HE BOARD S ROLE IN DEFENDING AGAINST 2007 Foley & Lardner LLP THE BOARD’S ROLE IN DEFENDING...

71

©2007 Foley & Lardner LLP THE BOARD’S ROLE IN DEFENDING AGAINST HOSTILE BIDS 1:15 PM Bryan Armstrong, Ashton Partners Justin Friesen, UBS Securities LLC Richard Grubaugh, D. F. King & Co., Inc. Charles J. Hansen, Saks, Inc. Cary Kochman, UBS Securities LLC Steve Vazquez, Foley & Lardner LLP

-

Upload

vuongduong -

Category

Documents

-

view

215 -

download

1

Transcript of HE BOARD S ROLE IN DEFENDING AGAINST 2007 Foley & Lardner LLP THE BOARD’S ROLE IN DEFENDING...

©2007 Foley & Lardner LLP

THE BOARD’S ROLE IN DEFENDING AGAINST HOSTILE BIDS 1:15 PM

Bryan Armstrong, Ashton Partners

Justin Friesen, UBS Securities LLC

Richard Grubaugh, D. F. King & Co., Inc.

Charles J. Hansen, Saks, Inc.

Cary Kochman, UBS Securities LLC

Steve Vazquez, Foley & Lardner LLP

©2007 Foley & Lardner LLP

BRYAN ARMSTRONG PARTNER ASHTON PARTNERS

Bryan Armstrong has been with Ashton Partners, a strategic investor relations and crisis management firm, for over nine years currently serving as one of the firm’s three Partners. In addition to business development, client oversight and execution, Mr. Armstrong leads the Quantitative and Fundamental Research group and is part of the Crisis and Transaction group at Ashton.

Mr. Armstrong regularly provides commentary on topics such as shareholder activism and hedge funds to respected national financial media outlets including the Chicago Tribune, Seattle Times, First Business, Investment Dealers Digest, Financial Week and Investor Relations Business. In addition, Mr. Armstrong has published several articles in national publications and has presented at numerous conferences including the NASDAQ IR Seminar and the NIRI National conference.

Prior to joining Ashton Partners, Mr. Armstrong was an investment analyst at Merrill Lynch conducting security research and analysis, portfolio allocation schemes and retirement planning for high net worth clients and small businesses.

Mr. Armstrong received his BBA in Finance at the University of Wisconsin Madison, with a concentration in International Business. In addition, Mr. Armstrong holds the Chartered Financial Analyst (CFA) designation, is a member of the Investment Analysts Society of Chicago (IASC) and the CFA Institute.

©2007 Foley & Lardner LLP 2

JUSTIN FRIESEN EXECUTIVE DIRECTOR, MERGERS & ACQUISITIONS UBS SECURITIES LLC

Justin Webb Friesen is an Executive Director, Mergers & Acquisitions in the Investment Banking Department of UBS and is based in Chicago. Mr. Friesen has been involved in a wide variety of strategic and capital raising transactions in the diversified industrials, consumer / retail and business services sectors. Mr. Friesen’s transaction experience includes hostile M&A defense, corporate acquisitions, mergers and divestitures along with high-yield, equity and private placement capital raising for Fortune 500 and middle-market companies. His most recent transactions include ADESA’s leveraged buy-out sale to a private equity consortium led by Kelso, Banta’s white knight hostile defense and sale to R.R. Donnelley & Sons, JLG Industries’ sale to Oshkosh Truck, Pentair Inc.’s acquisition of APW Limited’s thermal enclosure assets and The Shaw Group’s acquisition of 20% of Westinghouse Electric.

Prior to joining UBS in May 2004, Mr. Friesen was a Vice President at Credit Suisse First Boston where he participated in significant M&A assignments including: Cooper Industries’ successful defense of Danaher Corporation’s hostile raid; S.C. Johnson’s acquisition of Bayer AG’s global household insecticide business; Pentair’s acquisition of Everpure from Veolia Environnement; sale of Collegis, Inc. to Sungard Data Systems and Whitman Corporation’s asset realignment with PepsiCo and subsequent acquisition of PepsiAmericas. Mr. Friesen began his investment banking career in 1994 as an analyst at Dean Witter Reynolds Inc.

Mr. Friesen received his M.B.A. from The Wharton School at the University of Pennsylvania where he graduated with highest honors and was recognized as a Palmer Scholar. He graduated with distinction from the Indiana University School of Business earning a B.S. in Accounting.

©2007 Foley & Lardner LLP 3

RICHARD GRUBAUGH SENIOR VICE-PRESIDENT D. F. KING & CO., INC.

Richard H. Grubaugh is a Senior Vice President of D.F. King & Co., Inc. and co-manager of the firm’s Extraordinary Events Group. Primarily advises corporations involved in complex shareholder transactions specializing in corporate control situations such as proxy contests, mergers and hostile tender offers. Formulates and recommends shareholder communications strategies for public companies in crisis situations. Prior speaking engagements include programs sponsored by the Practising Law Institute, the American Society of Corporate Secretaries and Governance Professionals and at Georgetown University on corporate governance issues.

©2007 Foley & Lardner LLP 4

CHARLES HANSEN EXECUTIVE VICE-PRESIDENT &

GENERAL COUNSEL SAKS INCORPORATED

Charles J. Hansen is the Executive Vice President and General Counsel of Saks Incorporated. Saks Incorporated, listed on the New York Stock Exchange under the ticker symbol “SKS,” owns and operates 62 Saks Fifth Avenue stores; 54 Saks Off 5th stores; and 24 Club Libby Lu specialty stores. Mr. Hansen is a graduate of the University of Kansas and has a J. D. degree from Boston College, where he was an editor of the Boston College Law Review. He was an associate at Shearman & Sterling, New York, New York, and served as General Counsel for Carson Pirie Scott & Co. prior to its acquisition by Saks Incorporated. He is a member of the bars of the States of Illinois, New York, and Wisconsin.

©2007 Foley & Lardner LLP 5

CARY A. KOCHMAN MANAGING DIRECTOR UBS INVESTMENT BANK

Cary Allan Kochman is a Managing Director, Co-Head of Americas Mergers & Acquisitions, and serves as Co-Head of the Investment Banking Department’s (IBD’s) Chicago office and Midwest Region. He is a member of the Americas IBD Executive Committee. Mr. Kochman is also a member of the Business Review Group.

Mr. Kochman advised on numerous recent transactions including ISCAR’s $5 billion sale to Berkshire Hathaway, ADESA’s pending $3.7 billion LBO transaction, JLG’s $3.1 billion sale to Oshkosh Truck, Zimmer Holdings’ unsolicited, cross-border $3.7 billion takeover of Centerpulse AG, the successful defense of Cooper Industries, Banta Corporation’s White Knight sale to R.R. Donnelley & Sons, the merger of Case Equipment Company with New Holland N.V., Flowserve’s acquisition of IDP, Hussmann’s corporate sale to Ingersoll-Rand, Terex’s cross-border acquisition of Powerscreen Plc, S.C. Johnson’s acquisitions of DowBrands and Drackett, Giddings & Lewis’ cross-border white knight sale to Thyssen AG, Whitman’s realignment with PepsiCo and subsequent acquisition of Pepsi Americas, Goodyear’s acquisition of Debica, the LBO of Jostens by Investcorp, the defense of Clark Equipment, as well as the sale of Specialty Equipment to United Technologies.

Before joining UBS, Mr. Kochman worked at Credit Suisse for 14 years where he was head of the U.S. M&A Department for his last 2 years. He holds both his J.D. and M.B.A. from the University of Chicago. He also has a B.S. in Accounting from the University of Illinois at Chicago. Mr. Kochman is a member of the Illinois Bar and is both a C.P.A. and C.M.A. Mr. Kochman is a Trustee of the Shedd Aquarium. He serves as a member of the Visiting Committee of The Law School of the University of Chicago. He is a member of the Business Advisory Council to the University of Illinois at Chicago College of Business. Mr. Kochman is also a member of The Economic Club of Chicago, The Executive’s Club of Chicago and The Commercial Club of Chicago. He is also a frequent lecturer at Northwestern University’s MergerWeek.

