High Margin Growth Just Getting Started · SDX Energy – High Margin Growth Opportunity • High...

32

Proactive Investors One2One Forum February 9, 2017 SDX LN / SDX CN High Margin Growth – Just Getting Started SDX Energy Inc.

Transcript of High Margin Growth Just Getting Started · SDX Energy – High Margin Growth Opportunity • High...

Proactive Investors One2One Forum

February 9, 2017 SDX LN / SDX CN

High Margin Growth – Just Getting Started

SDX Energy Inc.

SDX Energy – High Margin Growth Opportunity

• High margin onshore production and development assets with transformational exploration

upside

• AIM and TSX-V listed (TSXV: SDX/ AIM:SDX) • Successful secondary listing and capital raise on AIM in May 2016

• Attracted new institutional backers and strong after market

• High margin production:

• Cash flow positive to US$21/bbl Brent (at the corporate level)

• Current net production of 4,705 boe/d, 12.03 MMBOE of 2P reserves (31/12/15)

• Development potential to double production and triple reserves (Meseda)

• High impact and funded exploration program underway

• Solid balance sheet as of 31 January 2017:

• US$ 42MM of Working Capital (US$ 18.3MM in Cash)

• No debt

• Well placed to capitalise on distressed asset opportunities in North Africa

Page 2

The Transaction

Acquisition of Circle Oil Plc Assets in Egypt & Morocco

Page 4

• Buying Circle Oil’s subsidiaries in Egypt and Morocco debt free, from ‘distressed’

Strategic Review process • Debt holders owed: c.US$77.5MM

• Price: US$30MM (39 cents/US$ on group debt)

• Assets:

• Egypt: • 40% of North West Gemsa Concession

• Net Production: 2600 boepd

• 2P Reserves: 3.77 Mmboe

• Net back: US$17.24/boe (Brent price US$58.40/bbl)

• Morocco: • 75% of Sebou Production & Lalla Mimouna Exp. Concessions

• Net Production: 4.5 MMscfd (750 boepd)

• 2P Reserves: 0.92 Mmboe

• Net back: US$52.25/boe (Brent price of US$58.40/bbl)

• Working Capital: US$18MM

• Totals: • Production: 3350 boepd

• 2P Reserves: 4.69 Mmboe

• Avg. Net back: US$24.11/boe

• Acquisition Price: US$6.40/boe (US$2.56/boe excl. W Cap)

: US$8,955 per flowing boe (US$3,582 per flowing boe excl. W Cap)

1 2

Benefits of the Transaction

Page 5

• Adds new High Margin asset in Morocco and consolidates existing High Margin asset in Egypt

• Expected to increase daily production by 247%, 2P Reserves by 64% & Cash flow by

cUS$22MM in 2017 and c.US$27MM 2018. Acquire US$18MM of Working Capital

(US$2.0MM cash and cUS$16.0m net receivables)

• Very Attractive Expected Acquisition Metrics : • Payback: 1.4 years (at current Brent Strip prices)

• IRR: 82%

• Highly Accretive:

• EV/2P BOE (Net): 15%

• EV/2016 Boed: 44%

• 2016 Production/Share: 26%

• NAV/Share: 34%

• Excellent strategic fit with current business:

Egypt

• Circle acquisition adds 40% of asset where SDX already holds 10%

• Increasing exposure with no additional increase in staffing or overhead

• Can substantially improve upon Circle’s payment record

• Improves the ability to influence operator

Morocco

• Provides diversification and an additional revenue source

• Growth potential in a high margin gas market

• Undercapitalized Circle could not capture low hanging upside

• Expands the exploration portfolio

Post-acquisition Illustrative Capex and Cashflow summary

Page 6

Operating cashflow uses Brent Fwd Curve US$58.40 & US$58.25 in 2017 & 2018 and no cash inflow from W. Capital reduction Circle Oil Morocco 2017 & 2018 Operating cashflow modelled at current run rate Circle Oil Egypt 2017 & 2018 Operating cashflow uses Operator’s proposed 2017 budget as basis SDX 2017 & 2018 Operating cashflow uses Operator’s proposed 2017 budgets as basis 2017 capex: 2 Dev & 2 Exp wells in Circle Oil Morocco & 2 Exp & 2 Dev wells plus facility expansion & w/flood in Meseda Egypt 2018 capex: 2 Dev wells in Circle Oil Morocco and 2 Dev wells in NW Gemsa (Circle Oil 40%/SDX 10%) Egypt

Assumptions

Why North Africa?

Why Egypt? Geology & Operating Environment

One of the best E&P Fiscal Regimes

• Royalty Rate – 5%

• Corporate Income Tax Rate – 30%

• 10 year tax holiday from start-up

Moroccan Gas Market – High Prices • Gas market is dominated by compressed natural gas

suppliers or “Bottled Gas”

• Bottled gas prices, for largest industrial customers,

average $18.00/MCF

• No local or national gas grids exist within Morocco

• Gas supplied by Circle sells for $8.10 - $9.90/MCF

Gas Demand Significantly Exceeds Supply • Currently more customers than COP can supply

• Industrial customers using COP gas have significant

price advantage in energy supply when compared to

bottled gas customers

• Pressure on government to locally raise gas prices to

reduce commercial advantage of COP customers

Dominant Commercial Position • COP owns 75% of the only private owned pipeline

• Connects producing basins to the industrial market

• Any future discoveries will likely have to pass through

COP’s line to be commercialized.

