HDFC Standard Life Insurance Company Limited is the sole and exclusive property of HDFC Life....

23

This is the sole and exclusive property of HDFC Life. October 26, 2016 HDFC Standard Life Insurance Company Limited Business presentation – H1 FY17

Transcript of HDFC Standard Life Insurance Company Limited is the sole and exclusive property of HDFC Life....

This is the sole and exclusive property of HDFC Life. October 26, 2016

HDFC Standard Life Insurance Company Limited

Business presentation – H1 FY17

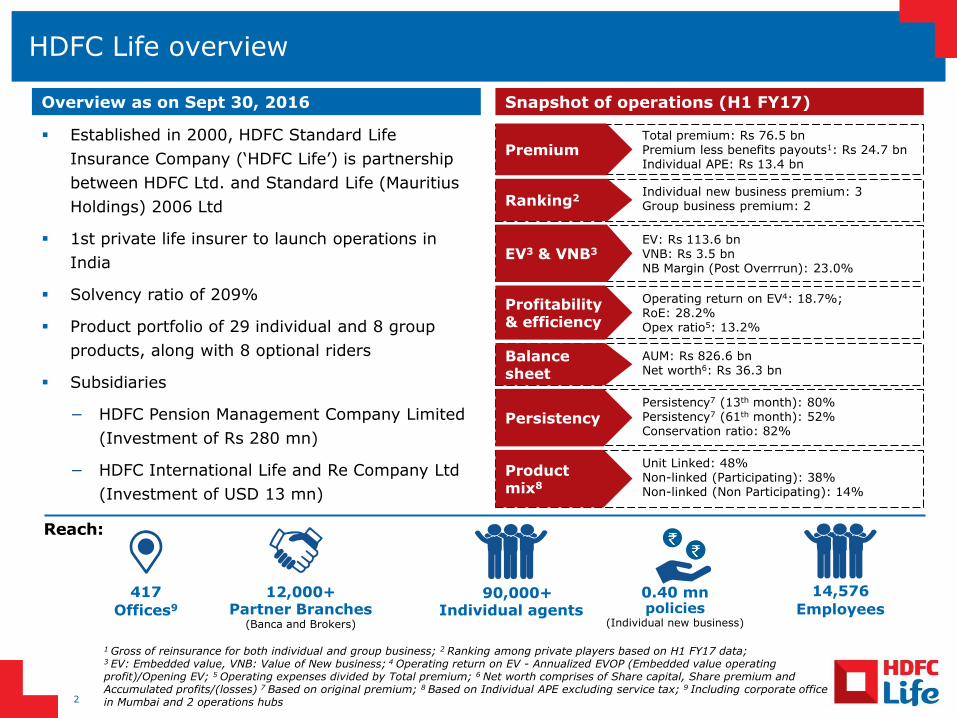

HDFC Life overview

Reach:

Employees

14,576

Partner Branches (Banca and Brokers)

12,000+

Offices9

417

Persistency7 (13th month): 80% Persistency7 (61th month): 52% Conservation ratio: 82% Persistency

AUM: Rs 826.6 bn Net worth6: Rs 36.3 bn Balance sheet

Total premium: Rs 76.5 bn Premium less benefits payouts1: Rs 24.7 bn Individual APE: Rs 13.4 bn Premium

Operating return on EV4: 18.7%; RoE: 28.2% Opex ratio5: 13.2%

Profitability & efficiency

EV: Rs 113.6 bn VNB: Rs 3.5 bn NB Margin (Post Overrrun): 23.0% EV3 & VNB3

Established in 2000, HDFC Standard Life

Insurance Company (‘HDFC Life’) is partnership

between HDFC Ltd. and Standard Life (Mauritius

Holdings) 2006 Ltd

1st private life insurer to launch operations in

India

Solvency ratio of 209%

Product portfolio of 29 individual and 8 group

products, along with 8 optional riders

Subsidiaries

− HDFC Pension Management Company Limited

(Investment of Rs 280 mn)

− HDFC International Life and Re Company Ltd

(Investment of USD 13 mn)

Snapshot of operations (H1 FY17) Overview as on Sept 30, 2016

Unit Linked: 48% Non-linked (Participating): 38% Non-linked (Non Participating): 14%

Product mix8

Individual new business premium: 3 Group business premium: 2 Ranking2

Individual agents

90,000+

1 Gross of reinsurance for both individual and group business; 2 Ranking among private players based on H1 FY17 data; 3 EV: Embedded value, VNB: Value of New business; 4 Operating return on EV - Annualized EVOP (Embedded value operating profit)/Opening EV; 5 Operating expenses divided by Total premium; 6 Net worth comprises of Share capital, Share premium and Accumulated profits/(losses) 7 Based on original premium; 8 Based on Individual APE excluding service tax; 9 Including corporate office in Mumbai and 2 operations hubs 2

policies (Individual new business)

0.40 mn

Our strengths

Strong parentage and a trusted brand that enhances our appeal to consumers

An independent, experienced leadership team driving business performance using a balanced scorecard approach

Growing and profitable multi-channel distribution footprint that provides market access across geographies & consumer segments

Leading position in bancassurance with longstanding partnerships

Efficient technology platform that ensures ease of purchase for consumers and enables rapid integration with distributors

Proven ability to consistently grow and deliver across business cycles

1

2

3

4

5

6

Strong financial performance defined by profitable growth reflecting robustness of the business model

7

3

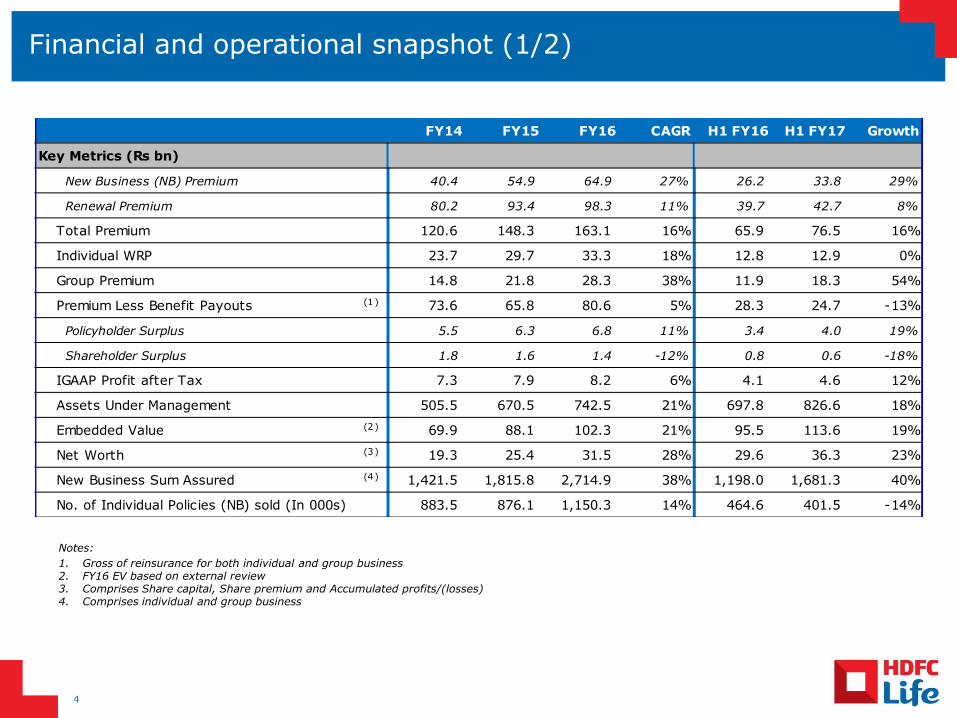

Financial and operational snapshot (1/2)

