Hidden in the cloudsftp01.economist.com.hk/ECN_papers/HiddenClouds.pdfHIDDEN IN THE CLOUDS The cloud...

14

Hidden in the clouds The future of cloud services and their impact on Asian IT efficiency and innovation Sponsored by A management brief prepared by the Economist Corporate Network

Transcript of Hidden in the cloudsftp01.economist.com.hk/ECN_papers/HiddenClouds.pdfHIDDEN IN THE CLOUDS The cloud...

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

Sponsored by

A management brief prepared by the Economist Corporate Network

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

1© The Economist Corporate Network 2014

VIEWSCOPEA summary of this report’s key findings

Get on the cloud—and stay on itThe cloud is growing among Asian enterprise IT capabilities, and will continue to transform their operations, according to a survey of senior decision-makers from the Economist Corporate Network. Making IT adoption decisions a strategic priority—and keeping it a priority—will be the only way Asia’s business leaders can take full advantage of the transformation potential embedded in on-demand, utility models.

Getting more comfortableThe survey shows clearly that acceptance of the cloud and cloud-like offerings is growing in Asia. When asked whether they would place their various IT capabilities on the cloud, or with a utility-based service provider, over three-quarters of respondents said they would do so in some fashion. And while ‘internal’ capabilities, such as corporate and customer data, where not as cloud-ready, a surprising number of respondents indicated that even these assets were up for cloud evaluation.

The boss calls the IT shots40% of respondents thought that the head of the company was the ultimate decision-maker on IT projects—more than those who assigned that responsibility to the CIO. This was even more prevalent amongst respondents from large. Asia-based enterprises see the strategic importance of IT, and the firm’s most senior executive is clearly seen to have IT implementation decisions worthy of his or her time. The familiarity that comes as a result of the digital devices and apps which percolate into all aspects of work and life may also be a contributing factor.

What you don’t know may still hurt youDecision-makers still have many concerns about virtualising their IT: nearly three quarters of respondents cited both data privacy and cyber-security risks as negatively affecting their adoption decisions. Other issues, such as the lack of technical talent, or cloud resources did not seem to be that great a deterrent—but while this is encouraging, perhaps these findings are telling us that Asia’s business leaders don’t know what they don’t know. This further implies that there are more subtle, and difficult, technology adoption issues for them ahead.

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

2 © The Economist Corporate Network 2014

HIDDEN IN THE CLOUDSThe cloud is growing among Asian enterprise IT capabilities, and will continue to transform their operations, according to a survey of senior decision-makers from the Economist Corporate Network. Despite the clear advantages perceived, there are considerable challenges to smooth adoption—and these hurdles may be much more difficult to overcome. Making IT adoption decisions a strategic priority—and keeping it a priority—will be the only way Asia’s business leaders can take full advantage of the transformation potential embedded in on-demand, utility models.

Senior executives in Asian enterprises are ‘technology forward’ when it comes to adopting new IT utility models and linking them to their growth strategies in the world’s fastest-growing economies. An Economist Corporate Network member survey, conducted with the support of Pacnet, shows that nearly a fifth of Asian-based enterprise respondents are actively converting the majority of their IT capabilities into cloud, “on-demand” or other utility models—and over 60% of them are replacing at least part of their technology platforms with cloud-based solutions. Underlying all of this is an acceptance—perhaps a requirement—that IT decision makers need to take a flexible approach when developing and managing IT needs. Practically everybody at the C-suite will contribute their strategic inputs to ‘hybrid’ sources.

Moreover, the survey shows that this is just the beginning: most respondents (and particularly, respondents from very large Asian enterprises) expressed a willingness to use utility models for the majority of their IT capabilities—even ‘sensitive’ IT assets such as corporate and client data.

