GSE Reform Research (Fed Reserve Bank)

71

FANNIE MAE &FREDDIE MAC:NEXT STEPS ACASE &PLAN FOR PRIVATIZATION Report to the Federal Reserve Bank of Cleveland March 2009 Haig Panossian Candidate for Master in Public Policy 2009 John F. Kennedy School of Government, Harvard University Advisor: Professor Akash Deep

-

Upload

haig-panossian -

Category

Documents

-

view

44 -

download

2

Transcript of GSE Reform Research (Fed Reserve Bank)

FANNIEMAE&FREDDIEMAC:NEXTSTEPSACASE&PLANFORPRIVATIZATION

Report to the Federal Reserve Bank of Cleveland

March 2009

Haig Panossian

Candidate for Master in Public Policy 2009

John F. Kennedy School of Government, Harvard University

Advisor: Professor Akash Deep

1

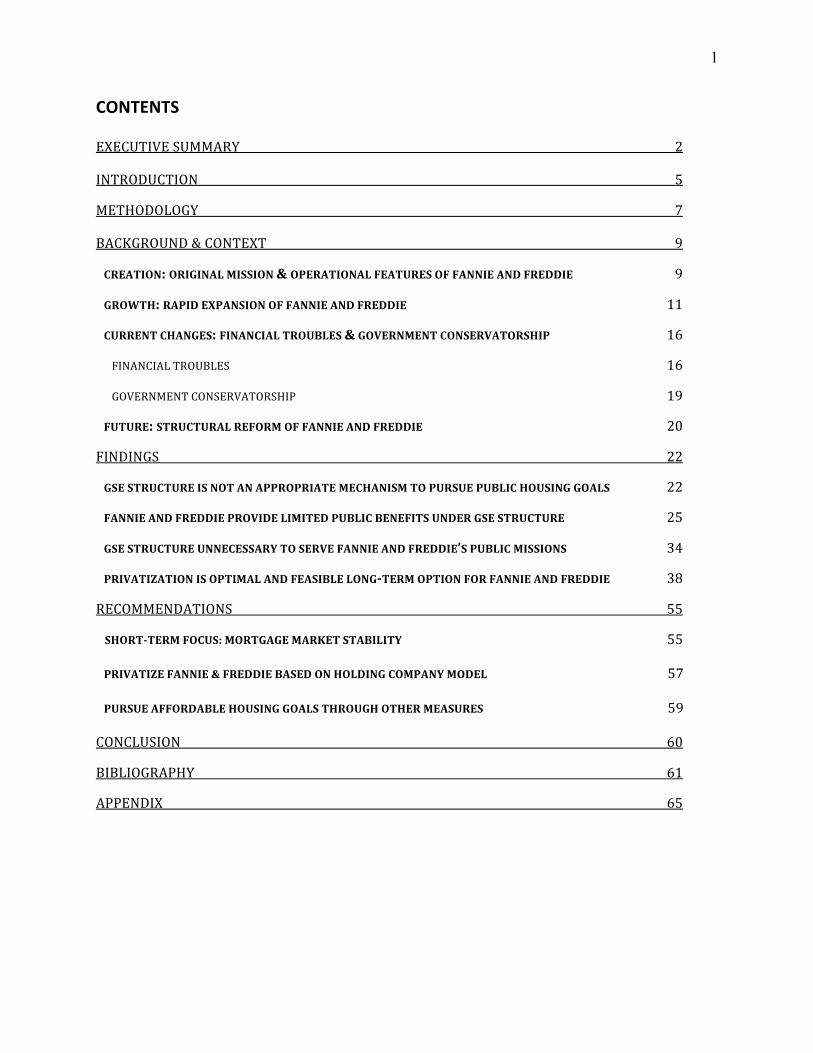

CONTENTS

EXECUTIVESUMMARY 2

INTRODUCTION 5

METHODOLOGY 7

BACKGROUND&CONTEXT 9

CREATION:ORIGINALMISSION&OPERATIONALFEATURESOFFANNIEANDFREDDIE 9

GROWTH:RAPIDEXPANSIONOFFANNIEANDFREDDIE 11

CURRENTCHANGES:FINANCIALTROUBLES&GOVERNMENTCONSERVATORSHIP 16

FINANCIALTROUBLES 16

GOVERNMENTCONSERVATORSHIP 19

FUTURE:STRUCTURALREFORMOFFANNIEANDFREDDIE 20

FINDINGS 22

GSESTRUCTUREISNOTANAPPROPRIATEMECHANISMTOPURSUEPUBLICHOUSINGGOALS 22

FANNIEANDFREDDIEPROVIDELIMITEDPUBLICBENEFITSUNDERGSESTRUCTURE 25

GSESTRUCTUREUNNECESSARYTOSERVEFANNIEANDFREDDIE’SPUBLICMISSIONS 34

PRIVATIZATIONISOPTIMALANDFEASIBLELONGTERMOPTIONFORFANNIEANDFREDDIE 38

RECOMMENDATIONS 55

SHORTTERMFOCUS:MORTGAGEMARKETSTABILITY 55

PRIVATIZEFANNIE&FREDDIEBASEDONHOLDINGCOMPANYMODEL 57

PURSUEAFFORDABLEHOUSINGGOALSTHROUGHOTHERMEASURES 59

CONCLUSION 60

BIBLIOGRAPHY 61

APPENDIX 65

2

EXECUTIVE SUMMARY

The Fannie Mae-Freddie Mac crisis may have been the most avoidable financial crisis in

history.1 For years before the crisis, critics warned about the macroeconomic risks and potential

taxpayer costs of these two housing government-sponsored enterprises (GSE) due to their GSE

status. Nevertheless, due to the “off-budget” nature of Fannie and Freddie’s costs to taxpayers,

effective lobbying, and a broad perception that housing GSEs were valuable and cost-free policy

measures to provide affordable housing, warnings generally fell on deaf ears.

However, by 2008, the housing market crash had transformed risk into reality. As the value of

mortgage assets Fannie and Freddie held plummeted and their share prices dropped from over

$60 in July 2007 to less than $10 just a year later, the government determined that the two GSEs

were likely to become insolvent and ultimately collapse. On September 7, 2008, facing the

prospect that Fannie and Freddie’s collapse would weaken housing and credit markets and

threaten macroeconomic stability, the government decided to temporarily placed the GSEs under

conservatorship. Although this measure may address immediate-term concerns, policymakers

must ultimately chart a future path for Fannie and Freddie. What is the appropriate structure for

Fannie and Freddie in the future? How should that structure be instituted?

The Federal Reserve Bank of Cleveland commissioned this report to help answer these

questions. Based on quantitative data, empirical studies, econometric analyses, relevant

literature, and a case study, this report finds that Fannie and Freddie do not provide a continued

public value through their role in the housing market and could be feasibly privatized.

Findings GSE structure is inappropriate policy measure.

The kind of market imperfection that justified government intervention to create a secondary mortgage market no longer exists because the private sector alone can now serve this function. Fannie and Freddie are inappropriate also because they are not narrowly tailored to meet housing goals for targeted homebuyers. They are allowed to purchase and securitize loans far beyond the range that includes most low-income first-

1 King, A. (September 8, 2008). Freddie Mac and Fannie Mae: An Exit Strategy for the Taxpayer. Washington

D.C.: CATO Institute.

3

time buyers. Further, GSEs are inappropriate means of intervention because two attributes essential to the soundness and safety of public companies are nonexistent in a GSE: primary concern for shareholder interests and conferring risks and rewards to investors only. As such, they lack important checks on risky decisions.

Fannie and Freddie provide limited public benefits.

The two housing GSEs claim that they provide affordable housing through lower mortgage rates and increase homeownership in the U.S. Nevertheless, analyses and econometric testing of quantitative data show that Fannie and Freddie have actually produced only limited public benefits. First, their impact on mortgage rates is not statistically significant. Second, reductions in mortgage rates are shown to translate into only small increases in homeownership rates generally and among targeted borrowers.

GSEs are not necessary to serve Fannie and Freddie’s public missions.

Private firms can serve the housing GSEs’ mission to expand homeownership through secondary mortgage market activities. Also, the market as a whole now finances a larger proportion of mortgages for targeted homebuyers than Fannie and Freddie. Indeed, much of the GSEs’ activities function only to boost the size of their retained portfolios, which have no bearing on their public missions.

Privatization of Fannie and Freddie is both optimal and feasible structural reform.

There are strong theoretical and policy arguments to privatize these GSEs, such as reducing their systemic risk and conferring to them essential attributes of safe and sound corporate decision-making. Moreover, the successful privatization of a similar GSE in the student loan market, Sallie Mae, highlights the benefits of privatizing and offers valuable lessons in charting a privatization course, such as the need to undo the effects of governmental sponsorship and the effectiveness of a holding company model in transitioning from GSE to private company. Historically, however, pragmatic challenges have undermined the normative case for privatization. These include political resistance due to effective lobbying and support networks and fear of increased mortgage rates on homeownership. Nevertheless, these historic obstacles can now be overcome because of recent political developments and the many ways to structure a privatization plan to effectively address such challenges. Lastly, compared to either nationalization or retaining them as GSEs but subject to size or regulatory restrictions, privatization is the best option. While a revised GSE structure may reduce systemic risk, it ignores GSEs’ other shortcomings due to their flawed structure, limited public value, and the limits of regulation. Inversely, while nationalization is more responsive to such shortcomings, it does not lower systemic risk. Only privatization addresses both sets of flaws.

This report finds a clear need to reform and privatize Fannie and Freddie. As GSEs, they are

inappropriate, minimally beneficial, and unnecessary means to serve their particular public

housing missions. Any long-term reform should thus remove their GSE status. Weighing various

alternatives, precedents, and key policy considerations, privatization is certainly the optimal

future path for Fannie and Freddie.

4

Recommendations

The U.S. Treasury Department should pursue reforms for Fannie and Freddie that will

successfully help them transition from GSEs to private companies without undermining either

immediate-term concerns or important housing goals. This report recommends that the Treasury

adopt a three-step approach:

Step 1: Short-Term Focus on Mortgage Market Stability

In the current economic environment, private firms are unlikely to adequately serve the secondary mortgage market as would be expected under better conditions. Also, Fannie and Freddie are too financially unstable right now to profitably operate as private firms. Accordingly, the Treasury should continue supporting the FHFA’s role as Fannie and Freddie conservator in the short-term and help finance the companies’ secondary market activities. During this period, the Federal Reserve Board should communicate with the Treasury Department and FHFA and develop a mutually agreeable privatization plan to propose to Congress. There is no set time frame for this period.

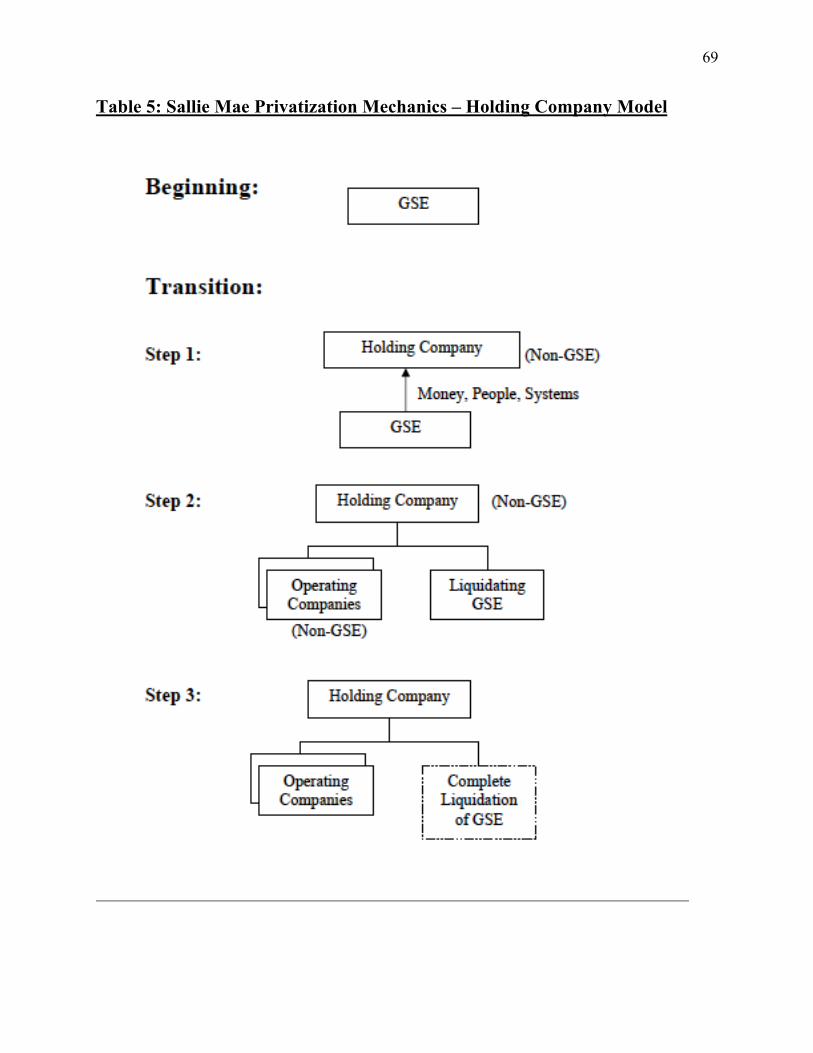

Step 2: Privatize Fannie and Freddie Using Holding Company Model

After the conservatorship period, the housing GSEs should be privatized according to a plan similar to Sallie Mae’s holding company model. As such, Fannie and Freddie should be owned by two different and new holding companies as their GSE subsidiaries. Those two holding companies should also each own a set of numerous other subsidiaries that initially can engage only in non-GSE activities until GSE subsidiaries all liquidate. These non-GSE subsidiaries will eventually represent a privatized form for Fannie and Freddie. Notably, unlike the Sallie model, the plan for Fannie and Freddie creates numerous non-GSE subsidiaries that will eventually form numerous private companies and restricts fund transfers from GSE to non-GSE subsidiaries.