Notes:

1. Gross of reinsurance for both individual and group business 2. FY16 EV based on external review 3. Comprises Share capital, Share premium and Accumulated profits/(losses) 4. Comprises individual and group business

4

FY14 FY15 FY16 CAGR H1 FY16 H1 FY17 Growth

Key Metrics (Rs bn)

New Business (NB) Premium 40.4 54.9 64.9 27% 26.2 33.8 29%

Renewal Premium 80.2 93.4 98.3 11% 39.7 42.7 8%

Total Premium 120.6 148.3 163.1 16% 65.9 76.5 16%

Individual WRP 23.7 29.7 33.3 18% 12.8 12.9 0%

Group Premium 14.8 21.8 28.3 38% 11.9 18.3 54%

Premium Less Benefit Payouts (1) 73.6 65.8 80.6 5% 28.3 24.7 -13%

Policyholder Surplus 5.5 6.3 6.8 11% 3.4 4.0 19%

Shareholder Surplus 1.8 1.6 1.4 -12% 0.8 0.6 -18%

IGAAP Profit after Tax 7.3 7.9 8.2 6% 4.1 4.6 12%

Assets Under Management 505.5 670.5 742.5 21% 697.8 826.6 18%

Embedded Value (2) 69.9 88.1 102.3 21% 95.5 113.6 19%

Net Worth (3) 19.3 25.4 31.5 28% 29.6 36.3 23%

New Business Sum Assured (4) 1,421.5 1,815.8 2,714.9 38% 1,198.0 1,681.3 40%

No. of Individual Policies (NB) sold (In 000s) 883.5 876.1 1,150.3 14% 464.6 401.5 -14%

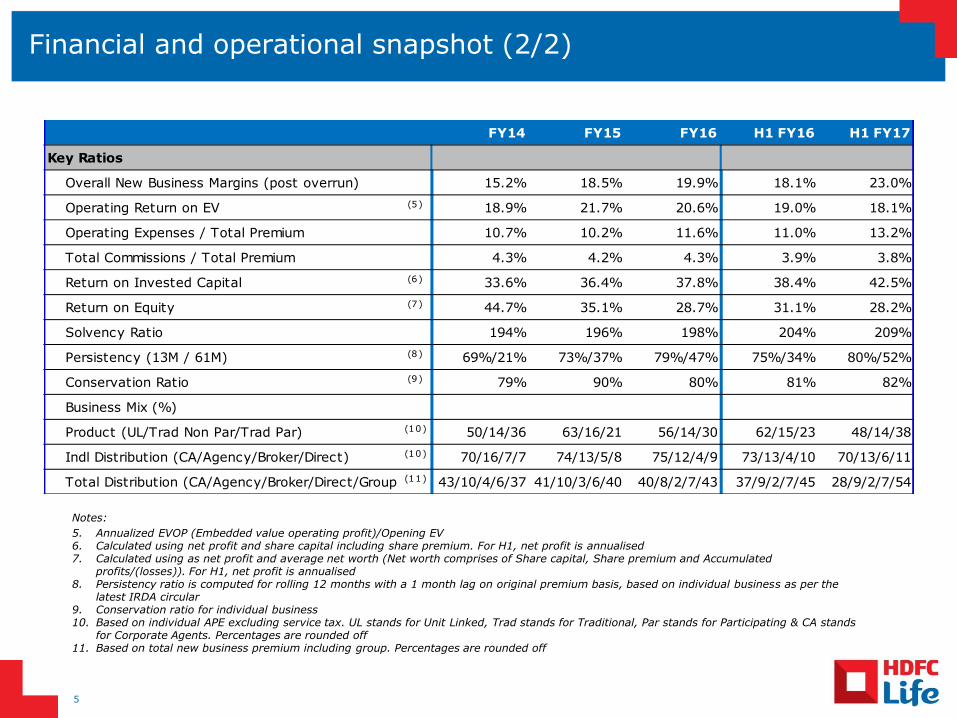

Financial and operational snapshot (2/2)

Notes:

5. Annualized EVOP (Embedded value operating profit)/Opening EV 6. Calculated using net profit and share capital including share premium. For H1, net profit is annualised 7. Calculated using as net profit and average net worth (Net worth comprises of Share capital, Share premium and Accumulated

profits/(losses)). For H1, net profit is annualised 8. Persistency ratio is computed for rolling 12 months with a 1 month lag on original premium basis, based on individual business as per the

latest IRDA circular 9. Conservation ratio for individual business 10. Based on individual APE excluding service tax. UL stands for Unit Linked, Trad stands for Traditional, Par stands for Participating & CA stands

for Corporate Agents. Percentages are rounded off 11. Based on total new business premium including group. Percentages are rounded off

5

FY14 FY15 FY16 H1 FY16 H1 FY17

Key Ratios

Overall New Business Margins (post overrun) 15.2% 18.5% 19.9% 18.1% 23.0%

Operating Return on EV (5) 18.9% 21.7% 20.6% 19.0% 18.1%

Operating Expenses / Total Premium 10.7% 10.2% 11.6% 11.0% 13.2%

Total Commissions / Total Premium 4.3% 4.2% 4.3% 3.9% 3.8%

Return on Invested Capital (6) 33.6% 36.4% 37.8% 38.4% 42.5%

Return on Equity (7) 44.7% 35.1% 28.7% 31.1% 28.2%

Solvency Ratio 194% 196% 198% 204% 209%

Persistency (13M / 61M) (8) 69%/21% 73%/37% 79%/47% 75%/34% 80%/52%

Conservation Ratio (9) 79% 90% 80% 81% 82%

Business Mix (%)

Product (UL/Trad Non Par/Trad Par) (10) 50/14/36 63/16/21 56/14/30 62/15/23 48/14/38

Indl Distribution (CA/Agency/Broker/Direct) (10) 70/16/7/7 74/13/5/8 75/12/4/9 73/13/4/10 70/13/6/11

Total Distribution (CA/Agency/Broker/Direct/Group) (11) 43/10/4/6/37 41/10/3/6/40 40/8/2/7/43 37/9/2/7/45 28/9/2/7/54

