Hero Motocorp Ltd -...

6

Hero Motocorp Ltd ‘Buy & Add On Dips,

Transcript of Hero Motocorp Ltd -...

Hero Motocorp Ltd ‘Buy & Add On Dips,

Shareholding Pattern Particulars Dec’17 Sept’17 June'17 Promoter 34.6% 34.6% 34.6% FPIs 42.3% 42.1% 42.9% Insti. 7.3% 6.6% 11.5% N. Insti. 15.8% 16.7% 11%

Relative Capital Market Strength

Hero Motocorp Ltd

1

Mar 21, 2018

Rating Matrix CMP Rs.3513.3 Rating Buy And Add On Dips Holding Period 12-18 Months

Current Level Investment 52 week H/L Rs. 4200.0/3180.0 Upside Potential 25% - 30% Face value Rs.2

Sector Automobile and ancillaries

Category Large Cap F&O Stock Yes Risky Level Rs.4000.0 Safety Level Rs.3400.0

Source: Choice Research/ Annual reports; Financial data-Ace equity, bloomberg.

Financial Snapshot: Particulars (Rs. Mn) FY15 FY16 FY17 FY18E FY19E

Revenue from operations 2,75,380.3 3,07,153.3 3,09,581.9 3,18,108.0 3,54,203.0

EBITDA (Excl OI) 34,967.3 43,977.0 45,759.7 52,306.0 57,131.0 EBITDA Margin (%) 12.7% 14.3% 14.8% 16.4% 16.1%

PAT 23,485.1 31,122.0 35,453.0 36,999.0 40,559.0 NPM (%) 8.5% 10.1% 11.5% 11.6% 11.5% ROE (%) 34.4% 33.9% 32.2%

P/E 19.9 18.9 17.3 EPS 177.6 199.7 203.1

EV/EBITDA 15.3 12.3 11.3 P/BV 6.2 6.1 5.5

Company Synopsis: • Hero MotoCorp Ltd has a domestic 2 wheeler market share of 36.9% and 51.1%

domestic motorcycle market share. • The company has a global presence in 35 countries and the cumulative sales of the

company reached 70mn units since inception. • The subsidiaries of HMCL include HMC MM Auto Limited, HMCL Niloy Bangladesh

Limited, HMCL(NA) INC, HMCL Netherlands B.V, HMCL Colombia SAS and HMCL Americas Inc.

Outlook: • The global economy is expected to rise from 3.5% in 2017 to 3.6% in 2018, due to

buoyant financial markets and long-awaited cyclical improvement in trade and manufacturing.

• The Indian Government is targeting around US$ 376500mn investment in infrastructure over a period of three years, which will include US$ 120490mn for development of 27 industrial clusters and additional US$ 75.3bn for roads, railways and port connectivity projects. HMCL is geared to capitalize these opportunities by increasing market reach, brand strength and appropriate technology leverage.

• The company had started manufacturing of BS-IV vehicles proactively well before the stipulated time. The BS-III inventory was liquidated with minimum losses to the stakeholders. This shows the pioneering nature of the company towards new changes in the market. The preparation for production of BS-VI compliant products have started and are expected to be implemented before the proposed timeline in 2020.

• The capital expenditure of Rs.25,000mn for the next two fiscal years show the possibility of new product development, aggressive market share gains, capacity expansion of existing facilities in Gujarat as well as probable increased productivity for upcoming plants in Andhra Pradesh and Bangladesh. The CAPEX might also lead to up-gradation and modernization of the existing plant and machinery.

• The 4 new products introduced by the company namely: Glamour125, Maestro Edge, Duet and Pleasure are expected to add to the company’s sales performance in the future. The investment in Ather Energy shows increased growth in external ecosystem capacities by promoting more two wheeler start-ups in the future.

