Growth to Continue - Bursa Malaysia · Crude Oil Production –From 2% Depletion to 3% Growth Rate...

32

Growth to Continue June 2014 Perisai Petroleum Teknologi Bhd

Transcript of Growth to Continue - Bursa Malaysia · Crude Oil Production –From 2% Depletion to 3% Growth Rate...

Growth to

Continue

June 2014

Perisai Petroleum Teknologi Bhd

2

TABLE OF CONTENTS

� Perisai Today

� Strategizing Growth

� Market Outlook

� Business Segments

� Shareholdings & Key Management

� Financial Performance

� In Summary

Perisai Today

4

A STRONGER PERISAI

� Listed on Main Market

of Bursa Malaysia,

Malaysian Stock

Exchange

� Owner/Operator

of Offshore Marine

Assets

� Market Capitalisation of

RM1.9b /

USD592m as at

2.6.2014

OSVsOffshore

ConstructionProduction

Derrick Lay

Barge

3 AHTS /

2 AHT (1) /

3 Crew

Boats

MOPUFPSO

Drilling

3 Units of Pacific

Class 400 Jack-

Up Rigs

51% Jointly-

Controlled

Entity (2)

51%

51% Jointly-

Controlled

Entity

100% 100%

(1) Currently acquiring additional AHT, Lewek Robin from Ezra Group.

(2) Call and put option for the disposal of remaining 51% interest within the next 3 years.

