GROUP STRATEGY & GROWTH INVESTMENTS

108

GROUP STRATEGY & GROWTH INVESTMENTS Capital Markets Day 2018 Frankfurt am Main, November 28 Dr. Eric Taberlet, CEO

Transcript of GROUP STRATEGY & GROWTH INVESTMENTS

GROUP STRATEGY & GROWTH INVESTMENTS

Capital Markets Day 2018 Frankfurt am Main, November 28

Dr. Eric Taberlet, CEO

Agenda Group strategy

Our mission

Our strategic goals

Structure of the market and PV positioning

PV strategy and investment program

Summary

■ 4© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Our mission Collaboration … Communication

Pfeiffer Vacuum as a leader in high vacuum technology is contributing through its high value services and product offer to the ongoing industry revolution driven by:

The digitalization The energy transition The biotechnology ramp-up The nanotechnology revolution

Agenda Group strategy

Our mission

Our strategic goals

Structure of the market and PV positioning

PV strategy and investment program

Summary

■ 6

To become a strong number 2 in high vacuum technology:

Increasing market share (organically & acquisition) up to > 20% Increasing EBIT profitability > 20% Strengthening technology differentiation

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Our strategic goals

Agenda Group strategy

Our mission

Our strategic goals

Structure of the market and PV positioning

PV strategy and investment program

Summary

■ 8

High performance

Price/Performance

Costs

Positioning/Classification Pfeiffer Vacuum market segments

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Market segments Key drivers

• R&D• Analytics High performance

• Industry “Function”

• Semiconductor• Coating

Price, Performance, Reliability

Vacuum market

■ 9

The vacuum technology market Vacuum markets 12M 2017 (ISVT)

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Industrial Vacuum; 17%

Process Vacuum; 7%

R&D; 5%

Inst. Manufacturers; 7%

Thin-Film Deposition; 6%

Flat Panel Display; 8% Solar; 2%

Semi/Process Vacuum; 38%

Rough Vacuum;

10% Business Unit Analytics, Industry and R&D

36% of total market

Business Unit Semiconductor and Coating

54% of total market

Total market size 12M 2017: 4.49 bn Euro 3M 2018: 1.15 bn Euro

* Source: ISVT: Vacuum markets 12M 2017

■ 10

Major growth drivers Significant growth drivers in both business units

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Business units Growth drivers

Semiconductor and Coating

Digitalization (Big Data) Energy Electromobility

Analytics, Industry and R&D

Health/Life-science Security Materials

Display size / resolution / 3D etc.

Mobility Energy etc.

■ 11

Sales volume in 9M 2018: € 491 m (12M/2017: € 587 m, in € millions)

407 452 474

587 491

Guidance 640 - 660

0

100

200

300

400

500

600

700

2014 2015 2016 2017 9M/2018

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 12

Revenues Top 10 Customers

Number of Customers

Semiconductor 38% 80% >500

Industry 22% 21% >7,000

Analytics 17% 66% >700

Coating 13% 45% >1,000

R & D 10% 24% >2,000

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Structure of sales Pfeiffer Vacuum 2017

■ 13

Global sales, production and service network

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

€ 587 m sales in 2017 Today, around 3,100 employees Over 20 sales & service locations 8 production sites

Sales and services Production Distributor

Agenda Group strategy

Our mission

Our strategic goals

Structure of the market and PV positioning

PV strategy and investment program

Summary

■ 16

Technology and quality culture

Broad product portfolio

Great customer proximity and long-term customer relationships

Very good application knowledge

Worldwide presence of sales and service

Strong brand and very good image

Strengths of Pfeiffer Vacuum

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

1

2

3

4

5

7

High value oriented

Experienced and motivated management team

6

8

■ 17

Fields of application

Innovation leadership – Growth through new products

New business models- Wider service offer

China

Supply chain & global footprint

Selective acquisitions to extend technology

Strategic focus Pfeiffer Vacuum

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

1

2

3

4

5

6

■ 18

Enabler 1: Technology solutions = Innovation

Investment in development

Industry 4.0: Business opportunity and a differential value

Partnership to expand expertise: IP

Digitalization and big data as a value offer

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 19

Enabler 2: Operational excellence = Performance & Agility

Industrial footprint: Investment plan to increase capacity and regional presence

Automation and flexibility development: Smart manufacturing as a driver for agility

