Healthcare Reform - TMHRA · PDF file• Baby-boomer enrollment wave • Decreasing...

56

We’re for you. Healthcare Reform What The Future Holds

-

Upload

hoangtuyen -

Category

Documents

-

view

215 -

download

0

Transcript of Healthcare Reform - TMHRA · PDF file• Baby-boomer enrollment wave • Decreasing...

We’re for you. Healthcare Reform What The Future Holds

Average Annual Premiums for Single and Family Coverage,

1999-2012

* Estimate is statistically different from estimate for the previous year shown (p<.05).

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2012.

$15,745*

Cumulative Increases in Health Insurance Premiums, Workers’ Contributions to Premiums, Inflation, and

Workers’ Earnings, 1999-2012

38%

109%

172%

38%

113%

180%

11%

29%

47%

8%

24%

38%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Health Insurance Premiums Workers' Contribution to Premiums Workers' Earnings Overall Inflation

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2012. Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April), 1999-2012; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey, 1999-2012 (April to April).

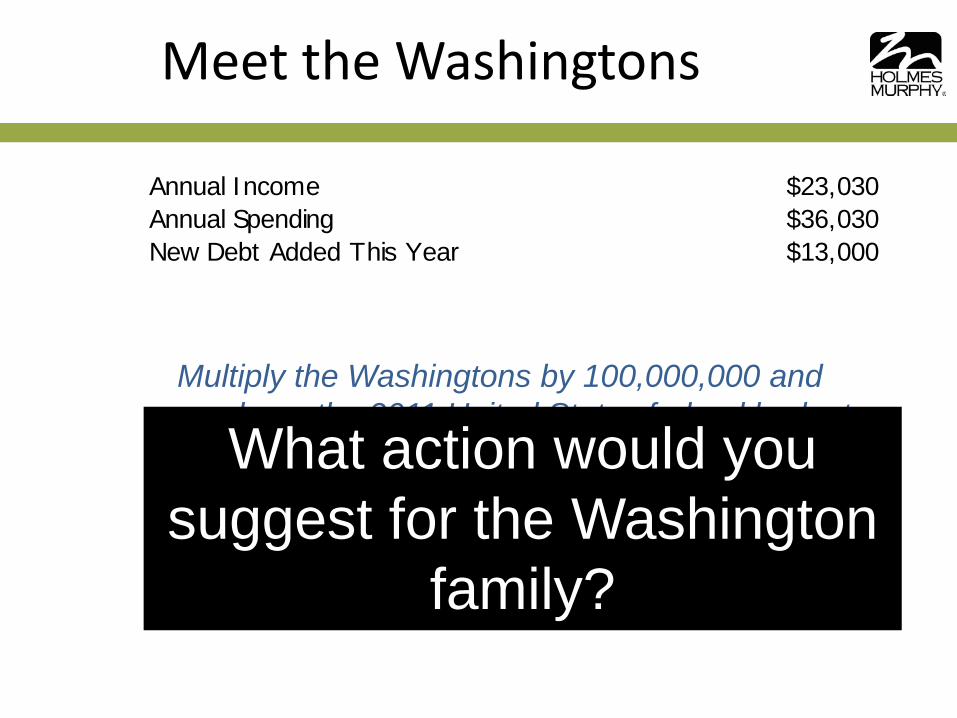

Annual Income $23,030Annual Spending $36,030New Debt Added This Year $13,000Credit Card Balance $101,280Mortgage $633,000

Meet the Washingtons

Annual Income $2,303,000,000,000Annual Spending $3,603,000,000,000New Debt Added This Year $1,300,000,000,000Debt Held by Public $10,128,000,000,000Unfunded Soc. Sec. / Medicare Liability $63,300,000,000,000

Multiply the Washingtons by 100,000,000 and you have the 2011 United States federal budget

What action would you suggest for the Washington

family?

PPACA and Medicare

• The gap between Medicare and private insurance payments to hospitals will continue to spread because the inflation rate for Medicare is now legislatively fixed

• Medicare future funding – Average of medical services CPI

and urban consumer CPI – After 2019, GDP growth plus 1%

• Independent Payment Advisory Board (IPAB)

6

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

2009 2010

$89.22

$36.60

Trill

ion

$

Medicare Unfunded Liability

Liability dropped by

over $56 trillion in one year

Medicare Solvency 2009 vs 2012 Trustee Report

Factors Driving Insolvency • Increasing costs per enrollee • Baby-boomer enrollment wave • Decreasing workers per enrollee

Factors Delaying Insolvency • New Medicare taxes eff 1/1/13 • Cuts to hospital reimbursements • Cuts to Medicare Advantage plans

Public vs Private Inflation

Confidential © Copyright 2012 Holmes Murphy & Associates 8

The Healthcare Squeeze

1%

2%

3%

4%

5%

6%

7%

Healthcare Inflation

5.06% Medicare Healthcare

Inflation 2.04%

Commercial Healthcare

Inflation 7.05%

Hidden Medicare Tax

Medicare Commercial Source: Standard & Poor Healthcare Economic Indices, Nov 2012

3

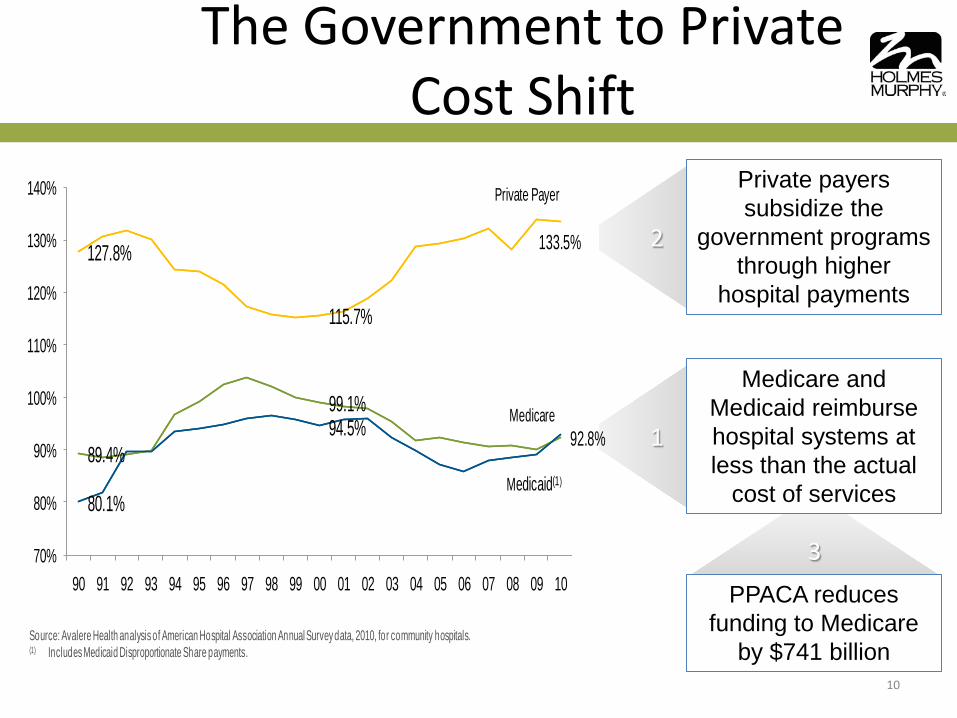

1

Source: Avalere Health analysis of American Hospital Association Annual Survey data, 2010, for community hospitals. (1) Includes Medicaid Disproportionate Share payments.

