Health Investment Portfolioapi.ning.com/.../HealthInvestmentPortfolio.pdf · 2016-10-21 ·...

12

Health Investment Portfolio © July 2014 A Common Sense Guide to Health & Wealth © By Dr. Nancy Gahles, DC, CCH As a Health Investment Portfolio Advisor with over 30 years experience, I welcome the opportunity to consult with you, to empower you, and to inspire you to a Healthy and Wealthy Life! Dr. Nancy Gahles is an internationally recognized expert in the field of integrative healthcare. Dr. Gahles is a Doctor of Chiropractic, a Certified Classical Homeopath and an Ordained Interfaith Minister in family practice since 1979. Dr. Gahles is an advocate for choice and access to integrative healthcare providers, their services and products. She is an ardent advocate for personal empowerment for consumers through presentations, her TEDXTalk(www.tedx.talks.com), http://www.youtube.com/watch?v=l6bZBwl636s as a freelance journalist and via her book, The Power of $elfCare:A Common Sense Guide to YOUR Wellness Solution.(Amazon.com), http://amzn.to/16G1hAB Dr. Gahles is the creator and author of Health Investment Portfolios, a health investment and health management enterprise. She is President Emerita of the National Center for Homeopathy; member of the Board of Directors of the Integrative Healthcare Policy Consortium and CoChair of the Federal Policy Committee; CEO and Founder of Health & Harmony Wellness Education and Tele Health & Harmony; CoChair of the healthcare working group of the American Sustainable Business Council and on the Advisory Board of the

Transcript of Health Investment Portfolioapi.ning.com/.../HealthInvestmentPortfolio.pdf · 2016-10-21 ·...

Health Investment Portfolio © July 2014

A Common Sense Guide to Health & Wealth © By Dr. Nancy Gahles, DC, CCH As a Health Investment Portfolio Advisor with over 30 years experience, I welcome the opportunity to consult with you, to empower you, and to inspire you to a Healthy and Wealthy Life! Dr. Nancy Gahles is an internationally recognized expert in the field of integrative healthcare. Dr. Gahles is a Doctor of Chiropractic, a Certified Classical Homeopath and an Ordained Interfaith Minister in family practice since 1979. Dr. Gahles is an advocate for choice and access to integrative healthcare providers, their services and products. She is an ardent advocate for personal empowerment for consumers through presentations, her TEDXTalk(www.tedx.talks.com), http://www.youtube.com/watch?v=l6bZBwl636s as a free-‐lance journalist and via her book, The Power of $elfCare:A Common Sense Guide to YOUR Wellness Solution.(Amazon.com), http://amzn.to/16G1hAB Dr. Gahles is the creator and author of Health Investment Portfolios, a health investment and health management enterprise. She is President Emerita of the National Center for Homeopathy; member of the Board of Directors of the Integrative Healthcare Policy Consortium and Co-‐Chair of the Federal Policy Committee; CEO and Founder of Health & Harmony Wellness Education and Tele Health & Harmony; Co-‐Chair of the healthcare working group of the American Sustainable Business Council and on the Advisory Board of the

Integrative Healthcare Symposium in addition to several ask-‐the expert panels. Dr. Gahles is a widely published free-‐lance journalist, a member of the Association of Healthcare Journalists, a newspaper columnist and radio host/guest. Dr. Gahles is CEO and Co-‐Founder of the Integrative Telehealth Association. Follow her blogs: www.allabouttelehealth.wordpress.com [email protected]. Follow her on Twitter @askdrnancy. What is a Health Investment Portfolio? A portfolio is a term used in finances to describe a purposeful collection of investments that reflect your lifestyle goals and risk-‐limiting strategy Creating an investment portfolio for your health involves the same principles. There are short-‐term investments and long-‐term investments.

Health is your short-‐term investment. Health is your daily level of energy. Health is the state of absence of disease or symptoms that allows you to live your life unencumbered by physical, psychological or emotional burdens.

Harmony is your long-‐term investment. Harmony is the quality of your life. Harmony is the state of well-‐being that represents your sense of inner peace. Harmony is the state of being which allows the whole organism to work together to access the higher purpose of our existence. The term ROI, return on investment, is used to assess the yield from an investment.