Valuation: On our valuation front, at CMP of Rs.3513.3, the company is trading at a P/E multiple of 20.3x and EV/EBITDA multiple of 14.4x which is at a discount as compared to the average P/E and average EV/EBITDA of 28.8x and 21.0x respectively. After considering all these factors and high probability of strong growth in the future, we recommend a “Buy & Add On Dips” rating on this stock.

Particular (Rs. Mn)

Q3FY18 Q3FY17 Change (YoY)

Total Revenue 73,054.0 68,986.0 5.9%

EBITDA (Excl OI) 11,579.9 10,812.6 7.1%

EBITDA Margin (%)

15.9% 15.7%

PAT 8054.3 7720.5 4.3%

NPM (%) 11.0% 11.2%

Quarterly Snapshot:

• Hero MotoCorp Limited is a two-wheeler manufacturer. The Company manufactures and sells motorized two wheelers up to 350 cubic centimeters (cc) engine capacity, spare parts and related services.

• Its manufacturing plants are located in Dharuhera, Haryana; Gurgaon, Haryana; Haridwar, Uttarakhand; Neemrana, Rajasthan, and Villa Rica, Colombia. Its research and development center is located in Jaipur, Rajasthan.

• It has a Global Parts Centre for manufacturing and supplying the parts at local and global markets at Neemrana, Rajasthan.

• Its products include Karizma ZMR, Karizma, Xtreme Sports, Xtreme, Hunk, Impulse, Achiever, Ignitor, Glamour Programmed FI, Glamour, Super Splendor, Passion XPRO, iSmart 110, Passion PRO, Passion PRO TR, Splendor iSmart, Splendor PRO Classic, Splendor PRO, Splendor+, HF Deluxe ECO, HF Deluxe, HF Dawn, Duet, Maestro Edge, Maestro and Pleasure.

