Guide to how the University of Arkansas’ Chart of Accounts ... · Finance & Administration. Vice...

29

Guide to how the University of Arkansas’ Chart of Accounts is designed.

Transcript of Guide to how the University of Arkansas’ Chart of Accounts ... · Finance & Administration. Vice...

Guide to how the University of Arkansas’ Chart of Accounts is designed.

What is AccountingAccounting is the language used to communicate information

about the financial condition and operations of all types of organizations. Accounting is the system that records, evaluates, compares, and reports the financial activities of an organization.

Accounting information serves many purposes depending upon the users of the information. Various groups and individuals, such as managers, deans and directors, vice chancellors, and outside regulatory agencies, use accounting information to make informed decisions about the organization.

Accurate and complete accounting information is used to: Effectively allocate and use an organization’s resources. Understand the operations and financial activities of an

organization. Evaluate the effectiveness and efficiency of operations. Make investment decisions.

University Accounting ObjectivesUniversity accounting objectives are similar to those of other types

of organizations. Like businesses and corporations, the university is concerned with the effective use and allocation of the organization’s resources, and the accurate and effective reporting of financial activity.

However, businesses and corporations operate to maximize their profits while providing goods and services. A university, on the other hand, operates to meet certain needs without a profit motive by providing goods and services; namely education, research, and public service. This fundamental difference is the basis for the special reporting requirements of university accounting. Providers of the funds used by a university to carry out its mission often have special guidelines or restrictions concerning how those funds may be used.

University Accounting OverviewThe terms "university accounting" and "fund accounting" are used by

colleges and universities, as well as government and other not-for-profit organizations, to refer to the unique accounting requirements of non-profit entities. Since funding for these organizations is often provided by legislative bodies, foundations, and donations, special accounting and reporting requirements are used to account for their financial activities.

Financial Affairs is responsible for maintaining and administering the University’s official accounting and financial records. However, most of the financial activity originates in campus departments, like yours. In other words, you are a crucial part of the financial reporting process for the University. Therefore, it is critical that you understand the accounting policies and procedures of the University.

Chart of AccountsAll of the accounts used by the University are referred to

as the chart of accounts. The chart of accounts is a listing of the accounts in a logical order consistent with the layout and structure of financial statements and reports. Classes or groupings of similar accounts are assigned within specified ranges. This helps ensure more accurate reporting and makes it easier to identify and summarize groupings of similar accounts.

The University's chart of accounts is maintained by Financial Affairs.

Company Cost Center (CCC)A company cost center (normally referred to as cost

center) is the smallest classification in our accounting structure hierarchy. It is the basic building block of the Departmental Accounting, Reporting, and Tracking (DART) system. When any transaction or financial activity takes place, a cost center is used to record the accounting information. Each cost center is assigned to a budgetary unit.

The University’s cost center structure consists of a 15-digit number made up of four sets of identifiers.

Company Center Function Project

XXXX XXXXX XX XXXX

CompanyThe first four digits in the company cost center refer to the

company to which a cost center belongs. It identifies the type of fund and fund location.

Company - first 2 digits

Company - third digit Note: does not pertain to auxiliary or federal formula fund companies

Company - Location of fund - last digit

01 – Educational and General fund –Current funds 0 – General 1 – System Administration02 – Auxiliary funds – Current funds 1 – Dedicated funds 2 – Fayetteville03 – Gifts and grants – Current funds 2 – Service and Revolving 3 – Agriculture Experiment Station04 – Research – Current funds 3 – Grants and Contracts - Cost Sharing 4 – Cooperative Extension Service05 – Loan funds 4 – Dedicated funds 5 – Archeological Survey

06 – Endowment funds5 – Walton Matching Foundation funds or Cost Share Centrally funded 6 - Criminal Justice Institute

07 – Plant funds 6 – Walton Foundation funds 7 – Clinton School08 – Renewals and replacements 7 – Gifts and grants 8 – AREON09 – Debt retirement 8 – Restricted gifts 9 – Winthrop Rockefeller Institute10 – Physical properties 9 – Foundation funds11 – Agency funds99 – Cash Pool

