HCMC Quarterly Knowledge Report | Q1 2016

19

HO CHI MINH CITY QUARTERLY KNOWLEDGE REPORT Q1 2016

-

Upload

colliers-international-vietnam -

Category

Real Estate

-

view

421 -

download

1

Transcript of HCMC Quarterly Knowledge Report | Q1 2016

Accelerating successwww.colliers.com/vietnam

HO CHI MINH CITY QUARTERLY KNOWLEDGE REPORT Q1 2016

TABLE OF CONTENTS

ECONOMIC OVERVIEW...............................................................................................................

VIETNAM ....................................................................................................................................

HO CHI MINH CITY ......................................................................................................................

HA NOI ........................................................................................................................................

HO CHI MINH CITY MARKET OVERVIEW ........................................................................ OFFICE ........................................................................................................................................

RETAIL ........................................................................................................................................

CONDOMINIUM ............................................................................................................................

VILLA & TOWNHOUSE .................................................................................................................

SERVICED APARTMENT ..............................................................................................................

INDUSTRIAL ................................................................................................................................

Cover Page: Saigon Skyline

4-5

4

5

5

6-18

6

9

11

13

15

17

Page

LIST OF FIGURES Figure 1: Vietnam GDP .....................................................................................................................

Figure 2: Interest Rate and Exchange Rate of Vietnam ......................................................................

Figure 3: FDI Capital of HCMC and Hanoi ..........................................................................................

Figure 4: GDP Growth Rate of HCMC and Hanoi ................................................................................

HO CHI MINH CITY MARKET OVERVIEW Figure 5: Office, Net Absorption .........................................................................................................

Figure 6: Office, Occupancy Rate .......................................................................................................

Figure 7: Retail, Market Performance...................................................................................................

Figure 8: Retail, Average Asking Rent ................................................................................................

Figure 9: Retail, Supply by District ...................................................................................................

Figure 10: Condominium, Sold Units...................................................................................................

Figure 11: Condominium, Average Asking Rent by Segment ................................................................

Figure 12: Condominium, Q-o-Q and Y-o-Y Changes in Asking Price ..................................................

Figure 13: Villa and Townhouse, Supply by Year .................................................................................

Figure 14: Villa and Townhouse, Current Supply by District ................................................................

Figure 15 Villa and Townhouse, Changes in Asking Price.....................................................................

Figure 16: Serviced Apartment, Current Grade A&B Supply ................................................................

Figure 17: Serviced Apartment, Average Asking Rent by Grade ...........................................................

Figure 18: Industrial, Net Absorption ..................................................................................................

Figure 19: Industrial, Supply by District ..............................................................................................

LIST OF TABLES Table 1: Macroeconomic Indicators of HCMC and Hanoi ......................................................................

Table 2: Office, Future Supply ............................................................................................................

Table 3: Significant Office Projects ....................................................................................................

Table 4: Significant Retail Projects ....................................................................................................

Table 5: Condominium, Significant new Projects launched in Q1 2016 ................................................

Table 6: Villa and Townhouse, Significant new Projects launched in Q1 2016 ......................................

Table 7: Serviced Apartment, Significant Future Projects under construction ......................................

Table 8: Significant Serviced Apartment Projects ...............................................................................

Table 9: Industrial, Future Supply .......................................................................................................

Table 10: Industrial, Market Overview ................................................................................................

4

4

5

5

6

6

9

9

9

11

11

11

13

13

13

15

15

17

17

5

6

7

10

12

14

15

16

17

18

Page

GDPVietnam’s GDP has grown 5.46% in Q1 2016. This was a noticeable reduction from a rate of 6.12% in Q1 2015 but still higher than GDP growth rate of the same periods in 2012, 2013 and 2014. The three main compositions of the GDP which are agriculture–forestry-fishery, industry-construction and services had growth rates of -1.23%, 6.72% and 6.13% y-o-y respectively. Financial, banking and insurance sectors increased slightly over the same period, reaching 5.99%. Real estate trading rose 3.43% y-o-y which achieved the highest growth rate from 2012 to date.

CPIIn Q1 2016, the Consumer Price Index (CPI) increased 1.25% y-o-y while the core CPI grew 1.76% y-o-y. Factors that contributed to the increase in CPI in Q1 2016 were an upward in energy prices on the world market and the El Nino’s impact in Vietnam which cut down the supply and inflated up the price of livestock and agricultural products such as rice or sugarcanes.An increase in health care fees scheduled in July 2016 and school fees scheduled in September 2016 would expectedly push the CPI to increase even higher in the coming quarters.

FDIAs of 20th March, there have been about 473 new foreign investment projects in Vietnam with total registered investment worth USD2.74 billion, an increase of 125.2% y-o-y. In addition, 203 other projects registered to increase its investment by USD1.285 billion, an increase of 107% compared to the same period last year. In total, foreign investment in the first quarter of 2016 reached USD4.02 billion, up 119.1% compared to Q1-2015. Disbursement from FDI projects also grew 14.8% over last year’s period with USD3.5 billion were paid out.

RETAIL SALES Vietnam’s retail sales of goods and services in Q1 2016 achieved USD38.2 billion, a 0.99% increase compared to Q4-2015 and 9.1% y-o-y growth (or 7.9% y-o-y growth if price increase is excluded). The proportions of four main compositions are as follows: retail sales 76.4%, accommodation and catering services 11.3%, travel 0.8% and other services 11.5%. The four sectors all witnessed significant growths compared to last year’s periods, which were 9.2%, 8.5%, 8.8% and 8.9% y-o-y respectively.

INTERNATIONAL ARRIVALS The number of international visitors to Vietnam in Q1 2016 reached 2.459 million, 19.9% increase y-o-y. China and Korea were the two countries which accounted for highest number of visitors to Vietnam in the review period with 580,000 and 408,100 visitors respectively.

EXCHANGE RATEIn contrast to the intense volatility in 2015, the exchange rate USD/VND in the first quarter of 2016 was relatively calm. The exchange rate did not increase as many predicted in 2015, but decreased slightly from VND22,500 to around VND22,382 VND per USD1. The stability of the exchange rate in recent months has been partly contributed by favorable condition on the international financial market.According to forecasts of the International Monetary Fund (IMF), world economic growth trends have been slowed and this would further contribute to the slowing of the Fed’s rate hikes in the coming months. In the next quarters, if the dollar does not rise sharply and the Yuan is not significantly devalued, pressure on the exchange rate USD/USD in 2016 should not be too big.

