HEALTH & WELFARE PLAN LUNCH GROUP - Alston

69

HEALTH & WELFARE PLAN LUNCH GROUP December 7, 2006 ALSTON & BIRD LLP One Atlantic Center 1201 W. Peachtree Street Atlanta, GA 30309-3424 (404) 881-7885 E-mail: [email protected] © 2006 All Rights Reserved

Transcript of HEALTH & WELFARE PLAN LUNCH GROUP - Alston

HEALTH & WELFARE PLAN LUNCH GROUP

December 7, 2006

ALSTON & BIRD LLP One Atlantic Center 1201 W. Peachtree Street Atlanta, GA 30309-3424 (404) 881-7885 E-mail: [email protected] © 2006 All Rights Reserved

INDEX

Article 1 .....................Red Light/Green Light: IRS Provides Guidance on Use of Electronic Payment Cards With Transit Benefits

Article 2 .....................Health & Welfare Plan 2006 Compliance Chart Article 3 .....................VEBA Compliance and Welfare Plan Nondiscrimination Testing

ADMIN/11057048v2

Red Light/Green Light: IRS Provides Guidance on Use of Electronic Payment Cards With Transit Benefits

By Ashley Gillihan and John Hickman (Alston & Bird, LLP) 1

On November 20, 2006, the Internal Revenue Service issued Revenue Ruling (“Rev. Rul.”) 2006-572, which describes the situations in which an electronic payment card may be used to make tax free payments for eligible transportation expenses under a Code Section 132 transportation fringe benefit program (“Transportation Plan”). This is the first time that the IRS has addressed the use of electronic payment cards for transportation expenses under a Transportation Plan. The Rev. Rul. is not effective until January 1, 2008; however, the Rev. Rul. may be relied on prior to January 1, 2008.

The Rev. Rul. addresses four fact patterns that collectively involve payment of eligible transportation expenses with a “smartcard” (a card with an embedded information “chip”), a terminal-restricted debit card (a card that may only be used at terminals that only sell fare media for a particular transit system(s)), and a merchant category code (“MCC”) restricted debit card (a card that may only be used at merchants with a MCC indicating that they sell fare media). The Rev. Rul. indicates that payments made with a smartcard and/or a terminal-restricted debit card are generally excluded from income and are considered to be “vouchers”. Since these cards are vouchers, they can be used even if other vouchers are readily available without regard to the “significant administrative cost” restriction (described below).

With regard to MCC restricted debit cards the news is not so good. According to IRS, such cards would constitute a cash reimbursement arrangement (and thus could not be used if a voucher is readily available), and that the MCC filter coupled with employee certification does not provide the level of substantiation necessary to make the arrangement a bona fide reimbursement arrangement.

More specifically, with regard to MCC-filtered cards, the Rev. Rul. addresses two different MCC arrangements. In one fact pattern (Situation 3), the MCC-restricted debit card closely resembles the Dependent Care FSA debit card addressed in Notice 2006-69. Claims are initially substantiated, and the card is subsequently “loaded” based on the initially substantiated amount and recurring amounts for the same seller and time period. While transit expenses paid under this program are excluded from income, an MCC-restricted debit card is not a voucher. In the end, TPAs and card vendors may find the MCC-restricted debit card to be an impractical and unattractive program given the

1 John Hickman is a partner with Alston & Bird (an Atlanta, New York, Charlotte, and Washington, DC based law firm) where he has been a member of the Employee Benefits Practice Group since 1989. Mr. Hickman has been a pioneer in the consumer directed health care arena, working closely with health plans, financial institutions, and employers as well as the IRS, Treasury, and DOL in developing guidance for tax-favored health reimbursement arrangements (HRAs) and health savings accounts (HSAs). Ashley Gillihan is also a Partner with Alston & Bird’s Employee Benefits and Executive Compensation Group.

2 http://www.irs.gov/pub/irs-irbs/irb06-47.pdf

- 2 -ADMIN/11057048v2

administrative complexity, especially when compared to smartcards and terminal-restricted debit cards.

In the other MCC restricted debit card program (Situation 4), which is more indicative of many currently operating transit card arrangements, the MCC restricted card is very similar to health debit card MCC-based arrangements because participants use the MCC restricted card to purchase transportation expenses at an eligible merchant without first incurring substantiated but unreimbursed transportation expenses. However, unlike health benefit cards that satisfy the requirements of Rev Rul 2003-43 (i.e., where expenses must be substantiated through auto-adjudication or after the fact substantiation), no after the fact substantiation is required in Situation 4. Although more convenient, IRS had little difficulty in finding that such an arrangement did not qualify as a bona fide reimbursement arrangement for transit expenses. The Rev. Rul does not address whether substantiation after the fact would cure the otherwise impermissible MCC restricted program.

As noted above, an analysis of the validity of an MCC-restricted debit card may be a moot point, at least in certain parts of the country. The Rev. Rul. treats the MCC-restricted debit card as a “cash reimbursement”, which means an MCC-restricted debit card will only be available for transit passes in areas where a voucher for transit passes is not otherwise “readily available” (as defined in the regulations). Under IRS rules issued under Code Section 132(f)(3), there are only a few areas in the country in which a voucher is not “readily available”. But, one notable area where vouchers are not readily available (thus permitting MCC-restricted debit cards) is the New York metropolitan area, which has several million people commuting via mass transit on a daily basis. Nevertheless, the only practical, widespread method of purchasing transit passes with an electronic payment card in light of the Rev. Rul. may be the smartcard and the terminal-restricted card.

Readers of the Rev. Rul. should be careful not to read the guidance too broadly. The three permissible programs addressed in the Rev. Rul. would seem to be the only currently approved methods of using an electronic payment card for transportation expenses. We believe, however, that that a point-of-sale or real-time verification method of adjudicating transportation expenses similar to the IIAS system for health benefit cards might be permitted for MCC-restricted transit cards. In addition, the Rev. Rul. relates only to the use of an electronic payment card to purchase transit passes. The guidance does not specifically indicate that electronic payment cards may be used for parking expenses. Again, a merchant based point of sale adjudication arrangement (similar to an IIAS system) may be possible for parking expenses.

The following is a more detailed summary of the Rev. Rul.

Overview:

- 3 -ADMIN/11057048v2

Rev. Rul. 2006-57 addresses four hypothetical fact patterns, each of which addresses a particular electronic payment card method. Only three of the four fact patterns involve a permissible electronic payment card program. We address each of these fact patterns below.

Permissible Payment Card Programs

Situation #1: Smartcards

In situation #1, payments for transportation expenses with an electronic “smartcard” are excluded from gross income to the extent paid in accordance with the following requirements:

• The employer limits reimbursement to the statutory max for transit passes.• Transit System X provides smart cards to employers as a means for providing fare

media for Transit System X to employees. • The smartcards are plastic cards with a memory chip that stores information

including the serial number of the card and the value of fare media. The smartcard can only be used to purchase fare media from Transit System X.

• Employer makes monthly payments to X with instructions on how to appropriately allocate the amounts to each participant’s card.

• No substantiation is required.

In situation #1, the smartcards prevent use of the card for anything other than a transit pass on Transit System X. Consequently, the smartcard is a voucher and no substantiation is required.

Situation #2: Terminal Restricted Debit Cards

In situation #2, payments for transportation expenses with a terminal-restricted debit card are excluded from gross income to the extent paid in accordance with the following requirements:

• Employer distributes debit cards to participants to pay for transportation expenses.• The cards may only be used at merchant terminals at points of sale at which only

fare media for transit system Y is sold.• Employer makes monthly payments to the debit card provider who then allocates

the amounts to each participant accordingly.• No substantiation is required.

Much like the smart cards in Situation #1, the terminal-restricted cards prevent the use of the card for anything other than a transit pass for the particular transit system. Consequently, terminal-restricted cards are vouchers and no substantiation is required. Although the fact pattern restricts use of the card to a single transit system, the card could presumably be restricted to terminals that only sold fare media for one or more transit systems in an area.

- 4 -ADMIN/11057048v2

Situation #3: MCC restricted debit card that pays in arrears

In situation #3, payments for transportation expenses with an MCC-restricted debit card are excluded from gross income to the extent paid in accordance with the following requirements:

• Employer provides each participant with a debit card to pay for transportation expenses. The participant certifies initially and annually that he or she will only use the card for eligible transportation expenses.

• The debit cards have been restricted to use at merchants assigned an MCC by the card network/association (based on information from the merchant) indicating that the merchant sells fare media for some or all of the following categories:

o Local and suburban commuter passenger transporto Passenger railwayo Bus lines, excluding charters and tours, o Transportation service.

• A voucher or similar item is not readily available for purchase by employer and direct distribution to employees.

• For the first month of participation the participant pays for fare media with after-tax amounts and substantiates the amount to the employer (or its administrator) in accordance with reasonable substantiation procedures set forth in Treas. Reg. 1.132-9, Q-16.

• After determining that the expense was an eligible transportation expense, the employer submits an equal amount to the debit card provider who then allocates that amount to the participant’s card.