Step 3: Pursue Affordable Housing Goals Through Other Measures

Compared to housing GSEs, there are more narrowly tailored, effective, and efficient policy measures to meet affordable housing goals without posing a systemic risk or contingent taxpayer liability. Although this report does not conduct a detailed evaluation of alternatives, options include down-payment or monthly payment assistance, expansion of other housing programs, a new agency whose sole function is as lender of last resort, or increased funding for nonprofit organizations and public-private partnerships.

5

INTRODUCTION

As of September 7, 2008, Fannie Mae and Freddie Mac, government-sponsored enterprises

(GSE) with a critical role in the U.S. home mortgage market, have been government

conservatorships.2 Previously, akin to all GSEs, Fannie and Freddie were shareholder-owned

corporations with a public mission. However, in accordance with the Federal Housing Finance

Regulatory Reform Act of 2008, enacted July 30, 2008, the Federal Housing Finance Agency

(FHFA), the new housing GSE regulatory agency, is now the Conservator for Fannie and

Freddie.3 As Conservator, the FHFA has assumed the power of Fannie and Freddie’s Board of

Directors and management, with full control of the assets and operations of the two GSEs.4 As

such, GSEs’ CEOs have been replaced and shareholders’ voting rights are suspended until the

termination of the conservatorship period.

Government-sponsored enterprises (GSE) are financial services corporations created by the US

Congress to increase the availability and lower the cost of credit to targeted borrowing sectors.

Sectors in which GSEs have operated include agriculture, home finance, and education. The two

large housing government-sponsored enterprises (GSE) in the United States are Fannie Mae and

Freddie Mac.5 They were created to offer affordable housing to the US community where credit

markets were imperfect by facilitating the stability and liquidity of the secondary residential

mortgage market. For example, in the early 20th century, many potential rural homeowners did

not have ready access to bank loans due to their geographic isolation. Housing GSEs, in

response, would help extend mortgages to rural residents when the mortgage market itself was

insufficient to meet this need.

2 Mark Jickling, "Fannie Mae and Freddie Mac in Conservatorship," CRS Report for Congress, September 15, 2008.

(According to FHFA, a conservatorship is “the legal process in which a person or entity is appointed to establish

control and oversight of a Company to put it in a sound and solvent condition.”) 3 Arnold King, Freddie Mac and Fannie Mae: An Exit Strategy for the Taxpayer, Briefing Papers (Washington D.C.:

CATO Institute, September 8, 2008). 4 Id. 5 This report will not discuss another home finance GSE, Federal Home Loan Banks (FHLB) because their function

is substantially different from that of Fannie and Freddie. Specifically, the FHLB provide advances (i.e. loans) to

member-institutions, such as commercial banks or thrift institutions. The FHLB rely on the mortgages member-

institutions originate as collateral to continue extending more mortgage loans. Unlike Fannie and Freddie, the FHLB

are not allowed to guarantee mortgage-backed securities or to hold mortgages in their portfolios.

6

Credit markets today are much less likely to have market imperfections due to the evolution of

highly efficient financial markets. Nonetheless, Fannie Mae and Freddie Mac continue to exist

and own a large and growing share of the secondary mortgage market. Their size and

concentration has proven to be a huge risk to US economic health and stability, as evidenced by

the subprime mortgage industry’s role in the 2008 economic crisis.

According to FHFA, the purpose of placing Fannie and Freddie into conservatorship is to

preserve and conserve their assets and put them in a sound and solvent condition.6 In doing so,

the FHFA hopes to respond to immediate-term concerns, reasoning that conservatorship would

help restore confidence in Fannie and Freddie, improve the GSEs ability to serve their missions,

mitigate the systemic risk partly responsible for the instability in the current market, and help

provide mortgage financing during a crisis in credit markets.7 Although conservatorship of

Fannie and Freddie may respond to such immediate-term concerns, the government must

eventually implement a long-term plan for the two GSEs. The conservatorship period is

temporary and once its purpose has been adequately met, Congress may redefine the mission and

redesign the structure of Fannie and Freddie. Accordingly, this report focuses on answering the

key questions: What should be done with Fannie and Freddie going forward? How?

The next section details the research methodology used to address these questions. Then, in the

Background and Context section, Fannie and Freddie’s features, mission, growth, risks, financial

troubles, and present conservatorship status are discussed. After providing a contextual

framework for Fannie and Freddie, the Findings section analyzes the quantitative data and

qualitative arguments, drawn from the research methodology discussed earlier, to support four

findings regarding the need to remove Fannie and Freddie’s GSE status and privatize them.

Finally, the Recommendations section lists the three major steps to privatize Fannie and Freddie.

6 Arnold King, Freddie Mac and Fannie Mae: An Exit Strategy for the Taxpayer, Briefing Papers (Washington D.C.:

CATO Institute, September 8, 2008). 7 Id.

7

METHODOLOGY

In deciding the most appropriate structure and role for Fannie and Freddie after the

conservatorship period, some secondary questions were addressed: What were the implications

or consequences of the GSE status of Fannie and Freddie? Are Freddie and Fannie appropriate or

necessary to accomplish their missions? Would private markets better serve these missions? Is

privatization possible? Answering these questions requires a research design that includes

collection and analysis of both quantitative and qualitative data.

Quantitative analyses could be divided into three categories:

1. Empirical Studies of Macroeconomic Effects of Fannie and Freddie GSE Structure: Both before and after placing Fannie and Freddie in conservatorship, many government agency and think tank studies have evaluated the macroeconomic risks and effects of the two companies due to their structure as GSEs. These studies demonstrates the context in which the government decided to place the GSEs in conservatorship and the reasons for broad consent both in and out of government circles to restructure Fannie and Freddie.

2. Empirical Studies of Social Impact of Fannie and Freddie: Numerous government agencies, think tanks, and academicians have published studies that assess and value Fannie and Freddie in different ways. These studies were part of the evaluation of the two GSEs’ impact on mortgage rates and homeownership, social benefits and costs, risks, and public value relative to alternative policy measures. Their statistical methods included regression discontinuity analysis, vector autoregression, and underwriting simulations.

3. Econometric Analyses: Econometric tests were conducted to evaluate the impact of Fannie and Freddie on mortgage rates and homeownership in targeted groups. The tests included a t-test for statistical significance and a regression discontinuity analysis. These tests were based on current and historic data on and trends in Fannie and Freddie, homeownership rates, mortgage rates, and mortgage rate spreads.

While quantitative data and analyses was valuable in measuring the impact and effectiveness of

Fannie and Freddie, qualitative research and analysis would be required to determine the

appropriateness of the GSE structure as a policy mechanism, learn from previous attempts to

reform GSEs, and evaluate various policy responses. As such, qualitative research included:

1. Literature Review: Research of publications from a range of sources was valuable to obtain qualitative information about Fannie and Freddie’s structure, original intent, institutional growth, mission expansion, macroeconomic role, conservatorship, and options for structural

8

change. The literature review included legislative documents, agency publications, statements, and press releases, academic and think tank publications, media articles, and transcripts of interviews with government officials.

2. Case Study: In light of significant similarities between Sallie Mae and Freddie and Fannie, the successful privatization of Sallie Mae was used as a case study with potentially valuable lessons for charting Fannie and Freddie’s future. Despite accounting for the key differences between Fannie and Freddie and Sallie Mae, this case study would help identify requirements of successful privatization and offer lessons in privatizing Fannie and Freddie.

9

BACKGROUND & CONTEXT

Creation: Original Mission & Operational Features of Fannie and Freddie

In the 1930s, housing markets were in turmoil. The wave of bank defaults during the Great

Depression left a large gap in the mortgage lending industry. A typical mortgage required about a

50 percent down payment and a balloon principal payment a few years later. Limitations in

financial and communication technology hindered the transfer of funds between regions of the

country, which was often required to finance homeownership. Congress responded by creating a

series of entities and programs that fostered the development of long-term, amortizing mortgages

and facilitated the movement of capital, including the creation of a government housing agency,

Fannie Mae, in 1938.8 Under budgetary pressures during the Johnson administration, however, in

1968 Congress spun off Fannie Mae to private investors and transformed it into a GSE in 1968.

As a GSE owned by shareholders just like public companies, Congress effectively removed the

Fannie’s expenses from the federal budget. Then in 1970, to prevent monopolistic behavior and

to overcome regulatory impediments in providing mortgage financing in California, Congress

created a new government housing agency, Freddie Mac. In 1989, Freddie was sold to private

investors and became a housing GSE just like Fannie in 1968.

Mission

Under their charters, the mission of Fannie and Freddie is to facilitate the steady flow of low-cost

mortgage funds. Specifically, Freddie Mac’s website states as its goal “to provide liquidity,

stability, and affordability” to the housing market. Similarly, Fannie’s website states that the

company seeks to “expand affordable housing and bring global capital to local communities to

serve the US housing market.” Further, through new legislation in 1992, Congress formally

expanded Fannie and Freddie’s mission to promote homeownership for low-income and minority

households and neighborhoods.9 Thus, Federal Reserve Chairman Ben Bernanke concludes

8 Office of Management and Budget, Budget of the U.S. Government: Fiscal Year 2009 (Washington D.C., 2009),

77. 9 Neil Bhutta, Regression Discontinuity Estimates of the Effects of the GSE Act of 1992, Federal Reserve Board

(Washington D.C., 2009). 1992 Federal Housing Enterprise Financial Safety and Soundness Act (hereinafter “GSE

Act of 1992”)

10

“Congress chartered these two companies with the goal of expanding the amount of capital

available to the residential mortgage market, thereby promoting homeownership, particularly

among low- and middle-income households.”10 Thus, Fannie and Freddie were created to meet

three related goals: (1) to expand homeownership (2) particularly to low- and middle-income

households (3) with affordable housing.

Operational Features

Among the numerous forms available to address a market imperfection through government

intervention, the GSE structure is a popular mechanism for Congress because its costs are hidden

“off-budget”.11 Indeed, even though Fannie Mae had increased liquidity in the market as a

government agency, the Johnson restructured it as a GSE precisely in response to budgetary

pressures during the late 1960s. Thus, by structuring them as private companies with a federally-

chartered public mission, Congress used the GSE structure “as a back-door method to increase

spending on housing without having to go through the appropriations process.”12

Congress envisioned that the specific method by which Fannie and Freddie would serve their

public mission would be to purchase and guarantee mortgages through the secondary mortgage

market. While institutions in the primary mortgage market were wholly responsible for

originating and servicing mortgages, the secondary mortgage allowed the purchase and sale of

mortgage loans and servicing rights between mortgage originators, mortgage aggregators

(securitizers), and investors. The secondary mortgage market could thus free capital and provide

liquidity to mortgage originators so that they, in turn, can extend more home loans.

How could Fannie and Freddie free capital and inject liquidity into the mortgage market? A

prospective homeowner would obtain a mortgage in the primary mortgage market from an

institution that originates and services mortgages in this market, such as a mortgage company or

a commercial bank. These primary market institutions could then sell mortgages (or mortgage-

backed securities (MBS) that have been issued back to them) to secondary market institutions

like Fannie and Freddie, who finance their purchases through debt issues. The sale proceeds from

10 Ben Bernanke, "GSE Portfolios, Systemic Risk, and Affordable Housing," Independent Community Bankers of

America's Annual Convention (Honolulu, March 6, 2007). 11 Vern McKinley, "The Mounting Case for Privatizing Fannie Mae and Freddie Mac," CATO Policy Analysis

(1997), 11. 12 Ibid.

11

this sale to a secondary mortgage market institution then frees up the funds initially used to

originate those mortgages so that the originators can use those funds to originate new mortgages.

Thus, secondary market institutions like Fannie and Freddie ensure that mortgage originators in

the primary market continue to have funds for new mortgages.

