HfS Research Blueprint: HR Operations in the As-a-Service ... · The Services Research Company HfS...

64

The Services Research Company HfS Research Blueprint: HR Operations in the As-a-Service Economy Excerpt for Accenture May 2016 Mike Cook Research Director, HRaaS [email protected] @MikeMarkC

Transcript of HfS Research Blueprint: HR Operations in the As-a-Service ... · The Services Research Company HfS...

The Services Research Company

HfS Research Blueprint: HR Operations in the As-a-Service EconomyExcerpt for Accenture

May 2016

Mike CookResearch Director, [email protected]@MikeMarkC

©2016 HfSResearch Proprietary │Page2Excerpt forAccenture.

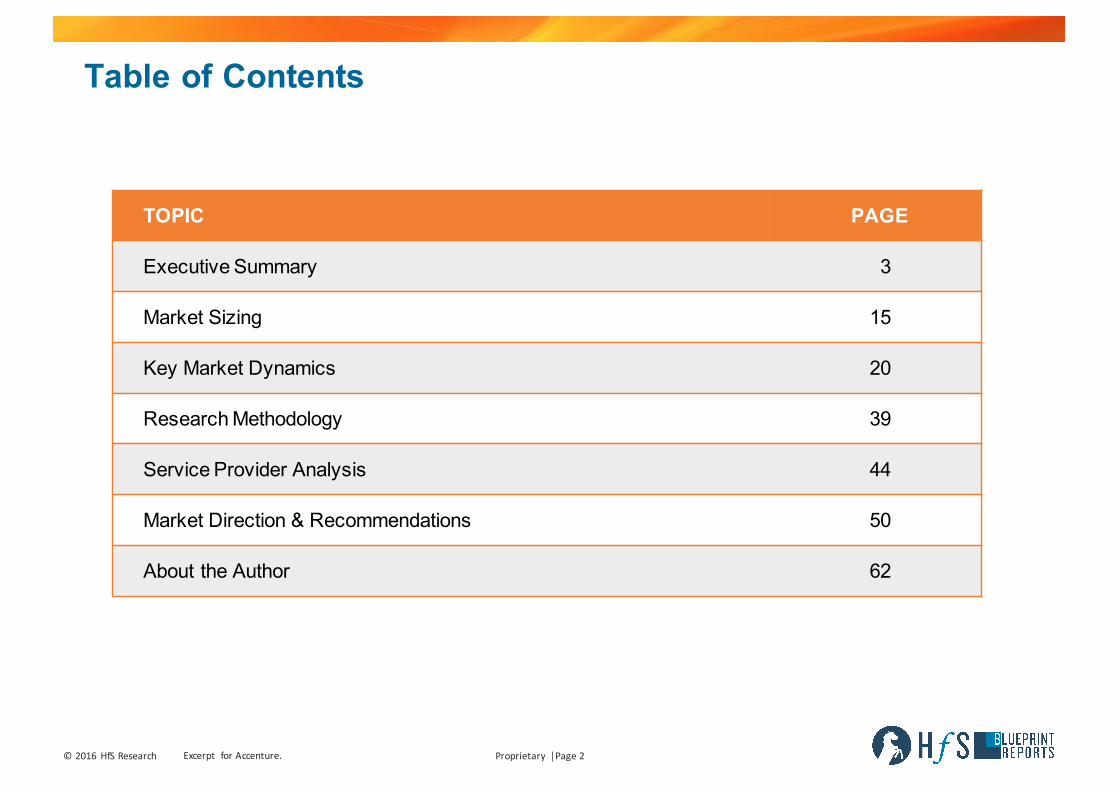

Table of Contents

TOPIC PAGE

Executive Summary 3

Market Sizing 15

Key Market Dynamics 20

Research Methodology 39

Service Provider Analysis 44

Market Direction & Recommendations 50

About the Author 62

Executive Summary

Proprietary │Page4©2016 HfSResearch Ltd. Excerpt forAccenture.

Introduction to the 2016 HfS Blueprint Report: HR Operations in the As-a-Service Economy

n HfS Research takes a fresh look at HR Operations—the Multi-Process HR BPO market in this Blueprint,reviewing the market activity and a comparative analysis of the innovation and execution capabilitiesof 13multi-national, multi-functional service providers.

n These service providers have multi-process HR (MPHRO) business process support capability in theirportfolio—at least two of the following services: Recruitment Process Outsourcing (RPO), Learning,Benefits Admin, Payroll, Workforce Development Services andHR Analytics.

n Two of the significant elements in the emerging HR market are cloud-based HCM platformimplementation and management and the managed delivery of HR business services. Along theselines, the scope of the Blueprint covers SaaS-based HCM implementation and managed multi-processHR services for the functional areas.

n This research takes a look at the evolution of HR BPO to a market that is increasingly agile,collaborative and consumer-centric. HfS considers this transition in outsourcing a move to the As-a-Service Economy, placing increasing value on diverse talent, analytics, and collaboration, as well asincreasingly on platform-based services.

n As such, in this Blueprint we use the Eight Ideals of The As-a-Service Economy as a significant elementof our service provider assessment methodology. The eight ideals describe the operations of servicebuyers and service buyers in a business-outcome focused outsourcing partnership.

Proprietary │Page5©2016 HfSResearch Ltd. Excerpt forAccenture.

Introduction to the 2016 HfS Blueprint Report: HR Operations in the As-a-Service Economy, Cont.

n As the MPHRO market matures there is an increasing focus on the underpinning cloud HCM platformsused in the delivery of HR service. Buyers recognize this and as such are seeking service providers whonot only have excellent service delivery credentials but can implement, manage and optimize thesenew HCM platforms to extract maximum value; essentially embracing ideals of the As-A-ServiceEconomy.

n A key element of the report is the focus by both service providers and buyers on employeeengagement. Therefore, as HfS looks at the MPHRO market and the role of service providers, it is fromthe perspective of enabling closer ties to employees, often using automation and analytics to supportthis engagement.

n This report does not include a software evaluation of MPHRO related features and functions, althoughreference will be made to certain tools.

Proprietary │Page6©2016 HfSResearch Ltd. Excerpt forAccenture.

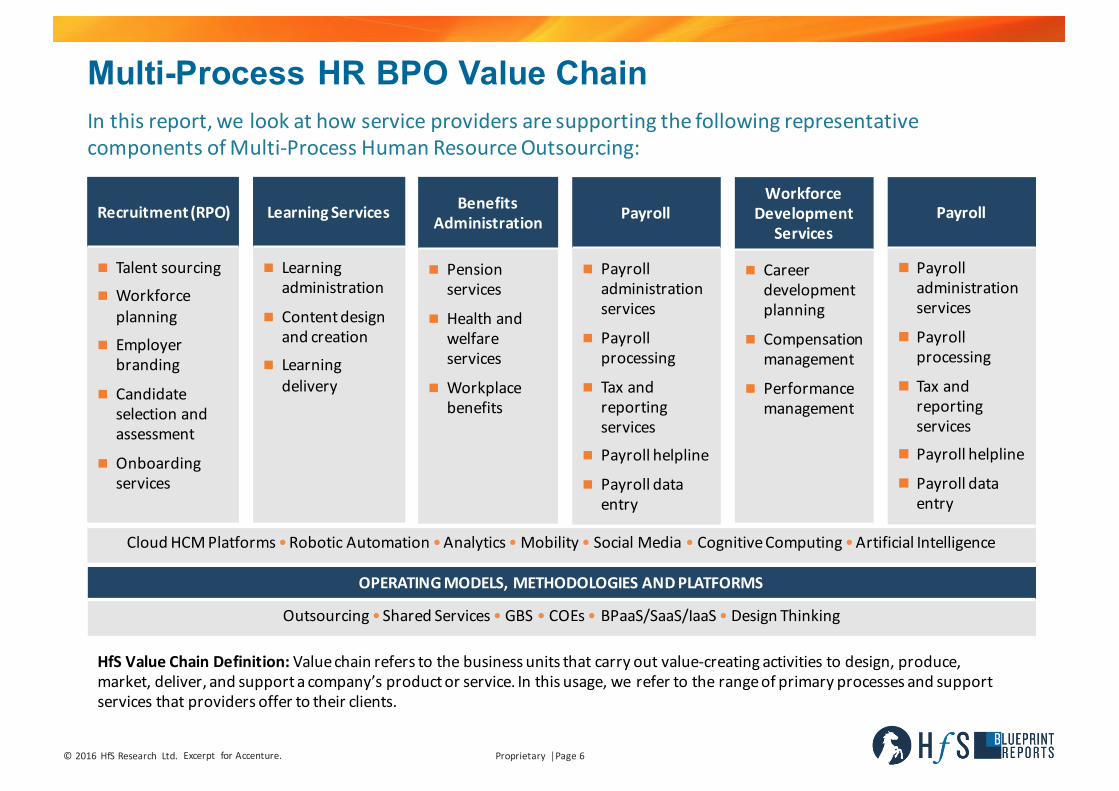

WorkforceDevelopment

Services

n Careerdevelopmentplanning

n Compensationmanagement

n Performancemanagement

BenefitsAdministration

n Pensionservices

n Healthandwelfareservices

n Workplacebenefits

Recruitment(RPO)

n Talentsourcing

n Workforceplanning

n Employerbranding

n Candidateselectionandassessment

n Onboardingservices

LearningServices

n Learningadministration

n Contentdesignandcreation

n Learningdelivery

HfSValueChainDefinition:Valuechainreferstothebusinessunitsthatcarryoutvalue-creatingactivitiestodesign,produce,market,deliver,andsupportacompany’sproductorservice.Inthisusage,werefertotherangeofprimaryprocessesandsupportservicesthatprovidersoffertotheirclients.

Payroll

n Payrolladministrationservices

n Payrollprocessing

n Taxandreportingservices

n Payrollhelpline

n Payrolldataentry

CloudHCMPlatforms•RoboticAutomation•Analytics• Mobility• SocialMedia• CognitiveComputing•ArtificialIntelligence

OPERATINGMODELS,METHODOLOGIESANDPLATFORMS

Outsourcing•SharedServices• GBS• COEs• BPaaS/SaaS/IaaS• DesignThinking

Inthisreport,welookathowserviceprovidersaresupportingthefollowingrepresentativecomponentsofMulti-ProcessHumanResourceOutsourcing:

Multi-Process HR BPO Value Chain

Payroll

n Payrolladministrationservices

n Payrollprocessing

n Taxandreportingservices

n Payrollhelpline

n Payrolldataentry

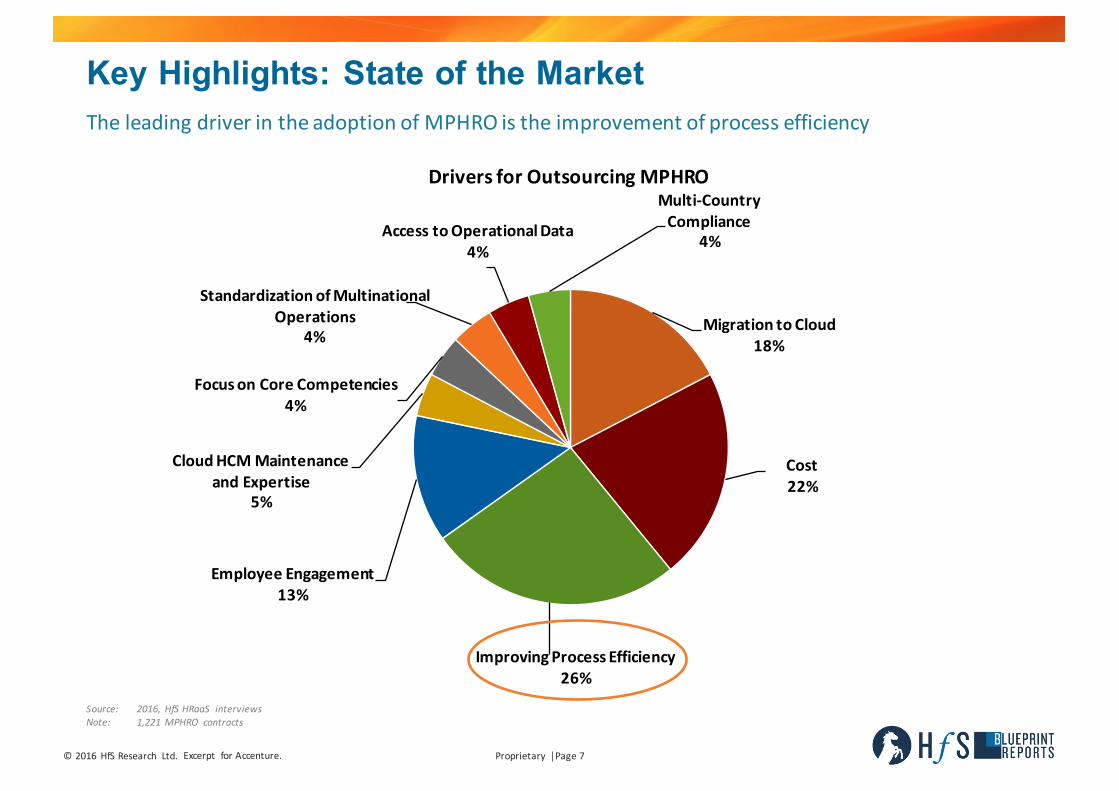

©2016 HfSResearch Ltd. Proprietary │Page7Excerpt forAccenture.

MigrationtoCloud18%

Cost22%

ImprovingProcessEfficiency26%

EmployeeEngagement13%

CloudHCMMaintenanceandExpertise

5%

FocusonCoreCompetencies4%

StandardizationofMultinationalOperations

4%

AccesstoOperationalData4%

Multi-CountryCompliance

4%

TheleadingdriverintheadoptionofMPHROistheimprovementofprocessefficiency

DriversforOutsourcingMPHRO

Key Highlights: State of the Market

Source: 2016, HfSHRaaS interviewsNote: 1,221MPHRO contracts

Proprietary │Page8©2016 HfSResearch Ltd. Excerpt forAccenture.

Key Highlights: State of the Market, Cont.

n Improving Process Efficiency is the Key Driver: Outsourcing in the MPHRO market is now primarilydriven by the need for improving process efficiencies within buyer HR departments, specifically with theU.S, U.K, and Continental Europe. Much of the process improvement involves the application ofAutomation and Analytics within the areas of: data capture and transfer, auditing and compliance, queryresolution, email response and auctioning and rules based processing within the HR function.

n Cost Is No Longer the Primary Driver to Outsource MPHRO: Through client interviews, service providerbriefings, and additional research, HfS observes that the market is no longer primarily led by the needfor cost take-out. Having said this there is still of course a need to reduce the price of operations. Clientsin the U.S. are the predominant group still driven to outsourcing MPHRO in order to remove cost. Thisindicates that price is still a differentiator among MPHRO service providers but it doesn’t carry the sameimportance it once did.

n Multi-Country Deals Are Increasing: Multi-country MPHRO deals are continuing to rise. This is leadingmany service providers to partner with local and/or large payroll providers in order to deliver on thesecontracts. ADP is used as a payroll partner by 33% of the leading MPHRO service providers. Around 80%of service providers covered in this Blueprint partner with either large payroll providers or in countrypayroll specialists to deliver on these long tail payroll contracts.

n Bundling Patterns of MPHRO Deals: Currently the most common bundling of HR functions withinMPHRO deals are workforce development services, payroll and helpdesk support. Recruitment andlearning support are usually provided on a standalone basis. This mix of services has remained constantfrom historic MPHRO contracts.

Proprietary │Page9©2016 HfSResearch Ltd. Excerpt forAccenture.

Key Highlights: State of the Market, Cont.

n Technology Catchup is Stimulating MPHRO Growth in APAC: Much of the MPHRO growth in the APACregion, specifically Australia, is driven by the need to adopt cloud based HCM platforms and applicationsas many organizations in the region have been slow to implement. This has created a follow on scenariowheremany implementation only deals have evolved into deals that include service delivery.

n The Emergence of Employee Engagement: The need to increase employee engagement is now a keyconsideration across buyer organizations. Losing highly trained employees in a market with limitedtalent resources is more expensive than ever. As such, service providers are now brought in to addressthe business outcome of reducing attrition through increasing employee engagement. Capgemini’sDigital Maturity Assessment aims to ascertain where a client is in terms of employee engagement, forexample.

n Multi-Departmental Coverage Challenges Adoption of MPHRO: Having to engage and win over anumber of service line department heads within the MPHRO value chain is a challenge service providershave to overcome when selling MPHRO contracts. There is also a reluctance to change within themiddle-tiers of management, further exacerbating the problem. A sales focus on the c-suite andappealing to business outcomes within the c-suite is assisting in overcoming this inhibitor. Serviceproviders are building up their consulting capability and increasingly starting with transformationalprojects that ultimately lead into service delivery.

n Data Privacy is Still a Concern for Buyers: Multiple buyers are inhibited in the adoption of outsourcedMPHRO due to the security concerns of releasing personal employee information to a third party.Service providers such as Xerox have leveraged internal data security teams from the wider organizationto address the concerns of clients and build robust securitymeasures.

Proprietary │Page10©2016 HfSResearch Ltd. Excerpt forAccenture.