To calculate your ROI from health investments, you need to measure the medical costs that you have saved, the sick time from work that you have saved, the presenteeism in your workplace and family life/relationships that you have eliminated in favor of active, healthy participation and a viable work-‐life balance. You can chart this over a month and then sequentially over a year and review quarterly and on a year-‐to-‐year basis. Example: “Fifteen months after I began study with a study group of the National Center for Homeopathy, I had to collect my medical expense records for income tax purposes. Usually, I get a few hundred dollars over the 7.5% of adjusted gross income to deduct. For this past year, I had a few hundred dollars total, mostly for my daughter’s insect bite and routine checkups. Discontinuing some prescription drugs and enjoying better health through homeopathy meant no tax deduction last year, because my total spent was way too low!” The long-‐term investment in study of self-‐care techniques in this case yielded an ROI in the short term of “better health”. The ROI also yielded a

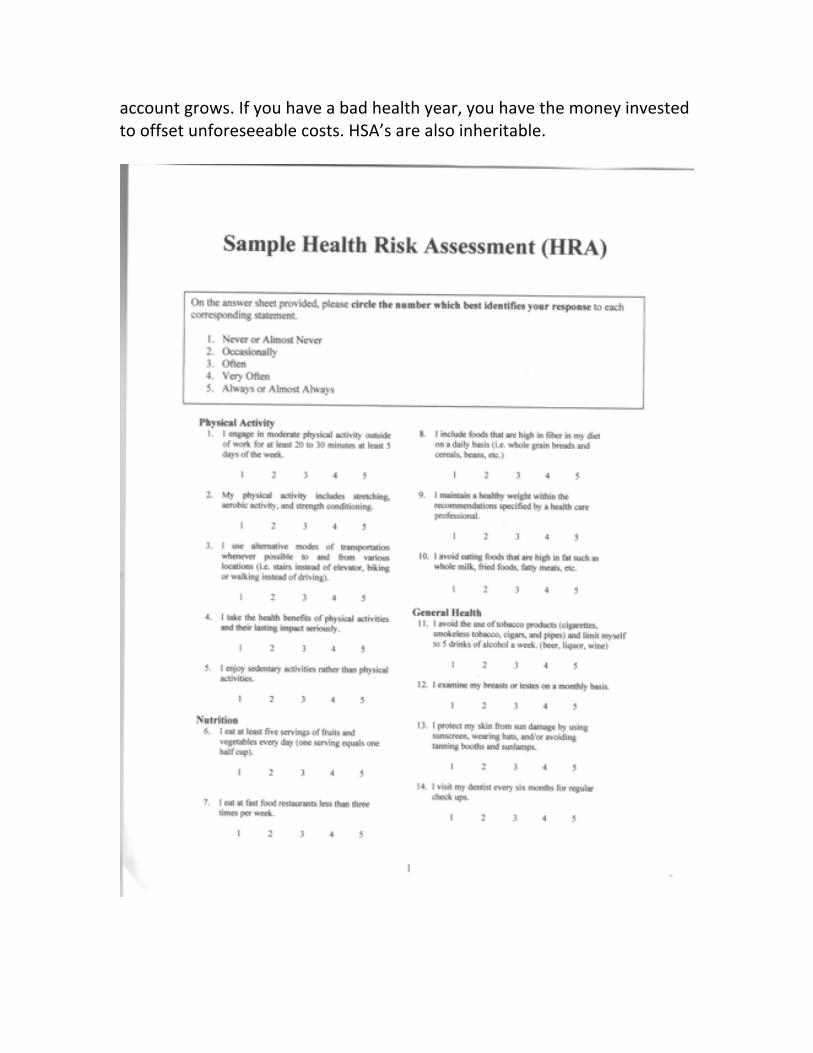

monetary savings in cost of prescription drugs in the short term. Risk Assessment As your health changes with age and circumstances, so will your areas of investment. Effective risk assessment provides a mechanism for identifying your health assets and liabilities so as to determine the best investment products and services for you. Example: ( sample health risk assessment attached) Once you have identified your personal risk factors, you can design your own recession proof strategies as you develop an ideal individualized health investment portfolio, create long term wellness models, maximize dividends in health and harmony. You will enjoy the experience of a personal sense of satisfaction and celebrate the sensation of peace in your life.