Although Fannie and Freddie were assigned a public mission, as public companies whose shares

were traded on the New York Stock Exchange, they were also profit-driven companies with

shareholders. Fannie and Freddie generate profit in two ways:

1. Guarantee Fee Income – Fannie and Freddie retain a certain percentage of each mortgage payment for each mortgage they have guaranteed a timely principal and interest payment of to a MBS holder. Basically, the housing GSEs would hope to collect more in guarantee fee income than they were obligated to pay to MBS holders in the event of borrower default. The MBS the public held have averaged about one-quarter of the US mortgage market and totaled $3.5 trillion as of November 30, 2007.13

2. Retained Portfolios – Fannie and Freddie have huge retained portfolios of mortgages and MBSs. They invest heavily in their own, and each other’s, securities. When GSEs retain securities instead of selling them, they earn a financing profit due to the spread between the retained security yield and interest rate on issued debt.14 Combined mortgage assets of Fannie and Freddie retained portfolios were valued at $1.5 trillion as of June 30, 2008.15

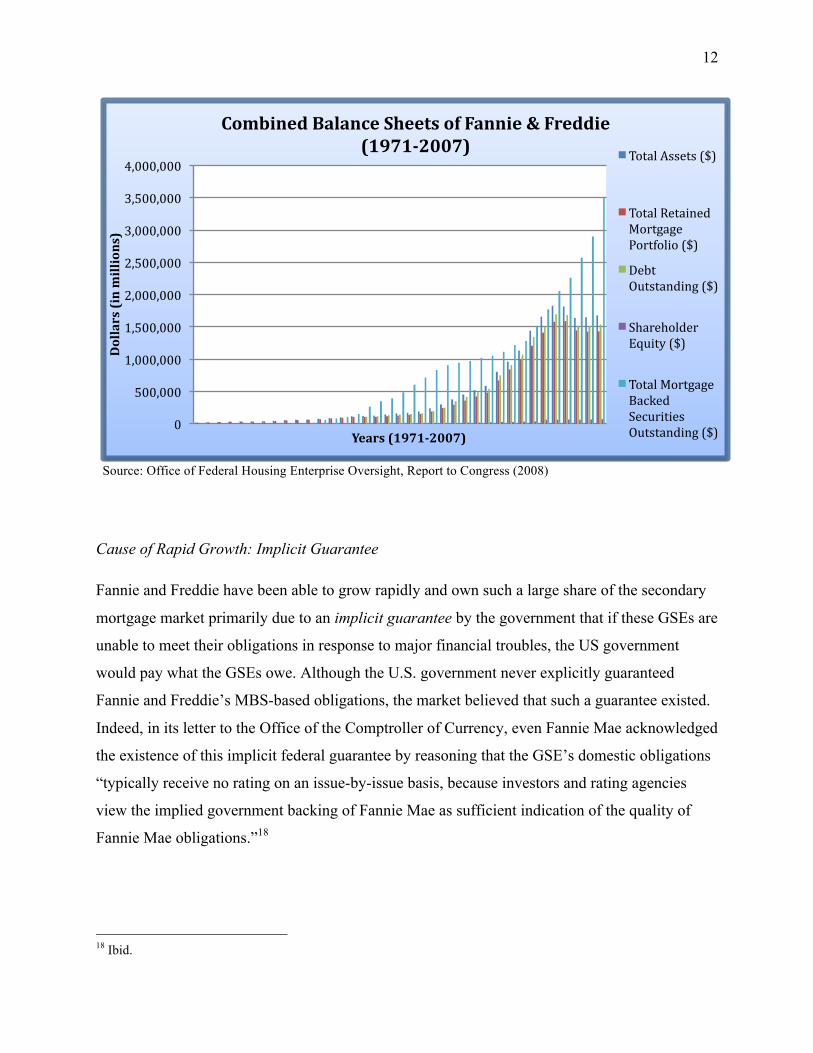

Growth: Rapid Expansion of Fannie & Freddie

Since their creation, Fannie and Freddie have steadily grown at a rapid pace and now own a large

percentage of the secondary housing market. According to then Treasury Secretary Robert K.

Steel, at 2006 year end the combined mortgage portfolios of Fannie and Freddie was $1.4

trillion.16 On average, the combined size of Fannie and Freddie has more than doubled every five

years since 1968.17

13 Office of Management and Budget, Budget of the U.S. Government: Fiscal Year 2009 (Washington D.C., 2009),

78. 14 Wayne Passmore, Shane M. Sherlund Andreas Lehnert, GSEs, Mortgage Rates, and Secondary Market Activities, Federal Reserve Board (Washington D.C., 2006), 3. 15 Jickling (2008) 1. 16 Barry Nielson, Fannie Mae and Freddie Mac, Boon or Boom. 17 Kevin R. Kosar, Government-Sponsored Enterprises (GSEs): An Institutional Overview, CRS Report to Congress

(Washington D.C.: Congressional Research Service, April 23, 2007), 5.

12

Source: Office of Federal Housing Enterprise Oversight, Report to Congress (2008)

Cause of Rapid Growth: Implicit Guarantee

Fannie and Freddie have been able to grow rapidly and own such a large share of the secondary

mortgage market primarily due to an implicit guarantee by the government that if these GSEs are

unable to meet their obligations in response to major financial troubles, the US government

would pay what the GSEs owe. Although the U.S. government never explicitly guaranteed

Fannie and Freddie’s MBS-based obligations, the market believed that such a guarantee existed.

Indeed, in its letter to the Office of the Comptroller of Currency, even Fannie Mae acknowledged

the existence of this implicit federal guarantee by reasoning that the GSE’s domestic obligations

“typically receive no rating on an issue-by-issue basis, because investors and rating agencies

view the implied government backing of Fannie Mae as sufficient indication of the quality of

Fannie Mae obligations.”18

18 Ibid.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

Dollars(inmillions)

Years(19712007)

CombinedBalanceSheetsofFannie&Freddie

(19712007)TotalAssets($)

TotalRetainedMortgagePortfolio($)

DebtOutstanding($)

ShareholderEquity($)

TotalMortgageBackedSecuritiesOutstanding($)

13

The implicit guarantee of federal backing for Fannie and Freddie obligations resulted from the

many valuable benefits Congress conferred upon the GSEs as quasi-governmental entities.19

These express, legislative benefits included exemption from state and local taxes, availability of

a $2.25 billion line of credit from the Treasury, exemption from SEC registration and reporting

requirements, and the designation of GSE securities as “government securities” for purposes of

the SEC Act of 1934. By treating the GSEs almost as favorably as government agencies, these

legislative benefits gave Fannie and Freddie the appearance of fully government guaranteed

entities whose obligations were backed by the government in the event of default.

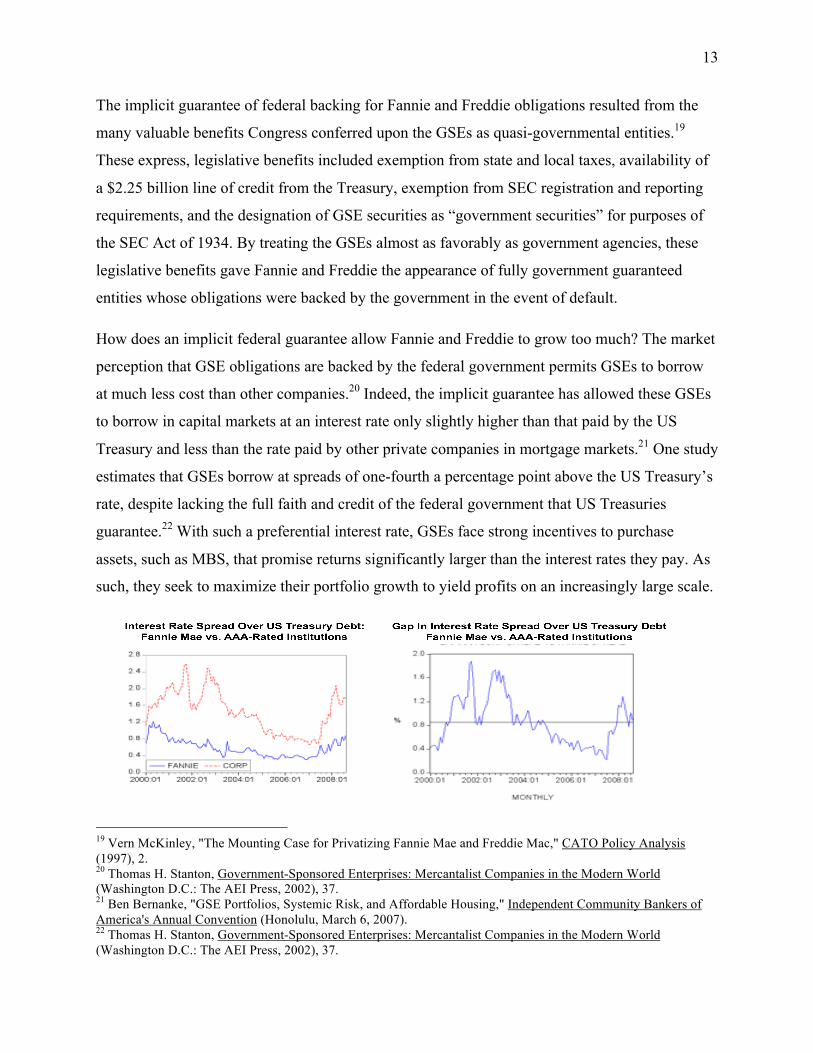

How does an implicit federal guarantee allow Fannie and Freddie to grow too much? The market

perception that GSE obligations are backed by the federal government permits GSEs to borrow

at much less cost than other companies.20 Indeed, the implicit guarantee has allowed these GSEs

to borrow in capital markets at an interest rate only slightly higher than that paid by the US

Treasury and less than the rate paid by other private companies in mortgage markets.21 One study

estimates that GSEs borrow at spreads of one-fourth a percentage point above the US Treasury’s

rate, despite lacking the full faith and credit of the federal government that US Treasuries

guarantee.22 With such a preferential interest rate, GSEs face strong incentives to purchase

assets, such as MBS, that promise returns significantly larger than the interest rates they pay. As

such, they seek to maximize their portfolio growth to yield profits on an increasingly large scale.

19 Vern McKinley, "The Mounting Case for Privatizing Fannie Mae and Freddie Mac," CATO Policy Analysis

(1997), 2. 20 Thomas H. Stanton, Government-Sponsored Enterprises: Mercantalist Companies in the Modern World (Washington D.C.: The AEI Press, 2002), 37. 21 Ben Bernanke, "GSE Portfolios, Systemic Risk, and Affordable Housing," Independent Community Bankers of

America's Annual Convention (Honolulu, March 6, 2007). 22 Thomas H. Stanton, Government-Sponsored Enterprises: Mercantalist Companies in the Modern World

(Washington D.C.: The AEI Press, 2002), 37.

14

By lowering the cost of borrowing and allowing Fannie and Freddie to earn profits greater than

competitors in the secondary mortgage market, the implicit guarantee confers a federal subsidy

to the GSEs. Specifically, the value of the subsidy in a given year equals the value of interest

savings on new securities originated that year.23 The Congressional Budget Office (CBO) defines

this value of interest savings on newly originated securities as “the spread between the rates on

the enterprises’ securities and those originated by financial firms with comparable ratings.”24

CBO estimates that this subsidy is 41 basis points on debt and 3 basis points on MBS.

The federal subsidy to Fannie and Freddie in the form of lower interest rates is also reflected by

the amount of the housing GSEs’ total subsidy. According to CBO’s 2004 update to an earlier

study estimating the total subsidies to housing GSEs, the federal government’s subsidy to the

housing GSEs amounted to roughly $19.6 billion in 2003 (the last year for which the CBO

published estimates of subsidy to housing GSEs.)25 Notably, this base case estimate is based on

the assumption that mortgages purchased by GSEs and the MBS they issue to finance them have

an average life of seven years and will not be reissued upon maturity. However, consistent year-

over-year increases in the GSEs’ outstanding securities and assets suggest that this assumption is

inaccurate. Instead, it is more likely that future growth in outstanding debt and MBS will be

sustained and securities will be reissued when they mature. Accordingly, the federal subsidy

would more than double the base case estimate to $41.7 billion.26

Risks of Fannie & Freddie’s GSE Structure

Critics of housing GSEs worry about their systemic risk to the U.S. economy and financial risk

to taxpayers. They argue that by facilitating the growth and huge market share of Fannie and

Freddie, this implicit guarantee results in a major systemic risk and contingent liability for

taxpayers if the GSEs faced major financial troubles. Systemic risk is “the risk that disruptions

occurring in one firm or financial market may spread to other parts of the financial system, with

possibly serious implications for the performance of the broader economy.”27

23 Congressional Budget Office, "Updated Estimates of the Subsidies to the Housing GSEs," (2004), 1. 24 Ibid. 25 Ibid 10. The CBO study data includes three housing GSEs – Fannie, Freddie, and the FHLB. This report has

adjusted the CBO study’s data to exclude FHLB. 26 Ibid 8. 27 Ben Bernanke, "GSE Portfolios, Systemic Risk, and Affordable Housing," Independent Community Bankers of

America's Annual Convention (Honolulu, March 6, 2007).