Strategizing

Growth

6

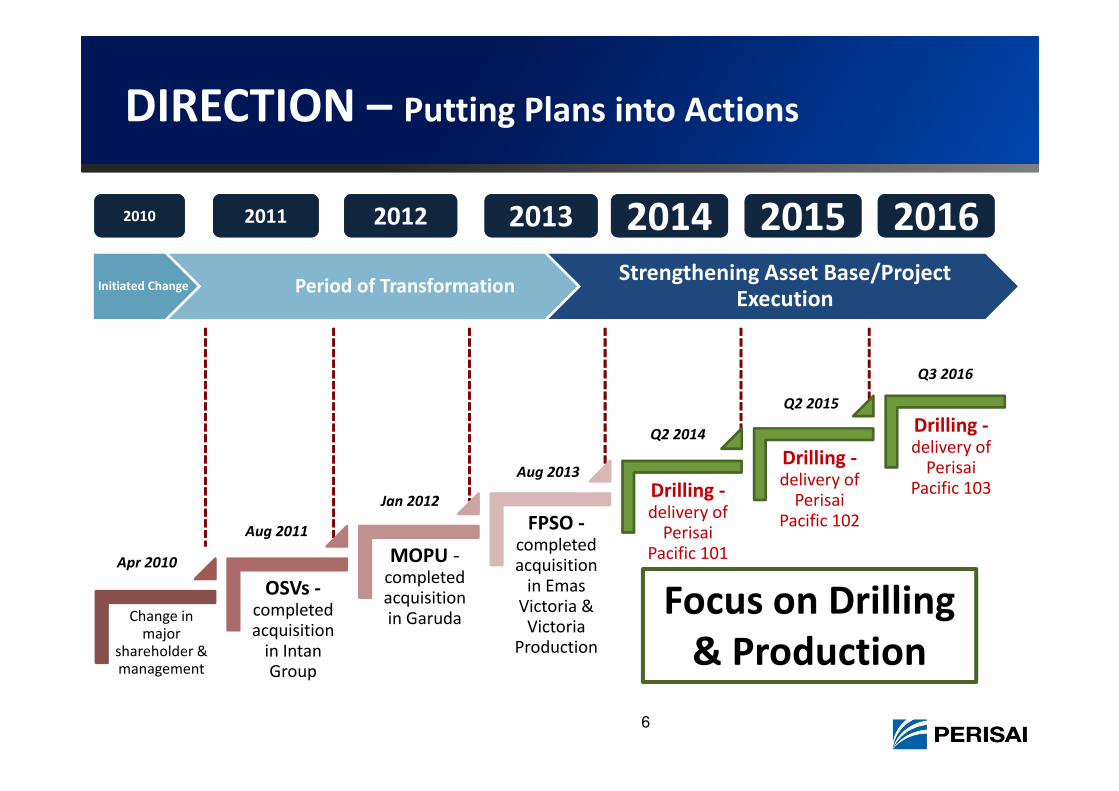

DIRECTION – Putting Plans into Actions

20122012 201320132011201120102010 20142014

Change in major

shareholder & management

OSVs -completed acquisition

in IntanGroup

MOPU -completed acquisition in Garuda

FPSO -completed acquisition

in EmasVictoria &

Victoria Production

Drilling -delivery of

PerisaiPacific 101

Drilling -delivery of

PerisaiPacific 102

Drilling -delivery of

PerisaiPacific 103

20152015 20162016

Initiated Change Period of TransformationStrengthening Asset Base/Project

Execution

Apr 2010

Aug 2011

Jan 2012

Aug 2013

Q2 2014

Q2 2015

Q3 2016

Focus on Drilling

& Production

7

FOCUS - From Bareboat to Operations

ProductionDrilling

Import Substitution

� Limited local

players.

� High barriers to

entry – financial &

technical.

Diverse Risk Profile

� Long term vs short

term contract.

� Build with/without

contract.

� Customized vs

commodity.

OSVsOffshore

Construction

� Exiting within

next 3 years

� Long term

contract

� Stable cash flow

and earnings

Production – FPSO

Commenced Operations

since Nov 2013

� Asset Expansion

� Operational

Efficiency

8

STRATEGIES – Key Drivers

Production

Drilling

Ezra Group

New Focus

� Leverage on Ezra Group

Leverage

� Moving up

value chain

� Sustainable

earnings

growth

• Diverse fleet + AMC engineering expertise

• Global presence

• Strategic alliances with Aker Solutions

Global Offshore Service Provider

• Offshore Support – AHTS / AHT / MPSV / fast crew utility vessels

• Engineering & Fabrication – offshore & marine support design,

engineering, training, repair, fabrication and marine supply services

• Construction & Production – heavylift crane barges / heavylift pipelay

vessels / FPSO

• Deepwater Subsea – SURF installation / inspection & maintenance / well

intervention & drilling / decommissioning services

Broad Capabilities

9

LEVERAGING ON EZRA GROUP

World class

EPIC / SURF

subsea player

Market Outlook

OUTLOOK - GENERAL

Current Landscape

Outlook

� Global E&P Capex to increase by 7% in 2014

11

� Oil prices remain high, currently hovering above USD100/barrel (Brent & Nymex)

Crude Oil Production – From 2% Depletion to 3% Growth Rate

12

OUTLOOK - SEA/MALAYSIA

� Petronas spending – (2011 – Q3 2013) estimated

only RM125b (42%) of total 5-year capex budget of

RM300b spent

� ASEAN – Malaysia & Indonesia expected to

spearhead capex spending

� Petronas likely to accelerate spending in 2014

� Focus remains on 3 key strategies, i.e. EOR, marginal

fields & exploration activities

Petronas’ Capex Spending

Outlook

Current Landscape - Malaysia

Remaining

balance of

RM175b within

next 2 years

O&G activities

expected to remain

robust in 2014

Business

Segments

Technologically advanced, high

specification (capable to drill high

pressure high temperature

wells) latest generation rig

DRILLING – Jack-Up Rigs

14

Perisai Pacific 101

� Contract signed in Apr 2012

� Construction Costs (turnkey

fixed lump sum) – USD208m

Perisai Pacific 102

� Contract signed in Feb 2013

� Construction Costs (turnkey

fixed lump sum) –

USD208m

Perisai Pacific 103

� Contract signed in Dec 2013

� Construction Costs (turnkey

fixed lump sum) –

USD211.5m

Mid 2014Mid 2014

Q2 2015Q2 2015

Q3 2016Q3 2016

New Focus - Entry into the offshore drilling segment

(Malaysia & AP region)

• Secured contract from Petronas

Carigali at USD158m in May 2014

• Tenure: 3 years firm

The Contract

� Water depth (operating) 400ft / 122m

� Leg length 532ft / 162m

� Drilling depth 30,000 ft

� Accommodation 150 pax

� Mud pump 2,200 hp 3 units

� Generator set 5 units

� Blow Out Prevention 15,000 psi

� Hook Load 1.5m lbs

PPL PACIFIC CLASS 400

The Assets (100%-Owned)

� Payment Term: 20% upfront and 80% upon delivery

� Builder: PPL Shipyard, Singapore (subsidiary of Sembcorp Marine)

� Signed Management Agreement with Hercules Offshore, Inc.