Key Highlights: State of the Market, Cont.

n Long Sales Cycles Denting MPHRO Adoption: Due to the multi-departmental challenge of sellingMPHRO contracts, there is an inherently longer sales cycle than other functions such as finance orcustomer service that are often centralized. As such there is a risk of key stakeholders in the buyerorganization moving on before a deal is brought to conclusion, thereby bringing negotiations back anumber of steps. This reemphasizes how important it is for service providers to be speaking to c-levelexecutives at a strategic level from the outset. Building scope into long-term engagement will helpaddress this as both sides of the party can then build on an existing relationship.

n Majority of MPHRO Contracts Use a Multi-Tiered Pricing Model: Within the MPHRO stack: payroll,elements of RPO (primarily onboarding), benefits administration and talent management are largelypriced on either a per employee/transaction or FTE basis. Increasingly an element of outcomes basedpricing is included in these contracts. SaaS offerings are priced on a subscription basis while learning isoccasionally priced on a fixed price basis.

n FTE Pricing is Declining in Popularity: Only 25% of MPHRO contracts now contain an element of FTEpricing; it is now being replaced by per employee/transaction pricing for managed service offeringswhich is now included in 54% of MPHRO contracts. Per employee/transaction pricing is more conduciveto fostering a BPaaS contract as service providers will not cannibalize revenues, through the use ofautomation and other efficiency enhancements, to the same extent as when FTE pricing is used. Thispricing model in addition to an element of outcomes pricing is the best compromise for both serviceproviders and buyers.

Proprietary │Page11©2016 HfSResearch Ltd. Excerpt forAccenture.

Key Highlights: State of the Market, Cont.

n Prescriptive and Predictive Analytics are a Differentiator: The use of prescriptive and predictiveanalytics, specifically in workforce development services, payroll and RPO is set to become adifferentiator in the MPHRO market. This form of analytics has been rolled out by HCM softwaremanufacturers at this point (Ultimate Software) but is in the pipeline from many service providers aseither an application or embedded within proprietary HCM platforms. For example OneSource Virtual isset to go-to-market with a packaged prescriptive and predictive analytics application by H2 2016. Thiswill, at the front end, be a verticalized scorecard of behavioral characteristics for employees by industryand job type which then seeks to identify churn, at the predictive level, but then also the best remedy,at the prescriptive level.

n Multi-Tenancy of F&A and HRO is Increasing in Adoption: BPO organizations that offer multiple servicelines are starting to see an increased adoption of HRO by current F&A clients. Capgemini and Infosys inparticular are now making HRO service delivery a priority as these service providers look to growportfolios.

n Legacy HCM is On its Way Out: Approximately 55% of the buyers covered in this Blueprint are nowusing cloud based HCM systems. The most common of these been Workday and SuccessFactors,followed by Oracle HCM. Therefore the move from legacy systems such as SAP is now well on its way.Nearly all buyers covered in this Blueprint have stated their intention to move to a cloud based HCMplatform at some point in the future. Wide scale BPaaS engagements (where the service provider usesits own resources of talent and technology to deliver an agreed upon business outcome) are still a wayoff. At this stage theMPHRO market is largely defined by platform enabled BPO.

Proprietary │Page12©2016 HfSResearch Ltd. Excerpt forAccenture.

Key Highlights: State of the Market, Cont.

n Consultation on Cloud HCM Implementation Is An Entry point For MPHRO Services: With thelargescale move to cloud HCM platforms there is a niche created for consultation around theseplatforms. The majority of the consulting at this point is handled by the likes of Deloitte although bothmulti-tenant and pure HR service providers such as Accenture, IBM, Capgemini, NGA HR and Infosys areusing this implementation as an entry point for managed service delivery of MPHRO.

n Verticalization of Services in MPHRO is Not Relevant But Understanding Businesses Is: There is almostno verticalization of MPHRO services by service providers. The standardization of processes aroundpayroll and RPO administration are not industry specific. Where there is service specialization isbetween blue collar and white collar workforces, specifically in the areas of timemanagement, learningand workforce development services.

n Contract Duration Remaining Stable: Contract duration for the MPHRO market is remaining consistentwith previous studies into the MPHRO marketwith most contracts at 3-5 year duration.

n Desire for Proven Practices from Other Clients: HfS heard quite a bit of interest from clients wantingnew ideas and practices from, and more interaction with, other clients. While most service providers areproviding cross client communication at some level, for the most part this has not been taken to level atwhich it is really needed, whereby a framework/platform is created for HR best practice in relation toHCM platform used.

Proprietary │Page13©2016 HfSResearch Ltd. Excerpt forAccenture.

Key Highlights: State of the Market, Cont.

n As-a-ServiceWinnersinthisBlueprintarearticulatinganddemonstratingthemostmatureuseofthe8IdealsoftheAs-a-ServiceEconomytoincreasethevalueofsourcingintargetedareasofMPHRO:

• Accenturehasadistinctmixofservicedeliveryexpertiseandtechnologicalinnovation

• Xeroxhasadevelopedframeworkforinnovationandisactivelybringingthistothetableinclientdiscussions

• NGAHRhasredefineditsimplementationstrategyonafitforpurposeapproach,combiningserviceandcloudHCMimplementationandmaintenance

• AonHewitt hasthescaleandoperationalexpertisetoexcel

• ADP’sglobalpayrollcoveragecoupledwithitsapproachtodesignthinkingmakeitaleaderintheMPHROmarket

AS-A-SERVICEECONOMY

Useofoperatingmodels,enablingtechnologiesandtalenttodrivebusinessoutcomesthroughoutsourcing.Thefocusisonwhatmatterstotheendconsumer.

HfSusestheword“economy”todescribethenextphaseofoutsourcingasanewwayofengagingandmanagingresourcestodeliverservices.

The8IdealsoftheAs-a-ServiceEconomy:1. Write OffLegacy2. DesignThinking3. IntelligentEngagement4. BrokersofCapability5. IntelligentAutomation6. AccessibleandActionableData7. Holistic Security8. Plug&PlayDigitalServices

Source:BewareoftheSmoke:YourPlatformisBurningbyHfSResearch,2015

Proprietary │Page14©2016 HfSResearch Ltd. Excerpt forAccenture.

Key Highlights: State of the Market, Cont.

n TheHighPerformersareestablishedandwell-regardedserviceprovidersinMPHRO:

• OneSourceVirtual hastheidealsoftheAs-A-ServiceEconomyatitsroots

• Capgemini isbuildingonitsF&Aheritagetowinmulti-towerdealsandestablishitselfasaMPHROserviceproviderofchoice

• Neeyamo receivespraisefromitsclientbaseonitsexceptionaloperationaldelivery

• IBMeffectivelyleveragesinternalanalyticscapabilitytofurtherfutureservicedelivery

• CeridianisastrongoperationalserviceproviderintheUK,Ireland,U.SandCanada

n TheHighPotentialsareinnovativeandwell-regardedserviceprovidersinMPHRO:

• Infosysisfocusedontechnologicalinnovation

AS-A-SERVICEECONOMY

Useofoperatingmodels,enablingtechnologiesandtalenttodrivebusinessoutcomesthroughoutsourcing.Thefocusisonwhatmatterstotheendconsumer.

HfSusestheword“economy”todescribethenextphaseofoutsourcingasanewwayofengagingandmanagingresourcestodeliverservices.

The8IdealsoftheAs-a-ServiceEconomy:1. Write OffLegacy2. DesignThinking3. IntelligentEngagement4. BrokersofCapability5. IntelligentAutomation6. AccessibleandActionableData7. Holistic Security8. Plug&PlayDigitalServices

Source:BewareoftheSmoke:YourPlatformisBurningbyHfSResearch,2015

Market Sizing

Proprietary │Page16©2016 HfSResearch Excerpt forAccenture.

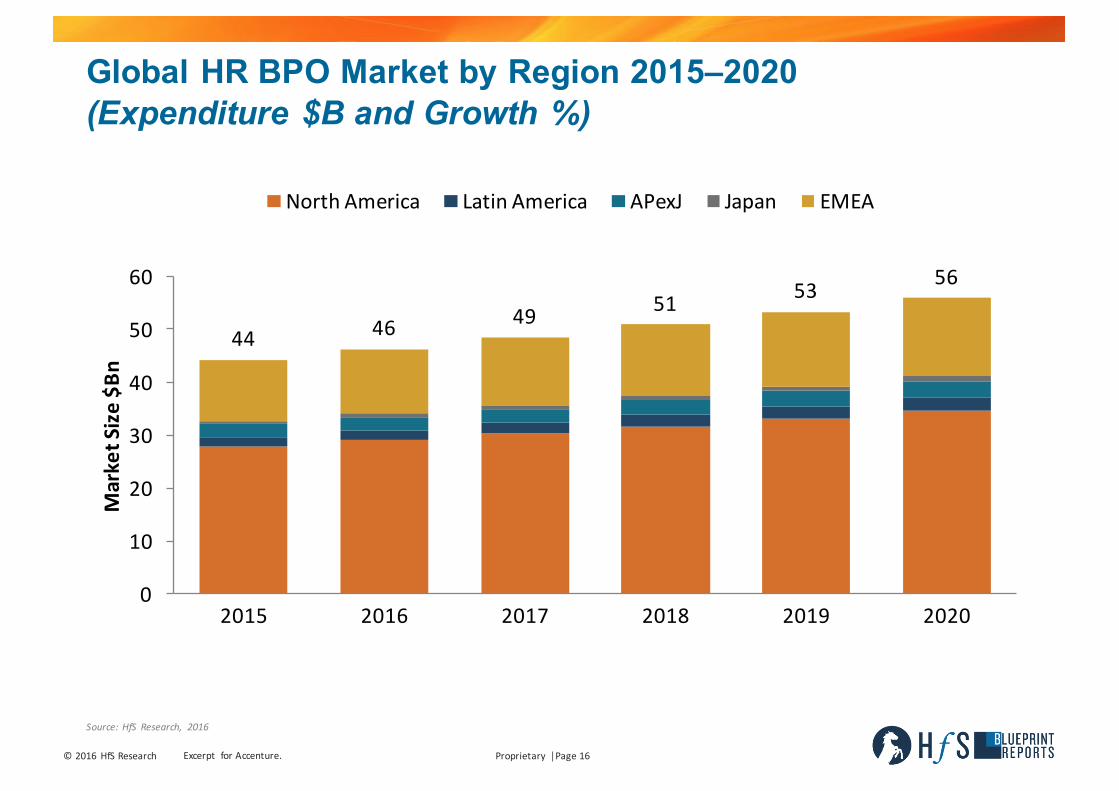

Global HR BPO Market by Region 2015–2020 (Expenditure $B and Growth %)

Source: HfS Research, 2016

44 46 49 51 53 56

0

10

20

30

40

50

60

2015 2016 2017 2018 2019 2020

MarketSize$B

n

NorthAmerica LatinAmerica APexJ Japan EMEA

Proprietary │Page17©2016 HfSResearch Excerpt forAccenture.

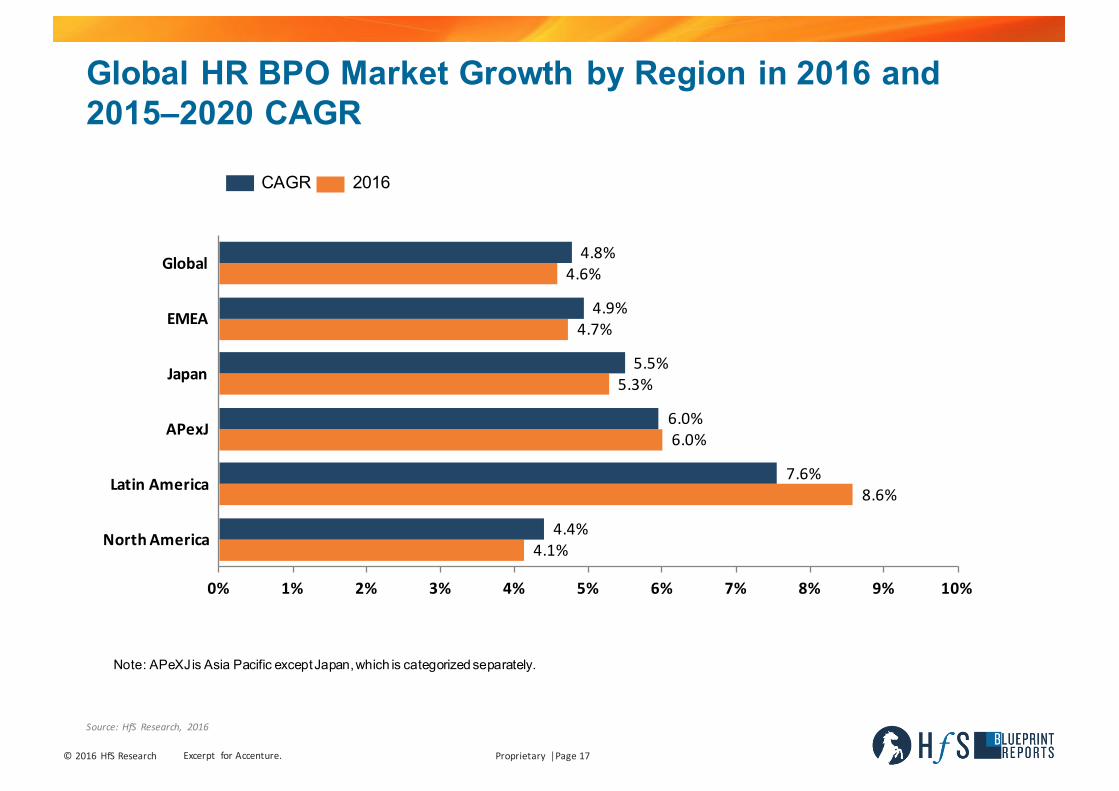

Global HR BPO Market Growth by Region in 2016 and 2015–2020 CAGR

Source: HfS Research, 2016

2016CAGR

4.1%

8.6%

6.0%

5.3%

4.7%

4.6%

4.4%

7.6%

6.0%

5.5%

4.9%

4.8%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

NorthAmerica

LatinAmerica

APexJ

Japan

EMEA

Global

Note: APeXJis Asia Pacific except Japan, which is categorized separately.

Proprietary │Page18©2016 HfSResearch Excerpt forAccenture.

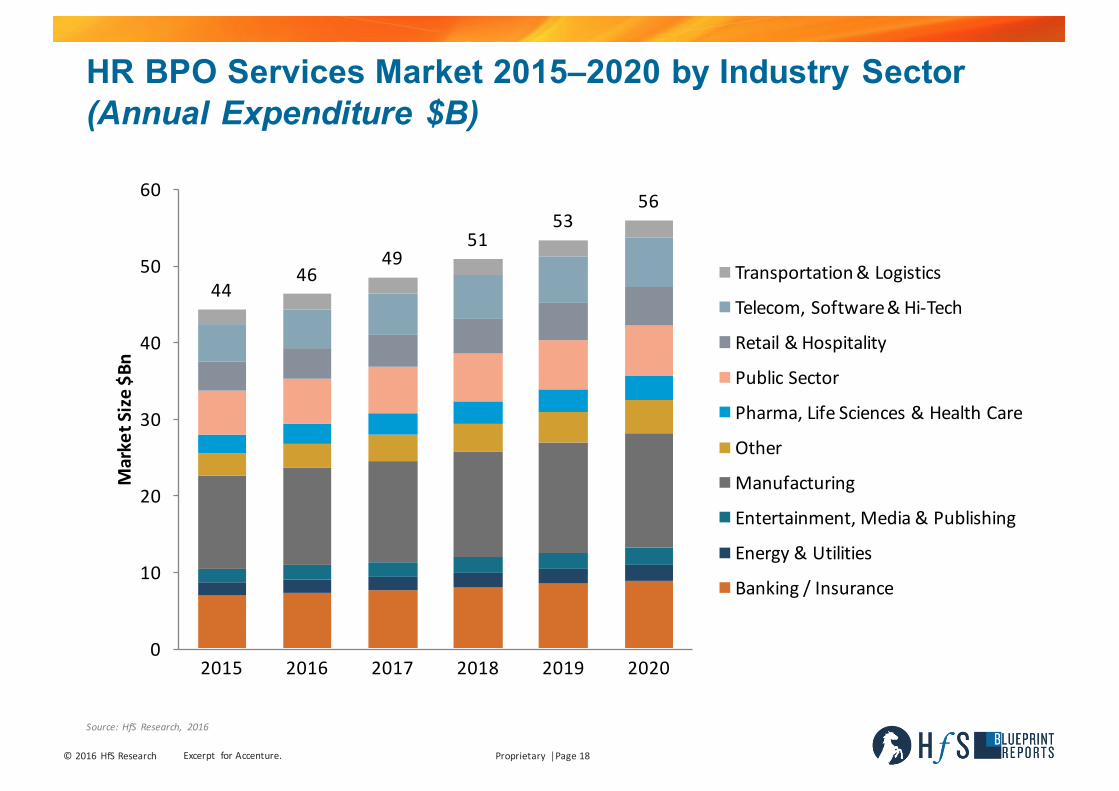

HR BPO Services Market 2015–2020 by Industry Sector(Annual Expenditure $B)

Source: HfS Research, 2016

4446

4951

5356

0

10

20

30

40

50

60

2015 2016 2017 2018 2019 2020

MarketSize$B

n

Transportation&Logistics

Telecom,Software&Hi-Tech

Retail&Hospitality

PublicSector

Pharma,LifeSciences&HealthCare

Other

Manufacturing

Entertainment,Media&Publishing

Energy&Utilities

Banking/Insurance

Proprietary │Page19©2016 HfSResearch Excerpt forAccenture.