89.4%

99.1% Medicare

80.1%

94.5%

Medicaid(1)

127.8%

115.7%

Private Payer

70%

80%

90%

100%

110%

120%

130%

140%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

133.5%

92.8%

The Government to Private Cost Shift

10

Medicare and Medicaid reimburse hospital systems at less than the actual

cost of services

2

Private payers subsidize the

government programs through higher

hospital payments

PPACA reduces funding to Medicare

by $741 billion

PPACA Insurance Provision Funding

Confidential © Copyright 2012 Holmes Murphy & Associates 11

Gross Cost, $1,872

Gross Income and Savings, $553

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

$ Bi

llion

Year

Insurance Coverage Provisions of PPACA 2014-2023

Funding Healthcare Reform 2013-2022

$ Tr

illio

n

$0

$1

-$2

$1.86 Trillion in new

insurance provision spending

-Medicaid expansion - Exchange subsidies

- Small business tax credits

$.73 Trillion in new spending

cuts -Hospitals -Medicare Advantage

$.57 Trillion in new Medicare

taxes and industry fees

Insurance Provisions Other Funding Sources Primarily Medicare

$.67 Trillion in new insurance provision taxes and penalties

Source: Congressional Budget Office, July 2012

Budget Neutral

Medicare Accounting

13

“In practice, the improved Part A financing cannot be simultaneously used to finance other Federal outlays (such as the coverage expansions under the PPACA) and to extend the trust fund, despite the appearance of this result from the respective accounting conventions.” Solomon Musey, A.S.A. Office of the Actuary Centers for Medicare and Medicaid Service April 22, 2010

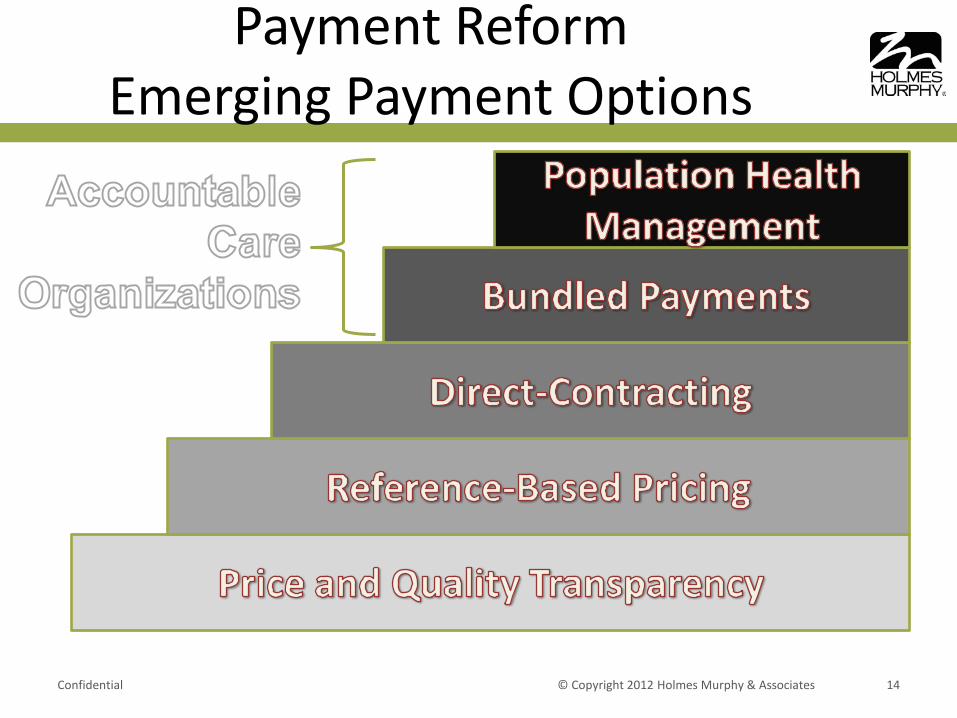

Payment Reform Emerging Payment Options

Confidential © Copyright 2012 Holmes Murphy & Associates 14

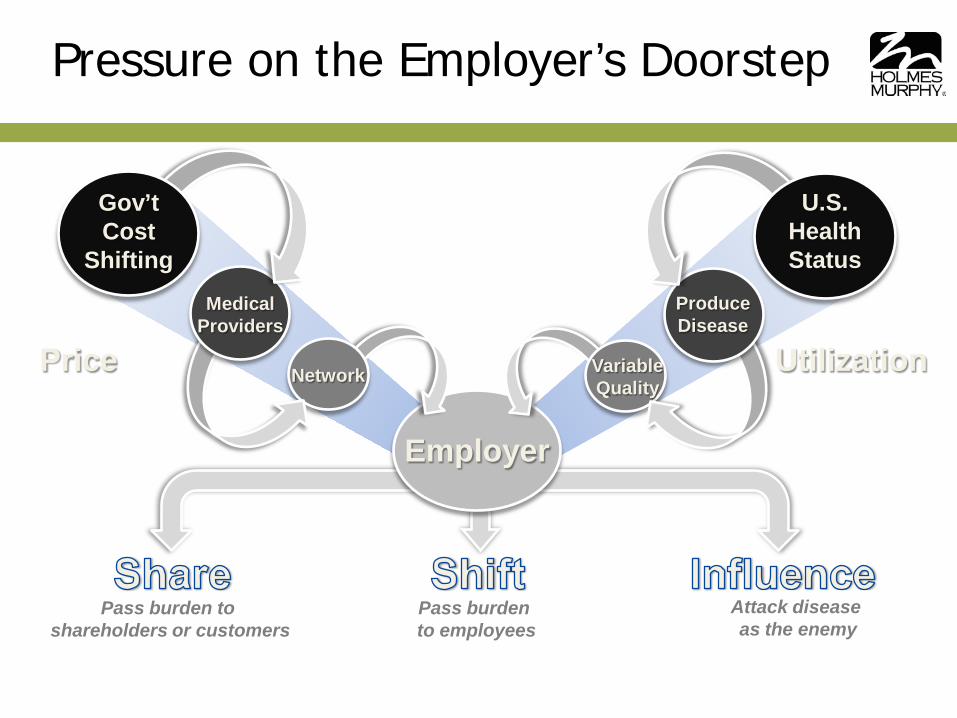

Attack disease as the enemy

Pass burden to shareholders or customers

Pass burden to employees

Pressure on the Employer’s Doorstep

Employer

Network

Produce Disease

Medical Providers

Variable Quality

Gov’t Cost

Shifting

U.S. Health Status

Price Utilization

Healthcare 2020

Confidential © Copyright 2012 Holmes Murphy & Associates 16

What Is An ACO?