15

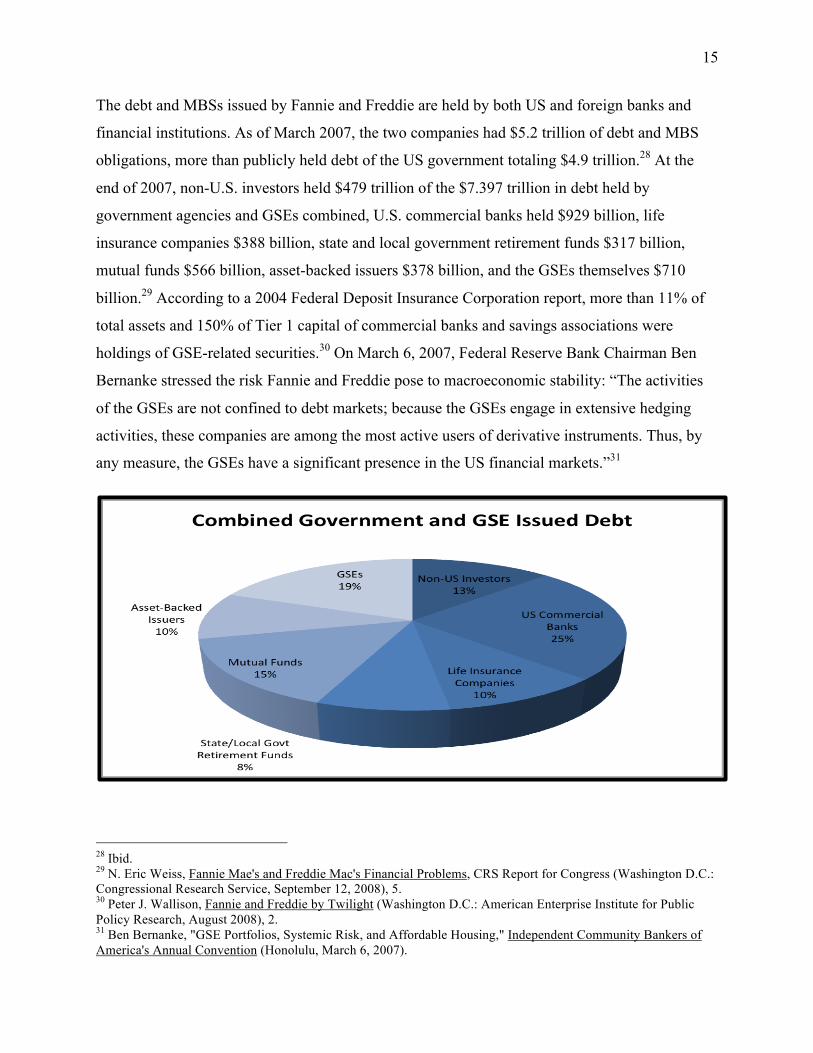

The debt and MBSs issued by Fannie and Freddie are held by both US and foreign banks and

financial institutions. As of March 2007, the two companies had $5.2 trillion of debt and MBS

obligations, more than publicly held debt of the US government totaling $4.9 trillion.28 At the

end of 2007, non-U.S. investors held $479 trillion of the $7.397 trillion in debt held by

government agencies and GSEs combined, U.S. commercial banks held $929 billion, life

insurance companies $388 billion, state and local government retirement funds $317 billion,

mutual funds $566 billion, asset-backed issuers $378 billion, and the GSEs themselves $710

billion.29 According to a 2004 Federal Deposit Insurance Corporation report, more than 11% of

total assets and 150% of Tier 1 capital of commercial banks and savings associations were

holdings of GSE-related securities.30 On March 6, 2007, Federal Reserve Bank Chairman Ben

Bernanke stressed the risk Fannie and Freddie pose to macroeconomic stability: “The activities

of the GSEs are not confined to debt markets; because the GSEs engage in extensive hedging

activities, these companies are among the most active users of derivative instruments. Thus, by

any measure, the GSEs have a significant presence in the US financial markets.”31

28 Ibid. 29 N. Eric Weiss, Fannie Mae's and Freddie Mac's Financial Problems, CRS Report for Congress (Washington D.C.: Congressional Research Service, September 12, 2008), 5. 30 Peter J. Wallison, Fannie and Freddie by Twilight (Washington D.C.: American Enterprise Institute for Public

Policy Research, August 2008), 2. 31 Ben Bernanke, "GSE Portfolios, Systemic Risk, and Affordable Housing," Independent Community Bankers of

America's Annual Convention (Honolulu, March 6, 2007).

16

Further, unlike other private firms, the risk these GSEs pose cannot be expected to be mitigated

through market discipline. Typically, market disciplines curbs excessive risk-taking because the

creditors of a firm have strong incentives to monitor risky activities. If creditors believe that a

firm is taking on too much risk, they will respond by either reducing their exposure through

removing their invested capital in the firm or require greater compensation in lieu of the

additional risk. However, market discipline by creditors does not restrain risky behavior by

Fannie and Freddie because creditors believe that these two GSEs are backed by the US

government’s “implicit guarantee.”32

Current Changes: Financial Troubles & Government Conservatorship

Financial Troubles

In July 2007, both Fannie and Freddie shares traded above $60. Between July 8 and 15, 2008,

however, Fannie and Freddie’s shares fell from $17.51 and $13.46 to $7.02 and $5.26,

respectively.33 Share prices fell because the credit risk of Fannie and Freddie materialized. Credit

risk indicates the impact borrower defaults will have on the lender. When home prices are rising,

there is less risk of mortgage default. In a February 6, 2004 speech, the chairman of Fannie Mae,

Franklin Raines, argued that although Fannie is highly leveraged, it is not a significant risk to the

government or taxpayers because it invests in home mortgages, one of the safest investments in

the world.”34 However, since US home prices peaked in July 2006, they have declined 19.3% on

a cumulative basis and are currently back to the lowest price level since May 2004.35

32 Douglas Holtz-Eakin, "Aligning the Costs and Benefits of the Housing Government-Sponsored Enterprises," CBO Testimony (Washington D.C.: Committee on Banking, Housing, and Urban Affairs, April 21, 2005), 8. 33 Jickling (2008) 2. 34 Thomas H. Stanton, Bert Ely Peter J. Wallison, Privatizing Fannie Mae, Freddie Mac, and the Federal Home Loan

Banks: Why and How, American Enterprise Institute (Washington D.C.: The AEI Press, 2004), 4. 35 First American Core Logic, Media Alert: February 18, 2009, available at: http://www.loanperformance.com/

17

Source: Fannie Mae

With declining home prices, homeowners began defaulting on mortgages in unexpected

numbers. In 2004, William Poole, President of the Federal Reserve Bank of St. Louis, expressed

his confidence in Fannie and Freddie’s credit risk mitigation measures, not considering home

prices may drop nationwide: “Even though default rates on mortgages in the United States are

low, in recent years less than 1 percent, they are not zero and vary considerably across regions.

Credit risk on mortgages can be handled, as in fact Fannie and Freddie do very effectively … In

assessing credit risk, it is important not to focus just on national average conditions. For

example, although average house prices in the United States have not declined year to year since

the Great Depression, prices have declined in particular significant markets.”36

Falling home prices may not have triggered such huge spikes in default rates had it not been for

Fannie and Freddie’s role in greatly increasing subprime and Alt-A mortgages.37 By 2007,

Fannie and Freddie were required to show that 55% of their total mortgage purchases were low-

36 William Poole, "GSE Risks," Speech to St. Louis Society of Financial Analysts (Federal Reserve Bank of St.

Louis, January 13, 2005). 37 Peter J. Wallison, Cause and Effect: Government Policies and the Financial Crisis, American Enterprise Institute:

Financial Services Outlook (November 2008) (stating “There is no universally accepted definition of either

subprime or Alt-A loans, except that neither of them is considered a prime loan (fifteen- or thirty-year amortization,

fixed interest rate, good credit history) and both thus represent enhanced risk. The Federal Reserve Bank of New

York defines a subprime loan as one made to a borrower with blemished credit or who provides only limited

documentation. The federal bank regulators define a loan to a borrower with less than a 660 FICO score as subprime. Alt-A loans generally have a higher balance than subprime and one or more elements of added risk, such

as a high loan-to-value ratio (often as a result of a piggyback second mortgage), interest-only payments, little or no

income documentation, and the borrower as an investor rather than a homeowner. The term "subprime,"

accordingly, generally refers to the financial capabilities of the borrower, while Alt-A loans generally refer to the

quality of the loan terms.” p. 5)

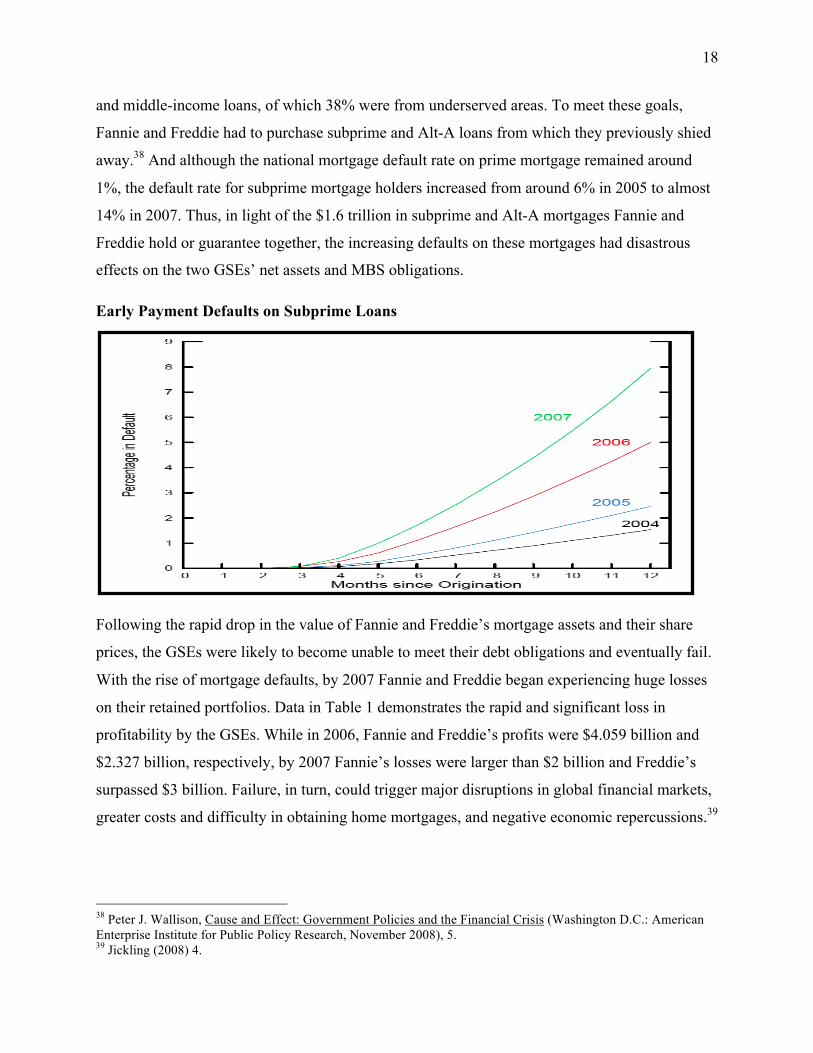

18

and middle-income loans, of which 38% were from underserved areas. To meet these goals,

Fannie and Freddie had to purchase subprime and Alt-A loans from which they previously shied

away.38 And although the national mortgage default rate on prime mortgage remained around

1%, the default rate for subprime mortgage holders increased from around 6% in 2005 to almost

14% in 2007. Thus, in light of the $1.6 trillion in subprime and Alt-A mortgages Fannie and

Freddie hold or guarantee together, the increasing defaults on these mortgages had disastrous

effects on the two GSEs’ net assets and MBS obligations.

Early Payment Defaults on Subprime Loans

Following the rapid drop in the value of Fannie and Freddie’s mortgage assets and their share

prices, the GSEs were likely to become unable to meet their debt obligations and eventually fail.