DRILLING – Established Partners

15

� A subsidiary of Sembcorp Marine and based in Singapore, an

integrated rig design and rig building yard with a proven track

record in the building and servicing of jack-up and semi-

submersible rigs

� To-date, built 56 jack-ups, 6 semi-submersibles and 4 swamp

barges. Delivered 27 flagship Pacific Class 375 jack-up rigs

� In 2010, launched the enhanced PPL Pacific Class 400 series.

Total 17 rigs ordered and 8 have been delivered to date

� One of the leading global provider of offshore contract drilling and liftboat services,

with operations in nine (9) countries on three (3) continents.

� Headquartered in Houston, Texas, listed on the NASDAQ in 2005 and is an ISO

9001:2008 certified company.

� Currently owns and operates the largest shallow water jack-up drilling rig fleet in the

US Gulf of Mexico and the 3rd largest jack-up fleet worldwide, comprising 40 jack-up

drilling rigs.

� A global leader in shallow water services with a diverse and unique fleet capable of

providing services such as oil and gas exploration and development drilling, well

service, platform inspection, maintenance and decommissioning operations in shallow

water markets.

Rig Builder

O&M Partner

16

Global/Regional - Demand expected to remain bullish

� Ageing fleet

� Approx. 55% of total rigs > 30 years old

� Newbuild will be absorbed

� Dayrates to strengthen further

� Drilling activities in SEA region to be dominated by jack-up rigs.

� Malaysia, Indonesia, Vietnam and Myanmar – key growth

markets

Age Profiles by 2016

Malaysia – Expected high level of activities going forward

� Currently 15 rigs operating in Malaysia.

� Average 159 wells expected to be drilled annually (2013 – 2018)

DRILLING - Outlook

17

PRODUCTION – FPSO

New Focus – The Other Half of the Equation

� Secured contract from Hess – 3 years firm (+ 1 + 1 + 1 years) at USD90 million p.a.

� Aug 2013 - Acquired 51% interests in the FPSO Companies - USD89.25m, funded by:

� Aug 2013 – issuance of 144,661,250 new Perisai shares @ RM1.10/share (USD52.25m)

� Dec 2013 – disposal of 49% interest in SJR (owner of E3) (USD37m) *

The Investment (51%-owned)

(*) There are call and put options to

dispose of the remaining 51% equity

at the same price as the 1st 49%

disposal

PRODUCTION – FPSO (cont’d)

• Area of Operations : Kamelia Field (North Malay Basin)

• Client: Hess Exploration and Production Malaysia B.V.

• Contract Tenure: 3 years firm time charter + 3 x 1-year extension

options (commenced in Nov 2013)

• Contract Value: USD272m for 3-years firm

The Contract

PERISAI KAMELIA

� Dedicated gas FPSO

� Proven track record since 2008

� New turret mooring system

� Built (as Aframax tanker) 1980

� Converted in 2008 (Keppel Singapore)

� Flag Panama

� Class DNV

� Capacity 175mmscfd / 8,000 BPD of gas

condensate

540,000 bbls storage

18

19

PRODUCTION - MOPU

� Jan 2012 - Acquired 100% interests in Garuda Energy

� Purchase price : USD70m (USD50m cash and USD20m new Perisai shares @

RM0.65 / share) + assuming Garuda Energy’s borrowing of USD40m

� Valuation (MOPU) by DNV GL (formerly GL Noble Denton): USD105m – USD110m

� Bareboat charter commenced on 30 Sept 2011 and completed in end Sept 2013

The Investment (100%-owned)

RUBICONE

� Class BV

� Converted in 2011

� Length 58m

� Breadth 40m

� Hydraulic Crane 22T

� 3 Legs 96m

� Daily Production Capacity 165MMscfd Gas

5,262 BPD of Oil

2,044 BPD of Water

20

Global/Regional

� Over 50 FPSOs to be awarded from 2014 – 2017.