Auxiliary Companies

0202 – Fayetteville Auxiliary Enterprises0212 – Fayetteville – Athletics0222 – Fayetteville – Women’s Athletics (no longer used)0232 – Fayetteville – Bookstore0242 – Fayetteville - Housing

Federal Formula Funds Companies

0313 – AGRI Experiment Station -Hatch0323 – AGRI Experiment Station -Regional Research0333 – AGRI Experiment Station -McIntire Stennis0343 – AGRI Experiment Station -Animal Health

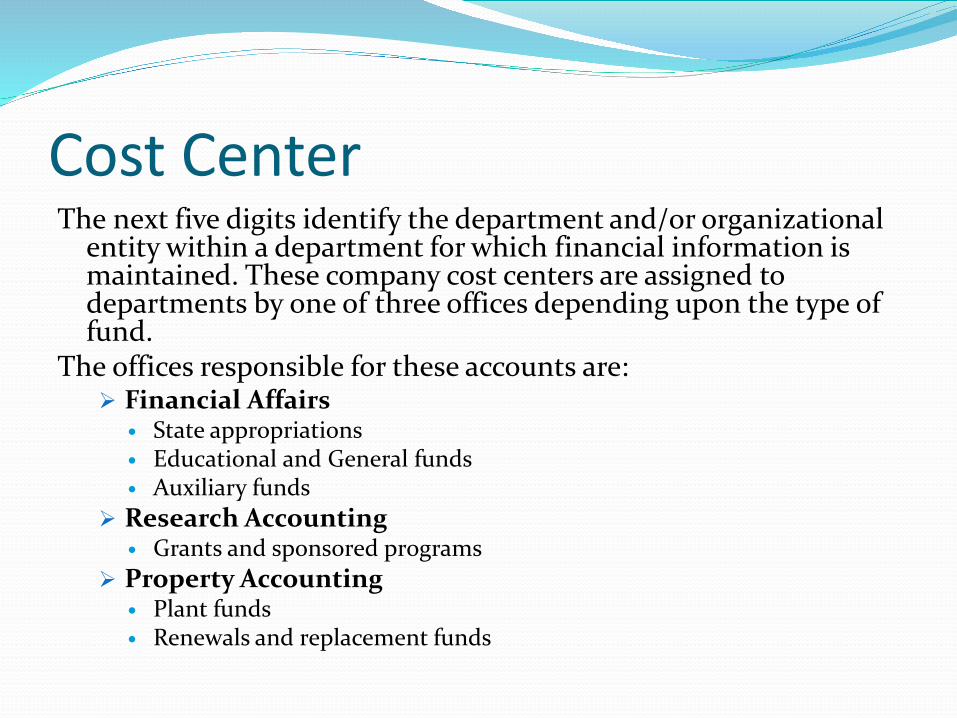

Cost CenterThe next five digits identify the department and/or organizational

entity within a department for which financial information is maintained. These company cost centers are assigned to departments by one of three offices depending upon the type of fund.

