HALYK FINANCE Weekly

17

1 WEEKLY UPDATE May 16, 2011 900 1100 1300 1500 1700 1900 2100 2300 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 KASE index Economics 1Q2011 GDP: a stronger consumer demand 2 Labor market overheating 4 Credit in 1Q: demand on the rise, but quality borrowers are scarce 4 Banks BTA equity still negative despite $6.7bn profit 5 Oil & Gas KMG EP withdraws Iraqi bid 6 Max Petroleum continues exploration 6 Tethys updates on Kazakh activities, reports 1Q2011 results 6 Global Markets 8 International bonds 11 Domestic bonds 12 KASE 15 International Stock Exchanges 16 144.00 145.00 146.00 147.00 148.00 149.00 150.00 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 KZT/USD 60 70 80 90 100 110 120 130 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Brent oil 1000 1100 1200 1300 1400 1500 1600 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Gold spot

Transcript of HALYK FINANCE Weekly

Halyk Finance Weekly Update May 16, 2011

1

WEEKLY UPDATE

May 16, 2011

900

1100

1300

1500

1700

1900

2100

2300

May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11

KASE index

Economics

1Q2011 GDP: a stronger consumer demand 2

Labor market overheating 4

Credit in 1Q: demand on the rise, but quality borrowers are scarce 4

Banks

BTA equity still negative despite $6.7bn profit 5

Oil & Gas

KMG EP withdraws Iraqi bid 6

Max Petroleum continues exploration 6

Tethys updates on Kazakh activities, reports 1Q2011 results 6

Global Markets 8

International bonds 11

Domestic bonds 12

KASE 15

International Stock Exchanges 16

144.00

145.00

146.00

147.00

148.00

149.00

150.00

May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11

KZT/USD

60

70

80

90

100

110

120

130

May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11

Brent oil

1000

1100

1200

1300

1400

1500

1600

May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11

Gold spot

Halyk Finance Weekly Update May 16, 2011

2

Economics

1Q2011 GDP: a stronger consumer demand

According to SARK’s preliminary estimates, 1Q11 GDP rose by 6.6% YoY due to a boost in trade, consumer services, and industrial production. Financial services and construction remain depressed. GDP deflator rose by 14.6% YoY on the back of higher commodity prices, utility tariffs and wages in services and public sector.

In seasonally adjusted terms, after a 4.5% QoQ sa surge in the previous quarter, 1Q GDP is almost unchanged (see Table 1). The growth in consumer sectors, such as telecom, trade and hotels and restaurants, was offset by QoQ declines in industrial production, construction, and transportation Financial services rose QoQ, but remained subdued, as lending is still tight amid borrowers’ quality problems and high NPLs (see our note on Credit market in 1Q in this Weekly for more detail). Public sector, which represents around 8% of GDP, continued to rise steadily. Net taxes added 2.5 QoQ sa, exceeding the GDP growth rate.

We maintain our GDP growth forecast unchanged at 6% YoY for 2011, which, we believe, will be driven by (1) export demand that will support growth of industrial production and transportation of

commodities; and (2) consumer demand that will benefit from rising wages and employment and will have a positive impact on trade, food production, telecom and other consumer services (see Signs of overheating in labor market in this Weekly).

Table 1. Preliminary 1Q2011 GDP statistics

Growth, YoY

Growth, QoQ sa

Deflator, YoY %GDP

Agriculture 1.8 4.9 25.6 2.3

Industry 6.0 -1.9 12.8 33.9

Construction 3.1 -3.2 5.1 4.7

Trade 14.3 5.8 4.8 13.0

Hotels and restaurants 10.8 3.0 12.4 1.1

Transport 6.9 -19.8 9.5 6.9

Telecom 14.6 11.0 -11.6 2.3

Financial activity -1.9 8.5 27.7 3.8

Real estate and services to business, incl: 1.8 -3.2 17.9 17.2

Real estate transactions 0.5 n/a 17.5 9.2

Professional, scientific and technical activity 3.7 n/a 23.2 5.6

Administrative services and consulting 2.8 n/a 6.8 2.4

Government administration 0.9 3.7 13.5 1.8

Education 4.6 1.3 23.4 3.9

Healthcare 5.0 1.7 25.4 2.1

FISIM -10.4 -47.6 117.6 -2.7

Net taxes 10.5 2.6 83.8 8.2

Gross domestic product 6.6 0.1 14.6 100.0

Source: SARK, HF estimates

Figure 1. IP and transportation declined in 1Q Figure 2. Consumer services rose sharply in 1Q

80

90

100

110

120

130

140

150

160

170

2005Q

1

2005Q

3

2006Q

1

2006Q

3

2007Q

1

2007Q

3

2008Q

1

2008Q

3

2009Q

1

2009Q

3

2010Q

1

2010Q

3

2011Q

1

Industry, sa Transport, sa Agriculture, sa

80

100

120

140

160

180

200

220

240

260

280

2005Q

1

2005Q

3

2006Q

1

2006Q

3

2007Q

1

2007Q

3

2008Q

1

2008Q

3

2009Q

1

2009Q

3

2010Q

1

2010Q

3

2011Q

1

Trade, saTelecom, saHotels and restaurants, sa

Source: SARK, HF estimates Source: SARK, HF estimates

Halyk Finance Weekly Update May 16, 2011

3

Figure 3. Public sector VA grows steadily Figure 4. Construction and financial sector are still depressed

95

100

105

110

115

120

125

1302005Q

1

2005Q

3

2006Q

1

2006Q

3

2007Q

1

2007Q

3

2008Q

1

2008Q

3

2009Q

1

2009Q

3

2010Q

1

2010Q

3

2011Q

1

Education, saGovernment administration, saHealthcare, sa

95

145

195

245

295

345

395

2005Q

1

2005Q

3

2006Q

1

2006Q

3

2007Q

1

2007Q

3

2008Q

1

2008Q

3

2009Q

1

2009Q

3

2010Q

1

2010Q

3

2011Q

1

Construction, sa Financial activity, saFISIM, sa

Source: SARK, HF estimates Source: SARK, HF estimates

Figure 5. Real GDP

80

100

120

140

160

180

200

2005Q

1

2005Q

3

2006Q

1

2006Q

3

2007Q

1

2007Q

3

2008Q

1

2008Q

3

2009Q

1

2009Q

3

2010Q

1

2010Q

3

2011Q

1

Index

RGDP RGDP, sa

Source: SARK, HF estimates

Madina Kurmangaliyeva

Halyk Finance Weekly Update May 16, 2011

4

Labor market overheating

According to the latest statistics on labor market, March wages reached T87.5 th (+21% YoY). Seasonally adjusted, wage growth accelerated to 3.6% MoM sa due to a surge in industrial wages (+13% MoM). Wages rose in almost all sectors, except for public sector (where they government promised a 30% raise in July) and construction. Employment continued its steady rise (+1.3% YoY in March), unemployment remained low at 5.5%.

We expect high revenues of the oil sector, upturn in consumer demand and the further rise in fiscal social spending to support these trends throughout 2011. Real wages growth is expected to stay at

around 7-8% YoY in 2011, with the average wage rising from T77,500 in 2010 to T91,000.

Figure 1. Average monthly wage, seasonally adjusted

40

50

60

70

80

90

100

110

120

Jan-0

8

Apr-

08

Jul-

08

Oct-

08

Jan-0

9

Apr-

09

Jul-

09

Oct-

09

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

KZT th

Average monthly wage, sa Wage in industry, sa

Source: SARK, HF estimates

Madina Kurmangaliyeva

Credit in 1Q: demand on the rise, but quality borrowers are scarce

Last week’s results of NBK 1Q2011 credit market survey may signal the beginning of a recovery. The

survey showed that in 1Q2011:

- Demand for corporate and consumer loans has risen, while demand for mortgage loans continued to lag,

- Despite higher demand, new lending remained low as quality borrowers are hard to find,

- Thanks to foreign-owned banks, competition for good credit risk has intensified leading to lower interest rates, longer terms and bigger loans,

- In the corporate sector, banks prefer to finance working capital needs, while limiting the financing of

ongoing investment projects and avoiding loans to start-ups,

- In retail lending, banks limit lending issued without income verification,

- New equity, local and foreign debt became more accessible.

Banks expect these trends to continue in 2Q11 with further softening of credit requirements and higher demand for loans.