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

28-

Feb

-17

31-

Mar

-17

30-

Ap

r-17

31-

May

-17

30-

Jun

-17

31-

Jul-

17

31-

Au

g-17

30-

Sep

-17

31-

Oct

-17

30-

No

v-17

31-

Dec

-17

31-

Jan

-18

Hero Motocorp Ltd Sensex

23

7,6

81

.10

25

7,1

96

.60

27

5,3

80

.30

30

7,1

53

.30

30

9,5

81

.90

13.82% 13.76%

12.70%

14.32%

14.78%

11.50%

12.00%

12.50%

13.00%

13.50%

14.00%

14.50%

15.00%

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

350,000.00

FY13 FY14 FY15 FY16 FY17

Revenue From Operations

EBITDA Margin

2 Source: Choice Research/ Annual reports; Financial data-Ace equity

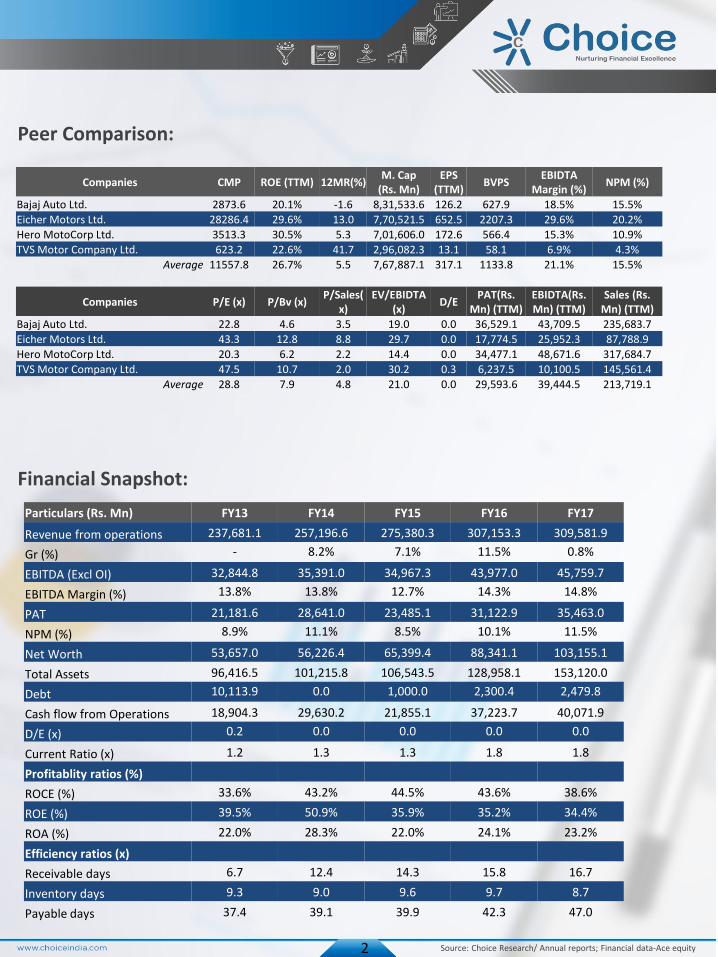

Peer Comparison:

Financial Snapshot:

Particulars (Rs. Mn) FY13 FY14 FY15 FY16 FY17

Revenue from operations 237,681.1 257,196.6 275,380.3 307,153.3 309,581.9

Gr (%) - 8.2% 7.1% 11.5% 0.8%

EBITDA (Excl OI) 32,844.8 35,391.0 34,967.3 43,977.0 45,759.7

EBITDA Margin (%) 13.8% 13.8% 12.7% 14.3% 14.8%

PAT 21,181.6 28,641.0 23,485.1 31,122.9 35,463.0

NPM (%) 8.9% 11.1% 8.5% 10.1% 11.5%

Net Worth 53,657.0 56,226.4 65,399.4 88,341.1 103,155.1

Total Assets 96,416.5 101,215.8 106,543.5 128,958.1 153,120.0

Debt 10,113.9 0.0 1,000.0 2,300.4 2,479.8

Cash flow from Operations 18,904.3 29,630.2 21,855.1 37,223.7 40,071.9

D/E (x) 0.2 0.0 0.0 0.0 0.0

Current Ratio (x) 1.2 1.3 1.3 1.8 1.8

Profitablity ratios (%)

ROCE (%) 33.6% 43.2% 44.5% 43.6% 38.6%

ROE (%) 39.5% 50.9% 35.9% 35.2% 34.4%

ROA (%) 22.0% 28.3% 22.0% 24.1% 23.2%

Efficiency ratios (x)

Receivable days 6.7 12.4 14.3 15.8 16.7

Inventory days 9.3 9.0 9.6 9.7 8.7

Payable days 37.4 39.1 39.9 42.3 47.0

Companies CMP ROE (TTM) 12MR(%) M. Cap

(Rs. Mn) EPS

(TTM) BVPS

EBIDTA Margin (%)

NPM (%)

Bajaj Auto Ltd. 2873.6 20.1% -1.6 8,31,533.6 126.2 627.9 18.5% 15.5%

Eicher Motors Ltd. 28286.4 29.6% 13.0 7,70,521.5 652.5 2207.3 29.6% 20.2%

Hero MotoCorp Ltd. 3513.3 30.5% 5.3 7,01,606.0 172.6 566.4 15.3% 10.9%

TVS Motor Company Ltd. 623.2 22.6% 41.7 2,96,082.3 13.1 58.1 6.9% 4.3%

Average 11557.8 26.7% 5.5 7,67,887.1 317.1 1133.8 21.1% 15.5%

Companies P/E (x) P/Bv (x) P/Sales(

x) EV/EBIDTA

(x) D/E

PAT(Rs. Mn) (TTM)

EBIDTA(Rs. Mn) (TTM)

Sales (Rs. Mn) (TTM)

