Growth ambitions in the CEE region Foto gebouw. 2 Reminder: KBC’s presence in CEE Update on...

24

Growth ambitions in the CEE region Foto gebouw

-

date post

21-Dec-2015 -

Category

Documents

-

view

218 -

download

5

Transcript of Growth ambitions in the CEE region Foto gebouw. 2 Reminder: KBC’s presence in CEE Update on...

Growth ambitions in the CEE region

Foto gebouw

2

Reminder: KBC’s presence in CEE

Update on economic and financial background

KBC’s opportunities

Update on Poland

Financial outlook

Agenda

3

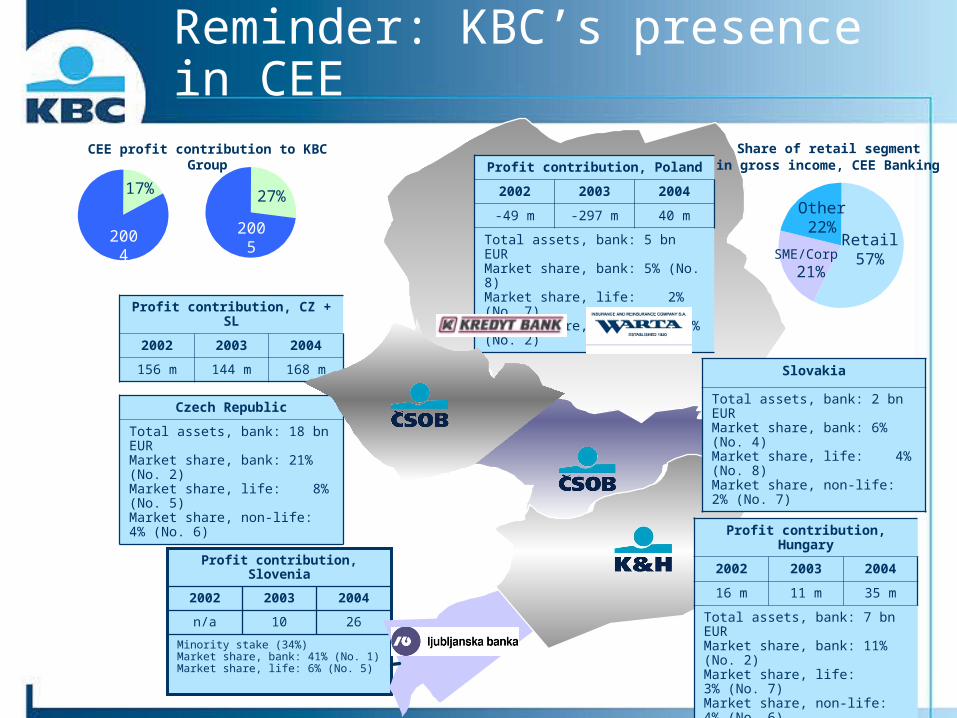

Profit contribution, Slovenia

Minority stake (34%) Market share, bank: 41% (No. 1)Market share, life: 6% (No. 5)

2610n/a

200420032002

Reminder: KBC’s presence in CEE

Profit contribution, CZ + SL

2002 2003 2004

156 m 144 m 168 m

Profit contribution, Poland

2002 2003 2004

-49 m -297 m 40 m

Total assets, bank: 5 bn EURMarket share, bank: 5% (No. 8)Market share, life: 2% (No. 7)Market share, non-life: 12% (No. 2)

Profit contribution, Hungary

2002 2003 2004

16 m 11 m 35 m

Total assets, bank: 7 bn EURMarket share, bank: 11% (No. 2)Market share, life: 3% (No. 7)Market share, non-life: 4% (No. 6)

Czech Republic

Total assets, bank: 18 bn EURMarket share, bank: 21% (No. 2)Market share, life: 8% (No. 5)Market share, non-life: 4% (No. 6)

Slovakia

Total assets, bank: 2 bn EURMarket share, bank: 6% (No. 4)Market share, life: 4% (No. 8)Market share, non-life: 2% (No. 7)