That said, decision-makers still have many concerns about virtualising their IT. These stem from the historical legacy which the cloud brings with it and could slow down the speed and scale with which their cloud transformation takes place. Long-standing issues were amongst our respondents’ top concerns: nearly three quarters of them cited both data privacy and cyber-security risks as affecting their adoption decisions in a negative way; nearly one-third of respondents felt that maintaining sufficient data privacy conditions—for their own, and their customers’ data—was a major deterrent to adoption. Other issues, such as the lack of technical talent, or cloud resources did not seem to be that great a deterrent to the IT transformation aspirations of Economist Corporate Network members. While this is encouraging on one level, perhaps these findings are telling us that Asia’s business leaders don’t know what they don’t know—which further implies that there are more subtle, and difficult, technology adoption issues for them ahead.

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

3© The Economist Corporate Network 2014

ASIA’S VIRTUOUS IT CYCLE EMERGESAsia’s long boom endures. Asia’s markets continue to expand rapidly, fueled in large part by the speedy growth of consumer demand within each the region’s domestic economies, and increasingly as a result of trade between them. Since 2000, inter-regional trade has grown six-fold in value in developing Asia alone: exports within emerging Asian economies is now more than $60bn monthly, and has doubled in proportion to more than 15% of the region’s total international trade. Home to two thirds of the global population, and the world’s fastest growing cohorts of middle class consumers, Asia’s economic destiny is intertwined with its technological destiny. Increased wealth and greater access to digital service platforms means that the demands on Asia’s Internet ecosystem grow even more intense: EIU data suggests that Asia’s consumers will see their average disposable incomes roughly double in the coming decade, and over 950m of those consumers will access the Internet through a smartphone this year, according to forecast data from eMarketer.

Thus, the dynamics of Asia’s economics and its demographics are putting intense pressure on enterprise ITC infrastructure, and network services—though depending on the market, these pressures can be very different. Much of Asia is generating considerable advantage from their ‘demographic dividend’ of increasing numbers of youthful, aspirational consumers and workers; Indonesia, Vietnam and other South East Asian economies will see over 100m new workers added to payrolls over the next quarter-century, and India and the rest of South Asia should see four times as many. As fast as these youthful markets are growing, other markets—chiefly Asia’s biggest economies, China and Japan—are ageing and shrinking as rapidly. The IT strategy implications for these two types of markets are quite distinct, but also linked in a common pursuit of efficiency. Younger, poorer economies, with millions of tech-savvy consumers have high digital expectations but a low ability to pay for IT-enabled services. Asian-based businesses will have to tease out customer insights from this group to access and service them cost-effectively. On the other end of the demographic spectrum, China will continue to have richer, older (and fewer) workers, and thus its enterprises need to invest in technologies and processes to get the most out of them.

Added to this is the powerful gravitational pull of Asia’s ‘e-conomy’: as Asian consumers and enterprises escalate their usage of e-commerce services and social media, they create massive amounts of data. This offers enterprise decision makers with copious amounts of raw material from which customer insight and operational performance perspectives can be extracted. This rising tide of Big Data in Asia, and the innovative ways in which applications and services are developed and deployed from it, is informing digital commerce trends globally.

Geo-cyberpolitics adds another dimension to Asia’s digital ecosystems. Concerns about security and data sovereignty, are putting pressure on stakeholders to ‘localise’ digital assets, even as network services themselves are further virtualising and moving to the cloud. Regarded with optimism, this may actually speed up the development of nation-specific cloud services in response to domestic data sovereignty laws which require customer and other operational data to be ‘housed’ within the

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

4 © The Economist Corporate Network 2014

physical jurisdiction (fairly restrictive measures have recently been implemented in Asian IT markets as disparate as Australia and Indonesia). Will this accelerate the trend towards inter-connected ‘clouds of clouds’ as a result? The availability of cloud-based resources for applications and processes is also increasing, as is the ‘software-ification’ of network resources. This has meant that there has been a step change in the power and cost-effectiveness of all the technology resources from which IT-dependent businesses in Asia can benefit.