With the rise of mortgage defaults, by 2007 Fannie and Freddie began experiencing huge losses

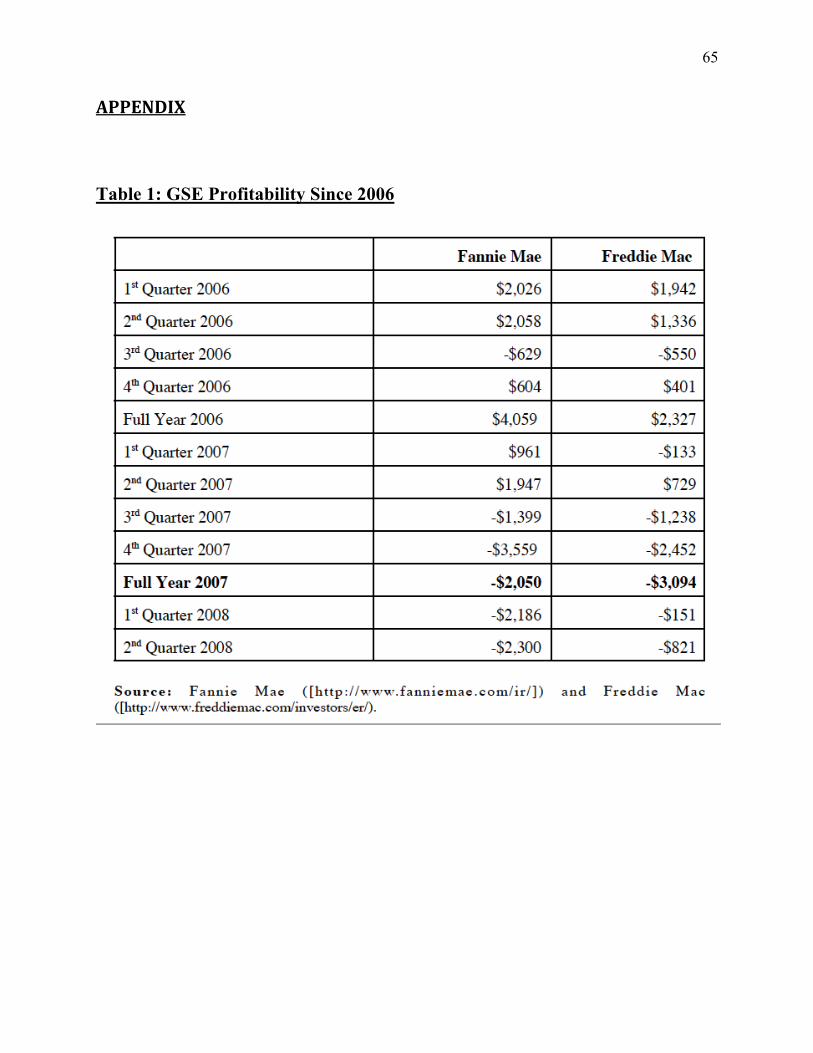

on their retained portfolios. Data in Table 1 demonstrates the rapid and significant loss in

profitability by the GSEs. While in 2006, Fannie and Freddie’s profits were $4.059 billion and

$2.327 billion, respectively, by 2007 Fannie’s losses were larger than $2 billion and Freddie’s

surpassed $3 billion. Failure, in turn, could trigger major disruptions in global financial markets,

greater costs and difficulty in obtaining home mortgages, and negative economic repercussions.39

38 Peter J. Wallison, Cause and Effect: Government Policies and the Financial Crisis (Washington D.C.: American

Enterprise Institute for Public Policy Research, November 2008), 5. 39 Jickling (2008) 4.

19

Government Conservatorship

As of 2008, Fannie and Freddie were unable to access capital markets without governmental

financial assistance. Without access to new capital, the GSEs would have to stop new business

and shed their assets in a weak market.40 This would, in turn, have disastrous implications for

both the mortgage markets and the GSEs since mortgage rates would continue to increase,

Fannie and Freddie shares would then drop in price, and credit losses would have increased.

In 2008, FHFA concluded that the two GSEs would be insolvent and government intervention

was necessary. FHFA Director James B. Lockhart decided that “in order to restore the balance

between safety and soundness and mission, FHFA placed Fannie Mae and Freddie Mac into

conservatorship. That is a statutory process designed to stabilize a troubled institution with the

objective of maintaining normal business operations and restoring its safety and soundness.”41

Further, the FHFA’s determination that Fannie and Freddie needed to be placed in

conservatorship was supported by both the Chairman of the Board of Governors of the Federal

Reserve System, Ben Bernanke,42 and Secretary of the Treasury, Henry Paulson.43

A central goal of the conservatorship plan is to keep the financial operations and conditions of

the GSEs solvent and sustainable by providing government financing to Fannie and Freddie.

Under the September 7, 2008 conservatorship plan, several government agencies extend various

forms of capital investments totaling $100 billion in each GSE. These include Federal Reserve

purchases of GSE debt and GSE-held mortgage backed securities and Treasury Department

purchases of GSE stock and MBS. The Treasury’s commitments end on December 31, 2009,

when the GSEs must begin reducing the size of their portfolios by 10% annually. Moreover, on

February 18, 2009, under the new Obama Administration, the federal government doubled its

financial backing of Fannie and Freddie to $200 billion in each. 44

40 James B. Lockhart III, "Statement of The Honorable James B. Lockhart III Before the House Committee on

Financial Services on the Appointment of FHFA as Conservator for Fannie Mae and Freddie Mac" (Washington

D.C., September 25, 2008), 2, 5. 41 Ibid 6. 42 Ben Bernanke, "Statement by Federal Reserve Board Chairman Ben Bernanke," Press Release, September 7, 2008. 43 Henry M. Paulson, Statement by Secretary Henry M. Paulson on Treasury and Federal Housing Finance Agency

Action to Protect Financial Markets and Taxpayers (Washington D.C.: U.S. Department of the Treasury, September

7, 2008). 44 Jickling (2008) 3-5.

20

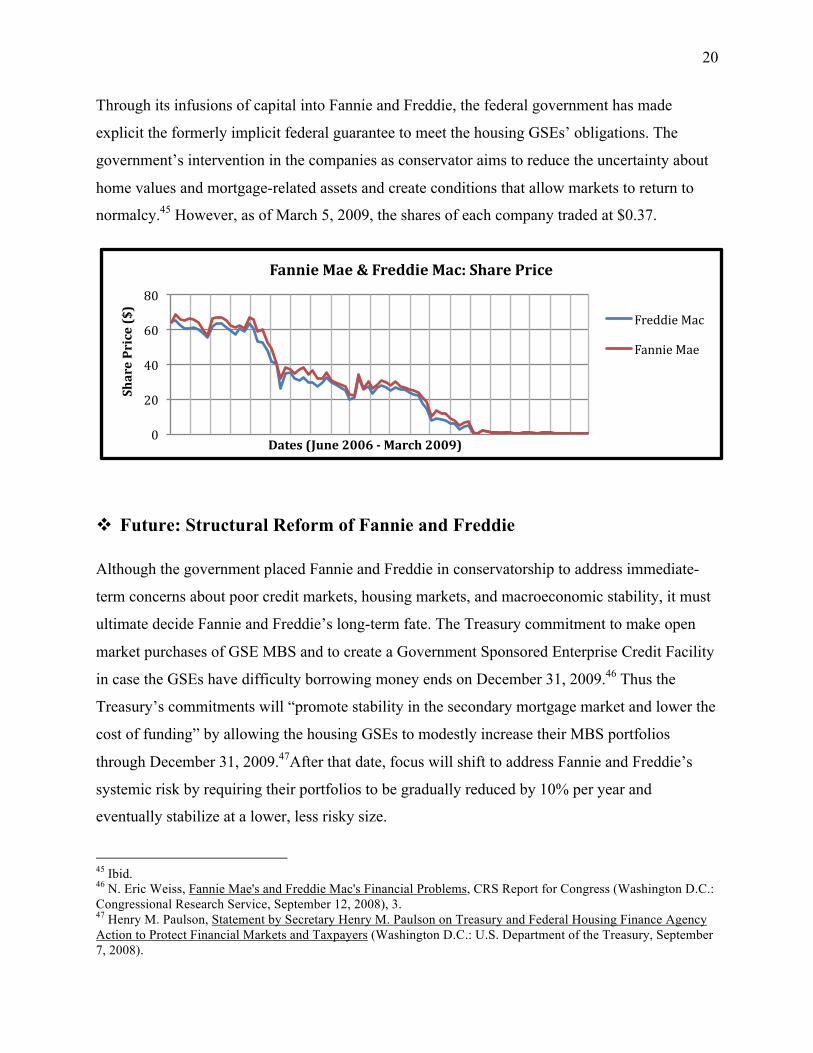

Through its infusions of capital into Fannie and Freddie, the federal government has made

explicit the formerly implicit federal guarantee to meet the housing GSEs’ obligations. The

government’s intervention in the companies as conservator aims to reduce the uncertainty about

home values and mortgage-related assets and create conditions that allow markets to return to

normalcy.45 However, as of March 5, 2009, the shares of each company traded at $0.37.

Future: Structural Reform of Fannie and Freddie

Although the government placed Fannie and Freddie in conservatorship to address immediate-

term concerns about poor credit markets, housing markets, and macroeconomic stability, it must

ultimate decide Fannie and Freddie’s long-term fate. The Treasury commitment to make open

market purchases of GSE MBS and to create a Government Sponsored Enterprise Credit Facility

in case the GSEs have difficulty borrowing money ends on December 31, 2009.46 Thus the

Treasury’s commitments will “promote stability in the secondary mortgage market and lower the

cost of funding” by allowing the housing GSEs to modestly increase their MBS portfolios

through December 31, 2009.47After that date, focus will shift to address Fannie and Freddie’s

systemic risk by requiring their portfolios to be gradually reduced by 10% per year and

eventually stabilize at a lower, less risky size.

45 Ibid. 46 N. Eric Weiss, Fannie Mae's and Freddie Mac's Financial Problems, CRS Report for Congress (Washington D.C.:

Congressional Research Service, September 12, 2008), 3. 47 Henry M. Paulson, Statement by Secretary Henry M. Paulson on Treasury and Federal Housing Finance Agency

Action to Protect Financial Markets and Taxpayers (Washington D.C.: U.S. Department of the Treasury, September

7, 2008).

0

20

40

60

80

SharePrice($)

Dates(June2006March2009)

FannieMae&FreddieMac:SharePrice

FreddieMac

FannieMae

21

In addition to the termination of Treasury commitments, the conservatorship of Fannie and

Freddie is only temporary and will end when the FHFA Director concludes that the safety and

soundness of the GSEs has been restored.48 Following an FHFA finding that the conservatorship

has achieved its mission, the federal government must determine the future of the two housing

GSEs. Treasury Secretary Paulson stresses that “Policymakers must view this next period as a

‘time out’ where we have stabilized the GSEs while we decide their future role and structure …

We will make a grave error if we don’t use this time out to permanently address the structural

issues presented by the GSEs.”49 Thus, the government must answer: What is the appropriate

structure for Fannie and Freddie in the future?

48 Federal Housing Finance Agency, Questions and Answers on Conservatorship, Fact Sheet (Washington D.C.,

2008). 49 Paulson.

22

FINDINGS

This report discusses four key findings that support the recommended future course and long-

term structural reforms of Fannie and Freddie:

GSE structure is not an appropriate mechanism to pursue Fannie and Freddie’s missions

Fannie and Freddie provide limited public benefits under their GSE structure

Fannie and Freddie are no longer necessary to operate as GSEs to serve their public missions

Privatization is an optimal and feasible long-term option for Fannie and Freddie

GSE Structure is Inappropriate Policy Mechanism

No Inevitable Market Imperfection

Government interventions in markets are appropriate and justified if they are necessary and

narrowly-tailored to correct a market imperfection. A market is imperfect if private firms

produce less of a good or service than socially optimal.50 As discussed earlier, such an

imperfection clearly existed when Fannie and Freddie first became GSEs because of illiquidity in

the mortgage markets, nationwide credit shortages, market instability, regional credit imbalances

and differences in interest rates, difficulties in assessing the credit quality of mortgages, and

foregone positive externalities of increased homeownership.51 Government intervened by using

new agencies to create a secondary mortgage market. Since there was not enough liquidity in the

mortgage markets to allow mortgage originators to meet the demand for home loans, potential

borrowers were either required to offer large sums in down payments or could not obtain a loan

at all. Ultimately, the combination of illiquid mortgage markets, costly down payment

requirements, and high mortgage rates had a negative impact on homeownership rates. Certainly,

a secondary mortgage market where mortgages from originators are bought and securitized

would address the illiquidity problem in mortgage markets by freeing capital for originators to

underwrite new home loans. Before Fannie’s creation in 1938, however, such a secondary

50 Lawrence J. White, "On Truly Privatizing Fannie Mae and Freddie Mac: Why It's Important and How to Do It,"

Fixing the Housing Finance System (Wharton School, University of Pennsylvania, 2005), 14. 51 McKinley (1997) 2.

23

mortgage market did not exist. As such, Congress may well have been justified to intervene and

create a secondary mortgage market.

The case for government intervention in the mortgage markets to correct a market imperfection –

to create a secondary mortgage market – is much less obvious today.52 As quantitative data and

qualitative analysis shows53, commercial banks now have the technology and expertise to

participate in a secondary mortgage market. Indeed, despite no government intervention, the

private sector has created a robust and growing secondary market for automobile loans.54 This

purely privately created secondary market has experienced significant growth, with securitized

automobile loans outstanding increasing from about $18 billion in 1989 to $44 billion in 1995.

As such, the automobile securitization sector epitomizes the innovation in secondary markets

today and the ability that the private sector can be trusted to create and operate an effective

secondary market. Due to the private sector’s ability to correct an historic market imperfection,

government intervention in the mortgage markets through Fannie and Freddie is unjustified and

inappropriate.

GSE Structure is Not Narrowly-Tailored

Further, the use of Fannie and Freddie to expand homeownership by targeted groups is a broad-

based housing policy measure that increases housing consumption and construction throughout

the income and social spectrum and not just among targeted homebuyers.55 For instance, the

median home price in 2008 was about $210,000, and an 80% mortgage on that price would have

been $168,000. Nevertheless, the conforming loans limit for Fannie and Freddie that year was

$417,000, more than twice the 80% mortgage on a median-priced home. The high ceiling for

conforming loans allow Fannie and Freddie to buy home mortgage loans that are far beyond the

range that includes most low- or moderate-income first-time buyers.