CEE profit contribution to KBC Group

2004 2005 Q1

17% 27%

Retail 57%

Other22%

SME/Corp

21%

Share of retail segment in gross income, CEE Banking

4

Reminder: KBC’s presence in CEE

Update on economic and financial background

KBC’s opportunities

Update on Poland

Financial outlook

Agenda

5

Growth fundamentals maintained

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5

Germany

SwitzerlandItaly

Denmark

UKSweden

EMU

BelgiumFrance

The Netherlands

Portugal

US

Spain Finland

Ireland (9,4;5,0)

High flyers

Average real GDP growth, 1997-2001 (in %)

Ave

rag

e re

al G

DP

gr o

wt h

, 200

2-20

04 (

in %

)

Czech Rep.

Slovakia

Slovenia

Poland

HungaryEU-13

(not-EMU)

Turkey (1,2; 7,5)

(Source: IMF) 0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Belgium

EU-15

US

Poland

Hungary

Czech Republic

Slovakia

Slovenia

Financial services (banking & insurance) in % of GDP (2004)

2005/2006 growth prospects have recently been reviewed downwards due to global economic slowdown

But growth in CEE will still be at higher rate (+/-2%) than euro zone

0%

1%

2%

3%

4%

5%

6%

2004 2005 2006

CEE-5 (forecast 4Q04) CEE-5 (forecast 2Q05)

EMU (forecast 4Q04) EMU (forecast 2Q05)

…but positive gap maintained

GDP growth prospects adjusted… (Source: IMF)

(Source: Vienna Institute for International Economic Studies)

6

EU entry - catalyst for developmentResults of one-year EU membership

Adoption of EU-compatible regulation and legislation EU-10 economic growth double of EU-25 (5% vs. 2%) Exports to EU-15 rose spectacularly (market share from

2% in 1997 up to probably 4% in 2005) FDIs in EU-10 continue (2004: 11 bn EUR or 3% of CEE-

10’s GDP) Agricultural subsidies / EU funds Stimulation of macroeconomic stability Strong financial integration with EU Declining inflation (11.7% in 1998 down to 4.3% in 2004) No budgetary deterioration Decrease in unemployment, though rather slow

EBRD transition index (EMU = 100)50 60 70 80 90

Hungary

Cech Rep

Slovakia

Poland

Slovenia

Baltics

Bulgaria

Romania

Russia

Ukraine

1999

2004

EU accession acts as catalyst

(Source: OECD)

Limited impact on KBC of French and Dutch ‘NO’ to the treaty establishing a constitution for Europe

KBC is currently operating within EU countries only

Entry into euro is guaranteed by EU membership once economic criteria are met

7

UCI-HVB merger may transform landscape somewhat

In the Polish market, the UniCredit-HVB combination will strengthen their already strong individual positions; the impact will be somewhat less in Slovakia and very limited in the other markets where KBC is active.

The UniCredit-HVB merger should be seen as much an opportunity as a threat: In Poland, the merger efforts may temporarily weaken the commercial

clout of the parties involved, enabling other parties to increase market share

Potential for gaining new customers preferring to be ‘multi-banked’ rather than ‘uni-banked’

The merger could trigger the much-needed start of early consolidation in Poland

In the short run, UniCredit-HVB may partly divest from some markets, creating investment opportunities for other players.

8

Reminder: KBC’s presence in CEE

Update on economic and financial background

KBC’s opportunities

Update on Poland

Financial outlook

Agenda

9

KBC’s opportunities in CEE

Unique bancassurance concept, enabling cross-selling

Outstanding track record in the promising AM market

Well positioned in the emerging markets of HNWI and private banking through the epb know-how

Nationwide branch network in all countries

Introduction of uniform corporate image

Setting up of technology for centralization of processing

Increasing hands-on management approach

10

Bancassurance to fuel earnings

Major challenges to exporting the model to CEE:

Re-organization of insurance network & implementation of new branch organization models

Enhancement of pro-active sales approach in both bank branches and agents’ networks

Streamlining of business processes and IT systems in both bank and insurance company