©2007 Foley & Lardner LLP 6

STEVEN W. VAZQUEZ PARTNER FOLEY & LARDNER LLP

Steven Vazquez is a partner with Foley & Lardner LLP, where he is a member of its Transactional & Securities and Private Equity & Venture Capital Practices, as well as its Emerging Technologies, Life Sciences and Nanotechnology Industry Teams. He practices in the areas of securities law and mergers and acquisitions, concentrating on debt and equity securities offerings, public and private mergers and acquisitions, and venture capital financings.

Mr. Vazquez has represented issuers in numerous initial and secondary public offerings and regularly counsels public companies and special committees of public companies.

Mr. Vazquez’s mergers and acquisitions expertise includes public and private company transactions in a variety of industries. He has specific experience in mergers and acquisitions involving health care, real estate, and technology companies.

Mr. Vazquez’s venture capital expertise includes representing emerging growth companies in the technology and telecommunications industries. Since 2000, Mr. Vazquez has represented investors and companies in more than 25 venture capital transactions raising an aggregate of more than $300 million.

Mr. Vazquez graduated, with honors, from the University of Florida College of Law in 1993, where he was elected to Order of the Coif and was an editor of the Florida Law Review and the Florida Tax Review. He received his bachelor's degree in finance from Florida State University in 1990.

Mr. Vazquez is named in The Best Lawyers in America®. In 2005, he was recognized as one of Florida’s Legal Elite™ by Florida Trend magazine.

2007 National Directors Institute

March 2007

Hostile Takeover Discussion Materials

STRICTLY CONFIDENTIAL

1

Table of Contents

SECTION 1 M&A Market Overview 2

SECTION 2 Hostile Activity and Hedge Fund Activism 8

SECTION 3 How to Prepare for a Hostile Bid 16

SECTION 1

M&A Market Overview

3

Rebound inM&A Activity

♦ 2006 volumes up 46% globally, 34% in the Americas♦ Resilient markets♦ Strategic imperatives

Rise of Hostile Activity and Shareholder

Activism

♦ Hostile bids comprise substantial portion of M&A volume♦ Market dynamics have resulted in a new era of aggressive

acquirors/agitators: hedge funds♦ Activists have increasingly attacked larger targets: Time

Warner, Heinz, McDonald’s

HistoricallyStrong Financing

Environment Continues

♦ Corporates across industries face the challenge of effectively deploying robust cash balances

♦ Leveraged loan market continues to be strong

Financial Sponsors Impact

♦ Mega-funds driving sponsors into mainstream of large cap M&A

♦ As a whole, sponsors are still sitting on over $230 billion of uninvested capital

♦ Low interest rate environment has helped make sponsors price-competitive with strategic acquirers

M&A Environment Overview

4

Global M&A Has Surpassed Record Levels

Source: Thomson Financial as of 12/31/06Note:1 All deals with disclosed deal value, excluding minority stake purchases, repurchases, spinoffs or withdrawn deals and deals less than $50 million

US M&A Announced Deal Volumes 1

Global M&A Announced Deal Volumes 1

0

500

1,000

1,500

2,000

2,500

3,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

(US$

bn)

<US$1bn US$1bn - US$10bn >US$10bn

654818

1,228

2,015

2,726 2,676

1,297

9321,052

1,532

2,157

3,152

Down: 65%

Up:238%

1,667 2,074 2,840 3,160 3,406 3,592 2,399 2,225 2,484 2,955 3,571 4,067No. of Transactions

0200400600800

1,0001,2001,4001,600

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

(US$

bn)

<US$1bn US$1bn - US$10bn >US$10bn

Down: 73%

No. of Transactions

341499

711

1,393 1,3131,439

652

388483

683

983

1,226Up:

233%

827 1,096 1,520 1,652 1,573 1,588 960 906 1,041 1,185 1,368 1,576

5

Factors Influencing M&A Activity

Mid 1990s–2000 2001–2002 Today

Economic Environment

Stock Market Performance

Credit Market Strength

Investor Confidence

CEO Confidence

Corporate Scandals/Bankruptcies

Geopolitical Situation

Regulatory Environment

Shareholder Activism

6

Acquiror Target Value ($bn)

Type of Transaction

83.1 Stock

66.7 Raid

55.7 Stock 1

36.0 Raid

34.7 Stock

34.6 Stock

32.5 LBO

Investor Group 32.2 LBO

30.1 Stock

Investor Group 27.4 LBO

Total Top 10 433.0

Industry Consolidation Driving Biggest Deals2006 Top 10 Announced Transactions

Source: Bloomberg

Note:1 Merger occurred following takeover attempt by Enel

7

Leveraged Buyout EBITDA Multiples Have Rebounded to Pre-2000 Levels

Global M&A market continues to be supported by significant LBO activity

Source: Standard & Poor’s PMD (average purchase multiples are for Leveraged Buyouts with total sources of $500mm or greater). LTM figures as of 9/30/06

US Leveraged Buyouts Are Increasing as a Percentage of Overall Activity

♦ Total uninvested capital continues to exceed US$230 billion ♦ Recent industrial LBOs have been completed at historically high leverage levels (6.0x+ common)

Significant Leveraged Buyout Activity

56.7 51.940.5

19.5

47.0

130.3

171.3

22.1

94.4

6%

10%

14%

4% 4% 3% 3%

13%

18%

020406080

100120140

1998 1999 2000 2001 2002 2003 2004 2005 LTM2006

LBO

Vol

ume

(US$

bn)

0%2%4%6%8%10%12%14%16% LB

O V

olume as a %

of Total M

&A Volume

18%160

Significantly higher if financial institutions are

excluded

5.44.7

4.2 4.1 4.04.6 4.9

5.3 5.05.6

33%33%30%

33%35%35%34%

32%28%

37%

0

1

2

3

4

5

6

1998 1999 2000 2001 2002 2003 2004 2005 2006 LTM2006

Tota

l Deb

t / L

TM E

BITD

A (x

)

15%

20%

25%

30%

35%

40%

45% Equity Contribution (%

)

SECTION 2

Hostile Activity and Hedge Fund Activism

9

Historical Unsolicited and Hostile Activity Has Increased There has been a sharp increase in Global Hostile and Unsolicited M&A activity since 2004

Source: Thomson Financial, SDC as of 2/9/2007Note:1 All deals with disclosed deal value, excluding minority stake purchases, repurchases, spin-offs and deals less than $50 million. Includes withdrawn deals

57

47

11%

141

98

15%

82

75

7%

136

78

8%

96

76

4%

699

111

18%

115

83

3%

108

40

6%

43

38

4%

93

46

7%

239

50

12%

199

72

7%Unsolicited / Hostileas % of Total

Unsolicited / Hostile Deals

Hostile Volume ($bn) 402

79

11%

Global M&A Announced Hostile / Unsolicited Activity 1♦ CVRD acquired Inco

for C$22 billion after initialInco / Falconbridge merger was thwarted by separate hostile offers on both original merger partners

♦ Banta’s $1.3 billion White Knight sale to R.R. Donnelley after a successful defense against Cenveo, Inc.