• Participants may use the amount allocated to the card equal to the previously substantiated expense to purchase subsequent transit passes or the participant may continue to pay for transit passes with after-tax dollars. If the participant uses the amount allocated to the card to pay for a transportation expense (with the amount from the prior month’s expense), subsequent certification is generally not required for recurring expenses that match previously substantiated expenses as to seller and time period. Moreover, the employer can instruct the card provider to allocate an amount equal to or less than the previously substantiated expense for each subsequent card transaction, to the extent that the employer reviews the participant’s card transactions on periodic statements to ensure that the card transactions continue to match the previously substantiated expenses as to seller and time period.

• If the participant wishes to increase the amount allocated to the card (or change the seller or time period for the expense), he or she will need to pay for the eligible expense with after-tax dollars and substantiate the new expense to the employer (including a new certification). The employer can then reimburse the participant for the new expense by adding that amount to the card for the next month. Under the Rev. Rul. the participant is not reimbursed directly for any of the expenses. All reimbursements are made in the form of allocations to the card.

- 5 -ADMIN/11057048v2

The following examples illustrate how the MCC-restricted debit card operates in Situation 3:

Example 1: Bob is employed by Employer A and participates in Employer A’s transit plan. Bob elects $75 per month for transit passes. Employer gives Bob a debit card. Bob certifies that he will only use it for eligible transportation expenses. In month #1, Bob purchases a transit pass for $75 with after-tax dollars from his checking account. Bob submits the appropriate substantiation to Employer A who determines that the $75 amount paid by the employee was for an eligible transportation expense. Employer A forwards $75 to Debit Card Provider D and instructs Debit Card Provider D to allocate that $75 to Bob’s debit card. In month #2, Bob uses his debit card to purchase another $75 transit pass. Employer A reviews his periodic statement and determines that the card swipe was indeed for an eligible transit expense (e.g., it matches the previously substantiated expense as to seller and time period and is less than or equal to the prior expense). Employer A transfers another $75 to D and instructs D to allocate that $75 to Bob’s card. In month #3, Bob uses the $75 on his card to buy transportation related expenses from another transit agency. Employer sees from the periodic statement that the card transaction was not from the same seller as the previously substantiated expense. Employer does not transfer any money to D to allocate to Bob’s card. If Bob wishes to use the card again for transportation expenses, Bob will have to pay an eligible expense with after–tax dollars and then substantiate the expense to A (including a new certification).

Example 2: Same facts as Example #1, except that in month #3, Bob buys a more expensive transit pass, using the $75 on his card plus paying an additional $25 in after–tax dollars. Bob submits the appropriate substantiation to Employer (including a new certification). Upon a determination that it was an eligible expense, Employer transmits $100 to D to allocate to Bob’s card in each subsequent month. Bob will need to recertify at least annually that the debit card is used only to purchase fare media.

If you are familiar with Notice 2006-69 issued earlier this year, you will find this electronic card payment process very similar to the Dependent Care FSA electronic payment card process. Most importantly, the IRS treats this process as cash reimbursement, which is only available if there is no voucher or similar item “readily available” for purchase by the employer and direct distribution to employees. Under applicable tax regulations, a voucher is readily available for direct distribution by an employer to employees (which means that a reimbursement arrangement is not allowed) if and only if:

• The employer can obtain vouchers from a “voucher provider”; • Without incurring “significant administrative costs”. The regulations indicate that

the employer incurs significant administrative costs (and thus the vouchers are not readily available) if the fare media charges that the employer reasonably expects to incur for transit system vouchers purchased from the voucher provider exceed 1% of the average annual value of the vouchers; and

- 6 -ADMIN/11057048v2

• The voucher provider does not impose non-financial restrictions that effectively prevent the vouchers from being readily available.

A voucher is an instrument that may be purchased by employers by a voucher provider that is accepted by one or more mass transit operators in an area as fare media or in exchange for fare media. Unfortunately, vouchers are “readily available” in most areas, thereby precluding cash reimbursement. This would also seem to preclude use of the MCC-restricted debit card in most areas (other than the New York City area). Arguably, the MCC-restricted debit card is accepted by the transit system in exchange for fare media (i.e. the transit pass), which would allow use of the card even in areas where cash reimbursement is not otherwise permitted; however, the IRS concludes that it nevertheless is not a “voucher or similar item” since it can be used to purchase items other than transit passes.

Impermissible Payment Card Programs

Situation #4: MCC restricted debit card that does not pay in arrears

The Rev. Rul. indicates that payments made under the following program would not be excluded from gross income under Code Section 132:

• Same facts in Situation #3 (discussed above) except for the following differences:

o Participants are able to use the card during the first month on the first expense, and

o The participants certify that they will not use the card for ineligible expenses as in Situation 3; however, the participants do not substantiate any of the fare media expenses that have been incurred in Situation #4.

The IRS concludes that the arrangement does not constitute a “bona fide reimbursement arrangement” as otherwise required for cash reimbursement arrangements under Section 132 because the program provides for impermissible “advances” rather than reimbursements and because “it relies solely on employee certifications provided before the expense is incurred.” Consequently, the payments are taxable. This begs the question—would the conclusion be different if the employer in Situation #4 required substantiation, albeit after the fact? It is hard to ignore the following two factors:

• Transportation plans generally have less rigid substantiation requirements than health flexible spending accounts (a reimbursement arrangement); however, health flexible spending accounts that utilize an MCC-restricted debit card may allow payment with an electronic payment card provided that appropriate substantiation is provided after the fact. If substantiation is not provided or the substantiation indicates it was not an eligible transaction, the card is turned off. It is difficult to argue that such a system should not also be sufficient for Transportation Plans.

- 7 -ADMIN/11057048v2

• The Treasury regulations appear to specifically contemplate after the fact substantiation. In Treas. Reg. 1.132-9, Q-16(c), an expense under a bona fide reimbursement arrangement must be substantiated within a reasonable period of time. An expense that is substantiated to the payor (presumably the employer) within 180 days after it has been paid is deemed to be a reasonable period of time. This provision from the regulations seems to support after the fact substantiation.

Unfortunately, even if after the fact substantiation was adequate, the IRS conclusion that an MCC-restricted transit card is not a “voucher or similar item” since it can be used to purchase items other than transit passes would make such an arrangement useful only in areas where a voucher was not readily available (such as New York City and the surrounding metropolitan area).

What Now ?

Many plan sponsors already allow participants to use electronic payment cards to pay for transportation expenses. Plan sponsors will need to assess the current electronic payment card systems with their administrators and card issuers to determine what changes are required to comply with the Rev. Rul. As noted above, the rules are effective January 1, 2008, but employers and employees may rely on the Rev. Rul. prior to January 1, 2008. The guidance does not affirmatively provide that plan sponsors may continue to use existing electronic payment card programs until January 1, 2008. Nonetheless, IRS’ conclusion with regard to the voucher issue casts serious doubt on some current transit card arrangements, and employers, TPAs and card vendors may need to seek counsel regarding whether to make compliance changes to their systems prior to 2008.

The IRS also notes that it continues to review whether a terminal-restricted card (identified in Situation 2) is a voucher that is “readily available” such that cash reimbursement would be prohibited outside of the card arrangement in areas where the terminal-restricted card is used. In this regard, the IRS notes that they are considering circumstances in which a terminal-restricted card is not “readily available” because of implementation charges and other restrictions that effectively prevent the employer from distributing the card to employees.

ADMIN/20052107v1

Health & Welfare Plan 2006 Compliance ChartBy John R Hickman, Esq., Ashley Gillihan, Esq.,

and Johann Lee, Esq. (Alston & Bird, LLP)

Once again, 2006 proved to be an incredibly fast-paced compliance year for health and welfare benefit plan administrators and plan sponsors. The legal and regulatory year started early with the GoZone Technical Correction to the dependent definition for dependent care assistance plans and health savings accounts. [Those who followed the WFTRA rule and applied those statutory changes had to address how best to undo those changes.] This was followed by final USERRA regulations (addressing benefit obligations during military leave), HHS HIPAA enforcement guidance, proposed dependent care tax credit regulations (affecting eligible dependent care FSA expenses), and final HSA comparability regulations. The pace then accelerated with additional IRS guidance addressing electronic payment cards for health and dependent care FSA and transit benefits and DOL shedding further light on HSAs and ERISAand the application of prohibited transaction rules under the Internal Revenue Code to HSAs in FAB 2006-2. As 2006 comes to a close, we are anxiously awaiting final HIPAA regulations addressing bona fide wellness programs and the long-awaited integrated cafeteria plan regulation package. To assist you in handling these compliance issues, we provide our annual compliance chart and 2007 COLA adjustment Table to assist you in plan administration. As always, if you have questions about your obligations under these new rules and regulations, contact your legal counsel.

The following cost of living adjustments apply for 2007.