Q1 2016 | ECONOMIC OVERVIEW

©2016 Colliers International Research

VIETNAM QUARTERLY KNOWLEDGE REPORT

Page 4

Q2 2016 forecast

Figure 1: Vietnam GDP

Source: World Bank | Colliers International Research

Figure 2: Interest rate and Exchage rate of Vietnam

Source: Asian Development Bank (ADB) | Colliers International Research

VIETNAM

0

500

1,000

1,500

2,000

2,500

0

1

2

3

4

5

6

7

8

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1 2016

US

D/c

apita

%

GDP per capita (nominal) GDP growth rate

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

4

5

6

7

8

9

10

11

12

13

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q12016

VND

/USD

% p

er a

nnum

Interst Rate Exchange Rate

Q1 2016 | ECONOMIC OVERVIEW

VIETNAM QUARTERLY KNOWLEDGE REPORT

Q1 2016 | ECONOMIC OVERVIEW

©2016 Colliers International Research

VIETNAM QUARTERLY KNOWLEDGE REPORT

Page 5

Figure 4: GDP Growth Rate of HCMC and Hanoi

Source: General Statistics Office | Colliers International Research

Source: General Statistics Office | Colliers International Research

Table 1: Marcoeconomic Indicators of HCMC and Hanoi

HCMC Hanoi

Q1 2016 Q2 2016F Q1 2016 Q2 2016F

GDP (billion) 9.86 5.33

FDI (million) 275.3 269.6

Retail sales (billion) 7.78 5.29

Export (billion) 6.69 2.56

Import (billion) 7.87 5.72

HO CHI MINH CITYThe Gross Regional Domestic Product (GRDP) of Q1 2016 achieved USD9.9 billion, an increase of 7.1% y-o-y. In more detail, the services sector had the highest growth rate of 7.8%, reaching USD5.7 billion. The industrial and construction sector came second with a growth rate of 6.25%, equivalent to USD2.7 billion. The agriculture-forestry-fishery sector achieved USD79 million, up 5.8% y-o-y.Total newly registered and supplementary FDI reached USD275.3 million. There are 147 new projects worth of USD190.3 million and 36 supplementary projects worth of USD 85 million. The amount of FDI of Q1 2016 significantly decreased, equivalent to 18.5% q-o-q and 49.5% y-o-y. This is a downside for HCMC as in the same period Vietnam witnessed an increase of 125.2% y-o-y in FDI. Three nations with the highest new capital investments are Japan, Singapore and Korea, accounting for 34.4%, 22.3% and 7% of the FDI respectively. Total retail sales of consumer goods and services reached USD7.8 billion, up 11.6% y-o-y. The four compositions, namely retail sales, accommodation & catering, travelling services and other services, accounted for 79.2%, 12.1%, 2.4% and 6.4% of the total sales of goods consequentially. Compared to the same period last year, travelling services had the highest growth rate of 14.4% while accommodation and catering had a slowest growth rate of 6.8%.Consumer Price Index (CPI) had a growth rate of -0.03%, 0.05% and 0.09% from January to March subsequently which pushed the CPI of Q1 2016 to 0.11%. Export values were USD 6.688 billion, equivalent to an increase of 0.1% q-o-q. Import values were USD7.873 billion equivalent to a growth of 8.2% y-o-y. In the previous quarter, the values of export and import were USD363 million and USD417.8 million respectively.

HANOIThe GRDP in Q1-2016 achieved USD5.3 billion which was equivalent to a rise of 6.95% y-o-y. Industrial & construction sector had the highest growth rate of 7.54% which was followed by growth rate of 7.05% y-o-y of services sector. In contrast, Agricultural-forestry-fishery industry suffered a negative growth rate of -0.69% y-o-y.The CPI in January and February climbed to 0.12% and 0.47% m-o-m. The Statistical Office of Hanoi did not publish CPI for March but it was reported to be slightly increased from February level. Compared with the previous quarter, the CPI of the Q1 2016 would be much higher due to increases in prices of energy and agricultural products.The city attracted USD269.6 million of new and supplementary FDI capital in the first quarter of 2016. Total retail sales of consumer goods and services extended 9% y-o-y to achieve USD5.3 billion. Compared with the previous quarter, this was a drop of 11.5%.Export values went up 2.3% y-o-y to achieve USD2.558 billion. Import values were USD5.715 billion which experienced a moderate reduction of -2% y-o-y. This brought about a trade deficit of USD3.157 billion in the review quarter. In Q1 2016, the capital city welcomed 761,000 tourists. This was a remarkable uptrend of 28.7% y-o-y.

Figure 3: FDI Capital of HCMC and Hanoi

Source: General Statistics Office | Colliers International Research

6%

8%

10%

12%

14%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q12016

HCMC Hanoi

0

500

1000

1500

2000

2500

3000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2012 2013 2014 2015 2016

mill

ion

USD

HCMC Hanoi

Figure 6: Office, Occupancy Rate

PERFORMANCERental growth across all grades was recorded in the review quarter. Grade A’s average net asking rents increased 1.92% q-o-q, staying at USD40.5/sqm/month while those of Grade B surged 5.1% q-o-q, reaching USD22.07/sqm/month.

Average occupancy rate witnessed downward trend over the quarter but maintained at a high rate of 93.4%. Grade A and Grade B’s occupied rate were 92.3% and 94.8%, down 3.1% and 1.86% q-o-q respectively.

SUPPLYNo new office building entered the market in the first quarter of 2016. The supply pipeline remained stable with 11 Grade A and 57 Grade B office buildings, providing approximately 1,331,347 sqm GFA.Grade B will domininate new supply in the next quarters with nearly 77,000sqm NLA from 4 projects. Despite having no additional buildings this year, Grade A stock will grow substantially in the next two years. By the end of 2018, the market is expected to welcome 4 more Grade A office buildings which are Deutsches Haus, Saigon Centre (Phase 2), Saigon One Tower and The One, providing nearly 172,859sqm NLA.

