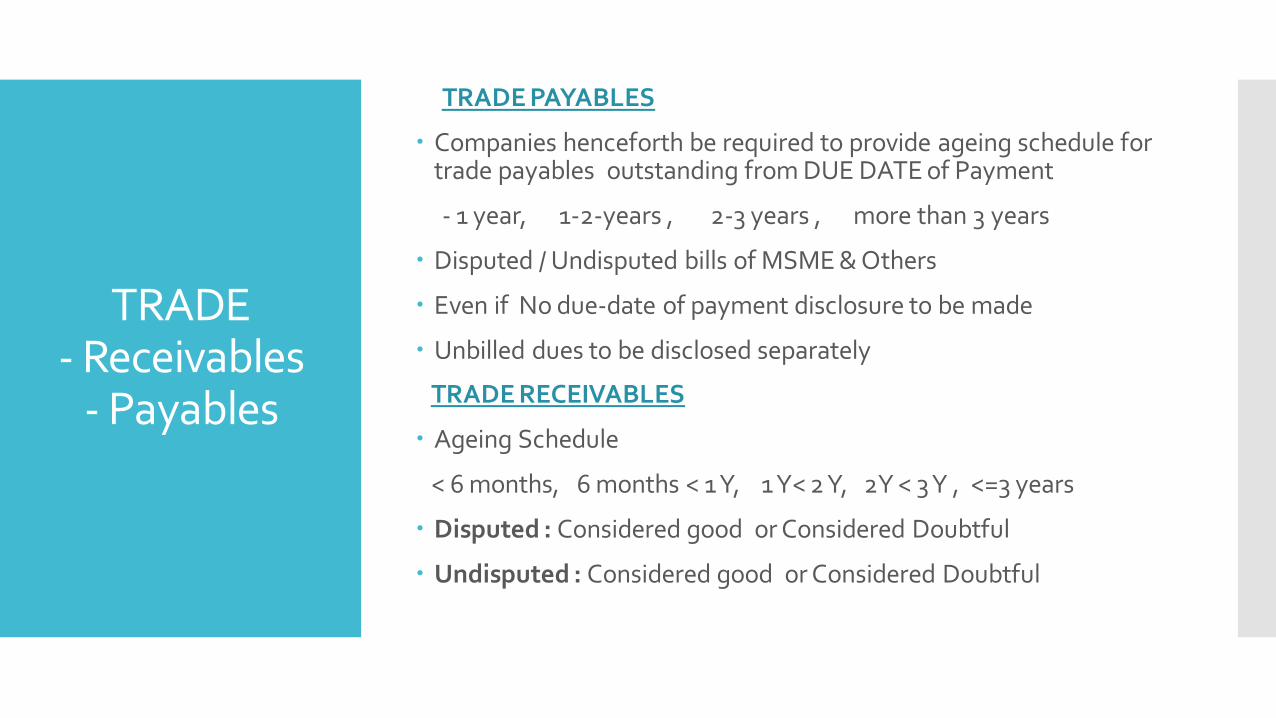

TRADE - Receivables

- Payables

TRADE PAYABLES

Companies henceforth be required to provide ageing schedule for trade payables outstanding from DUE DATE of Payment

- 1 year, 1-2-years , 2-3 years , more than 3 years

Disputed / Undisputed bills of MSME & Others

Even if No due-date of payment disclosure to be made

Unbilled dues to be disclosed separately

TRADE RECEIVABLES

Ageing Schedule

< 6 months, 6 months < 1 Y, 1 Y< 2 Y, 2Y < 3 Y , <=3 years

Disputed : Considered good or Considered Doubtful

Undisputed : Considered good or Considered Doubtful

Capital Goods Intangible

Goods

WORK IN PROGRESS

Ageing Schedule for Capital WIP

Ageing Schedule for Intangible Assets under Development

Projects in Progress/ Projects temporarily suspended (!)

Whether projects Overdue?