HOW CLOUDY IS ASIAN BUSINESS?Insight from the Economist Corporate Network member surveyAsia’s complex collection of economic and technology drivers is thus creating a gathering of the clouds for Asian enterprises, one complemented by the rising tide of big data in the world’s single largest collection of markets. Asian enterprises need to leverage their IT assets across the entirety of their operations, not only for convenience and competitive advantage, but for efficiency, and—perhaps—even for sustainable development. All these factors taken together may accelerate the pace of IT innovation for Asian-based businesses. Cloud computing and utility models will definitely help Asian businesses continue on their success trajectory. What remains to be seen is if Asian businesses will pursue cloud adoption in uniquely innovative ways, and whether cloud adoption challenges unique to Asia will prevent these technologies from being as transformational as they could be in this region.

To understand the current state of play with cloud and utility IT adoption in the Asian enterprise, the Economist Corporate Network surveyed 106 senior executives across Asia Pacific on their role in making IT decisions for their Asian-based organizations. The survey also examined which aspects of IT capabilities are currently being placed onto the cloud (or in the hands of a cloud-based or virtualized service provider). Nearly half of our respondents were C-level, and 20% each were the CEO or the CIO (see Figure 1). We also asked them to what extent they were willing to convert various IT assets (ranging from network and communications infrastructure to their corporate and customer data) to on-demand or virtual service providers. To put it simply: we were looking to understand the extent to which strategic benefits of virtualized ITC outweighed the concerns, and whether that equation will hasten or slow IT transformation in the region.

Technology ‘literate’ firms were perhaps over-represented in our survey responses: over a quarter came from the IT and software space, with another significant slice from financial services. This may have introduced a slight ‘pro-cloud’ bias in the responses, and indeed adoption levels were slightly (but only slightly) higher than the rest of the survey’s heterogeneous industry respondents (see Figure 2). Respondent company sizes were somewhat evenly spread across

Figure 1Respondents by job title

0

20

40

60

80

100

Source: Economist Corporate Network survey

(%)

Manager reporting into CEO or CFO

Business Unit Director

CIO

CEO or Managing Director

COOCFO or primary budget holder

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

5© The Economist Corporate Network 2014

the spectrum; roughly a quarter of respondents were each from very small (less than $10m in 2013 revenue) and very large ($10bn and up) companies. This gave us insight into small firms that were both (presumably) strapped for internal IT resources and those that, as large corporates, could leverage considerable internal capabilities. (Ironically—or perhaps not—our small-sized respondents skewed very heavily towards the IT sector, so perhaps they are better IT-resourced than the average SME). Below, we examine responses to our survey, and what it implies for ITC strategy for Asian and Asian-based operations.

ROLES IN IT DECISION-MAKINGPrimary responsibilities in the IT investment process

The boss calls the IT shots40% of respondents thought that the head of the company was the ultimate decision-maker on IT projects—more than the CIO (see Figure 3). This was even more prevalent amongst firms with more than $5bn in revenues: 60% of large firms said that the CEO took the lead in technology planning. Asia-based enterprises see the strategic importance of IT, and the firm’s most senior executive is clearly seen to have IT implementation decisions worthy of his or her time. A couple of driving factors contribute to this. An obvious one is the aforementioned economic shifts in Asia, forcing both the

Figure 2Respondents by industry

Source: Economist Corporate Network survey

(%) Chemicals 1%Consumer goods 2.9%

Electronics 2.9%

Government 6.7%

Healthcare 1.9%Hotels & leisure 2.9%

IT & software 23%

Manufacturing 5.8%Media & marketing 6.7%

Mining, metals & minerals 1%

Pharmaceutical 2.9%

Professional services 4.8%

Property & construction 4.8%

Retail 1.9%

Telecoms 7.7%

Transport & logistics 3.8%

Other, please specify 10.6%

Engineering 1%Financial services 7.7%

Respondents’ estimated global revenues in 2013 (US$bn)

0

5

10

15

20

25

US$10bn or more

US$5bn to US$10bn

US$1bn to US$5bn

US$500m to US$1bn

US$100m to US$500m

US$50m to US$100m

US$10m to US$50m

Less th

an US$10m

Source: Economist Corporate Network survey

Nearly half of all IT sector respondents had less than $10m in revenue

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

6 © The Economist Corporate Network 2014

need to extract operational efficiencies quickly, while trying to extract more top-line value. In looking to keep pace with these changes, the head of the business has had to stay close to the issues which have the greatest potential impact on both.