Item 2006 Amount 2007 AmountSocial Security Wage Base (for 6.2% OASDI) $94,200 $97,500Medicare Premiums (monthly)• Part A (for individuals with less than 30 quarter

hours)$393 $410

• Part B (**May go up to $161.40, depending on modified AGI and filing status)

$88.50 $93.50**

Medicare Deductible• Part A $952 $992• Part B $124 $131Definition of Highly Compensated Employee under Code Section 414(q) (for purposes of Code Section 125 and 129 non-discrimination testing)

$100,000 $100,000

Compensation limits for officers under Code Section 416(i)-key employees (for purposes of Code Section 79 and Code Section 125 non-discrimination testing and for VEBA purposes)

$140,000 $145,000

Adoption Credit. This credit starts to phase out at modified adjusted gross income (AGI) levels of:and is completely phased out when modified AGI reaches:The exclusion from income provided through an employer or a Section 125 Cafeteria Plan also has a

$10,960

$164,410204,410

$11,390

$170,820$210,820

- 2 -ADMIN/20052107v1

$11,390 limit for the 2007 taxable year. And remember – a participant may take the exclusion from income and the tax credit if enough expenses were incurred to support both platforms.

Health Savings Account (HSA). Minimum deductible amounts for the qualifying high-deductible health insurance remained unchanged from 2004. The single- coverage deductible must be at least:and the family-coverage deductible must be at least : Maximums for out-of-pocket expenses for single coverage:and family coverage rose to:

Maximum contribution levels to an HSA for single coverage is:With family coverage at:Catch-up contribution for those 55 and over is:

$1,050

$2,100

$5,250$10,500

$2,700$5,450$700

$1,100

$2,200

$5,500$11,000

$2,850$5,650$800

Archer Medical Savings Account (MSA). For a high-deductible insurance plan that provides single coverage, the deductible amount must be: Total out- of-pocket expenses under a plan that provides single coverage cannot exceed:The deductible amount for family coverage must be:

and out-of-pocket expenses must not exceed: Maximum contributions to an MSA that is attributable to a single-coverage plan is 65% of the deductible amount. Maximum contributions for a family-coverage plan is 75% of the deductible amount.

Between$1,800 and $2,700

$3,650Between

$3,650 and $5,450$6,650

Between$1,900 and $2,850

$3,750Between

$3,750 and $5,650$6,900

Dependent and/or Child Daycare Expenses. The cafeteria plan daycare contribution limit is $5,000 for a married couple filing a joint return, or for a single parent filing as “Head of Household.” For a married couple filing separate returns, the limit is $2,500 each.The limits for the daycare expenses credit went up in 2003. Generally, for expenses covering one child, the limit is $3,000, with the limit for two or more children is set at $6,000. If one of the parents is going to school full time or is incapable of self-care, the non-working spouse would be “deemed” as earning $250 per month for one qualifying child and $500 for two or more qualifying children. This “deemed” earned income is to be used whether a person is using the employer’s cafeteria plan or taking the daycare credit.

- 3 -ADMIN/20052107v1

Medical Mileage. The mileage allowance for medical care has been increased for 2007.

$0.18 $0.20

Long-Term Care. For a qualified long-term care insurance policy, the maximum non-taxable per-diem.

$250 $260

Transportation Benefits. The monthly limit for parking.Transit and vanpooling limits.

$205$105

$215$110

401(k) Plans.The maximum for elective deferrals.

And for those 50 or older, the catch-up contribution limit is:

$15,000

$5,000

$15,500

$5,000

ADMIN/20052107v1

2006 Year-End ReviewHealth & Welfare Benefits

“Dependent” Definition

Summary In 2004, Congress enacted the Working Families Tax Relief Act of 2004 (“WFTRA”), which provides a uniform definition of “child” for several tax purposes. WFTRA caused some disparity between the broader health plan definition of eligible dependent (which did not impose an income limitation for health coverage for qualifying relatives) and the post-WFTRA definition used for purposes of HSAs and dependent care FSAs. This oversight was retroactively corrected by the Gulf Opportunity Zone Act of 2005 (GoZone Act), to conform this aspect of the definition of eligible dependent for purposes of health coverage (including health FSAs), dependent care FSAs, and HSAs. [Keep in mind, however, for dependent care purposes an individual must still satisfy the other requirements to be a qualifying individual under Code Section 21 (e.g. a “dependent” age 13 or older must be disabled and live with the employee for more than half the year)].

Action Item Review plan documents, communication materials and administrative practices to ensure that they reflect the current statutory definition of dependent. If changes were made to accommodate the WFTRA restriction for dependent care, revise plans for broader GoZone definition.

HIPAA Administrative Simplification (privacy, security, EDI) Enforcement

Summary HHS issued regulations, setting forth the manner in which the statutory penalty for violations of HIPAA’s privacy, security and electronic data interchange rules is determined and enforced. The penalty for such violations is up to $100 each day for each violation, but limited to $25,000 for violation of a single HIPAA requirement. The rule clarifies that plans are generally responsible for the violations of their “agents” committed in the scope of their agency. However, covered entities are not responsible for the acts of business associates to the extent that i) the plan did not or should not have known about (e.g. unexpected acts by business associates/vendors) and ii) the plan has entered into a business associate agreement with the business associate. This could help insulate the plan and plan sponsor from breaches by business associates where the plan hadno reason to know of the violation.

Action Item Plan sponsors should carefully review their internal HIPAA procedures andbusiness associate agreements to ensure that their group health plan is in compliance. Where knowledge of a violation by a business associate exists, corrective action should be taken.

- 5 -ADMIN/20052107v1

HSA Comparability Rules

Summary In late July, the IRS issued final regulations that clarify the non-discrimination requirements for employer contributions to HSAs (the “Comparability Rule”). Importantly, the final regulations provide that HSA contributions made “though a cafeteria plan” will not be subject to the Comparability Rule. A series of examples in the final regulations confirms that an employer’s contributions to the HSA of an employee who has the option of making additional pre-tax salary reduction contributions to his or her HSA is a contribution “made through a cafeteria plan,” regardless of whether the employee actually opts to make additional pre-tax HSA contributions, and regardless of whether the employer’s HSA contributions could be received as cash.

Action Item Review HSA programs to ensure compliance with the final Comparability Rule and/or to take advantage of the broad cafeteria plan exception to the Comparability Rule.

HSAs and ERISA Issues

Summary DOL Field Assistance Bulletin 2006-02 provides important clarification on when HSAs are subject to ERISA, and how the prohibited transaction restrictions included in the Code and ERISA apply. This guidance addresses:

• How the HSA ERISA safe harbor applies when an employer selects an HSA vendor, contributes to the HSA, and even pays the HSA vendor’s fees.

• The impact of “mirroring” 401(k) investment options.• The application of the plan asset rules to HSA contributions (whether

subject to ERISA or not).• The impact of an employer’s receipt of discounts and incentives on non-

HSA products.• Whether an HSA vendor can extend a line of credit to HSA account

holders.

Action Item(s) Review HSA arrangement and communication documents in light of FAB 2006-02, and take any necessary steps to ensure that it will not be deemed an ERISA plan. Review HSA vendor arrangements to ensure compliance with prohibited transaction requirements.

- 6 -ADMIN/20052107v1

Health Benefit Card Guidance

Summary IRS Notice 2006-69 provides clarification and additional guidance on the substantiation requirements that must be satisfied for a health benefit card to access funds in an FSA or an HRA. The guidance also addressed how an electronic card could be used to access funds in a dependent care FSA. Specifically, the Notice:

• Expanded the co-pay match category to allow certain multiples of co-pays at merchants that have a health related merchant category code (MCC)

• Permits merchant based adjudication (via inventory information approval system or “IIAS”) for all merchants (including those without a health care MCC)

• Allows electronic card substantiation for certain dependent care FSA expenses under a recurring expense type approach

• Clarified EOB rollover adjudication methodology• Strictly prohibits use of self-certification for substantiation of expenses

The Notice also confirms that, with the exception of a compliant IIAS arrangement, health benefit cards cannot be used at merchants that do not have a health care merchant category code (e.g., most discount stores and grocery storeswould not qualify).

Action Items • Discuss current card configuration with advisors, TPAs and cardvendors, specifically focusing on health MCC limitation

• Clearly communicate to participants the substantiation requirements and current limitations (particularly regarding the inability to use health benefit cards in discount stores or grocery stores)

• Stay tuned for possible additional year-end guidance from IRS and IIAS compliant announcements from vendors in 2007

Transit Card Guidance

Summary The IRS issued Rev Rul 2006-57, which describes the situations in which an electronic payment card may be used to make tax free payments for eligible transportation expenses under a Code Section 132 transportation fringe benefit program (“Transportation Plan”). The Rev. Rul. is not effective until January 1, 2008; however, the Rev. Rul. may be relied on prior to January 1, 2008.

The Rev. Rul. addresses four fact patterns that collectively involve payment ofeligible transportation expenses with a “smartcard” (a card with an embeddedinformation “chip”), a terminal-restricted debit card (a card that may only be used at terminals that only sell fare media for a particular transit system(s)), and a merchant category code (“MCC”) restricted debit card (a card that may only be used at merchants with a MCC indicating that they sell fare media).

The Rev. Rul. indicates that payments made with a smartcard and/or a terminal-restricted debit card are generally excluded from income and are considered to

- 7 -ADMIN/20052107v1

be “vouchers”. Since these cards are vouchers, they can be used even if other vouchers are readily available without regard to the “significant administrative cost” restriction.