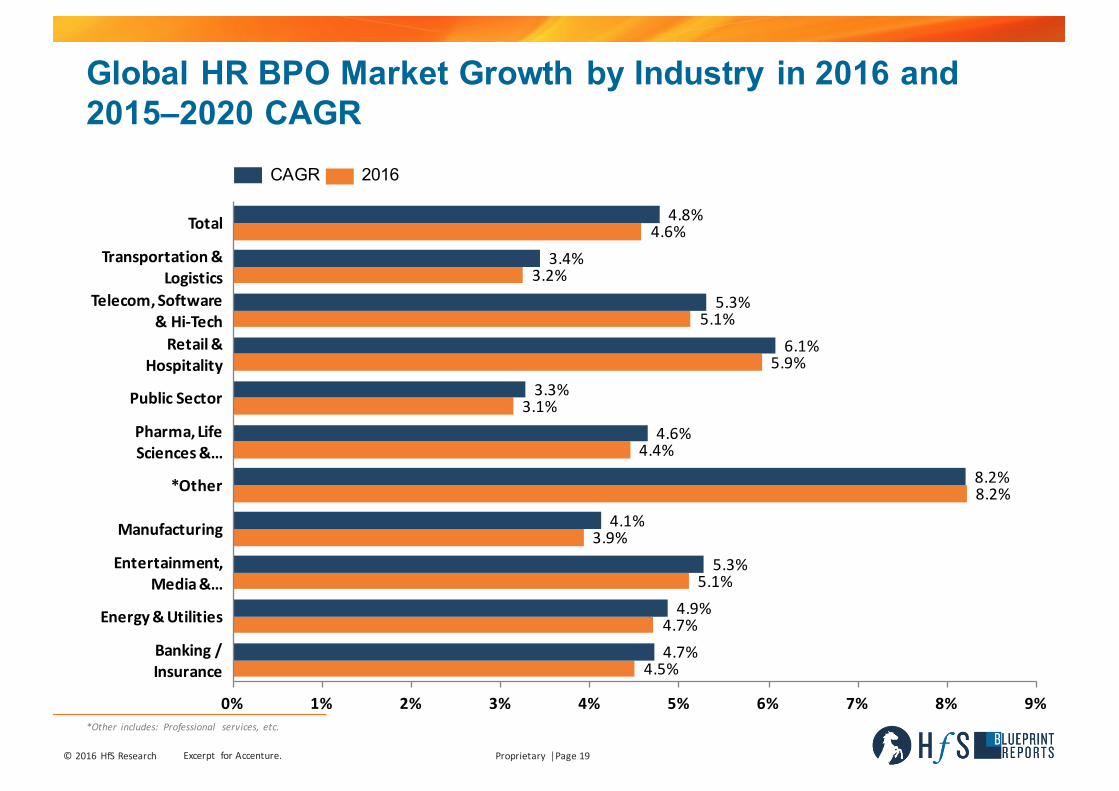

Global HR BPO Market Growth by Industry in 2016 and 2015–2020 CAGR

4.5%

4.7%

5.1%

3.9%

8.2%

4.4%

3.1%

5.9%

5.1%

3.2%

4.6%

4.7%

4.9%

5.3%

4.1%

8.2%

4.6%

3.3%

6.1%

5.3%

3.4%

4.8%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Banking/Insurance

Energy&Utilities

Entertainment,Media&…

Manufacturing

*Other

Pharma,LifeSciences&…

PublicSector

Retail&Hospitality

Telecom,Software&Hi-Tech

Transportation&Logistics

Total

2016CAGR

*Other includes: Professional services, etc.

Key Market Dynamics

©2016 HfSResearch Ltd. Excerpt forAccenture.

As the MPHRO market continues its evolution to an As-A-Service Economy, it is fundamental to understandwhy this evolution is taking place. The answer is employees. The need to attract, retain and nurture talentis now more important than ever as organizations look to grow and adapt to a more digital ecosystem.Corporate culture plays a part in this but mission critical is having a HR function that can improve employeeengagement and interact in a way that is natural to the employee.

As millennials enter the workplace, employee interaction has to change. The always on, always connectedworkforce is here. Organizations need to adapt HR functions accordingly and embrace mobile and cloudtechnology that can be accessed anyway and anytime.

Cloud HCM platforms have developed user interfaces that speak to this new workforce, but with ~50% oforganizations still using on premise legacy HCM systems, there is still a long way to go for manyorganizations. By partnering with proven service providers, organizations can now make the migration tothe cloud quickly and efficiently. Also by leveraging the managed service expertise of these providers,organizations are more enabled to focus on key moments of truth with employees thereby reducingemployee churn and having a more aligned, motivated and focusedworkforce.

Who Is the Employee?

Proprietary │Page22©2016 HfSResearch Ltd. Excerpt forAccenture.

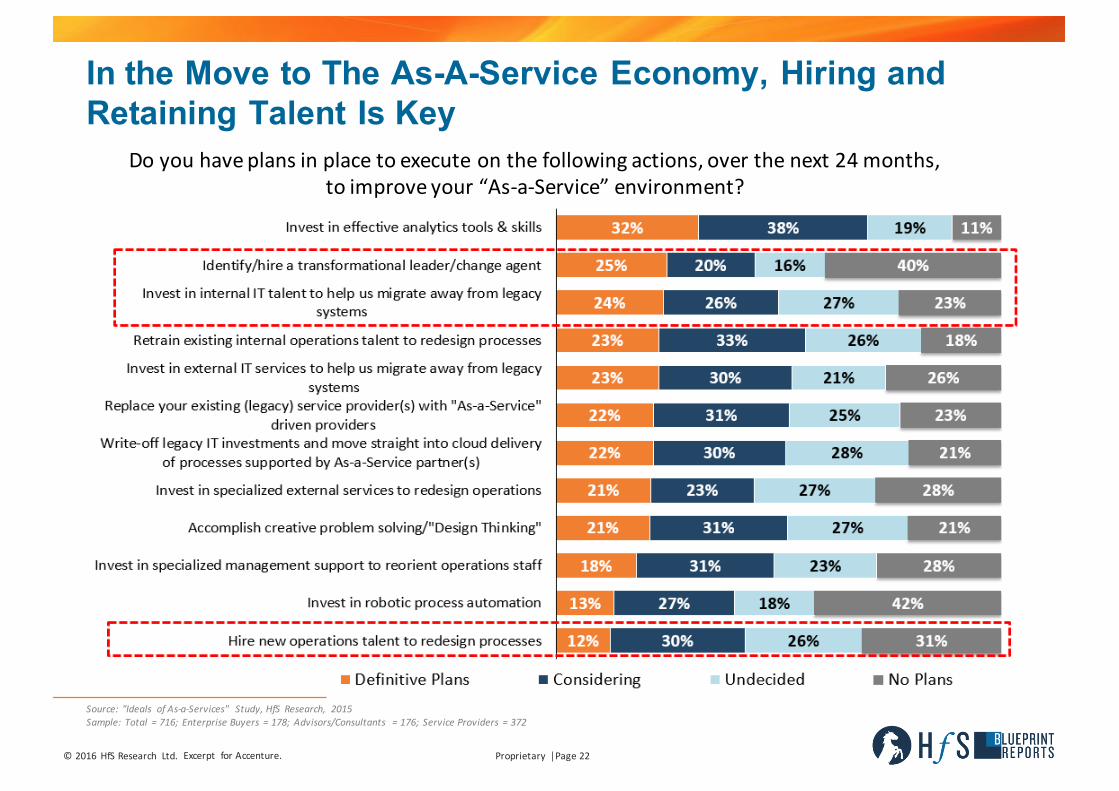

In the Move to The As-A-Service Economy, Hiring and Retaining Talent Is Key

Doyouhaveplansinplacetoexecuteonthefollowingactions,overthenext24months,toimproveyour“As-a-Service”environment?

Source: "Ideals ofAs-a-Services" Study,HfS Research, 2015Sample: Total =716; EnterpriseBuyers =178; Advisors/Consultants =176; ServiceProviders =372

©2016 HfSResearch Ltd. Excerpt forAccenture.

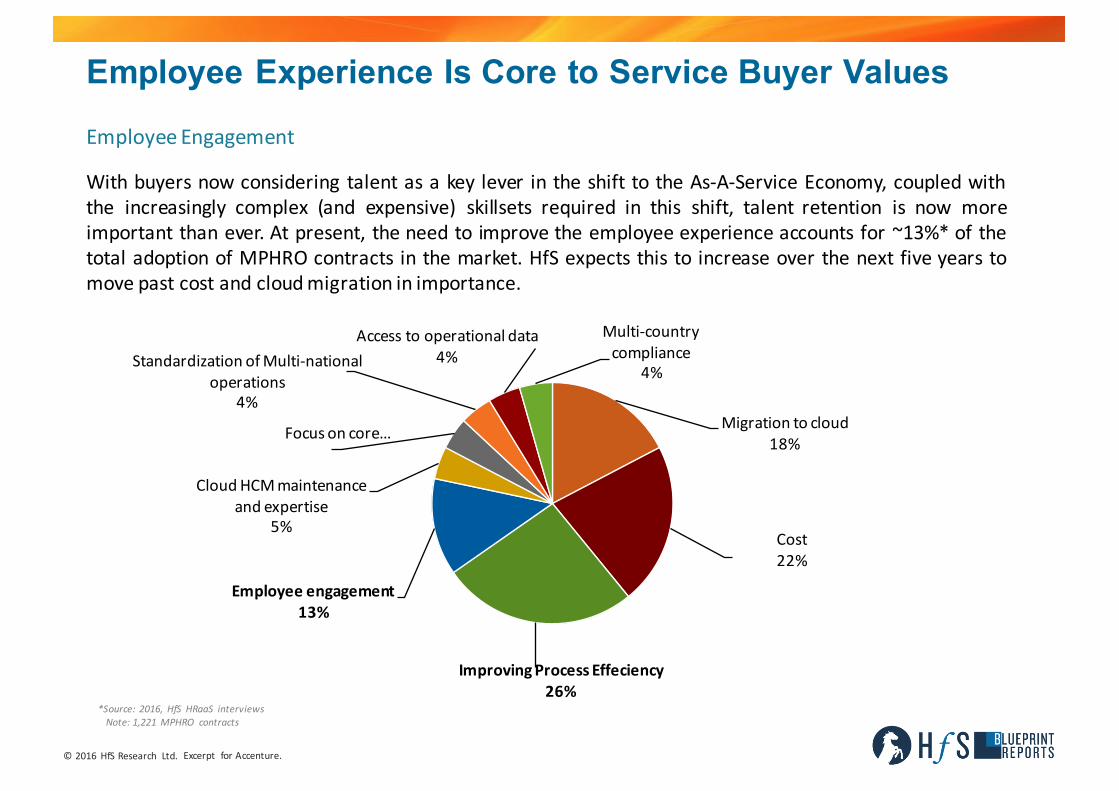

With buyers now considering talent as a key lever in the shift to the As-A-Service Economy, coupled withthe increasingly complex (and expensive) skillsets required in this shift, talent retention is now moreimportant than ever. At present, the need to improve the employee experience accounts for ~13%* of thetotal adoption of MPHRO contracts in the market. HfS expects this to increase over the next five years tomove past cost and cloudmigration in importance.

Employee Experience Is Core to Service Buyer Values

Migrationtocloud18%

Cost22%

ImprovingProcessEffeciency26%

Employeeengagement13%

CloudHCMmaintenanceandexpertise

5%

Focusoncore…

StandardizationofMulti-nationaloperations

4%

Accesstooperationaldata4%

Multi-countrycompliance

4%

*Source: 2016, HfS HRaaS interviewsNote: 1,221MPHRO contracts

EmployeeEngagement

©2016 HfSResearch Ltd. Excerpt forAccenture.

n Phase 1, Process Improvement: At present this is largely where both buyers and service providers aretargeting employee engagement as ~26% of MPHRO contracts are now won on a service provider’sability to provide a better, more streamlined HR function. This reduces employee frustration due toinaccurate HR processes and creates a more transparent working environment. The use of automationfor more mundane tasks and predictive analytics to detect likely employee churn, free up more time forHR managers to engage with and rectify employee concerns, leading to a more connected workforce. Atpresent all service providers covered in this Blueprint are able to deliver on this phase of employeeengagement.

Employee Experience Is Core to Service Buyer Values, Cont.

HfS seesthisasthemovetoaddressemployeeengagementtakingplaceintwophases:

©2016 HfSResearch Ltd. Excerpt forAccenture.

n Phase 2, Proactive Employee Engagement: Prescriptive and predictive analytics around talentmanagement are all well and good, but they are ultimately reactive measures to a problem already athand and are undertaken to maintain talent and will in the future be used as a measure of last resort.Therefore HfS sees the next stage in the evolution of MPHRO will revolve around employeeengagement. This will be a proactive step in reducing attrition in the workplace. This employeeengagement will take place from hire to retire across RPO, learning and workforce developmentservices.

In the RPO space, firms such as Hexaware are launching technologies that allow for quicker and moreengaged onboarding experiences, through mobile technology, for new hires. This is in response to thehigh dropout rate of new hires in the APAC market. As another example, the ADPMarketplace allows HRprofessionals to search and find vetted service provider and software capability with approved APIs toplug in and address specific elements of employee experience. There are also a raft of smallercompanies such as ZenNut, which are coming to the market with employee social interaction toolsaimed at creating community bonding within organizations. Large service providers will be looking tobuild and acquire capabilities in this area over the next five years.

Employee Experience Is Core to Service Buyer Values, Cont.

HfS seesthisasthemovetoaddressemployeeengagementtakingplaceintwophases:

©2016 HfSResearch Ltd. Excerpt forAccenture.

n Platform and Basic Service Framework Development: Currently the MPHRO market is in the earlystages of HR framework development and most activity is revolving around cloud softwareimplementation and basic service delivery in support of it. Previously the majority of service providershave gone to great lengths to create bespoke HR software implementations for clients, the cause of thiswas largely due to clients believing their HR operations were unique and service providers undertakinglift and shift HR delivery. The knock on effect of this was increased cost and time to deploy but alsoincreasingly complex software support post implementation.

Contracts such as these are also vulnerable to service delivery collapse as key stakeholders move onfrom both the provider and buyer side, taking with them IP that was crucial to the delivery of thesebespoke systems and services. Service providers are now in the process of creating best “fit forpurpose” implementations. NGA HR has done this in the UK market with its ResourceLink platform.Service frameworks are also beginning to be developed, for example, Capgemini is now undertakingmaturity assessments of clients’ HR operations and then adapting its HR services framework aroundthese.

Service Frameworks Are Key to Driving Innovation

With“Theneedforprocessefficiencyimprovements”asthepredominantdriverintheMPHROmarket,serviceprovidersareidentifyingwaysinwhichtoformalizeframeworksofservicedeliveryandtechnologyinordertoaddressthis.HfS seesthisstandardizationtakingplaceintwophases:

©2016 HfSResearch Ltd. Excerpt forAccenture.

n Business Outcomes Based Platform and Basic Service Framework Development: In the nearfuture, we believe service providers will deploy HR service frameworks aimed at addressing thebusiness outcomes of clients. Similar to what has happened in the contact center market where serviceproviders are beginning to implement frameworks to target increased revenue generation, customersatisfaction (CSAT), etc. The HR market will move in a similar direction, with service providersimplementing targeted frameworks aimed at addressing business outcomes, such as reducing attrition,either across the MPHRO value chain or in discrete processes. In order for this to be done, effectivebenchmarking and closer ties with top level management of buyer organizations need to be in place.Infosys is in the process of bringing this type of framework to market through its Business ValueDelivery (BVD) framework.

Service Frameworks Are Key to Driving Innovation, Cont.

With“Theneedforprocessefficiencyimprovements”asthepredominantdriverintheMPHROmarket,serviceprovidersareidentifyingwaysinwhichtoformalizeframeworksofservicedeliveryandtechnologyinordertoaddressthis.HfS seesthisstandardizationtakingplaceintwophases:

©2016 HfSResearch Ltd. Excerpt forAccenture.

Welcome to the As-a-Service EconomyHfSusestheword“economy”toemphasizethattheemergingnextphaseofoutsourcingisamoreflexible,outcomefocusedwayofengagingandmanagingresourcestodeliverservices.OperatingintheAs-a-ServiceEconomymeansarchitectinguseofincreasinglymatureoperatingmodels,enablingtechnologiesandtalenttodrivetargetedbusinessoutcomes.Thefocusisonvaluetotheconsumer—inthiscase,theemployee.

TOOLS/INFRASTRUCTURE GOVERNANCE

I.THEOPTIMUMOPERATINGMODEL

Outsourcing|SharedServicesGBS|BPaaS/SaaS/IaaS|Crowdsourcing

II.EMPOWERINGTALENTTOMAKEITALL

POSSIBLECapabilitiesoverSkills|

DefiningOutcomes|Creativity|DataScience

IV.TECHNOLOGYTOAUGMENTKNOWLEDGELABOR

Digitization&RoboticAutomation|Analytics|Mobility|SocialMedia|CognitiveComputing

III.ABURNINGPLATFORMFORCHANGE

GlobalizationofLabor|High-growthEmergingMarkets|

DisruptiveBusinessModels|Consumerization

AS-A-SERVICEECONOMY

Agility|CollaborationOne-to-Many|OutcomeFocus

Plug-and-PlayServices

©2016 HfSResearch Ltd. Excerpt forAccenture.