♦ Cemex’s $13 billion hostile raid of Rinker via public Bear Hug

$57

$141

$82

$136 $96

$699

$115 $108

$43

$93

$239 $199

$402

$0

$100

$200

$300

$400

$500

$600

$700

$800

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

10

Target Name Acquiror Name Value of Transaction ($bn)

66.7

36.0

24.1

21.8

18.0

17.9

17.4

13.7

12.7

11.4

Hostile Activity Has Re-Emerged

Top 10 Hostile Deals—2006

The World’s Leading Airport Company

There has been a sharp increase in Global Hostileand Unsolicited M&A activity since 2002

11

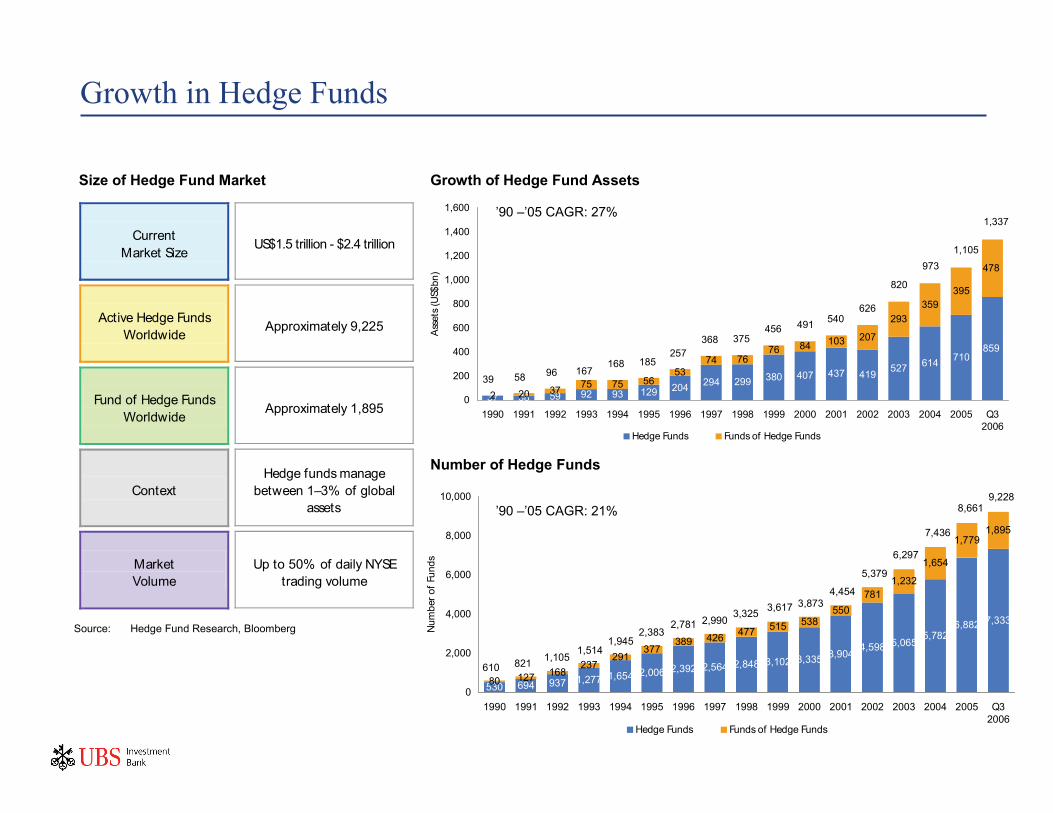

37 38 59 92 93 129 204 294 299 380 407 437 419 527 614 710859

2 20 37 75 75 5653

74 7676 84 103 207

293359

395

478

0

200

400

600

800

1,000

1,200

1,400

1,600

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Q32006

Ass

ets

(US$

bn)

Hedge Funds Funds of Hedge Funds

39 58 96 167168 185

257368 375

456 491 540626

820

9731,105

1,337

530 694 937 1,277 1,654 2,006 2,392 2,564 2,848 3,102 3,335 3,9044,598 5,065

5,7826,882 7,333

80 127 168237

291377

389 426 477 515 538550

7811,232

1,654

1,7791,895

0

2,000

4,000

6,000

8,000

10,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Q32006

Num

ber o

f Fun

ds

Hedge Funds Funds of Hedge Funds

610 821 1,1051,514

1,9452,383

2,781 2,9903,325 3,617 3,873

4,454

5,379

6,297

7,436

8,6619,228

Growth in Hedge Funds

Size of Hedge Fund Market Growth of Hedge Fund Assets

Number of Hedge Funds

Source: Hedge Fund Research, Bloomberg

Current Market Size

US$1.5 trillion - $2.4 trillion

Active Hedge Funds Worldwide

Approximately 9,225

Fund of Hedge Funds Worldwide

Approximately 1,895

Context

Hedge funds manage

between 1–3% of global assets

Market Volume

Up to 50% of daily NYSE

trading volume

’90 –’05 CAGR: 21%

’90 –’05 CAGR: 27%

12

Hedge Funds Are Increasingly Serving As Activist / Hostile Investors

♦ General positive perception of “hostile” deals– Post-scandal era has led to increased corporate activism and the desire to eradicate all corporate

malfeasance, which is thought to be a common goal of hedge funds– Investors have a higher level of support for hedge funds as opposed to their 1980s predecessors– Benefit to shareholders in that pressure is put on boards to explain why their chosen course will create

the most value

Control of Capital

ParallelInvesting

DiminishingTarget Takeover

Defenses

ChangingAttitudes About

Hostile M&AActivity

♦ Hedge funds control vast pools of capital — total AUM of approximately $2.5 trillion– Raider of 1980s had to rely on third party financing, while hedge funds control their own assets– Approximately $120 billion in assets controlled by hedge funds is invested in “event driven” strategies– Limited exposure to fluctuations in credit markets– Enhances credibility in M&A realm

♦ “Wolf pack” tactics– Hedge funds network extensively and take similar positions in other funds’ targets– Success of takeover efforts have worked despite relatively small stakes in targets– Have avoided being treated as a “group” for Regulation 13D purposes

♦ Director’s increased sensitivity to shareholder activism– Corporate governance activists’ voices are increasingly heeded by Directors– Evidence that growing number of governance changes are initiated by hedge funds

2007 and Beyond

♦ Activist investors have performed well over last 12-18 months which should drive continued activist investing– Success of recent proxy fights will drive future activity during upcoming proxy season– Lower profile investors to search for activists to pursue selected situations– Successful acquisition of a company by an activist hedge fund will lead to further convergence of private

equity and public equity worlds

Continued corporate governance activism, increasing social acceptance to hostile activity, rapid accumulation of un-invested capital and the emergence of new low-risk / high-return investment strategies have reshaped the hostile M&A market and led to a wave of aggressive hedge fund activist investing

13

Evolution of the Corporate Raider Events:

Impact:

♦ 1980s:– Unprecedented number of

highly-levered takeovers and restructurings

– Emergence of junk bond market– Peak of the hostile takeover

and materialization of the corporate raider

– Late ‘80s market “bust”

– Creation of poison pill and rise of takeover defense

– Increased shareholder activisim– Council of Institutional

Investors (CII) formed in 1985– Institutional Shareholder

Services (ISS) also formedin 1985

– Anti-poison pill resolutions– Declassification of Boards– Opposition to takeover defenses

– Shareholder proposals on poison pills are regularly approved

– More US companies adhereto investor demands to halt takeover defenses

– Increasing Director vulnerability

♦ 1990s:– End of cash bids and hostile

deals– New era of stock deals, synergy

claims and MOEs– Foundations of new corporate

governance activism movement

♦ 2000s:– Continued corporate governance

activism– New ISS policy concerning

shareholder votes and poison pills– SEC proposed rule to allow

shareholder direct access to proxiesto nominate directors

– Corporate scandals– Hedge funds emerge as new

M&A sharks

Takeover Boom Shifting Balance of Power Rising Shareholder Activism 2006 1980 2000 1990

Raiders Seen As “Enemies” Of Public

Investor

Hedge Funds/Activists Seen As “Friends” Of

Public Investor

14

Hedge Funds are Increasingly Successful in Contested Situations

Other10%

Board Represent

ation56%

Activism Against Merger

3%

Board Control31%

Primary Campaign Types, 2006 Proxy Fights

10156

39

62 67 74

64%

55%46%46%

44% 38%

0

20

40

60

80

100

120

2001 2002 2003 2004 2005 20060%

10%

20%

30%

40%

50%

60%

70%

Proxy Fights Dissident Success Rate

Dissident Success Rate, Proxy Fights

Success breeds success and hedge funds are becoming more aggressive in their M&A investing activities