Page 8

Multiple world class hydrocarbon basins • 3 Basins in the Top 10 (MENA)

• W. Desert 3rd best value creator over the last 10 years

• Zohr discovery 22+TCF (4 Billion bbl equivalent) largest

discovery globally in 2015

Excellent operating environment • Competitive fiscal terms combined with low opex

• Operating Costs are still dropping • Egyptian currency depreciated 50%+ vs $USD

Historic pay-out backlog clearing • Government pledged to clear balance by end 2017

Economy stabilising • Government has removed currency controls and

“floated” the Egyptian pound in the market

• IMF US$12 Billion loan terms agreed, first US$2.7 Billion

dispersed • Improved the availability of the USD$ in the economy

Local gas prices increasing • Domestic gas market significantly underserved

(importing LNG @$6-$10/Mmbtu)

• Long term demand not satisfied by Zohr alone due to

demand growth and natural declines in existing fields

Why Morocco? Commercial terms & Gas Market

Egypt: Production & Exploration Assets

Assets - Egypt

Page 10

Exploration

Production & Development

Production

Development

SDX – 55% WI & Operator

SDX – 50% WI & Joint Operator

SDX – 10% WI, Rising to 50% post transaction

SDX – 12.75% WI

Egypt– Production Assets

• Very Low Cost Production Base: <$10/bbl

• Onshore

• Low Capex Spend Going Forward

• North West Gemsa

• Gross Daily Production: 6,510 BOEPD

• Equity Interest: 50%

• Net 2P Reserves: 4.7 Mmbo (31/12/15)

• Operating Cost: $7.38/bbl, Netback: $17.24

• SDX Capex – 2017: $1.75MM

• Meseda

• Gross Daily Production: 4,250 BOEPD

• Equity Interest: 50%

• Net 2P Reserves: 6.4 Mmbo (31/12/15)

• Operating Cost: $8.44/bbl, Netback: $23.78

• SDX Capex – 2017: $4.8MM

• Plans to 2X production by Q2 2017

Assets significantly cash flow positive

Page 11

Egypt – Exploration Asset - South Disouq

55% Working Interest (Operator)

1,275 km2 Concession area

585 BCF (P Mean) Gross Prospective Resources

6.4 TCF &

100 Mmboe Rec. Volumes within Abu Madi Baltim Trend (IHS)

65 km north of Cairo within prolific Abu Madi – Baltim trend

Located within existing oil and gas transport infrastructure

Main gas, condensate and oil lines transect block

Prospects are 5 & 11 kms from connection points

1st period work commitment: 300km2 seismic & 1 well

Successful farm out to IPR for 45% – carries Exploration

Well cost (subject to a cap of $3MM)

Abu-Madi – Baltim Trend

2017 WORK PLAN

Complete interpretation of 300 km2 3D seismic data

Drill Exploration Well – Q1 2017

Initiate fast track development program (assuming

successful exploration) into local infrastructure

Page 12

South Disouq Top Abu Madi Structure Map

• Seismic data confirms Abu Madi

play fairway extends into SDX

Acreage

SD-1X Abu Madi Prospect

SD Deep-1X Abu Roash/AEB

Prospect

Map area shown in inset

South Disouq Survey Area

Page 13

SD-1X Abu Madi Prospect

• Robust ~1000 acre four-way dip closure mapped on seismic data

• 175’ of structural closure at Abu Madi level

• Positive AVO response reduces risk of not

encountering reservoir

• Deeper potential identified in Abu Roash and AEB zones which are prolific Western Desert oil producers

Incr

easi

ng

Res

ervo

ir Q

ual

ity

Extent of SD-1X closure

SW NE

SD-1X

Page 14

Morocco: Production & Exploration Assets

Morocco – Production Assets

Sebou Permits - Production • Working interest: 75% & Operator (Partner: ONHYM 25%)

• Located in Rharb Basin

• 134 km2 area covered by 3D seismic

• Currently producing 6.2 MMscf/day (1,033 boepd)

• Connected to sales by new 8” pipeline

Lalla Mimouna Permit - Exploration

• Working interest: 75% & Operator (Partner: ONHYM 25%)