Madina Kurmangaliyeva

Halyk Finance Weekly Update May 16, 2011

5

Banks

BTA equity still negative despite $6.7bn profit

On May 13, BTA bank published its 2010 audited results, posting a net profit of T986.3bn ($6.7bn) profit that led to a 16-fold reduction in the capital deficit over the year (from T1.7 trillion to T104.5bn). The 2010 profit is largely attributable to income from restructuring of the bank's bond debt, which amounted to T853.9bn ($5.8bn).

Following 2010 debt restructuring at BTA (T1.7 trillion), Alliance bank (T734.2bn) and Temirbank (T154.9bn), the government controlled 70-80% in each of the three banks. With similar credit quality, the yields on these banks’ debt securities moved in sync (see Figure 1.)

The BTA’s 2010 result is much better than the losses of T1.2 trillion and T1.1 trillion reported in 2008 and 2009, respectively. However, quality of the bank’s earnings is still poor. In 2010, BTA received only 54.2% of the accrued interest (T196.9bn) in cash, while Alliance bank received 85.1% of its accrued interest (T44.4bn) in cash. Additionally, according to the local financial regulator data, the difference

between provisions and NPLs as % of gross loans is greater for BTA than for Alliance bank (10.1% vs.

5.1%). These differences in earnings of the two banks led to the recently formed gap in their yields (see Figure 1).

Figure 1. YTM on BTA Jul’25 and Alliance bank’s Mar’17 bonds.

Source: Bloomberg

Going forward, we believe that a possible sale of the government stake to Sberbank of Russia (S&P:

BBB, Moody's: Baa1) may help lower yields on BTA debt and improve its credit ratings. In this scenario, in addition to benefiting from both the new parent’s credit ratings and potential Kazakh government support, BTA bank would gain from Sberbank’s capacity to rehabilitate the Kazakh bank’s business and, when necessary, inject additional equity in BTA.

Bakytzhan Khochshanov

Halyk Finance Weekly Update May 16, 2011

6

Oil & Gas

KMG EP withdraws Iraqi bid

According to KMG EP 1Q2011 financial results released on May 10, 2011, the company's revenues grew to $1,308mn, or by 31% QoQ due to a 34% growth in the average realized prices (from $64.6 to $86.6 per bbl). In the first three months of the year, KMG EP earned a net profit of $403mn (+14% QoQ). The positive effect of the oil price growth on net income was partially offset by increases in operating taxes,

production costs and selling, general and administrative expenses. In 1Q2011, the share of results of associates and joint ventures in KMG EP's revenues amounted to $148mn, up from $82mn in the same period of 2010. The company reported an operating cash flow of $317mn, which is 5x higher than in 2010.

A day after releasing 1Q2011 results, KMG EP said it withdrew from participation in Akkas Field Development project in Anbar province, Iraq. As reported earlier, in October 2010, KMG EP, jointly with Korea Gas Corporation (KOGAS), won a tender for development of the gas field. Since then, the

companies had been negotiating details of the contract with the Iraqi government. In February 2011, Iraq's Oil and Gas Ministry announced a second postponement of the contract signing citing an

unresolved dispute between Kazakh-Korean partners and local authorities. The government of Anbar province, where the gas field is located, demanded that KMG EP and KOGAS build new housing and improve living conditions in the province, mostly inhabited by Sunnites. Following the last year's tender, Sunnite leaders warned that foreigners would be able to develop the gas field only if their investment benefits local residents. In its announcement, KMG EP said the parties failed to resolve their

disagreements, but emphasized that the company still believes that Iraq remains attractive for foreign investment.

We have KMG EP under coverage with a target price of $28.4/GDR and a Buy recommendation.

Miramgul Maralova

Max Petroleum continues exploration

On May 16, Max Petroleum announced positive results achieved at an appraisal well at Zhana Makat oil field. The company noted that the well reaches a high-quality reservoir and that its testing will start upon receipt of government approvals. Last week, Max Petroleum reported that, as a part of the post-salt drilling program, the company started drilling an exploration well at Narmundanak South prospect, targeting a deeper, Triassic section. The company also continues exploration drilling at Asanketken ,

after mechanical problems with the rig slowed down progress there. The results of Asanketken, which too targets the Triassic section, will be announced in the next few weeks, after the target depth is reached.

Max Petroleum proceeds with the program of drilling at its post-salt portfolio according to schedule. We expect more news on post-salt drilling results to come out by the end of this month, which should serve as the price catalyst. However, the results of its first pre-salt well will be much more important, we believe. The company plans to start the pre-salt drilling program in August 2011, expecting first results in 1Q2012.

We have Max Petroleum under coverage with a target price of 37GBp per share and a 'Buy' recommendation.

Miramgul Maralova

Tethys updates on Kazakh activities, reports 1Q2011 results

According to 1Q2011 results released by Tethys Petroleum (TSX: TPL) on May 13, in the first three months of 2011, the company's sales doubled to $4.48mn, compared to $2.12mn in the same period of 2010. The net loss narrowed by 21%QoQ to $6.3mn. Cash and cash equivalents increased 17% in 1Q2011.

Last week, Tethys Petroleum also said it has reached total depth at AKD04 appraisal well, drilling of which was started earlier this year. The AKD04 well data shows signs of hydrocarbons at the two geological levels of interest. The company will now complete casing of the well and then proceed with a testing program. Tethys also reported that it continues testing AKD03 exploration well where it

encountered 400bopd. According to the testing results no commercial oil flow was found at Upper

Halyk Finance Weekly Update May 16, 2011

7

Jurassic level. Further testing will take place at another Cretaceous level. Finally, Tethys said that in July

2011 it plans to reach total depth at KBD01 exploration well with observed hydrocarbons in the drilled

section.

We do not currently cover Tethys Petroleum. Over the past week Tethys stock lost 4.7% on the news as the company failed to find commercial oil at Upper Jurassic level of AKD03 well. We expect a report on testing results at Cretaceous to serve as a further stock price catalyst.

Miramgul Maralova

Halyk Finance Weekly Update May 16, 2011

8

Global Markets

Interest Rates, %

Kazakhstan Russia Ukraine

NBK ref. rate 7.50 CBR ref. rate 8.25 NBU discount rate 7.75

KAZPRIME 1.63 MOSPRIME 4.07 Ukr Interbank Weighted Rate 3.30

Europe USA UK

ECB ref. rate 1.25 Discount rate 0.75 Minimum lending rate 0.50

LIBOR EUR 3M 1.37 LIBOR USD 3M 0.26 LIBOR BP 3M 0.82

Japan China Korea

Basic discount rate 0.30 Base Rate 6.31 Official rate 3.00

Libor JPY 3M 0.20 Shanghai interbank rate 4.50 KORIBOR 3.46

Belarus

NBRB ref. rate 13.00

Exchange Rates

Country¹ Ticker

Spot 3M Forward impl. yield, % Volatility

%

13-May

Change, %

13-May

Change

1W 1M 6M 1Y 1W 1M Impl³ Hist*

Kazakhstan USDKZT 145.80 (0.1) 0.3 (1.2) (0.5) (0.4) 0.2 1.6 4.0 1.2

Russia USDRUB 28.15 1.6 (0.2) (8.8) (6.1) 3.2 (0.1) (0.6) 10.7 7.0

Ukraine USDUAH 7.99 0.1 0.2 0.4 0.8 7.5 0.8 2.0 9.5 3.8

Belarus USDBYR 3085 1.6 1.1 1.8 3.3 n/a n/a n/a n/a 3.5

Euro² EURUSD 1.41 (1.8) (3.1) 2.7 11.0 (1.0) (7.5) (13.5) 13.2 11.8

UK² GBPUSD 1.62 (1.0) (0.5) 0.5 8.7 (0.5) (4.2) (1.8) 9.8 8.3

Japan USDJPY 80.80 0.2 (3.9) (2.1) (13.1) (0.2) 0.8 (17.1) 11.0 10.9

China USDCNY 6.50 0.1 (0.5) (2.1) (4.8) (2.0) 0.8 (0.7) 2.5 1.4

Korea USDKRW 1087 0.3 (0.1) (3.6) (5.0) 2.6 1.3 0.2 12.4 7.8

Canada USDCAD 0.969 0.3 1.0 (4.2) (4.7) 0.9 1.2 3.9 9.8 8.3

Australia² AUDUSD 1.057 13.1 11.0 4.1 (5.3) (4.6) (4.6) 2.4 13.6 11.1

Turkey USDTRY 1.60 3.4 5.1 10.9 4.9 6.7 13.6 19.5 13.0 11.5

India USDINR 44.9 0.2 0.8 0.1 (0.5) 6.4 0.9 3.3 8.5 5.5

Brazil USDBRL 1.64 1.3 3.1 (5.0) (7.8) 7.9 6.9 13.7 13.1 9.4

UAE USDAED 3.67 0.0 0.0 0.0 0.0 (0.0) 0.0 (0.0) 0.5 0.0

Malaysia USDMYR 3.00 (0.2) (0.7) (3.7) (6.3) 3.4 2.0 (0.6) 7.7 4.8

¹Source: Bloomberg Price Source:BGN, except for Kazakhstan, and Ukraine CMPN (Composite New York) ²negative value of forward yield means depreciation

³3M ATM Implied volatility, %

*the annualized st.d. of the relative change of closing price for the 90 most recent trading days.