Source: Shark Repellent

Board Representation

56%

15

Hedge Fund Activists Have Increasingly Been Aggressive

Year Company Market

cap. ($bn) Agitator Ownership Stake (%) Contested issue Results

2006 General Motors 16.8 Kirk Kerkorian/Tracinda 9.9 Directors Pending 2006 Knight Ridder 4.1 Private Capital Management 17.3 Sale V 2006 Heinz 12.5 Nelson Peltz/Trian Fund 5.4 Directors Pending 2006 Gencorp 1.1 Pirate Capital LLC 9.3 Directors V 2006 Acxiom Corp 2.1 ValueAct Capital 11.9 Directors Pending 2006 Motient Corp 1.2 Highland Capital 14.3 Directors Pending 2006 Massey Energy Co 2.8 Daniel Loeb(DNU) 5.9 Directors V 2006 New Century Financial 2.2 Greenlight Capital 6.2 Directors S 2005 Wendy’s 5.5 Nelson Peltz/Trian Fund 5.5 Spin off/elect directors V 2005 McDonald’s 34.7 Pershing Square Capital Management 0.0 Spin off/sell assets V 2005 Time Warner 76.5 Carl Icahn 1.4 Spin off/share repurchases S 2005 Office Max 2.1 K Capital Partners 8.6 Directors S 2005 Career Education Corp. 3.6 Steve Bostic 1.2 Amend by-laws V 2005 Beverly Enterprises 1.4 Investor Group 8.1 Directors S 2005 Kerr-McGee 8.9 Carl Icahn 4.2 Directors V 2005 Sovereign Bancorp Inc 8.0 Relational Investors 8.4 Directors S 2005 Blockbuster 1.1 Carl Icahn 9.7 Directors V 2005 Circuit City 4.5 Highfields Capital 6.9 Unsolicited offer D 2004 Payless Shoesource 1.3 Barington Capital Group 1.1 Directors D 2004 Mylan Laboratories 3.9 Carl Icahn 10.0 Vote against merger D 2004 State Street 16.2 Patrick Jorstad n/a Amend by-laws D

V = Victory for AgitatorD = Defeat for AgitatorS = Settled

SECTION 3

How to Prepare for a Hostile Bid

17

How Could a Suitor Make an Approach?

Casual Pass/ Friendly Lunch Private Letter/“Bear Hug” Public “Bear Hug” Proxy Fight

Tender/ Exchange Offer

Comment ♦ CEO to CEO ♦ CEO to friendly

board member

♦ To CEO only ♦ To CEO and

board members ♦ To board members only ♦ With threat to go public

if Target is unwilling to negotiate

♦ More likely only after a rebuffed approach

♦ More likely as a threatened course of action or pursued with a cash tender

♦ More likely as a threatened course of action than one which is actually pursued

Advantages to Acquirer

♦ May be the easiest way to get discussion going

♦ An unsuspecting CEO may signal a willingness to consider a transaction

♦ May be a way to solicit board members without doing anything overly hostile vis-à-vis management

♦ Can gauge Target reaction without public knowledge

♦ Keeps door open for friendly negotiations

♦ Degree of hostility can be varied

♦ Allows financial flexibility

♦ May provide opportunity to get an inside look

♦ Allows bidder to get a reaction to a price without initiating a tender offer

♦ Can be effective even if threatened and not actually commenced

♦ Potentially least expensive way to gain control or effect change

♦ Fastest approach ♦ Minimum reaction time ♦ Start clock running for

anti-trust and tender offer regulations

♦ Pure economic basis ♦ Unilateral action ♦ Maximum pressure

Disadvantages to Acquirer

♦ Can easily be discouraged by management

♦ Doesn’t exert any real pressure

♦ Less pressure put on Target as compared to public alternatives

♦ May give Target time to explore alternatives if insufficient pressure applied

♦ Easier to reject than tender offer

♦ May have to be backed up with threat of tender offer to be effective

♦ Management’s stronger position via control of proxy process

♦ War of words-limited chance to make economic proposal

♦ Limited information (public only) on Target

♦ Pure economic basis ♦ Extremely “ hostile”

approach ♦ Additional litigation

possibilities ♦ Risk of being topped

Less AggressiveLess Pressure

More AggressiveMore Pressure

18

Strategic Preparedness

Avoid Putting Target in Play

Deter Suitors from Going

Hostile

Keep Control

Preserve Options

Set Your Own Terms

♦ Once a public proposal is received, enormous pressures are brought to bear on management and the Board, regardless of Target’s defenses

♦ A hostile bid that escalates to a proxy battle can often cause irreparable harm to Target, regardless of who “wins”

♦ Important to be offensively prepared

♦ Target’s Board and management team that provides appropriate and well rehearsed responses to casual inquiries will convey preparedness, strength, solidarity and resolve

♦ Convinces unwelcome suitor that they would lose if they went hostile

♦ The timing and wording of Target’s early press releases following a public hostile overture can often define the chain of events that follows

♦ First impressions are critical

♦ It is important to define the conflict and to brand the “raider” in the public domain

♦ The public pressure of a hostile bid can severely constrain the flexibility of Target to pursue growth ambitions if they are remotely controversial

♦ If and when Target is willing to relinquish its independence, it can do so on its own terms

♦ Retain flexibility to choose preferred partner and to begin negotiations at an appropriate time

Why is preparedness important?

Early preparation offers the maximum ability to maintain control of decisions which impact its long-term strategic direction

19

Pre-Unsolicited Overture PreparationEstablish a defense working group in order to remove the element of surprise

Defense Preparation

Investment Banker Legal Counsel Shareholder Relations CEO

♦ Prepare financial analysis and valuation with periodic updates to the Board

♦ Identify and prioritize strategic alternatives

♦ Prepare and periodically update response playbook for different unsolicited approaches

♦ Prepare due diligence file♦ Regular contact and

communication of material developments

♦ Understand White Squire/White Knight possibilities

♦ Identify potential (hostile) suitors or hedge fund aggressors

♦ Assess impact of change of control on the business

♦ Review and analyze recapitalization alternatives

♦ Review Director duties in context of 3rd party solicitations

♦ Review and implementation of structural defenses

♦ Understand Delaware corporate law considerations

♦ Review of business for antitrust analysis

♦ Regulatory agency approvals for change of control

♦ Disclosures that might cause a potential acquiror to look elsewhere

♦ Understand procedures regarding Rule 14a-8 and shareholder proposals

♦ Monitor SEC responses during proxy season (reconsiderations)

♦ Financial public relations♦ Contacts with research

analysts, institutional holders and hedge funds

♦ Activist institutional investors and corporate governance and proxy issues

♦ Ensure security of all forms of shareholder lists

♦ Contact with specialist and monitor trading activity

♦ Prepare internal employee communications programs

♦ Have “game plan” in the event of activist shareholder proposals that identify alternatives to satisfy investors

♦ Sole spokesperson on independence and takeover issues

♦ Prepare responses to different unsolicited approaches

♦ Maintain communication with Executive officers and Board

♦ Gain Board endorsement of business plan through regular updates

♦ Prepare communication program– employees– clients– officers– board– public officials

20

Target’s Fundamental Defense Profile

Strength Weakness Neutral Comments

Liquidity

Size

Valuation

Historical Stock Performance

Shareowner Confidence in Management

and Plan

Leverage

Insider Control

InstitutionalOwnership

Availability of White Knights

21

Target’s Tactical Defense Profile - Illustration♦ Company Name—Target

♦ Headquarters—Chicago, IL

♦ State of Incorporation—Delaware

♦ Annual Meeting—Last annual meeting held on June 30, 2006; annual meetings of stockholders held on such date and at such time as may be fixed by the BoD; notice of annual meeting shall be given to stockholders not less than ten (10) nor more than sixty (60) days before the date of such annual meeting

♦ Board of Directors—The BoD can be no less than three (3) nor more than ten (10); Board currently consists of five (5) directors– Board may increase or decrease size of Board without shareholder

approval

♦ Staggered Board—No; board of directors is elected annually

♦ Cumulative Voting—No

♦ Special Meetings of the Board—Special meetings of the BoD may be held upon 48 hours written notice or 24 hours oral notice by the Chairman of the Board or President or any two directors

♦ Board Vacancy/Removal—Any vacancy on the BoD may be filled by a majority of the Board then in office, but shall be required to stand for election at the next annual meeting; a director, or the entire BoD, may be removed from office at any time, but only for cause with the affirmative vote of a majority of the directors currently in office