• Located in Rharb Basin

• 2,112 km2 concession area,154 km2 covered by 3D seismic

• Adjacent to Sebou permit with existing gas sales line

Page 16

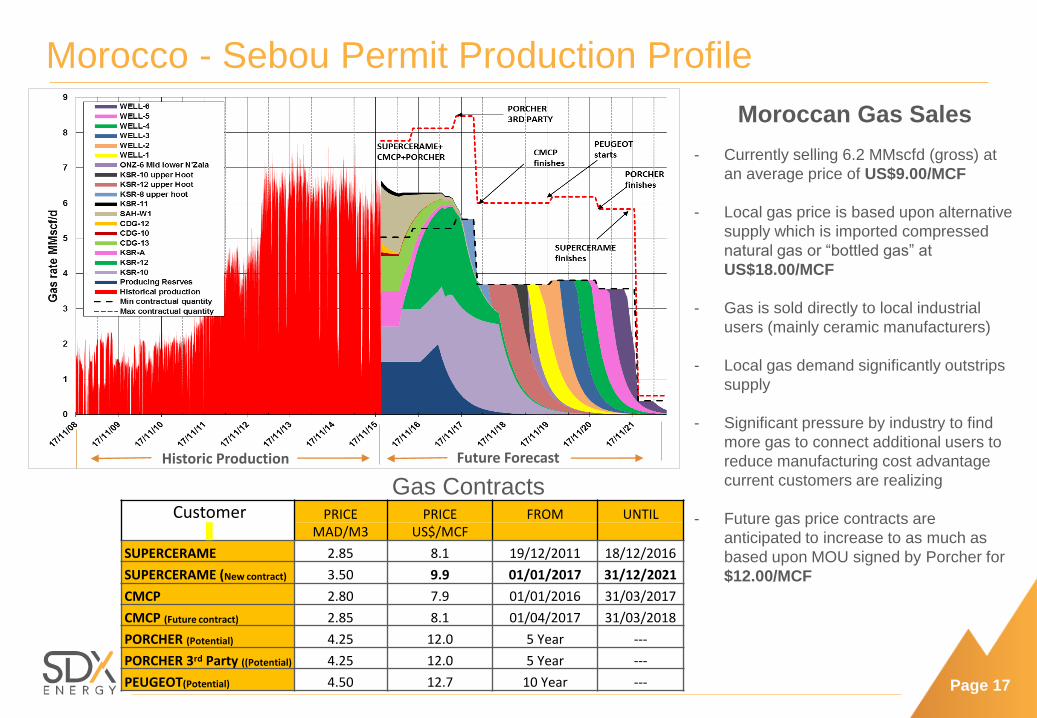

Morocco - Sebou Permit Production Profile

Customer PRICE PRICE FROM UNTIL MAD/M3 US$/MCF

SUPERCERAME 2.85 8.1 19/12/2011 18/12/2016

SUPERCERAME (New contract) 3.50 9.9 01/01/2017 31/12/2021

CMCP 2.80 7.9 01/01/2016 31/03/2017

CMCP (Future contract) 2.85 8.1 01/04/2017 31/03/2018

PORCHER (Potential) 4.25 12.0 5 Year ---

PORCHER 3rd Party ((Potential) 4.25 12.0 5 Year ---

PEUGEOT(Potential) 4.50 12.7 10 Year ---

Moroccan Gas Sales

- Currently selling 6.2 MMscfd (gross) at

an average price of US$9.00/MCF

- Local gas price is based upon alternative

supply which is imported compressed

natural gas or “bottled gas” at

US$18.00/MCF

- Gas is sold directly to local industrial

users (mainly ceramic manufacturers)

- Local gas demand significantly outstrips

supply

- Significant pressure by industry to find

more gas to connect additional users to

reduce manufacturing cost advantage

current customers are realizing

- Future gas price contracts are

anticipated to increase to as much as

based upon MOU signed by Porcher for

$12.00/MCF

Page 17

Gas Contracts

Historic Production Future Forecast

Morocco - Rharb Basin: Regional Exploration potential

Page 18

• Regional basin architecture well

understood from extensive 2D

seismic framework

• Prospectivity established in multiple

horizons throughout Miocene-aged

strata

• Potential for material upside

discoveries through 3D seismic

acquisition

• Potential to expand acreage footprint

to adjacent open acreage

Seismic Anomaly

2D Seismic Line

Concession Boundary

3D Seismic Survey

Lalla Mimouna Nord

Lalla Mimouna Sud

Exploration Potential: Seismic Anomalies

Amplitude analysis suggest the presence

of several gas-filled sand bodies across

the area • Similar response to Sebou Permit

Five amplitude-supported prospects

mapped in 3D seismic area • 13.2 BCF* of unrisked recoverable gas

Multiple target horizons creates potential

for stacked pay

Amplitude-supported Prospects

*Circle Oil internal estimate of middle-range recoverable volumes

Page 19

2

2

“Roll-Up” Opportunity

EGYPT – THE CASE FOR CONSOLIDATION

Several large players focused on gas (primarily offshore)

Many (20+) small and medium sized companies that are focused on oil (primarily on shore) Too small to prosper in the current environment These are the targets (see next page)

Company NPV10, NPV10/boe and net reserves

Page 21

Eni

BP

Apache

Sinopec Shell

Edison Kuwait Energy

Company Merlon DEA

Dana Gas

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0.00 2.00 4.00 6.00 8.00 10.00 12.00

Rem

ain

ing

PV

(10%

) U

S$ (

millio

n)*

Remaining PV/boe (US$/million)* Source: Wood Mackenzie

*Discounted to 1st January 2016

= 500

mmboe

Liquids

Gas

Egypt - the consolidation opportunity set

Page 22

More than half of the companies identified above looking to exit or reduce exposure Numerous public and private sales processes on going Financial markets mostly shut for smaller companies to raise equity or debt Many companies caught by a potentially “toxic” combination of: - Egyptian receivables - USD denominated debts - US Dollar shortage in country Two companies have already failed, several others are teetering Buyer’s market