Inflation

Country 2010

Last

month

available

Last

Month 12M

Kazakhstan 6.3 Apr 11 0.5 8.4

Russia 8.8 Apr 11 0.4 9.6

Ukraine 9.1 Apr 11 1.3 9.4

Belarus 9.9 Mar 11 1.9 13.9

Eurozone 0.9 Mar 11 1.4 2.7

UK 2.9 Mar 11 0.3 4.0

Japan 0.0 Mar 11 0.3 0.0

China 4.6 Mar 11 0.1 5.3

USA 1.4 Mar 11 0.6 2.9

Korea 3.5 Apr 11 0.0 4.2

Canada 2.4 Mar 11 1.1 3.3

Australia 2.7 Apr 11 1.6 3.3

Turkey 6.4 Apr 11 0.9 4.3

India 9.5 Apr 11 0.9 8.8

Brazil 5.9 Mar 11 0.8 6.1

UAE 1.7 Mar 11 -0.2 1.2

Malaysia 2.1 Apr 11 0.1 3.0

Halyk Finance Weekly Update May 16, 2011

9

Stock Market Indices

Commodities, USD

Index 13-May 1W,% 1M,% 6M,% 1Y,% Impl.Vol¹ Hist.Vol²

MSCI World 1343 (1.2) 0.3 8.6 16.5 n/a 12.5

NASDAQ 100 2379 (0.2) 2.7 11.3 22.3 19.1 14.8

S&P 500 1338 (0.2) 1.8 11.6 15.6 16.7 12.5

DJ Industrial 12596 (0.3) 2.6 12.5 16.8 15.7 11.6

Russel 2000 836 0.3 1.4 16.2 17.7 28.1 18.2

Russel 3000 800 (0.1) 1.8 12.6 16.6 n/a 12.8

FTSE 100 5926 (0.9) (1.4) 2.2 9.1 16.2 14.4

DAX 7403 (1.2) 3.1 9.9 18.4 19.7 16.7

CAC 40 4019 (1.0) 0.3 4.9 7.7 19.4 16.8

Nikkei 225 9649 (2.1) 0.1 (0.8) (9.1) 21.7 30.3

Shanghai SE comp 2871 0.2 (5.9) (3.8) 5.9 n/a 17.5

Hang Seng 23276 0.5 (3.6) (3.9) 14.0 17.1 16.6

India (BSE) 18531 0.1 (5.9) (8.1) 7.3 22.8 20.5

Malaysia (KLSE) 196 1.4 0.4 5.2 16.1 n/a 10.2

KOSPI 2120 (1.3) (0.1) 10.8 25.1 n/a 16.5

Indonesia (JCI) 3832 0.9 2.6 4.5 34.6 n/a 17.9

Thailand (SET) 1085 3.2 0.0 6.5 41.5 n/a 18.2

Pakistan (KSE 100) 11967 0.7 2.0 10.1 16.4 n/a 15.7

KASE 1638 (0.4) (8.0) (0.6) 2.7 n/a 19.2

RTS 1866 (3.6) (9.5) 15.8 26.4 n/a 21.5

Czech (PX) 1266 0.3 1.3 9.5 3.3 n/a 13.0

Hungary (BUX) 23338 (1.6) (2.3) 5.5 (1.6) 19.7 19.5

Poland (WIG) 2823 (1.6) (3.5) 3.0 14.8 14.0 14.2

Romania (BET) 5719 (1.3) (4.5) 11.0 5.2 n/a 17.0

ISE National 100 64585 (5.4) (5.3) (7.1) 11.5 n/a 23.1

Argentina (Merv) 3378 1.9 (0.9) 5.1 48.1 n/a 18.3

Brazil (LBOV) 63235 (1.8) (4.9) (10.1) (2.4) n/a 17.1

Chile (IPSA) 4851 0.8 4.4 (2.6) 25.3 n/a 16.3

Mexico 35045 (0.5) (6.2) (2.8) 8.4 n/a 12.4

Colombia (IGBC) 14263 3.0 0.0 (5.6) 15.5 n/a 17.5

Eqypt (EGX) 5005 1.4 (5.6) (25.8) (27.6) n/a n/a

UAE (ADSMI) 2673 (0.9) 0.5 (2.8) (4.7) n/a 12.6

South Africa (JALSH) 31960 0.3 (1.2) 0.8 14.0 n/a 17.0

¹3M put implied volatility,%

²the annualized st.d. of the relative change of closing price for the 90 most recent trading days.

Unit 13-May 1W,% 1M,% 6M,% 1Y,% YTD,%

1Y

Futures, % Impl¹ Hist²

Brent bbl 113.8 4.3 (6.9) 29.8 30.5 20.1 (3.5) 45.0 30.8

Copper mt 8769.8 (0.4) (7.6) 1.6 23.0 (9.1) 0.5 33.4 24.2

Lead mt 2300.8 (0.7) (15.8) (7.8) 13.1 (10.2) (0.4) n/a 32.3

Zinc mt 2134.5 0.6 (11.1) (10.0) 0.2 (12.7) 2.4 n/a 29.7

Nickel mt 24398.0 (0.8) (7.1) 7.9 7.5 (1.3) (0.9) n/a 33.4

Aluminium mt 2590.3 (0.5) (1.0) 8.9 20.7 5.3 1.0 n/a 19.7

Uranium lb 52.1 (5.1) 2.2 (13.2) 24.6 (14.6) 13.4 n/a 40.3

Ferroalloy mt 2976.2 0.0 0.0 3.8 (0.7) 3.8 n/a n/a n/a

Steel mt 540.0 (4.3) 0.7 5.7 17.5 (1.5) n/a n/a n/a

Natural gas MMBtu 4.2 0.3 1.0 4.5 (22.6) (3.5) n/a 31.2 31.5

Gold t oz 1495.0 (0.0) 2.6 9.2 21.3 5.2 1.5 n/a 14.2

Silver mt 35.4 (0.6) (12.8) 35.8 82.3 14.5 29.8 n/a 48.0

Wheat mt 254.4 (3.0) (3.6) 10.0 56.8 (5.1) 0.5 39.0 39.5

Corn mt 262.6 (0.4) (9.4) 34.3 91.1 15.9 1.8 36.9 35.9

Sugar bu 21.5 4.8 (9.3) 1.6 35.4 (26.8) 9.0 43.7 41.8

Soybean bu 1329.5 0.3 (1.2) 4.1 38.2 (5.6) 0.6 23.0 25.6

Rough rice bu 14.0 (2.5) 0.3 (5.2) n/a (4.1) (1.3) 28.4 32.3

¹put implied volatility,%

²the annualized st.d. of the relative change of closing price for the 90 most recent trading days