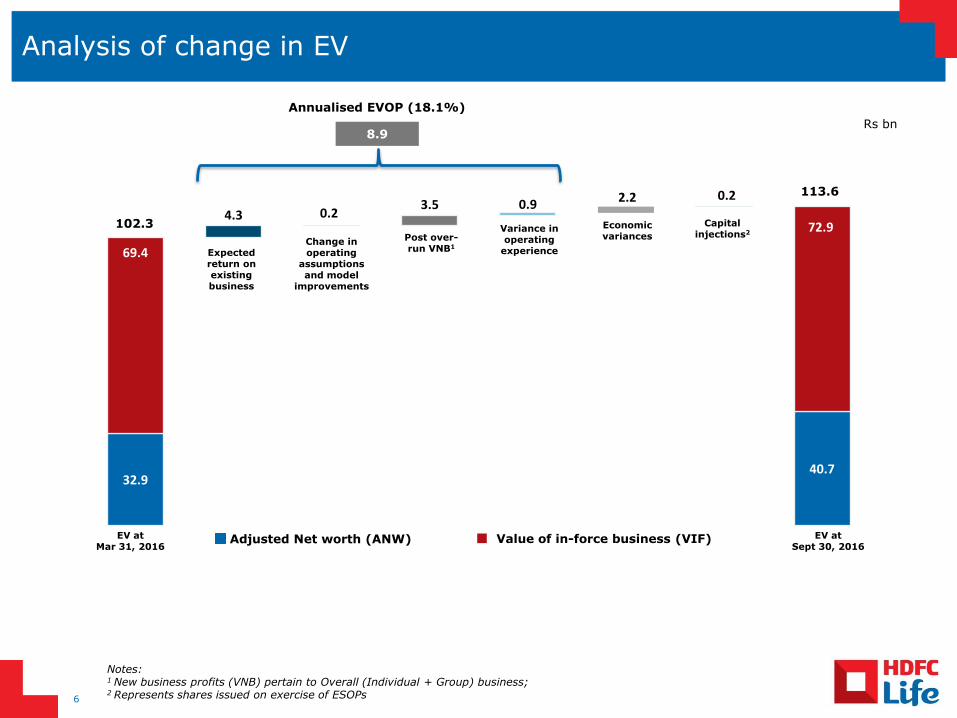

Analysis of change in EV

32.9 40.7

69.4

4.3 0.2 3.5 0.9

2.2 0.2

72.9

Annualised EVOP (18.1%)

8.9

EV at Mar 31, 2016

EV at Sept 30, 2016

Expected return on existing business

Capital injections2

Change in operating

assumptions and model

improvements

Post over-run VNB1

Variance in operating

experience

Economic variances

Rs bn

102.3

113.6

Notes: 1 New business profits (VNB) pertain to Overall (Individual + Group) business; 2 Represents shares issued on exercise of ESOPs

Value of in-force business (VIF) Adjusted Net worth (ANW)

6

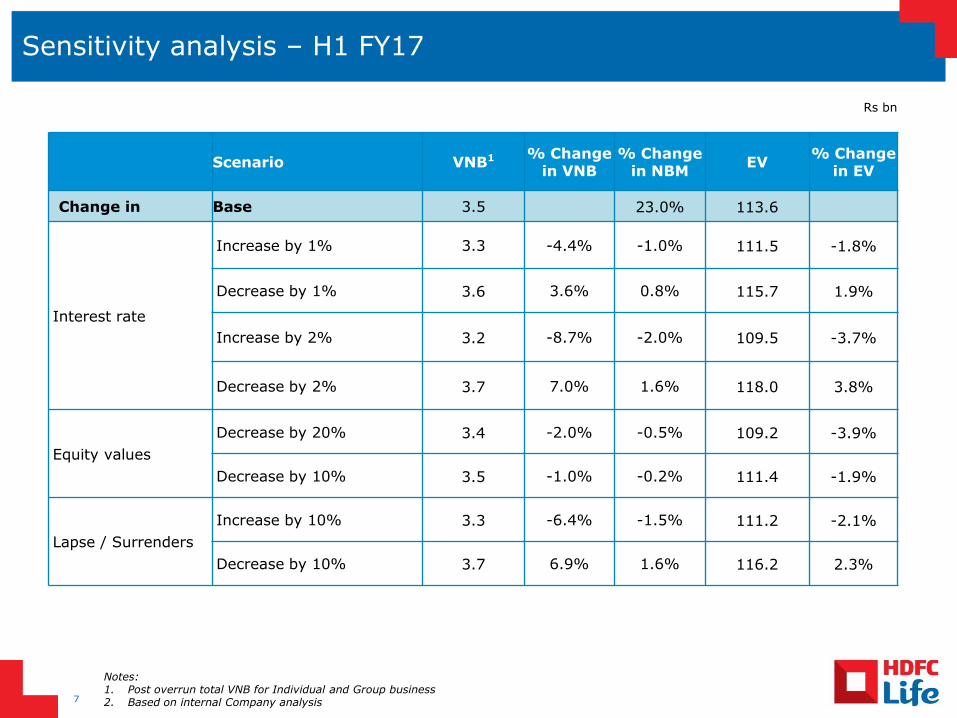

Sensitivity analysis – H1 FY17

Notes: 1. Post overrun total VNB for Individual and Group business 2. Based on internal Company analysis 7