With regard to MCC restricted debit cards the news is not so good. According toIRS, such cards would constitute a cash reimbursement arrangement (and thus could not be used if a voucher is readily available), and the MCC filter coupled with employee certification does not provide the level of substantiation necessary to make the arrangement a bona fide reimbursement arrangement.

Action Items • Discuss current card configuration with advisors, TPAs and card vendors specifically focusing on MCC limitation

• Make adjustments, as needed, to bring arrangement into compliance with the Rev. Rul.

USERRA and FMLA

Summary Department of Labor’s final regulations (effective January 18, 2006) clarified existing USERRA rules, including guidance on:

• The types of health plans covered (includes Health FSAs)• How employees may select and pay for continued coverage• The permissible cost of continued coverage• Health plan administrator’s obligations• The duration of continued health coverage (NOTE: The Veterans

Benefits Improvements Act of 2005 extended the duration of continued health coverage to 24 months and these regulations confirm and implement that extension)

In addition, the DOL issued 2006-03 which clarified that employer cashable credits that are applied to health contributions must be continued during the FMLA leave in the same manner as any other employer contribution.

Action Items • Determine which employees are subject to USERRA protection• Review the health and welfare benefit rights of qualifying employees• Review plan documents and operation to ensure compliance• Coordinate coverage continuation requirements with COBRA

requirements• Ensure that cashable flex credits are continued as required by FMLA for

employees on FMLA leave

- 8 -ADMIN/20052107v1

Coordination with Tricare

Summary Effective January 1, 2008, group health plan sponsors cannot offer incentives to Tricare-eligible participants and beneficiaries to not enroll in (or disenroll from) the group health plan. In addition, group health plan sponsors must not impose on Tricare-eligible participants or dependents any condition or requirements that do not apply to similarly situated non-Tricare-eligible employees and beneficiaries. For covered individuals, the group health plan must be primary to Tricare. Up to $5,000 in penalties for each violation.

Action Item Review plan documents and administrative practices for provisions affecting Tricare eligible employees and dependents. Look for further DoD guidance in Spring 2007 addressing interaction between Tricare rules and cafeteria plans. Ensure compliance with the new requirements not later than January 1, 2008.

Dependent Care

Summary The IRS proposed dependent care tax credit regulations that impact what expenses may be eligible employment related expenses for dependent care FSA plans in a number of ways. Highlights relevant to dependent care FSA plans include clarifications on kindergarten expenses (not eligible); specialty day camp expenses (generally eligible, even if educational in nature if necessary to enable the employee and spouse to work); transportation expenses charged by dependent care provider for transit to and from the day care center (generally eligible); registration/application fees (may be eligible once care with provider commences) and certain expenses incurred while sick or on leave (may be eligible).

Action Item Review current plan documents and communication materials to determine whether changes are necessary and communicate any changes to participants.

- 9 -ADMIN/20052107v1

Leave-Sharing Programs

Summary In IRS Notice 2006-59, the IRS extended favorable tax treatment to “bona fide leave-sharing plans” that provide leave sharing for certain declared disasters, as long as such a plan is in writing and satisfies eight enumerated requirements. Employers, however, must treat payments made to leave recipient as “wages” for purposes or FICA, FUTA and tax withholding. A leave donor may not claim an expense, charitable contribution, or loss deduction on account of the deposit of the leave or its use by a leave recipient.

Action Item Prevent adverse tax consequences to employees by ensuring that vacation time or paid time off (PTO) sharing arrangements satisfy the bona fide leave-sharing plan requirements. Leave-sharing is also permitted for certain medical emergencies, pursuant to Rev. Rul. 90-29.

Subrogation

Summary The Supreme Court’s decision in Sereboff v. Mid Atlantic Medical Services, Inc.clarified the right of an ERISA plan to recover benefit payments by pursuing certain funds received from a third party. By affirming an ERISA plan’s right to seek recovery from specifically identifiable funds in the plan beneficiary’s possession, this decision provided much needed guidance to lower courts and to ERISA plans with regard to pursuing recovery actions.

Action Item Subrogation and right of recovery provisions of ERISA plan documents should be reviewed and modified (as needed) in light of the Sereboff decision in order to maximize the ability to obtain reimbursement from participants and beneficiaries who receive third party payments.

Medicare Part B Premium

Summary Beginning 2007, the Medicare Part B premium amount depends on the individuals’ modified adjusted gross income and income tax filing status. The income threshold will be adjusted for inflation. Increases will be phased in over a three-year period so that only one-third of the increase will take effect in 2007.

Action Item Plans that pay all or part of an individual’s Medicare Part B premium should be reviewed to adjust as necessary for the new premium pricing structure. A simple promise to pay Part B premiums may result in an unexpected cost increase.

- 10 -ADMIN/20052107v1

Medicare Part D Requirements

Summary Medicare Part D prescription drug creditable coverage notices and retiree subsidy applications required each year.

Action Item Both active and retiree health plans are required to determine if plan provides “creditable prescription drug coverage”, which is prescription drug coverage that is equal to, on average, Medicare prescription drug coverage. Notices of such determination are required to be provided to all Part D eligible individuals upon entry into the Plan and all those covered under the plan on or before eachNovember 15th. Also, the plan must electronically file with CMS as well. .If coverage passes a two-part actuarial equivalence test, employer may apply for annual 28% tax free subsidy on certain retiree prescription drug costs for those not covered by Part D. An annual application for the subsidy is required.

Electronic Notice and Elections

Summary The IRS issued final regulations, effective January 1, 2007, regarding the permitted use of electronic notices, consents and elections under employee benefit plans and programs (including HSAs, cafeteria plan, medical plan, etc.). The regulations do not apply to areas subject to authority of other agencies such as theDepartment of Labor (e.g., COBRA, SPD, etc.).

• Consumer Consent Method. Under this permitted method, recipients must affirmatively consent to electronic delivery of notice, and must be provided with a "clear and conspicuous statement" of various rights (e.g., to receive paper notice, withdraw consent), scope of consent, procedures for updating electronic contact information, and hardware/software requirements for access and retention.

• Alternative Method. An alternative method is available if the recipient has "effective ability" to access the electronic medium used to provide the noticeand if, at the time of the notice, the recipient is told that a paper copy is available without charge.

• Elections. Individuals must have an "effective ability" to securely access the electronic medium, have an opportunity to review, confirm, modify, or rescindtheir election and receive election confirmation.

Action Item Review any current or proposed use of electronic notice and elections, and configure future application to comply with the final regulations.

- 11 -ADMIN/20052107v1

409A Requirements

Summary Deferred compensation regulations under Code Section 409A. IRS Notice 2006-100 allows relief for reporting and withholding requirements for 2005 and 2006.

Action Item Review all welfare plan arrangements to determine whether impacted by 409A. Particular attention should be paid to health coverage that is extended to individuals on a discriminatory basis (with regard to cost or eligibility), severance arrangements, and vacation/PTO banks. Individual separation arrangements should be reviewed as well.

HIPAA Portability Requirements

Summary Final HIPAA portability requirements effective January 1, 2006 for calendar year plans. New rules regarding:§ Pre-existing condition exclusion notice required with enrollment material

(where plan has pre-existing condition exclusion/limitation)§ Revised certificate of creditable coverage§ Clarification regarding definition of “loss” of coverage for special

enrollment purposes and coverage options available upon special enrollment.

Action Item Evaluate health plans under HIPAA guidance. Determine whether “hidden pre-existing condition limitations exist; update certificates of creditable coverage; evaluate lifetime maximums and special enrollment procedures.

VEBA Compliance and Welfare Plan

Nondiscrimination Testing

VEBA Compliance and Welfare Plan

Nondiscrimination Testing

Health and Welfare Lunch GroupNovember & December 2006

VEBASVEBAS

• Voluntary Employees’ Beneficiary Association• Tax exempt organization

– But see UBIT below

• Qualified under IRC §501(c)(9)– Tax filing required

• Nondiscrimination Requirements Apply• Limitations on Deductions

– Qualified Direct Cost plus– Qualified Asset Account (QAA)

VEBA/Plan CorrelationVEBA/Plan Correlation

• No direct correlation between number of VEBAs and plans:– Plan can be funded by multiple VEBAs– VEBA can fund multiple plans

Permissible Benefits

• Can accumulate tax free funds for:– Life, Sickness, Accident– Supplemental unemployment benefits– Severance pay– Education or training programs

Eligible Member/ParticipantsEligible Member/Participants

• Must be eligible for coverage under plan• At least 90% must be employees related by

employment-related common bond– Current employees– Former employees (LOA or retirees)– Surviving spouse and dependents

• Other 10% may be– Sole proprietor, independent contractors, non-employee

directors, etc.