FixedAssetsLeveragedAssets

2DesignThinking

3BrokersofCapability

1WriteOffLegacy

4CollaborativeEngagement

7HolisticSecurity

5IntelligentAutomation

6Accessible&Actionable

Data

8Plug&PlayDigitalServices

SOLUTIONIdeals

LEGACYECONOMY

AS-A-SERVICEECONOMYCHANGEMGMT

Ideals

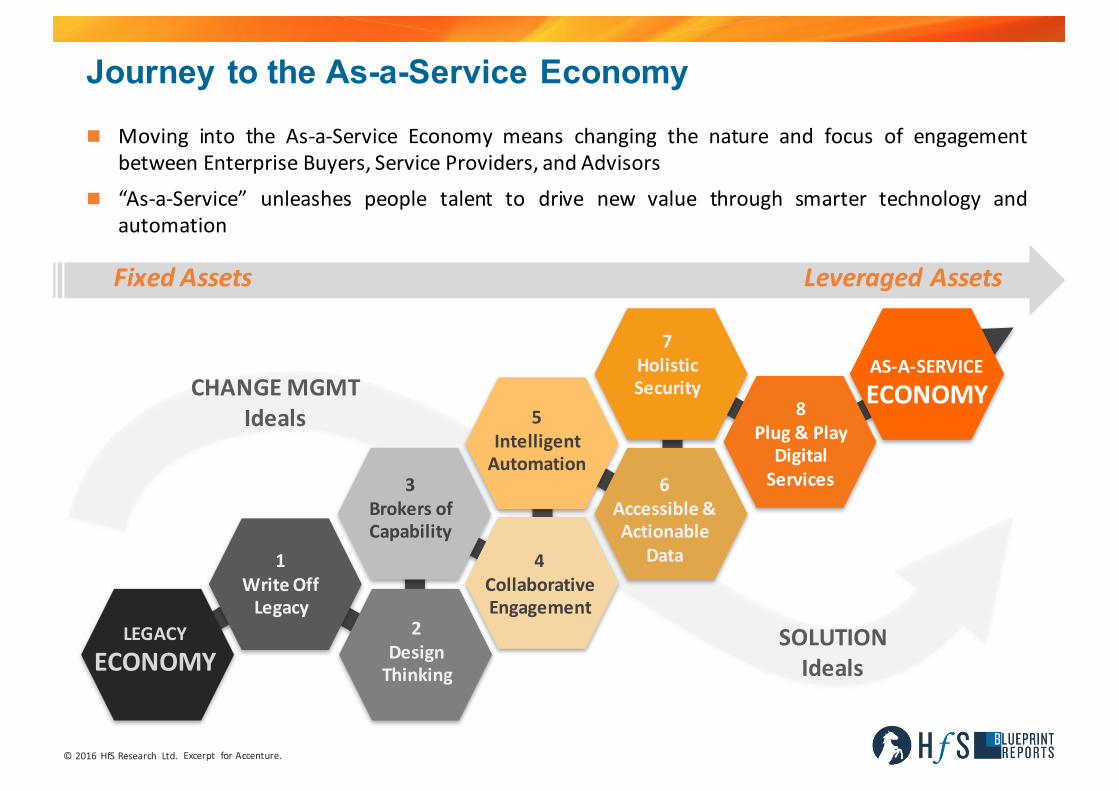

n Moving into the As-a-Service Economy means changing the nature and focus of engagementbetween Enterprise Buyers, Service Providers, and Advisors

n “As-a-Service” unleashes people talent to drive new value through smarter technology andautomation

Journey to the As-a-Service Economy

Proprietary │Page30©2016 HfSResearch Ltd. Excerpt forAccenture.

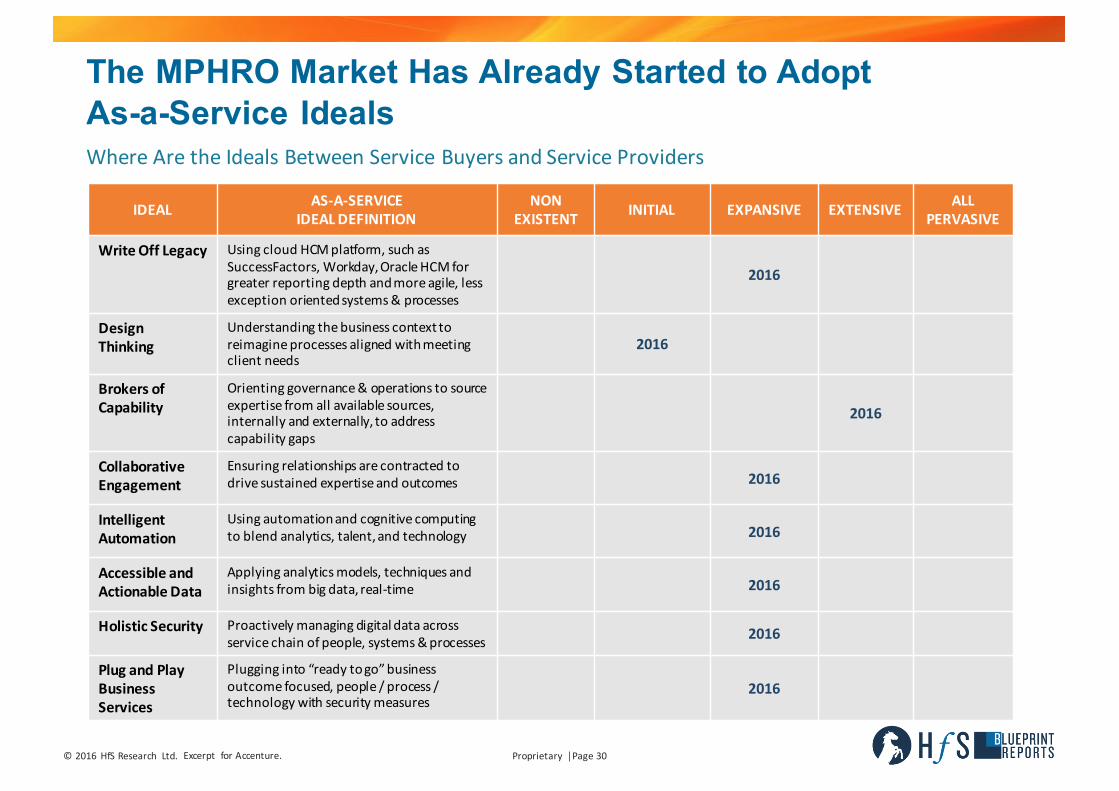

The MPHRO Market Has Already Started to Adopt As-a-Service Ideals

IDEAL AS-A-SERVICEIDEALDEFINITION

NONEXISTENT INITIAL EXPANSIVE EXTENSIVE ALL

PERVASIVE

WriteOffLegacy UsingcloudHCMplatform,suchasSuccessFactors,Workday,OracleHCMforgreaterreportingdepthandmoreagile,lessexceptionorientedsystems&processes

2016

DesignThinking

Understandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds

2016

Brokers ofCapability

Orientinggovernance&operationstosourceexpertisefromallavailablesources,internallyandexternally,toaddresscapabilitygaps

2016

CollaborativeEngagement

Ensuringrelationshipsarecontractedtodrivesustainedexpertiseandoutcomes 2016

IntelligentAutomation

Usingautomationandcognitivecomputingtoblendanalytics,talent,andtechnology 2016

Accessible andActionableData

Applyinganalyticsmodels,techniquesandinsightsfrombigdata,real-time 2016

Holistic Security Proactivelymanagingdigitaldataacrossservicechainofpeople,systems&processes 2016

PlugandPlayBusinessServices

Plugginginto“readytogo”businessoutcomefocused,people/process/technologywithsecuritymeasures

2016

WhereAretheIdealsBetweenServiceBuyersandServiceProviders

Proprietary │Page31©2016 HfSResearch Ltd. Excerpt forAccenture.

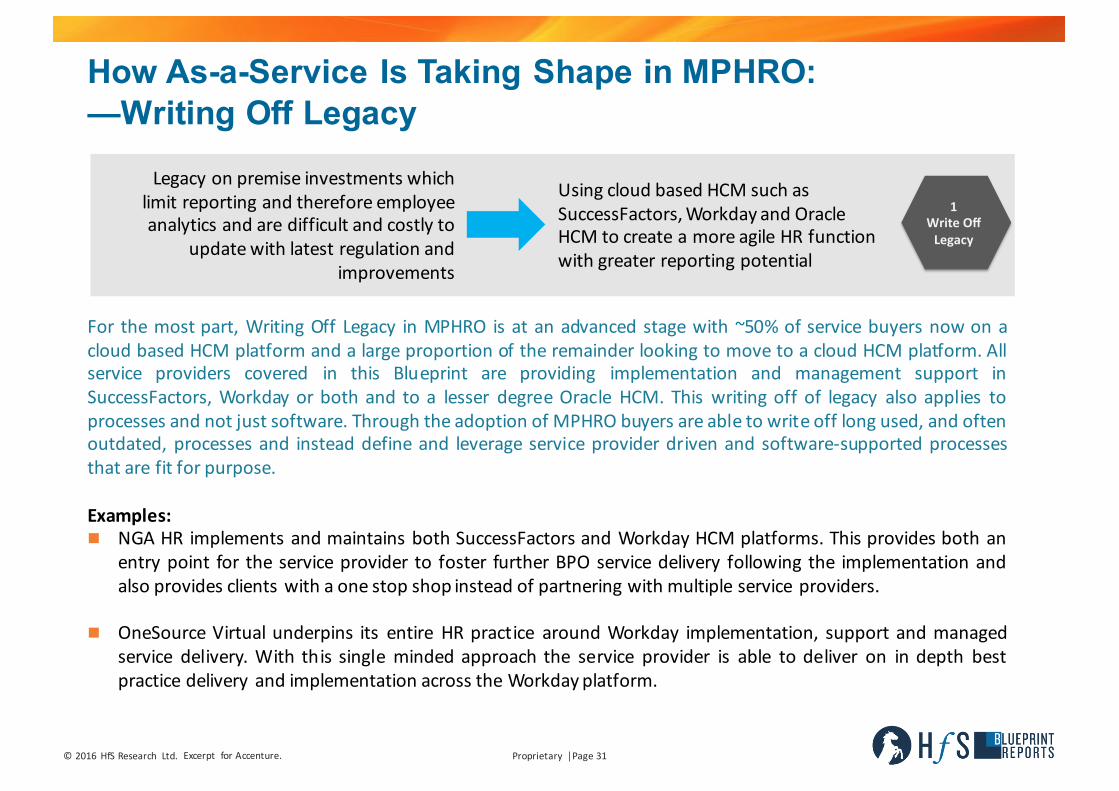

How As-a-Service Is Taking Shape in MPHRO: —Writing Off Legacy

1"Write"Off"Legacy"

Legacyonpremiseinvestments whichlimitreportingandthereforeemployeeanalyticsandaredifficultandcostlyto

updatewithlatestregulationandimprovements

Usingcloud basedHCMsuchasSuccessFactors,WorkdayandOracleHCMtocreateamoreagileHRfunctionwithgreaterreportingpotential

For the most part, Writing Off Legacy in MPHRO is at an advanced stage with ~50% of service buyers now on acloud based HCM platform and a large proportion of the remainder looking to move to a cloud HCM platform. Allservice providers covered in this Blueprint are providing implementation and management support inSuccessFactors, Workday or both and to a lesser degree Oracle HCM. This writing off of legacy also applies toprocesses and not just software. Through the adoption of MPHRO buyers are able to write off long used, and oftenoutdated, processes and instead define and leverage service provider driven and software-supported processesthat are fit for purpose.

Examples:n NGA HR implements and maintains both SuccessFactors and Workday HCM platforms. This provides both an

entry point for the service provider to foster further BPO service delivery following the implementation andalso provides clients with a one stop shop instead of partnering with multiple service providers.

n OneSource Virtual underpins its entire HR practice around Workday implementation, support and managedservice delivery. With this single minded approach the service provider is able to deliver on in depth bestpractice delivery and implementation across the Workdayplatform.

Proprietary │Page32©2016 HfSResearch Ltd. Excerpt forAccenture.

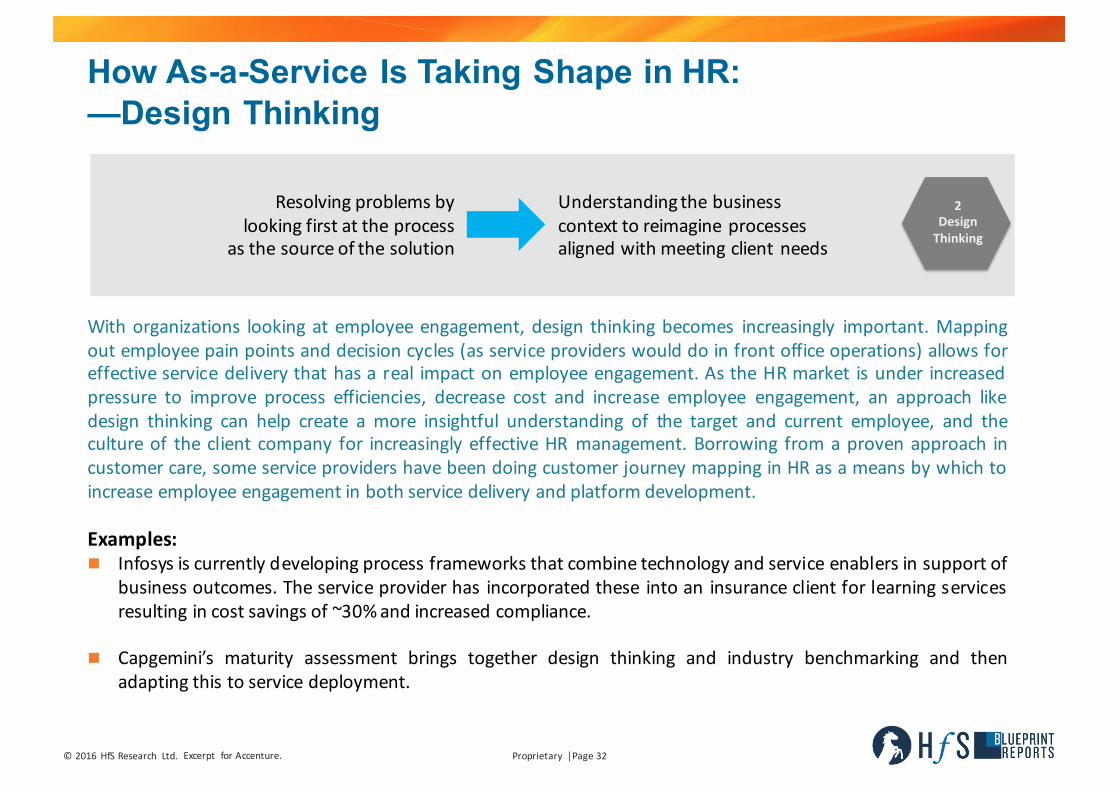

2"Design"Thinking"

How As-a-Service Is Taking Shape in HR: —Design Thinking

Resolvingproblemsbylookingfirstattheprocess

asthesourceofthesolution

Understandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds

With organizations looking at employee engagement, design thinking becomes increasingly important. Mappingout employee pain points and decision cycles (as service providers would do in front office operations) allows foreffective service delivery that has a real impact on employee engagement. As the HR market is under increasedpressure to improve process efficiencies, decrease cost and increase employee engagement, an approach likedesign thinking can help create a more insightful understanding of the target and current employee, and theculture of the client company for increasingly effective HR management. Borrowing from a proven approach incustomer care, some service providers have been doing customer journey mapping in HR as a means by which toincrease employee engagement in both service delivery and platform development.

Examples:n Infosys is currently developing process frameworks that combine technology and service enablers in support of

business outcomes. The service provider has incorporated these into an insurance client for learning servicesresulting in cost savings of ~30%and increased compliance.

n Capgemini’s maturity assessment brings together design thinking and industry benchmarking and thenadapting this to service deployment.

Proprietary │Page33©2016 HfSResearch Ltd. Excerpt forAccenture.

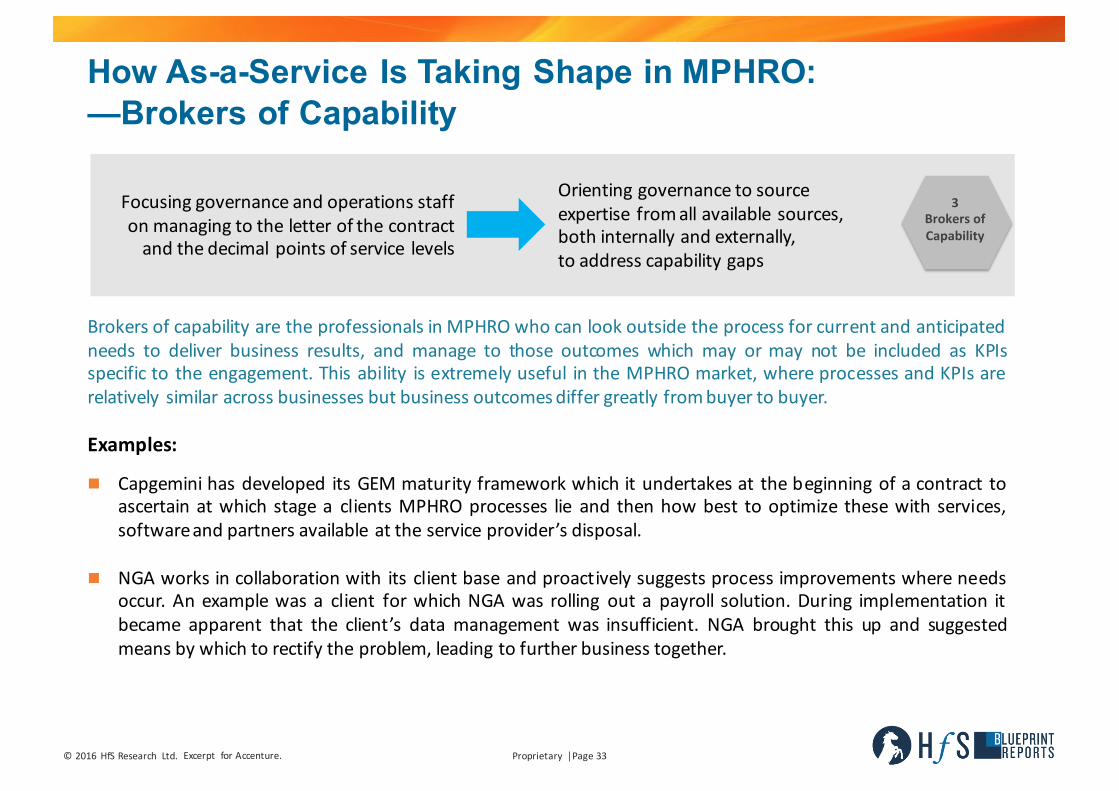

3"Brokers"of"Capability"

How As-a-Service Is Taking Shape in MPHRO: —Brokers of Capability

Focusinggovernanceandoperationsstaffonmanagingtotheletterofthecontractandthedecimalpointsofservice levels

Orientinggovernancetosourceexpertise fromallavailable sources,bothinternallyandexternally,toaddresscapabilitygaps

Brokers of capability are the professionals in MPHRO who can look outside the process for current and anticipatedneeds to deliver business results, and manage to those outcomes which may or may not be included as KPIsspecific to the engagement. This ability is extremely useful in the MPHRO market, where processes and KPIs arerelatively similar across businesses but business outcomesdiffer greatly frombuyer to buyer.