Majority in Asia, Africa and Brazil

� 10-12 contracts expected to be awarded annually

(2014 – 2017)

� Asia – 3rd highest capex spending for floating

production systems (2013 – 2017)

Malaysia

� Opportunities for production

systems - RSC fields

Geographical Distribution of Potential Awards

Floating Production

Systems CAPEX

breakdown (by region)

2013 – 2017 estimates

PRODUCTION - Outlook

21

OFFSHORE CONSTRUCTION – DLB

� Worked offshore of Sarawak &

Terengganu, Malaysia

� Laid > 200km of offshore

pipelines since 2008

� Installed multiple risers and

mattress

Track Record

ENTERPRISE 3

Derrick Pipelay Barge (Shallow Water)

� Flag: Malaysian

� Classification: ABS Class A1 Barge

� Year Built: 2008

� Length: 120.0m

� Accommodation: 300 men

Pipelay

� Pipe Size: 6” to 36”

� Tension Capacity: 136 Ton (2 x 68 Ton each)

Main / Derrick Crane (Mast Crane)

� Main Hook Capacity - Fixed Mode: 800MT

Mooring System

� Mooring Winch: 8 nos

� Call & put option for the disposal of

remaining 51% within next 3 years

The Investment (51%-owned)

22

OFFSHORE SUPPORT VESSELS

� Aug 2011 – Acquired 51% interests in Intan Offshore Group

� Purchase price: RM45.2m (issuance of 70,683,000 new Perisai shares @ RM0.64 / share)

� Average age of 9 years

� All 8 vessels with firm bareboat charters with Ezra Group

� Current borrowings of approx. RM127m

� Labuan structure completed end 2012 – tax savings from 2012 onwards

The Investment (51%-owned)

RM’000 Audited

31.8.11

Audited

31.12.12

(16 months)

Audited

31.12.13

(100% of Intan Offshore Group)

Revenue 40,802 54,357 42,129

PBT15,871 26,298 22,227

PAT11,819 49,800 22,206

Note 1: Higher PAT due to 16 months results and reversal of deferred tax

arising from Labuan structure.

Mar 2014 – Announced the proposed

acquisition of the AHT, Lewek Robin for

USD7m

Note 1

23

OFFSHORE SUPPORT VESSELS (cont’d)

Lewek Mallard

(7,340 bhp)

AHTS AHTCrew Boat

Lewek Emerald

(11,000 bhp)

Lewek Swift

(12,240 bhp)

Sarah Gold

(50 pax)

Sarah Jade

(80 pax)

Sarah Pearl

(50 pax)

Bayu Intan

(4,200 bhp)

Lewek Eagle

(4,200 bhp)

All are contracted

3 years (firm till Aug

2015) + 2 x 1-year

extension options

Will be contracted

post completion of

acquisition – 7

yearsLewek Robin

(4,750 bhp)

Shareholdings &

Key Management

25

MAJOR SHAREHOLDING

Major Shareholders Current

Ezra Group (HCM / Emas / EOC) 23.58%

EPF 7.38%

Mercury Pacific 7.31%

Izzet Ishak 5.53%

1,193,124,978

26

MANAGEMENT PROFILE

Chairman – Dato’ Dr. Mohamed Ariffin Bin Hj. Aton

� Appointed as an Independent Non-Executive Director on 1 June 2004

� Re-designated as Non-Independent Non-Executive Director in May 2013

� Holds a Doctorate in Chemical Engineering from the University of Leeds. A Fellow

of the Institute of Engineers Malaysia, Chartered Member of Institute of Chemistry

Malaysia and Fellow of the Malaysian Scientific Association

� Presently, sits on the Boards of Kumpulan Perangsang Selangor Berhad and

HeiTech Padu Berhad

� Previously, Dean (Founder) of the Engineering Faculty and professor at Universiti

Kebangsaan Malaysia, MD/CEO of Petronas Research & Scientific Services and

President and CEO of SIRIM

Managing Director – Zainol Izzet Bin Mohamed Ishak

� Appointed as MD on 21 April 2010

� More than 15 years of experience in oil & gas industry

� Previously CEO of SapuraCrest

� Prior to SapuraCrest, SVP of Sapura Group, CEO of Sapura Digital (ADAM), GM of

Corporate Planning - Sapura Group, GM of Seccolor (M) Industries, Management

Consultant of Kassim Chan and Consultant of Hymans Robertson, Consulting

Actuaries, London

27

MANAGEMENT PROFILE (cont’d)