Confidential © Copyright 2012 Holmes Murphy & Associates 17

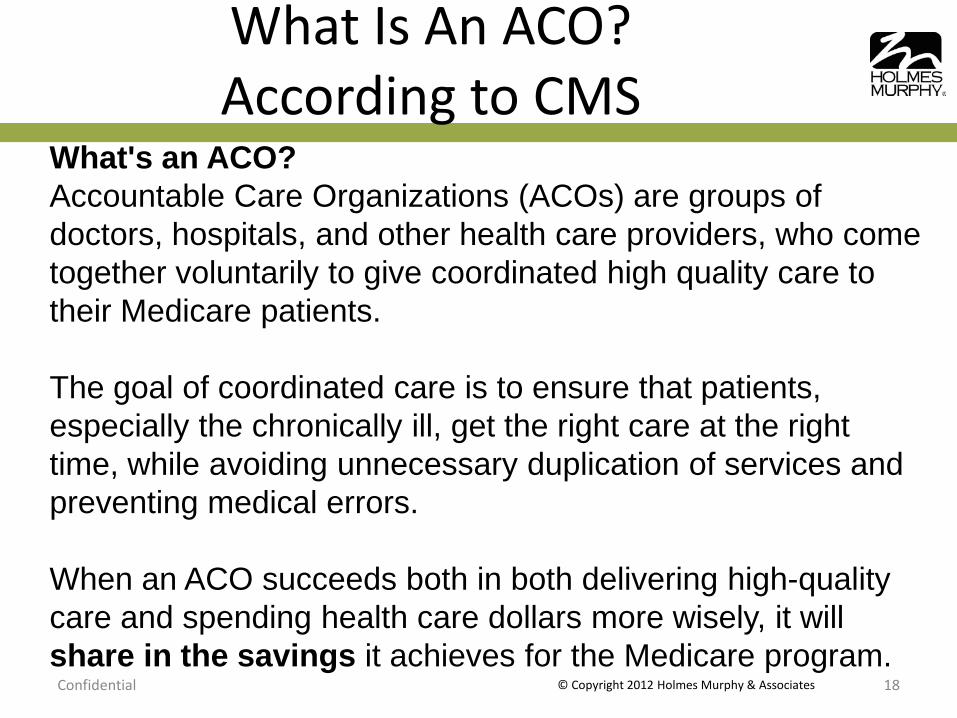

What Is An ACO? According to CMS

Confidential © Copyright 2012 Holmes Murphy & Associates 18

What's an ACO? Accountable Care Organizations (ACOs) are groups of doctors, hospitals, and other health care providers, who come together voluntarily to give coordinated high quality care to their Medicare patients. The goal of coordinated care is to ensure that patients, especially the chronically ill, get the right care at the right time, while avoiding unnecessary duplication of services and preventing medical errors. When an ACO succeeds both in both delivering high-quality care and spending health care dollars more wisely, it will share in the savings it achieves for the Medicare program.

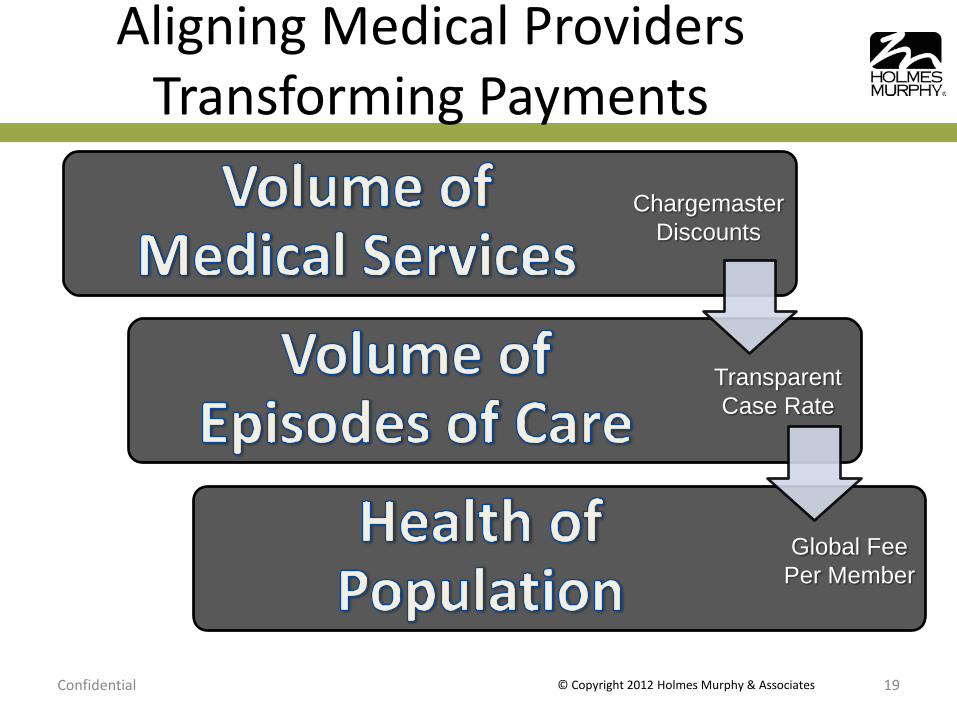

Aligning Medical Providers Transforming Payments

Confidential © Copyright 2012 Holmes Murphy & Associates 19

Chargemaster Discounts

Transparent Case Rate

Global Fee Per Member

Aligning Medical Providers Private vs Government System

Confidential © Copyright 2012 Holmes Murphy & Associates 20

47.4%

12.3%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Canada

United States

% Physician Who Are General Practitioners

Source: OECD Health at a Glance, 2011

Aligning Medical Providers Physician Compensation

Confidential © Copyright 2012 Holmes Murphy & Associates 21

0% 1%

6% 8%

9% 9%

15% 18%

34% 41% 42%

52% 54%

55% 70%

73% 73%

81% 89%

94% 98% 98%

101% 102% 102%

0% 20% 40% 60% 80% 100% 120%

Pediatrics Family Medicine

Internal Medicine Diabetes/Endocrinology

HIV/ID Psychiatry

Rheumatology Neurology

Nephrology OB/Gyn

Pathology Emergency Medicine

Critical Care Pulomonary Medicine

General Surgery Plastic Surgery Opthalmology

Dermatology Oncology

Gastroenterology Anesthesiology

Urology Cardiolology

Radiology Orthopedics

Compensation by Specialty, 2012

Source: Medscape

Payment Reform Bad News and Good News

• Healthcare reform is creating the platform to pay providers differently – Creation of Accountable Care