Examples:

n Capgemini has developed its GEM maturity framework which it undertakes at the beginning of a contract toascertain at which stage a clients MPHRO processes lie and then how best to optimize these with services,softwareand partners available at the service provider’s disposal.

n NGA works in collaboration with its client base and proactively suggests process improvements where needsoccur. An example was a client for which NGA was rolling out a payroll solution. During implementation itbecame apparent that the client’s data management was insufficient. NGA brought this up and suggestedmeans by which to rectify the problem, leading to further business together.

Proprietary │Page34©2016 HfSResearch Ltd. Excerpt forAccenture.

4"Collabora)ve"Engagement"

How As-a-Service Is Taking Shape in MPHRO: —Collaborative Engagement

The key to a sustainable MPHRO engagement is collaboration, working together to produce a result. TraditionallyMPHRO work has been directive from service buyers to service providers, and managed strictly by procurementorganizations. As more HR business units and global shared services centers take responsibility for relationships,HfS is seeing amove over time to more of a collaborative naturewhere there is trust and experience in place, oftenthrough shared outcomes and results.

Examples:n OneSource Virtual has been praised by clients for proactively seeking out feedback and then incorporating this

into ongoing service delivery improvements.

n Neeyamo’s clients see them as part of their internal teams through Neeyamo’s constant engagement withclients and the feeding back of this into service delivery.

n Clients have praised Xerox’s flexibility and ability to truly partner with them in order to understand clientbusiness outcomesand how best to influence these from an HR perspective.

Evaluatingrelationshipsonbaselinesofcost,

effort,andlabor

Ensuringrelationshipsarecontractedtodrivesustainedexpertiseandoutcomes

Proprietary │Page35©2016 HfSResearch Ltd. Excerpt forAccenture.

5"Intelligent"Automa/on"

How As-a-Service Is Taking Shape in MPHRO: —Intelligent Automation

Operatingfragmentedprocessesacrossmultipletechnologieswithsignificantmanualinterventions

Usingofautomationandcognitivecomputingtoblendanalytics,talent,andtechnology

Automation—software used to do rules-defined tasks—is prevalent in HR email processing, and data capture andtransfer as well as for workflow management in operations. What HfS terms “Intelligent Automation,” extendingautomation across processes and bringing in natural language processing and machine learning, has started to beimplemented in employee query resolution.

Examples:n Accenture proactively uses automation within MPHRO processes addressing compliance, email and workflow.

n Infosys is using RPA for audits and compliance, data capture and transfer, query resolution and email responseand auctioning.

n Neeyamo is set to launch an automated compliance tracking offering in July 2016 that will include dynamiccompliance alerts for payroll.

n OneSource Virtual rolled out an automated email function for a client in the U.S. which reduced the processfrom20 hours down to eight minutes and reduced FTE count on the process fromeight to one.

Proprietary │Page36©2016 HfSResearch Ltd. Excerpt forAccenture.

6"Accessible"&"Ac+onable"

Data"

How As-a-Service Is Taking Shape in MPHRO: —Accessible & Actionable Data

PerformingAd-hocanalysisonunstructureddatawithlittleintegrationorbusinesscontext

Applyinganalyticsmodels,techniquesandinsightsfrombigdata,real-time

Service providers are cultivating skillsets of Data Scientists, and subject matter experts to help develop models,dashboards, and tools to help drive increasingly real-time access and analysis, addressing all aspects of the valuechain from RPO and reducing onboarding churn, identifying payroll mistakes to identifying underperformingemployees and in some cases howbest to rectify the issue.

Examples:n OneSource Virtual is currently bringing to market an analytics offering that will track and benchmark data from

a client’s operation against industry best practices. Predictive analytics will be used to forecast, such asturnover, for the next year. Predictive analytics will take this one step further in the package and offer remedieson an individual employee basis.

n Neeyamo has embedded predictive analytics within its automated employee helpdesk portal.

n Aon Hewitt is using analytics in the design of its clients front end HCM platforms. One example is how it isbeing used to identify dropout rate from pages and enable root cause of channel churn. This can then be fedback into the design on the platform to make it more user friendly and drive employees to the channel of leastfriction.

Proprietary │Page37©2016 HfSResearch Ltd. Excerpt forAccenture.

7"Holis(c"Security"

How As-a-Service Is Taking Shape in MPHRO:—Holistic Security

Respondingreactivelywithpost-eventfixes.

Little focusonend-to-endprocessvaluechains.

Proactivelymanagingdigitaldataacrossservicechainofpeople,systems&processes

The risk of leaked employee data is one of the major inhibitors to adoption of MPHRO services. HfS takes theposition that security is not just about having security software or technology, but practices and culture forcreating digital trust all along the value chain and internal and external in networks. People will becomeincreasingly interested in sharing data when they realize the benefits of doing so, but will only do so withcompanies and systems they trust. The adoption of cloud HCM platforms that require a greater degree ofemployee data has been inhibited to an extent by security concerns.

Example:n Xerox has a stand alone “Xerox Security Office” where agents and other MPHRO operational staff are trained.

The service provider also undertakes a full data security analysis for each client prior to an MPHROengagement.

n The ADP Marketplace allows HR professionals to select from pre-approved and vetted service providers andsoftwareproviders to ensure secure APIs.

Proprietary │Page38©2016 HfSResearch Ltd. Excerpt forAccenture.

8"Plug"&"Play"Digital"Services"

How As-a-Service Is Taking Shape in MPHRO:—Plug & Play Business Services

Undertakingcomplexandoftenpainfultechnologytransitions

toreachasteadystate

Plugginginto“readytogo”businessoutcomefocused,people/process/technologywithsecuritymeasures

The MHRO market was previously characterized by elaborate bespoke platforms and services. This reducedinnovation potential and also increased costs, a plug and play option that includes platform with business processservices puts the onus of capital expenditure and talent management on the service provider, although it alsoassumes the service provider can use the solution for more than one client to get scale and return on investment.

Example:n NGA HR has stopped doing bespoke integrations of its ResourceLink HCM platform in the U.K and has instead

designed a best “fit for purpose” design that it can integrate into clients operations on a “Plug & Play” basis.This reduces implementation time and simplifies the update process thereby improving compliance.

n Aon Hewitt has UPoint which integrates client’s HR systems (proprietary TBA system, Workday, PeopleSoft,Employee Central, SAP, Cornerstone, Taleo, web chat, casemanagement), organizational HR policy content, andHR business program announcements into one commoncustomer experience framework.

n Accenture’s integrated HR service and technology delivery is delivered on a plug and play basis and is aimed ataddressing the business outcomesof clients.

n Xerox has predefined stack of HR services that can be rapidly deployed into a client organizations on a plug andplay basis.

Research Methodology

Proprietary │Page40©2016 HfSResearch Ltd. Excerpt forAccenture.

Research Methodology

DataSummaryn DatawascollectedinQ12016,frombuyersand

serviceprovidersofMPHROservices

ParticipatingServiceProviders

THISREPORTISBASEDON:

n TalesfromtheTrenches:Interviewswithbuyerswhohaveevaluatedserviceprovidersandexperienced theirservices.Somecontactswereprovidedbyserviceproviders,andotherswereinterviewsconductedwithHfS ExecutiveCouncilmembersandparticipantsinourextensivemarketresearch.

n Sell-SideExecutiveBriefings:Structureddiscussionswithserviceprovidersregardingtheirvision,strategy,capability,andexamplesofinnovationandexecution.

n PubliclyAvailableInformation:Thoughtleadership,investoranalystmaterials,websiteinformation,presentationsgivenbyseniorexecutives,industryevents,etc.

Proprietary │Page41©2016 HfSResearch Excerpt forAccenture.

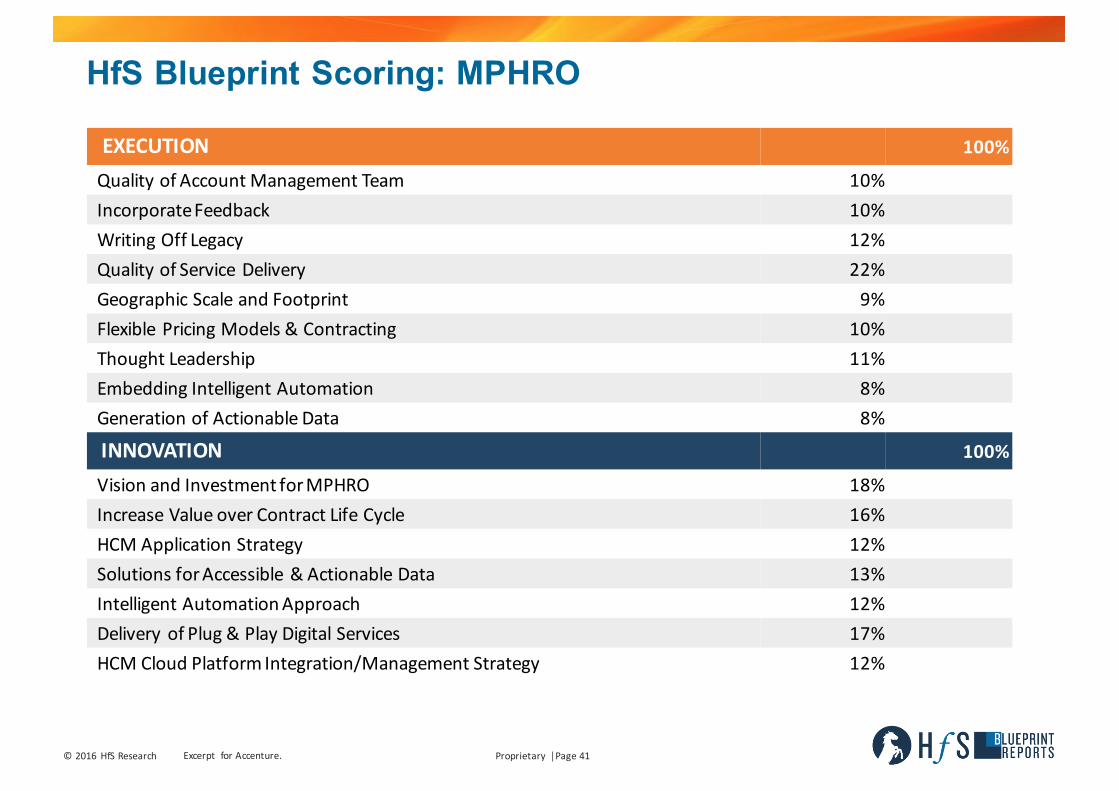

HfS Blueprint Scoring: MPHRO

EXECUTION 100%

QualityofAccountManagement Team 10%IncorporateFeedback 10%WritingOffLegacy 12%Quality ofServiceDelivery 22%GeographicScaleandFootprint 9%FlexiblePricingModels&Contracting 10%ThoughtLeadership 11%EmbeddingIntelligentAutomation 8%GenerationofActionableData 8%

INNOVATION 100%

Visionand InvestmentforMPHRO 18%IncreaseValueoverContractLifeCycle 16%HCMApplicationStrategy 12%Solutions forAccessible&ActionableData 13%IntelligentAutomationApproach 12%DeliveryofPlug &PlayDigitalServices 17%HCMCloudPlatformIntegration/ManagementStrategy 12%

Proprietary │Page42©2016 HfSResearch Excerpt forAccenture.

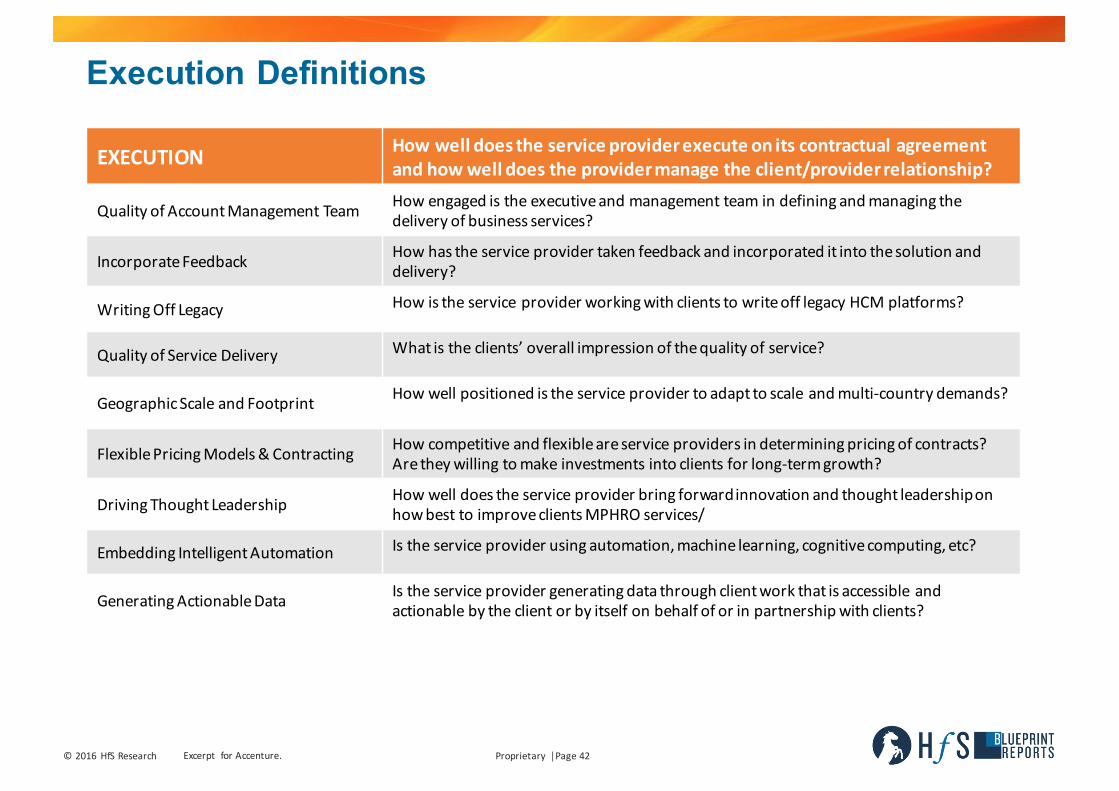

Execution Definitions

EXECUTION Howwelldoestheserviceproviderexecuteonitscontractualagreementandhowwelldoestheprovidermanagetheclient/providerrelationship?

QualityofAccountManagement Team Howengagedis theexecutiveandmanagementteamindefiningandmanagingthedeliveryofbusinessservices?

IncorporateFeedback Howhas theserviceprovidertakenfeedbackandincorporateditintothesolutionanddelivery?

WritingOffLegacy HowistheserviceproviderworkingwithclientstowriteofflegacyHCMplatforms?

Quality ofServiceDelivery Whatisthe clients’overallimpressionofthequalityofservice?

GeographicScaleandFootprint Howwell positionedistheserviceprovidertoadapttoscaleandmulti-countrydemands?

FlexiblePricingModels&Contracting How competitiveandflexibleareserviceprovidersindeterminingpricingofcontracts?Aretheywillingtomakeinvestmentsintoclientsforlong-termgrowth?

DrivingThoughtLeadership How welldoestheserviceproviderbringforwardinnovationandthoughtleadershiponhowbesttoimproveclientsMPHROservices/

EmbeddingIntelligentAutomation Is theserviceproviderusingautomation,machinelearning,cognitivecomputing,etc?

GeneratingActionableData Istheserviceprovidergeneratingdatathrough clientworkthatisaccessibleandactionablebytheclientorbyitselfonbehalfoforinpartnershipwithclients?

Proprietary │Page43©2016 HfSResearch Excerpt forAccenture.

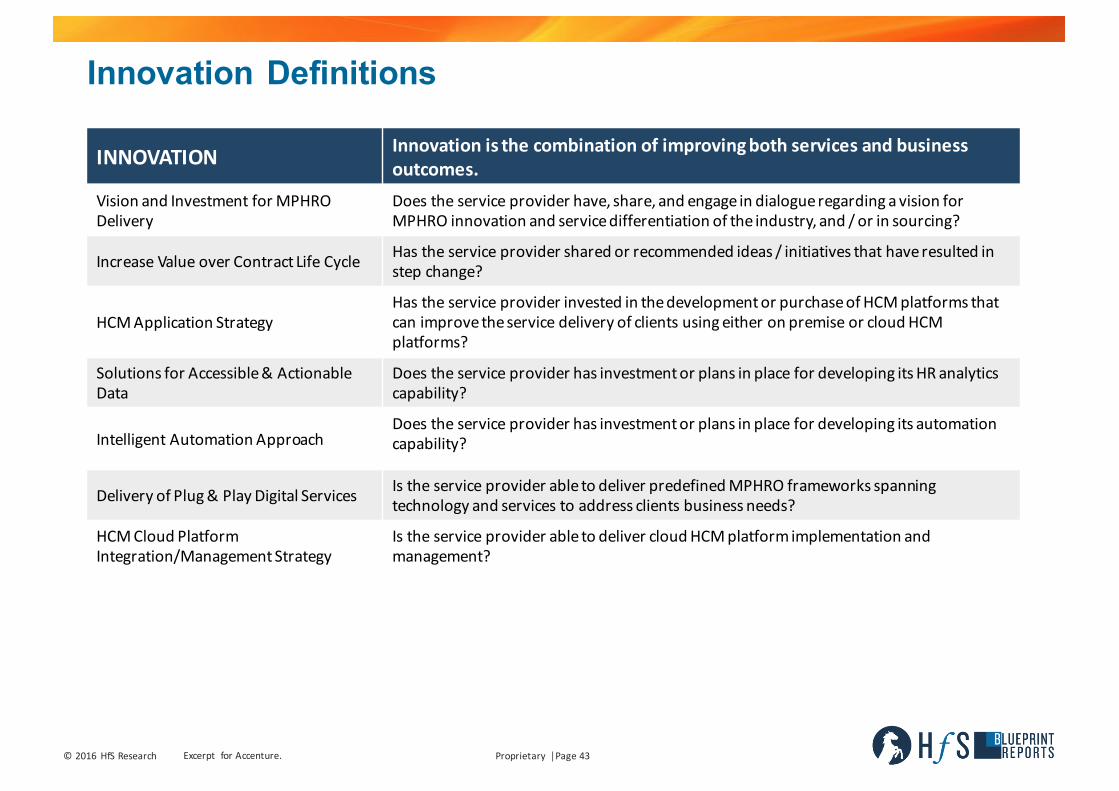

Innovation Definitions

INNOVATION Innovationisthecombinationofimprovingbothservicesandbusinessoutcomes.