DEMANDAs a result of stronger FDI inflow to the city, the growing number of foreign enterprises will continue to drive office demand. This type of tenants would have distinctive enquiries such as green buildings with good access to natural light and energy efficiency, contiguous floor plates of larger than 1,000 sqm, prime locations with accessibility to public transport and staff amenity or close proximity to clients and brand profile. Landlords should be strategic to statisfy sophisticated leasing requirements from clients.

OUTLOOKAs there is a current drought of premium office stock, landlords are gaining confidence in offering higher rents and pushing back incentives. High quality assets are expected to achieve a rent growth up to 10%.

With prime locations and in close proximity of traffic hubs, CBD office buildings continue to be highly sought-after. Decentralised districts with well-established infrastructure and traffic system such as District 7 and Thu Thiem new urban area will become alternative options for tenants looking for large contiguous floor plates.

Q1 2016 | HO CHI MINH CITY | OFFICE

©2016 Colliers International Research

VIETNAM QUARTERLY KNOWLEDGE REPORT

Page 6

Table 2: Office, Future Supply

Source: Colliers International Research

Source: Colliers International Research

Source: Colliers International Research

Figure 5: Office, Net Absorption

-10,000 0 10,000 20,000 30,000 40,000

Q1

Q3

Q1

Q3

Q1

Q3

Q1

2013

2014

2015

20 16

sq m

Grade B Grade A

0

10

20

30

40

50

60

70

80

90

100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2011 2012 2013 2014 2015 2016

Grade A Grade B%

Project name Grade NLA sqm Expected Completion

Hai Quan Tower A 30,000 2016

SGGP Building B 16,940 2016

HQC Royal Tower B 22,500 2016

Deutsches Haus A 24,900 2017

Saigon Center Phase 2 A 40,000 2017

Mapletree Business Center B 30,000 2017

E-Town Central B 34,000 2017

Q1 2016 | HO CHI MINH CITY | OFFICE Q1 2016 | HO CHI MINH CITY | OFFICE

©2016 Colliers International Research

VIETNAM QUARTERLY KNOWLEDGE REPORT

Page 7

(*) US$/sqm/month (NLA)

Table 3: Significant Office Projects

No Name Address Completion Year

NLA (sqm)

Service Charges (*)

Occupancy rate

Average asking rent

(**)1 Saigon Centre 65 Le Loi 1996 11,650 9.0 99% 45.0

2 Saigon Tower 29 Le Duan 1997 13,950 8.0 99% 46.03 Sunwah Tower 115 Nguyen Hue 1997 20,800 8.0 98% 48.04 The Metropolitan 235 Dong Khoi 1997 15,200 8.0 90% 47.05 Diamond Plaza 34 Le Duan 1999 15,936 8.0 77% 45.06 Kumho Asiana Plaza 39 Le Duan 2009 26,000 8.0 89% 43.0

7 Bitexco Financial Tower 45 Ngo Duc Ke 2010 37,710 8.0 96% 34.08 President Place 93 Nguyen Du 2012 8,330 7.0 98% 42.0

9 Times Square 22-36 Nguyen Hue 2012 12,704 7.0 72% 40.010 Le Meridien 3C Ton Duc Thang 2013 9,125 6.0 94% 29.011 Vietcombank Tower 5 Me Linh Square 2015 41,250 7.0 95% 37.0

Grade A 212,655 7.7 92.3% 40.5

1 VTP-OSIC 8 Nguyen Hue 1993 6,500 6.5 98% 25.02 Yo Co Building 41 Nguyen Thi Minh Khai 1995 5,000 3.0 100% 23.03 Somerset Chancellor Court 21-23 NguyenThi Minh Khai 1996 3,200 5.0 100% 22.0

4 Central Plaza 17 Le Duan 1997 6,094 6.5 93% 24.0

5 Harbour View Tower 35 Nguyen Hue 1997 8,000 5.0 77% 20.06 Saigon Riverside Office 2A-4A Ton Duc Thang 1997 10,000 5.0 100% 28.07 Saigon Trade Center 37 Ton Duc Thang 1997 31,416 6.5 71% 24.0

8 MeLinh Point Tower 2 Ngo Duc Ke 1999 17,600 6.0 99% 27.09 Zen Plaza 54-56 Nguyen Trai 2001 11,037 7.0 86% 29.010 Bitexco Building 19-25 Nguyen Hue 2003 6,000 6.0 92% 27.011 The Landmark 5B Ton Duc Thang 2005 8,000 8.0 100% 27.012 Opera View 161-167 Dong Khoi 2006 3,100 7.0 100% 27.013 City Light 45 Vo Thi Sau 2007 10,000 5.0 100% 19.014 Petro Tower 1-5 Le Duan 2007 13,304 9.0 94% 35.015 The Lancaster 22 – 22 Bis Le Thanh Ton 2007 7,000 5.0 90% 25.016 CJ Building 5 Le Thanh Ton 2008 14,000 8.0 97% 29.017 Continential Tower 81-85 Ham Nghi 2008 15,000 6.0 98% 22.018 Havana Tower 132 Ham Nghi 2008 7,326 8.0 81% 31.0

19 Royal Center 235 Nguyen Van Cu 2008 14,320 6.0 100% 23.020 Sailing Tower 51 Nguyen Thi Minh Khai 2008 16,910 6.0 100% 26.0

21 TMS 172 Hai Ba Trung 2009 4,000 4.0 100% 24.022 A&B Tower 76 Le Lai 2010 17,120 6.0 95% 29.023 Bao Viet Tower 233 Dong Khoi 2010 10,650 5.0 100% 22.024 Green Power Tower 35 Ton Duc Thang 2010 15,600 6.0 99% 25.025 Maritime Bank Tower 192 Nguyen Cong Tru 2010 19,596 5.0 84% 22.026 Saigon Royal 91 Pasteur 2010 5,340 6.0 100% 23.027 Vincom Center 68 -70 -72 Le Thanh Ton 2010 56,600 7.0 94% 32.028 Empress Tower 138 Hai Ba Trung 2012 19,538 6.0 100% 30.029 Lim Tower 9-11 Ton Duc Thang 2013 22,000 6.0 99% 28.030 MB Sunny Tower 259 Tran Hung Dao, Co Giang 2013 13,200 6.0 99% 23.031 Lim Tower 2 Vo Van Tan 2015 8,400 5.5 100% 24.0