Other Disclosures

Registration of charges / satisfaction pending to be registered with ROC: Statutory period, details and reasons for delay to be disclosed

Number of layers prescribed under clause (87) of section 2 of the Act read with Companies (Restriction on number of Layers) Rules, 2017, the name and CIN of the companies beyond the specified layers and the relationship/extent of holding of the company in such downstream companies shall be disclosed.

Disclosure whether Revaluation of Assets by Registered Valuer

A disclosure to effect that the books of accounts of the company are in accordance with the approved scheme of arrangement and accounting standards in case the competent authority has approved the same.

Disclosure of RATIOS

a. Current Ratio,

b. Debt-Equity Ratio,

c. Debt Service Coverage Ratio,

d. Return on Equity Ratio,

e. Inventory turnover ratio,

f. Trade Receivables turnover ratio,

g. Trade payables turnover ratio,

h. Net capital turnover ratio,

i. Net profit ratio,

j. Return on Capital employed,

k. Return on investment.

In respect of dealings with

BANKS

Details of Borrowing: Where the Company has borrowings from banks or financial institutions on the basis of security of current assets, it shall disclose the following:-

a. whether quarterly returns or statements of current assets filed by the Company with banks or financial institutions are in agreement with the books of accounts?

b. If not, summary of reconciliation and reasons of material discrepancies, if any to be adequately disclosed.

Wilful Defaulter: Where a company is a declared wilful defaulter by any bank or financial Institution or other lender, following details shall be given:

a. Date of declaration as wilful defaulter,

b. Details of defaults (amount and nature of defaults)

Curb Money Laundering

Details of Loans & Advances to Directors/ KMP’s/ Related Parties

Details of Benami Property : If proceedings initiated or pendingunder Benami Transactions (Prohibitions) Act, 1988

Disclosure only if Title deeds not in the name of Company

If such immovable property is jointly held with others, details are required to be given to the extent of the Company’s share

The company not to be employed nor to be acting as a “conduit entity” for any financial transaction. Disbursement of funds by way of advance, loan, investment, guarantee or security by the company to any person/ entity being an ultimate beneficiary through any intermediary. Disclosure shall also be made about any receipt of funds in such manner

Undisclosed Income (Reconciliation of Income Tax and Companies Act):

Details of any transaction not recorded in the books of accounts that has been surrendered or disclosed as income during the year in the tax assessments

CSR Disclosure:

- Details of CSR activities:

- details of related party transactions, e.g., contribution to a trust controlled bythe company in relation to CSR expenditure

- where a provision is made with respect to a liability incurred by entering into a contractual obligation, the movements in the provision during the year should be shown separately.

Details of Crypto Currency or Virtual Currency:

Where the Company has traded or invested in Crypto currency or Virtual Currency during the financial year, the following shall be disclosed: –

a. profit or loss on transactions involving Crypto currency or Virtual Currency

b. amount of currency held as at the reporting date,

c. deposits or advances from any person for the purpose of trading or investing in Crypto Currency/ virtual currency.

CARO 2020Highlights

Features

Major changesClause 1

Clause 1 Fixed Assets

a. Separate Reporting for PPE and Intangible Assets instead of Fixed Assets

b. No Reporting on title deeds, where Company is lessee and lease agreement is executed in favour of the Company

c. Specific details are required to be given in case title deeds are not in name of the Company

d. Reporting on revaluation of PPE

e. Reporting on any proceedings initiated or pending against the Company under Benami Transactions (Prohibition) Act, 1988 for holding Benami Property.

Major changesClause 2

Clause 2 Inventory

a. Coverage and Procedure of physical verification by the management isappropriate or not

b. Discrepancies to report for each class of inventory only if it is 10% ormore

c. Quarterly statements filed with banks or financial institutions are inagreement with the books of account

Note: Sanctioned working capital limits > Rs. 5 crore rupees

(Banks + financial institutions) and

Secured against current assets

Major changesClause 3

Clause 3 Loans, Investments, Guarantees, Securities and Advances in the nature of Loan

a. Reporting of Loans given to any party

b. Reporting on adequacy of terms and conditions regarding Investmentsmade, securities given, guarantees provided and advances given innature of loan.