VisionandInvestmentforMPHRODelivery

Doestheservice providerhave,share,andengageindialogueregardingavisionforMPHROinnovationandservicedifferentiationoftheindustry,and/orinsourcing?

IncreaseValueoverContractLifeCycle Hastheservice providersharedorrecommendedideas/initiativesthathaveresultedinstepchange?

HCMApplicationStrategyHastheserviceproviderinvested inthedevelopmentorpurchaseofHCMplatformsthatcanimprovetheservicedeliveryofclientsusingeitheronpremiseorcloudHCMplatforms?

SolutionsforAccessible&ActionableData

Doestheservice providerhasinvestmentorplansinplacefordevelopingitsHRanalyticscapability?

IntelligentAutomationApproachDoestheserviceproviderhasinvestmentorplansinplacefordevelopingitsautomationcapability?

DeliveryofPlug&PlayDigitalServices Istheservice providerabletodeliverpredefinedMPHROframeworksspanningtechnologyandservicestoaddressclientsbusinessneeds?

HCMCloudPlatformIntegration/ManagementStrategy

IstheserviceproviderabletodelivercloudHCMplatformimplementationandmanagement?

Service Provider Analysis

Proprietary │Page45©2016 HfSResearch Excerpt forAccenture.

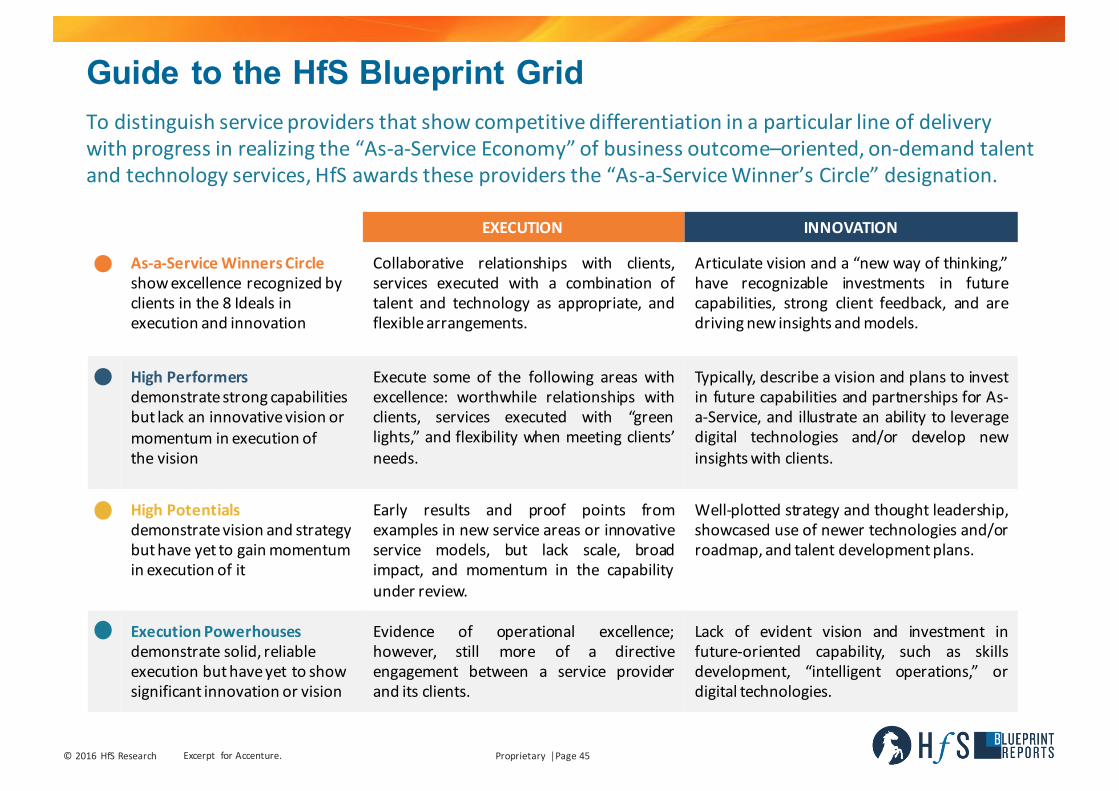

Todistinguishserviceprovidersthatshowcompetitivedifferentiationinaparticularlineofdeliverywithprogressinrealizingthe“As-a-ServiceEconomy”ofbusinessoutcome–oriented,on-demandtalentandtechnologyservices,HfSawardstheseprovidersthe“As-a-ServiceWinner’sCircle”designation.

Guide to the HfS Blueprint Grid

EXECUTION INNOVATION

As-a-ServiceWinnersCircleshowexcellencerecognizedbyclientsinthe8Idealsinexecutionandinnovation

Collaborative relationships with clients,services executed with a combination oftalent and technology as appropriate, andflexiblearrangements.

Articulate vision and a “new way of thinking,”have recognizable investments in futurecapabilities, strong client feedback, and aredrivingnew insights andmodels.

HighPerformersdemonstratestrongcapabilitiesbutlackaninnovativevisionormomentuminexecutionofthevision

Execute some of the following areas withexcellence: worthwhile relationships withclients, services executed with “greenlights,” and flexibility when meeting clients’needs.

Typically, describe a vision and plans to investin future capabilities and partnerships for As-a-Service, and illustrate an ability to leveragedigital technologies and/or develop newinsightswith clients.

High Potentialsdemonstratevisionandstrategybuthaveyettogainmomentuminexecutionofit

Early results and proof points fromexamples in new service areas or innovativeservice models, but lack scale, broadimpact, and momentum in the capabilityunder review.

Well-plotted strategy and thought leadership,showcased use of newer technologies and/orroadmap, and talent developmentplans.

ExecutionPowerhousesdemonstratesolid,reliableexecutionbuthaveyettoshowsignificantinnovationorvision

Evidence of operational excellence;however, still more of a directiveengagement between a service providerand its clients.

Lack of evident vision and investment infuture-oriented capability, such as skillsdevelopment, “intelligent operations,” ordigital technologies.

Proprietary │Page46©2016 HfSResearch Excerpt forAccenture.

INNOVA

TION

EXECUTION

ExcellentatInnovationandExecutionInvestinginInnovationtoChange

BuildingAllCapabilities ExecutionIsAheadofInnovation

AS-A-SERVICEWINNER’SCIRCLE

EXECUTIONPOWERHOUSES

HIGHPOTENTIALS

HIGHPERFORMERS

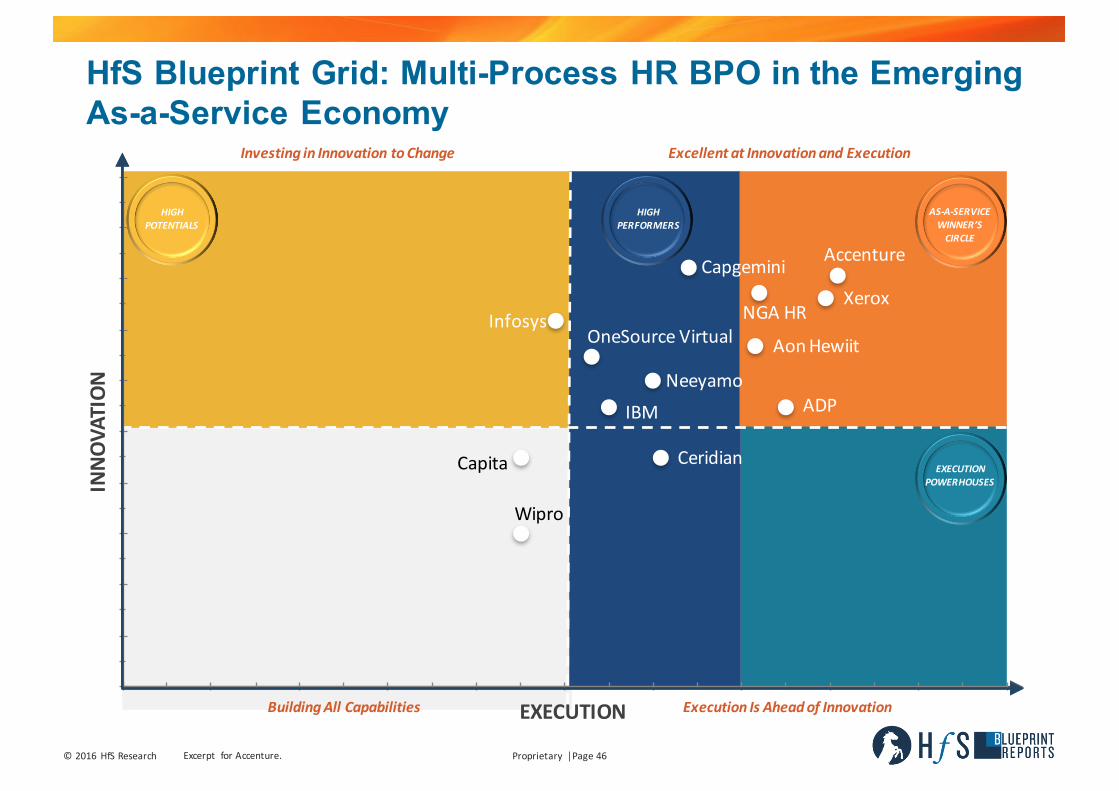

Accenture

ADP

AonHewiit

Capgemini

Capita Ceridian

IBM

Infosys

Neeyamo

NGAHROneSourceVirtual

Wipro

Xerox

HfS Blueprint Grid: Multi-Process HR BPO in the Emerging As-a-Service Economy

Proprietary │Page47©2016 HfSResearch Ltd. Excerpt forAccenture.

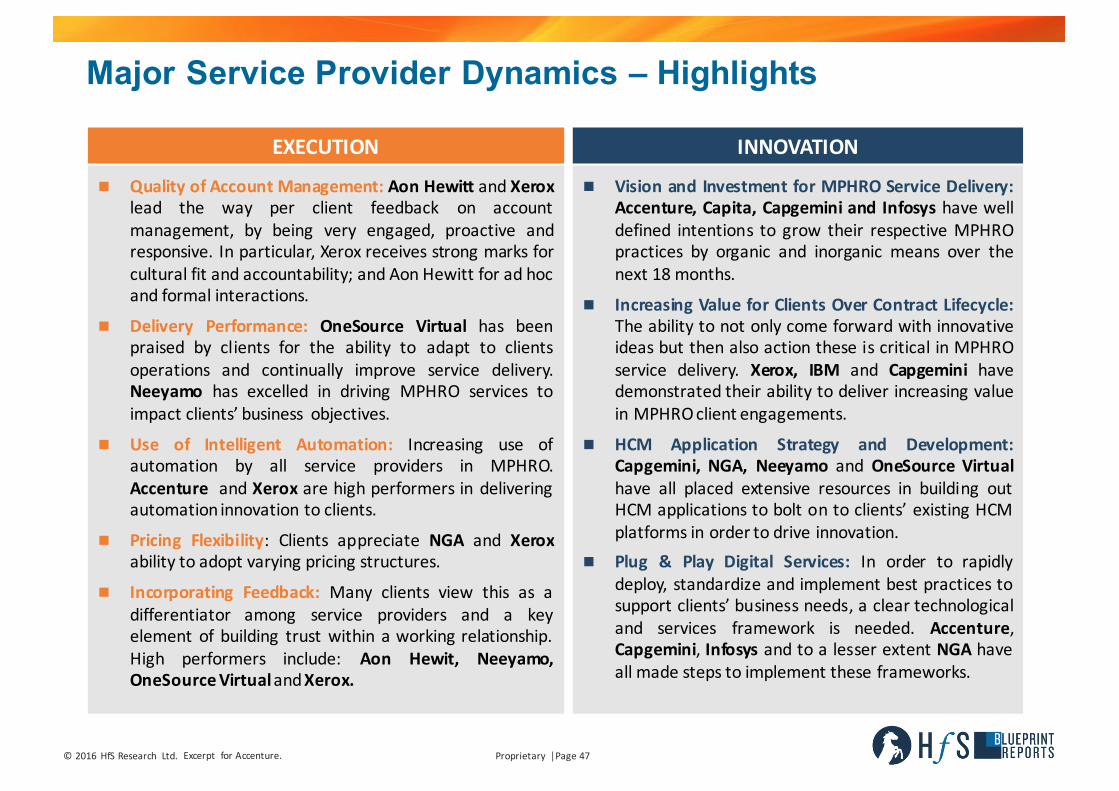

Major Service Provider Dynamics – Highlights

EXECUTION

n Quality of Account Management: Aon Hewitt and Xeroxlead the way per client feedback on accountmanagement, by being very engaged, proactive andresponsive. In particular, Xerox receives strong marks forcultural fit and accountability; and Aon Hewitt for ad hocand formal interactions.

n Delivery Performance: OneSource Virtual has beenpraised by clients for the ability to adapt to clientsoperations and continually improve service delivery.Neeyamo has excelled in driving MPHRO services toimpact clients’ business objectives.

n Use of Intelligent Automation: Increasing use ofautomation by all service providers in MPHRO.Accenture and Xerox are high performers in deliveringautomation innovation to clients.

n Pricing Flexibility: Clients appreciate NGA and Xeroxability to adopt varying pricing structures.

n Incorporating Feedback: Many clients view this as adifferentiator among service providers and a keyelement of building trust within a working relationship.High performers include: Aon Hewit, Neeyamo,OneSourceVirtualandXerox.

INNOVATION

n Vision and Investment for MPHRO Service Delivery:Accenture, Capita, Capgemini and Infosys have welldefined intentions to grow their respective MPHROpractices by organic and inorganic means over thenext 18 months.

n Increasing Value for Clients Over Contract Lifecycle:The ability to not only come forward with innovativeideas but then also action these is critical in MPHROservice delivery. Xerox, IBM and Capgemini havedemonstrated their ability to deliver increasing valuein MPHROclient engagements.

n HCM Application Strategy and Development:Capgemini, NGA, Neeyamo and OneSource Virtualhave all placed extensive resources in building outHCM applications to bolt on to clients’ existing HCMplatforms in order to drive innovation.

n Plug & Play Digital Services: In order to rapidlydeploy, standardize and implement best practices tosupport clients’ business needs, a clear technologicaland services framework is needed. Accenture,Capgemini, Infosys and to a lesser extent NGA haveall made steps to implement these frameworks.

Proprietary │Page48©2016 HfSResearch Ltd. Excerpt forAccenture.

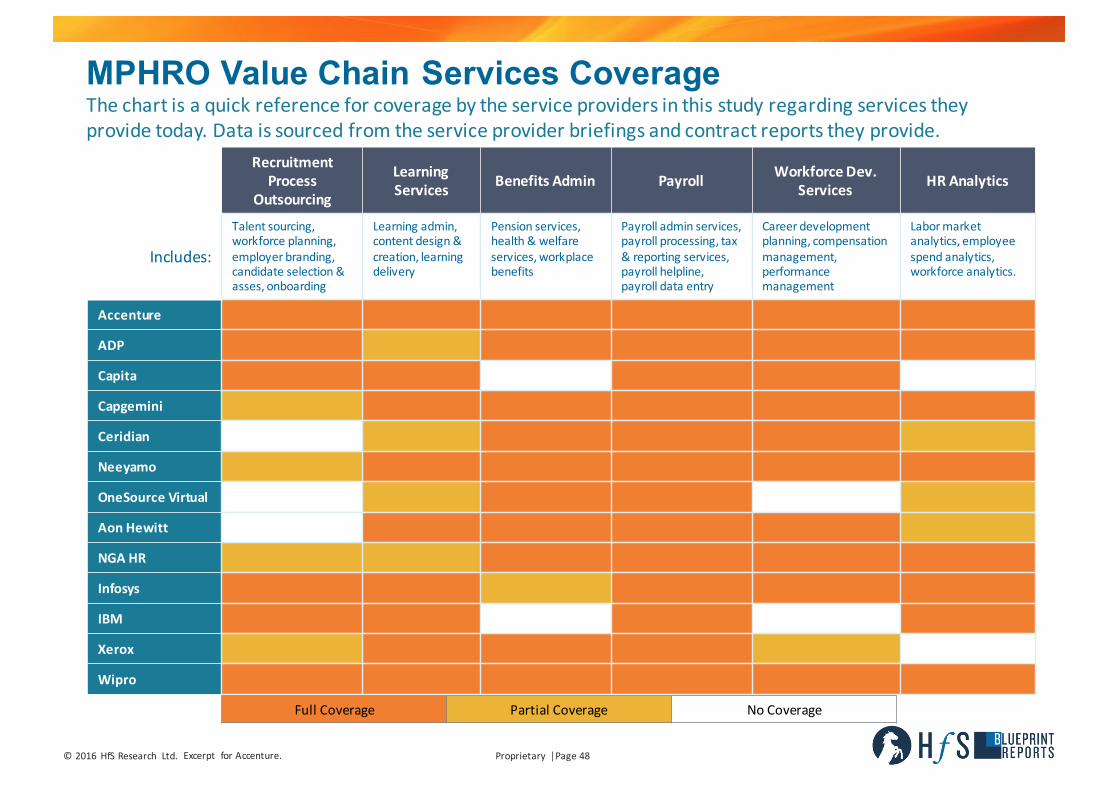

MPHRO Value Chain Services CoverageThechartisaquickreferenceforcoveragebytheserviceprovidersinthisstudyregardingservicestheyprovidetoday.Dataissourcedfromtheserviceproviderbriefingsandcontractreportstheyprovide.