The offices responsible for these accounts are: Financial Affairs

State appropriations Educational and General funds Auxiliary funds

Research Accounting Grants and sponsored programs

Property Accounting Plant funds Renewals and replacement funds

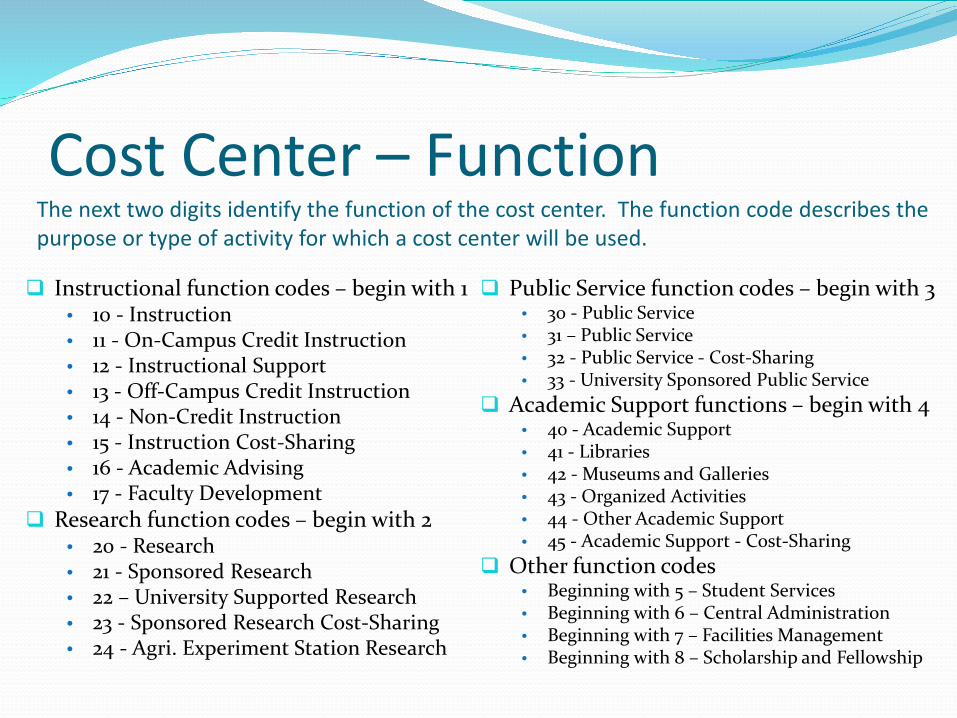

Cost Center – Function The next two digits identify the function of the cost center. The function code describes the purpose or type of activity for which a cost center will be used.

Instructional function codes – begin with 1 • 10 - Instruction • 11 - On-Campus Credit Instruction • 12 - Instructional Support • 13 - Off-Campus Credit Instruction • 14 - Non-Credit Instruction • 15 - Instruction Cost-Sharing • 16 - Academic Advising • 17 - Faculty Development

Research function codes – begin with 2• 20 - Research • 21 - Sponsored Research • 22 – University Supported Research • 23 - Sponsored Research Cost-Sharing • 24 - Agri. Experiment Station Research

Public Service function codes – begin with 3• 30 - Public Service • 31 – Public Service • 32 - Public Service - Cost-Sharing • 33 - University Sponsored Public Service

Academic Support functions – begin with 4• 40 - Academic Support • 41 - Libraries • 42 - Museums and Galleries • 43 - Organized Activities • 44 - Other Academic Support • 45 - Academic Support - Cost-Sharing

Other function codes• Beginning with 5 – Student Services• Beginning with 6 – Central Administration• Beginning with 7 – Facilities Management• Beginning with 8 – Scholarship and Fellowship

Cost Center - ProjectThe last four digits of the cost center are used to further

define the cost center. Usually referred to as the project. Primarily used for project reporting in the Agricultural Experiment Station area.

Departmental Accounting Cost Center (DAC)

The departmental accounting cost center is normally the company cost center, but in the case of the Agri Experiment Station, it does not include the last four digits (project) of the cost center number. Special processing is used for Agriculture Experiment Station cost centers where the last four digits in the cost center in the balance file will be set to 0100 (except for companies 0133, 0373 and 0403 which will be set to 0001).

Agriculture Experiment Station uses the last four digits of the company cost center (called the project number) to support project accounting. The budgets for these projects, however, are posted to the departmental accounting cost centers (DAC). Expenditures are maintained and tracked at the project level. Normally, Agriculture Experiment Station prefers to view the balances at a summary level and therefore, DART employs the use of the departmental accounting center (DAC) which is defined as agriculture's cost centers ending in 0100 or 0001. All accounting transactions for Agriculture are posted to the cost center and the departmental accounting center which give them the opportunity to view their financial activity at a departmental accounting center level or the cost center project level.

Account CodesAn Account Code is a general ledger eight digit number

that represents the category, class code, and object code or ID. The first 2 digits represent the category, the third digit represents the transaction code, and the last five digits represent the object code.