Achievements:

Transfers of product know-how and implementation of KBC’s distribution model

Setting up of sales-incentive schemes

Unified management responsibility (joint management committee of bank and insurance)

Focus on: ‘Plugged-in’ non-life and life products Life investment insurance (savings & investment)

Results are encouraging: realizations in 2004

Cross selling rates Czech Rep Hungary Poland Slovakia Belgium

Consumer loan X life assurance 83% n/a 100% 94% 67%

Mortgage loan X life assurance 45% 50% 100% 75% 67%

Mortgage X property insurance 54% 71% 42% 30% 50%

11

Key developments in AM Total AUM in CEE as at 31/03/2005: 5.5 bn

AUM grew in 04 by 25%; in Q105 up by 7.3% Projected growth: 1-2 bn EUR p.a.

Continued high growth of revenue: CAGR revenue on mutual funds: 15-20% CAGR revenue on pension funds: 11-14% Margins on mutual funds already aligned

with rest of Europe

Strong appetite for ‘risk-free’ investments: money-market and capital-guaranteed funds, KBC’s speciality

Market share

2003 200431/03/200

5Trend

CZ 19% 22% 23% ++

HU 8% 9% 10% ++

SL 6% 7% 7% ++

SI - 8% 9% +

PL 4% 4% 5% ++

Total AUM CE

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

Discretionary

Assets34%

Funds -

Institutional 9%

Funds -

Other5%

Funds - Retail

42%

Life Assurance

2%

Pension Funds

8%

Breakdown of AUM

12

Key developments in AM

Market challenger with excellent reputation in foreign funds and as product innovator (hedge funds, capital-guaranteed funds, etc.)

Adequate risk-control measures and state-of-the-art front-office systems developed over the past years

Cost/AUM ratios well below European average (around 16 bp vs. 20 bp for Europe)

Through the funds business, new clients are brought in and retained

Existing clients using their deposits to buy funds will replenish their deposit accounts after one year

Poland:

big succes: capital-guaranteed funds

20% of clients in funds are new clients

Czech Rep:

Most important market player

KBC-owned pension funds companies (10% market share, No. 3 in the market)

Slovenia:

Recently created AM company (mutual funds’ market share from 0 to 10% in < 1 year)

Pension fund company with market share of 21% (first player on the market)

Slovakia:

Recently created AM and pension fund companies

7.4% market share in mutual funds

Hungary:

3rd in mutual funds (10% market share)