Executive Director – Adarash Kumar A/L Chranji Lal Amarnath

Chief Financial Officer – Yeo Peck Chin

� Appointed as ED on 21 April 2010

� Presently Group COO of Ezra Holdings

� More than 30 years of experience in the marine industry

� Prior to Ezra Holdings, Assistant GM of Bumi Armada and held

various positions onboard vessels while working for the Malaysian

International Shipping Corporation

� Joined in 2004 as Group Financial Controller and subsequently appointed

as CFO in 2008

� Fellow member of ACCA and member of MIA

� Prior to Perisai, AGM (Finance) of Corroless (M), FM of Hong Leong

Properties and also attached to an audit firm Azman, Wong, Salleh

Financial

Performance

29

NUMBERS – INCOME STATEMENT

� Lower revenue & profit in Q1 2014 vs Q1 2013 due to expiry of Garuda’s

(MOPU) and SJR Marine's (E3) contracts in Sept 2013

RM’000 Q1 2014

Unaudited

Q1 2013

Unaudited

31.12.13

Audited

31.12.12

Audited

31.12.11

Audited

Revenue 10,870 31,699 111,663 128,370 22,041

PBT 53 25,655 82,548 93,254 35,268

(LAT)/PAT (2,989) 23,682 71,785 92,175 28,496

30

NUMBERS – FINANCIAL POSITION

RM’000 Q1 2014

Unaudited

31.12.13

Audited

31.12.12

Audited

31.12.11

Audited

ASSETS

PPE 547,025 548,291 549,103 519,651

Investments 497,819 490,014 315 139,028

Prepayment - Non-Current 211,171 142,238 - -

Asset Held for Sale (E3) - - 381,233 -

Trade Receivables 24,138 20,386 41,118 26,588

Other Receivables 218,249 188,727 132,538 65,886

Cash 22,010 62,917 24,940 40,880

LIABILITIES

Borrowings - Non-Current 257,427 272,023 264,709 138,807

Borrowings - Current 151,687 82,012 77,905 125,735

Trade Payables 357 543 2,510 3,129

Other Payables 107,003 93,189 70,629 137,067

Derivative Liability 1,235 1,443 - -

Liabilities Held for Sale

(E3) - - 148,840 -

EQUITY 899,459 902,957 482,424 329,205

No. of Shares ('000) 1,084,700 1,084,599 851,775 753,883

Gross Gearing 0.5 0.4 0.7 0.8

� 2013 - 51% interests in the FPSO companies and SJR Marine (as at

2012, SJR Marine was classified as Asset & Liabilities held for Sale.

Subsequently reclassified to Investments in JCE following disposal

of 49% interest in SJR Marine)

Investments

� 2013 - mainly comprises downpayment paid & payable for Perisai

Pacific 102 & 103 rigs

� Q1 2014 – includes downpayment paid for Perisai Pacific 103 rig

Prepayment

� Q1 2014 & 2013 - includes pre-operating expenses for Perisai Pacific

101 rig, in addition to the downpayments paid

� Q1 2014 - Other Payables includes provision for balance 10% deposit

for Perisai Pacific 103 (RM63m),

Other Receivables & Payables

� Q1 2014 – (Borrowings – Current) includes new borrowings to

fund rigs investment

Borrowings

� 2013 - relates to the cross currency swap transaction entered into

to swap SGD MTN proceeds to USD

Derivative Liability

� Q1 2014 - cash utilised mainly for rigs investment

Cash

People

� Strong Management Team

Leverage� Ezra Group

� Petronas Licensed

� Vast O&G experiences

� Ability to secure new contracts +

new acquisitions

IN SUMMARY – From Bareboat to Operations

31

Assets

� Technically Niche

� Contract-Backed

� Jack-Up Rigs (3 units)

� FPSO & MOPU

� DLB

� AHTS / AHT / Crew Boats

(8 vessels)

� 1st Jack-Up Rig: 3 years (firm)

(from mid 2014)

� OSVs: 3 (firm) + 1 + 1 year

(from Aug 2012)

� FPSO: 3 (firm) + 1 + 1 + 1 year

(from Nov 2013)

� Access to more/specialised

vessels & regional markets

� Provision of vessels, FPSOs,

drilling rigs, pipelay barge and T&I

of offshore facilities

2 Core Segments:

� Drilling

� Production

Poised for

Substantial

Growth

Clear

Focus &

Direction

THANK YOU