RecruitmentProcess

Outsourcing

LearningServices BenefitsAdmin Payroll WorkforceDev.

Services HRAnalytics

Includes:

Talentsourcing,workforceplanning,employerbranding,candidateselection&asses, onboarding

Learning admin,contentdesign&creation,learningdelivery

Pensionservices,health& welfareservices,workplacebenefits

Payrolladminservices,payrollprocessing,tax& reportingservices,payrollhelpline,payrolldataentry

Careerdevelopmentplanning,compensationmanagement,performancemanagement

Labormarketanalytics,employeespend analytics,workforceanalytics.

Accenture

ADP

Capita

Capgemini

Ceridian

Neeyamo

OneSourceVirtual

AonHewitt

NGAHR

Infosys

IBM

Xerox

Wipro

FullCoverage Partial Coverage NoCoverage

Proprietary │Page49©2016 HfSResearch Ltd. Excerpt forAccenture.

Accenture

RelevantAcquisitions/Partnerships ClientProfile ServiceDeliveryOperations ProprietaryTechnologies

Acquisitions:• FusionX (2015) toenhancecybersecurity• Cloud Sherpas (2015)toenhancecloud consulting

capability• i4CAnalytics(2014)toenhanceanalytics

capability• SoliumPartnerships:• Technology:ServiceNow,Workday,

Successfactors, Oracle• Service:MajorGlobalPayrollProvider

~80MPHROclientsIncluding:• Unilever• AlcatelLucent• BankofIreland

• TOTALMPHRO Headcount:~5,500

• MPHROdeliveryin20centers

• Deliverycenterlocations: NorthAmerica,Brazil,Argentina,WesternEurope,China,SriLanka,Japan,thePhilippines,andSingapore,India,Czech Republic, RomaniaandSouthAfrica

• WorkdayCOEinBucharest

• MPHROGeographicSupport:NorthAmerica,LATAM,EMEAandAsiaPacific

• OneLearningPlan(1LP)• HRChattoolHRApps:• CandidateInterviewApp• IntelligentRecruiterApp• TalentDemandForecasterApp• TalentPerformanceProfilerApp• RecruitmentFunnelAnalyzerApp• TalentSupplyAnalyzerApp• AttritionPredictorApp

Forwardthinkingandinnovativeserviceproviderwithaglobalreach

Winners Circle

Strengths Challenges

• Extensive Use of Intell igent Automation Within MPHRO Service Delivery : Accent ure hasimplemented extensive use of a utomation in its MPHRO contract s from compliance thr oug h toemail re sponse and a ctioning. Clients have praised the pr oactive nature of Accenture’sautomation implementation within MPHRO functions

• Service Delivery Based on Business Out comes: A ccenture is aiming t o sell MPHRO deal s thr oughaddressing end business goals.

• Integrated Service and Technology Delive ry: Accentur e has an ecosystem of part ner andproprietary HR technol ogies that it implements into client organizations and are included inAccenture’s outcomes and transactional based pricing.

• Global MPHRO Support Acr oss Value Chain: Accent ure has reached a “critical mass” whereby itcan deliver on multi-country and multi -lang uage MPHRO contracts. The service pr ovider haspartnered with a major global payr oll service pr ovider in its delivery of long-tail country payrollcontracts.

• Key Focus on Em ployee Engag ement: A ccenture has developed its MPHRO service s aroundempl oyee engagement and sati sfa ction. As t his is one of t he leading drivers t o MPHRO adoptionit will help foster growth for Accenture within the MPHRO market.

• Platform Agnosti c: A ccenture has partnered with both S uccessFa ctors and Work day to deliverimplementations, even going so far as launching a Workday CoE in Bucharest.

• Fast Paced Career Culture within A ccent ure: Thefast paced career traje ctory of its sta ff means thevital member s of a delivery team are oftenmoved off of a ccounts a fter a relatively shorttime. Accent ure needs to manage clientexpectations and transitions to make this asmooth experience for both employees anclients.

• Prici ng Flexibility: Clients have stated thatAccenture i s average when it comes tonegotiating the pricing terms of a contract.

• Cross Cli ent Eng agement : Accenture has not yetsuccessfully launched speci fi c cr oss client HROfor ums or summits. These forums create thebreedi ng ground for best pra ctice sharingbetween clients and can also be useful to theservice pr ovider i n devel opment of servicedelivery through holistic client feedback.

Blueprint Leading Highlights

• Use of Intelligent Automation• Application of Plug&PlayDigital

Business Services• Collaborative Engagement• WritingOff Legacy• Focus onBusiness Outcomes

Recruitment(RPO)

LearningServices

BenefitsAdmin

Payroll

Workforce DevServ.

Analytics

Proprietary │Page50©2016 HfSResearch Ltd. Excerpt forAccenture.

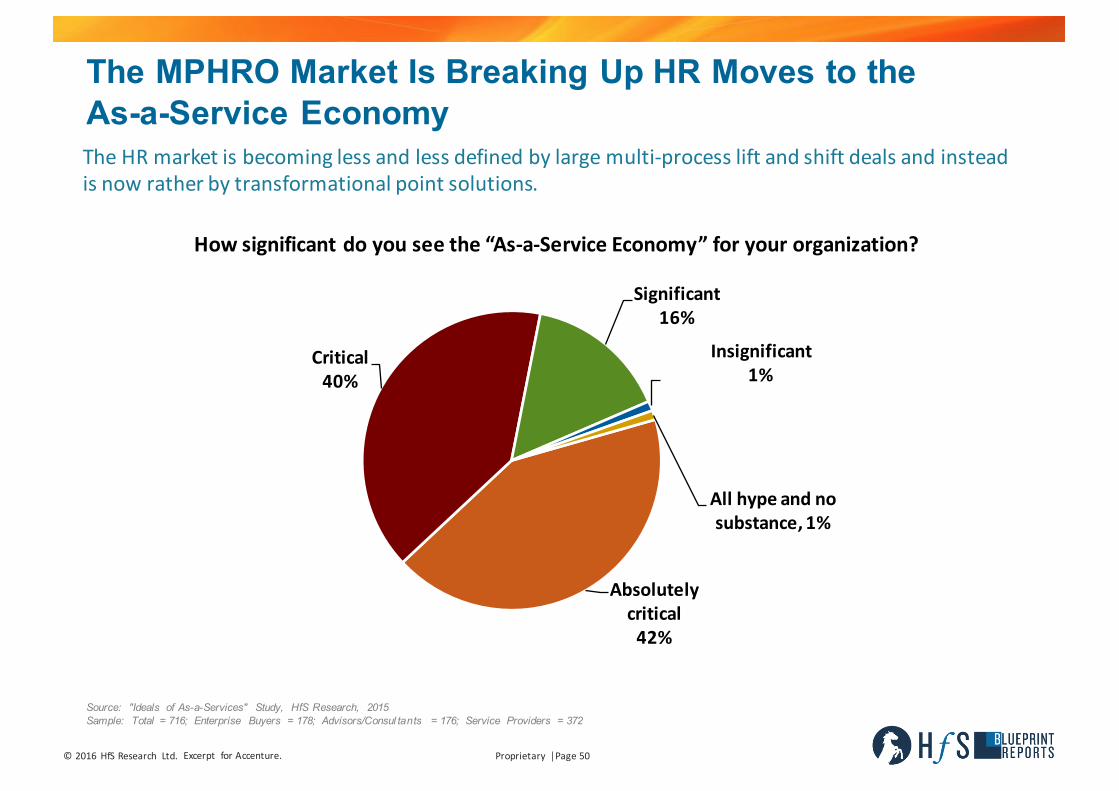

The MPHRO Market Is Breaking Up HR Moves to the As-a-Service Economy

Howsignificantdoyouseethe“As-a-ServiceEconomy”foryourorganization?

Source: "Ideals of As-a-Services" Study, HfS Research, 2015Sample: Total = 716; Enterprise Buyers = 178; Advisors/Consul tants = 176; Service Providers = 372

Absolutelycritical42%

Critical40%

Significant16%

Insignificant1%

Allhypeandnosubstance,1%

TheHRmarketisbecominglessandlessdefinedbylargemulti-processliftandshiftdealsandinsteadisnowratherbytransformationalpointsolutions.

Proprietary │Page51©2016 HfSResearch Ltd. Excerpt forAccenture.

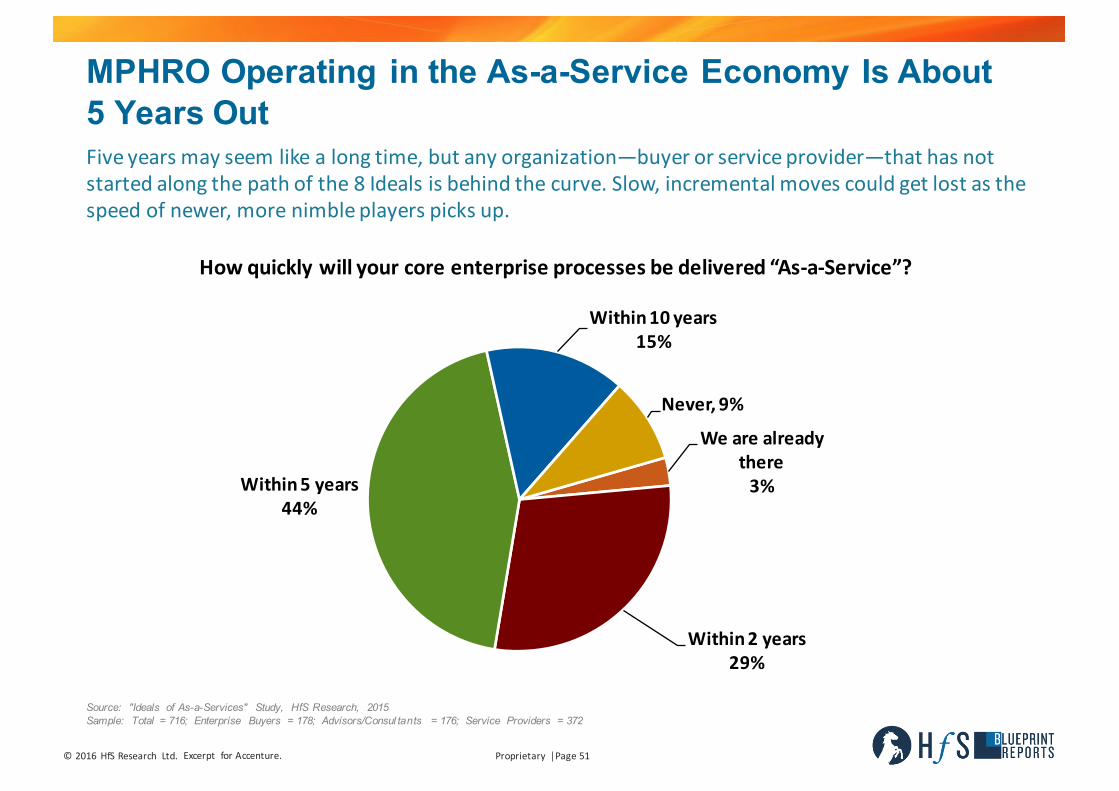

MPHRO Operating in the As-a-Service Economy Is About 5 Years Out

Howquicklywillyourcoreenterpriseprocessesbedelivered“As-a-Service”?

Fiveyearsmayseemlikealongtime,butanyorganization—buyerorserviceprovider—thathasnotstartedalongthepathofthe8Idealsisbehindthecurve.Slow,incrementalmovescouldgetlostasthespeedofnewer,morenimbleplayerspicksup.

Source: "Ideals of As-a-Services" Study, HfS Research, 2015Sample: Total = 716; Enterprise Buyers = 178; Advisors/Consul tants = 176; Service Providers = 372

Wearealreadythere3%

Within2years29%

Within5years44%

Within10years15%

Never,9%

Proprietary │Page52©2016 HfSResearch Ltd. Excerpt forAccenture.

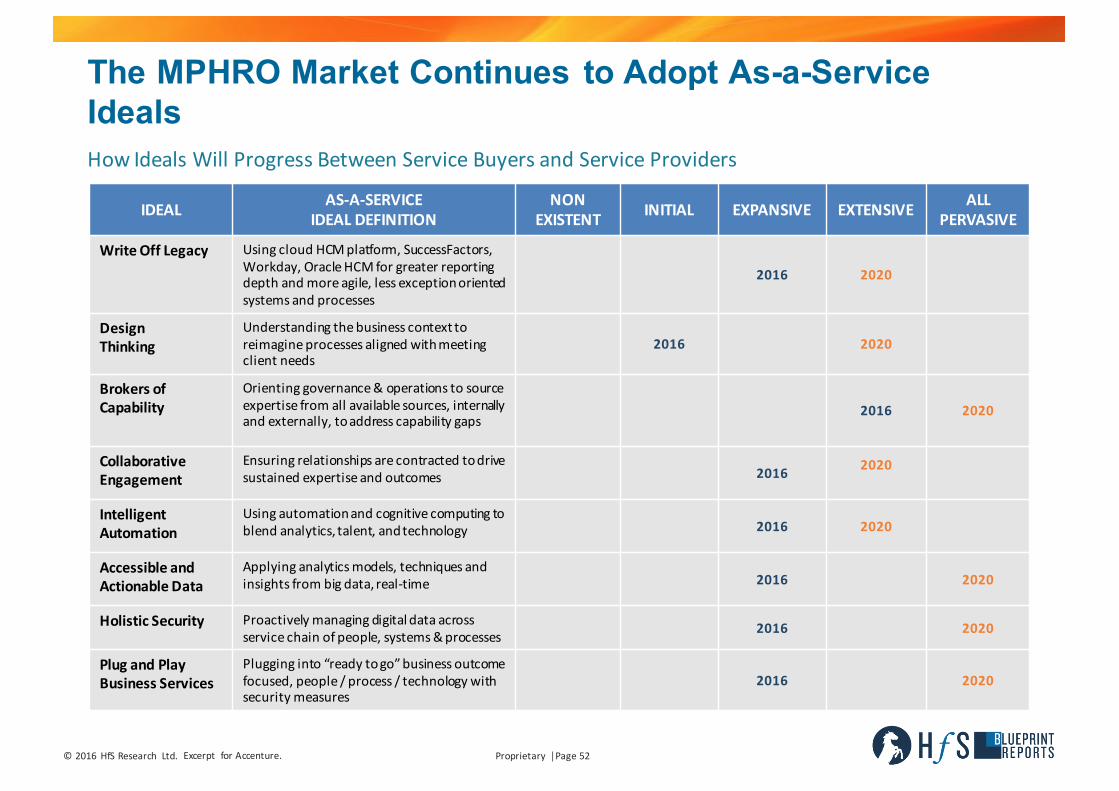

The MPHRO Market Continues to Adopt As-a-Service Ideals

IDEAL AS-A-SERVICEIDEALDEFINITION

NONEXISTENT INITIAL EXPANSIVE EXTENSIVE ALL

PERVASIVE

WriteOffLegacy UsingcloudHCMplatform,SuccessFactors,Workday,OracleHCMforgreaterreportingdepthandmoreagile,lessexceptionorientedsystemsandprocesses

2016 2020

DesignThinking

Understandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds

2016 2020

Brokers ofCapability

Orientinggovernance&operationstosourceexpertisefromallavailablesources,internallyandexternally,toaddresscapabilitygaps

2016 2020

CollaborativeEngagement

Ensuringrelationshipsarecontractedtodrivesustainedexpertiseandoutcomes 2016 2020

IntelligentAutomation

Usingautomationandcognitivecomputingtoblendanalytics,talent,andtechnology 2016 2020

Accessible andActionableData

Applyinganalyticsmodels,techniquesandinsightsfrombigdata,real-time 2016 2020

Holistic Security Proactivelymanagingdigitaldataacrossservicechainofpeople,systems&processes 2016 2020

PlugandPlayBusinessServices

Plugginginto“readytogo”businessoutcomefocused,people/process/technologywithsecuritymeasures

2016 2020

HowIdealsWillProgressBetweenServiceBuyersandServiceProviders

©2016 HfSResearch Ltd. Excerpt forAccenture.