Organizations – Move toward integrated

bundled payments – Vision toward population

health management and payment

Confidential © Copyright 2012 Holmes Murphy & Associates 22

• Discounts are not an

effective sustainable cost-containment tool – No control over retail

“charge-master” – No control over utilization

increases – No control over service or

billing intensity

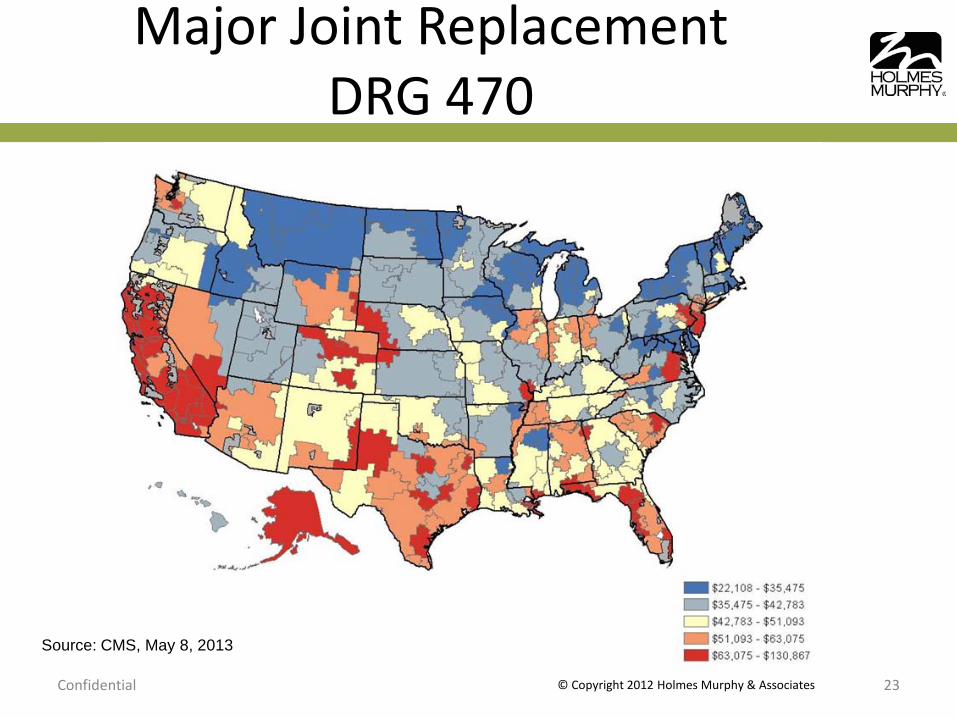

Major Joint Replacement DRG 470

Confidential © Copyright 2012 Holmes Murphy & Associates 23

Source: CMS, May 8, 2013

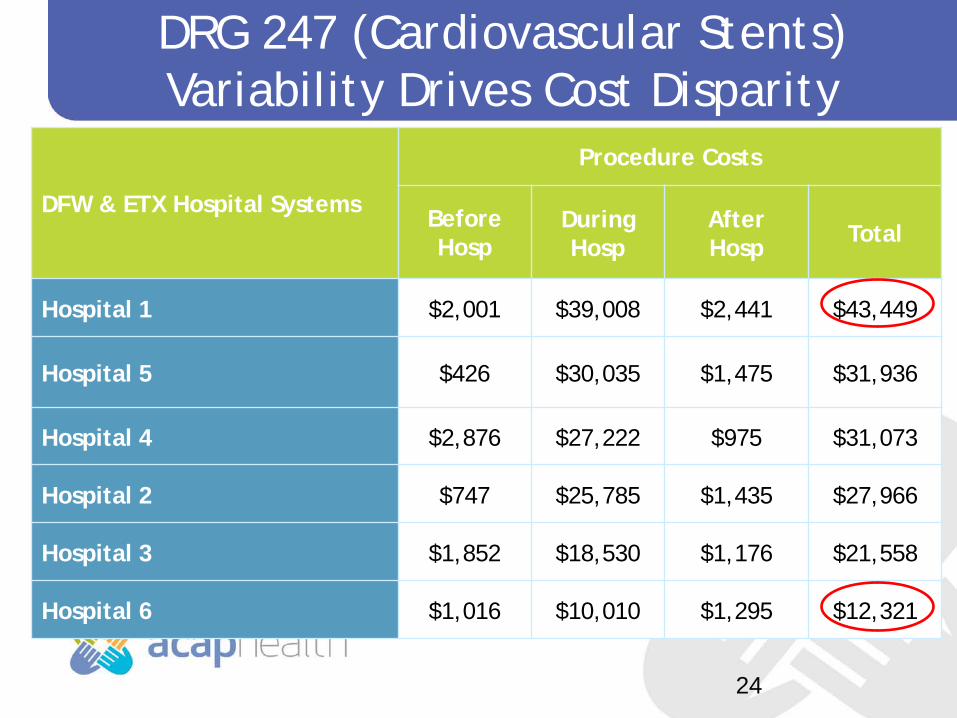

DRG 247 (Cardiovascular Stents) Variability Drives Cost Disparity

24

DFW & ETX Hospital Systems

Procedure Costs

Before Hosp

During Hosp

After Hosp Total

Hospital 1 $2,001 $39,008 $2,441 $43,449

Hospital 5 $426 $30,035 $1,475 $31,936

Hospital 4 $2,876 $27,222 $975 $31,073

Hospital 2 $747 $25,785 $1,435 $27,966

Hospital 3 $1,852 $18,530 $1,176 $21,558

Hospital 6 $1,016 $10,010 $1,295 $12,321

Age-Adjusted Prevalence of Obesity and Diagnosed Diabetes Among U.S. Adults Aged 18 Years or older

Obesity (BMI ≥30 kg/m2)

Diabetes

1994

1994

2000

2000

No Data <14.0% 14.0-17.9% 18.0-21.9% 22.0-25.9% >26.0%

No Data <4.5% 4.5-5.9% 6.0-7.4% 7.5-8.9% >9.0%

CDC’s Division of Diabetes Translation. National Diabetes Surveillance System available at http://www.cdc.gov/diabetes/statistics