Bajaj Auto Ltd. 22.8 4.6 3.5 19.0 0.0 36,529.1 43,709.5 235,683.7

Eicher Motors Ltd. 43.3 12.8 8.8 29.7 0.0 17,774.5 25,952.3 87,788.9

Hero MotoCorp Ltd. 20.3 6.2 2.2 14.4 0.0 34,477.1 48,671.6 317,684.7

TVS Motor Company Ltd. 47.5 10.7 2.0 30.2 0.3 6,237.5 10,100.5 145,561.4

Average 28.8 7.9 4.8 21.0 0.0 29,593.6 39,444.5 213,719.1

3 Source: Choice Research/ Annual reports; Financial data-Ace equity

Q3FY18 Result Highlights: During Q3FY18, the operating income increased from Rs.68,986mn in Q3FY17 to Rs.73,054mn in Q3FY18, with a 5.9% increase in YoY basis. The EBITDA increased from Rs.10,812.6mn in Q3FY17 to Rs.11,579mn in Q3FY18, with a 7.1% increase in YoY basis. PAT increased from Rs.7720.5mn in Q3FY17 to Rs.8054.3mn in Q3FY18. Con-Call Highlights: • The PAT of Rs.8050mn that reflects a 4% growth compared to an EBITDA growth of 7%, which is lower due to capitalization

of Halol and CIT over the last four quarters and also lower other income which is due to MTM losses on back of rising bond yields.

• The domestic 2 wheeler industry is expected to grow close to double digit in FY19 on account of the robust rural demand. • The rural demand is expected to increase with the help of the increased Government focus on rural infrastructure as per

the Union Budget. • The new launch in the 200CC category in India namely Xtreme200 is expected to generate high revenues. The company

also plans to enter the 300CC category in the future. • The revenue from spare parts business also witnessed a 35% growth in the current quarter. • The dealership networks of Hero Motocorp currently include 6500 dealership networks across India and the company aims

to expand it in the future. Capital Expenditure: • The company has planned a capital expenditure of around Rs.25,000mn up to FY19 towards new product development,

digitization, phase wise capacity installation and expansion at existing as well as at upcoming facilities in Andhra Pradesh and Bangladesh.

• The capital expenditure also includes investments towards upgradation and modernization of plant and machinery. Indian Two Wheeler Growth Trends: Indian Two Wheeler Growth Trends: (Domestic + Exports) (Domestic)

Subsidiary Company Information: • HMCL Netherlands B.V. (HNBV): HNBV is a wholly owned subsidiary of HMCL which was incorporated in Amsterdam as a

private company, with the objective of promoting foreign investments. During FY17 HNBV invested in operating companies in Colombia and Bangladesh, but reported a net loss of Rs.8.3mn

• HMCL Colombia S.A.S. (HMCLC): HMCLC was incorporated in Colombia as a JV between HNMV and Woven Holdings LLC as a simplified stock corporation company. HNBV owns 51% equity in HMCLC and 49% equity in Woven Holdings LLC. The production capacity of HMCLC is 60,000 units per annum. During FY17 the subsidiary reported a loss of Rs6530mn.

• HMCL Niloy Bangladesh Limited (HNBL): HNBL was incorporated as a JV between HNBV and Neloy Motors Ltd. HNBV holds 55% equity in HNBL and 45% equity in Nitol Niloy Group.

• HMCL Americas Inc. (HMCLA), HMCL (NA) and Eric Buell Racing, Inc.(EBR): Both these subsidiaries are incorporated in Delaware, USA. HMCL (NA) has invested in Eric Buell Racing Inc. by subscribing 49.2% of equity.

• HMC MM Auto Limited (‘HMCMMA’): HMC has a JV with Magneti Marelli S.p.A Italy, which was set to carry out manufacturing assembly, sale and distribution of two wheeler fuel injection systems and parts. HMCL holds 60% equity in HMCMMA.