Another contributing factor may be the consumerization of IT—one reason why the CEO ‘gets’ the relationship between IT and strategic change. “With more devices, and more accessible technology permeating the lives of senior executives, a deepening familiarity with IT is created,” observes Cardi Prinzi, President of Global Markets, Pacnet, “as is an understanding of the transformational power it holds.” The ‘embedding’ of smartphones, tablets and digitally enabled processes into senior executives’ lives also means that all C-suite decision makers likely feel they have more of a direct stake in their firm’s IT adoption.

Two cheque-signers are better than oneNotably, the largest number of respondents

indicate that the CIO’s primary responsibility in technology adoption is determining the cost implications of IT decisions, and making the investment decision based on that. At the same time, nearly as many thought this was the CFO’s primary job. While this may imply ambiguity in the decision-making process, or an expansion of the CIO’s role, it is more likely that the implication of this finding is that the evaluation of the ROI implications of tech decisions is a core task of the management board, and multiple stake-holders are likely needed to weigh in on this.

Everybody’s got something to addDefining the business case and the specifications for IT performance in Asian enterprises is obviously a shared management responsibility. But again, the increasing presence of IT in more business processes, and the resultant familiarity with the capability of ITC assets, means that decisions about specifications can be diffused and decentralized without compromising direction, allowing line managers or business unit ‘owners’ to increase their direct input into the process.

Figure 3What is the primary role of each senior executive in making IT decisions?(%)

Source: Economist Corporate Network survey

ChiefInformation

Officer orequivalent

ChiefExecutiveOfficer orManagingDirector

ChiefFinancial

Officer

Business UnitHead

Other

0

10

20

30

40

50

60

70

80

90

100

Primary ‘architect’ and ultimate decision maker for the organisationEvaluation of options and financial influencerDefinition of business requirements and influencerSpecification only for specific projectsNo direct role in technology adoption decisions