2010

2010

Healthcare 2020

Confidential © Copyright 2012 Holmes Murphy & Associates 26

American Obesity

Confidential © Copyright 2012 Holmes Murphy & Associates 27

Safe Harbor Trap

Mary earns $38,000 per year She is single with two children

Single Coverage $4800 annual premium

Employer Subsidy $2000

Mary’s Cost $2800

Affordability @ 9.5% of W-2 $3610

Family Coverage $10,000 annual premium

Employer Subsidy $4000

Mary’s Cost $6000

Affordability for family is not applicable

Family Coverage Employer, $6,000

Family Coverage Exchange, $2,394

$- $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000

Employer vs Exchange Net Cost

Healthcare 2020

Confidential © Copyright 2012 Holmes Murphy & Associates 29

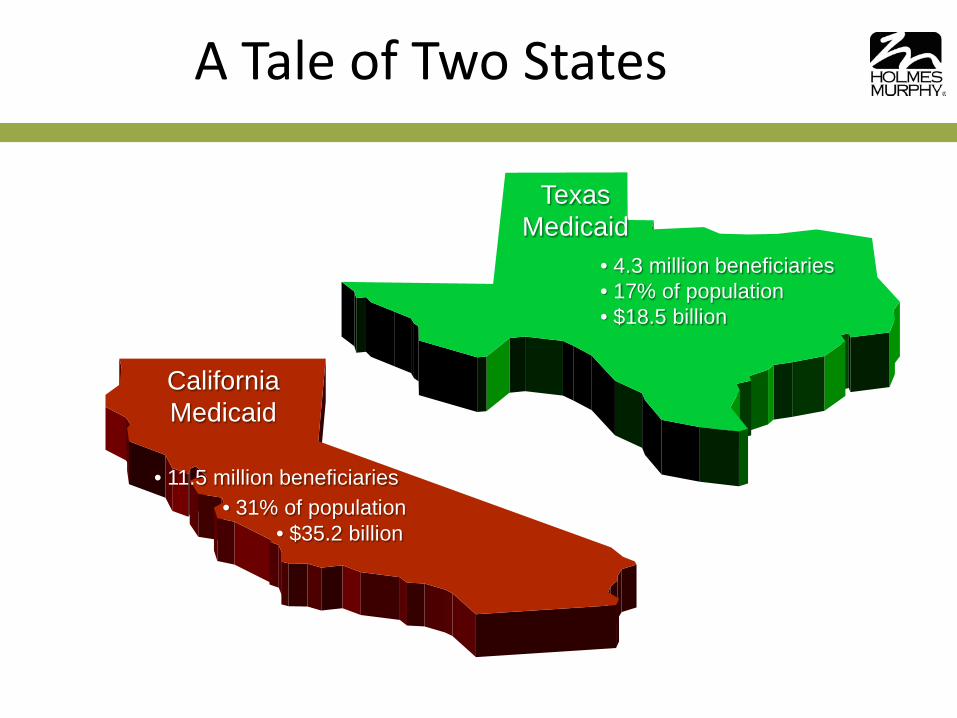

Medicaid Consumes More of the State Budget

-53.4%

-18.6%

70.8%

-4.9%

-60.0% -40.0% -20.0% 0.0% 20.0% 40.0% 60.0% 80.0%

Other

Public Safety

Medicaid / HHS

Public Education

Budget Allocation Change From 2000 to 2012-2013

Source: State of Texas

California Medicaid

Texas Medicaid

• 4.3 million beneficiaries • 17% of population • $18.5 billion

• 11.5 million beneficiaries • 31% of population

• $35.2 billion

A Tale of Two States

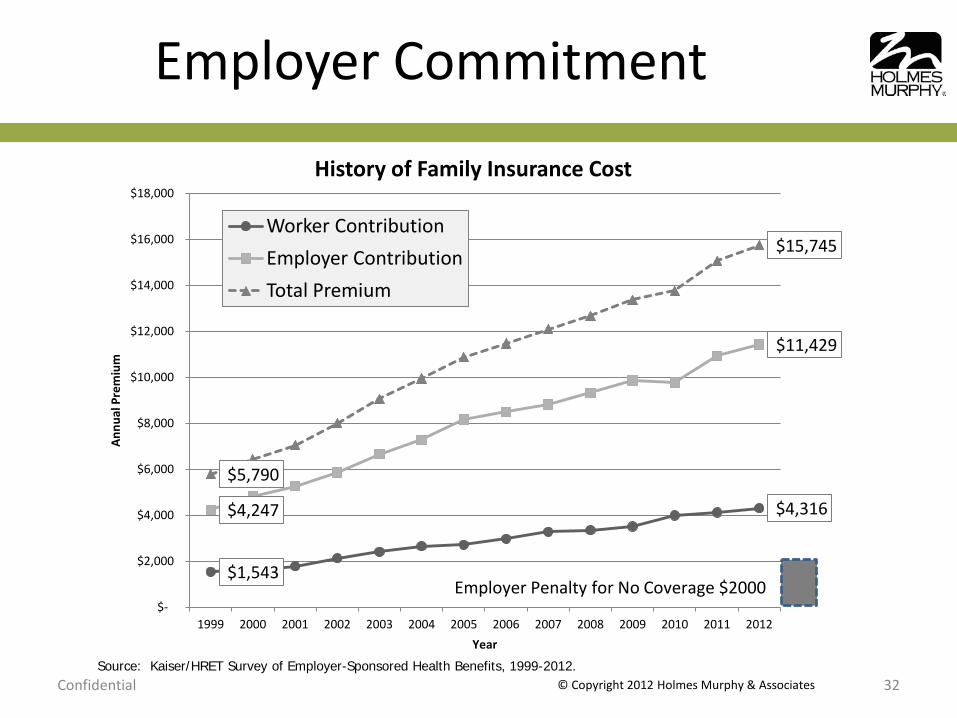

Employer Commitment

Confidential © Copyright 2012 Holmes Murphy & Associates 32

$1,543

$4,316 $4,247

$11,429

$5,790

$15,745

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Annu

al P

rem

ium

Year

History of Family Insurance Cost

Worker Contribution Employer Contribution Total Premium

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2012.