52 This analysis only considers Fannie and Freddie mission to expand homeownership broadly through their secondary mortgage market activities and not their mission under the GSE Act of 1992. 53 Refer to page 34-35. 54 McKinley (1997) 8. 55 Lawrence White, Fannie Mae, Freddie Mac, and Housing Finance: Why True Privatization Is Good Public Policy,

Draft, CATO Foundation (Washington D.C., 2004), 11.

24

GSE Structure Results in Companies Lacking Essential Attributes of Corporate Structure

Even if some market imperfection or social need today justified government intervention in

mortgage markets, GSEs are not the appropriate form of intervention because they are supposed

to be public companies yet lack attributes that are essential to the soundness and safety of public

companies: primary concern for shareholder interests and conferring both risks and rewards to

investors. Without these essential elements of the corporate form, managers at Fannie and

Freddie have engaged in excessively risky activities.

Some government officials have complained that minority, low-, and moderate-income

homeownership is too low in the U.S. Indeed, many congressmen complained that while Fannie

and Freddie may have lowered mortgage rates and generated huge gains for their shareholders,

the GSEs did not do enough to increase minority, middle-, and low-income homeownership. In

response, Congress passed the GSE Act of 1992 and mandated that Fannie and Freddie meet

certain housing goals for these targeted homebuyers. To meet these goals, however, the two

GSEs were burdened in balancing their investors’ private interests with a potentially conflicting

public mission. For example, while a private firm accountable only to shareholders would be

reluctant to purchase low-quality, high-risk subprime and Alt-A mortgages, Fannie and Freddie

increasingly bought such loans to meet their government-mandated goals. As recent history

proves, due to the size of their retained portfolios and the guarantees they sold to MBS

purchasers, an increase in the default rate for such risky mortgages results in huge losses for

Fannie and Freddie and a significant drop in their share prices.

A second example also illustrates the financial risks and costs of Fannie and Freddie’s dual

missions. While Congress limits permitted GSE activities through restrictions in a GSE charter to

protect against monopolistic effects in related industries and align GSE activities to a specific

public policy goal, such restrictions impair the ability of GSEs to protect against unexpected

risks and, consequently, threaten their financial stability. Charter limitations on permissible GSE

activities means that a GSE will become specialized in a designated market, unable to protect

itself against financial and political risks in that designated market through diversification.56 As

such, Fannie and Freddie activities in pursuit of their public mandate threaten their financial

56 Thomas H. Stanton, The Privatization of Sallie Mae and Its Consequences (Washington D.C.: American

Enterprise Institute, May 9, 2007), 3.

25

soundness and stability. Thus, the impossible task of “serving two masters” whose interests are

not always aligned renders GSEs an inappropriate means of governmental intervention.

Further, GSEs are inappropriate as a public policy measure because, unlike most other public

companies, they privatize rewards but socialize their costs. Free market proponents trust

company managers to make sound and responsible decisions based on the notion that recipients

of company rewards also bear its risks. The transfer of both risk and reward to investors protects

against “moral hazard” and ensures that those investors will exercise “market discipline” and

curb excessively risky behavior by company managers.

While the large spread between their relatively low borrowing costs and the yield from

purchased mortgages and MBS due to an implicit guarantee have allowed Fannie and Freddie to

multiply in size and consistently produce huge gains for their private investors, that same

implicit guarantee has socialized the costs of Fannie and Freddie’s financial failure. As the

federal government’s rescue of the two GSEs in the last year demonstrates, taxpayers bear the

cost of rescuing the two companies when their risks materialize. Fannie and Freddie creditors,

confident in the federal government’s implicit guarantee to back the GSEs’ obligations, felt no

need to exercise “market discipline” on the two companies to protect their investment by

pressuring GSE managers to limit very risky behavior because the investors and creditors would

not have to bear the risk of any loss. Therefore, in addition to the dilemma in serving too many

masters, the GSE structure, with its corporate form, is an inappropriate policy measure because it

creates public companies whose decisions are guided mainly by investor interests despite

significant social risks and costs.

Fannie and Freddie Provide Limited Public Benefits

According to Fannie and Freddie, they provide a range of public benefits due to their GSE status.

For instance, Fannie claims the GSEs’ public benefits include affordable housing finance for

low- and middle-income and minority homebuyers and lower mortgage rates for all homebuyers.

Even if the GSEs actually conferred such public benefits, it is important to note that they are not

the source of these benefits, but rather a vehicle for conveying a subsidy to intended

26

beneficiaries – homebuyers.57 Beyond the public benefits they deliver, the case for maintaining

their GSE status must show that they are an efficient method of conferring such benefits.

Also, the exact public benefit, or positive externality, from lower home purchase costs is mainly

based on increasing homeownership rates, not just increasing home purchases. Homeowners are

more likely than renters to care about the upkeep of the home (with positive spillovers to

neighbors), to contribute to economic growth through spending on construction and home

furnishings, to refrain from criminal activity, and to be more community-minded.58 Thus, in

estimating Fannie and Freddie’s public benefit, the important issue is their impact on first-time

buyers and not on homebuyers generally.

Moreover, despite Fannie and Freddie’s contentions, substantial quantitative data and analyses

indicate that the two companies have actually generated only limited public benefits. As analyses

show, the impact of the two GSEs on mortgage rates is not statistically significant. Also, even if

they do measurably lower mortgage rates, such reductions are shown to translate into only small

increases in homeownership rates. Further, due to the operational features of Fannie and Freddie,

they fail to narrowly and effectively target low- and moderate-income and minority home buyers

and provide relatively little help to these groups. Thus, given Fannie and Freddie’s significant

systemic risk to the economy and mortgage markets due to their GSE structure, their limited

public benefits buttresses the case for restructuring Fannie and Freddie.

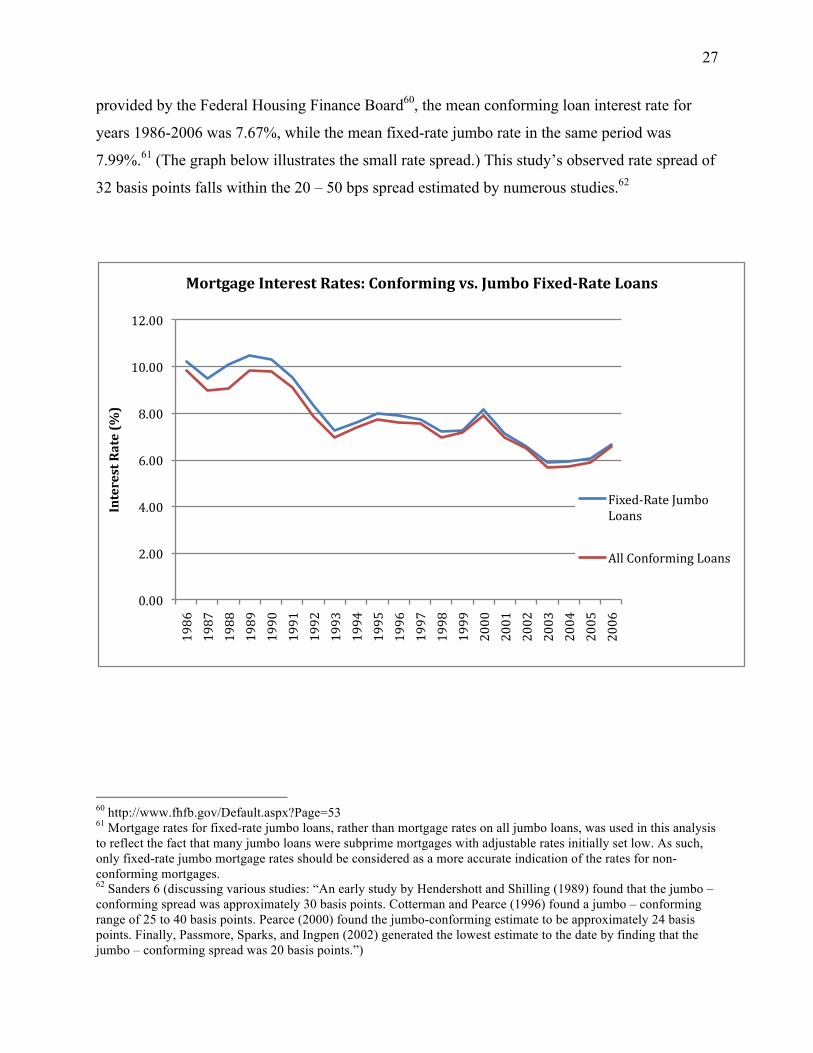

Benefit #1: Lower Mortgage Rates

Comparison of mortgage rates between conforming and jumbo mortgages (jumbo-conforming

loan spread) reveals that Fannie and Freddie have negligible effects on mortgage rates. Perhaps

the simplest measure of lowering mortgage rates by the GSEs, the jumbo-conforming loan

spread measures the mortgage rate reduction that consumers would receive by receiving a

conforming loan (a loan that qualifies for Fannie Mae and Freddie Mac mortgage programs)

versus a jumbo mortgage (a mortgage that is larger than the conforming loan limit).59 Under data

57 McKinley (1997) 21. 58 Lawrence J. White, "On Truly Privatizing Fannie Mae and Freddie Mac: Why It's Important and How to Do It,"

Fixing the Housing Finance System (Wharton School, University of Pennsylvania, 2005), 8. 59 Anthony Sanders, "The Role of the Government Sponsored Enterprises in the Mortgage Market," Before the

Committee on Banking, Housing, and Urban Affairs United States Senate, February 10, 2005, 5.

27

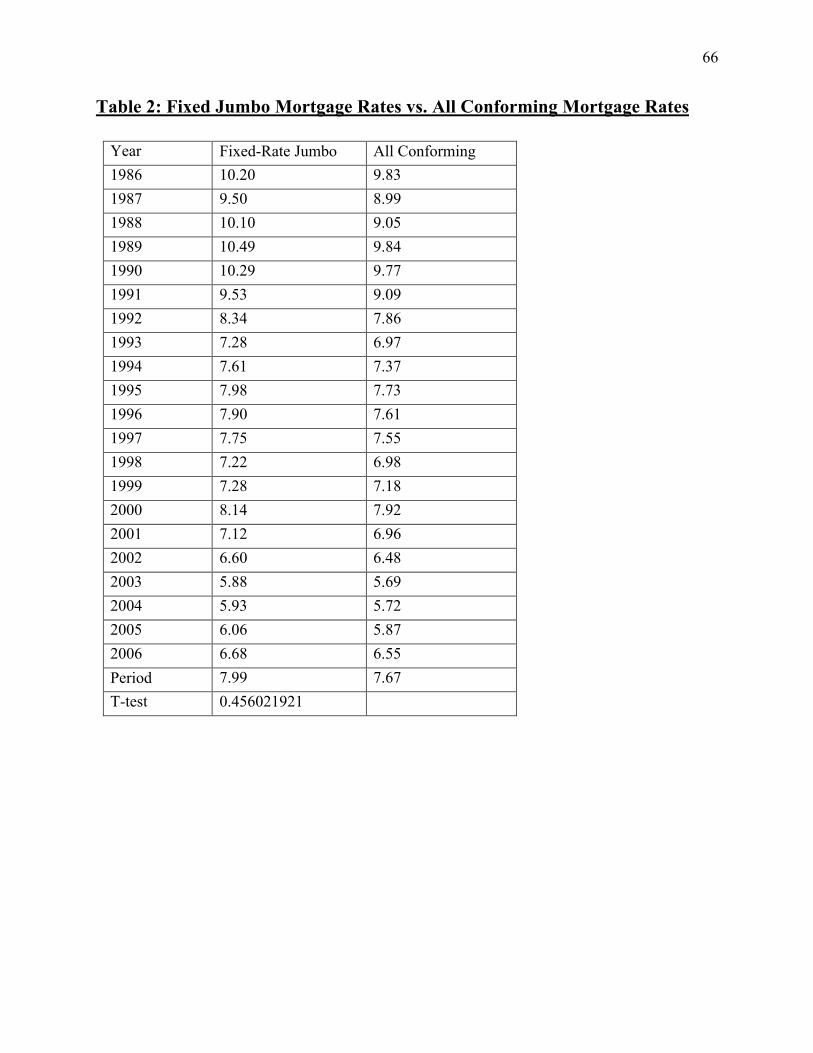

provided by the Federal Housing Finance Board60, the mean conforming loan interest rate for

years 1986-2006 was 7.67%, while the mean fixed-rate jumbo rate in the same period was

7.99%.61 (The graph below illustrates the small rate spread.) This study’s observed rate spread of

32 basis points falls within the 20 – 50 bps spread estimated by numerous studies.62

60 http://www.fhfb.gov/Default.aspx?Page=53 61 Mortgage rates for fixed-rate jumbo loans, rather than mortgage rates on all jumbo loans, was used in this analysis

to reflect the fact that many jumbo loans were subprime mortgages with adjustable rates initially set low. As such,

only fixed-rate jumbo mortgage rates should be considered as a more accurate indication of the rates for non-

conforming mortgages. 62 Sanders 6 (discussing various studies: “An early study by Hendershott and Shilling (1989) found that the jumbo –

conforming spread was approximately 30 basis points. Cotterman and Pearce (1996) found a jumbo – conforming

range of 25 to 40 basis points. Pearce (2000) found the jumbo-conforming estimate to be approximately 24 basis

points. Finally, Passmore, Sparks, and Ingpen (2002) generated the lowest estimate to the date by finding that the

jumbo – conforming spread was 20 basis points.”)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

InterestRate(%)

MortgageInterestRates:Conformingvs.JumboFixedRateLoans

Fixed‐RateJumboLoans

AllConformingLoans

28

T-Test for Statistical Significance of Fannie and Freddie’s Effect on Mortgage Rates

One method to evaluate the difference in mortgage rates between fixed jumbo and conforming

mortgages is to conduct a test for statistical significance. Significance is a statistical term that

means a difference or relationship exists given a certain level of confidence. In this analysis, a t-

test was used to determine if the higher mean rate for fixed-rate jumbo loans was statistically

higher than the mean rate for conforming loans during the period 1986-2006.63 Data used for this

t-test is in Table 2. The t-statistic from this test was 0.456. At the .001 confidence level, which is

regarded “highly significant”, the critical t-value for a sample size of 21 is 3.85. Since the value

of the t-statistic is lower than the critical t-value at the .001 confidence level, there is a 0.1%

chance that the gap between fixed-rate jumbo mortgage and conforming mortgage rates is

statistically significant. Therefore, this t-test suggests that GSEs have not had a significant effect

on mortgage rates.