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

7© The Economist Corporate Network 2014

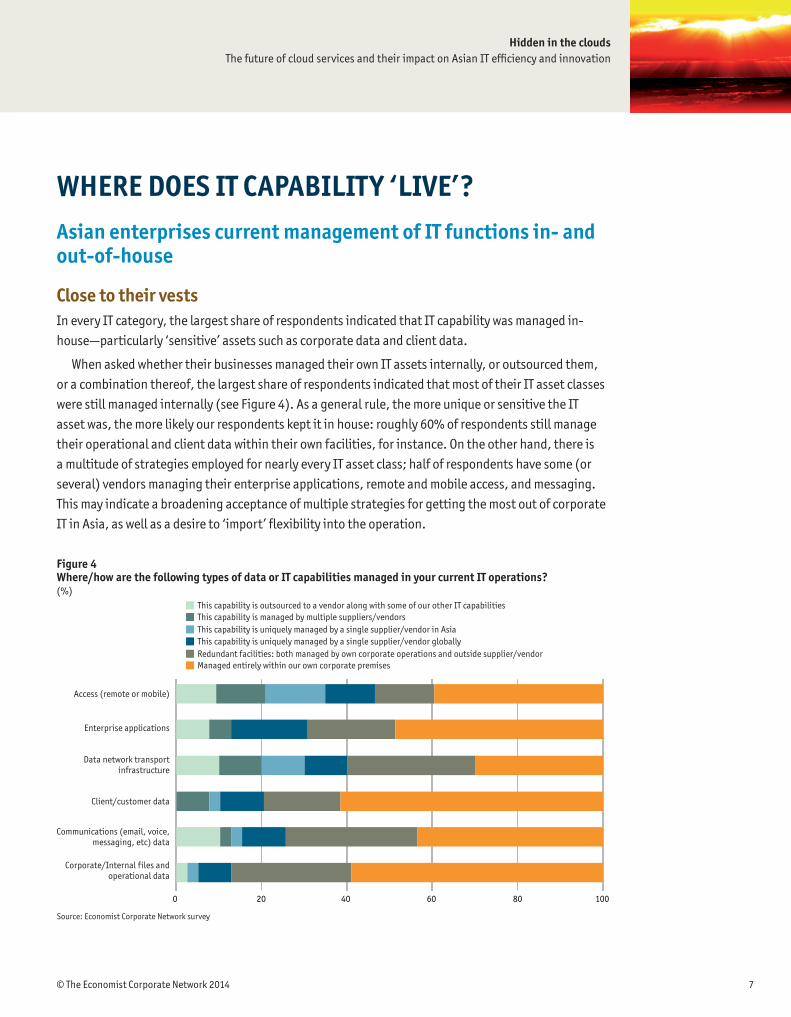

WHERE DOES IT CAPABILITY ‘LIVE’?Asian enterprises current management of IT functions in- and out-of-house

Close to their vestsIn every IT category, the largest share of respondents indicated that IT capability was managed in-house—particularly ‘sensitive’ assets such as corporate data and client data.

When asked whether their businesses managed their own IT assets internally, or outsourced them, or a combination thereof, the largest share of respondents indicated that most of their IT asset classes were still managed internally (see Figure 4). As a general rule, the more unique or sensitive the IT asset was, the more likely our respondents kept it in house: roughly 60% of respondents still manage their operational and client data within their own facilities, for instance. On the other hand, there is a multitude of strategies employed for nearly every IT asset class; half of respondents have some (or several) vendors managing their enterprise applications, remote and mobile access, and messaging. This may indicate a broadening acceptance of multiple strategies for getting the most out of corporate IT in Asia, as well as a desire to ‘import’ flexibility into the operation.

0 20 40 60 80 100

Figure 4Where/how are the following types of data or IT capabilities managed in your current IT operations?(%)

Source: Economist Corporate Network survey

Access (remote or mobile)

Enterprise applications

Data network transportinfrastructure

Client/customer data

Communications (email, voice,messaging, etc) data

Corporate/Internal files andoperational data

This capability is outsourced to a vendor along with some of our other IT capabilitiesThis capability is managed by multiple suppliers/vendorsThis capability is uniquely managed by a single supplier/vendor in AsiaThis capability is uniquely managed by a single supplier/vendor globallyRedundant facilities: both managed by own corporate operations and outside supplier/vendorManaged entirely within our own corporate premises

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

8 © The Economist Corporate Network 2014

Large enterprises DON’T do IT themselvesResults for respondents from companies with more than $5bn in global revenues are somewhat different from the mean. With the exception of ‘internal’ data, only about a quarter of respondents indicated that their IT capabilities were solely managed in house. The majority of respondents from large firms indicated that combined management or outsourced relationships were the norm. Particularly notable was data transport and management; a quarter of large firms outsource it along with other parts of their IT operations.

Back-up plansWhile full-fledged outside party management of IT assets was relatively low (and comprehensive outsourcing virtually non-existent) many IT capabilities were managed by multiple sources—particularly transport and communications infrastructure—pointing to Asian enterprises’ perceived needs to maintain back-up data.

HOW CRITICAL ARE ASIAN IT RESOURCES?How IT capabilities are meeting Asian business objectives

No longer ‘just plumbing’Our survey findings point to an increasing appreciation of the strategic importance of all IT assets. With the exception of remote and mobile access, only a minority of respondents thought that their

Figure 5How would you rate the strategic importance of each of these IT capabilities to your business in Asia?(%)

Source: Economist Corporate Network survey

Corporate/Internalfiles and

operational data

Communications(email, voice,

messaging, etc)data

Client/customer data

Data networktransport

infrastructure

Enterpriseapplications

Access(remote or mobile)

0

10

20

30

40

50

60

70

80

90

100

Significant to our operations, but not mission criticalMission critical/critically important to meeting business objectivesStrategically important–used to execute new revenue and/or efficiency projectsA source of unique competitive advantage to our operations

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

9© The Economist Corporate Network 2014

IT capabilities were ‘not mission critical’, or even more integral to their business operations (see Figure 5). 20% or less than that thought that enterprise applications and client data were ‘not mission-critical’; clearly decision-makers see that IT is far from simply a ‘plumbing’ capability within the organisation.