13

0%

20%

40%

60%

80%

100%

120%

140%

160%

1995

2001

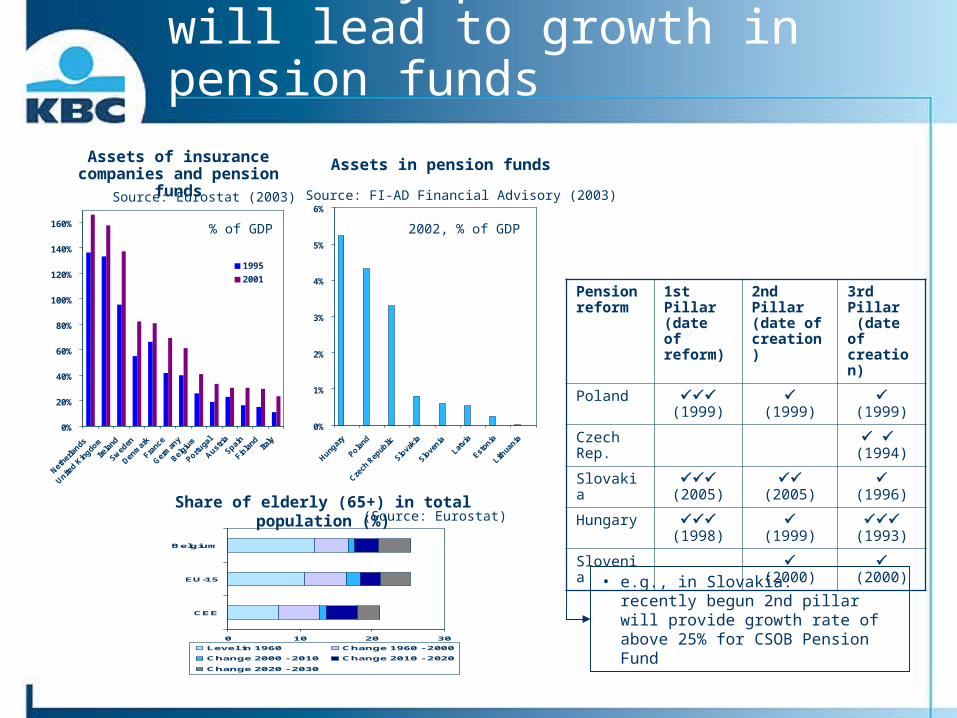

Necessary pension reformswill lead to growth in pension funds

Assets of insurance companies and pension funds

Source: Eurostat (2003)

0%

1%

2%

3%

4%

5%

6%Source: FI-AD Financial Advisory (2003)

% of GDP

Assets in pension funds

2002, % of GDP

0 10 20 30

CEE

EU-15

Belgium

Level in 1960 Change 1960 - 2000

Change 2000 - 2010 Change 2010 - 2020

Change 2020 - 2030

Share of elderly (65+) in total population (%)

• e.g., in Slovakia: recently begun 2nd pillar will provide growth rate of above 25% for CSOB Pension Fund

Pension reform

1st Pillar(date of reform)

2nd Pillar(date of creation)

3rd Pillar (date of creation)

Poland (1999)

(1999)

(1999)

Czech Rep.

(1994)

Slovakia (2005)

(2005)

(1996)

Hungary (1998)

(1999)

(1993)

Slovenia (2000)

(2000)

(Source: Eurostat)

14

Centralized organization for AM

Results: Lower costs (e.g., for Warta in Poland: -37%) Independent risk control and compliance Better investment process

KBC TFI

CSOB AM & IC

K&H SFIM

Poland

Czech Rep

Hungary

4 companies of KB and Warta

4 KBC-owned AM entities

2 KBC-owned AM entities (incl. ABN-AMRO AM)

Integration of companies (situation as at 1Q 2005)

KBC AMFormer entities

15

Nationwide branch networks

The density of KBC’s branch network is amongst the highest in the CEE region

In the Czech Rep.: branches in 123 of the 264 municipalities having more than 5 000 inhabitants. Additionally, products distributed via dense network of PSB (Postal Bank), which covers all 264 municipalities

In Slovenia: twice as many branches as the next competitor, being present in almost all municipalities having more than 5 000 inhabitants

In Hungary: presence in all larger towns and in half of the smaller towns. Only OTP has denser branch network

In Slovakia: branches in 58 of the 124 municipalities with more than 5 000 inhabitants

In Poland: presence in almost all major cities and in 25% of the smaller cities, comparable to or greater than competitors with similar market share. Further branch openings may be considered (under review)