Top 11 to 30 companies by remaining value and reserves

Summary

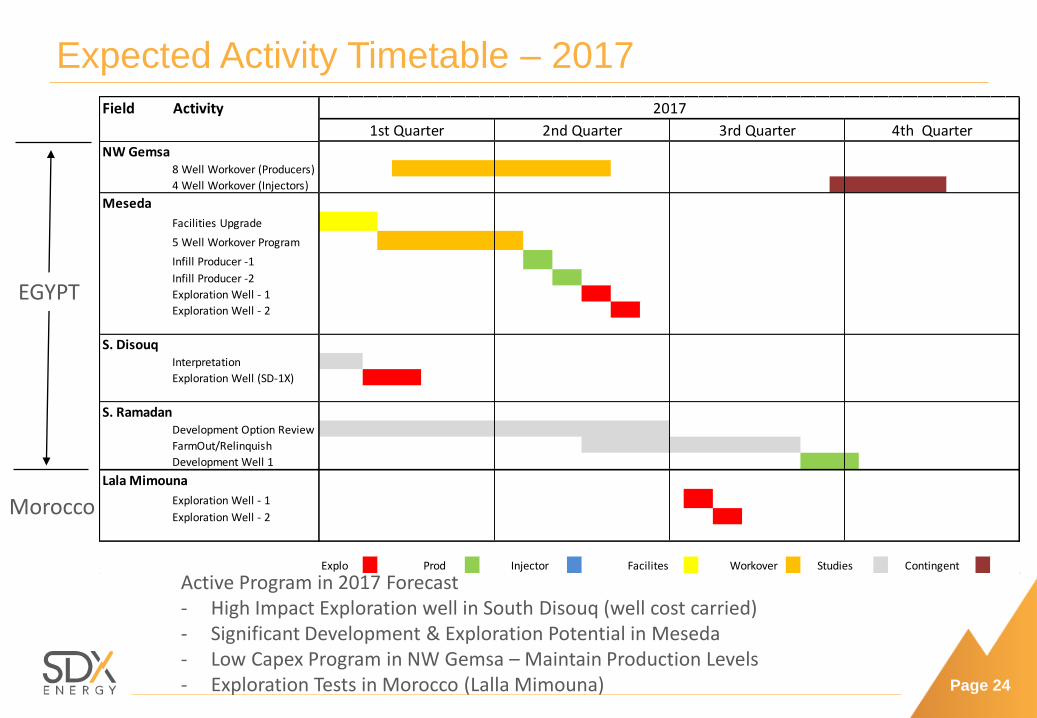

Expected Activity Timetable – 2017

Active Program in 2017 Forecast - High Impact Exploration well in South Disouq (well cost carried) - Significant Development & Exploration Potential in Meseda - Low Capex Program in NW Gemsa – Maintain Production Levels - Exploration Tests in Morocco (Lalla Mimouna) Page 24

Field Activity

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

NW Gemsa8 Well Workover (Producers)

4 Well Workover (Injectors)

Meseda

Facilities Upgrade

5 Well Workover Program

Infill Producer -1

Infill Producer -2

Exploration Well - 1

Exploration Well - 2

S. DisouqInterpretation

Exploration Well (SD-1X)

S. RamadanDevelopment Option Review

FarmOut/Relinquish

Development Well 1

Lala Mimouna

Exploration Well - 1

Exploration Well - 2

Explo Prod Injector Facilites Workover Studies Contingent

2017

EGYPT

Morocco

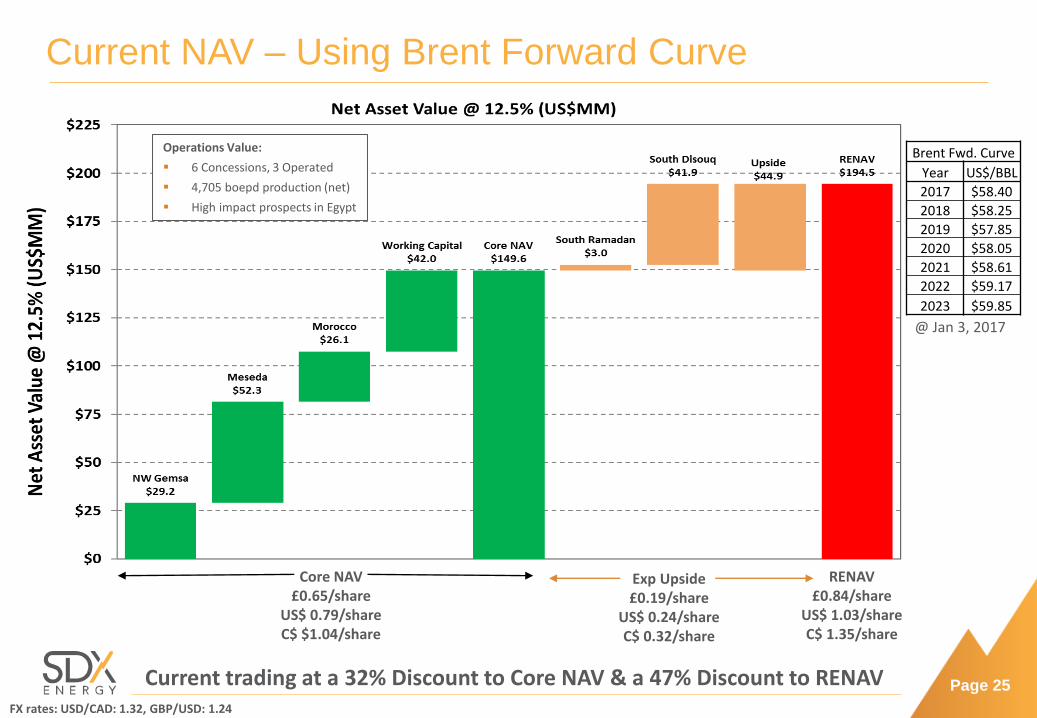

Current NAV – Using Brent Forward Curve

Page 25

Core NAV £0.65/share

US$ 0.79/share C$ $1.04/share

Exp Upside £0.19/share

US$ 0.24/share C$ 0.32/share

RENAV £0.84/share

US$ 1.03/share C$ 1.35/share

Brent Fwd. Curve

Year US$/BBL

2017 $58.40

2018 $58.25

2019 $57.85

2020 $58.05

2021 $58.61

2022 $59.17

2023 $59.85

Base

Base +, Workovers, Waterflood

Base

@ Jan 3, 2017

FX rates: USD/CAD: 1.32, GBP/USD: 1.24

Current trading at a 32% Discount to Core NAV & a 47% Discount to RENAV

Operations Value:

6 Concessions, 3 Operated

4,705 boepd production (net)

High impact prospects in Egypt

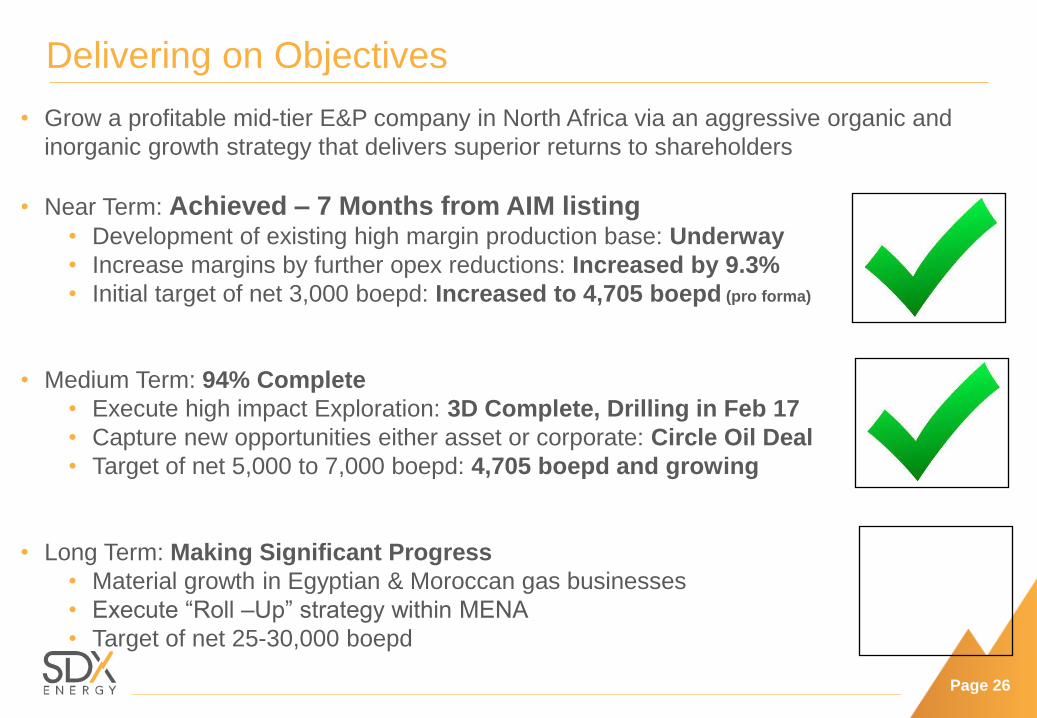

Delivering on Objectives

• Grow a profitable mid-tier E&P company in North Africa via an aggressive organic and

inorganic growth strategy that delivers superior returns to shareholders

• Near Term: Achieved – 7 Months from AIM listing • Development of existing high margin production base: Underway

• Increase margins by further opex reductions: Increased by 9.3%

• Initial target of net 3,000 boepd: Increased to 4,705 boepd (pro forma)

• Medium Term: 94% Complete

• Execute high impact Exploration: 3D Complete, Drilling in Feb 17

• Capture new opportunities either asset or corporate: Circle Oil Deal

• Target of net 5,000 to 7,000 boepd: 4,705 boepd and growing

• Long Term: Making Significant Progress

• Material growth in Egyptian & Moroccan gas businesses

• Execute “Roll –Up” strategy within MENA

• Target of net 25-30,000 boepd

Page 26

Page 27

High Margin Growth

Appendix

Advisory Forward-looking Statements

This presentation and any additional documents handed out at the meeting (together the “Presentation Materials”) contain certain

statements or disclosures relating to, among other things, SDX Energy Inc. (“SDX”), its proposed private placement (“Private Placement”)

and its proposed acquisition (the “Acquisition” and, together with the Private Placement, the “Transactions”) of certain subsidiaries of

Circle Oil Plc (“Circle Oil”) which constitute “forward-looking statements” as such term is used in applicable Canadian securities laws. Any

statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions

or future events or are not statements of historical fact should be viewed as forward-looking statements. In particular, statements

concerning SDX, the Transactions, the anticipated benefits that will result from the Transactions and the key characteristics of SDX or of the

assets to be acquired in the Acquisition should be viewed as forward-looking statements.