Halyk Finance Weekly Update May 16, 2011

10

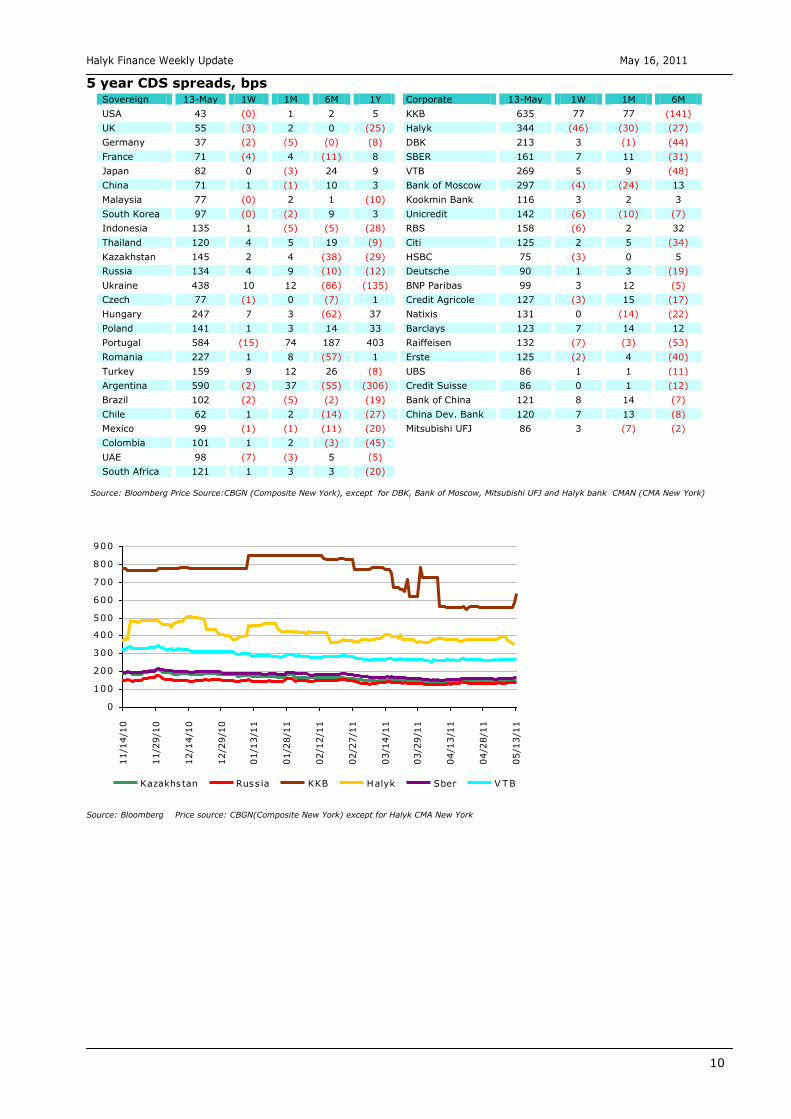

5 year CDS spreads, bps

Sovereign 13-May 1W 1M 6M 1Y Corporate 13-May 1W 1M 6M

USA 43 (0) 1 2 5 KKB 635 77 77 (141)

UK 55 (3) 2 0 (25) Halyk 344 (46) (30) (27)

Germany 37 (2) (5) (0) (8) DBK 213 3 (1) (44)

France 71 (4) 4 (11) 8 SBER 161 7 11 (31)

Japan 82 0 (3) 24 9 VTB 269 5 9 (48)

China 71 1 (1) 10 3 Bank of Moscow 297 (4) (24) 13

Malaysia 77 (0) 2 1 (10) Kookmin Bank 116 3 2 3

South Korea 97 (0) (2) 9 3 Unicredit 142 (6) (10) (7)

Indonesia 135 1 (5) (5) (28) RBS 158 (6) 2 32

Thailand 120 4 5 19 (9) Citi 125 2 5 (34)

Kazakhstan 145 2 4 (38) (29) HSBC 75 (3) 0 5

Russia 134 4 9 (10) (12) Deutsche 90 1 3 (19)

Ukraine 438 10 12 (86) (135) BNP Paribas 99 3 12 (5)

Czech 77 (1) 0 (7) 1 Credit Agricole 127 (3) 15 (17)

Hungary 247 7 3 (62) 37 Natixis 131 0 (14) (22)

Poland 141 1 3 14 33 Barclays 123 7 14 12

Portugal 584 (15) 74 187 403 Raiffeisen 132 (7) (3) (53)

Romania 227 1 8 (57) 1 Erste 125 (2) 4 (40)

Turkey 159 9 12 26 (8) UBS 86 1 1 (11)

Argentina 590 (2) 37 (55) (306) Credit Suisse 86 0 1 (12)

Brazil 102 (2) (5) (2) (19) Bank of China 121 8 14 (7)

Chile 62 1 2 (14) (27) China Dev. Bank 120 7 13 (8)

Mexico 99 (1) (1) (11) (20) Mitsubishi UFJ 86 3 (7) (2)

Colombia 101 1 2 (3) (45)

UAE 98 (7) (3) 5 (5)

South Africa 121 1 3 3 (20)

Source: Bloomberg Price Source:CBGN (Composite New York), except for DBK, Bank of Moscow, Mitsubishi UFJ and Halyk bank CMAN (CMA New York)

0

100

200

300

400

500

600

700

800

900

11/1

4/1

0

11/2

9/1

0

12/1

4/1

0

12/2

9/1

0

01/1

3/1

1

01/2

8/1

1

02/1

2/1

1

02/2

7/1

1

03/1

4/1

1

03/2

9/1

1

04/1

3/1

1

04/2

8/1

1

05/1

3/1

1

Kazakhstan Russ ia KKB Halyk Sber V TB

Source: Bloomberg Price source: CBGN(Composite New York) except for Halyk CMA New York

Halyk Finance Weekly Update May 16, 2011

11

International bonds

Issuer

Issue

size,

mn Curr

Coupon

Issue

date

Matur

date

Price YTM,%

1W change

YTM, bps

6M change

YTM, bps Credit Rating,

Fitch|Moody's

|S&P Type % Bid Ask Bid

Ask

Bid

Ask Bid Ask

Alliance Bank 615 USD Fix 10.5 Mar-10 Mar-17 95.1 95.6 11.7 11.6 77 76 69 68 B-│Caa2│B-

ATF Bank 100 USD Var 10.0 Nov-06 n/a 92.4 94.3 9.4 9.2 (0) (0) n/a n/a N.R.│B1│NR

ATF Bank 350 USD Fix 9.0 May-06 May-16 105.1 106.0 7.7 7.5 (0) 7 10 22 BBB│Ba2│NR

ATF Bank 450 USD Fix 9.3 Feb-07 Feb-14 106.4 106.9 6.7 6.5 (2) 3 (6) (21) BBB│Ba2│NR

ATF Bank 200 USD Fix 9.3 Apr-05 Apr-12 103.5 103.9 5.2 4.8 (8) (9) (10) (7) BBB│Ba2│NR

BTA Bank 2082 USD Var 10.8 Aug-10 Jul-18 93.3 93.8 13.4 13.3 235 231 336 333 B-│N.R.│N.R.

BTA Bank 497 USD Fix 7.2 Aug-10 Jul-25 56.9 57.4 14.4 14.3 251 248 392 387 CC│N.R.│N.R.

CenterСredit 500 USD Fix 8.6 Jan-07 Jan-14 101.5 102.0 8.0 7.8 5 (0) 96 97 B│B2│N.R.

DBK 150 USD Fix 6.0 Mar-06 Mar-26 75.7 110.4 9.0 5.0 0 0 100 (174) BBB-│Baa3│BBB

DBK 100 USD Fix 6.5 Jun-05 Jun-20 90.5 118.8 8.0 4.0 0 0 100 (231) BBB-│Baa3│BBB

DBK 100 USD Fix 7.4 Nov-03 Nov-13 103.1 113.0 6.0 2.0 (0) 0 100 (101) BBB-│Baa3│BBB

DBK 777 USD Fix 5.5 Dec-10 Dec-15 104.7 105.2 4.4 4.2 (2) (4) n/a n/a BBB-│Baa3│BBB

Eurasian Bank 500 USD Fix 7.4 Sep-09 Sep-14 110.2 110.9 4.1 3.9 (12) (11) (80) (81) BBB│A3│BBB

Halyk Bank 700 USD Fix 7.3 May-07 May-17 103.8 104.4 6.5 6.4 10 10 (12) (8) BB-│Ba3│B+

Halyk Bank 300 USD Fix 7.8 May-06 May-13 105.9 106.4 4.6 4.4 10 10 (85) (73) BB-│Ba3│B+

Halyk Bank 500 USD Fix 9.3 Apr-08 Oct-13 110.0 110.5 4.8 4.6 7 2 (73) (77) BB-│Ba3│B+

Halyk Bank 500 USD Fix 7.3 Jan-11 Jan-21 102.3 102.8 6.9 6.8 4 4 n/a n/a BB-│Ba3│B+

INTERGAS 600 USD Fix 6.4 May-07 May-17 105.9 106.9 5.2 5.0 (5) (7) 12 1 BB+│Baa3│BB

INTERGAS 250 USD Fix 6.9 Nov-04 Nov-11 102.5 103.0 1.4 0.4 33 26 (70) (149) BB+│Baa3│BB

KazAtomProm 500 USD Fix 6.3 May-10 May-15 106.6 107.0 4.4 4.3 (15) (12) (15) (19) BBB-│Baa3│N.R.