Vector Autoregression Analysis of Fannie and Freddie’s Effect on Mortgage Rates

Moreover, a Federal Reserve Board study applied another statistical tool, a vector autoregression

(VAR) approach, to show that Fannie and Freddie’s secondary market activities - retained

portfolios and MBS issuances - do not significantly affect mortgage rates. VAR is used to

evaluate interrelationships between variables over time. In this case, VAR can be used to

determine whether the primary or secondary mortgage rate spread between conforming and

nonconforming loans increases over time as GSEs suddenly increase their secondary market

activities during the same period. In this 2006 Federal Reserve Board study, GSEs, Mortgage

Rates, and Secondary Market Activities, Andreas Lehnert, Wayne Passmore, and Shane

Sherlund, used a VAR approach on monthly data from March 1993 to December 2005 to reveal

that GSE portfolio purchases have no significant effects on either primary or secondary mortgage

rate spreads while MBS issuances and securitization has a small effect.64 Accordingly, the

authors of this study suggest that “curbing the growth of these portfolios might not increase

63 See Table 1 64 Wayne Passmore, Shane M. Sherlund Andreas Lehnert, GSEs, Mortgage Rates, and Secondary Market Activities,

Federal Reserve Board (Washington D.C., 2006), 3.

29

mortgage rates paid by new mortgage borrowers while mitigating the risks posed to taxpayers

and the financial system.”65

Benefit #2: Increased Homeownership

Even if Fannie and Freddie did lower mortgage rates significantly, their minimal reductions are

unlikely to cause a significant increase in homeownership by both the overall population of

homebuyers and homebuyers targeted by the GSE Act of 1992. The following analyses indicate

that it is wrong to assume that lower mortgage rates result in increased homeownership.

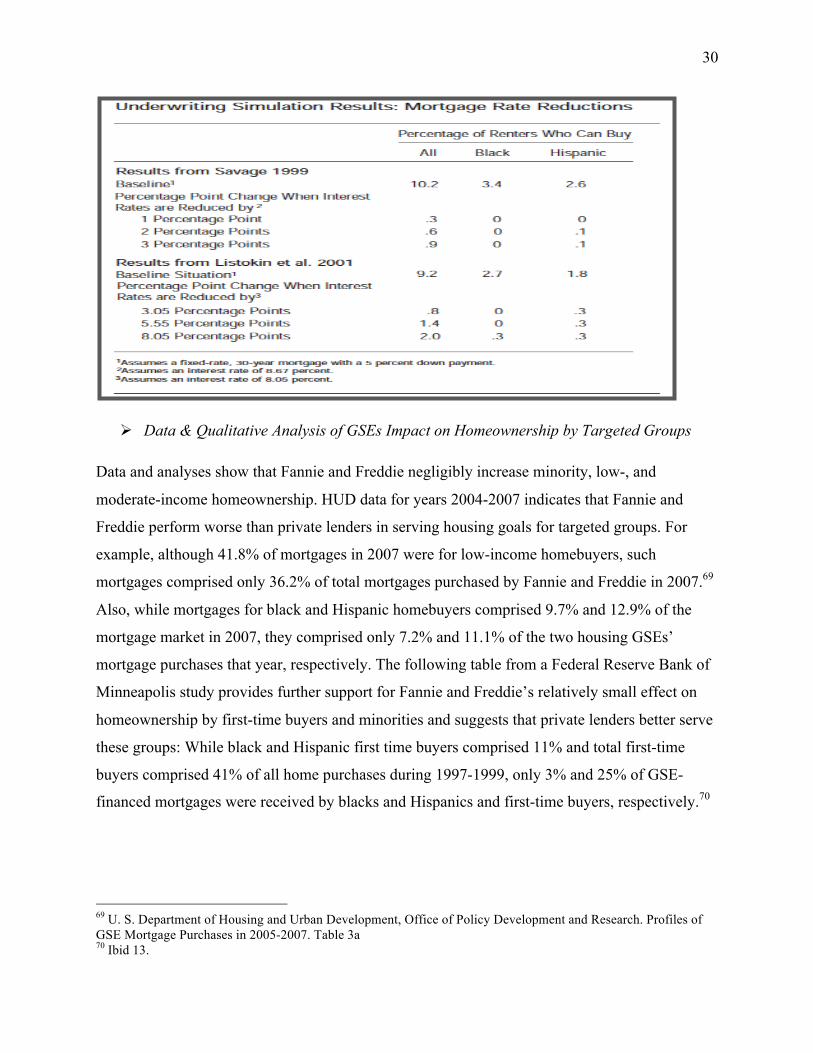

Underwriting Simulations on the Effect of Lower Mortgage Rates on Homeownership

Various underwriting simulations focused on quantifying the effect of a change in mortgage rates

on homeownership rates demonstrate the limited impact of Fannie and Freddie on

homeownership on both targeted groups and homebuyers generally.66 According to a Federal

Reserve Bank of Minneapolis study, a mortgage rate reduction of 200 bps will generally increase

the percentage of households that can buy a house by 50 bps.67 As discussed earlier, Fannie and

Freddie lower mortgage rates by 20-50 bps and, accordingly, will increase the homeownership

rate by much less than 50 bps. Most of the simulations found that the same 200 bps mortgage

rate shift would alter the percentage of black households that could buy a house by a mere 10

bps. The following table from this study shows the impact various levels of mortgage rates

reductions have on different groups’ homeownership rates according to two different studies.68

65 Ibid 6. 66 Ron Feldman, "Mortgage Rates, Homeownership Rates, and GSEs," 2001, 13. 67 Ibid 5. 68 Ibid 8.

30

Data & Qualitative Analysis of GSEs Impact on Homeownership by Targeted Groups

Data and analyses show that Fannie and Freddie negligibly increase minority, low-, and

moderate-income homeownership. HUD data for years 2004-2007 indicates that Fannie and

Freddie perform worse than private lenders in serving housing goals for targeted groups. For

example, although 41.8% of mortgages in 2007 were for low-income homebuyers, such

mortgages comprised only 36.2% of total mortgages purchased by Fannie and Freddie in 2007.69

Also, while mortgages for black and Hispanic homebuyers comprised 9.7% and 12.9% of the

mortgage market in 2007, they comprised only 7.2% and 11.1% of the two housing GSEs’

mortgage purchases that year, respectively. The following table from a Federal Reserve Bank of

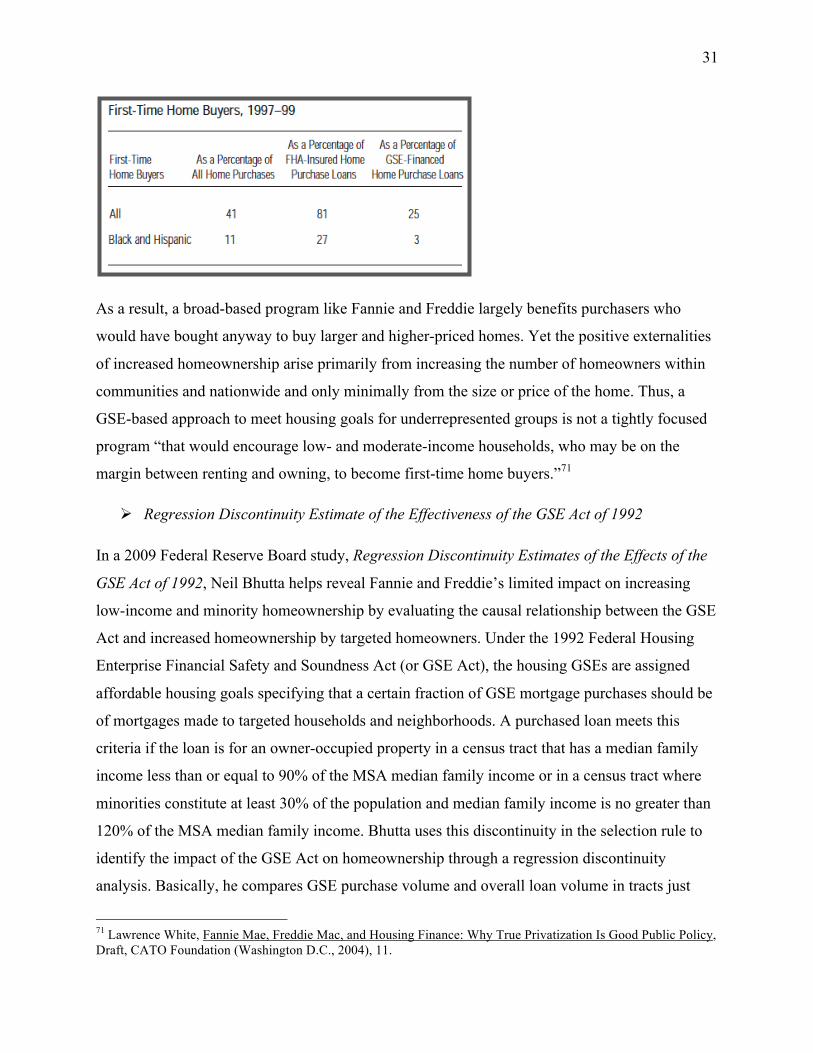

Minneapolis study provides further support for Fannie and Freddie’s relatively small effect on

homeownership by first-time buyers and minorities and suggests that private lenders better serve

these groups: While black and Hispanic first time buyers comprised 11% and total first-time

buyers comprised 41% of all home purchases during 1997-1999, only 3% and 25% of GSE-

financed mortgages were received by blacks and Hispanics and first-time buyers, respectively.70

69 U. S. Department of Housing and Urban Development, Office of Policy Development and Research. Profiles of

GSE Mortgage Purchases in 2005-2007. Table 3a 70 Ibid 13.