♦ Special Meetings of the Stockholders—Special meetings of the stockholders may be called by (i) the Chairman of the Board, (ii) the President, (iii) resolution of the Board of Directors, or (iv) by shareholders holding at least 20% of the vote

♦ Notice of Proposal—Stockholder notice (of business/proposal) must be delivered to or mailed and received at the principal executive offices of the Corporation not less than sixty (60) days nor more than ninety (90) days prior to the meeting

♦ Action by Written Consent—Any action required or permitted to be taken by the Board of Directors may be taken without a meeting if all of the members of the Board of Directors consent in writing to the adoption of a resolution authorizing such action (unanimous written consent)

♦ State Statutes– Expanded Constituency: Board may consider interests of customers,

employees, creditors and communities, in addition to shareholders, when taking any action

– Freezeout with Fair Price Provision: Company may not enter into a business combination with an interested shareholder (20%+ ownership) for five years from the date of becoming an interested shareholder. After five years, any business combination must be approved by non-interested shareholder(s) or certain fair price provisions must be met

– Anti-greenmail: Company may not purchase more than 10% of its stock from a shareholder at more than market price without offering to purchase all outstanding shares

♦ Amendments– Bylaws: The Board of Directors shall have concurrent power with the

shareholders to adopt, amend, or repeal the bylaws of the corporation as set forth in the bylaws but in no event less than a majority of the BoD(currently majority vote)

– Articles of Incorporation: May be amended by a majority vote of the BoDand a majority vote of shareholders

♦ Authorized Capital– Common Stock—50,000,000 shares (par value $0.01) authorized,

18,762,062 issued and outstanding (basic)– Preferred Stock—1,000,000 shares authorized, none issued or

outstanding

♦ Shareholder Rights Plan—Yes; flip-in/flip-over with an exercise price of $80.00 (3.8x recent price, 3.3x price at adoption).

– Occurs upon Acquiring Person obtaining 20% ownership

– The shareholder rights plan expires 11/10/2007

♦ Ownership—97% float; largely traditional institutional ownership– 3% insider ownership (primarily ESOP)– 87% institutional ownership (59% held by top 15 institutions)– 13% hedge fund ownership

22

ISS Recommends Shareholders Vote Against 1

ISS Shareholder Rights Plan Overview

♦ Twenty percent or higher flip-in– Pills should not discourage potential bidders from

accumulating a meaningful stake in the company or cause a large shareholder to inadvertently trigger the rights

♦ Two- to three-year sunset provision– Shareholders ought to have the opportunity to ratify or

reject pill at least every two to three years, thus permitting shareholders to reaffirm or redeem a pill based on how the company’s board has used it in the past, market conditions, or the firm’s performance

♦ Board redemption feature– A redemption clause allows the board to rescind or disapply

a pill even after a potential acquirer has surpassed the ownership threshold, thus giving the board sufficient flexibility when employing poison pill in negotiations

♦ Shareholder vote on poison pill– Shareholders ought to vote for proposals requesting that

the company submit its poison pill to shareholder vote in order to redeem it

♦ Shareholder Redemption Features– If the Board refuses to redeem the pill 90 days after an offer

is announced, 10% of the shares may call a special meeting or seek a written consent to vote on rescinding the pill

♦ Dead-hand or no-hand features– Only the incumbent directors may amend or redeem the

rights plan, thus preventing a hostile acquirer from effectinga merger until the pill elapses, even if it gains board control

– The “continuing director” provisions pose severe restraints on a future board’s ability to manage the company’s affairs and should be excluded from shareholder rights plans

♦ Expanded constituency provision– Shareholders should vote against proposals that ask the

board to consider non-shareholder constituencies or other non-financial effects when evaluating a merger or business combination

♦ No Redemption Features

Source: ISS Proxy U.S. Proxy Voting Manual

ISS General Approval of PillsContaining the Following Features

Note:1 If no shareholder vote, ISS withholds vote on director(s)

23

Takeover Defense Considerations

♦ Efficacy against hedge funds takeover activities is debatable

♦ Limiting hedge funds’ stake to even 10% of a company’s stock will not prohibit funds from undertaking effective destabilization campaigns– “Wolf pack” tactics can effectively avoid Regulation 13D treatment and/or triggering poison pills

♦ Increasing number of companies are repealing shareholder rights plans to have one “on the shelf” instead

Shareholder Rights Plans

ClassifiedBoard

CharterProvisions

Advance NoticeBy-Law

♦ Currently one of the most effective protections against proxy contests– Weakened by recent activist efforts such as direct access proposals and the push for majority elections– Chairman may be vulnerable if his class of Directors is up for election at upcoming shareholder meeting

♦ Activist investors continue to demand de-staggered Boards and companies are generally complying to investor demands

♦ Prohibit the removal of Directors for any reason other than “for cause” and protect against proxy contests to “pack” the Board

♦ Prevent raiders from finding end runs around staggered Boards

♦ Very difficult to amend public company charters to insert this type of “defensive” provision if not originally included

♦ By-law can be adopted requiring advance notice of board nominations by shareholders not less than a certain number of days (usually 60–90 days) and no more than a certain number of days (usually 90–120) before an annual meeting or shareholder meeting

♦ Limits a company’s chances of a proxy contest to a shorter period (usually 30 days)

24

Spectrum of Strategic Alternative Considerations - Illustration

Hostile defense advisory

Ongoing sense of value

Financial / tactical vulnerability

Evaluation of potential unsolicited offers

Other Board Considerations

Pre-unsolicited overture preparation

Informed view of value implications of various strategic alternatives

Fiduciary duties in takeover situations

Response alternatives to various approaches

Business / Asset Optimization

Acquisition

Divestitures

Organic Investment

Capital Structure Realignment

Bank debt amendment

Follow-on / secondary offering

Rights offerings

Exchange offer / equitization

Formulation of strategic plan

Internal valuation analysis / sensitivity

Industry / competitor analysis

Communication with the Street

Change of Control / Ownership

Strategic sale of company

Break-up

Re-IPO

Going private transaction

Target

Defense Preparedness Standalone Analysis

25

Do Nothing/ “Just Say No”

♦ Highlight upside potential of business plan♦ Intensity and tenor of independence campaign will signal whether or not it is simply a matter of price

Auction Company

♦ With the takeover battle in the public domain, potential interlopers will be encouraged to consider a move regardless of whether or not Target solicits them

♦ Target could pursue a “just say no” campaign publicly, and still entertain interloper discussions privately

♦ Should Target’s Board succeed in securing another offer, it may still feel compelled to give Acquiroran opportunity to enter a competitive bidding situation

Strategic Divestitures

♦ Can be pursued in connection with an independence campaign as a means of bolstering the stock price by providing shareholders with near-term milestones

♦ Presumes Target is fundamentally undervalued in the market

“Pac-Man”

♦ Target could launch hostile bid on Acquiror♦ Would validate strategic rationale of transaction♦ Battle centered almost exclusively on management credibility♦ Would suggest a compromise could be reached to the benefit of both sets of shareholders

Spin-Offs/Recapitalizations

♦ Excess cash could be distributed to stockholders♦ Target could seek to break itself up into two or more separate pieces♦ presumes sum-of-parts valuation is greater than current market♦ Significant credit complications

Target’s Defensive Alternatives

26

GreaterImmediateImpact

LesserImmediateImpact

CorporateStructure

CapitalStructure

White SquireArrangements

Dividends

Employee Incentives(ESOP/Options)

Do Nothing

Structural Protections(Rights Plan, CharterAmendments)

StrategicAcquisitions/Divestitures/Joint Ventures

SubsidiaryOfferings(IPO)

Leveraged BuyoutRecapitalization/Share Repurchase

Split-ups/Spin-offs

Auction Company

Active Takeover Defenses

♦ Cash♦ Stock♦ Debt Capacity♦ Business/Assets♦ Employees

Actions in Light of Unsolicited Public Offer

National Directors Institute

The Board’s Role in Defending Against Hostile Bids

March 8, 2007

2

Ashton Partners Snapshot

Full service investor relations and crisis management firm

National reputation for helping clients design and better execute high ROI programs