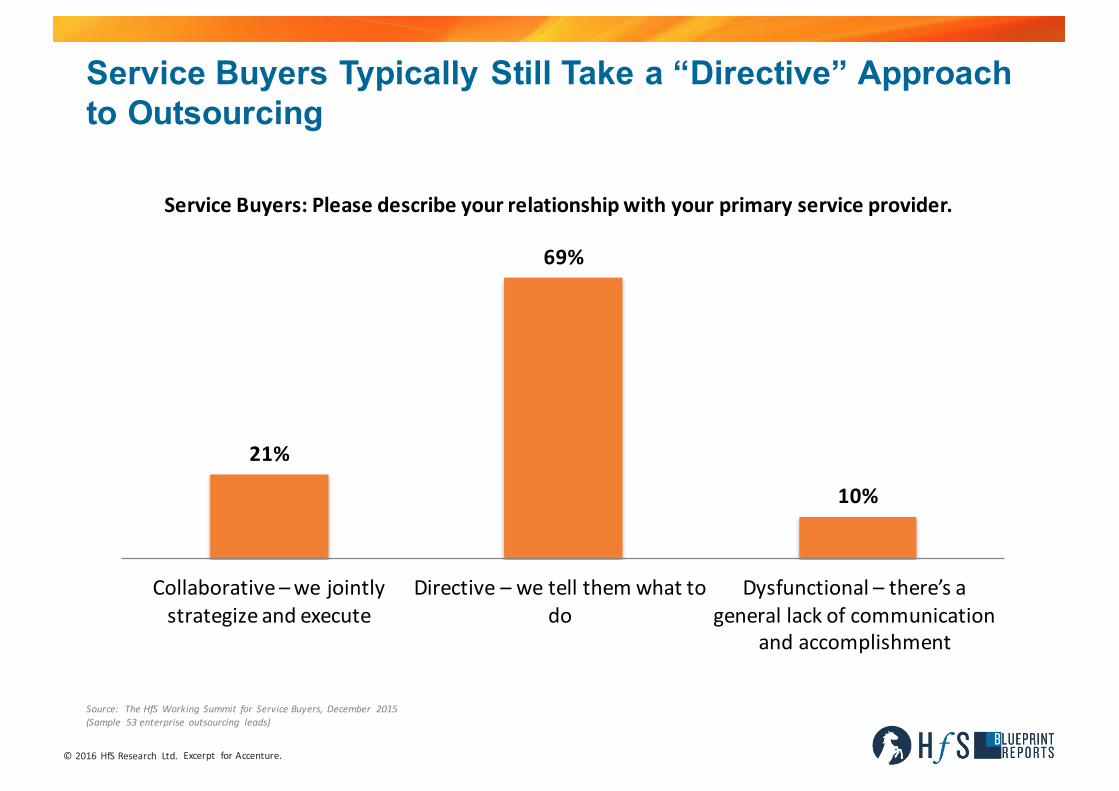

Service Buyers Typically Still Take a “Directive” Approach to Outsourcing

21%

69%

10%

Collaborative–wejointlystrategizeandexecute

Directive– wetellthemwhattodo

Dysfunctional– there’sagenerallackofcommunication

andaccomplishment

ServiceBuyers:Pleasedescribeyourrelationshipwithyourprimaryserviceprovider.

Source: TheHfSWorking Summit for ServiceBuyers, December 2015(Sample 53enterprise outsourcing leads)

©2016 HfSResearch Ltd. Excerpt forAccenture.

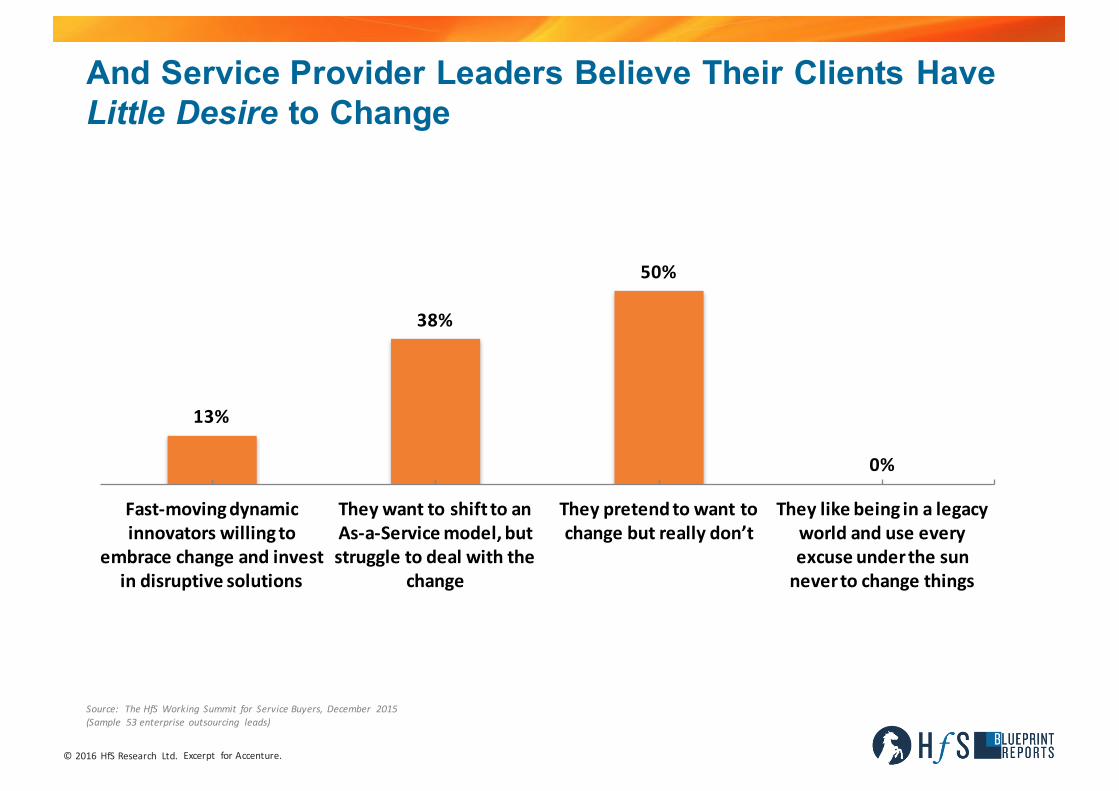

And Service Provider Leaders Believe Their Clients Have Little Desire to Change

13%

38%

50%

0%

Fast-movingdynamicinnovatorswillingto

embracechangeandinvestindisruptivesolutions

TheywanttoshifttoanAs-a-Servicemodel,butstruggletodealwiththe

change

Theypretendtowanttochangebutreallydon’t

Theylikebeinginalegacyworldanduseeveryexcuseunderthesunnevertochangethings

Source: TheHfSWorking Summit for ServiceBuyers, December 2015(Sample 53enterprise outsourcing leads)

Proprietary │Page55©2016 HfSResearch Ltd. Excerpt forAccenture.

Increasing the Value of Engagement Through BPO and the Emerging As-a-Service Economy

n Collaborate Across the Industry: Service buyers together with service providers have anopportunity to take a more prominent role in facilitating collaboration within the MPHRO market.With the dynamics of the market changing as employee engagement, and a focus on widerbusiness outcomes becomes increasingly important. Service providers have to be leading from thefront in thought and industry leadership, while buyers need to be engaging in these forums andwilling to embrace partnership with service providers.

n Continue to Facilitate the Writing Off of Legacy Through Outsourcing: The move to cloud HCMplatforms in the MPHRO market is becoming increasingly common, although it is not yet allpervasive. Larger organizations in particular are still too often entrenched in legacy and thereforerequire comprehensive change management partners, and senior level sponsorship, to make themove to these cloud HCM platforms and embrace the requisite changes that come along with theeasier workflow and access to data.

Even organizations that have moved to the cloud are often at a loss of how best to use thetechnology available to them to impact business outcomes. Outsourcing platform managementand managed service delivery to platform specific experts (service providers) allows for theoptimization and best use of these systems. Service providers are increasingly developing appsthat integratewith SuccessFactors andWorkday to bring further value to clients.

Proprietary │Page56©2016 HfSResearch Ltd. Excerpt forAccenture.

Increasing the Value of Engagement Through BPO and the Emerging As-a-Service Economy, Cont.

n Embrace the Efficiency Gains of Intelligent Automation: Process automation in the areas of datacapture and transfer, auditing and compliance, query resolution, employee service, informationupdates, escalation, email response and actioning and rules based processing are now becomingmore commonplace in the MPHRO market. These process automations enhance productivity,significantly add value and reduce manual back-office functions. However we have yet to see truecognitive automation inMPHRO case studies.

n Utilize Economies of Scale Via Plug & Play Processes: Infosys, Capgemini, Xerox and NGA HR haverolled out standardized MPHRO managed services and platform implementations that not onlyallow for quicker, and often more efficient processes than bespoke alternatives, but also allow foran element of cost reduction through the use of cross client economies of scale in deliverycenters. Most often the largest component of customization in these implementations is the “lookand feel” of the service and front end user dashboard. In order for service providers to excel inthis market they need to have pre-built process and software implementation maps that addressthe business needs of buyers. HfS expects all major service providers to have a service andsoftware implementation framework by 2020.

Proprietary │Page57©2016 HfSResearch Ltd. Excerpt forAccenture.

Increasing the Value of Engagement Through BPO and the Emerging As-a-Service Economy, Cont.

n Extend Capability and Scope of Service to Support Change and Growth: Service providers arebuilding off of established capability—talent, tools, ecosystems/partnerships—to provide morebusiness outcomeoriented, change enabling, and innovative collaboration, including:• Payroll Services: Multi-national buyers of MPHRO engagements that have an element of payroll

require specific long-tail country payroll services that go beyond the direct capabilities of manyorganizations. These long-tailed country engagement pose extensive regulatory concerns. Serviceproviders that don’t have adequate in-country operations or experience are partnering in order todeliver on these engagements rather than acquire. OneSource Virtual, Neeyamo, Infosys, Capgemini,and Xerox are all partnering with payroll specialist and in-country payroll organizations to deliver long-tail country engagements.

• Verticalization of HR Analytics: Given that the majority of HR processes are fairly standardized acrossindustry, there has been no need for service providers to tailor services to industries in the mannerthat they have in front office operations. However, given the targeting of buyer business outcomes inAs-A-Service MPHRO engagements, buyers are now seeing a need to define HR analytics by vertical,or at least by employment type (blue collar, white collar). This needs to be done in order to relatechanges in HR state (employee churn rate, absenteeism, employee engagement level, etc.) to effectson business outcomes such as: revenue impact on a per store basis, manufacturing production rates,billable hours, etc.

• Multi-tower Engagements Driving Adoption of MPHRO: Service providers including Accenture,Capgemini, Infosys and Xerox are leveraging their multi-tower outsourcing ability to drive adoption ofMPHRO contracts. Most often clients stack back office engagements with a service provider.

Proprietary │Page58©2016 HfSResearch Ltd. Excerpt forAccenture.

Increasing the Value of Engagement Through BPO and the Emerging As-a-Service Economy, Cont.

n Take Up of Digital Technology:What we see happening with social, mobile and analytics includes:• Use of Social Media for Recruiting:MPHRO service providers are expanding their social media usage

for recruitment and employee engagement. ADP’s Recruiting Manager incorporates social mediasupport functionality, allowing for posting of positions as well as search both internal and externalcandidates.

• Proving the Value of Mobility: Employees expect to interact with their organization in the same waythey interact with their friends and as consumers. Service providers are identifying this niche and aredeveloping products in support. Xerox is leveraging its in-house mobility department and haslaunched employee wellness and benefits apps that integrate with SuccessFactors, Workday andOracle HCM.

• Evolving the Use of Analytics Into the Predictive and Prescriptive Realm: The majority of serviceproviders in this study have or are in the process of developing predictive and to a lesser extentprescriptive HR analytics. The majority of this upper tier analytics is been aimed at talentmanagement functions including the prediction of likely employee churn and then the prescription ofrecommendedmanagement interventions based off of industry best practice.

Proprietary │Page59©2016 HfSResearch Ltd. Excerpt forAccenture.

Recommendations for Service Buyers and ProvidersService providers are largely geared for change and innovation in the MPHRO market; nearly all buyers haveindicated that their respective service providers continually come forward with potential areas forinnovation in respect of app implementation and predictive/prescriptive analytics. Where certain servicesproviders are lagging is on their packaging of these innovation measures. Buyers seem to be the stickingpoint in this market with many unable to adapt due to internal restrictions and lack of C-level buy in. This isand can be addressed by the following:

n Cross Client Engagement and Education: There are still a number of MPHRO service providers which donot engage clients in forums and summits. This is crucial to cross pollinate best practice between buyerorganizations. Buyers want this interaction as there is still an element of skepticism when innovation isbrought forward by a service provider who has a vested interest in providing this innovation.

n C-level Engagement: The need for C-level sponsorship of innovative MPHRO initiatives can not be overemphasized. Many innovative outsourcing engagements are scuttled due to not having top-level buy in.Also many outsourcing engagements get caught up in the tactical elements of the service delivery asopposed to the strategic outcomes of the engagement. Most buyers interviewed in this study have atactical & technical, as opposed to a strategic, relationship with their MPHRO service providers. Serviceproviders need to foster top level buy in at the initial stages of a contract.

n Working Across MPHRO Silos: Both service providers and buyers need to adapt internal practices to fitMPHRO engagements. At present much service provision from service providers is siloed by HR serviceline; in addition buyer organizations often silo internal HR departments. This often limits theeffectiveness of HR analytics due to data security differences between departments. Buyers have alsovoiced frustration at having to deal with multiple contacts from a single service provider in an MPHROenvironment.

Proprietary │Page60©2016 HfSResearch Ltd. Excerpt forAccenture.

Recommendations for Service Buyers, Cont.

Both service buyers and service providers need to regularly step outside of the everyday routine, andarticulate the business problem they are solving today, and consider the solution, and how they mightchange the current approach. One of the ways to do this is to incorporate Design Thinking into theengagement.

The value here is not just in simplifying project management and engagement, or even in price or cost, butalso in moving effectively toward a more business outcome focused, strategic, and end to end collaborationbetween service buyers and service providers.

Proprietary │Page61©2016 HfSResearch Ltd. Excerpt forAccenture.

Related Research

SOUNDBITES

ShortReadOnline:n HaveHROServiceProvidersTappedIntothe

PowerofHCMAnalytics?n AcquisitionsinHROareaResponsetothe

EmergingAs-A-ServiceEconomyn NGAGoesOnaCrash-DiettoSurvive intheAs-

A-ServiceEconomy

PoVs(POINTS OFVIEW)

DownloadWithFreeRegisteredAccess:n HRWillMakeorBreakOrganizationsinthe

DigitalAgen FromtheAshesofHROComesHRAs-A-Service

RESEARCHPAPERS

DownloadWithFreeRegisteredAccess:n BewareoftheSmoke:YourPlatformIsBurning

TheEvolutiontotheAs-a-ServiceEconomyPosesMajorOpportunitiesandThreatstoEnterprisesn TheBPOProfessionin2015:Today’sAccidentalCareerPath,Tomorrow’sCapabilityBroker

About the Author

©2016 HfSResearch Proprietary │Page63Excerpt forAccenture.

Overviewn Mike Cook is the Human Resource Services Research Director at HfS Research, shaping the firm’s

research in a newly formed ”HR-as-a-Service” domain that helps enterprises transform their HR andworkforcemanagement capabilities in the emerging As-a-Service Economy.

n Mike is responsible for driving and authoring a compelling research agenda focused on HR servicedelivery, talent management and HR-as-a-Service strategies for HR practitioners and HR industrystakeholders. He works with the HfS research team on key researchareas that are impacting HfS clients,including multi-process HRO, Payroll Outsourcing,Recruitment ProcessOutsourcing andHR SaaS.

n Mike also has specific focus on developing and supporting analyst services for HfS buyside practitionerclients across Business Process Outsourcing domains, working across the multi-disciplinary HfS analystteams.

Previous Experiencen Previously, Mike worked at BPO researcher NelsonHall as one of the firm’s leading principal analysts.

In his most recent role, he assisted buyside organizations in making strategy and provider selectiondecisions for outsourcing services across multiple BPO domains, including HRO, Customer ManagementServices, F&A, LPO,Marketing BPOand InsuranceOutsourcing.

n Mike prides himself on his ability not only to analyze a market accurately and identify how it is changing,but also to apply this knowledge in a practical, thought provoking and hands on manner for enterpriseservice buyers, providers and investors inoutsourcing and technology services.

Educationn Mike holds a Post Graduate degree in International Trade and Development Studies from the University

of Johannesburg.

Mike CookHumanResourceServicesResearchDirector,HfSResearch– Wokingham,UK

Proprietary │Page64©2016 HfSResearch Ltd. Excerpt forAccenture.

About HfS ResearchHfSResearch isTheServicesResearchCompany™—theleadinganalystauthorityandglobalcommunityforbusinessoperationsandITservices.Thefirmhelpsenterprisesvalidatetheirglobaloperatingmodelswithworld-classresearchandpeernetworking.

HfSResearchcoinedthetermTheAs-a-ServiceEconomy toillustratethechallengesandopportunitiesfacingenterprisesneedingtore-architecttheiroperationstothriveinanageofdigitaldisruption,whilegrapplingwithanincreasinglycomplexglobalbusinessenvironment.HfScreatedtheEightIdealsofBeingAs-a-Service asaguidingframeworktohelpservicebuyersandprovidersaddressthesechallengesandseizetheinitiative.

Withspecificfocusonthedigitizationofbusinessprocesses,intelligentautomationandoutsourcing,HfShasdeepindustryexpertise inhealthcare,lifesciences,retail,manufacturing,energy, utilities, telecommunications andfinancialservices. HfSusesitsgroundbreakingBlueprintMethodology™toevaluatetheabilityofserviceandtechnologyproviderstoinnovateandexecutetheEightIdeals.

HfSfacilitatesathrivinganddynamicglobalcommunityofmorethan100,000activesubscribers,whichaddsrichnesstoitsresearch.Inaddition,HfSholdsseveralServiceLeadersSummits everyyear,bringingtogetherseniorservicebuyers,providersandtechnologysuppliersinanintimateforumtodevelopcollective recommendationsfortheindustryandadddepthtothefirm’sresearchpublicationsandanalystofferings.

Nowinits tenthyearofpublication,HfSResearch’sacclaimedblogHorsesforSources isthemostwidelyreadandtrusteddestinationforunfetteredcollective insight,researchandopendebateaboutsourcingindustryissuesanddevelopments.HorsesforSourcesandtheHfSnetworkofsitesreceivemorethanamillionwebvisitsayear.

HfSwasnamedAnalystFirmoftheYearfor2016,alongsideGartnerandForrester,byleadinganalystobserverInfluencerRelations.