Employer Penalty for No Coverage $2000

Pay or Play Penalties

Penalties Individual

2014

$95 or 1%

2015

$325 or 2%

2016

$695 or 2.5%

Employer

<50 FTE

No penalty

No Plan

$2000 First 30

Free

Not Affordable

$3000 per person

with subsidy

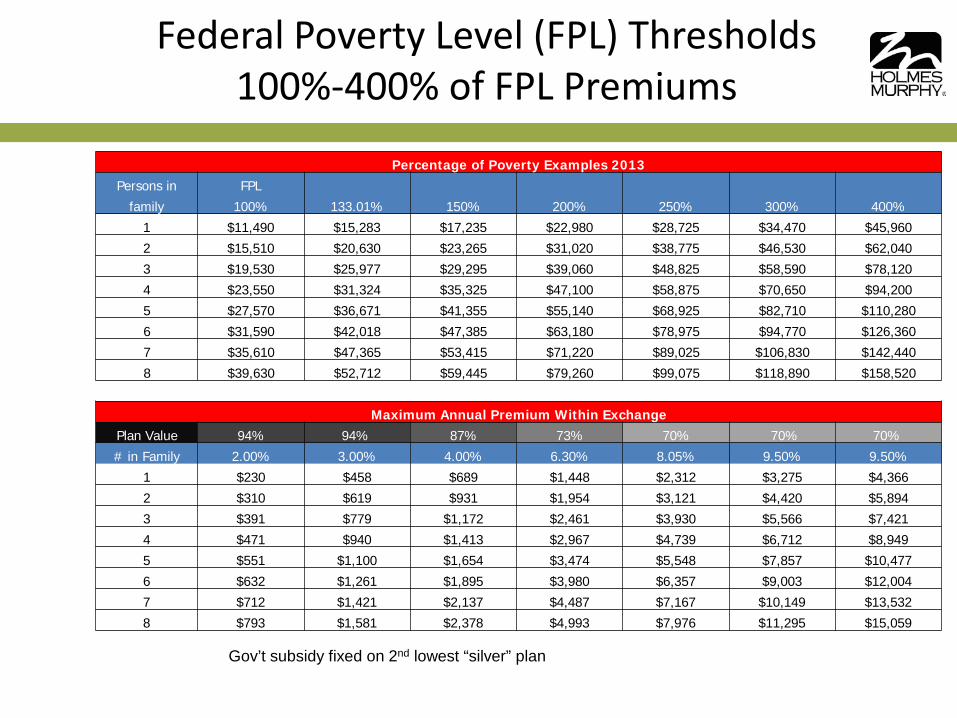

Percentage of Poverty Examples 2013 Persons in FPL

family 100% 133.01% 150% 200% 250% 300% 400%

1 $11,490 $15,283 $17,235 $22,980 $28,725 $34,470 $45,960

2 $15,510 $20,630 $23,265 $31,020 $38,775 $46,530 $62,040

3 $19,530 $25,977 $29,295 $39,060 $48,825 $58,590 $78,120

4 $23,550 $31,324 $35,325 $47,100 $58,875 $70,650 $94,200

5 $27,570 $36,671 $41,355 $55,140 $68,925 $82,710 $110,280

6 $31,590 $42,018 $47,385 $63,180 $78,975 $94,770 $126,360

7 $35,610 $47,365 $53,415 $71,220 $89,025 $106,830 $142,440

8 $39,630 $52,712 $59,445 $79,260 $99,075 $118,890 $158,520

Maximum Annual Premium Within Exchange Plan Value 94% 94% 87% 73% 70% 70% 70%

# in Family 2.00% 3.00% 4.00% 6.30% 8.05% 9.50% 9.50%

1 $230 $458 $689 $1,448 $2,312 $3,275 $4,366

2 $310 $619 $931 $1,954 $3,121 $4,420 $5,894

3 $391 $779 $1,172 $2,461 $3,930 $5,566 $7,421

4 $471 $940 $1,413 $2,967 $4,739 $6,712 $8,949

5 $551 $1,100 $1,654 $3,474 $5,548 $7,857 $10,477

6 $632 $1,261 $1,895 $3,980 $6,357 $9,003 $12,004

7 $712 $1,421 $2,137 $4,487 $7,167 $10,149 $13,532

8 $793 $1,581 $2,378 $4,993 $7,976 $11,295 $15,059

Federal Poverty Level (FPL) Thresholds 100%-400% of FPL Premiums

Gov’t subsidy fixed on 2nd lowest “silver” plan

Percentage of Poverty Examples 2013 Persons in FPL

family 100% 133.01% 150% 200% 250% 300% 400%

1 $11,490 $15,283 $17,235 $22,980 $28,725 $34,470 $45,960

2 $15,510 $20,630 $23,265 $31,020 $38,775 $46,530 $62,040

3 $19,530 $25,977 $29,295 $39,060 $48,825 $58,590 $78,120

4 $23,550 $31,324 $35,325 $47,100 $58,875 $70,650 $94,200

5 $27,570 $36,671 $41,355 $55,140 $68,925 $82,710 $110,280

6 $31,590 $42,018 $47,385 $63,180 $78,975 $94,770 $126,360

7 $35,610 $47,365 $53,415 $71,220 $89,025 $106,830 $142,440

8 $39,630 $52,712 $59,445 $79,260 $99,075 $118,890 $158,520

Maximum Annual Premium Within Exchange Plan Value 94% 94% 87% 73% 70% 70% 70%

# in Family 2.00% 3.00% 4.00% 6.30% 8.05% 9.50% 9.50%

1 $230 $458 $689 $1,448 $2,312 $3,275 $4,366

2 $310 $619 $931 $1,954 $3,121 $4,420 $5,894

3 $391 $779 $1,172 $2,461 $3,930 $5,566 $7,421

4 $471 $940 $1,413 $2,967 $4,739 $6,712 $8,949

5 $551 $1,100 $1,654 $3,474 $5,548 $7,857 $10,477

6 $632 $1,261 $1,895 $3,980 $6,357 $9,003 $12,004

7 $712 $1,421 $2,137 $4,487 $7,167 $10,149 $13,532

8 $793 $1,581 $2,378 $4,993 $7,976 $11,295 $15,059

Federal Poverty Level (FPL) Thresholds 100%-400% of FPL Premiums

Gov’t subsidy fixed on 2nd lowest “silver” plan

$70,650 x 9.5% = $6,712

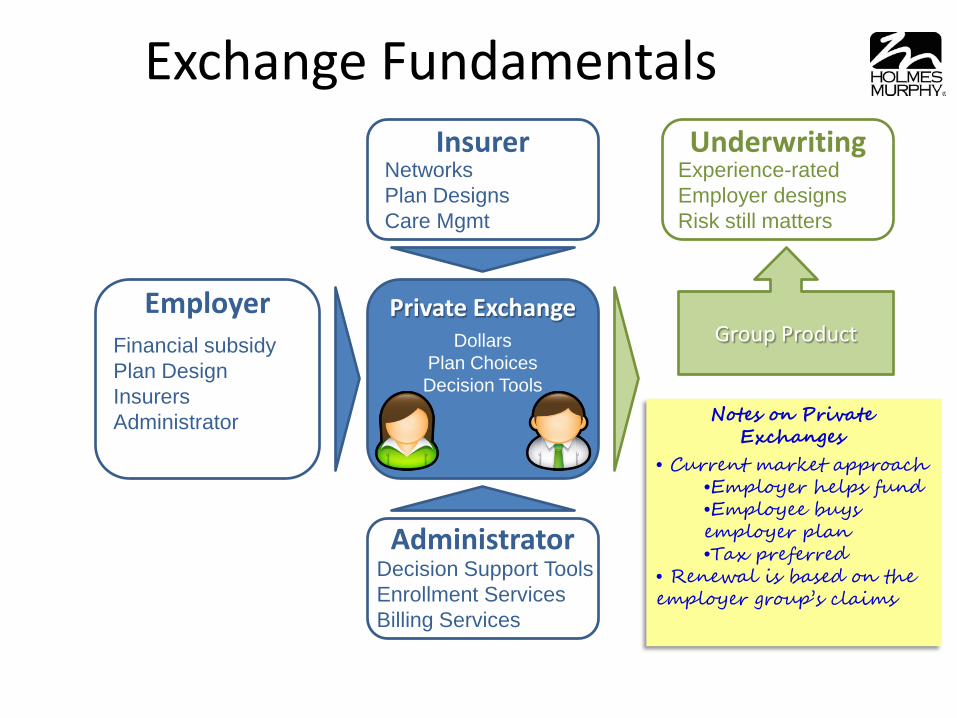

Exchange Fundamentals

Private Exchange

Employer

Insurer

Administrator

Decision Support Tools Enrollment Services Billing Services

Networks Plan Designs Care Mgmt

Financial subsidy Plan Design Insurers Administrator

Dollars Plan Choices Decision Tools

Individual Product

Underwriting

Community-rated Insurer designs Risk neutral

• Ideal scenario

•Employer helps fund •Employee buys on the open market •Tax preferred

• Unfortunately it is not allowable under current regulations

Notes on Private Exchanges

Exchange Fundamentals

Private Exchange

Employer

Insurer

Administrator

Decision Support Tools Enrollment Services Billing Services

Networks Plan Designs Care Mgmt

Financial subsidy Plan Design Insurers Administrator

Dollars Plan Choices Decision Tools

Group Product

Underwriting

Experience-rated Employer designs Risk still matters