Wide range of clients served by size, industry, issues faced, programs executed

Flexible team staffing by individuals with strong financial backgrounds

3

Our Differentiation

Each client is staffed by seasoned financial advisors with advanced degrees and experience across a wide spectrum of corporate issues

Focus on managing credibility through relationship management and specific messaging

Emphasis on quantitative research with track record of predicting investor behavior

Dedicated research team provides real-time intelligence on:

SEC complianceAccounting issuesInvestor sentimentShifts in portfolio focus

4

Increased Visibility Buy-Side & Sell-Side RoadshowsInvestor Meeting PrioritizationFinancial Media Outreach

Seamless Event SupportIPO/Secondary ProgramsContested Proxy SupportShareholder Activism DefenseTransaction Support

Improved Market FeedbackBenchmarked Perception StudiesInvestor Meeting Preparation & Follow-UpPredicting Shareholder Movements

Enhanced CredibilityStrategic Messaging & PositioningCrisis ManagementCEO/CFO Coaching

Value-Added Services

5

Explosion of Shareholder Activism

Growing numbers…Over one hundred known shareholder activists with total equity AuM in excess of $150B

Scarce returns…Number of activists and campaigns continues to grow while ‘alpha’ diminishes

Over-crowed hedge fund class

Limited returns from traditional hedge strategies

Activism = Proven Opportunity…Based on recent research, of 94 campaigns over the past few years, activists succeeded in 75% of those cases

6

Hostile Bids – By Type

0

50

100

150

200

Financial Buyers Corporate Buyers

Last YearLast 10 Years

0

10

20

30

40

Financial Buyers Corporate Buyers

31%

69%

41%

59%

7

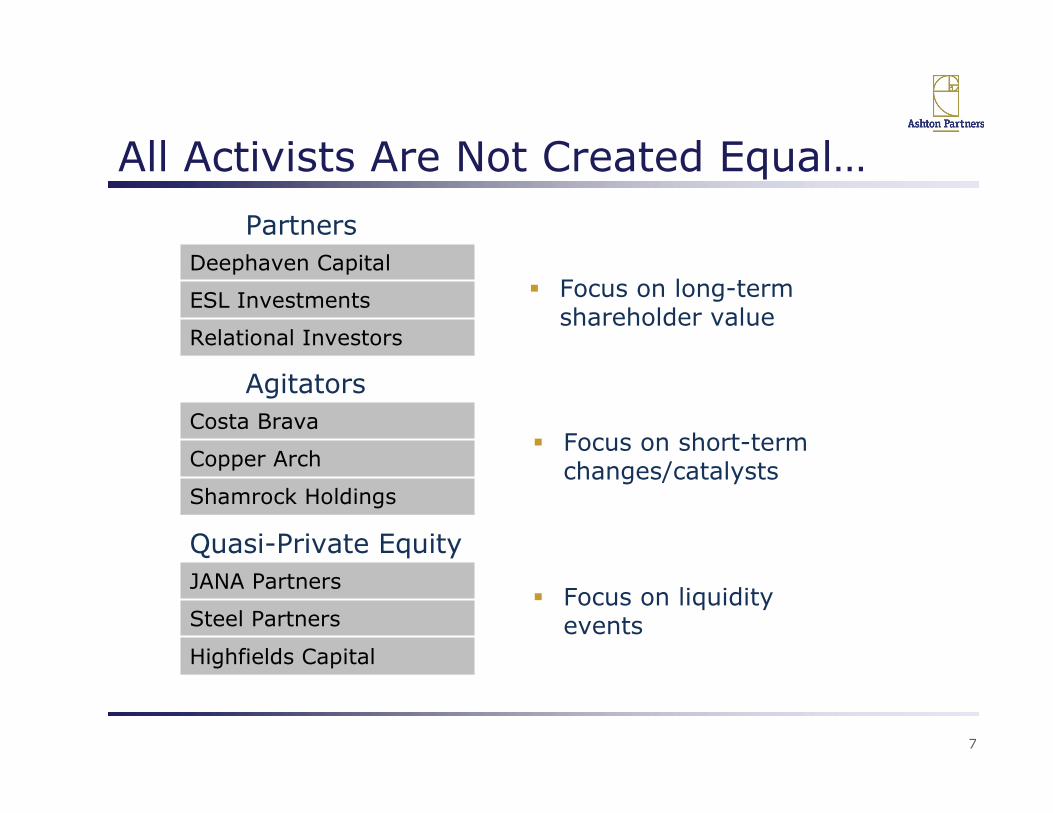

All Activists Are Not Created Equal…

Relational Investors

ESL Investments

Deephaven Capital

Shamrock Holdings

Copper Arch

Costa Brava

Partners

Agitators

Focus on long-term shareholder value

Focus on liquidity events

Highfields Capital

Steel Partners

JANA Partners

Quasi-Private Equity

Focus on short-term changes/catalysts

8

Activist Scorecard

% of Campaigns with Particular Outcome

22%

21%

20%

21%

4%

50%

63%

44%

47%

75%

55%

70%

50%

38%

33%

32%

5%

24%

26%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Special Dividend

Elimination of DefensiveMechanisms

Block M&A Bid

Share Repurchase

New Management

Sale of Companyor Assets

Board Presence

Company Success Company Defeat Ongoing

Source: Morgan Joseph & Co. Inc.

9

Why Do Activists Succeed?

They are well prepared before making an investment

Know the by-laws of your company

Know your shareholder base, trading environment, etc.

Have a detailed plan/agenda that has worked in similar situations

They often echo a sentiment many core holders share, but haven't acted upon

Particularly strategic plans that are not deemed rational or defensible

They are well versed in using influencers to support their agenda (e.g., sell-side, media, ISS)

Activists sell the need for ‘change’ which hinges on the absence of a reasonable alternative

10

Companies At-Risk

YES/NOInefficient use of cash

YES/NOMissed opportunities (e.g., M&A)

YES/NOEntrenched management, BOD

YES/NOPoor stock price performance

YES/NOUnclear, unsubstantiated strategy

YES/NOPoor operating performance

Issue?Typical Activist Angles

YES/NOSignificant operating history

YES/NODefensive business model

YES/NOCheap valuation

YES/NORecurring revenue and cash flow

YES/NOHigh net cash

Appeal?Business Characteristics

Real/Perceived Issues Investment Protection

11

Activist Decision Matrix

Expected Probability of Winning

Expected Value Creation from Control Transfer

Activist’s Target Return

Reduce V

alue

Proposit

ion

12

Preventing Hostile Situations

Reduce expected probability of winning

Long-Term

Investors

35%

Activists

24%

Short-Term /

Hedge

4%

Passive Investors

29%

Insiders

8%

Share DistributionRecognize early warning signs of activist movements

Demand better shareholder intelligence

Regular feedback from all types of shareholders

Build pipeline of long-term, active institutional investors

Gain support from third-party influencers

ISS typically influences at least 30% of shares outstanding

13

Preventing Hostile Situations

Reduce expected value creation from control transfer

Value Creation OpportunitiesLead efforts to articulate a well vetted strategy

Communicate key priorities

Provide benchmarks and milestones

Address messaging gaps

Make proactive operation decisions

Address troubled areas of business (e.g., sale/divestiture of underperforming business units)

Restructure/cost alignment

Put excess cash to work

Execution

Operational

Changes

Cash

Deployment

Credibility

Gap

0%

20%

40%

60%

80%

100%

Value Creation

14

Preventing Hostile Situations

Moderate

Accumulate stake

Use trading and hedging strategies to increase position and leverage

Encourage other hedge funds to enter stock

Observe and comment

Agitate privately

Aggressive questioning on conference calls

“Cheap Activism”

Shareholder proposals

Withhold vote campaign

Agitate for removal of takeover defenses

Form alliance with other shareholders

Interview customers and employees

Leak ideas to sell-side analysts

File Schedule 13D

Hire experts in sector

Hostile

Present detailed proposal

Demand Board seats

PR battle

Solicit buyers

Enlist ISS/ Glass Lewis to publicly support dissident action

Litigation

Tender offer

Proxy fight

Recognize the early warning signs…

15

Preventing Hostile Situations

Demand better shareholder intelligence:

Regular feedback from all types of shareholders

Understand what’s driving shareholder interest in your story

Determine support level, long-term commitment to story

Proactive plan to build pipeline of attractive long-term investors that can serve as potential supporters in a hostile situation

Window of opportunity to attract these types of investors will close if/when hostile situation turns public

Stock surveillance (a.k.a. stockwatch) is not the answer

Fraught with integrity issues and factual inaccuracies

16

Preventing Hostile Situations

Gain support from third-party influencers:

Proxy advisory firms

Primary audience: passive institutional investors

Focus: ISS will conduct side-by-side evaluation of strategic plans from management and dissident group

Media

Primary audience: individual investors

Focus: steady stream of positive press releases

Sell-side

Primary audience: active institutional investors

Focus: consistent participation in non-deal road shows, investor conferences

17

Preventing Hostile Situations

Lead efforts to articulate a well vetted strategy:

Status quo is not enough

Don’t let your historical performance speak for itself

Don’t assume investors have unabated confidence/trust in management

Articulate key priorities for the company/management

Provide realistic/achievable benchmarks, milestones that investors can use to evaluate management’s execution progress

Address messaging gaps in your story

18

Preventing Hostile Situations

Make proactive operational decisions:

Address the tough decisions where appropriate

Restructure

Sell/divest underperforming business units

Cost realignment

Put cash to work under your own terms

Reinvestments in the business

Initiate/expand share repurchase program

Make strategic acquisitions

19

Other Do’s and Don’ts

What not to do:

Don’t wait for a full blown issue, be prepared early

Don’t avoid communications with the activist

Don’t engage in a PR battle unless you are willing to fully commit and can show signs of recovery

What to do:

Consider standstill or confidentiality agreements with the activist

Keep negotiating door open at all times

National Director’s InstituteHYPOTHETICAL SHARE OWNERSHIP AND PRELIMINARY

VOTE OUTLOOK

ABC Company Preliminary Shareholder ProfileDecember 31, 2006

Shareholder CategoryDecember 31, 2006

Share Holdings % of the O/S ChangeChange as %

of the O/SDecember 1, 2006 Share Holdings % of the O/S

Hedge Funds & Event Driven Investors 25,000,000 25.00% 20,000,000 20.00% 5,000,000 5.00%

Institutional Investors 64,500,000 64.50% (16,000,000) -16.00% 80,500,000 80.50%

Retail Holders 8,000,000 8.00% (4,000,000) -4.00% 12,000,000 12.00%

Officers & Directors 2,500,000 2.50% 0 0.00% 2,500,000 2.50%

Total: 100,000,000 100.00% 0 0.00% 100,000,000 100.00%

Note: December 1, 2006 and December 31, 2006 share holdings are reflective of trade settlements on each day.

Institutional Investors80,500,000

80.5%

Hedge Funds5,000,000

5.0%

Officers & Directors2,500,000

2.5%

Retail Holders12,000,000

12.0%

Pre-Announcement Post-Announcement

ABC Company Preliminary Shareholder ProfileDecember 31, 2006

Hedge Fund Ownership increased from 5,000,000 shares (5.00% O/S) to 25,000,000 shares (25.00% O/S) between December 1, 2006-December 31, 2006

Institutional Ownership decreased from 80,500,000 shares (80.50% O/S) to 64,500,000 shares (64.50% O/S) between December 1, 2006-December 31, 2006

Retail Ownership decreased from 12,000,000 shares (12.00% O/S) to 8,000,000 shares (8.00% O/S) between December 1, 2006-December 31, 2006

Institutional Investors64,500,000

64.5%

Hedge Funds25,000,000

25.0%

Officers & Directors2,500,000

2.5%

Retail Holders8,000,000

8.0%

ABC Company Required Institutional Support for Board Victory in an Election ContestAssumes ISS and Glass Lewis Support Dissident

Charles J. Hansen 1

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• The Delaware courts have developed The Delaware courts have developed three standards of judicial review for three standards of judicial review for directorsdirectors’’ decisions in the takeover decisions in the takeover contextcontext–– Business judgment ruleBusiness judgment rule–– Enhanced scrutinyEnhanced scrutiny–– Entire fairnessEntire fairness

Charles J. Hansen 2

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• Business judgment ruleBusiness judgment rule——DelawareDelaware’’s basic s basic standard of judicial reviewstandard of judicial review–– DirectorsDirectors’’ decisions are presumed to have been decisions are presumed to have been

made on an informed basis, in good faith, and in made on an informed basis, in good faith, and in the honest belief that the action taken was in the the honest belief that the action taken was in the best interest of the company. best interest of the company. Ivanhoe Partners v. Ivanhoe Partners v. Newmont Mining Corporation, Newmont Mining Corporation, 535 A.2d 1334 535 A.2d 1334 (Del. 1987).(Del. 1987).

Charles J. Hansen 3

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• If the court determines the business judgment If the court determines the business judgment rule is applicable, the court will defer to the rule is applicable, the court will defer to the directorsdirectors’’ decision unless the plaintiff carries decision unless the plaintiff carries its burden of proof that the directors did not its burden of proof that the directors did not meet their duty of care or duty of loyaltymeet their duty of care or duty of loyalty

Charles J. Hansen 4

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• Duty of careDuty of care——directors must act on an informed directors must act on an informed basis after appropriate consideration of relevant basis after appropriate consideration of relevant information, including financial and legal advice, information, including financial and legal advice, and duly deliberate. and duly deliberate. Smith v. Van Gorkom,Smith v. Van Gorkom, 488 A. 488 A. 2d 858 (Del. 1985).2d 858 (Del. 1985).

•• Duty of loyaltyDuty of loyalty——directors may not engage in selfdirectors may not engage in self--dealing and cannot have an improper interest in the dealing and cannot have an improper interest in the transaction. transaction. Ivanhoe Partners v. Newmont Mining Ivanhoe Partners v. Newmont Mining Corporation, Corporation, 535 A.2d 1334 (Del. 1987).535 A.2d 1334 (Del. 1987).

Charles J. Hansen 5

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• Enhanced scrutinyEnhanced scrutiny——business judgment rule business judgment rule may not apply when, for example:may not apply when, for example:–– Board responds to a takeover threat by adopting Board responds to a takeover threat by adopting

an antian anti--takeover device.takeover device.–– Board approves a changeBoard approves a change--in control transaction.in control transaction.

Charles J. Hansen 6

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• If the enhanced scrutiny standard is If the enhanced scrutiny standard is applicable, the court will :applicable, the court will :–– Review the boardReview the board’’s processes and actionss processes and actions–– Determine whether the boardDetermine whether the board’’s decisions were s decisions were

reasonable reasonable

•• Unocal Corporation Unocal Corporation v. v. Mesa Petroleum Co.Mesa Petroleum Co., , 493 A.2d 946 (Del. 1985) and 493 A.2d 946 (Del. 1985) and Revlon, Inc. Revlon, Inc. v.v.MacAndrews & Forbes Holdings, Inc.MacAndrews & Forbes Holdings, Inc., 506 A. , 506 A. 2d 173 (Del. 1886).2d 173 (Del. 1886).

Charles J. Hansen 7

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• UnocalUnocal standardstandard——defensive measures in defensive measures in response to perception of threatresponse to perception of threat–– Did board reasonably believe corporate policy Did board reasonably believe corporate policy

threatened?threatened?–– Was boardWas board’’s response reasonable in relation to s response reasonable in relation to

the perceived threat?the perceived threat?–– If the answer to these questions is If the answer to these questions is ““yes,yes,”” the the

boardboard’’s decision is protected by the business s decision is protected by the business judgment rule.judgment rule.

Charles J. Hansen 8

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• Revlon Revlon testtest——enhanced judicial review for enhanced judicial review for salesale--ofof--control transactions.control transactions.

•• Under Under RevlonRevlon, when the board decides to sell , when the board decides to sell the company, the directorsthe company, the directors’’ role changes role changes from from ““defenders of the corporate bastion to defenders of the corporate bastion to auctioneers charged with getting the best auctioneers charged with getting the best priceprice”” for the stockholders.for the stockholders.