Production Facilities:

0

5

10

15

20

25

All 2W Motorcycles Scooters Moped

FY17 FY16

0

5

10

15

20

25

30

35

40

All 2W Motorcycles Scooters Moped

FY17 FY16

Locations Capacity

Haryana 4.2mn units p.a

Uttarakhand 2.7mn units p.a

Rajasthan 1.1mn units p.a

Gujarat 1.2mn units p.a

The upcoming production facilities of the company are expected to increase phase-wise product development and expansion. The first phase capacity of the new plant in Vadodra is expected to have a capacity of 1.2mn units p.a., which will ultimately lead to an overall increase of 1800mn units p.a.

Choice’s Rating Rationale The price target for a large cap stock represents the value the analyst expects the stock to reach over next 12 months. For a stock to be classified as Outperform, the expected return must exceed the local risk free return by at least 5% over the next 12 months. For a stock to be classified as Underperform, the stock return must be below the local risk free return by at least 5% over the next 12 months. Stocks between these bands are classified as Neutral. Don’t be an Investor by Force, Be an investor by CHOICE

• Create a Wealth Building Portfolio with the help of CHOICE Fundamental Research. • CHOICE Fundamental Research will handpick stocks for you to invest in an oversold market by helping you build positions in

heavily beaten down fundamentally strong stocks. • Opportunities to invest in fundamentally strong stocks at a low arise only 2-3 times in a full year cycle. • Investors are advised to sell the stock if the recommended upside potential achieves. • If recommended upside potential remains under-achieved, investors are advised to consider the update report on

suggested stock.

Fundamental Research Team

Name Designation Email id Contact No.

Sunder Sanmukhani Head-Fundamental Research [email protected] 022 - 6707 9910

Satish Kumar Research Analyst [email protected] 022 - 6707 9913

Rajnath Yadav Research Analyst [email protected] 022 - 6707 9912

Aman Lamba Research Associate [email protected] 022 - 67079917

Rahul Agarwal Research Associate [email protected] 022 - 67079916

Shrey Gandhi Research Associate [email protected] 022 - 67079914

Dhruv Thakkar Research Associate [email protected] 022 - 67079915

4

OUR TEAM

Disclaimer

This is solely for information of clients of Choice Broking and does not construe to be an investment advice. It is also not intended as an offer or solicitation for the purchase and sale of any financial instruments. Any action taken by you on the basis of the information contained herein is your responsibility alone and Choice Broking its subsidiaries or its employees or associates will not be liable in any manner for the consequences of such action taken by you. We have exercised due diligence in checking the correctness and authenticity of the information contained in this recommendation, but Choice Broking or any of its subsidiaries or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this recommendation or any action taken on basis of this information. This report is based on the fundamental analysis with a view to forecast future price. The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. Choice Broking has based this document on information obtained from sources it believes to be reliable but which it has not independently verified; Choice Broking makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. The opinions contained within the report are based upon publicly available information at the time of publication and are subject to change without notice. The information and any disclosures provided herein are in summary form and have been prepared for informational purposes. The recommendations and suggested price levels are intended purely for stock market investment purposes. The recommendations are valid for the day of the report and will remain valid till the target period. The information and any disclosures provided herein may be considered confidential. Any use, distribution, modification, copying, forwarding or disclosure by any person is strictly prohibited. The information and any disclosures provided herein do not constitute a solicitation or offer to purchase or sell any security or other financial product or instrument. The current performance may be unaudited. Past performance does not guarantee future returns. There can be no assurance that investments will achieve any targeted rates of return, and there is no guarantee against the loss of your entire investment.

POTENTIAL CONFLICT OF INTEREST DISCLOSURE (as on date of report) Disclosure of interest statement – • Analyst interest of the stock /Instrument(s): - No. • Firm interest of the stock / Instrument (s): - No.

Choice Equity Broking Pvt. Ltd. Choice House, Shree Shakambhari Corporate Park, Plt No: -156-158,

J.B. Nagar, Andheri (East), Mumbai - 400 099.

+91-022-6707 9999 +91-022-6707 9959 www.choicebroking.in

5