KYC for strategic success Unsurprisingly, customer data is seen as the single most significant component of their IT assets. The old adage (if not a post-crisis compliance requirement for financial services and other sectors) that a firm must “Know Your Customer” to succeed is taken extremely literally by our Economist Corporate Network survey respondents: half of respondents thought that customer data was either “strategically important” or “a source of unique competitive advantage”. Clearly, this belief explains why most respondents also felt (as stated above) that managing client data was something the firm needed to do themselves.

Mission-critical, or just reliable? Respondents in the majority saw data networks and enterprise apps as ‘mission-critical’. As many thought that their enterprise apps were a uniquely-defined competitive asset as did their customer data (roughly ten percent each). This would seem to sit at odds with the earlier finding which showed that management of enterprise apps was the most ‘diffuse’ IT asset of all: as many respondents indicated that they outsourced app management, either to one vendor, or many, and often bundled with ‘one-stop-shop’ managed service providers.

Perhaps, however, this is not a discrepancy at all: redundancy in service provision, and/or keeping multiple options for management open, could be seen as a way to maintain IT integrity in and of itself. This is particularly important in the fast-evolving ecosystem of enterprise applications; relying exclusively on internal developers and team members is often seen as a good way to doom an app to obsolescence in the digital economy, no matter how ‘unique’ it is. This, in turn, provides a strong rationale specifically for engaging cloud and utility platforms in the management and development of enterprise apps, to take advantage of ongoing ‘cloud-sourced’ innovation.

HOW UTILITY-BASED COULD YOU BE?Willingness to use utility models in achieving strategic objectivesIt would appear that this rationale is, at least implicitly, integrated into the IT decision-making processes of our survey respondents. When asked whether they would place their various IT capabilities on the cloud, or with a utility-based service provider, over three-quarters of respondents said they would in some fashion—with the exception, of course, of the ‘internal’ capabilities of corporate and customer data (see Figure 6). But a surprising number of respondents indicated that even these assets

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

10 © The Economist Corporate Network 2014

were up for cloud evaluation, which will be discussed below. This is yet another piece of confirming evidence that acceptance of the cloud and cloud-like offerings are growing in Asia.

Customers on the cloud? Half of respondents indicated that they would never outsource the management of customer data, reflecting its perceived high strategic value. Yet, another sizable cohort (over a quarter of respondents) indicated that they actually would consider cloud/utility adoption. Again, while several factors are likely driving this, the main factors are the confluence of acceptance, and growing demand for efficiency. The cloud may also, for far-sighted executives, offer a unique proposition for trying to get the most out of customer data: many new CRM solutions, as well as analytics and other ‘big data’ management options live in the cloud, or are managed by providers in hybrid private-public clouds.

Heading for the utility modelMore mature outsourcing categories (communications, data network) show the most willingness to consider cloud or utility models, but generally most categories show respondents with a high willingness to consider utility models.

Figure 6To what degree WOULD your technology decision-making team consider outsourcing each of the following ITcapabilities?(%)

Source: Economist Corporate Network survey

Corporate/Internalfiles and

operational data

Communications(email, voice,

messaging, etc)data

Client/customer data

Data networktransport

infrastructure

Enterpriseapplications

Access(remote or mobile)

0

10

20

30

40

50

60

70

80

90

100

Could completely outsource capability to on-demand/utility/virtual service-based providerMay outsource capability to on-demand/utility/virtual service-based provider, with our own managed back-upCould completely outsource capability to facilities-based service providerMay outsource capability to facilities-based service provider, with our own managed back-upMay enlist service provider to manage our own facilitiesWould not ever outsource this capability to a third party

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

11© The Economist Corporate Network 2014

HOW CLOUDY IS YOUR COMPANY?The current state of cloud ‘readiness’ in AsiaLeading on from this high willingness to consider virtualizing their IT operations, it is little surprise that two-thirds of Economist Corporate Network survey respondents have already engaged cloud-based solutions (see Figure 7). Perhaps the most telling insight from these responses is that nearly one-fifth of respondents are actively converting the majority of their IT resources into cloud utilities—and while nearly as many have stated they have no cloud plans at all, “the extent to which Asian enterprises are already on the cloud is indicative of how swiftly the cloud is becoming a integral component of IT strategy,” says Pacnet’s Prinzi.