Scenario VNB1 % Change in VNB

% Change in NBM

EV % Change

in EV

Change in Base 3.5 23.0% 113.6

Interest rate

Increase by 1% 3.3 -4.4% -1.0% 111.5 -1.8%

Decrease by 1% 3.6 3.6% 0.8% 115.7 1.9%

Increase by 2% 3.2 -8.7% -2.0% 109.5 -3.7%

Decrease by 2% 3.7 7.0% 1.6% 118.0 3.8%

Equity values

Decrease by 20% 3.4 -2.0% -0.5% 109.2 -3.9%

Decrease by 10% 3.5 -1.0% -0.2% 111.4 -1.9%

Lapse / Surrenders

Increase by 10% 3.3 -6.4% -1.5% 111.2 -2.1%

Decrease by 10% 3.7 6.9% 1.6% 116.2 2.3%

Rs bn

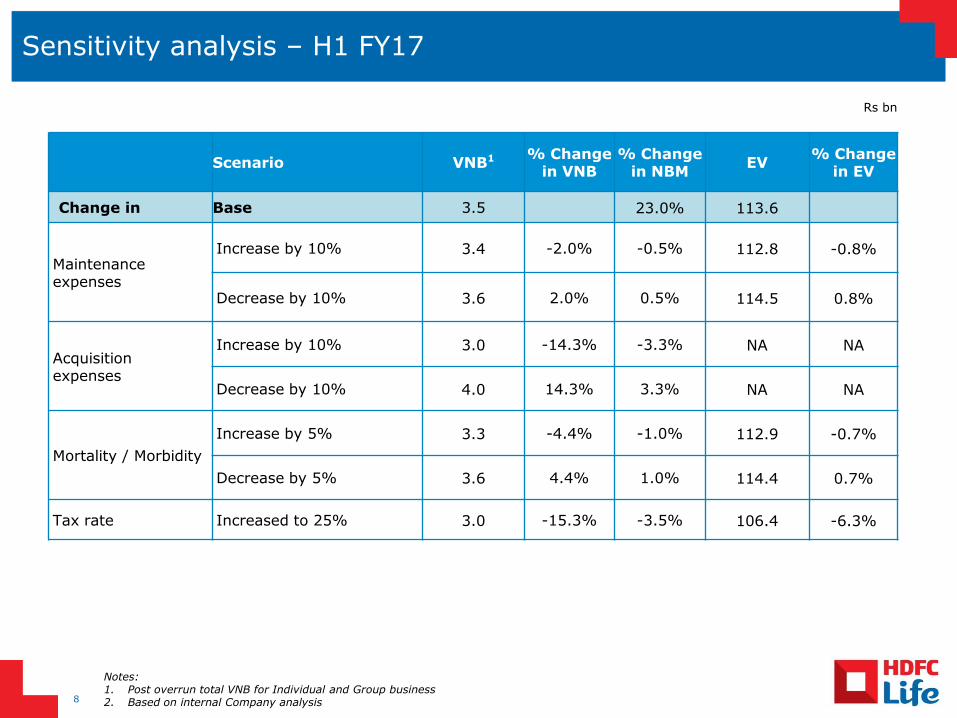

Sensitivity analysis – H1 FY17

Notes: 1. Post overrun total VNB for Individual and Group business 2. Based on internal Company analysis 8

Scenario VNB1 % Change in VNB

% Change in NBM

EV % Change

in EV

Change in Base 3.5 23.0% 113.6

Maintenance expenses

Increase by 10% 3.4 -2.0% -0.5% 112.8 -0.8%

Decrease by 10% 3.6 2.0% 0.5% 114.5 0.8%

Acquisition expenses

Increase by 10% 3.0 -14.3% -3.3% NA NA

Decrease by 10% 4.0 14.3% 3.3% NA NA

Mortality / Morbidity

Increase by 5% 3.3 -4.4% -1.0% 112.9 -0.7%

Decrease by 5% 3.6 4.4% 1.0% 114.4 0.7%

Tax rate Increased to 25% 3.0 -15.3% -3.5% 106.4 -6.3%

Rs bn

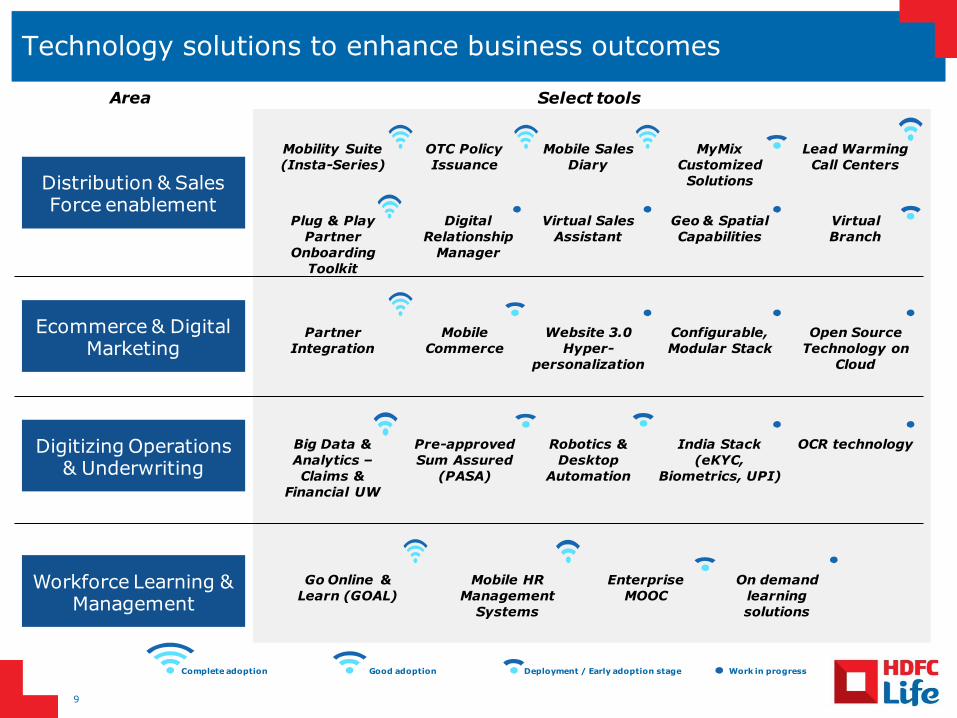

Technology solutions to enhance business outcomes

9

Distribution & Sales Force enablement

Ecommerce & Digital Marketing

Digitizing Operations & Underwriting

Workforce Learning & Management

Work in progressDeployment / Early adoption stageGood adoptionComplete adoption

Big Data &

Analytics –

Claims &

Financial UW

Pre-approved

Sum Assured

(PASA)

Robotics &

Desktop

Automation

India Stack

(eKYC,

Biometrics, UPI)

Go Online &

Learn (GOAL)

Mobile HR

Management

Systems

Enterprise

MOOC

On demand

learning

solutions

Mobility Suite

(Insta-Series)