• Current market approach

•Employer helps fund •Employee buys employer plan •Tax preferred

• Renewal is based on the employer group’s claims

Notes on Private Exchanges

Healthcare 2020

Confidential © Copyright 2012 Holmes Murphy & Associates 38

What You Pay vs Medicare

Confidential © Copyright 2012 Holmes Murphy & Associates 39

$283.00

$20.44

$-

$50

$100

$150

$200

$250

$300

Billed Charge Medicare

Chest X-Ray

Source: Time, March 4, 2013

$157.61

$11.02

$-$20 $40 $60 $80

$100 $120 $140 $160 $180

Billed Charge Medicare

CBC Test

Source: Time, March 4, 2013

Diminishing Discount Value

Confidential © Copyright 2012 Holmes Murphy & Associates 40

100 100 100 100 100 100 100 100 100 100 100 100

104 114 125 139 157 167 178 181 185 193 207 218

0

50

100

150

200

250

300

350

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Reta

il Pr

ice

Year

Hospital Retail Price Vs Actual Cost

Markup

Cost

Source: MedPAC analysis of American Hospital Association Annual Survey of Hospitals

Budget Projection Sources of Health Insurance

Confidential © Copyright 2012 Holmes Murphy & Associates 41

American Insurance Enrollment (millions) 2013 2023 # Change % Change

Medicaid and CHIP 36 48 12 33.3%

Employer 154 160 6 3.9%

Nongroup and Other 24 24 0 0.0%

Exchanges 0 25 25 N/A

Uninsured 58 30 -28 -48.3%

Total 272 287 15 5.5%

Source: Congressional Budget Office, Feb 2013

Penalty vs Subsidy Imbalance

Confidential © Copyright 2012 Holmes Murphy & Associates 42

$5,510 $5,500 $5,570 $5,840

$6,330 $6,580

$6,950 $7,390

$7,850 $8,290

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Per Enrollee Exchange Subsidies

Large employer $2000 penalty

The Big Shift

Confidential © Copyright 2012 Holmes Murphy & Associates 43

Piling On the Employer-Based Private Healthcare System

Finding the Missing Link

Confidential © Copyright 2012 Holmes Murphy & Associates 44

89.4%

162.7%

213.3% 228.5%

127.8%

187.3%

308.2%

329.4%

274.2%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

350.0%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Paym

ent t

o Co

st R

atio

Year

Aggregate Hospital Payment-to-cost Ratios Trended for Inflation and Capped at Medicare + 20% in 2016

Medicare Private Payer

Healthcare 2020

Confidential © Copyright 2012 Holmes Murphy & Associates 45

Confidential © Copyright 2012 Holmes Murphy & Associates 46

What do you call it when someone keeps you in confinement for days or weeks?

Confidential © Copyright 2012 Holmes Murphy & Associates 47

What do you call it when someone takes a knife and slices you through the abdomen?

Confidential © Copyright 2012 Holmes Murphy & Associates 48

What do you call someone who takes thousands of dollars from your bank account?

Confidential © Copyright 2012 Holmes Murphy & Associates 49

What do you call someone who causes you to take pills every day for the rest of your life?

Confidential © Copyright 2012 Holmes Murphy & Associates 50

What do you call someone who kills people without regard to age, gender, race, or economic status?

Confidential © Copyright 2012 Holmes Murphy & Associates 51

Who is this kidnapping, torturing, thieving, drug dealing mass murderer?

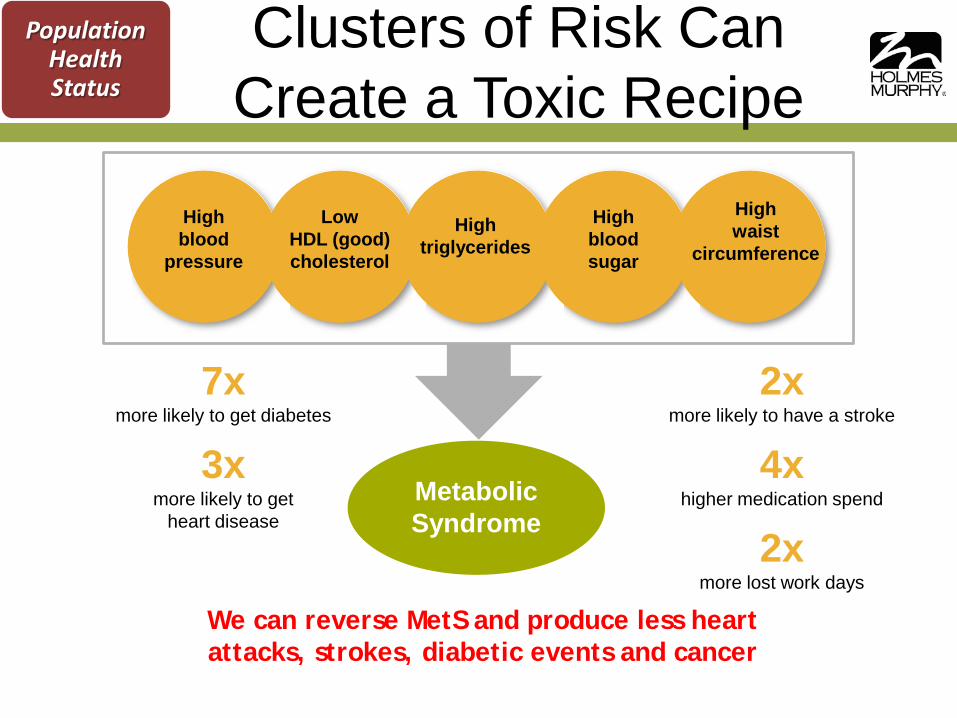

Metabolic Syndrome

Clusters of Risk Can Create a Toxic Recipe

7x more likely to get diabetes

3x more likely to get

heart disease

High blood

pressure

Low HDL (good) cholesterol

High triglycerides

High blood sugar

High waist

circumference

2x more likely to have a stroke

4x higher medication spend

2x more lost work days

We can reverse MetS and produce less heart attacks, strokes, diabetic events and cancer