31

As a result, a broad-based program like Fannie and Freddie largely benefits purchasers who

would have bought anyway to buy larger and higher-priced homes. Yet the positive externalities

of increased homeownership arise primarily from increasing the number of homeowners within

communities and nationwide and only minimally from the size or price of the home. Thus, a

GSE-based approach to meet housing goals for underrepresented groups is not a tightly focused

program “that would encourage low- and moderate-income households, who may be on the

margin between renting and owning, to become first-time home buyers.”71

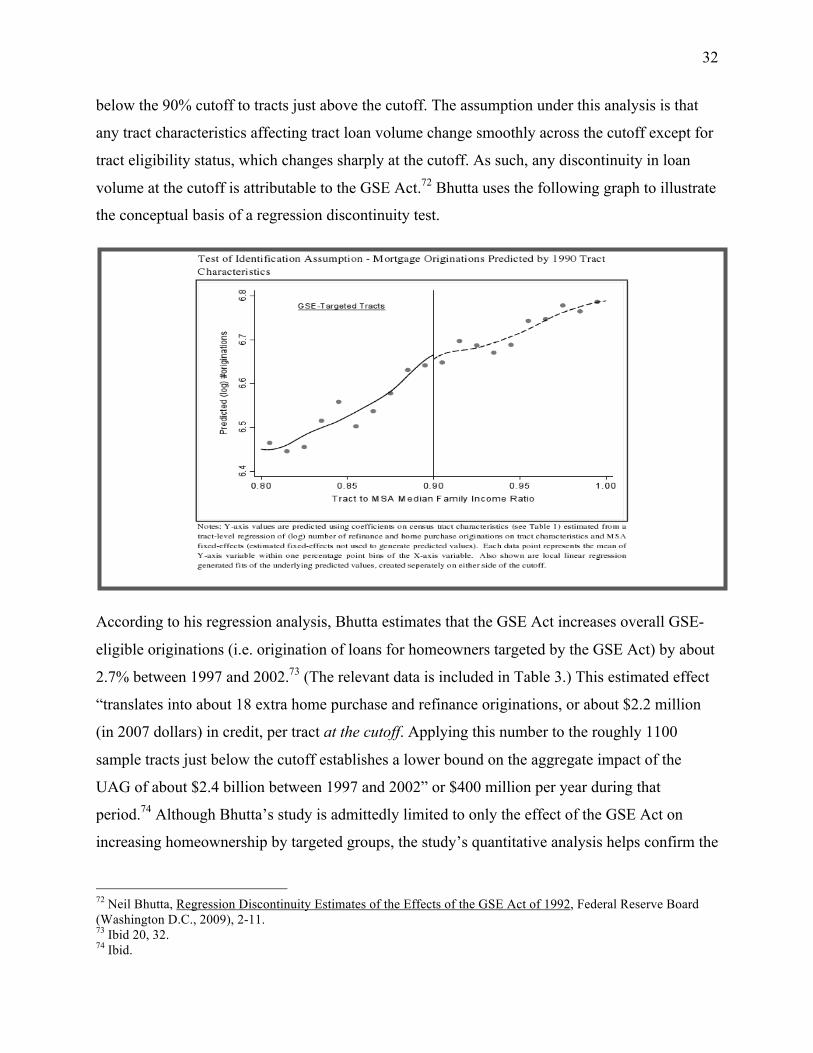

Regression Discontinuity Estimate of the Effectiveness of the GSE Act of 1992

In a 2009 Federal Reserve Board study, Regression Discontinuity Estimates of the Effects of the

GSE Act of 1992, Neil Bhutta helps reveal Fannie and Freddie’s limited impact on increasing

low-income and minority homeownership by evaluating the causal relationship between the GSE

Act and increased homeownership by targeted homeowners. Under the 1992 Federal Housing

Enterprise Financial Safety and Soundness Act (or GSE Act), the housing GSEs are assigned

affordable housing goals specifying that a certain fraction of GSE mortgage purchases should be

of mortgages made to targeted households and neighborhoods. A purchased loan meets this

criteria if the loan is for an owner-occupied property in a census tract that has a median family

income less than or equal to 90% of the MSA median family income or in a census tract where

minorities constitute at least 30% of the population and median family income is no greater than

120% of the MSA median family income. Bhutta uses this discontinuity in the selection rule to

identify the impact of the GSE Act on homeownership through a regression discontinuity

analysis. Basically, he compares GSE purchase volume and overall loan volume in tracts just

71 Lawrence White, Fannie Mae, Freddie Mac, and Housing Finance: Why True Privatization Is Good Public Policy,

Draft, CATO Foundation (Washington D.C., 2004), 11.

32

below the 90% cutoff to tracts just above the cutoff. The assumption under this analysis is that

any tract characteristics affecting tract loan volume change smoothly across the cutoff except for

tract eligibility status, which changes sharply at the cutoff. As such, any discontinuity in loan

volume at the cutoff is attributable to the GSE Act.72 Bhutta uses the following graph to illustrate

the conceptual basis of a regression discontinuity test.

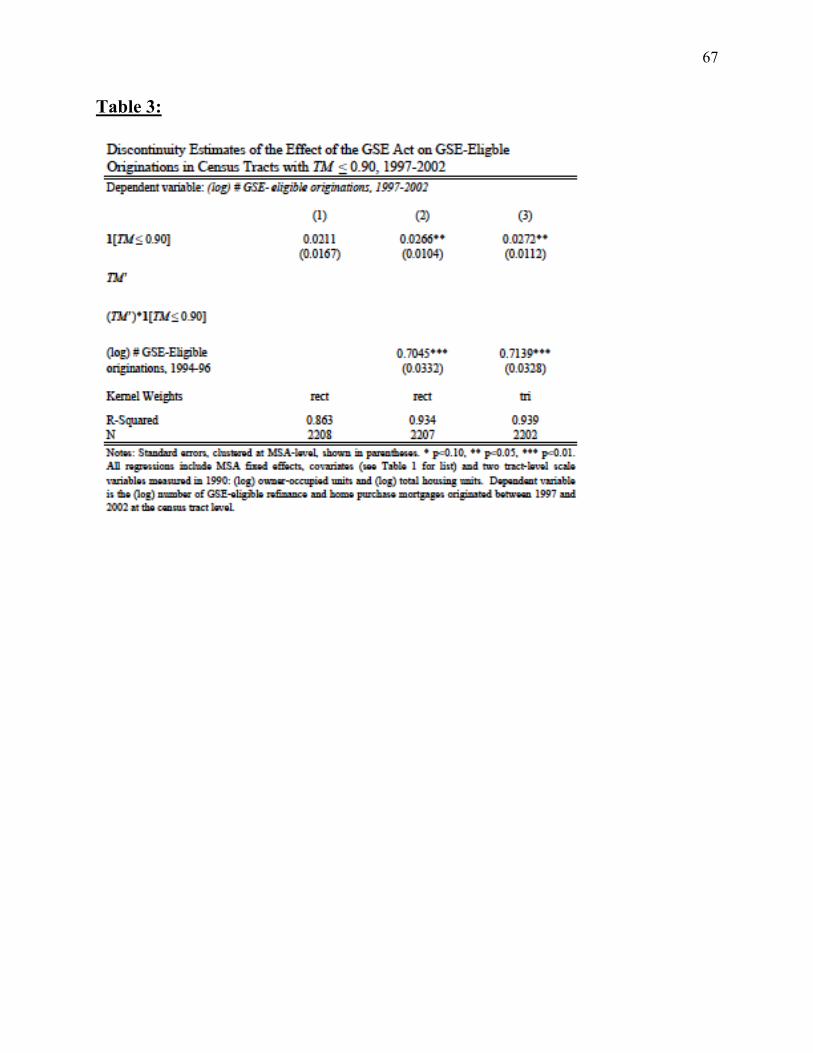

According to his regression analysis, Bhutta estimates that the GSE Act increases overall GSE-

eligible originations (i.e. origination of loans for homeowners targeted by the GSE Act) by about

2.7% between 1997 and 2002.73 (The relevant data is included in Table 3.) This estimated effect

“translates into about 18 extra home purchase and refinance originations, or about $2.2 million

(in 2007 dollars) in credit, per tract at the cutoff. Applying this number to the roughly 1100

sample tracts just below the cutoff establishes a lower bound on the aggregate impact of the

UAG of about $2.4 billion between 1997 and 2002” or $400 million per year during that

period.74 Although Bhutta’s study is admittedly limited to only the effect of the GSE Act on

increasing homeownership by targeted groups, the study’s quantitative analysis helps confirm the

72 Neil Bhutta, Regression Discontinuity Estimates of the Effects of the GSE Act of 1992, Federal Reserve Board

(Washington D.C., 2009), 2-11. 73 Ibid 20, 32. 74 Ibid.

33

qualitative case supporting the view that Fannie and Freddie have a limited impact on increasing

low-income and minority homeownership.

Limitations: Analysis of Benefits Omits Consideration of Fannie and Freddie Costs

Analysis of Fannie and Freddie’s public benefits offers only minimal insight about their

efficiency in serving policy goals because it excludes consideration of costs. Indeed, it is

plausible that Fannie and Freddie yield limited benefits but are still a desirable policy measure

because they are necessary to meet an important public need and even their minimal benefits

outweigh their costs. Thus, a finding that the GSEs’ public benefits are limited does not, in itself,

offer a persuasive reason to restructure them; at most, it buttresses the case for reform.

Although a benefit-cost analysis would be a better measure of Fannie and Freddie’s efficiency

than an assessment of their benefits, numerous uncertainties about the GSEs’ expected costs

would undermine the accuracy of such an analysis here. Benefit-cost analysis assesses the

productive efficiency of a program by comparing its net benefits to its net costs. If net benefits

exceed net costs, the program or policy is deemed efficient. If net costs exceed benefits,

however, the program or policy is inefficient and should be rejected.

Fannie and Freddie impose two types of social costs. First, the lower interest rates the two

housing GSEs enjoy due to an implicit federal guarantee effectively subsidizes Fannie and

Freddie. While some of this subsidy passes onto borrowers via lower mortgage rates, much of it

passes to Fannie and Freddie’s investors. As such, the share of this federal subsidy retained by

Fannie and Freddie’s shareholders is a cost to taxpayers. Second, taxpayers also bear the cost of

bailing out the two companies in case their existence is threatened due to financial troubles.

While numerous studies provide a range of cost estimates for the share of the federal subsidy that

passes to investors75, it is much more difficult to accurately estimate the cost of a taxpayer

75 Congressional Budget Office, Assessing the Public Costs and Benefits of Fannie Mae and Freddie Mac, CBO

Study (Washington D.C., May 1996); Congressional Budget Office, "Updated Estimates of the Subsidies to the

Housing GSEs," (2004); Dan L. Crippen, Federal Subsidies for the Housing GSEs, Congressional Budget Office (Washington D.C., May 23, 2001); Douglas Holtz-Eakin, "Aligning the Costs and Benefits of the Housing

Government-Sponsored Enterprises," CBO Testimony (Washington D.C.: Committee on Banking, Housing, and

Urban Affairs, April 21, 2005). James E. Pearce James C. Miller III, "Revisiting the Net Benefits of Freddie Mac

and Fannie Mae," November 2006. Wayne Passmore, The GSE Implicit Subsidy and the Value of Government

Ambiguity, Federal Reserve Board (Washington D.C., 2005).

34

bailout of the two companies. Although the federal government has agreed to extend up to $400

billion to help Fannie and Freddie meet their obligations, the actual financial implications of

federal backing to taxpayers could be a figure much larger than $400 billion or possibly even a

profit from the MBS the Treasury purchases.76 Taxpayers also bear the costs of the GSEs’

systemic risk materializing, such as illiquidity in credit markets, difficulty in obtaining loans, and

economic recession. Accurate valuation of these costs is unlikely in light of the uncertainties

regarding the future of Fannie and Freddie, recovery in the housing markets and economy, and

bank lending. Since the cost to taxpayers may well comprise a substantial portion of Fannie and

Freddie’s net costs and this cost is too difficult to estimate now, benefit-cost analysis of the two

GSEs would require too many assumptions and yield inaccurate results.

GSE Structure of Fannie & Fannie Unnecessary for Public Missions

Fannie and Freddie No Longer Needed for Secondary Mortgage Market

Fannie and Freddie were initially formed to expand homeownership and make it more affordable

almost 40 years ago through creation of a secondary mortgage market in which they could

securitize home loans and free capital available for new mortgage originations. In the 1970s and

1980s, Fannie and Freddie – and their implied guarantees – may have been needed for the

innovation and development of mortgage securitization and MBS as an efficient alternative for

residential mortgage finance.77 In the current financial markets characterized by continuous

innovation of financial products, however, Fannie and Freddie are no longer necessary to serve

the secondary market and securitize mortgages. This is clearly evidenced by the emergence of a

large secondary market in auto loans despite the lack of government intervention. Indeed, in his

discussion about the costs of retaining GSEs that have met their policy purpose, Thomas Stanton

worries that “GSEs can distort the marketplace and displace activities of the firms – here

competing lenders and guaranty agencies – that they originally were created to support.”78 Thus,

other lenders and banks should be able to expand their role in the secondary market.

76 "Suffering a Seizure: America's Government Takes Control of Freddie Mac and Fannie Mae," The Economist 8 September 2008. 77 Lawrence White, Fannie Mae, Freddie Mac, and Housing Finance: Why True Privatization Is Good Public Policy,

Draft, CATO Foundation (Washington D.C., 2004), 8, 27. 78 Thomas H. Stanton, The Privatization of Sallie Mae and Its Consequences (Washington D.C.: American

Enterprise Institute, May 9, 2007), 1, 17.

35

The inability of the private market to develop a secondary mortgage market in the middle of the

20th century no longer explains its absence from this market. Rather, its absence is a product of

the inability of commercial banks and lenders to obtain the relatively low borrowing costs

offered to Fannie and Freddie. Former President and CEO of another GSE, the Federal Home

Loan Bank of Chicago, Alex Pollock, summarized this observation: “It is true that private

securitization of prime, conforming loans has not previously existed, but this is only because no

private firms could compete with the government-granted advantages and economic subsidies

enjoyed by Fannie and Freddie. Once past the panic and the bust, and without GSEs, there would

be a private market for securitization of high quality loans. The financial technology is not very

hard and well known.”79 Therefore, if Congress required Fannie and Freddie to freeze their

mortgage purchase activities and also loosened the capital requirements for banks to hold low-

risk mortgages, the result would likely be an expanded role of banks and other financial

institutions in the mortgage market.80

Data on Fannie and Freddie’s role in the U.S. secondary mortgage market compared to the role

of private firms confirms that the GSEs secondary market function has become less important

over time.81 In the U.S. there are roughly 50,000 census tracts, a figure that remains fairly