OTC Policy

Issuance

Mobile Sales

Diary

MyMix

Customized

Solutions

Lead Warming

Call Centers

Virtual Sales

Assistant

Geo & Spatial

Capabilities

Virtual

Branch

Mobile

Commerce

Partner

Integration

Configurable,

Modular Stack

Open Source

Technology on

Cloud

Select toolsArea

Website 3.0

Hyper-

personalization

Digital

Relationship

Manager

Plug & Play

Partner

Onboarding

Toolkit

OCR technology

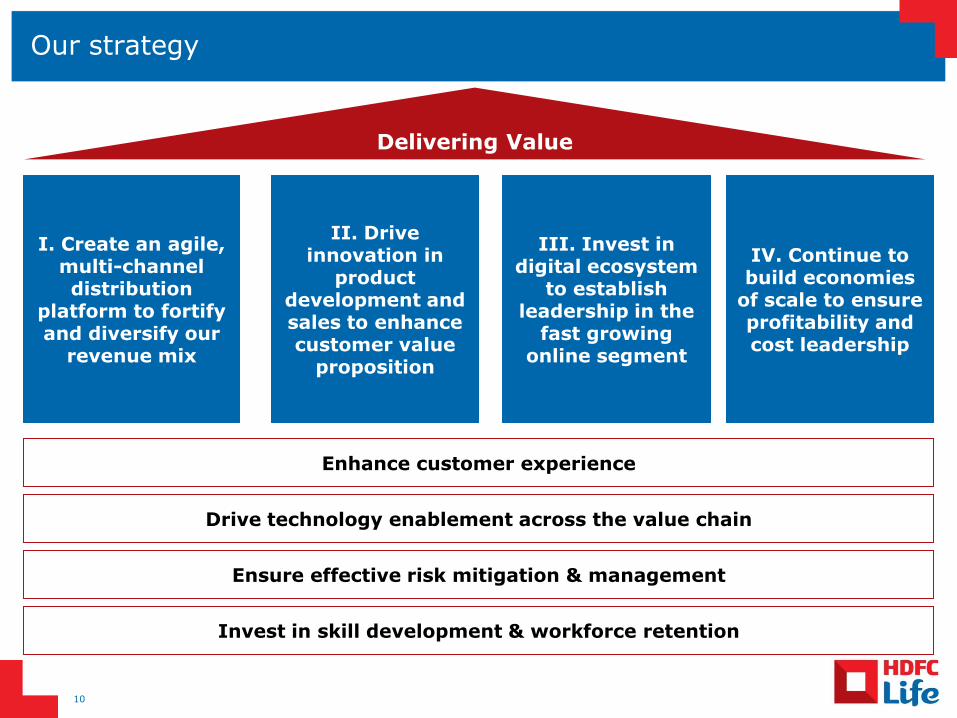

Our strategy

Drive technology enablement across the value chain

I. Create an agile, multi-channel distribution

platform to fortify and diversify our

revenue mix

II. Drive innovation in

product development and sales to enhance customer value

proposition

III. Invest in digital ecosystem

to establish leadership in the

fast growing online segment

IV. Continue to build economies

of scale to ensure profitability and cost leadership

Invest in skill development & workforce retention

Delivering Value

Ensure effective risk mitigation & management

Enhance customer experience

10

This is the sole and exclusive property of HDFC Life. October 26, 2016

Merger Update

11

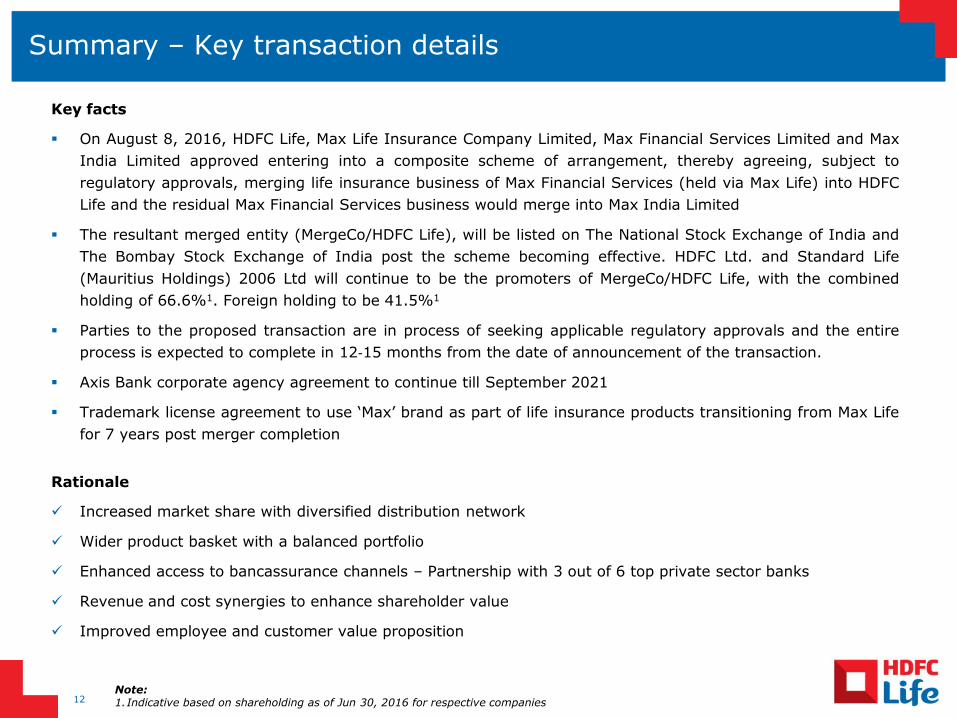

Summary – Key transaction details

12 Note: 1.Indicative based on shareholding as of Jun 30, 2016 for respective companies

Key facts

On August 8, 2016, HDFC Life, Max Life Insurance Company Limited, Max Financial Services Limited and Max

India Limited approved entering into a composite scheme of arrangement, thereby agreeing, subject to

regulatory approvals, merging life insurance business of Max Financial Services (held via Max Life) into HDFC

Life and the residual Max Financial Services business would merge into Max India Limited

The resultant merged entity (MergeCo/HDFC Life), will be listed on The National Stock Exchange of India and

The Bombay Stock Exchange of India post the scheme becoming effective. HDFC Ltd. and Standard Life

(Mauritius Holdings) 2006 Ltd will continue to be the promoters of MergeCo/HDFC Life, with the combined

holding of 66.6%1. Foreign holding to be 41.5%1

Parties to the proposed transaction are in process of seeking applicable regulatory approvals and the entire

process is expected to complete in 12‐15 months from the date of announcement of the transaction.

Axis Bank corporate agency agreement to continue till September 2021

Trademark license agreement to use ‘Max’ brand as part of life insurance products transitioning from Max Life

for 7 years post merger completion

Rationale

Increased market share with diversified distribution network

Wider product basket with a balanced portfolio

Enhanced access to bancassurance channels – Partnership with 3 out of 6 top private sector banks

Revenue and cost synergies to enhance shareholder value

Improved employee and customer value proposition

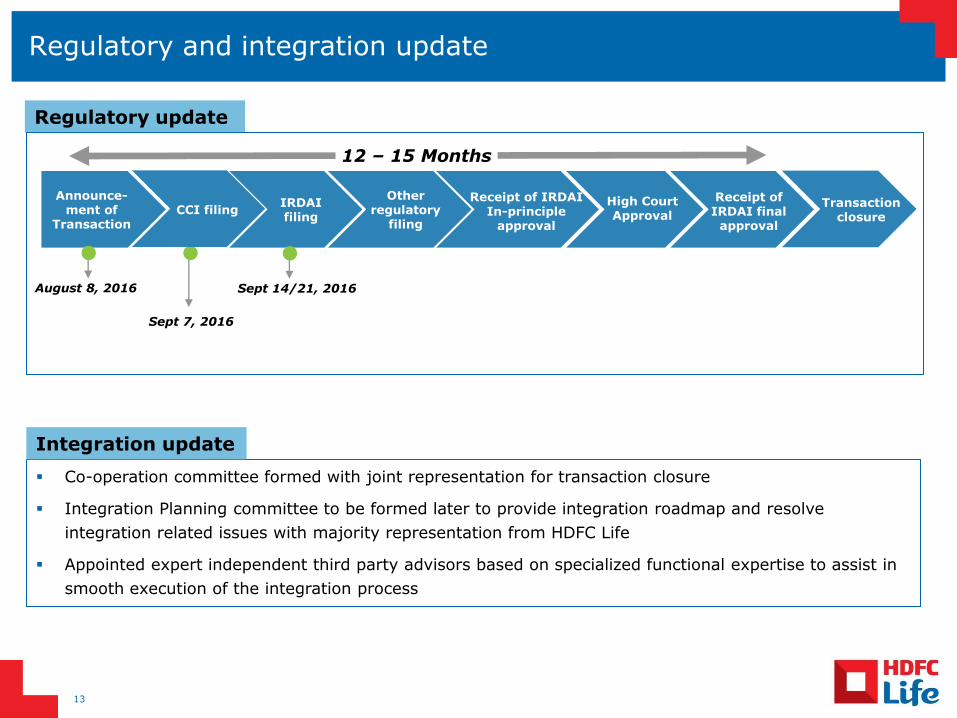

Regulatory and integration update

13

IRDAI filing

Other regulatory

filing

Receipt of IRDAI In-principle

approval

High Court Approval

Receipt of IRDAI final

approval

12 – 15 Months

Sept 7, 2016

Co-operation committee formed with joint representation for transaction closure

Integration Planning committee to be formed later to provide integration roadmap and resolve