Category Transaction Code 00 - Assets, Liabilities 1 - Asset10 - Salaries 2 - Liability20 - Wages 3 - Fund Balance30 - Fringe Benefits 4 - Revenue40 - Computer Allocation 5 - Expense60 - General Expenses 6 - Estimated Revenue70 - Travel 7 - Budget80 - Capital Outlay 8 - Interfund Transfer90 - Revenue 9 - Intrafund Transfer

Balance Forward Account Code 9078888

Budgetary Unit (BU)A budgetary unit is an organizational entity that either

receives a budget or has staff. It exists between the cost center and department levels. All cost centers are associated with a budgetary unit, and all budgetary units are associated with a department.

Chancellor

Provost and Vice Chancellor for

Academic Affairs

Vice Chancellor for Finance &

Administration

Vice Chancellor for Government &

Community Relations

Vice Chancellor for University

Advancement

Vice Chancellor for Intercollegiate

Athletics

Affirmative Action

Vice Chancellor/Director Level (VC)

Dale Bumpers College of Agricultural, Food & Life SciencesCollege of EngineeringFay Jones School of ArchitectureJ. William Fulbright College of Arts & SciencesSchool of Continuing Education and Academic OutreachCollege of Education and Health ProfessionalsGraduate School

Sam M. Walton College of BusinessSchool of LawHonors CollegeUniversity Libraries

Dean/Director/Associate Vice Chancellor Level

(DDAVC)

BASIS

Business Affairs

Facilities Management

Financial AffairsFinancial Management & Analysis

Human Resources

Information Technology Services

University Police

AccountingEconomicsFinanceInformation SystemsManagementMarketing & LogisticsWCOB Dean’s Office

Departments (DP)

Applied Sustainability Center

Center for Economic Education

Ctr for Management & Executive Education

County Financial Management System

Center for Retailing Excellence Bus Admin Lab Equipment Garrison Financial Institute

Information Technology Research InstitutOutreach Programs

Radio Frequency Identification Center

Small Business Development Center

Supply Chain Management Research Center

Tyson Ctr-Faith & Spirituality in Workpl

The Sustainability Consortium

Budgetary Units (BU)

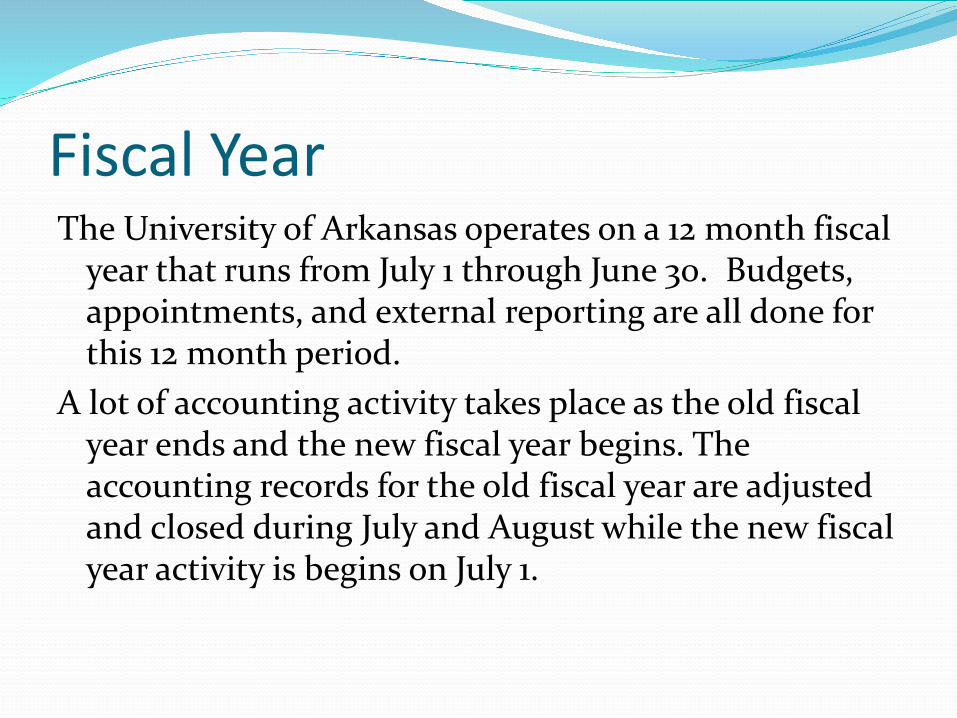

Fiscal YearThe University of Arkansas operates on a 12 month fiscal

year that runs from July 1 through June 30. Budgets, appointments, and external reporting are all done for this 12 month period.