Grade B 405,851 6.2 93.8% 26.6

Q1 2016 | HO CHI MINH CITY | OFFICE

©2016 Colliers International Research

VIETNAM QUARTERLY KNOWLEDGE REPORT

Page 8

SAIGON SKYLINE REVIEW- CBD HCMC GRADE A OFFICE BUILDINGS

KUMHO ASIANA PLAZA39 Le Duan, District 1

26,000/1,402$ 43.00$ 8.00

DIAMOND PLAZA SAIGON34 Le Duan, District 1

15,936/2,200$ 45.00$ 8.00

LE MERIDIEN 3C Ton Duc Thang, District 1

9,125/NA$ 29.00$6.00

SAIGON TOWER29 Le Duan, District 1

13,950/NA$ 46.00$ 8.00

DEUTSCHES HAUS3-5 Le Van Huu, District 1

THE METROPOLITAN235 Dong Khoi, District 1

15,200/1,000$ 47.00$ 8.00

PRESIDENT PLACE93 Nguyen Du, District 1

8,330/1,000$ 42.00$ 7.00

BITEXCO FINANCIAL TOWER45 Ngo Duc Ke, District 1

37,710/900-1,300$ 34.00$ 8.00

VIETCOMBANK TOWER5 Me Linh Square, District 1

41,250/NA$ 37.00$ 7.00

TIMES SQUARE SAIGON22-36 Nguyen Hue, District 1

12,704/1,450$ 40.00$ 7.00

SAIGON CENTRE65 Le Loi, District 1

11,650/ 1,073$ 45.00$ 9.00

SUNWAH TOWER115 Nguyen Hue, District 1

20,800/ 1,166$ 48.00$ 8.00

Q1 2016 | HO CHI MINH CITY | OFFICE Q1 2016 | HO CHI MINH CITY | RETAIL

©2016 Colliers International Research

VIETNAM QUARTERLY KNOWLEDGE REPORT

Page 9

Figure 9: Retail, Total supply

PERFORMANCELower rental rate in suburban areas resulted in a drop of 2% q-o-q and 10% y-o-y in the average net asking rent across all segments. Department stores and retail podiums maintained their rents while shopping centers was down 3% q-o-q in rents, averaging at USD44/sqm/month.

Average occupancy rate decreased 1.5% q-o-q, staying at 91.6% as some newly-opened retail projects have not fill up their vacant space.

SUPPLYThree new shopping centers in suburban area have come online The retail stock increased 65,400sqm NLA with the opening of two new shopping centers in suburban districts.

Vingroup has made all efforts to expand their retail network in every district in Ho Chi Minh City. While Vincom Le Van Viet marks Vingroup’s first presence in District 9, Vincom Plaza Go Vap is their second retail project in the highly-populated Go Vap District. To date, they have owned 6 retail properties across the city, providing more than 200,000sqm NLA.

DEMANDFood and beverage (F&B) tenants is expected to be the main driver that will support the performance of HCMC’s retail market in the short to medium term.

McDonald, Starbucks, Subway, KFC and Burger King are a few international names that are growing their empires in the local market. These retailers tend to sercure prime locations in a retail center to easily catch the eyes of customers and lower the chance of their competitors.

OUTLOOKThe supply pipeline of shopping malls will grow bigger when Saigon Center Phase II and Aeon Mall Binh Tan will come online in the next quarters of 2016. The two new shopping centers will bring more foreign brands to the local market, creating intense competition between Vietnam and international retailers. Given abundant new supply, low quality retail properties need to be repositioning to avoid downtrend in rents and occupancy rates.

Figure 8: Retail, Average Asking rent

Source: Colliers International Research

Source: Colliers International Research

Figure 7: Retail, Market performance

Source: Colliers International Research

13 21 140

50

100

150

200

250

300

350

Retail Podium Department Store Shopping Centre

US

D/

sq m

/ m

onth

Min average asking rent Max average asking rent

0

10

20

30

40

50

60

70

80

90

100

90%

92%

94%

96%

98%

100%

Podium Department store Shopping centre

USD/

sq m

/mon

th

Average asking rent Average occupancy

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2010 2011 2012 2013 2014 2015 2016YTD

NLA

(sq

m)

Q1 2016 | HO CHI MINH CITY | RETAIL

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 10

Table 3: Significant Office Projects

(*) ARR (Average Rental Rate): All rents are stated in net rents per sqm, inclusive service charge but exculding VAT

Table 4: Significant Retail Projects

No Name of Project/Building Address Location Completion Year

NLA (sq m) ARR (*) Occupancy

Rate1 Hotel Continental Sai Gon 132-134 Dong Khoi District 1 2000 200 90 100.0%2 Caravelle Hotel 19 Lam Son Square District 1 2000 150 220 100.0%3 New World Hotel 76 Le Lai District 1 2000 1,000 60 100.0%4 Sheraton Saigon 88 Dong Khoi District 1 2002 750 200 100.0%5 Opera View Lam Son Square District 1 2006 1,260 200 100.0%6 The Manor 1 91 Nguyen Huu Canh Binh Thanh 2006 2,000 14 83.0%7 Saigon Pearl 92 Nguyen Huu Canh Binh Thanh 2009 5,000 25 100.0%8 Rex Arcade 141 Nguyen Hue District 1 2010 2,000 120 100.0%

9 The Manor 2 91 Nguyen Huu Canh Binh Thanh 2010 2,500 13 92.0%

10 Bitexco Financial Tower 45 Ngo Duc Ke District 1 2011 8,000 55 95.0%11 The Vista Walk Hanoi Highway District 2 2012 10,000 13 80.0%

12 President Place 93 Nguyen Du District 1 2012 800 60 100.0%

13 Times Square 22-36 Nguyen Hue District 1 2012 9,000 300 97.0%14 Saigon Airport Plaza 1 Bach Dang Tan Binh 2013 7,623 15 100.0%

Retail Podium 50,283 87 94.0%

1 Zen Plaza 54-56 Nguyen Trai District 1 2001 6,817 58 100.0%2 Parkson Hung Vuong Plaza 126 Hung Vuong District 5 2007 24,000 60 99.0%3 Kumho Asiana Plaza 35 Le Duan District 1 2009 6,830 60 100.0%4 Parkson Flemington 184 Le Dai Hanh District 11 2009 26,000 25 90.0%5 Parkson Paragon 3 Nguyen Luong Bang District 7 2011 7,500 40 90.0%6 Parkson C.T Plaza 60A Truong Son Tan Binh 2012 12,235 21 95.0%7 Parkson Cantavil Premier Hanoi Highway District 2 2013 17,815 38 97%8 Taka Plaza 102 Nam Ky Khoi Nghia District 1 2011 1,000 70 70.0%