The forward-looking statements contained in this document are based on certain assumptions and although management of SDX consider

these assumptions to be reasonable based on information currently available to them, undue reliance should not be placed on the forward-

looking statements because SDX can give no assurances that they may prove to be correct. This includes, but is not limited to,

assumptions related to the ability of SDX to receive, in a timely manner, the necessary regulatory, stock exchange and other third party

approvals, the ability of SDX to satisfy, in a timely manner, the other conditions to the closing of each of the Private Placement and the

Acquisition and expectations and assumptions concerning, among other things commodity prices and interest and foreign exchange rates;

planned capital efficiencies and cost-savings; applicable tax laws; future production rates; the sufficiency of budgeted capital expenditures

in carrying out planned activities; the availability and cost of labour and services; the production capacity of SDX’s current and future assets

and those to be acquired pursuant to the Acquisition; the reserves and resources potential of SDX’s current and future assets and those to

be acquired pursuant to the Acquisition; future cash flow projections; the exploration potential of SDX’s current and future assets and those

to be acquired pursuant to the Acquisition; expectations for being paid in full and on time in the future; future operating expenditures; near-

term, medium-term and long-term projections for SDX; the benefits of the Transactions; future cost reductions; the economic and political

environment in Egypt and Morocco; oil and gas commodity prices; SDX’s development and exploration potential, including the success of

workover, infill drilling and waterflood extraction techniques and the costs and benefits related to same; risk and success potential related to

future drilling locations; Egyptian and Moroccan demand for oil, gas and LNG products; timing of capital expenditures including the drilling

of wells and costs associated with same; results of seismic programs; the relative price of assets and the financial status of buyers and

sellers in the Egyptian and Moroccan markets; opportunities related to legacy payment issues; the timing of the Transactions; and

completion of the Transactions. The anticipated dates provided may change for a number of reasons, including unforeseen delays in

preparing materials, investor demand, inability to secure necessary regulatory, stock exchange or other third party approvals in the time

assumed or the need for additional time to satisfy the other conditions to the completion of either the Private Placement or the Acquisition.

By their very nature, forward-looking statements are subject to certain risks and uncertainties (both general and specific) that could cause

actual events or outcomes to differ materially from those anticipated or implied by such forward-looking statements. Such risks and other

factors include, but are not limited to the timing of the Transactions, requisite approvals of the TSX Venture Exchange and the London

Stock Exchange, political, social and other risks inherent in daily operations of SDX, risks associated with the industries in which SDX

operates in general, such as: operational risks; delays or changes in plans with respect to growth projects or capital expenditures; costs

and expenses; health, safety and environmental risks; commodity price, interest rate and exchange rate fluctuations; environmental risks;

competition; failure to realize the anticipated benefits of the Acquisition; ability to access sufficient capital from internal and external

sources; and changes in legislation, including but not limited to tax laws and environmental regulations. There is a risk that SDX fails to

satisfy the conditions to either the Private Placement or the Acquisition which may result in such Transaction not being completed on the

proposed terms, or at all. Readers are cautioned that the foregoing list of risk factors is not exhaustive and are advised to reference SDX’s

Annual Information Form for the year ended December 31, 2015, which can be found on SDX’s SEDAR profile at www.sedar.com, for a

description of additional risks and uncertainties associated with SDX’s business, including its exploration activities.

No representation or warranty, express or implied, is or will be made and no responsibility or liability is or will be accepted by SDX or by any

of its respective officers, servants or agents or by Cantor Fitzgerald Europe Limited (“Cantor Fitzgerald”) FirstEnergy Capital Limited

(“FirstEnergy”) or Stifel Nicolaus Europe Limited (“Stifel” and together with Cantor Fitzgerald, and FirstEnergy, the “Bookrunners”) any

other person as to or in relation to the accuracy or completeness of the Presentation Materials or the information or opinions contained

herein or supplied herewith or any other written or oral information made available to any interested party or its advisers and, to the fullest

extent permitted by law, no responsibility or liability is accepted for the accuracy or sufficiency of any of the information or opinions, for any

errors, omissions or mis-statements, negligent or otherwise, or for any other communication, written or otherwise, made to anyone in, or

supplied with, the Presentation Materials or otherwise in connection with the proposed sale of the Investor Interest. In particular, no

representation or warranty is given as to the achievement or reasonableness of any future projections, management estimates, prospects

or returns.

The forward-looking statements contained in this presentation are made as of the date hereof and SDX does not undertake any obligation

to update publicly or to revise any of the included forward-looking statements, except as required by applicable law. The forward-looking

statements contained herein are expressly qualified by this cautionary statement.

Reserves Data

The determination of oil and natural gas reserves involves the preparation of estimates that have an inherent degree of associated

uncertainty. Categories of proved, probable and possible reserves have been established to reflect the level of these uncertainties and to

provide an indication of the probability of recovery. The estimation and classification of reserves requires the application of professional

judgment combined with geological and engineering knowledge to assess whether or not specific reserves classification criteria have

been satisfied. Knowledge of concepts including uncertainty and risk, probability and statistics, and deterministic and probabilistic

estimation methods is required to properly use and apply reserves definitions. The recovery and reserve estimates of oil reserves

provided herein are estimates only. Actual reserves may be greater than or less than the estimates provided herein. Terms related to

reserves classifications referred to herein are based on definitions and guidelines in the Canadian Oil and Gas Evaluation Handbook

(“COGE Handbook”) and are in accordance with National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities.

In relation to SDX’s assets, “Proved reserves” are those reserves that can be estimated with a high degree of certainty to be

recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves. “Probable reserves” are

those additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining

quantities recovered will be greater or less than the sum of the estimated proved plus probable reserves. The qualitative certainty levels

referred to in the definitions above are applicable to “individual reserves entities”, which refers to the lowest level at which reserves

calculations are performed, and to “reported reserves”, which refers to the highest level sum of individual entity estimates for which

reserves estimates are presented. Reported reserves should target the following levels of certainty under a specific set of economic

conditions:

• at least a 90 percent probability that the quantities actually recovered will equal or exceed the estimated proved reserves. This

category of reserves can also be denoted as 1P;

• at least a 50 percent probability that the quantities actually recovered will equal or exceed the sum of the estimated proved plus

probable reserves. This category of reserves can also be denoted as 2P; and

• at least a 10 percent probability that the quantities actually recovered will equal or exceed the sum of the estimated proved plus

probable reserves. This category of reserves can also be denoted as 3P.