Who May Receive BenefitsWho May Receive Benefits

• Members or eligible dependents– spouse– minors and students of member or spouse – tax dependents

• Rulings allow for deminimis amount to others– 2-3% threshold– domestic partner benefits

Impact of VEBA on BenefitsImpact of VEBA on Benefits

• VEBA-funded benefits generally treated as employer-paid:– Accident/health benefits:

• Section 106 exclusion for coverage• Section 105(b) exclusion for benefits

– Life benefits• Section 79 exclusion for some of coverage• Section 101 exclusion for insured proceeds

Permissible Benefits

• Can accumulate tax free funds for:– Life

• Life may be provided directly or through insurance• Whole life owned by VEBA may be feasible

– Sickness or accident coverage (other than w/comp)• Insurance or direct expense reimbursement• Could include Medicare premiums

– Supplemental unemployment benefits– Severance pay– Education or training programs

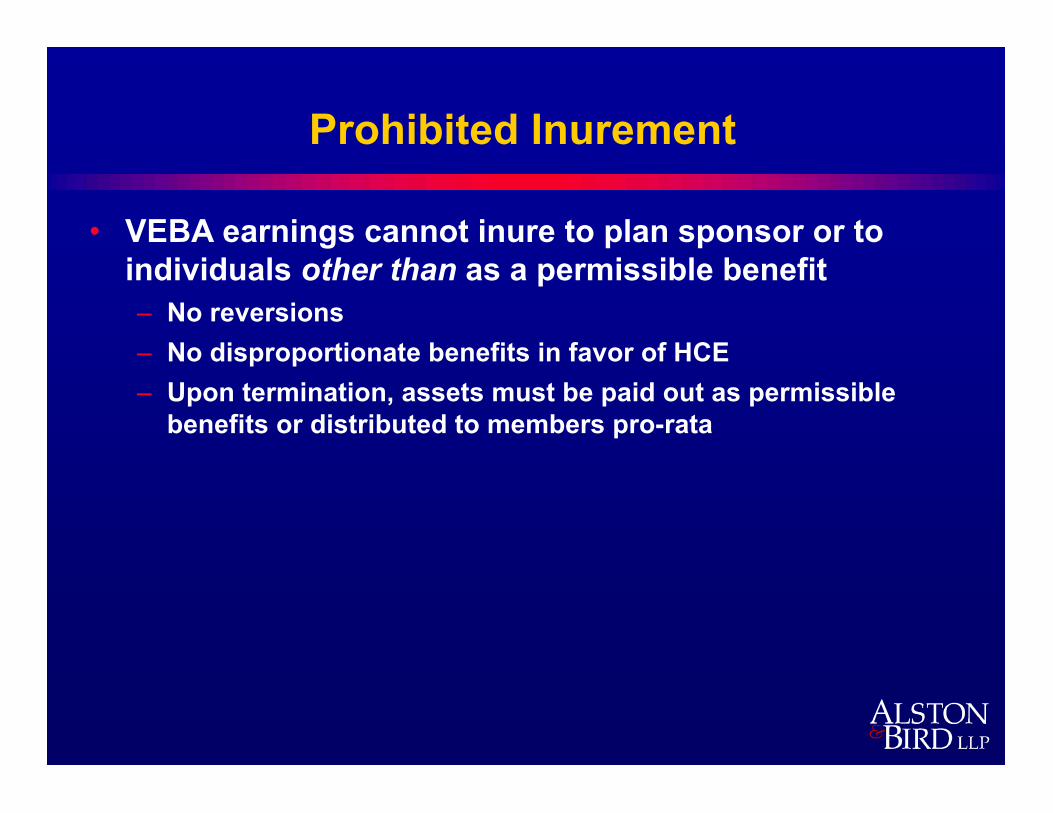

Prohibited InurementProhibited Inurement

• VEBA earnings cannot inure to plan sponsor or to individuals other than as a permissible benefit– No reversions– No disproportionate benefits in favor of HCE– Upon termination, assets must be paid out as permissible

benefits or distributed to members pro-rata

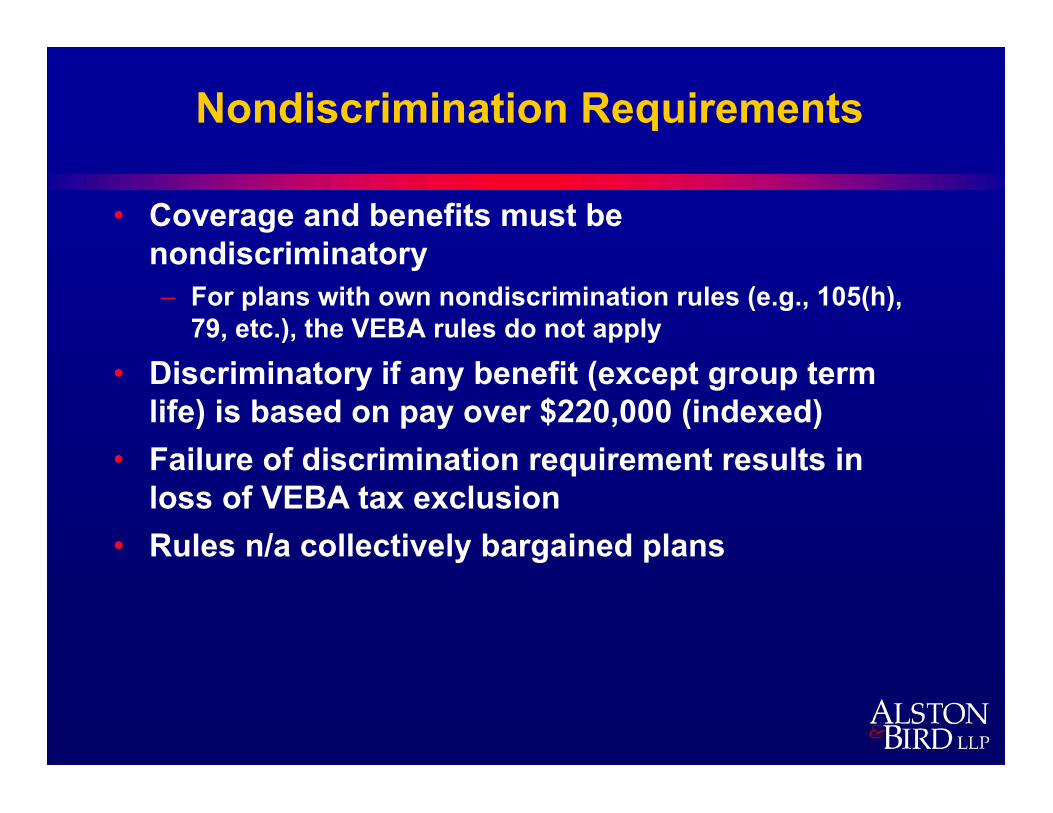

Nondiscrimination Requirements

• Coverage and benefits must be nondiscriminatory– For plans with own nondiscrimination rules (e.g., 105(h),

79, etc.), the VEBA rules do not apply

• Discriminatory if any benefit (except group term life) is based on pay over $220,000 (indexed)

• Failure of discrimination requirement results in loss of VEBA tax exclusion

• Rules n/a collectively bargained plans

Nondiscrimination RequirementsNondiscrimination Requirements

• Under VEBA test, HCE is defined as in 414(q):– More than 5% owner (with attribution)– Employee paid more than $100,000 in prior year

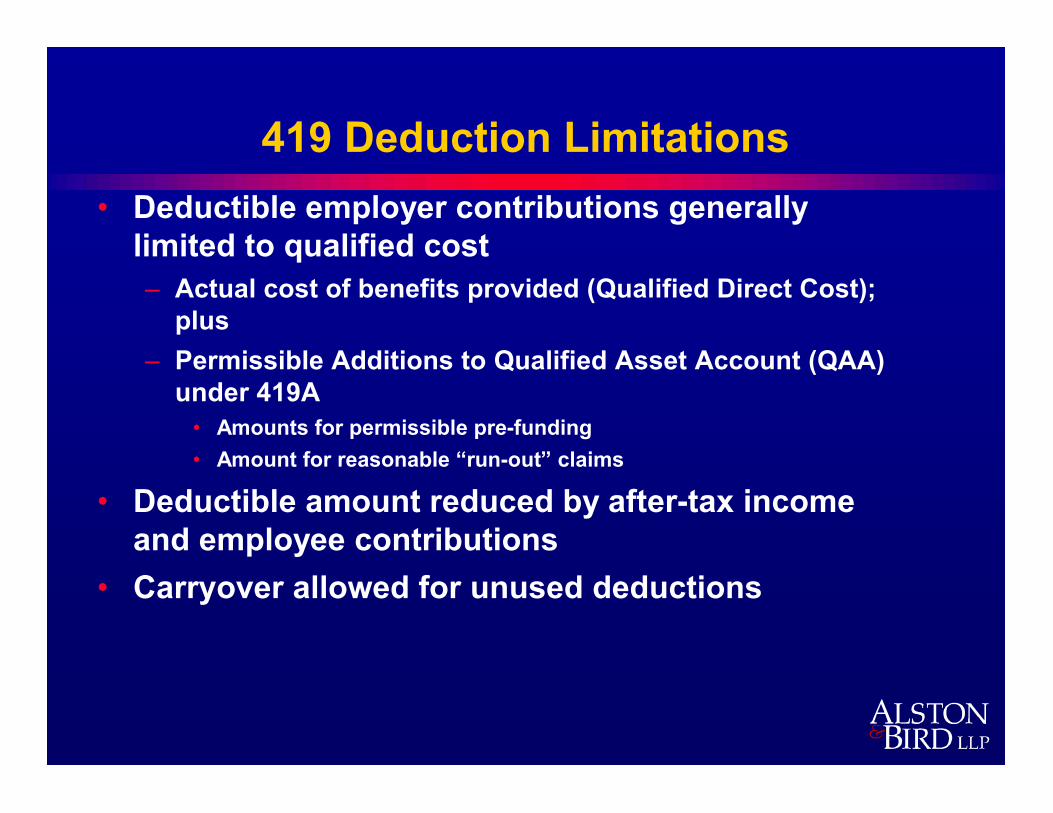

419 Deduction Limitations419 Deduction Limitations• Deductible employer contributions generally

limited to qualified cost– Actual cost of benefits provided (Qualified Direct Cost);

plus – Permissible Additions to Qualified Asset Account (QAA)

under 419A • Amounts for permissible pre-funding• Amount for reasonable “run-out” claims