Department Store 102,197 41.0 95.0%

1 Diamond Plaza 34 Le Duan District 1 1999 9,000 90 100.0%2 Parkson Saigontourist Plaza 35 Le Thanh Ton District 1 2002 17,000 90 99.0%3 Saigon Center 35 Nam Ky Khoi Nghia District 1 1996 Renovation Renovation Renovation4 City Plaza 102 Nam Ky Khoi Nghia District 1 2000 Renovation Renovation Renovation5 Superbowl Vietnam TSN 38 Nguyen Hue Tan Binh 2002 5,500 20 98.0%7 An Dong Plaza 18 An Duong Vuong District 5 2004 18,000 40 99.0%8 Saigon Square 1 77-89 Nam Ky Khoi Nghia District 1 2006 1,300 167 100.0%9 Nowzone 235 Nguyen Van Cu District 1 2008 9,000 55 100.0%10 Lotte Mart Saigon South 469 Nguyen Huu Tho District 7 2008 24,000 50 100.0%12 Vincom Center B 72 Le Thanh Ton District 1 2010 45,000 150 100.0%13 Maximark 3/2 Extention 3/2 Street District 10 2010 25,000 35 90.0%14 Lotte Mart Phu Tho Le Dai Hanh District 11 2010 24,500 30 99.0%15 Crescent Mall Nguyen Van Linh District 7 2011 45,000 26 100.0%16 Satra Pham Hung Pham Hung District 8 2011 11,528 14 100.0%17 CMC Plaza 79B Ly Thuong Kiet Tan Binh 2011 Renovation Renovation Renovation18 Union Square Dong Khoi District 1 2012 38,000 300 New opening

Shopping Centre 272,828 96 99.0%

Q1 2016 | HO CHI MINH CITY | RETAIL

VIETNAM QUARTERLY KNOWLEDGE REPORT

Accelerating success

Q1 2016 | HO CHI MINH CITY | CONDOMINIUM

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 11

Table 3: Significant Office Projects

Figure 12: Condominium, Q-o-q and Y-o-y changes in asking price

PERFORMANCEIn the first quarter of 2016, more than 9,000 units were sold across all segments, up 3.43% y-o-y. It is forecasted that throught out 2016, approximately 57,500 units will be available for sale.

High-end and mid-end segments account for more than 70% of the market share. Sale rate of mid-end segment grew 16% y-o-y while affordable segment declined 18.9% y-o-y. In the coming quarters, the market share of high-end segment will see more challenge from mid-end segment.

SUPPLYIn Q1-2016, it is estimated that 12,760 new units were launched for sale. Eastern and Southern areas account for majority of new units supplied.

Condominium market is expected to continually increase both in quantity and quality. Developers nowadays have to take part in intense competitions for potential buyers. Apart from prime location, high-end developers have come up with unique amenities and concept such as cruise habour, waterfall infinity pool, artificial sea or hanging gardens, while mid-end and affordable segments have competitively provided offers such as low construction density as well as associated public services such as internal parks, schools and sport centers.

DEMANDAcross all segments, buyers tend to be more selective in spending their money. Branding of a developer and its ability in assuring a project’s quality and progress are key factors considered by potential buyers.

Units with 1 or 2 bedrooms and price less than USD1,000/sqm are in excessive demand from end-users. Demand for affordable segment seems very high and is predicted to be grown steadily in the future.

OUTLOOKImproved infrastructure provides better connection between areas of the city as well as shorten the distance to the CBD. This helps to increase the demand and the price of projects in outer city areas. In addition, the new Law on Housing which permits foreigners to purchase up to 30% of the total number of apartments in a residential apartment project expects to boost sales further.

Nevertheless, condominium has one of the highest proportions of speculation among different segments of real estate market. It is therefore vulnerable to government policies and credit growth.

Source: Colliers International Research

Figure 10: Condominium, Sold units

Source: Colliers International Research

Source: Colliers International Research

Figure 11: Condominium, Average asking price by segment

0

5000

10000

15000

20000

25000

30000

35000

40000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q12016

units

0

1,000

2,000

3,000

4,000

5,000

Luxury High-end Mid-end Affordable

US

$/sq

mAverage primary price Average secondary price

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Primary market Secondary market

q-o-q changes y-o-y changes

Accelerating success

Q1 2016 | HO CHI MINH CITY | CONDOMINIUM

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 12

Table 5: Condominium, Significant new projects launched in Q1 2016

No Name of Project/Building Developer Location Completion Year

Number of units

Asking Price (US$/sqm)

1 9 view Apartment Hung Thinh District 9 2018 690 7202 M-One Nam Saigon Thao Dien Investment District 7 2017 963 1,1003 Vinhomes Park Paroma VinGroup Binh Thanh 2017 430 1,9004 Opal Riverside Dat Xanh Group Thu Duc 2017 626 9705 Dat Gia Residence Dat Gia Real Estate Thu Duc 2017 1,034 8006 Vinhomes Golden River Bason VinGroup District 1 2018 3,000 4,000-5,0007 Vinhomes Central Park - P7 VinGroup Binh Thanh 2017 893 1,600-1,8008 Samland Riverside Sacomreal Binh Thanh 2018 138 1,3009 Sunriver Usilk TGT District 7 2017 136 1,10010 De Capella Quoc Cuong Gia Lai District 2 2018 380 1,40011 The Avila Thai Bao District 8 2017 285 70012 Xi Grand Court Phu Son Thuan District 10 2017 748 1,40013 Kris Vue CapitaLand District 2 2018 128 1,30014 Viva Riverside Vietcomreal District 6 2018 567 1,20015 Scenic Valley 2 Phu My Hung District 7 2017 248 1,50016 Luxury Home Sacomreal District 7 2018 250 1,00017 Top Life TIEXIM District 10 2018 84 2,20018 Sarina Dai Quang Minh District 2 2016 233 1,75019 Madison NovaLand District 1 2018 109 5,000-6,000