Kazkom 750 EUR Fix 6.9 Feb-07 Feb-17 93.5 94.0 8.3 8.2 16 16 (32) (32) B-│B2│B

Kazkom 500 USD Fix 7.5 Nov-06 Nov-16 96.2 96.7 8.4 8.3 35 34 (134) (134) B-│B2│B

Kazkom 350 GBP Fix 7.6 Feb-07 Feb-12 100.3 100.5 7.0 6.7 59 59 (266) (266) B-│B2│B

Kazkom 400 USD Fix 7.9 Apr-04 Apr-14 101.2 101.7 7.4 7.2 35 34 (183) (184) B-│B2│B

Kazkom 500 USD Fix 8.5 Apr-03 Apr-13 101.8 102.2 7.5 7.3 36 39 (163) (160) B-│B2│B

Kazkom 250 USD Var 8.5 Jun-07 Jun-17 87.4 87.7 10.2 10.2 (1) 5 (164) (157) CC│B3│CCC+

Kazkom 500 USD Fix 8.0 Nov-05 Nov-15 100.7 101.0 7.8 7.7 27 27 (148) (148) B-│B2│B

Kazkom 200 USD Var 8.6 Jul-06 Jul-16 87.5 87.8 10.4 10.3 10 9 (167) (159) CC│B3│CCC+

Kazkom 100 USD Var 9.2 Nov-05 n/a 79.2 81.9 9.5 9.1 12 (1) (25) (57) CC│Caa1│CCC

Kazkom 300 USD Fix 8.5 May-11 May-18 95.7 96.2 9.3 9.2 51 48 n/a n/a B-e│B2e│B

KazTemZhol 350 USD Fix 7.0 May-06 May-16 110.9 111.6 4.5 4.4 (18) (18) (24) (30) BBB-│Baa3│BBB-

KazTemZhol 700 USD Fix 6.4 Oct-10 Oct-20 105.5 106.3 5.6 5.5 (17) (17) (20) (24) BBB-│Baa3│BBB-

KazakhGold 200 USD Fix 9.4 Nov-06 Nov-13 98.6 99.8 10.0 9.5 0 6 (447) (213) WD│N.R.│N.R.

KMG 1400 USD Fix 8.4 Jul-08 Jul-13 111.3 111.7 2.9 2.7 (5) (6) (162) (162) BBB-│Baa3│BBB-

KMG 1600 USD Fix 9.1 Jul-08 Jul-18 121.9 123.6 5.4 5.1 (7) (15) (94) (109) BBB-│Baa3│BBB-

KMG 1500 USD Fix 11.8 Jul-09 Jan-15 125.7 126.4 4.1 4.0 (11) (14) (130) (129) BBB-│Baa3│BBB-

KMG 1500 USD Fix 7.0 May-10 May-20 110.3 111.0 5.5 5.4 (17) (14) (101) (102) BBB-│Baa3│N.R.

KMG 1250 USD Fix 6.4 Nov-10 Apr-21 105.6 106.4 5.6 5.5 (14) (12) (100) (95) BBB-│Baa3│BBB-

Tengizchev 1100 USD Fix 6.1 Nov-04 Nov-14 105.7 106.6 4.4 4.1 (10) (5) (31) (22) BBB-│Baa3│N.R.

Temirbank 61 USD Fix 14.0 Jun-10 Jun-22 120.1 120.6 10.8 10.8 1 1 (107) (106) B-│N.R.│B

Nurbank 150 USD Fix 9.4 Oct-06 Oct-11 100.0 101.0 9.3 6.8 (2) (12) (785) (686) N.R.│B3│B

ZhaikMunai 450 USD Fix 10.5 Oct-10 Oct-15 103.8 108.6 9.4 8.1 (4) (24) n/a n/a N.R.│B3│B