IS THE CLOUD STILL A CONCERN?Current state of cloud concerns in the decision making processAnd yet, if there were no concerns or misperceptions about utility models, it could be argued that the cloud would be even farther embedded in Asian IT operations than our survey suggests it currently is. Our respondents were quite clear that despite their familiarity and willingness to use cloud resources, there remain deep concerns within their organisations, and many issues are still holding back their adoption plans. When asked to consider a range of ‘hurdles’, from talent and network resource availability to cyber security, roughly half of our respondents felt all these issues were, across the board, to some extent held back, or were holding back their adoption decisions (see Figure 8). Perhaps unsurprisingly in the post-Snowden, post-Heartbleed world, respondents’ top concerns were data privacy issues and cyber security, with the former being more critical: nearly a third of respondents thought the state of data privacy in Asia was a ‘major deterrent’ to adoption.

Data privacy is likely a more complex issue than our simple question adequately captured. A few years ago, stuffing sensitive company and client data on the cloud was viewed as an implicit security and privacy risk, the outlook is more nuanced today. Regulations and compliance rules that governments and policy makers have implemented around the proper management, use and even physical housing of client data have made a difference. Indeed, concerns around data sovereignty in Asia were a close third in our respondents’ ranking of concerns.

Figure 7Which best describes your company’s current approach to cloud computing in Asia?

Source: Economist Corporate Network survey

(%)

We are actively converting most IT resources onto the cloud 17.1%

31.4%We have selectively placed some of our IT resources onto

the cloud

We have used cloud-based solutions occasionally, or on a project basis 11.4%

We have plans to deploy cloud alternatives in the next year 2.9%

We are evaluating cloud options 20%

We have no plans 17.1%

Hidden in the cloudsThe future of cloud services and their impact on Asian IT efficiency and innovation

12 © The Economist Corporate Network 2014

Clouds hitting wallsOn the other hand, the relatively low concern about cloud asset availability—whether in terms of knowledgeable talent, or data centre or network resources in Asia—may tell us something about challenges yet to come. While cloud resources are being speedily developed in the region, they still trail behind the US and Europe by a large margin and, as mentioned, are not proliferating as quickly as smartphones and other Internet-connected devices in Asia. Pacnet’s Prinzi feels, as a result, “Asian business leaders likely don’t know what they don’t know about the resource availability in Asia’s cloud ecosystem,” and that could mean that their cloud development plans could soon hit an unanticipated wall.

Figure 8Do the following issues impact or delay your cloud adoption plan?(%)

Source: Economist Corporate Network survey

Local market talent availability

Cloud resource availability

Data sovereignty issues

Local market regulations

Cyber security risks

Data privacy issues

Does not affect our decisions at allMakes consideration and evaluation more lengthy, but does not have negative impact on our decisionsMakes consideration and evaluation more lengthy, and can have negative impact on our decisionsUsually has a negative impact and/or delays our decisionsGreat negative impact; major deterrent to adoption

0 25 50 75 100

Beijing, Hong Kong, Kuala Lumpur, Shanghai, Singapore, TokyoFor enquiries, please contact us at [email protected] follow us on Twitter @ecn_asia

About Economist Corporate Network AsiaEconomist Corporate Network (ECN) is The Economist Group’s advisory, briefing and networking service for Asia-based senior executives seeking insight into economic and business trends in key growth markets. Through a tailored blend of interactive meetings, high-calibre research, and private client briefings, ECN Asia delivers country-by-country, regional, global and industry-focused analysis.