Population Health Status

Summary of Screenings Fall Screenings 2008 to 2012

Year Total

Screened % Mets Employees Screened % MetS

Spouses Screened % MetS

2008

2,701 26%

2,701 26%

2009

4,078 27%

2,834 21%

1,244 34%

2010

4,329 22%

3,000 19%

1,329 29%

2011

3,997 20%

2,737 19%

1,260 26%

2012

3,562 16%

2,449 15%

1,113 18%

Sustainable MetS Reversal Leadership Pilot From 2007 to 2012

100%

56.8%55.0%54.8%48.1%48.1%

37%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% of Population with MetS

Pre

Post

Follow Up 12MonthFollow Up 24MonthFollow Up 36MonthFollow Up 48MonthFollow Up 60Month

27

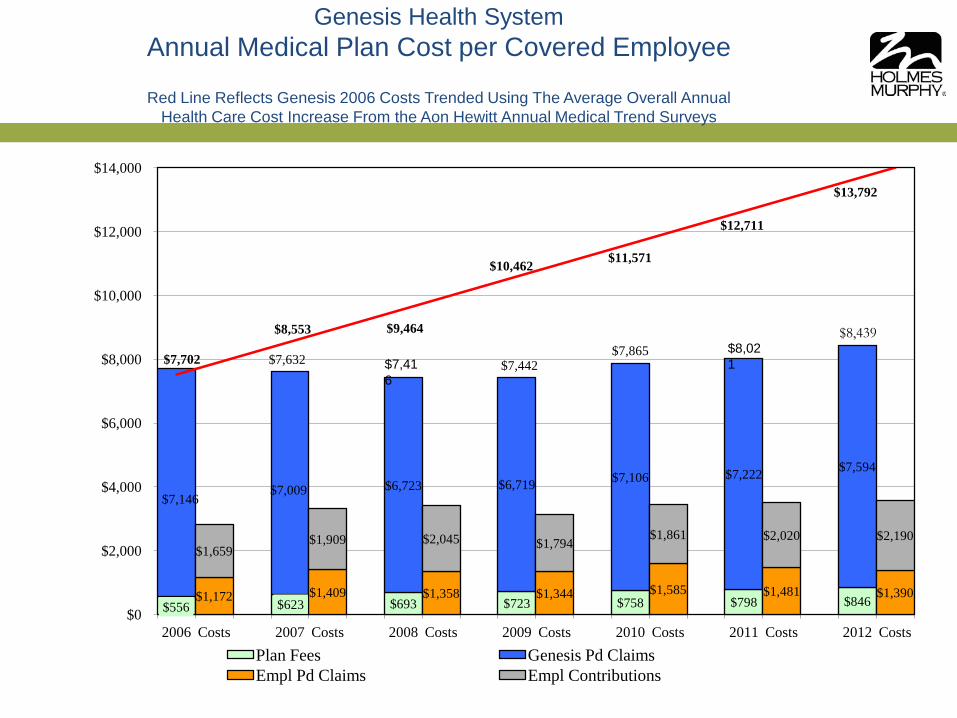

Genesis Health System Annual Medical Plan Cost per Covered Employee

Red Line Reflects Genesis 2006 Costs Trended Using The Average Overall Annual

Health Care Cost Increase From the Aon Hewitt Annual Medical Trend Surveys

$556 $623 $693 $723 $758 $798 $846

$7,146 $7,009 $6,723 $6,719 $7,106 $7,222 $7,594

$1,172 $1,409 $1,358 $1,344 $1,585 $1,481 $1,390

$1,659

$7,632

$1,909 $2,045

$7,442

$1,794

$7,865

$1,861 $2,020 $2,190

$7,702

$8,553 $9,464

$10,462 $11,571

$12,711

$13,792

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2006 Costs 2007 Costs 2008 Costs 2009 Costs 2010 Costs 2011 Costs 2012 Costs Plan Fees Genesis Pd Claims Empl Pd Claims Empl Contributions

$8,439

$8,021 $7,41

6

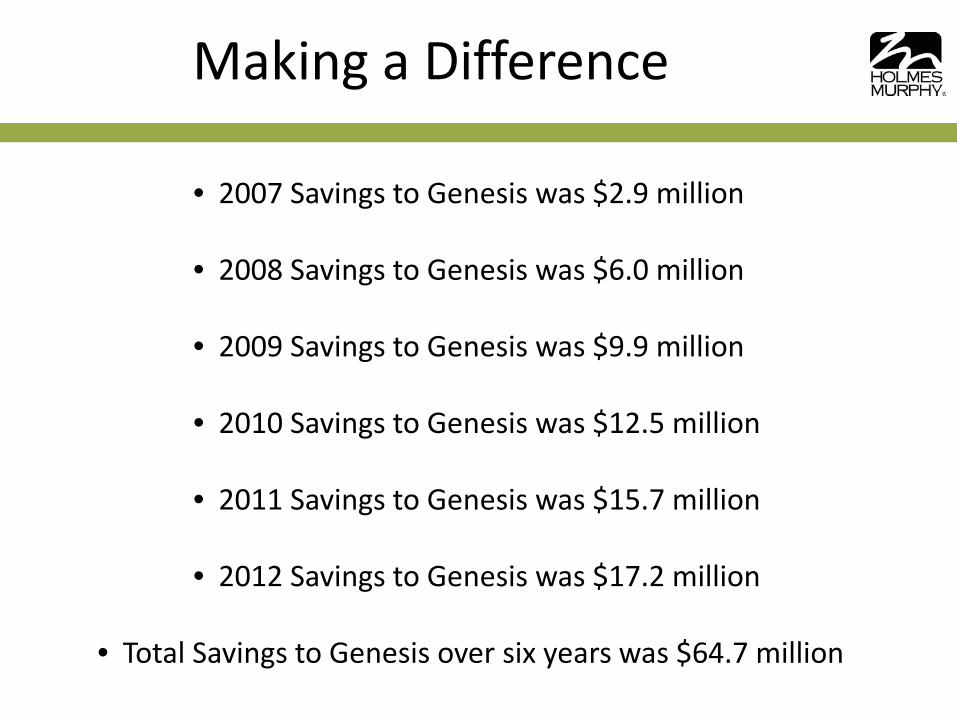

• 2007 Savings to Genesis was $2.9 million

• 2008 Savings to Genesis was $6.0 million

• 2009 Savings to Genesis was $9.9 million

• 2010 Savings to Genesis was $12.5 million • 2011 Savings to Genesis was $15.7 million • 2012 Savings to Genesis was $17.2 million

• Total Savings to Genesis over six years was $64.7 million

Making a Difference