Price source: CBBT (Composite Bloomberg Bond Trader), BVAL, BGN, KAZA

Halyk Finance Weekly Update May 16, 2011

12

Domestic bonds

Fixed coupon

Debt Instrument

Issue

Size, mn KZT

Coupon Rate, %

Rem

Life, years

Last Trade Current Bid* Current Ask*

Price YTM, % Date Price YTM, % Price YTM, %

AIC-Invest B2 5,000 12.0 0.0 100.3 10.0 05/04/11 100.0 12.0 100.0 10.0

AIC-Invest B3 10,000 12.0 0.3 99.8 12.7 20/04/11 100.0 12.0 100.6 10.0

Almatyenergosbyt B1 900 15.0 4.1 107.9 12.5 11/05/11 106.2 13.0 113.0 11.0

ATF Bank B4 4,500 8.5 3.5 101.5 8.0 13/04/11 98.5 9.0 111.2 5.0

BankCenterCredit B17 5,000 8.5 1.0 99.4 9.0 24/03/11 99.5 9.0 103.4 5.0

Becker&K B1 8,000 10.0 4.7 100.0 10.0 12/04/11 111.9 7.0 130.6 3.0

CentAsian PE Co. B1 20,000 12.5 7.6 84.7 16.0 01/03/11 84.9 16.0 93.1 14.0

Central Asia Cement B1 2,700 9.0 0.2 100.0 9.0 24/03/11 99.1 13.0 100.0 9.0

DBK-Leasing B1 5,000 8.0 4.7 107.0 6.3 08/04/11 106.0 6.5 124.4 2.5

Ekibastusz GRES-1 B1 10,000 12.0 3.6 115.4 7.3 05/03/11 109.1 9.0 115.8 7.0

Eurasian Bank B6 5,000 11.0 4.3 99.7 11.1 13/01/10 103.4 10.0 110.7 8.0

Eurasian Bank B9 35,000 13.0 0.4 115.6 8.7 29/04/11 114.3 9.0 122.5 7.0

Eximbank B1 10,000 9.0 2.5 84.2 17.0 12/05/11 81.7 18.5 88.8 14.5

Eximbank B2 10,000 9.0 1.1 90.8 18.5 29/04/11 91.1 18.5 94.7 14.5

Food Contract B3 15,000 10.5 1.7 103.5 9.0 02/06/10 102.3 9.0 105.5 7.0

Food Contract Corp B2 15,000 8.0 1.8 101.2 7.3 15/04/11 98.3 9.0 103.4 6.0

Halyk Bank B13 5,000 13.0 7.5 115.6 10.0 19/04/11 115.5 10.0 125.0 8.4

Halyk Bank B7 4,000 7.5 3.6 98.2 8.0 07/07/10 96.9 8.5 103.2 6.5

Halyk Bank B9 3,000 7.5 4.1 96.5 8.5 19/04/11 96.5 8.5 103.6 6.5

Kaspi Bank B6 10,000 8.5 4.0 86.2 13.0 19/04/11 86.4 13.0 92.1 11.0

Kaz Mortgage Co B11 5,000 6.9 3.9 83.6 12.0 01/02/11 90.2 10.0 96.4 8.0

Kaz Mortgage Co B18 5,000 11.0 1.5 104.1 8.3 15/04/11 102.8 9.0 105.8 7.0

Kazcat B1 5,000 10.0 1.6 91.4 16.0 25/04/11 91.7 16.0 94.3 16.8

Logicom B2 1,700 11.0 2.6 101.8 10.3 27/01/11 97.8 12.0 107.0 8.0

Mangys Power Distr B3 700 12.0 0.5 103.1 9.0 29/09/10 102.4 7.0 104.6 3.0

Mangys Power Distr B4 500 12.0 1.0 104.7 8.0 12/01/11 104.5 7.0 108.5 3.0

Mangys Power Distr B5 800 16.0 1.7 116.7 7.0 04/02/11 112.8 8.0 120.0 4.0

Mangys Power Distr B6 800 16.0 2.9 121.9 8.0 01/02/11 120.2 8.0 132.3 4.0

Nurbank B2 4,000 9.0 0.1 99.8 10.0 19/04/11 N/A N/A N/A N/A

Nurbank B5 5,000 7.5 5.0 82.2 12.0 12/11/10 80.2 13.0 90.3 10.0

Nurbank B7 10,000 11.0 2.5 100.0 11.0 11/05/11 97.9 12.0 106.6 8.0

Orda Credit B2 1,500 12.0 1.7 97.0 14.0 11/05/11 0.0 0.0 N/A N/A

RG Brands B4 1,500 8.0 0.2 100.5 6.0 27/04/11 99.5 10.0 100.4 6.0

RG Brands B5 1,500 8.0 1.4 97.2 10.0 06/04/11 98.7 9.0 101.3 7.0

RG Brands B6 2,000 8.0 3.4 87.6 12.5 26/04/11 84.1 14.0 86.5 13.2

Samruk-Kazyna b23 75,000 6.5 9.4 105.7 5.7 11/05/11 100.0 6.5 115.1 4.5

Sberbank B4 5,000 9.0 6.3 116.0 6.0 18/02/11 110.0 7.0 134.1 3.0

Temirbank B10 4,500 6.8 5.5 72.0 12.0 17/03/11 67.0 13.0 91.7 9.0

Temirbank B3 2,200 8.0 11.4 62.6 14.8 02/02/11 62.2 15.0 80.7 11.0

Temirbank B4 5,000 9.0 4.1 0.0 0.1 12/01/06 73.1 12.0 100.0 8.0

Temirbank B7 3,000 8.5 4.0 60.1 14.8 28/03/11 59.4 15.0 78.8 11.0

Temirbank B8 3,500 8.5 1.0 0.0 0.1 23/08/06 75.9 12.0 100.0 8.0

Tsesna Astyk B1 3,000 9.0 0.6 90.0 28.6 10/05/11 N/A N/A N/A N/A

Tsesna Bank B2 3,000 9.0 1.2 98.7 10.0 05/03/11 100.0 9.0 102.3 7.0

*As of 5/13/2011

Source: KASE

Halyk Finance Weekly Update May 16, 2011

13

Floating coupon

Debt Instrument

Issue Size,

mn KZT

Coupon

Rate, %

Rem Life,

years

Last trade Current Bid* Current Ask*

Price YTM, % Date Price YTM, % Price YTM, %

ABDI Company B1 9000 8.8 1.7 77.7 27.0 11/5/2011 75.8 29.0 79.8 25.0

Agri Credit Corp.B1 3000 8.3 1.2 100.4 8.0 25/03/2011 99.8 8.5 103.3 5.5

AtamekenAgro B2 11000 10.5 7.2 105.2 10.2 2/3/2011 105.0 10.2 128.8 6.2

ATF Bank B5 13000 9.2 1.0 101.2 8.0 19/04/2011 101.2 8.0 105.2 4.0

ATF Bank B6 13000 8.8 2.8 97.9 8.0 1/2/2011 97.1 10.0 107.1 6.0

ATF Bank B7 15000 8.2 0.5 100.7 8.1 1/7/2010 102.5 4.7 104.4 0.7

BankCenterCredit B10 3000 9.1 4.4 96.3 8.7 29/03/2011 96.8 10.0 111.8 6.0

BankCenterCredit B11 2000 7.7 4.6 98.4 8.1 19/01/2011 89.9 10.5 104.7 6.5

BankCenterCredit B13 4000 9.1 4.9 83.8 11.7 19/03/2010 96.6 10.0 113.0 6.0

BankCenterCredit B14 5000 9.1 5.4 96.3 10.0 19/04/2011 96.3 10.0 114.1 6.0

BankCenterCredit B15 3000 7.7 6.0 93.7 9.0 18/11/2010 96.0 10.0 115.3 6.0

BankCenterCredit B20 3500 7.5 12.5 94.5 8.2 19/01/2011 114.1 8.0 156.6 4.0

BankCenterCredit B4 2000 10.3 0.4 102.0 6.0 11/2/2011 100.4 9.0 101.9 5.0

BankCenterCredit B6 1300 8.2 3.6 94.6 10.0 6/5/2011 94.6 10.0 107.1 6.0

BankCenterCredit B7 2000 7.7 4.0 98.5 8.1 19/01/2011 92.5 10.0 106.0 6.0

BankCenterCredit B8 2000 10.0 4.3 100.0 10.0 28/03/2011 99.6 10.1 114.4 6.1

BankCenterCredit B9 4500 9.1 4.3 98.6 9.5 19/04/2011 98.6 9.5 113.5 5.5

Batys Transit B1 18830 8.6 7.9 95.0 9.5 15/04/2011 95.0 9.5 106.2 7.5

BTA Ipoteka B14 10000 8.7 2.9 55.5 34.0 12/5/2011 n/a n/a n/a n/a

BTA Ipoteka B3 2000 8.3 0.6 99.0 9.8 5/4/2011 n/a n/a 99.9 8.5

BTA Ipoteka B7 4000 8.8 1.2 98.6 10.0 5/4/2011 n/a n/a n/a n/a

BTA Ipoteka B8 7000 8.6 2.3 93.1 12.0 5/4/2011 n/a n/a 99.9 8.6

BTA Ipoteka B9 4000 8.2 4.8 83.3 13.0 11/5/2011 n/a n/a 83.3 13.0

Caspian Beverage H B1 500 12.0 1.9 85.0 22.4 6/5/2011 84.4 23.0 89.6 19.0

Delta Bank B1 3000 8.7 1.4 71.5 32.0 26/01/2011 n/a n/a n/a n/a

ERKA B1 2500 10.0 2.5 102.7 8.9 7/2/2011 100.0 10.0 104.5 8.0

Eurasian Bank B2 3000 7.5 0.6 101.2 6.0 4/2/2011 101.4 5.0 102.5 3.0

Eurasian Bank B3 10000 9.1 1.9 98.5 10.0 12/5/2011 97.6 10.5 101.9 8.0

Eurasian Bank B4 10000 7.8 3.3 93.8 10.0 19/04/2011 93.9 10.0 99.4 8.0

Eurasian Bank B7 5000 8.3 7.7 90.9 10.0 15/04/2011 101.7 8.0 114.0 6.0