• Deductible amount reduced by after-tax income and employee contributions

• Carryover allowed for unused deductions

419A Deductions For Reserves419A Deductions For Reserves

• Additional deduction allowed for additions to Qualified Asset Account (QAA) consisting of:– IBNR expense (i.e., “runout” claims)– Reserves for:

• post-retirement medical (funded over working lives and determined on basis of current medical costs)

• post-retirement life (not to exceed $50,000 in coverage)• severance benefits (75% of average of any 2 of last 7 years)• disability benefits

• Separate account required for key employees

Unrelated Business Income TaxUnrelated Business Income Tax

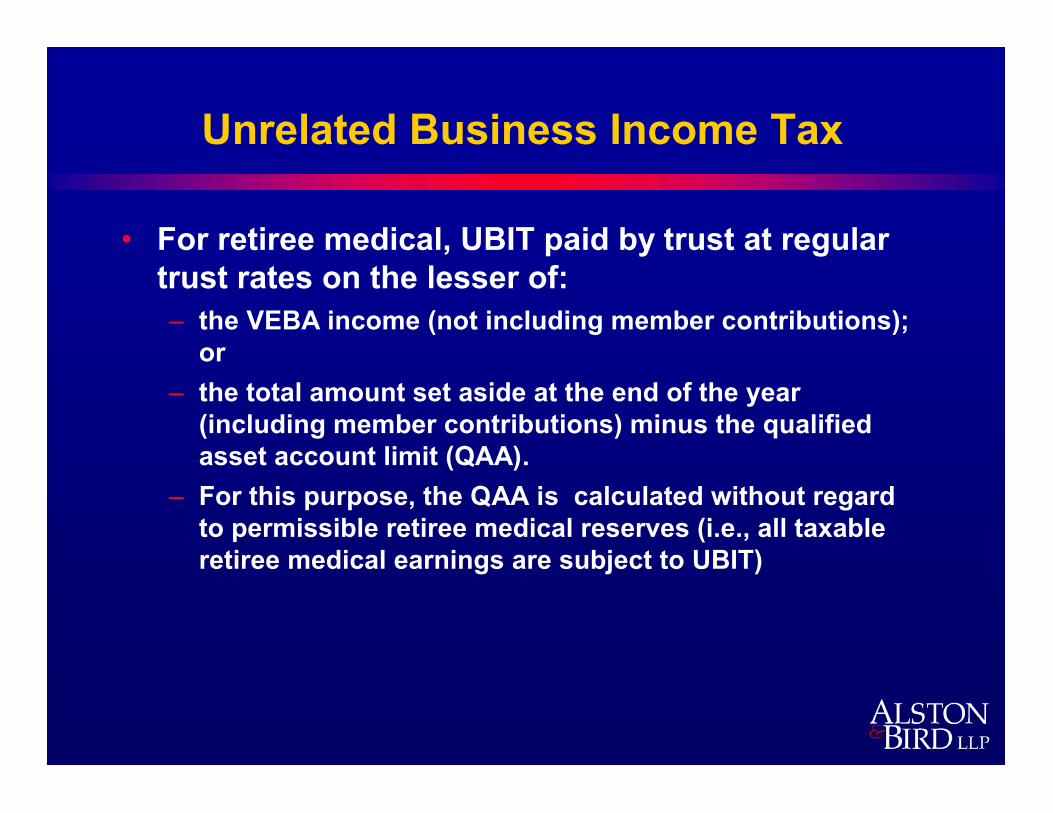

• For retiree medical, UBIT paid by trust at regular trust rates on the lesser of:– the VEBA income (not including member contributions);

or– the total amount set aside at the end of the year

(including member contributions) minus the qualified asset account limit (QAA).

– For this purpose, the QAA is calculated without regard to permissible retiree medical reserves (i.e., all taxable retiree medical earnings are subject to UBIT)

Unrelated Business Income Tax Unrelated Business Income Tax

• Exemptions from UBIT– Collectively bargained plans– Tax-exempt investments– Employee-pay-all plans

VEBA Excise TaxVEBA Excise Tax

• One-hundred percent excise tax if employer provides disqualified benefits:– Retiree medical or life benefits paid to key employee unless

from separate account– Retiree medical or life benefits from discriminatory plan– Reversions to employer

Overview of Nondiscrimination TestingOverview of Nondiscrimination Testing

• Generally-The IRC prohibits certain welfare benefit plans from discriminating in favor of – Highly compensated employees (HCEs) and/or– Key Employees

• Welfare Benefit Plans that require nondiscrimination testing– Group Term Life Insurance Plans—Code Section 79– Self-Insured Medical Reimbursement Plans (Health FSAs, HRAs,

Major Medical Plans)—Code Section 105– Cafeteria Plans-Code Section 125– Educational Assistance Plans—Code Section 127– Dependent Care Assistance Plans—Code Section 129

• VEBAs are also prohibited from discriminating in favor of HCEs-Code Section 505

Group Term Life InsuranceGroup Term Life Insurance

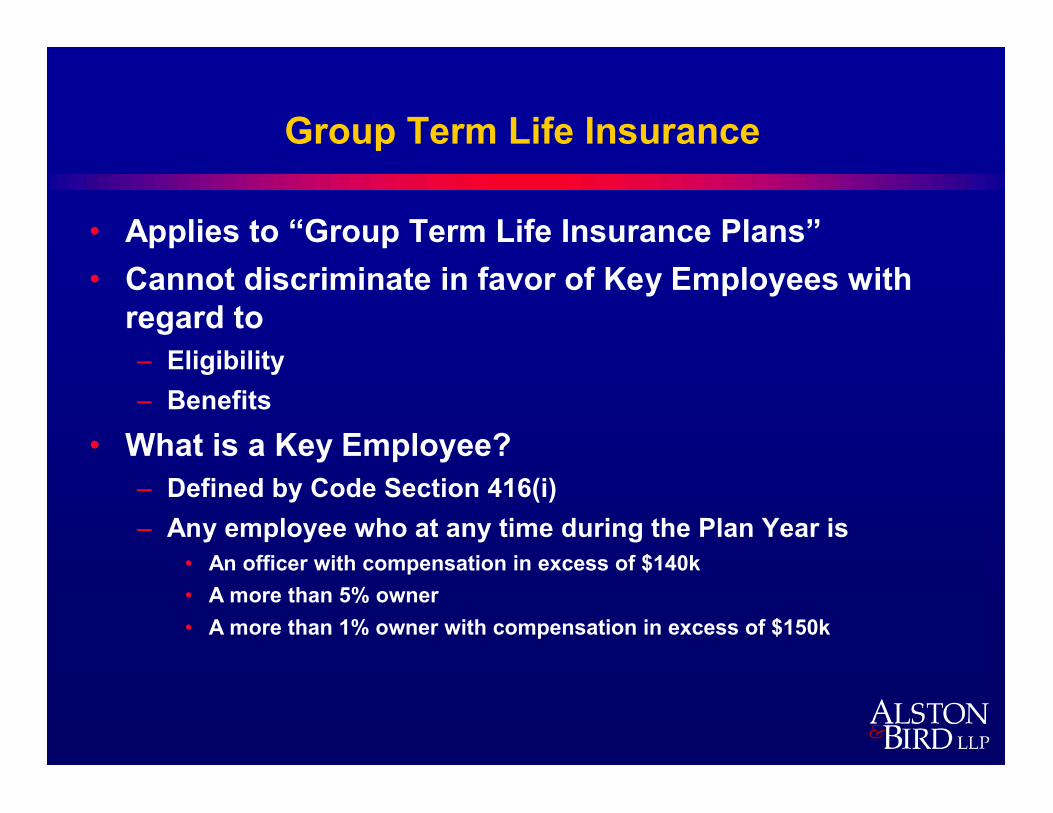

• Applies to “Group Term Life Insurance Plans”• Cannot discriminate in favor of Key Employees with

regard to – Eligibility– Benefits

• What is a Key Employee?– Defined by Code Section 416(i)– Any employee who at any time during the Plan Year is

• An officer with compensation in excess of $140k• A more than 5% owner• A more than 1% owner with compensation in excess of $150k

Group Term Life InsuranceGroup Term Life Insurance

• Eligibility Test Passes if– 70% of all employees are covered Or– 85% or more of all participants are not Key Employees Or– the Plan benefits a classification of employees found by IRS not to

be discriminatory Or– The Cafeteria Plans nondiscrimination tests are satisfied (if the plan

is offered under a cafeteria plan)• “Employee” means

– Employees and former employees– all employees (and former employees) of employers in the controlled group