integration related issues with majority representation from HDFC Life

Appointed expert independent third party advisors based on specialized functional expertise to assist in

smooth execution of the integration process

Regulatory update

Integration update

Sept 14/21, 2016

CCI filing Announce-

ment of Transaction

Transaction closure

August 8, 2016

This is the sole and exclusive property of HDFC Life. October 26, 2016

Annexures

14

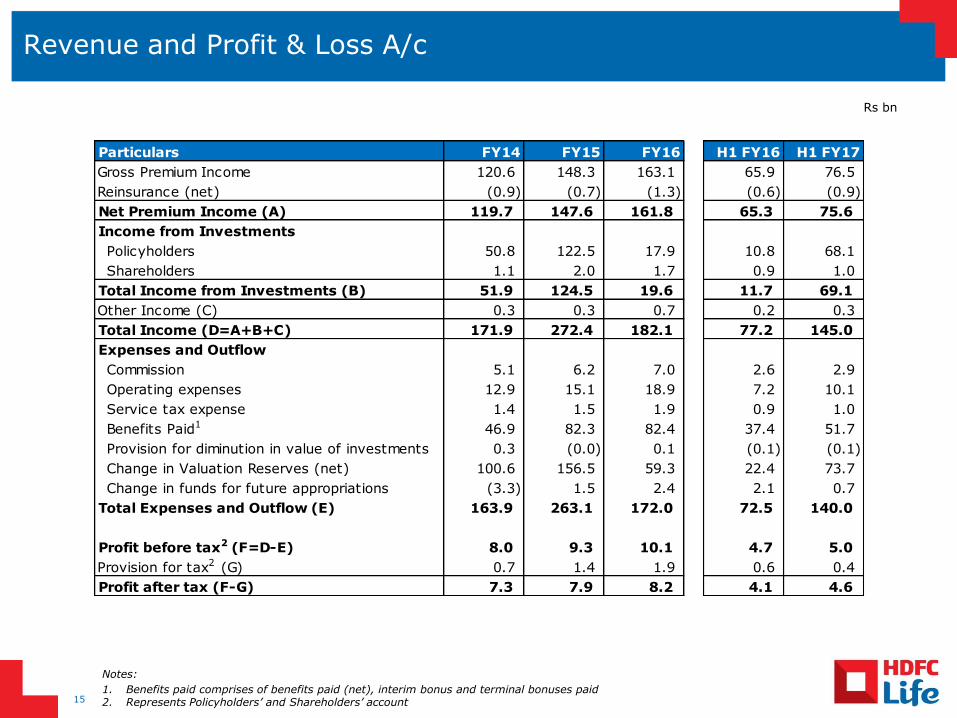

Revenue and Profit & Loss A/c

Notes:

1. Benefits paid comprises of benefits paid (net), interim bonus and terminal bonuses paid 2. Represents Policyholders’ and Shareholders’ account 15

Rs bn

Particulars FY14 FY15 FY16 H1 FY16 H1 FY17

Gross Premium Income 120.6 148.3 163.1 65.9 76.5

Reinsurance (net) (0.9) (0.7) (1.3) (0.6) (0.9)

Net Premium Income (A) 119.7 147.6 161.8 65.3 75.6

Income from Investments

Policyholders 50.8 122.5 17.9 10.8 68.1

Shareholders 1.1 2.0 1.7 0.9 1.0

Total Income from Investments (B) 51.9 124.5 19.6 11.7 69.1

Other Income (C) 0.3 0.3 0.7 0.2 0.3

Total Income (D=A+B+C) 171.9 272.4 182.1 77.2 145.0

Expenses and Outflow

Commission 5.1 6.2 7.0 2.6 2.9

Operating expenses 12.9 15.1 18.9 7.2 10.1

Service tax expense 1.4 1.5 1.9 0.9 1.0

Benefits Paid1 46.9 82.3 82.4 37.4 51.7

Provision for diminution in value of investments 0.3 (0.0) 0.1 (0.1) (0.1)