Health Investment Portfolio Models You invest in order to reap the benefits of your hard work at the point when you are not able to work as hard. When you are

young, you invest in more aggressive, risky allocations to yield higher dividends.

As you age, you tend to conservative strategies that will preserve your

capital investment and allow you to draw on these resources to use in your daily lives in your later years.

In health terms, we look at the Health Risk Assessment tool to determine our assets and liabilities. Your assets are your strong points in body, mind, emotion and spirit. Here you will use short term, high yield strategies to grow your assets. Investment in areas such as meditation to stay clear and focused; exercise and proper eating to create health and energy; adequate sleep to promote refreshment and restoration of function; nurturing relationships to give meaning to your life; and doing work that stems from a sense of purpose in providing a service to the world. Investment in these asset classes will increase your daily dividends and create long-‐term revenue in terms of health and harmony. Your liabilities are determined by the health condition(s) you currently suffer from such as diabetes, emphysema, heart disease, or obesity. These are categorized as chronic or have the potential to become chronic especially if there is family history/genetic predisposition.

The younger you are, the more time you have to make short-‐term investments that will eliminate these conditions and mitigate the need for, and expense of, long

term chronic disease management. Your portfolio will reflect the investments needed to ensure long term care such as fixed medical costs, durable equipment, doctor office visits, co-‐pays, deductibles and insurance premiums. The key is to diversify your portfolio. Proper asset allocation can prevent huge fluctuations in health returns and put you on the path to long term quality of life and growth.

Each asset has its own cycle. It is important to have different asset classes that are counter cyclical to each other so that your portfolio is balanced and has low volatility. A key concept is to diversify with different asset classes and to rebalance the portfolio in order to capture the opportunities of the time and manage the risks. In the financial investment world, market timing is used to predict the asset class for this cycle. In the healthcare world, you predict asset class by identifying the cycle of life that you are in. Investment Products and Services Nearly 40% of Americans use healthcare approaches developed outside of mainstream Western, or conventional, medicine for specific conditions or overall well-‐being. The National Center for Complementary and Alternative Medicine (NCCAM) describes Complementary Medicine to refer to the use of a non-‐mainstream approach together with conventional medicine. For example, guided imagery and massage, both once considered complementary and alternative (used in place of conventional medicine), are used regularly in some hospital and clinical settings for pain management. Integrative Medicine represents an array of non-‐mainstream healthcare approaches that are used collaboratively. For example, cancer treatment centers with integrative healthcare programs may offer services such as acupuncture, meditation and yoga. Integrative healthcare is no longer a trend. It is happening now. The Patient Protection and Affordable Care Act recognizes this shift towards inclusion by providing for a new national healthcare workforce known as “licensed CAM providers and integrative healthcare practitioners” ( ACA Sec. 5101). The ACA goes further in providing for nondiscrimination against these providers within a healthcare insurance policy in ACA Sec. 2706.