20 Hung Phat Golden Star Hung Loc Phat District 7 2018 478 1,300

21 I-Home Xa Lo Ha Noi C.T Group District 9 2017 431 70022 Botanica Premier NovaLand Tan Binh 2018 909 1,600

New launches in Q1 2016 12,760

* Excluding all kinds of tax, promotions and management feeThe information is updated as at the end of Q1 2016

Q1 2016 | HO CHI MINH CITY | CONDOMINIUM

Accelerating success

Q1 2016 | HO CHI MINH CITY | VILLA & TOWNHOUSE

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 13

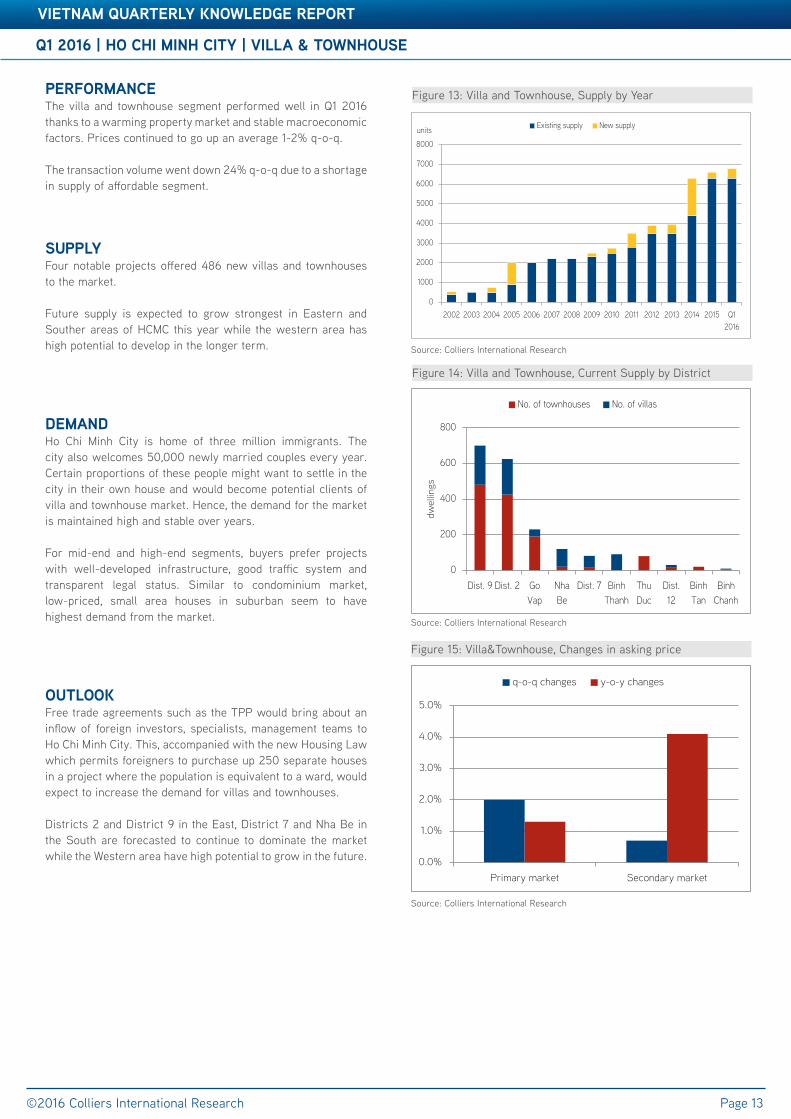

PERFORMANCEThe villa and townhouse segment performed well in Q1 2016 thanks to a warming property market and stable macroeconomic factors. Prices continued to go up an average 1-2% q-o-q.

The transaction volume went down 24% q-o-q due to a shortage in supply of affordable segment.

SUPPLYFour notable projects offered 486 new villas and townhouses to the market.

Future supply is expected to grow strongest in Eastern and Souther areas of HCMC this year while the western area has high potential to develop in the longer term.

DEMANDHo Chi Minh City is home of three million immigrants. The city also welcomes 50,000 newly married couples every year. Certain proportions of these people might want to settle in the city in their own house and would become potential clients of villa and townhouse market. Hence, the demand for the market is maintained high and stable over years.

For mid-end and high-end segments, buyers prefer projects with well-developed infrastructure, good traffic system and transparent legal status. Similar to condominium market, low-priced, small area houses in suburban seem to have highest demand from the market.

OUTLOOKFree trade agreements such as the TPP would bring about an inflow of foreign investors, specialists, management teams to Ho Chi Minh City. This, accompanied with the new Housing Law which permits foreigners to purchase up 250 separate houses in a project where the population is equivalent to a ward, would expect to increase the demand for villas and townhouses.

Districts 2 and District 9 in the East, District 7 and Nha Be in the South are forecasted to continue to dominate the market while the Western area have high potential to grow in the future.

Figure 13: Villa and Townhouse, Supply by Year

Source: Colliers International Research

Figure 14: Villa and Townhouse, Current Supply by District

Source: Colliers International Research

Figure 15: Villa&Townhouse, Changes in asking price

Source: Colliers International Research

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Primary market Secondary market

q-o-q changes y-o-y changes

0

200

400

600

800

Dist. 9 Dist. 2 GoVap

NhaBe

Dist. 7 BinhThanh

ThuDuc

Dist.12

BinhTan

BinhChanh

dwel

lings

No. of townhouses No. of villas

0

1000

2000

3000

4000

5000

6000

7000

8000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q12016

Existing supply New supplyunits

Accelerating success

Q1 2016 | HO CHI MINH CITY | VILLA & TOWNHOUSE

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 14

Table 6: Villa and Townhouse, Significant new projects launched in Q1 2016

No Name of Project/Building Developer Location Completion Year

Number of units

Asking Price (US$/sqm)

1 The Manera Khang Dien Tu Van Quoc Te District 9 N/A 54 1,8002 Saroma Villa Dai Quang Minh District 2 2016 177 N/A3 The Venica Khang Dien District 9 2016 43 500-1,5004 Camelia Gardern Nam Long Group Binh Chanh 2016 212 1,282-1,851

New launches in Q1 2016 486

Q1 2016 | HO CHI MINH CITY | VILLA & TOWNHOUSE

Accelerating success

Q1 2016 | HO CHI MINH CITY | SERVICED APARTMENT

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 15

PERFORMANCEGrade A’s average occupancy rate remained unchanged over the quarter, reaching 86.4%. The average gross asking rent recorded a drop of 2.61ppts q-o-q, staying at USD29.9/sqm/month.