0% 20% 40% 60% 80% 100%

PLCZSL

SIHU

0 200 400 600 800 1000

PL

CZ

SL

SI

HU

towns with KBC Groupbranch

No. of towns

Percent of towns with KBC Group branch Density of KBC Group’s branch network

16

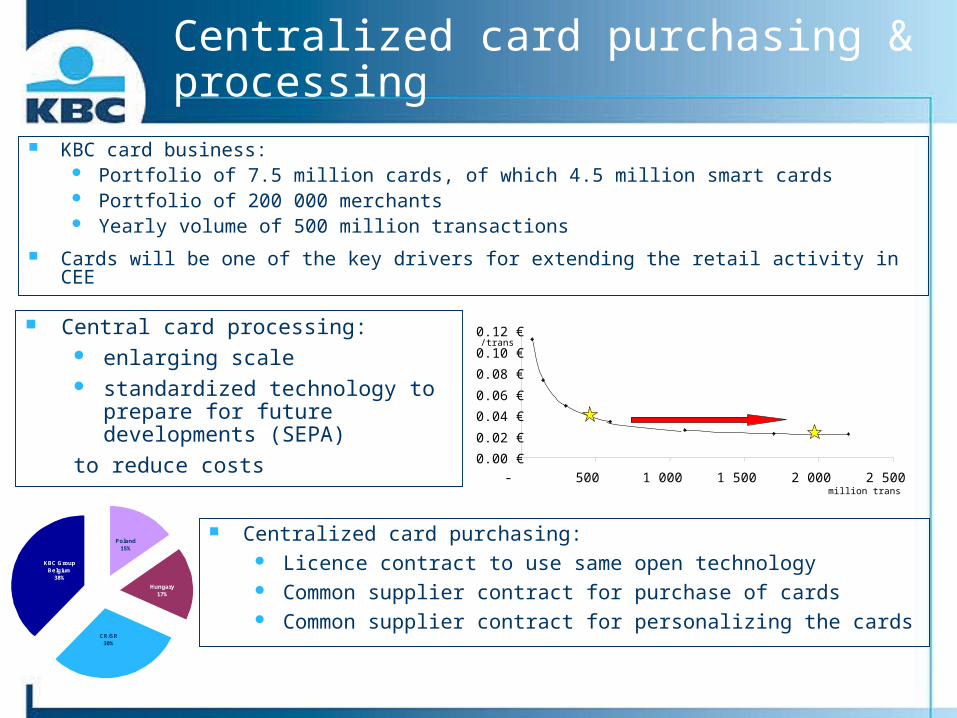

Centralized card purchasing & processing

KBC card business: Portfolio of 7.5 million cards, of which 4.5 million smart cards Portfolio of 200 000 merchants Yearly volume of 500 million transactions

Cards will be one of the key drivers for extending the retail activity in CEE

Central card processing: enlarging scale standardized technology to prepare

for future developments (SEPA)

to reduce costs0.00 €

0.02 €

0.04 €

0.06 €

0.08 €

0.10 €

0.12 €

- 500 1 000 1 500 2 000 2 500

/trans

million trans

Centralized card purchasing: Licence contract to use same open technology Common supplier contract for purchase of cards Common supplier contract for personalizing the cards