Eximbank B3 10000 9.0 4.2 96.5 10.0 14/02/2011 96.6 10.0 103.5 8.0

Halyk Bank B10 5000 7.7 4.5 86.5 11.6 21/04/2011 86.4 10.5 89.6 9.6

Halyk Bank B11 4000 6.4 4.9 91.1 10.5 7/12/2010 95.5 7.5 103.8 5.5

Halyk Bank B12 10000 10.6 6.4 102.8 10.0 11/5/2011 100.4 10.5 121.2 6.5

Imstalconb2 4400 10.6 5.4 99.3 8.9 11/10/2010 98.4 11.0 106.7 9.0

Jairem GOK B2 3900 9.1 1.9 99.8 8.9 21/01/2011 97.5 11.2 105.2 6.7

JP Morgan E1 1320 5.1 4.8 102.3 5.1 7/2/2011 110.9 9.5 119.8 7.4

Kaspi Bank B4 7000 7.6 0.1 100.1 6.0 28/04/2011 100.0 7.0 100.1 5.0

Kaspi Bank B5 3500 8.7 0.7 99.1 10.0 28/04/2011 98.5 11.0 99.8 9.0

Kaspi Bank B7 5000 9.8 7.1 89.7 12.0 11/5/2011 85.5 13.0 94.2 11.0

Kaspi Bank B8 6000 9.3 7.7 130.4 9.0 23/06/2010 121.0 6.0 136.5 4.0

Kaz Mortgage Co B12 5000 6.7 5.9 85.3 10.0 18/03/2011 81.3 12.0 89.0 10.0

Kaz Mortgage Co B16 5000 6.2 5.7 83.6 11.5 13/05/2011 83.6 11.5 89.4 10.0

Kaz Mortgage Co B17 10000 8.4 5.1 93.7 10.0 28/04/2011 88.3 11.5 95.6 9.5

Kaz Mortgage Co B19 5000 10.2 2.2 101.1 10.5 1/2/2011 100.9 10.5 104.8 8.5

Kaz Mortgage Co B2 3000 7.5 2.4 102.3 8.3 5/5/2011 100.8 9.0 105.2 7.0

Kaz Mortgage Co B20 8000 11.0 4.6 103.8 10.0 31/01/2011 107.4 9.0 109.3 8.5

Kaz Mortgage Co B21 10000 8.0 7.6 100.0 8.0 22/04/2011 100.0 8.0 112.1 6.0

Kaz Mortgage Co B3 5000 7.7 2.9 100.7 9.3 5/5/2011 99.0 10.0 104.0 8.0

Kaz Mortgage Co B4 5000 7.2 2.9 98.0 9.9 5/5/2011 97.8 10.0 108.1 6.0

Kaz Mortgage Co B7 5000 6.8 0.4 100.6 5.8 14/02/2011 101.4 5.0 102.2 3.0

Kaz Mortgage Co B8 5000 6.8 3.4 100.6 8.5 28/04/2011 96.3 10.0 102.0 8.0

KazExportAstyk B2 6000 8.7 0.1 101.0 5.0 18/03/2011 100.1 8.0 100.6 4.0

KazInvestBank B1 1250 8.8 1.6 96.5 11.0 3/3/2011 n/a n/a n/a n/a

Kazkommertsbank B4 7000 8.7 3.9 96.0 11.4 19/04/2011 95.7 11.5 108.6 7.5

Kazkommertsbank B5 5500 8.2 4.3 93.0 11.6 6/5/2011 92.7 11.7 106.5 7.7

Kazkommertsbank B6 10000 8.7 6.3 87.1 11.5 17/01/2011 85.5 12.0 103.4 8.0

Kazkommertsbank B7 10000 7.7 7.5 85.2 10.5 31/12/2010 84.8 10.7 105.8 6.7

Kazkommertsbank B8 10000 9.0 7.9 84.8 12.0 19/04/2011 85.4 12.0 106.4 8.0

KazTransCom B2 3000 10.0 1.5 99.6 11.0 8/12/2010 102.3 9.7 104.3 7.8

KedenTransServis B1 5000 8.3 0.9 96.4 12.8 5/5/2011 n/a n/a n/a n/a

KSMK B1 1300 9.9 0.9 47.4 50.0 14/09/2009 n/a n/a n/a n/a

Halyk Finance Weekly Update May 16, 2011

14

KSMK B2 1300 9.9 1.5 54.1 41.3 28/05/2010 n/a n/a n/a n/a

Nurbank B6 5000 7.4 3.7 112.7 4.0 27/12/2010 110.8 6.0 125.9 2.0

Ordabassy B2 12000 8.0 0.5 30.0 n/a 29/03/2011 n/a n/a 70.0 n/a

Sat & C B1 15000 9.8 3.6 94.5 10.5 15/12/2010 99.4 10.0 105.6 8.0

Sberbank B3 3000 8.5 0.5 101.8 5.0 22/04/2011 101.7 7.0 103.6 3.0

Temirbank B18 10000 8.0 8.8 79.2 13.9 4/4/2011 75.0 15.0 93.3 11.0

Tort Kudyk B1 2000 11.5 0.5 103.0 8.1 18/11/2010 101.8 9.7 103.6 5.7

Tsesna Bank B5 3000 8.3 3.1 95.5 10.0 4/5/2011 90.6 12.0 99.0 8.7

Tsesna Bank B6 4000 8.3 4.6 77.9 15.0 28/03/2011 90.5 11.0 101.1 8.0

*As of 5/13/2011

Source: KASE

Halyk Finance Weekly Update May 16, 2011

15

KASE

Stock Ticker Last Price

Weekly

Weighted

Average Price

One week change,%

Volume, last

week, KZT mn

Avg daily

volume,

3mths, KZT mn

Mkt Cap ($mn)

52-week low

52-week high

AktobeMunaiGaz p AMGZp 25000 1.5 161.9 18000 28500

BankCenterCredit CCBN 515 505 4.0 2.6 19.6 138.7 495 673

BTA Bank BTAS 3.5 4 (18.6) 8.6 1.7 1061.8 4 900

ENRC GB_ENRC 2087.6 2090 (0.6) 3.6 1.2 18446.9 1800 2600

Halyk Bank HSBK 355 349 2.9 2.5 8.6 3187.3 250 445

Halyk Bank p HSBKp 168.4 0.0 450.8 168 186

Kazakhmys GB_KZMS 3000 3021 (4.9) 33.4 5.4 11018.5 2155 3800

KazakhTeleCom KZTK 19190 18948 (0.1) 327.3 22.9 1438.3 11800 20850

KazakhTeleCom p KZTKp 9001 9250 0.9 1.5 75.0 6000 9990

Kazcat ZERD 1.4 2.7 29.2 1 3

Kazkommertsbank KKGB 469.7 452 (3.3) 3.3 3.7 2512.0 356 616

Kazkommertsbank p KKGBp 210 0.2 180.1 195 242

KazMunaiGaz RDGZ 19400 19180 2.1 107.3 8.1 9348.0 15155 21000

KZACi p KAZIp 335 335 3.4 0.4 34.5 300 390

MangystauMunaiGaz p MMGZp 9200 1.4 68.8 4000 10450

Rakhat RAHT 1000 0.0 24.7 1000 1300

SAT & Company SATC 71.1 71 5.9 1.5 572.3 70 72

Temirbank TEBN 500 0.0 135.3* 500 500

Temirbank p TEBNp 500 0.0 17.2 200 500

Tort Kudyk TKUDp 9 3.2 4.8 9 9

Tsesna Bank TSBN 865 0.1 121.7 833 970

Ust'-Kam TMC p UTMKp 4440 0.2 3.3 4000 5399

Source: KASE

*Based on the last price of GDR.

Halyk Finance Weekly Update May 16, 2011

16

International Stock Exchanges

Unresolved Greek debt crisis and the increasingly likely monetary tightening in China weighed donw on the international stock and commodity markets. Kazakhstan-based stocks tracked the international markets, with few exceptions.

The large-caps were mostly down: Uranium One (-8%), Cameco (-7.6%), Zhaikmunai (-7.3%), ENRC (-5.3%), Kazakhmys (-4.9%). Among the mid-caps, Kazakhgold GDR lost 11.9% on concerns that the Assaubayev’s will renege on their agreement with Polyus Gold. Frontier Mining (+12.2%) rose on the news of South Benkala project acquisition and the completion of $5mn debt funding. Among the small-

caps, the biggest losers were Kazakhstan Kagazy (-30.6%), Caspian Oil & Gas (-23.5%), Xtract Energy (-11%) and Aurum Mining (-10.6%), while the best performer was Oxus Gold (+9.1%).

Miramgul Maralova

Stock Ticker Crnc 13-May

Volume

of

trade,

5d avg,

USD th

Mkt

cap,

USD

mn

Change, % 52-

week

low

52-

week

high

Primary

Exch. 1W 1M YTD 1Y

ENRC ENRC LN GBp 835.5 28,504 17427 (5.3) (10.2) (20.3) (21.0) 801.0 1127 LSE

Ivanhoe Mines IVN US USD 24.05 32,739 15723 (0.5) (9.9) 4.9 67.8 11.5 29.29 NYSE

Ivanhoe Mines IVN CN CAD 23.30 17,530 15713 (0.1) (9.5) 1.3 57.2 12.4 28.98 TSX

Kazakhmys KAZ LN GBp 1213.0 39,427 10516 (4.9) (13.9) (24.8) (1.9) 955.5 1700 LSE