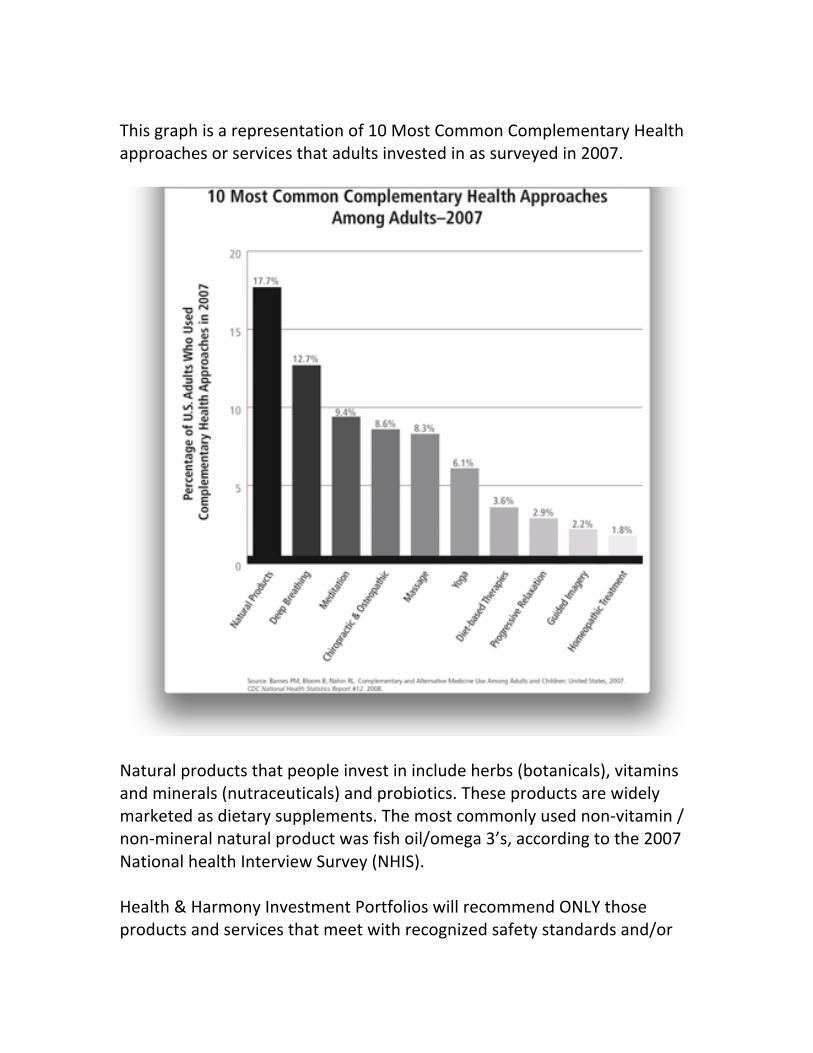

This graph is a representation of 10 Most Common Complementary Health approaches or services that adults invested in as surveyed in 2007.

Natural products that people invest in include herbs (botanicals), vitamins and minerals (nutraceuticals) and probiotics. These products are widely marketed as dietary supplements. The most commonly used non-‐vitamin / non-‐mineral natural product was fish oil/omega 3’s, according to the 2007 National health Interview Survey (NHIS). Health & Harmony Investment Portfolios will recommend ONLY those products and services that meet with recognized safety standards and/or

have evidence-‐based research and efficacy in real world clinical outcomes. Creating Wealth Health IS wealth! Health insurance premiums are skyrocketing despite the provisions in the ACA for subsidy-‐reduced premiums. Because of this, the sticker price appears lower than in previous years, however, the back-‐end costs are drastically increased. High deductible policies offered on the State exchanges range from $2500 -‐ $6,000 in deductible costs that you must reach before your insurance coverage begins. Once your deductible is met, you may be liable for 50% of all costs up to a maximum of $10,000. Health Savings Accounts (HSA) were created to relieve the burden of expensive medical care and to allow people the freedom to choose the practitioner, products and services of their choice that best meet their individual healthcare needs. The cost of healthcare is likewise escalating. Consumers with high deductible policies will be responsible to pay cash for all care up to the amount of their deductible. The onus is on the consumer to negotiate fees for services rendered by physicians so as to be fully informed of expenses and to budget for them. Having developed a Health Investment Portfolio, you will know the predictable costs of your care, the insurance policy that you own and how to maximize investment in your Health Savings Account to provide for your daily, monthly and yearly costs NOT covered by insurance. The tax free, money market investment products Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA) are your way to create a body of dollars to use for both short-‐term medical expenses and for long-‐term care management. You may choose to potentially grow your savings for future health care costs by investing some of your money in mutual funds. Once you reach the designated balance for your HSA, known as the investment threshold, you can invest a portion of your savings. Many people are now using HSA’s for retirement purposes. An additional benefit is that HSA’s roll over year to year. If you have a good health year, your

account grows. If you have a bad health year, you have the money invested to offset unforeseeable costs. HSA’s are also inheritable.

Follow my blogs: www.allabouttelehealth.wordpress.com [email protected] Contact: Dr. Nancy Gahles, DC, CCH, RSHom(NA) 241 Beach 137 St. Belle Harbor, NY 11694 Cell: 718-‐634-‐4577 Email: [email protected] Twitter: @askdrnancy Facebook:http://www.facebook.com/askdrnancy LinkedIn:www.linkedin.com/in/nancygahles Link to my book: The Power of $elf Care, A Common Sense Guide to YOUR Wellness Solution http://amzn.to/16G1hAB Link to my TEDxTalk: http://www.youtube.com/watch?v=l6bZBwl636s