• Employees and former employees are tested separately• Permissible Exclusions

– Employees with less than 3 years of service– Part-time/seasonal employees– Certain union employees – Non-resident aliens with no U.S. source income

Group Term Life InsuranceGroup Term Life Insurance

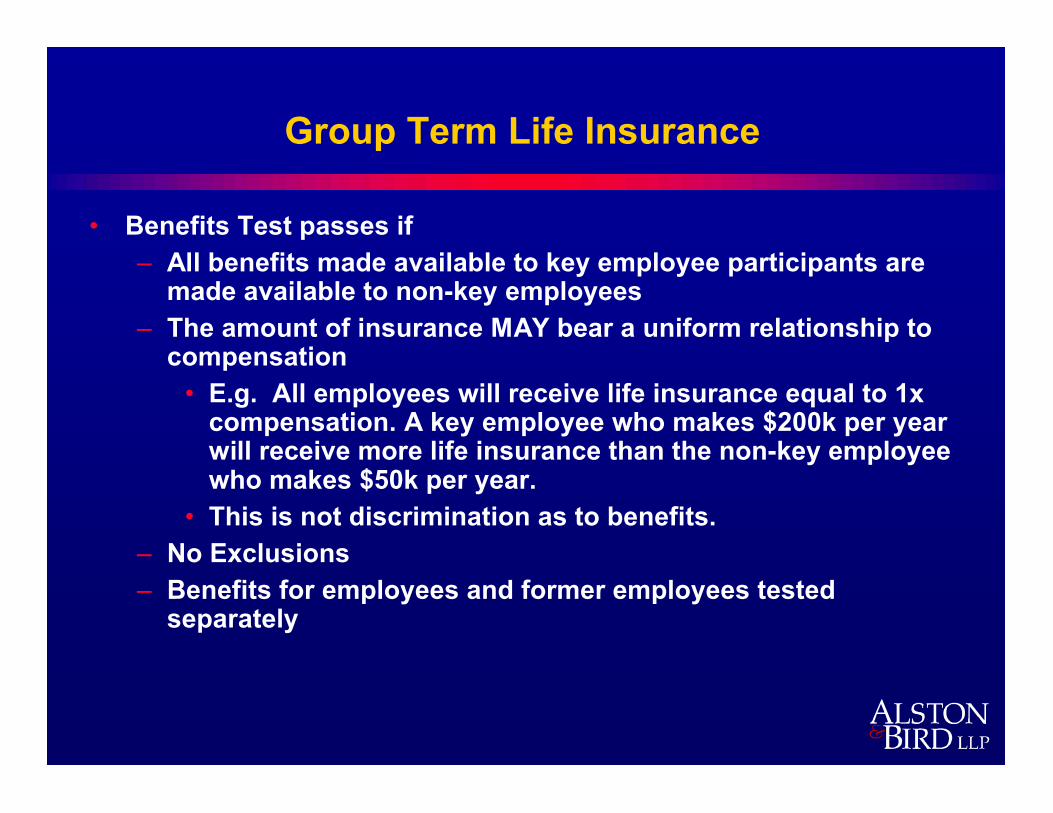

• Benefits Test passes if– All benefits made available to key employee participants are

made available to non-key employees– The amount of insurance MAY bear a uniform relationship to

compensation• E.g. All employees will receive life insurance equal to 1x

compensation. A key employee who makes $200k per year will receive more life insurance than the non-key employee who makes $50k per year.

• This is not discrimination as to benefits. – No Exclusions– Benefits for employees and former employees tested

separately

Group Term Life InsuranceGroup Term Life Insurance

• What are the consequences of failing the Section 79 Nondiscrimination tests:– Key employee must include “cost” of insurance in income– Formula to determine “cost” provided in regulations

Self-insured Medical Reimbursement PlansSelf-insured Medical Reimbursement Plans

• Health FSAs, HRAs, Major Medical/Dental/Vision Plans not provided pursuant to an insurance contract– What is an “insured” plan?

• Third party is paid an amount to be financially responsible for all claims payable under an insurance policy

• Minimum Premium Payment Arrangements/Cost Plus?• Plans may not discriminate in favor of HCEs as to eligibility and

benefits• What is an HCE for purposes of Code Section 105 testing?

– One of the 5 highest paid officers– A shareholder who owns more than 10% of the company– Among the highest paid 25% of all employees

• Compensation is presumably determined as of the Plan Year being tested– For other HCE determinations, it is a look back year

Self-insured Medical Reimbursement PlansSelf-insured Medical Reimbursement Plans

• Eligibility Test Passes if– 70% of all employees “benefit” under the plan Or– 80% benefit if 70% or more are eligible Or– The nondiscriminatory classification test is passed (410(b)

test) or the fair cross section test• Most employers will use one of these tests

• Permitted Exclusions:– Employees with less than 3 years of service– Employees under age 25– Part-time/seasonal employees

• Although not clear, conservative view is that the above must be actually excluded from participating in the plan as well to be excluded for testing

– Certain union employees

Self-Insured Medical Reimbursement PlansSelf-Insured Medical Reimbursement Plans

• What does “Benefit Mean”? – All “eligible” employees w/o regard to participation (this is the

rule for virtually same “classification” test under Code Section 125 and 129) or

– Just Those Who Have Elected Coverage• The first 2 eligibility sub tests use participation as benchmark

• In an analogous situation (voluntary salary deferrals for 401(k) plans), “benefiting” has been interpreted to mean all employees who are eligible to participate under the plan. Treas. Reg. § 1.410(b)-3(a)(2).

Self-Insured Medical Reimbursement PlansSelf-Insured Medical Reimbursement Plans

• Recurring Issues– Salaried-only plans– Plans that exclude part-time employees– Plans that cover employees in one division but not another– Multiple plans

Self-Insured Medical Reimbursement PlansSelf-Insured Medical Reimbursement Plans

• The Benefits Test is passed if– All benefits provided for participants who are highly

compensated individuals are provided for other individuals. Code § 105(h)(4) AND

– Benefits are not modified by reason of• Age• Service• Compensation

– No Exclusions

Self-Insured Medical Reimbursement PlanSelf-Insured Medical Reimbursement Plan

• Recurring Issues for Benefits Test– Only HCEs elect health FSA coverage– Dental benefits available to a limited group of employees (insured vs.

self-funded).– Different health plans for different groups– Health FSA benefits available to a limited group of employees– Health FSA with no annual limit– Different entry dates for different benefits– Lower health FSA limit for certain employees– Different flex credits

• For different geographic areas• For full-time vs. part-time employees• Based on years of service• Based on compensation

• Is Disaggregation Permitted?

Self-Insured Medical Reimbursement PlansSelf-Insured Medical Reimbursement Plans

• What are the consequences of failing tests?– HCEs must include “excess” reimbursement in

income– Eligibility test

• Excess reimbursement equals benefits received by HCE during the year multiplied by the ratio of benefits provided to all HCEs to benefits provided to all employees

– Benefits Test• Excess reimbursement equals benefits received by HCE that are

not received by non-HCEs

Cafeteria Plans Cafeteria Plans

• Do cafeteria plans tests after you do underlying benefit plan tests• Plans may not discriminate in favor of HCEs as to Eligibility and Benefits• Plans may not discriminate in favor of Key Employees• What is an HCE for purposes of the cafeteria plans tests

• An officer, or• A more-than-5% owner, or• A highly compensated individual based on a facts and

circumstances analysis:• Many plans borrow the dollar threshold from the definition of

HCE under Section 414(q) used for 401(k) plan testing• The borrowed definition includes any person who during the

preceding year was an employee who received compensation in excess of $100,000 (as indexed) or, if elected, top 20% rule.

• A spouse or dependent of any of the above• What is a Key Employee?

• Code Section 416(i) definition-same as GTL

Cafeteria PlansCafeteria Plans

• The Eligibility Test is passed if– The nondiscriminatory classification test is passed

• Is the classification reasonable (e.g., all salaried employees)?• A minimum percentage of non-HCEs must “benefit”

– Although not clear, presumably this is the same 410(b) test applied under 105

– All eligibles or just participants?• In this context, benefit appears to mean “eligible”

– Same service requirement (waiting period) must apply to all participants

• Maximum three years

– Employees must enter the plan by the first day of the plan year after completing the waiting period (if any)

Cafeteria PlansCafeteria Plans

• Permitted Exclusions for Eligibility Test:– Neither Code § 125 Nor the § 125 Regulations Contain Rules

on Permitted Exclusions– Possibly Can Borrow Exclusions From the Code § 410(b)

Pension Rules• Employees younger than 21, if the plan excludes them• Employees with less than one year of service (defined as 1,000 hours of

service or its equivalent during a 12-month period), if the plan excludes them

• Certain non-resident aliens without U.S. source earned income• Certain union employees

Cafeteria PlansCafeteria Plans

• Recurring Issues– Salaried-only plans– Plans that exclude part-time employees– Plans that cover employees in one division but not another– Multiple plans– Plans with different entry dates for different groups of

employees

Cafeteria PlansCafeteria Plans

• The contributions and benefits test is passed if:– qualified benefits and total benefits (or employer

contributions allocable to qualified benefits and employer contributions for total benefits) do not discriminate in favor of highly compensated participants.