Additional clarification of certainty levels associated with reserves estimates and the effect of aggregation is provided in the COGE

Handbook. The estimates of reserves for individual properties may not reflect the same confidence level as estimates of reserves for all

properties, due to the effects of aggregation.

Use of the term “boe” may be misleading, particularly if used in isolation. A “boe” conversion ratio of 6 Mcf: 1 bbl is based on an energy

equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

Certain volumes provided in this presentation represent a pro forma arithmetic sum of multiple estimates of proved plus probable

reserves, or proved plus probable plus possible reserves, which statistical principles indicate may be misleading as to volumes that may

actually be recovered. Readers should give attention to the estimates of individual classes of reserves and appreciate the differing

probabilities of recovery associated with each class as explained in the annual oil and gas disclosure filings of SDX (available on

www.sedar.com) and the effects of arithmetic aggregation. Factors that could affect the accuracy of the reported pro forma aggregated

reserves estimates include company level differences in evaluation effective dates, reservoir characteristics and pricing assumptions.

Reserves information in this presentation relating to SDX’s assets are based on the independent reserves evaluation of the Preliminary

Competent Person’s Report as of December 31,2015 on certain properties owned by SDX Energy Inc. in Egypt prepared by DeGolyer

and MacNaughton Canada Limited .

Reserves information in this presentation relating to Circle’s assets in Morocco are based on a draft independent reserves evaluation of

the Competent Person’s Report as of July 1, 2016 on certain properties owned by Circle Oil in Morocco which is being prepared by

Senergy (GB) Limited and which is being prepared in accordance with the 2007 Petroleum Resources Management System prepared by

the Oil and Gas Reserves Committee of the Society of Petroleum Engineers and reviewed and jointly sponsored by the World Petroleum

Council, the American Association of Petroleum Geologists and the Society of Petroleum Evaluation Engineers. The draft numbers are

subject to updating and the final report to be published in connection with the acquisition.

Information about the Circle Oil Group, its assets in Morocco and the business environment in Morocco has, except where stated, been

taken from publicly available information and information supplied by Circle Oil and is based on the expectation of Circle’s management.

Page 29

Advisory • THIS PRESENTATION IS CONFIDENTIAL AND IS BEING SUPPLIED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED, FURTHER DISTRIBUTED TO ANY OTHER PERSON OR PUBLISHED, IN WHOLE OR PART, FOR ANY PURPOSE,

WITHOUT THE EXPRESS WRITTEN CONSENT OF SDX.

• This presentation does not contain or constitute an offer to sell or a solicitation of an offer to purchase securities in the United States or any other jurisdiction. The securities of SDX have not been and will not be registered under the US Securities Act of 1933, as amended (the

“Securities Act”), or qualified for sale under the law of any state or other jurisdiction of the United States and may not be offered or sold in the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act.

The Company does not intend to register any securities under the Securities Act, and no public offering of securities in the United States will be made. In the United States, this presentation is directed only at, and may be communicated only to, persons that are “qualified

institutional buyers” as defined in Rule 144A under the Securities Act (such persons hereinafter referred to as “QIBs”).

• Neither this document, nor any copy of it, may be taken or transmitted into the United States (other than to a limited number of QIBs), Australia, South Africa or Japan or into any jurisdiction where it would be unlawful to do so. Any failure to comply with this restriction may

constitute a violation of relevant local securities laws. By receiving a copy of this presentation, you will be deemed to have represented to SDX, Cantor Fitzgerald and Stifel that you are a QIB.

• The information set out in these Presentation Materials will not form the basis of any contract. Any successful purchaser of an Investor Interest will be required to acknowledge in writing that it has not relied on or been induced to enter such agreement by any representation or

warranty, save as expressly set out in such agreement.

• The Presentation Materials have been delivered to interested parties for information only and upon the express understanding that such parties will use it only for the purpose set out above. SDX undertakes no obligation to provide the recipient with access to any additional

information or to correct any inaccuracies herein which may become apparent, and it reserves the right, without advance notice, to change the procedure for the acquisition of an Investor Interest or to terminate negotiations at any time prior to the completion of such acquisition.

The issue of the Presentation Materials shall not be taken as any form of commitment on the part of SDX to proceed with any transaction.

• The contents of this document have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 ("FSMA") for the purposes of section 21 of FSMA. The Presentation Materials are only being made available to the following:

• persons having professional experience in matters relating to investments and who are investment professionals as specified in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Financial Promotion Order”); and

• persons to whom Article 49(2) of the Financial Promotion Order applies, being high net worth companies, unincorporated associations, partnerships or trusts or their respective directors, officers or employees as described in Article 49 of the Financial Promotion Order.

It is a condition of your receiving the Presentation Materials that you fall within, and you warrant to SDX and to the Bookrunners that you fall within, one of the categories of person described above.