Change in Valuation Reserves (net) 100.6 156.5 59.3 22.4 73.7

Change in funds for future appropriations (3.3) 1.5 2.4 2.1 0.7

Total Expenses and Outflow (E) 163.9 263.1 172.0 72.5 140.0

Profit before tax2 (F=D-E) 8.0 9.3 10.1 4.7 5.0

Provision for tax2 (G) 0.7 1.4 1.9 0.6 0.4

Profit after tax (F-G) 7.3 7.9 8.2 4.1 4.6

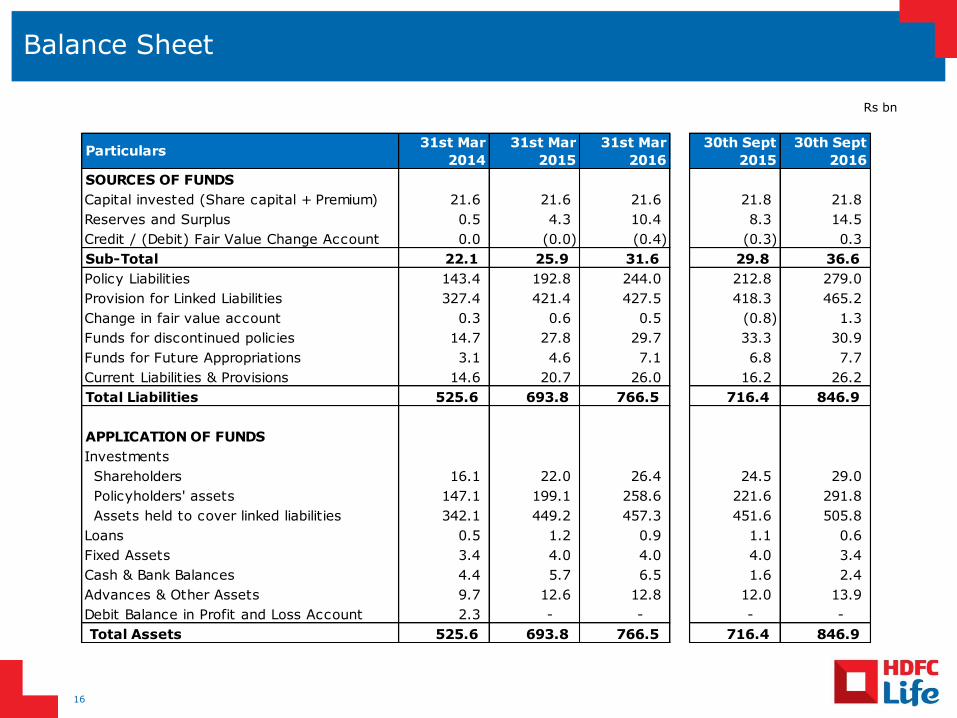

Balance Sheet

16

Particulars31st Mar

2014

31st Mar

2015

31st Mar

2016

30th Sept

2015

30th Sept

2016

SOURCES OF FUNDS

Capital invested (Share capital + Premium) 21.6 21.6 21.6 21.8 21.8

Reserves and Surplus 0.5 4.3 10.4 8.3 14.5

Credit / (Debit) Fair Value Change Account 0.0 (0.0) (0.4) (0.3) 0.3

Sub-Total 22.1 25.9 31.6 29.8 36.6

Policy Liabilities 143.4 192.8 244.0 212.8 279.0

Provision for Linked Liabilities 327.4 421.4 427.5 418.3 465.2

Change in fair value account 0.3 0.6 0.5 (0.8) 1.3

Funds for discontinued policies 14.7 27.8 29.7 33.3 30.9

Funds for Future Appropriations 3.1 4.6 7.1 6.8 7.7

Current Liabilities & Provisions 14.6 20.7 26.0 16.2 26.2

Total Liabilities 525.6 693.8 766.5 716.4 846.9

APPLICATION OF FUNDS

Investments

Shareholders 16.1 22.0 26.4 24.5 29.0

Policyholders' assets 147.1 199.1 258.6 221.6 291.8

Assets held to cover linked liabilities 342.1 449.2 457.3 451.6 505.8

Loans 0.5 1.2 0.9 1.1 0.6

Fixed Assets 3.4 4.0 4.0 4.0 3.4

Cash & Bank Balances 4.4 5.7 6.5 1.6 2.4

Advances & Other Assets 9.7 12.6 12.8 12.0 13.9

Debit Balance in Profit and Loss Account 2.3 - - - -

Total Assets 525.6 693.8 766.5 716.4 846.9

Rs bn

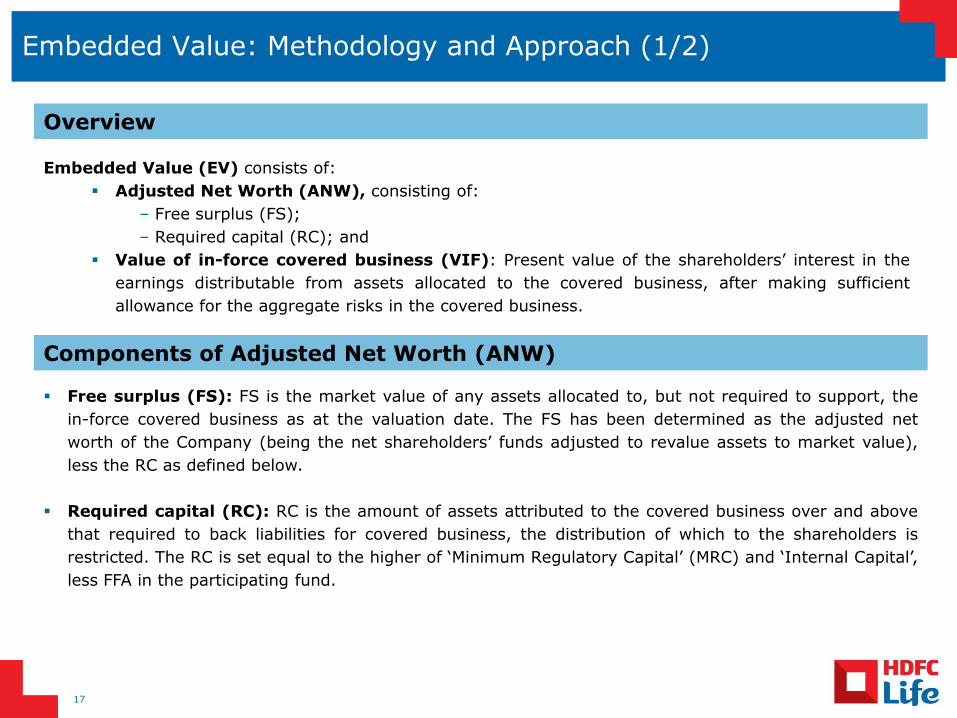

Embedded Value: Methodology and Approach (1/2)

17

Overview

Embedded Value (EV) consists of:

Adjusted Net Worth (ANW), consisting of:

– Free surplus (FS);

– Required capital (RC); and

Value of in-force covered business (VIF): Present value of the shareholders’ interest in the

earnings distributable from assets allocated to the covered business, after making sufficient

allowance for the aggregate risks in the covered business.

Free surplus (FS): FS is the market value of any assets allocated to, but not required to support, the

in-force covered business as at the valuation date. The FS has been determined as the adjusted net

worth of the Company (being the net shareholders’ funds adjusted to revalue assets to market value),

less the RC as defined below.

Required capital (RC): RC is the amount of assets attributed to the covered business over and above

that required to back liabilities for covered business, the distribution of which to the shareholders is

restricted. The RC is set equal to the higher of ‘Minimum Regulatory Capital’ (MRC) and ‘Internal Capital’,

less FFA in the participating fund.

Components of Adjusted Net Worth (ANW)

Embedded Value: Methodology and Approach (2/2)

Present value of future profits (PVFP): PVFP is the present value of projected distributable profits

to shareholders arising from the in-force covered business determined by projecting the shareholder

cash flows from the in-force covered business and the assets backing the associated liabilities.

Time Value of Financial Options and Guarantees (TVFOG): TVFOG reflects the value of the

additional cost to shareholders that may arise from the embedded financial options and guarantees

attaching to the covered business in the event of future adverse market movements. The intrinsic

value of such options and guarantees is reflected in the PVFP.

Frictional costs of required capital (FC): FC represents the investment management expenses and

taxation costs associated with holding the RC. VIF includes an allowance for FC of holding RC for the

covered business. VIF also includes an allowance for FC in respect of the encumbered capital in the

Company’s holdings in its subsidiaries.

Cost of residual non-hedgeable risks (CRNHR): CRNHR is an allowance for risks to shareholder

value to the extent that these are not already allowed for in the TVFOG or the PVFP. In particular, the

CRNHR makes allowance for:

– asymmetries in the impact of the risks on shareholder value; and

– risks that are not allowed for in the TVFOG or the PVFP.

CRNHR has been determined using a cost of capital approach. CRNHR is the present value of the cost

of capital charge levied on the projected capital in respect of the material risks identified.