• Availability Test• Utilization Test • Nondiscrimination in Actual Operation

Cafeteria PlansCafeteria Plans

• Recurring Issues for Benefits Plan Test– In a salary reduction plan, only HCEs can afford to elect health

coverage– Different health plans for different groups– Health FSA benefits available to a limited group of employees– Dental insurance available to a limited group of employees– Different entry dates for different benefits– Lower health FSA limit for certain employees– Different flex credits

• For different geographic areas• For full-time vs. part-time employees• Based on years of service• Based on compensation

• Is Disaggregation Permitted?

Cafeteria PlansCafeteria Plans

• The Key Employee Concentration Test is passed if:– No more than 25% of the total non-taxable benefits provided under the Plan

may be provided to Key Employee– What is a “non-taxable” benefit?

• Salary reductions• Employer contributions associated with coverage for which employee

must also contribute with pre-tax salary reductions– E.G. employer pays 100% of self-only coverage but employees must

pay the difference between family and self-only if they want family coverage

– Are employer contributions counted for the employee with self-only? Likely not

– What about the employee with family? Yes• Issue: Determining nontaxable benefits after a component plan has failed

its nondiscrimination tests

Cafeteria PlansCafeteria Plans

• What are the consequences of failing the tests?– Pre-tax contributions are included in gross income– Issue: Affect of failure of component benefit plan

tests

Dependent Care Assistance PlansDependent Care Assistance Plans

• Dependent care assistance plans may not discriminate in favor of HCEs as to Eligibility and Benefits

• Average benefits provided to non-HCEs must equal or exceed 55% of the average benefit provided to HCEs

• No more than 25% of the benefits provided under the plan can be provided to more than 5% shareholders

• What is an HCE for purposes of these tests?– More-than-5% owner in current or prior year– > $100,000 (indexed) compensation in prior year (Optional:

members of top 20% paid group if elected for ALL PLANS, including pension plans)

Dependent Care Assistance PlansDependent Care Assistance Plans

• Eligibility Test is passed if:– The nondiscriminatory classification test is passed– This is the same 410(b) type test conducted for self insured

medical and cafeteria plans– Same issues that arise under Cafeteria Plans Eligibility Test

arise here

• Permitted Exclusions– Employees < age 21 (if plan excludes them)– Employees < 1 year of service (if plan excludes them)– Certain union employees

Dependent Care Assistance PlansDependent Care Assistance Plans

– Salaried-only plans– Plans that exclude part-time employees– Plans that cover employees in one division but not another– Multiple plans

Dependent Care Assistance PlansDependent Care Assistance Plans

• The Benefits Test is passed if:– No regulations and no guidance– Presumably this is an “availability” test– IRS guidance is needed

• Recurring Issues– Lower DCAP limit for certain employees– Different flex credits

• For different geographic areas• For full-time vs. part-time employees• Based on years of service• Based on compensation

– Does the 55% Test supersede the general Benefits Test?

Dependent Care Assistance PlansDependent Care Assistance Plans

• The 55% average benefits test– Ensures that HCEs do not participate disproportionately (not more than 45% of the total

average benefits)– Focuses on average (not aggregate) benefits– TESTS ALL DEPENDENT CARE ASSISTANCE PLANS OF THE EMPLOYER AS A SINGLE

PLAN• It is a Utilization Test

– “Benefits provided” means the amount of dependent care reimbursement that the employee actually receives under the DCAP (not just salary reductions)

– Forfeitures under the DCAP aren’t benefits– If testing at the beginning of the year, plan sponsors can presumably assume that the

annual election will equal benefits provided• Who Must Be Included in the Test?

– Approach #1: Count all employees (other than Excludables), even if they aren’t eligible to participate in the DCAP?

– Approach #2: Count only the employees who are eligible to participate in the DCAP? • Can DCAP provide that only eligible if have no children?

– Approach #3: Count only those who actually participate? This is no-n0• Approach #1 appears more technically correct based statutory language and congress’ actions

Dependent Care Assistance PlansDependent Care Assistance Plans

• Who Can Be Excluded (“Excludables”)?– Employees who have not completed one year of service by the end of the

year – Employees who have not reached age 21 by the end of the year– Certain union employees– For benefits provided through pre-tax salary reduction, any employee whose

compensation is less than $25,000• EGTRAA Increases the Chance of Failure

– The increase in the tax credit ($6,000 in 2003) means that NHCEs will probably elect fewer DCAP benefits

– The $25,000 salary reduction exclusion needs to be increased• Many companies fail this test

Dependent Care Assistance PlansDependent Care Assistance Plans

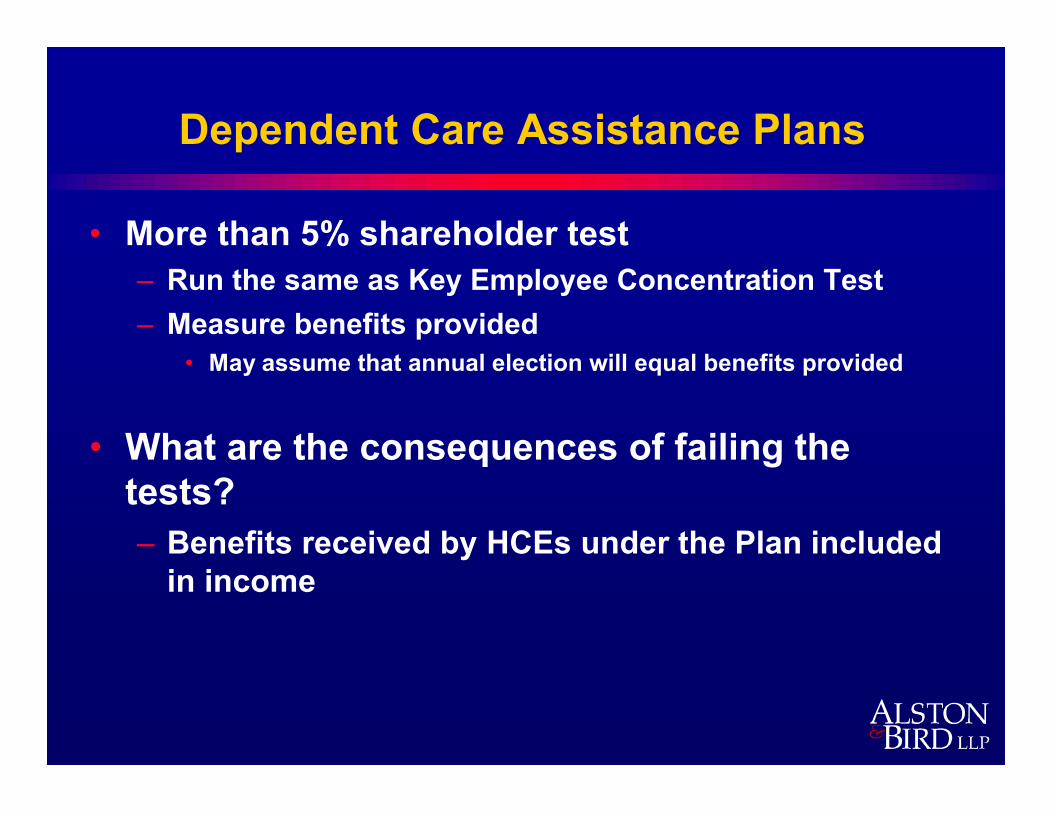

• More than 5% shareholder test– Run the same as Key Employee Concentration Test– Measure benefits provided

• May assume that annual election will equal benefits provided

• What are the consequences of failing the tests?– Benefits received by HCEs under the Plan included

in income

Educational Assistance PlansEducational Assistance Plans

• Cannot discriminate in favor of HCEs as to Eligibility• No more than 5% of educational benefits provided by the

employer during the year may be provided to– More than 5% shareholders– More than 5% owners– Spouses and/or dependents of the foregoing

• What is HCE for purposes of this test?– Same as Dependent Care Assistance Plan (414(q))

• Eligibility Test is passed if:– The nondiscriminatory classification test is passed– Presumably, this is the same 410(b) type test conducted for cafeteria

plans/dependent care assistance plans– Use only those actually eligible

Educational Assistance PlansEducational Assistance Plans

• What is not discrimination?– Utilization is greater among HCEs– Requiring completion of the course, a particular grade as a

condition precedent to receiving benefits or a condition subsequent (such as remaining employed for a period of time after completion)

• Permitted exclusions:– Certain union employees– Other 410(b) exclusions?

• What are the consequences of failing the tests?– Educational benefits provided to HCEs or other prohibited

group (shareholders, owners) are taxable

Common Terms and PrinciplesCommon Terms and Principles

• Compensation– All W-2– All salary reductions made under a 401(k), cafeteria plans and

transit plan (includes cashable flex credits)• Officer

– Someone with authority of officer– Title alone not sufficient

• When should you test– Prior to or shortly after the beginning of the plan year– Presumably, adjustments may be made to elections if done

during the year– No adjustments after the end of the year