• The Presentation Materials may contain unpublished price sensitive information or undisclosed material information with regard to SDX and/or its securities and Circle Oil and/or its securities. Recipients of the Presentation Materials should not deal or encourage any other any

other person to deal in the securities of SDX or Circle Oil whilst they remain in possession of such unpublished price sensi tive information or undisclosed material information and until the transactions described in the Presentation Materials are announced. Dealing in securities of

the Company or Circle Oil when in possession of unpublished price sensitive information or undisclosed material information could result in liability under the insider dealing restrictions set out in the Criminal Justice Act 1993 or the insider trading and/or tipping provisions of

Canadian securities laws. This document may contain information which is not generally available, but which, if available, would or would be likely to be regarded as relevant when deciding the terms on which transactions in the shares of SDX or Circle Oil should be effected.

Unreasonable behaviour based on such information could result in liability under the market abuse provisions of FSMA.

• Any prospective purchaser interested in acquiring an Investor Interest in SDX is recommended to seek independent financial advice. Law in certain jurisdictions may restrict the distribution of this document or of the giving of the Presentation Materials and any subsequent offer for

sale or sale of the Investor Interest. Persons into whose possession this document or the information from the Presentation Materials comes are required to inform themselves as to and observe any such restrictions.

• If the recipient does not fall within one of the categories above the recipient should either return, destroy or ignore the information in the Presentation Materials.

• Cantor Fitzgerald which is authorised in the United Kingdom by the FCA for the conduct of investment business is acting for SDX in relation to matters described in this document and will not be responsible in respect of such matters to any other person for providing protections

afforded to customers of Cantor Fitzgerald or for providing advice in relation to those matters.

• FirstEnergy which is authorised in the United Kingdom by the FCA for the conduct of investment business is acting for SDX in relation to matters described in this document and will not be responsible in respect of such matters to any other person for providing protections afforded

to customers of First Energy or for providing advice in relation to those matters.

• Stifel which is authorised in the United Kingdom by the FCA for the conduct of investment business is acting for SDX in relation to matters described in this document and will not be responsible in respect of such matters to any other person for providing protections afforded to

customers of Stifel or for providing advice in relation to those matters.

• If you are in any doubt about the investment to which the Presentation Materials relate, you should consult a person authorised by the Financial Conduct Authority who specialises in advising on securities of the kind described in this document.

• The following is a summary of the statutory rights of rescission or damages, or both, under securities legislation in Ontario, where such summary is required to be disclosed under relevant securities legislation and, as such, is subject to the express provisions of the legislation and

any related regulations and rules. The rights described below are in addition to, and without derogation from, any other right or remedy available at law to purchasers of the securities, subject to any applicable defences.

• Under Ontario securities legislation, certain purchasers resident in Ontario who purchase a security described in this document during the period of distribution will have a statutory right of action for damages, or while still the owner of the securities, for rescission against the issuer

if this document contains a misrepresentation without regard to whether the purchasers relied on the misrepresentation. The r ight of action for damages is exercisable not later than the earlier of 180 days from the date the purchaser first had knowledge of the facts giving rise to the

cause of action and three years from the date of the transaction that gave rise to the cause of action. The right of action for rescission is exercisable not later than 180 days from the date of the transaction that gave rise to the cause of action. If a purchaser elects to exercise the

right of action for rescission, the purchaser will have no right of action for damages against the issuer. In no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser and if the purchaser is shown to have purchased the

securities with knowledge of the misrepresentation, the issuer will have no liability. In the case of an action for damages, the issuer will not be liable for all or any portion of the damages that are proven to not represent the depreciation in value of the securities as a result of the

misrepresentation relied upon. These rights are in addition to, and without derogation from, any other rights or remedies available at law to an Ontario purchaser under Ontario securities legislation. These rights are not available for a purchaser that is: (a) a Canadian financial

institution, meaning either: (i) an association governed by the Cooperative Credit Associations Act (Canada) or a central cooperative credit society for which an order has been made under section 473(1) of that Act; or (ii) a bank, loan corporation, trust company, trust corporation,

insurance company, treasury branch, credit union, caisse populaire, financial services cooperative, or league that, in each case, is authorized by an enactment of Canada or a province or terr itory of Canada to carry on business in Canada or a province or territory of Canada; (b) a

Schedule III bank, meaning an authorized foreign bank named in Schedule III of the Bank Act (Canada); (c) "the Business Development Bank of Canada incorporated under the Business Development Bank of Canada Act (Canada); or (d) a subsidiary of any person referred to in

clauses (a), (b) or (c), if the person owns all of the voting securities of the subsidiary, except the voting securities required by law to be owned by directors of that subsidiary. The foregoing is a summary of the rights available to an Ontario purchaser. Not all defences upon which

the issuer or others may rely are described herein. Ontario purchasers should refer to the complete text of the relevant statutory provisions.

Page 30

Board of Directors

Page 31

Dir

ecto

rs

Individual Position Experience

Michael Doyle Chairman Former CEO of PetrelRoberston Ltd; responsible for advisory & project management Principle and Director of several private and public companies

Paul Welch CEO & Director CEO of two public exploration and production companies, 15 years with Shell Developed Pioneer’s Tunisian portfolio from 500 to a peak of over 25,000 boepd

David Mitchell Director CEO of Madison, extensive Int. experience with BP and as a Director of Nexen Int. Captured and built projects in the Mid East, W. Africa, S. America and the North Sea

David Richards Director Managing Director, Network Capital Inc, a Calgary based investment company

Mark Reid CFO & Director Finance Director at AIM listed Aurelian and Chariot Oil and Gas Limited (2009-2015) Former Head of Oil and Gas in London for BNP-Paribas Fortis

Michael Raynes Director Former COO of Waha Capital, Abu Dhabi Held Senior Executive roles with other large investment firms

Page 32

High Margin Growth