Grade B had the best performance in the review quarter. Average occupancy rate increased to 88.2%, up 0.45ppts while rental rate saw an improvement of 1.35ppts, averaging at USD22.4/sqm/month.

SUPPLYThe existing stock was stable with approximately 4,100 units from 80 projects. Due to well-establised public facilities and amenities, the CBD is home of more than 40% of total serviced apartments.

New supply from now until end of 2017 will grow substantially with approximately 1,459 units. It is notable that five out of seven significant future projects is located in District 1 and District 3. To meet current demand from single tenants, the proportion of one-bedroom and two-bedroom units tend to be increased in newly launched developments.

DEMANDServiced apartments in the CBD are typically preferred by professional singles due to its close proximity to their workplace.

District 2 and District 7 are attractive for expatriate families as these two locations can provide large size accommodation together with social amenities such as international schools, hospitals, shopping malls, etc. It is observed that District 2 with peaceful riverside environment is popular for Westerners while District 7 is a hot spot for Asian community.

OUTLOOKDemand for serviced apartments will be strengthen in the long term after Vietnam joined Trans Pacific Partnership and Asean Economic Community, leading to the growing number of foreign workforce. Despite solid demand, this market segment have to compete with buy-to-let apartments and private houses where offering competitive rents for long-term stays.

To maintain healthy occupancy rates, landlords need to adjust rents and consolidate their services when new completions enter the market expatriates and MNCs.

Project name District Grade Total units

Expected Completion

Sila Urban Living 3 B 217 2Q 2016

Ascott Waterfront Saigon 1 A 222 3Q 2016

Saigon Plaza 1 B 119 4Q 2016

New Pearl 3 B 120 4Q 2016

Saigon South Place 7 A 480 2017

Saigon Center Phase 2 1 A 216 2017

Berkley Service Residence 2 B 85 2017

Table 7: Serviced apartment, Significant future projects under construction

Source: Colliers International Research

Figure 16: Serviced Apartment, Current grade A&B supply

Source: Colliers International Research

Figure 17: Serviced Apartment, Average asking rent by grade

Source: Colliers International Research

0

1,000

2,000

3,000

4,000

2010 2011 2012 2013 2014 2015 Q1 2016

units

Grade A Grade B

15

20

25

30

35

2010 2011 2012 2013 2014 2015 Q1 2016

US$

/sqm

/mon

thGrade A Grade B

Accelerating success

Q1 2016 | HO CHI MINH CITY | SERVICED APARTMENT

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 16

Table 8: Significant Serviced Apartment Projects

No. Project Name Address Location Completion Year

Total Room

Average Occupancy

ARR(*) (**)

1 The Landmark 5B Ton Duc Thang District 1 1995 66 95.0% 262 Sedona Suites 65 Le Loi District 1 1996 89 89.0% 30

3 Somerset Chancellor Court 21-23 Nguyen Thi Minh Khai District 1 1996 172 96.0% 34

4 Nguyen Du Park Villas 111 Nguyen Du District 1 2004 41 98.0% 305 The Lancaster 22-22 Bis Le Thanh Ton District 1 2007 55 73.0% 376 Intercontinental Asian Saigon 39 Le Duan District 1 2009 260 95.0% 36

Grade A 683 92.9% 33.5

1 Norfork Mansion 17-21 Ly Tu Trong District 1 1998 126 85.0% 262 Saigon Sky Garden 20 Le Thanh Ton District 1 1998 154 85.0% 263 Somerset HCM 8A Nguyen Binh Khiem District 1 1998 165 94.0% 264 Diamond Plaza 34 Le Duan District 1 1999 42 95.0% 295 Garden View Court 101 Nguyen Du District 1 2000 76 91.0% 316 Ben Thanh Luxury 172-174 Ky Con District 1 2010 88 91.0% 18

7 Lafayette De SaiGon 8 Phung Khac Khoan District 1 2010 18 89.0% 28

8 Vincom Center 45A Ly Tu Trong District 1 2010 60 34.0% 26

9 Nikko Saigon 235 Nguyen Van Cu District 1 2011 54 100.0% 30

10 Saigon City Residence 8A/3D2 Thai Van Lung District 1 2011 17 84.0% 23

11 Spring Court 1Bis Phung Khac Khoan District 1 2011 14 76.0% 23

Grade B 814 85.7% 25.9

(*) US/sqm/month(**) ARR (Average Rental Rate): All rents are stated in gross rents per sqm, not including VAT and serviced charge

©2016 Colliers International Research

Q1 2016 | HO CHI MINH CITY | SERVICED APARTMENT

VIETNAM QUARTERLY KNOWLEDGE REPORT

Accelerating success

Q1 2016 | HO CHI MINH CITY | INDUSTRIAL

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 17

PERFORMANCEIn Q1 2016, the average rent of industrial parks (IPs) in HCM City was USD122/sqm/term and the average land use right term was 35.7 years. IPs in Cu Chi district have the lowest rents, averaging at USD50-USD60/sqm/term. On the contrary, IPs in Tan Binh District and District 7 have highest asking rents of, up to USD220-USD270/sqm/term. In general, rents in HCMC are currently more than double compared to those in the Southern Key Economic Region such as Binh Duong, Dong Nai, Long An, Vung Tau. The average occupancy rate was 68%, stable over the quarter. About two-thirds of IPs enjoyed above 90% occupancy rates due to its convenient location and efficient services. Common offers for ready-built factories were USD2.5-USD4/sqm/month (exclusive of VAT and service charge) with a minimum area from 1,000-5,000sqm.

SUPPLYIn the first three months of 2016, there is no new supply of IPS. The total areas of IPs in HCMC are over 3,900ha of which the leasable areas are over 2,700ha. By 2020, the total supply of industrial zones is estimated to rise to above 6,500 ha, up to 67% compared to the current supply. However, there is an uncertainty on the construction progress of some industrial parks.