KBC Group Belgium

38%

Poland15%

Hungary17%

CR/SR 30%

17

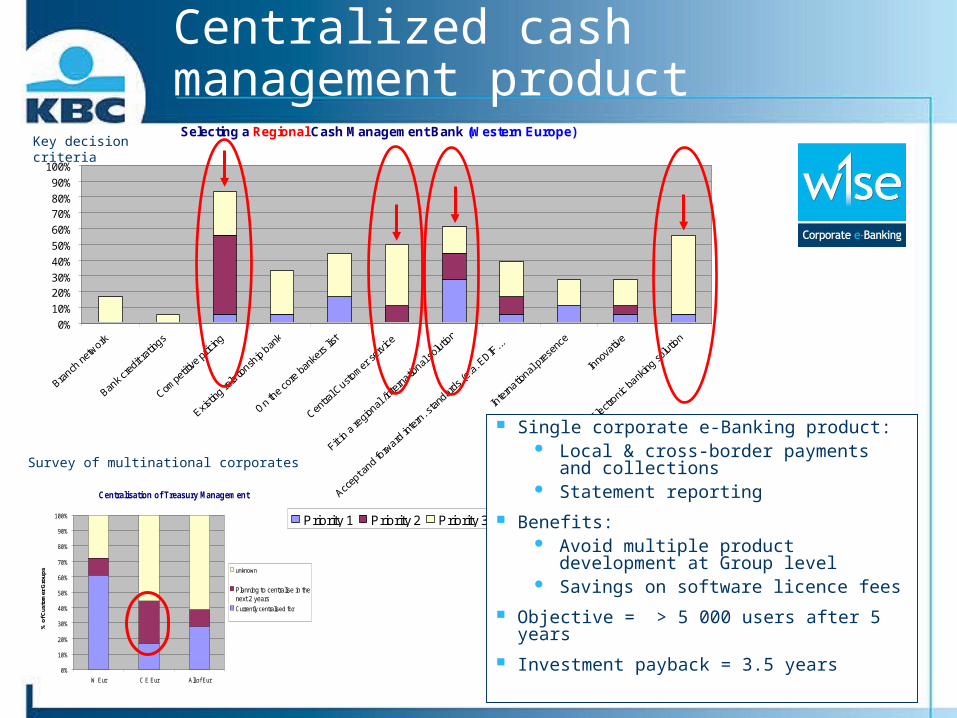

Centralized cash management product

Centralisation of Treasury Management

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

W Eur C E Eur All of Eur

% o

f Cus

tom

er G

roup

s unknown

Planning to centralise in thenext 2 yearsCurrently centralised for

Selecting a Regional Cash Management Bank (Western Europe)

0%

10%

20%30%

40%

50%

60%

70%80%

90%

100%

Priority 1 Priority 2 Priority 3-5

Key decision criteria

Single corporate e-Banking product: Local & cross-border payments and

collections Statement reporting

Benefits: Avoid multiple product

development at Group level Savings on software licence fees

Objective = > 5 000 users after 5 years

Investment payback = 3.5 years

Survey of multinational corporates

18

Centralized processing, cross-border payments

Business case: co-sourcing of cross-border transactions will lead to lower costs for the entire KBC Group

2007 …2003 2004 2005 2006

Sepa2010

CEEpre-study

legal/fiscal

Implementationsin CEE

Open for other

parties

Incl. KBC CEE

Incl. DZ Bank Group

Standalone

Volume of transactions

Pro

cessin

g c

osts 100

83

94

19

CEE entities: hands-on governance

KBC Group ExecutiveCommittee

CEE Management Committee

Steering committees CEEDirectorate

CEE business co-ordinators & task forces

CEEGroup companies

KBC expats(+ temporary presence

via various projects)

- General Manager

- Co-ordination unit

- Projects unit

- Controlling unit

Expats in banking: 35% of Management Board (of which 2 CEOs)*

Expats in insurance: 28% of Management Board (of which 4 CEOs)

Many KBC managers involved in CEE businesses and projects

For each business area, co-ordinators supervising the area, looking for synergies

CEE Directorate co-ordinates / supervises

0 2

23

04

24

16

31

12

17

54

2000 2001 2002 2005

Expat CEO's Expat MB members Expat Managers

KBC’s management expats in CEE

* Additionally 6 CEOs in AM and securities subsidiaries

20

Reminder: KBC’s presence in CEE

Update on economic and financial background

KBC’s opportunities

Update on Poland

Financial outlook

Agenda

21

Update on Poland Restructuring milestones:

22

Update on Poland

1Q 2005 achievements: Portfolio risk profile:

Portfolio quality improvement (NPL -20% y/y)

Zero cost of risk in 1Q 2005

Safe coverage ratio level (67%, one of the highest in the banking sector)

High net profit (23 m 1) and satisfactory ROE (21% 1 vs. 7% in 1Q 2004)

Continuous improvement of Cost/Income ratio (76% 1 vs. 86% in 1Q 2004)

Visible signs of growth acceleration:

18% increase in housing loans granted in PLN (y/y)

26% increase in loans granted in CHF(y/y)

75 000 new savings accounts (y/y) and 187% increase in saving accounts volume (y/y)

175% increase of mutual funds (y/y)

Today, we believe we are in a better shape than ever. We even intend to accelerate organic growth

1 Statutory accounts

23

Reminder: KBC’s presence in CEE

Update on economic and financial background

KBC’s opportunities

Update on Poland

Financial outlook

Agenda

24

Financial outlook

RWA2005-2007 CAGR

Net profit 2005-2007

CAGR

Loan-loss ratioMid-term

target

Cost/IncomeMid-term

target

Banking 10% – 15% 10% – 15% < 0.50% < 60%

Net earned premium 2005-2007

CAGR

Net profit 2004-2007

CAGR

Net Combined Ratio

Mid-term target

Insurance 15% – 25% 25% - 35% 95%