c. Additional reporting in terms of Amount of loans or advance in nature ofloan granted / guarantees and securities provided to group entities andto others and its balance outstanding as at balance sheet date

d. Additional reporting for any loan or advance in the nature of loanrenewed or extended or fresh loans granted to settle the overdues ofexisting loans

e. Reporting for such loans either repayable on demand or withoutspecifying any terms or period of repayment

Major changesClause 5Clause 7Clause 8

Clause 5 Deposits

a. Reporting of Deposits accepted

“deposits accepted by the company or amounts which are deemed tobe deposits”

Acceptance of Deposit Rules, 2014

Clause 7 Statutory Dues

a. Reporting now includes GST

b. Reporting of disputes in case of ALL types of statutory dues

Clause 8 Unrecorded Income

a. A new clause inserted which requires auditors to report whetherpreviously non recorded Income has been recorded properly based onthe outcome of the assessment under Income Tax Act. (Expensedisallowed not mentioned!!! as such only the income not-recorded)

Major changesClause 9

Clause 9 Repayment and Usage of Borrowings

a. Default of Interest payment is also covered

b. Application of term loan – Purpose , whether diverted?

c. Coverage of reporting is expanded to include all types of lenders

d. Whether the company is a declared willful defaulter by any lender

e. Additional reporting on:

Only if Usage of short term funds for long term purposes ,

Details of Funds borrowed by holding company for the purpose of discharging obligations of group entities (components)

Details of Funds borrowed by pledging the securities held in its group entities (components) and defaults in its repayment

Major changesClause 10Clause 11Clause 12

Clause 10 Money raised through own shares

a. Clauses are combined

b. Includes reporting also on compliance of Section 62 (Further issueof Share capital) i.r.o. Preferential and Private placement also

Clause 11 Fraud

a. Reporting of all the fraud by or on the company is required

b. Any reporting made by auditor to central government u/s 143(12)

c. consideration of whistle-blower complaints received by theCompany

Clause 12 Nidhi Company

a. Reporting of default in payment of deposits and its interest

Major changesClause 14Clause 16

Clause 14 Internal Audit

a. Whether company has an internal audit system commensurate withthe size and nature of its business

b. Whether the reports of the Internal Auditors were considered bythe statutory auditor

Clause 16 45-IA of RBI Act, 1934

a. Whether Non banking finance or housing finance activities are doneafter taking certificate of registration (CoR) from RBI

b. fulfilment of classification criteria laid down by RBI for CoreInvestment Company (CIC)

c. Number of CICs in the Group to which company belongs

Major changesClause 17Clause 18

Clause 17 Cash Losses

a. Whether the company has incurred cash losses in the financial yearand in the immediately preceding financial year, if so, state theamount of cash losses;

Clause 18 Auditor’sResignation

a. Reporting if Resignation of the statutory auditors during the year

b. Report about whether the (current)auditor has taken intoconsideration the issues, objections or concerns raised by theoutgoing auditors

Major changesClause 19Clause 20

Clause 19 Financial Position

a. On the basis of the financial ratios, ageing and expected dates ofrealization of financial assets and payment of financial liabilities, otherinformation accompanying the financial statements, the auditor’sknowledge of the Board of Directors and management plans, whetherthe auditor is of the opinion that no material uncertainty exists as onthe date of the audit report that company is capable of meeting itsliabilities existing at the date of balance sheet as and when they falldue within a period of one year from the balance sheet date

Clause 20 CSR compliance

a. Requires auditors to report whether unspent amount of CSR has beentransferred to a special designated bank account (related to anyongoing project) and to a fund as specified in Schedule VII (where nospecific project has been carried out or assigned) or not.

Major changes

Clause 21 Consolidated Financial Statements CFS

a. Managerial Remuneration clause removed from CARO (main auditreport)

b. The details of the companies and the paragraph numbers containingqualifications/adverse remarks by the respective auditors in the CAROreports of the companies to be included in the consolidated financialstatements (CFS).

Credits

mca.gov.in

taxguru.in

icai.org/resources

Absorbed by Light