A lot of accounting activity takes place as the old fiscal year ends and the new fiscal year begins. The accounting records for the old fiscal year are adjusted and closed during July and August while the new fiscal year activity is begins on July 1.

Monthly CloseEvery month Financial Affairs closes its accounting

activity for a month (or period). After a month has been closed, no more entries for that month may be posted. This ensures that the ending balances for that month remain intact.

Typically, the monthly close happens around the 5th or 6th working day of the following month. Except of course during the fiscal year end which normally remains open for approximately 3 weeks.

DART PeriodsDART is designed to provide users with flexibility in

posting accounting activity to the appropriate fiscal year. Thus while we normally think of accounting periods in terms of the past, in DART they are also open far into the future. This means that in some cases you may post an entry that will be effect at a future date, and that entry will not affect balances until the month in which that entry is effective. For example, salary encumbrances (posted in a batch process) are spread across periods in the fiscal year.

Institutional CategoryA predefined code, eight characters or less, used to

identify highest level of categorization of budget. This is the level at which the institution budgets. For example, "Maint" is the institutional category for maintenance. Departments may break their budgets down into a more detailed categories, but those categories must be within the same institutional category.

Departmental CategoryA code, eight characters or less, used to categorize

budget, expense, estimated revenues, revenues, and other financial activity at a more detail level useful to departments. For example, "SupOff" is the departmental category for office supplies, which would be considered maintenance at the institutional level. These categories may be listed by using a list such as LCAT (List Categories) or LCIC (List Categories for an Institutional Category) in DART.

If a category is needed that does not exist, please contact Financial Affairs.

Budget and Estimated RevenueBudget and estimated revenue transactions are normally

generated by the PSB system. Once the operating budget is finalized, balances within DART are updated accordingly. All of the budget is posted to the July month of the next fiscal year in the institutional categories. The department then has the option to distribute budget to departmental categories within that institutional category, and/or to distribute budget amounts over the next 12 months. Fringe benefits budgets are calculated and posted according to the salary to which it relates.

RevenuesRevenues are monetary inflows received by

the department as a result of carrying out its mission and operations. These may include internal service billings, sales, service fees, application fees, and registration fees.

ExpendituresExpenditures are charges for goods or

services purchased by the department to carry out its mission. Some common expenditures in your department may include salaries, supplies, travel, communications, utilities, and equipment.

Expenditures also measure the monetary outflows that relate to the provided services or the operating activities of the department.

CommitmentsA commitment represents a requisition amount that

have not been assigned a purchase order number. The requisition has been approved by all reviewers.

PendingAn e-business charge that has downloaded, but not yet

expensed. E-business charges include: Office Max partner, VWR, Voyager, procurement (P-Card) card, and administrative travel (T-Card) card.

The charges download using the default cost center on the PA (Procurement Authorization), but can be moved to other approved cost centers. The Pending amounts are updated as the cost centers and/or categories are changed.

EncumbrancesAn encumbrance is a means of reserving funds for future

expenditures. Purchase orders and salaries are recorded, committing such funds for future payment. Encumbrances are reversed (or relieved) when the actual expenditure is posted. Not all commitments are encumbered, such as blanket purchase orders, phone charges, utilities, and hourly wages.

Planned ActivityThe purpose of the PLAN function in the DART

application is to identify by Departmental Account Center and Category, anticipated expenses, credits, or revenue that will be incurred over a course of the FY, for which it is either not feasible or allowable to setup an encumbrance. Plans are never physically deleted, but are merely made to no longer be outstanding –either by the user doing a virtual delete (action D), the system matching the plan to an Accounting Transaction, or reaching the expiration date for the planned activity.

Balance ForwardAt the end of the year, remaining balances must be

brought forward from the old year to the new year. The transactions which do this are called balance forwards. Balance forward entries are processed by Financial Affairs using journal entries.

Balance forward entries post to DART as budget amounts. The account code used is 90788888.