•• The board must made a reasonable decision.The board must made a reasonable decision.

Charles J. Hansen 9

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• EntireEntire fairnessfairness——if a majority of the directors if a majority of the directors have a conflict of interest, the Delaware have a conflict of interest, the Delaware courts will determine if the transaction is courts will determine if the transaction is entirely fair to stockholders. entirely fair to stockholders. Cede & Co. Cede & Co. v. v. Technicolor, Inc., Technicolor, Inc., 634 A.2d 345 (Del. 1993).634 A.2d 345 (Del. 1993).

•• CourtsCourts’’ focus:focus:–– Board processBoard process–– Quality of resultQuality of result–– Quality of disclosures made to the stockholdersQuality of disclosures made to the stockholders

Charles J. Hansen 10

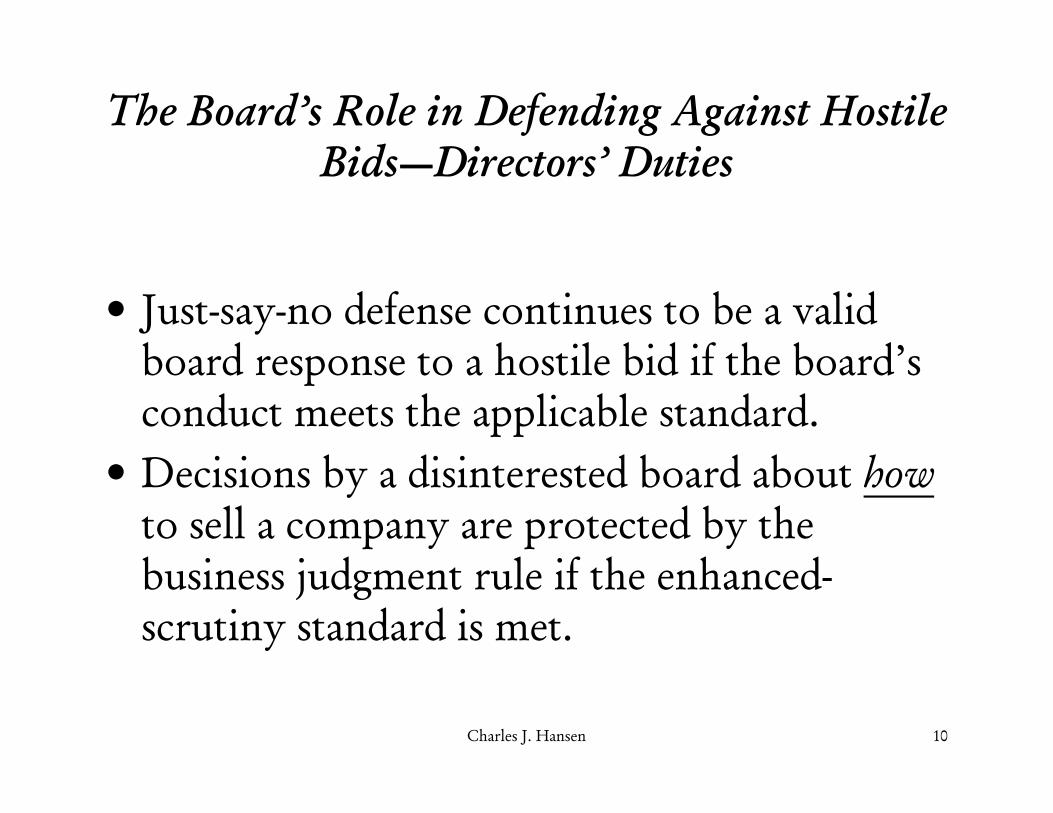

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• JustJust--saysay--no defense continues to be a valid no defense continues to be a valid board response to a hostile bid if the boardboard response to a hostile bid if the board’’s s conduct meets the applicable standard.conduct meets the applicable standard.

•• Decisions by a disinterested board about Decisions by a disinterested board about howhowto sell a company are protected by the to sell a company are protected by the business judgment rule if the enhancedbusiness judgment rule if the enhanced--scrutiny standard is met.scrutiny standard is met.

Charles J. Hansen 11

The BoardThe Board’’s Role in Defending Against Hostile s Role in Defending Against Hostile BidsBids——DirectorsDirectors’’ DutiesDuties

•• DirectorsDirectors’’ best practices:best practices:–– Assume an active role and remain fully informed Assume an active role and remain fully informed

during the entire process.during the entire process.–– Retain and fully utilize experienced legal and Retain and fully utilize experienced legal and

financial advisors.financial advisors.–– Carefully analyze and deliberate.Carefully analyze and deliberate.–– Let the independent directors make the decisions.Let the independent directors make the decisions.–– Carefully document the decisionCarefully document the decision--making process making process

to demonstrate the directors were fully informed.to demonstrate the directors were fully informed.

©2007 Foley & Lardner LLP

The Business Judgment Rule—Counsel’s Script for the Board of Directors

Charles J. Hansen

February 15, 2007

The business judgment rule is alive and well, at least in Delaware, despite attention-grabbing headlines that suggest that service on a corporate Board of Directors is hazardous to one’s financial health. See Walt Disney Co. Derivative Litigation, 906 A.2d 27 (Del. 2006).

The business judgment rule protects the decisions of board of directors from second guessing by presuming that the directors acted in good faith and on an informed basis. This presumption may be overcome only if the plaintiff can demonstrate that the directors breached their duties of care and loyalty or acted in bad faith.

When a board of directors convenes to consider taking important action, counsel can

protect the board by reminding the board about the requirements of the business judgment rule. Counsel can use the following script to explain to the board the requirements of the business judgment rule. Usually the best time to do this is after management, the investment bankers, and the lawyers have made their presentations to the directors and the directors have engaged in a full discussion. The script assumes that the board is disinterested and has preliminarily decided to “just say no” to a hostile takeover bid from Steal-The-Upside Partners, Inc.

Note: the script is merely a template and must be modified to reflect the circumstances

and details of each situation.

The courts should defer to the business judgment decision by this Board of Directors to reject the unsolicited takeover bid from Steal-The-Upside Partners, Inc. if you exercise due care. Due care means that you have acted to assure yourselves that you have the information required to take the action under consideration, that you have devoted sufficient time to the consideration of the information, and that you have obtained, where useful, advice from experts and counsel.

With respect to the unsolicited takeover bid from Steal-The-Upside Partners, Inc. under consideration today, the requirement to exercise due care means that each of you must, at a minimum, understand the following items:

1. [The details of the offer, including its amount, form, and timing; 2. The Company’s financial condition, new products, general

outlook; 3. The Company’s short-, medium-, and long-term strategies;

©2007 Foley & Lardner LLP

4. Management’s best estimates of the Company’s future financial performance;

5. The [investment banker’s] assessment of the adequacy of the offer;

6. The benefits and risks to the shareholders if the Company remains independent;

7. The benefits and risks to the shareholders if the Company accepts the offer;

8. The process management and the [investment bankers] used to analyze the offer;

9. Strategic alternatives to the offer; 10. Impact on constituencies other than the shareholders; 11. The adequacy of the Company’s takeover defenses; and 12. The obstacles to completing the transaction that have been

identified by [counsel]]. Taking into account your discussions with management and among yourselves, the information you have received, including the oral and written presentations by management, [the investment bankers], and the transaction summaries and other information prepared by [counsel], and the other information that we have discussed today, the following three statements should reflect your state of mind at the end of this meeting with respect to the offer if you intend to reject it:

a) First, you understand the offer, the consequences of accepting

and rejecting it, and the other information discussed at today’s meeting, because you believe you believe the information you have been given is sufficient to enable you to make an informed decision, and you have been given adequate time to consider the information;

b) Second, you believe that, where necessary, you are relying in good faith on outside experts with appropriate skills; and

c) Third, after giving due consideration to the foregoing, you believe that the offer is not in the best interests of shareholders [and other reasons].

If these statements do reflect your state of mind as to the offer, then the courts should conclude that the Board of Directors has exercised appropriate due care and that the Board’s business judgment to reject the offer, if that’s the action taken, is entitled to deference by the courts.