Cameco CCO CN CAD 25.44 63,824 10358 (7.6) (6.0) (36.9) (1.8) 21.6 44.28 TSX

Cameco CCJ US USD 26.24 95,624 10357 (7.6) (6.8) (35.0) 4.6 20.7 44.81 NYSE

KMG E&P GDR KMG LI USD 20.80 9,321 8750 (2.9) (8.3) 4.9 (4.2) 17.0 24.93 LSE

Centerra Gold CG CN CAD 19.15 15,454 4660 3.0 11.7 (3.5) 59.6 10.5 23.23 TSX

Dragon Oil DGO LN GBp 525.0 3,450 4387 0.6 (9.5) (2.4) 19.3 361.8 614 LSE

Uranium One UUU CN CAD 3.80 43,511 3752 (8.0) (0.5) (21.0) 65.9 1.6 7.02 TSX

Halyk Bank GDR HSBK LI USD 9.50 538 3107 0.2 (7.3) (5.5) 13.4 6.8 12.58 LSE

KKB GDR KKB LI USD 6.55 9 2552 (1.5) (11.4) 10.1 (6.4) 4.7 8.70 LSE

Zhaikmunai GDR ZKM LI USD 10.61 296 1963 (7.3) (16.8) (13.7) 24.8 5.5 13.60 LSE

Kazakhtelecom ADR KZTA GR EUR 6.00 2 1388 0.8 0.8 0.0 33.3 3.9 6.90 DAX

Tethys Petroleum TPL CN CAD 1.21 700 325 (4.7) (17.7) (24.8) (34.9) 1.2 2.19 TSX

Max Petroleum MXP LN GBp 16.00 794 239 (3.0) (8.6) (12.3) (11.1) 9.0 29.50 LSE

KazakhGold KZG LI USD 1.85 9 221 (11.9) (26.0) (52.6) (76.9) 1.8 8.24 LSE

Victoria Oil & Gas VOG LN GBp 5.20 2,141 177 (7.1) 1.4 (7.1) 67.7 2.5 6.95 LSE

Kentor Gold KGL AU AUD 0.13 282 146 0.0 (18.8) (27.8) 71.1 0.0 0.20 ASE

Temirbank GDR T3M GR EUR 9.60 n/a 136 0.0 8.3 (7.7) (2.5) 4.9 11 n/a

Steppe Cement STCM LN GBp 43.25 42 125 0.0 (1.7) (19.2) (35.0) 40.0 67.8 LSE

Frontier Mining FML LN GBp 4.13 210 124 12.2 (26.6) (44.9) (26.6) 3.6 9.00 LSE

Chagala Group GDR CHGG LI USD 3.30 n/a 70 0.0 (8.3) (2.9) (4.3) 3.0 4.00 LSE

Sunkar Resources SKR LN GBp 26.00 157 67 (3.7) (10.3) (38.1) (78.3) 16.8 52 LSE

Alhambra Resources ALH CN CAD 0.58 32 62 1.8 (34.1) (38.9) 93.3 0.2 1.20 Venture

Hambeldon Mining HMB LN GBp 4.88 16,349 59 0.0 8.4 (32.9) (5.6) 4.1 8.50 LSE

Kryso Resources KYS LN GBp 13.88 98 57 0.0 (7.5) (17.1) 29.1 8.4 19.75 LSE

BMB Munai KAZ US USD 0.97 88 54 1.0 1.6 12.8 9.4 0.5 1.22 NYSE

Manas Petroleum MNAP US USD 0.43 64 54 (7.6) (24.1) (29.2) (34.6) 0.4 0.70 OTC BB

Xtract Energy XTR LN GBp 3.25 172 46 (11.0) (16.2) (18.8) 116.7 1.0 5.48 LSE

Orsu Metals OSU CN GBp 15.75 6 40 5.0 (6.0) (27.6) (1.6) 10.5 26.50 LSE

Orsu Metals OSU LN CAD 0.23 35 37 (2.2) (6.2) (33.8) (10.0) 0.2 0.40 TSX

Caspian Energy CEK CN CAD 0.20 37 35 (9.1) (23.1) (9.1) 5.3 0.1 0.26 LSE

Roxi Petroleum RXP LN GBp 4.63 11 32 0.0 (13.9) (21.3) (46.3) 4.1 13.25 LSE

Caspian Oil & Gas CIG AU AUD 0.01 205 18 (23.5) 0.0 85.7 30.0 0.0 0.02 ASE

Centr. Asia Resources CVR AU AUD 0.05 4 16 0.0 6.7 65.5 20.0 0.0 0.06 ASE

Caspian Services CSSV US USD 0.16 0 8 3.2 0.0 6.7 (57.9) 0.1 0.40 OTC BB

Oxus Gold OXS LN GBp 1.20 54 8 9.1 (14.3) (77.1) (85.4) 0.7 9.75 LSE

Shalkiya Zinc SKZ LI USD 0.14 n/a 8 0.0 (22.2) (6.7) (30.0) 0.1 0.40 LSE

Aurum Mining AUR LN GBp 3.13 26 6 (10.6) (13.8) (45.6) (94.0) 1.2 16.50 LSE

Kazakh. Kagazy GDR KAG LI USD 0.05 1 5 (30.6) (68.8) (80.0) (72.2) 0.1 0.25 LSE

Caspian Holdings CSH LN GBp 0.48 6 3 (2.0) (9.4) (22.6) (26.2) 0.3 0.75 LSE

All quotes in local currency, unless otherwise noted

Sources: Bloomberg, Halyk Finance

Halyk Finance Weekly Update May 16, 2011

17

Disclaimer © 2011 Halyk Finance, a subsidiary of Halyk Bank. For contact details see the information on Halyk Finance website www.halykfin.kz

or contact Halyk Finance office. All rights reserved. This document and/or information has been prepared by and, except as otherwise specified herein, is communicated by Halyk Finance.

This document is for information purposes only. Opinions and views expressed in this document do not necessarily represent the

opinions and views held by Halyk Finance, or other subsidiaries of Halyk Bank. The differences of opinion stem from different

assumptions, sources information, criteria and methodology of valuation. Information and opinions expressed herein are subject to

change without notice; and neither Halyk Finance, or Halyk Bank, or any of its subsidiaries or affiliates are under any obligation to keep

them current.

This document is not an offer or an invitation to engage in investment activity. It cannot be relied upon as a representation that any

particular transaction necessarily could have been or can be effected at the stated price. This document does not constitute an

advertisement or an offer of securities, or related financial instruments. Descriptions of any company or companies or their securities or the markets or developments mentioned herein are not intended to be complete. Views and opinions expressed in this document

cannot substitute for the exercise of own judgment and do not attempt to meet the specific investment objectives, financial situation or

particular needs of any specific investor.

The information and opinions herein have been arrived at based on information obtained from sources believed to be reliable and in

good faith. Such sources have not been independently verified; information is provided on an ‘as is’ basis and no representation or

warranty, either expressed or implied, is provided in relation to the accuracy, completeness, reliability, merchantability or fitness for a

particular purpose of such information and opinions, except with respect to information concerning Halyk Finance and its affiliates.

The securities described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. Options, derivative

products and futures are not suitable for all investors and trading in these instruments is considered risky. Past performance is not

necessarily indicative of future results. Foreign-currency denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or the price of, or income derived from, the investment.

Halyk Finance and its affiliates, directors, representatives, employees, or clients may have or have had interests in issuers described

herein. Halyk Finance may have or have had long or short positions in any of the securities or other financial instruments mentioned

herein at any time and may make a purchase and/or sale, or offer to make a purchase and/or sale, of any such securities or other

financial instruments at any time, as principal or agent.

Halyk Finance and its affiliates may act or may have acted as market maker in the securities or other financial instruments described

herein, or in securities underlying or related to such securities. Employees of Halyk Finance or its affiliates may serve or have served as

officers or directors of the said companies. Halyk Finance and its affiliates may have or have had a relationship with or have provided

investment banking, capital markets, advisory, investment management, and/or other financial services to the relevant companies. Halyk Finance relies on information barriers to avoid the appearance of conflict of interests within Halyk Finance or in its relations with

clients, other issuers, and external investors.

The information herein is not intended for distribution to the public and may not be reproduced, redistributed or published, in whole or

in part, for any purpose without the written permission of Halyk Finance. Neither Halyk Finance nor any of its affiliates accepts any

liability whatsoever for the actions of third parties in this respect. This information may not be used to create any financial instruments

or products or any indices. Neither Halyk Finance, nor its affiliates, nor their directors, representatives, or employees accept any

liability for any direct or consequential loss or damage arising out of the use of any information herein.

Macro Sabit Khakimzhanov, 7 (727) 244-6541 [email protected] Madina Kurmangaliyeva, 7 (727) 330-0157 [email protected] Financial Sector. Fixed Income Securities Bakytzhan Khochshanov 7 (727) 2446-984 [email protected] Sabina Amangeldi, 7(727) 344-6986 [email protected]

Equity Research Timur Omoev [email protected] Mariyam Zhumadil 7 (727) 244-6538 [email protected] Miramgul Maralova 7(727) 244-6538 [email protected]

Address Bloomberg

Halyk Finance

19/1, Al-Farabi Ave., Nurly-Tau Business Center, Suite 3b Almaty, Republic of Kazakhstan, 050013

Tel. +7 (727) 259 0467

Fax.+7 (727) 259 0593

eng.halykfin.kz

HLFN