18

Components of Value in-force covered business (VIF)

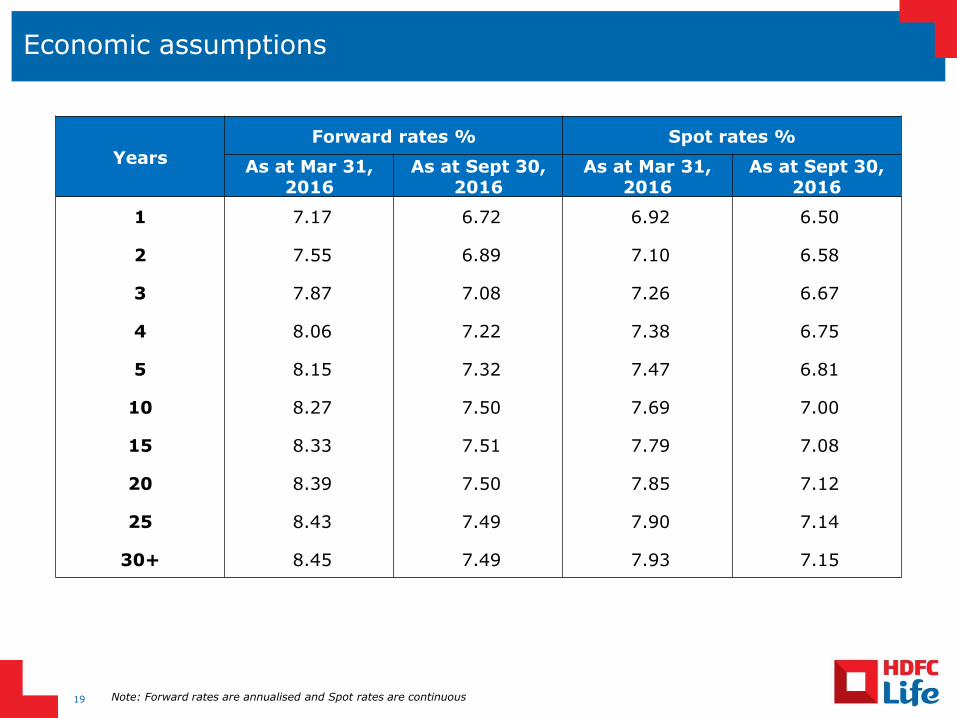

Economic assumptions

Years

Forward rates % Spot rates %

As at Mar 31, 2016

As at Sept 30, 2016

As at Mar 31, 2016

As at Sept 30, 2016

1 7.17 6.72 6.92 6.50

2 7.55 6.89 7.10 6.58

3 7.87 7.08 7.26 6.67

4 8.06 7.22 7.38 6.75

5 8.15 7.32 7.47 6.81

10 8.27 7.50 7.69 7.00

15 8.33 7.51 7.79 7.08

20 8.39 7.50 7.85 7.12

25 8.43 7.49 7.90 7.14

30+ 8.45 7.49 7.93 7.15

19 Note: Forward rates are annualised and Spot rates are continuous

Awards and accolades

20

Indian Insurance Awards for Best innovative

product – Life and Health insurance

DL Shah Award - Platinum Award for Enterprise Mobility Project

Intelligent Enterprise Awards for Mobility

Global Awards for Excellence in Quality Management &

Leadership

Asia BFSI Awards for Best Customer Service Organization

7th Asia's Best Employer Brand Awards was awarded to HDFC Life for 5 different categories

DMA Asia Echo Awards for ‘Memories.HDFCLife.com’ and its

campaign

Best Quality Circle Award for faster claims payout,

promoting GO Green concept and supporting

Digitization

Glossary

APE (Annualized Premium Equivalent) - The sum of annualized first year regular premiums and 10%

weighted single premiums and single premium top-ups

Conservation ratio - Ratio of current year renewal premiums to previous year's renewal premium and

first year premium

First year premiums - Regular premiums received during the year for all modes of payments chosen by

the customer which are still in the first year. For example, for a monthly mode policy sold in March 2016,

the first instalment would fall into first year premiums for 2015-16 and the remaining 11 instalments in

the first year would be first year premiums in 2016-17

New business received premium - The sum of first year premium and single premium.

Operating expense - All expenses of management excluding service tax. It does not include

commission

Operating expense ratio - Ratio of operating expenses (excluding service tax) to total premiums

Renewal premiums - Regular recurring premiums received after the first year

Solvency ratio - Ratio of available solvency margin to required solvency margins

Total premiums - Total received premiums during the year including first year, single and renewal

premiums for individual and group business

Weighted received premium (WRP) - The sum of first year premium and 10% weighted single

premiums and single premium top-ups

13th month persistency - Percentage of contracts measured by premium, still in force, 13 months after

they have been issued, based on reducing balance approach

21

Disclaimer

This presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase any securities (“Securities”) of HDFC Standard Life Insurance Company Limited (“HDFC Life” or the “Company”) in India, the United States, Canada, the People’s Republic of China, Japan or any other jurisdiction. This presentation is not for publication or distribution, directly or indirectly, in or into the United States (including its territories and possessions, any state of the United States and the District of Columbia). The securities of the Company may not be offered or sold in the United States absent registration or an exemption from registration under the U.S. Securities Act of 1933, as amended. The Company does not intend to register any securities in the United States. You confirm that you are either: (i) a “qualified institutional buyer” as defined in Rule 144A under the U.S. Securities Act of 1933, as amended, or (ii) outside the United States. By receiving this presentation, you are agreeing to be bound by the foregoing and below restrictions. Any failure to comply with these restrictions may constitute a violation of applicable securities laws. This presentation should not, nor should anything contained in it, form the basis of, or be relied upon in any connection with any contract or commitment whatsoever. The information contained in this presentation is strictly confidential and is intended solely for your reference and shall not be reproduced (in whole or in part), retransmitted, summarized or distributed to any other persons without Company’s prior written permission. The Company may alter, modify or otherwise change in any manner the contents of this presentation, without obligation to notify a any person of such revision or changes. This presentation may contain forward‐looking statements that involve risks and uncertainties. Forward‐looking statements are based on certain assumptions and expectations of future events. Actual future performance, outcomes and results may differ materially from those expressed in forward‐looking statements as a result of a number of risks, uncertainties and assumptions. Although Company believes that such forward‐looking statements are based on reasonable assumptions, it can give no assurance that such expectations will be met. Representative examples of factors that could affect the accuracy of forward-looking statements include (without limitation) the condition of and changes in India’s political and economic status, government policies, applicable laws, the insurance sector in India, and international and domestic events having a bearing on Company’s business, particularly in regard to the progress of changes in the regulation of the life insurance sector in India, and such other factors beyond our control. You are cautioned not to place undue reliance on these forward-looking statements, which are based on current view of Company’s management on future events. The data herein with respect to HDFC Life is based on a number of assumptions, and is subject to a number of known and unknown risks, which may cause HDFC Life’s actual results or performance to differ materially from any projected future results or performance expressed or implied by such statements. This presentation has been prepared by the Company. No representation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy , completeness or correctness of the information and opinions in this presentation. None of Company or any of its directors, officers, employees, agents or advisers, or any of their respective affiliates, advisers or representatives, undertake to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise and none of them shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation. Further, nothing in this presentation should be construed as constituting legal, business, tax or financial advice or a recommendation regarding the securities.

22

This is the sole and exclusive property of HDFC Life

Thank you