DEMANDInflows of Foreign direct investment (FDI) to Export Processing Zones (EPZs) and industrial parks (IPs) in Ho Chi Minh City plummeted 69.5% year-on-year to USD116 million in the first three months of 2016.As of the end of March 2016, domestic and foreign firms registered to invest in 1,390 projects with accumulated capital of USD9.17 billion in HCM City’ EZs and IPs of which foreign-owned-enterprises accounted for 554 projects and USD5.42 billion.Meanwhile, domestic companies pledged to invest nearly USD80.4 million in EZs and IPs in the first quarter of 2016, representing an 80% y-o-y increase.Companies from non-TPP member nations such as China, Korea, India would relocate their operations and factories to Vietnam in order to benefit from tax incentives for their products. Foreign investors, especially from the U.S and Japan, will also flow into Vietnam more heavily to take advantage of Vietnam’s abundant labor force and a 90-million consumers market. These factors positively contribute to the demand for industrial real estates.

OUTLOOKRents and occupancy rates are likely to go up in the coming quarters as the inflows of FDI and the expansion of production in preparation for the TPP and other FTAs are expected to continue.The number of industrial areas is still being expanded. However, the majority of future projects are in the process of site clearance and compensation and hence construction process is expected to be prolonged. Le Minh Xuan 2, Le Minh Xuan 3, Vinh Loc 3, Hiep Phuoc phase 2 are among those that are on track to be in operation soon.

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research

Figure 18: Industrial, Net absorption

Source: Colliers International Research

Figure 19: Industrial, Supply by District

Source: Colliers International Research

Source: Colliers International Research

Table 9: Industrial, Future Supply

Industrial Park Name District GFA (ha)

Le Minh Xuan Industrial Park - phase 3 Binh Chanh 242

Tay Bac Cu Chi Industrial Park - phase 2 Cu Chi 173

Hiep Phuoc Industrial Park - phase 2 Nha Be 597

0

10

20

30

40

50

60

70

80

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2012 2013 2014 2015 2016

ha

Dist. 922%

Cu Chi23%

Binh Chanh16%

Binh Tan10%

Dist. 78%

Nha Be8%

Others13%

Q1 2016 | HO CHI MINH CITY | INDUSTRIAL

VIETNAM QUARTERLY KNOWLEDGE REPORT

©2016 Colliers International Research Page 18

Table 3: Significant Office ProjectsTable 10: HCMC Industrial Market Overview

No Name of Industrial Park Location Distance to CBD (km)

Total Area(ha)

Total leasable area (ha)

Asking Rent (US$/sqm/

term)Occupancy LUR Term

1 Linh Trung 1 Export Processing Zone Thu Duc 18 62 46 60 100% 20422 Linh Trung 2 Export Processing Zone Thu Duc 17 62 44 60 99% 20503 Binh Chieu Industrial Park Thu Duc 16 27 27 150 100% 20464 Saigon Hi-tech Park P1 District 9 15 300 300 60 100% 20525 Tay Bac Cu Chi Industrial Park Cu Chi 36.5 208 150 90 99% 20476 Tan Thoi Hiep Industrial Park District 12 16 28 20 100 100% 20497 Tan Phu Trung Industrial Park Cu Chi 37 543 359 73 28% 20548 Tan Thuan Export Processing Zone District 7 6.4 300 205 260 81% 20419 Hiep Phuoc Industrial Park 1 Nha Be 21 331 224 100 93% 204810 Hiep Phuoc Industrial Park 2 Nha Be 22 597 345 100 10% 205811 Tan Tao Industrial Park 1 Binh Tan 17 161 97 251 97% 204712 Tan Tao Industrial Park 2 Binh Tan 17 183 116 251 78% 205013 Tan Binh Industrial Park Tan Binh 11 129 100 235 100% 204714 Le Minh Xuan Industrial Park Binh Chanh 20 100 66 100 95% 204715 Vinh Loc Industrial Park Binh Chanh 15 203 131 270 95% 204716 Dong Nam Industrial Park Cu Chi 30 343 287 63 69% 205817 An Ha Industrial Park Binh Chanh 23 124 124 64 23% 205818 Cat Lai Industrial Park District 2 21 137 87 90 100% 206119 Automotive - Mechanical (Hoa Phu) Cu Chi 40 99 67 56 83% 2057

Total 3,937 2,795 122 68%

Q1 2016 | HO CHI MINH CITY | INDUSTRIAL

VIETNAM QUARTERLY KNOWLEDGE REPORT

COLLIERS INTERNATIONAL | VIETNAM

HO CHI MINH CITYBitexco Office Building, 7th Floor19-25 Nguyen Hue StreetDistrict 1, HCM City, VietnamTel: + 84 8 3827 5665

HANOIPress Club Building, 4th Floor59A Ly Thai To Street, Hoan Kiem District, Hanoi, VietnamTel: +84 8 3827 5665

502 offices in67 countries on6 continents

Accelerating success

DAVID JACKSONGeneral Director

+84 8 3827 5665

About Colliers InternationalColliers International is a leader in global real estate services, defined by our spirit of enterprise.

Through a culture of service excellence and a shared sense of initiative, we integrate the resources of real estate specialists worldwide to accelerate the success of our partners.We connect through a shared set of values that shape a collaborative environment throughout our organization that is unsurpassed in the industry.

With more than 100 professionals in 2 offices in Vietnam, the team is market driven and has proven and successful track record with both international and local experience.

From Hanoi to Ho Chi Minh City, we provide a full range of real estate services

The foundation of our services is the strength and depth of our experience.

Publication Coverage Frequency Content Availability

Knowledge Report/Market Insights

Vietnam Cities Quarterly All market sectors Publicly available

Investment report Vietnam Quarterly Economic updates and Investment highlights

Publicly available

CBD Report HCMC CBD Monthly Office, Retail, Hotel and Serviced Apartment

Publicly available

Residential launch update

HCMC Monthly Residential Publicly available

Asia Pacific Office Report

Asia Pacificincluding Vietnam

Quarterly Office market Publicly available

Vietnam Property Market Report

Vietnam cities Quarterly All market sectors On subscription

Development Recommendation

Vietnam cities At request All market sectors On subscription

$2.30billion in annual revenue

1.7billion square feet under management

16,300professionalsand staff

This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. Any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. This publication is the copyrighted property of Colliers International and/or its licensor(s). ©2016. All rights reserved.

For further information, please contact us:

VIETNAM | RESEARCH & FORECAST REPORT

©2016 Colliers International Research www.colliers.com/vietnam

HA VOResearch Manager

+84 8 3827 5665