IoT and digitalization as innovation drivers

Global information system

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 20

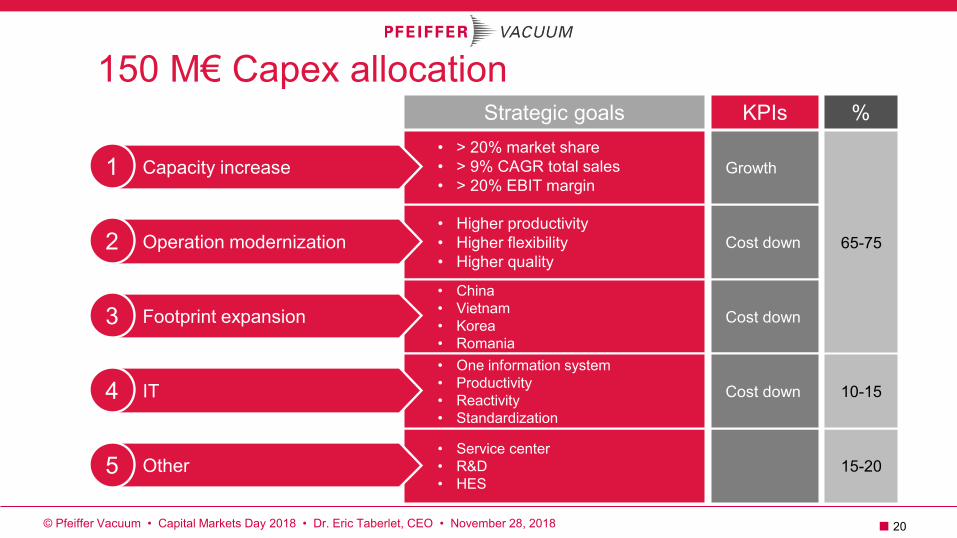

150 M€ Capex allocation

• Service center• R&D• HES

• Higher productivity• Higher flexibility• Higher quality

• China• Vietnam• Korea• Romania

• > 20% market share• > 9% CAGR total sales• > 20% EBIT margin

• One information system• Productivity• Reactivity• Standardization

Strategic goals

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Capacity increase

Operation modernization

Footprint expansion

IT

Other

1

2

3

4

5

Cost down

Cost down

Growth

Cost down

KPIs

15-20

65-75

10-15

%

■ 21

Enabler 3: People = Expertise and customer oriented Empowering employees: Innovation in management

toward more participative management

Skills development and HR digitalization as a driver

Expanding skills and knowledge to the regions: Applications

Key account management

Agile and lean organization

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 22

Enabler 4: Management Board: Reorganization

CEO & CSO Global market

strategy, Sales & Service

CFO Finance/Controlling,

HR, IT, Communication, IR

COO Operations

(Procurement, Production, Logistics)

CTO Global Product and

Technology strategy, R&D

In order to implement the individual areas of the growth strategy more quickly and with greater focus, it has been decided to rearrange the organizational structure of the Management Board as of January 1, 2019.

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 23

Enabler 5: Strategic cooperation with the Busch Group

Cooperation will be focused especially on the areas of Purchasing, Salesand Services, Research & Development as well as IT

Goals: Strengthening the competitive position, utilizing growth potential andincreasing efficiency

Cooperation supports growth strategy based on three-year investment planof € 150 millions

Negotiations are ongoing. Goal: Finalizing the agreement by end of this year

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 24

Positioning/Classification Pfeiffer Vacuum & Busch

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Pfeiffer Vacuum

Busch SE

High vacuum (+ UHV)

Fine vacuum

Rough vacuum

Different markets

Vacuum market

■ 25

Potential synergies of the cooperation with the Busch Group

IT

Common use of servicecenters & infrastructure Improve territory coverage Cross selling

Volume effect Global sourcing

Bundle purchase potential forIT services/licenses Exchange best practice approach

in ERP/Infrastructure processes Exchange on digitalization efforts

in respect of Industry 4.0

Co-development projects Align & strengthen common

product portfolio Development of

technology bricks

Pfeiffer Vacuum Busch Group

Procurement

Service & Sales R&D /

Products

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Agenda Group strategy

Our mission

Our strategic goals

Structure of the market and PV positioning

PV strategy and investment program

Summary

■ 27

Summary

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Our goal is to offer continuous contribution to the ongoing industrial revolution

Ambitious targets to strengthen our number 2 position in the Vacuum technology market

Clear product strategy reinforcing our technology leader positioning

Ambitious Capex and Opex to sustain the strategy

New Board organization to better focus on the key pillars of strategy

Strategic cooperation with Busch Group to speed up the strategy execution

GROUP CENTRAL FUNCTIONS

Capital Markets Day 2018 Frankfurt am Main, November 28

Nathalie Benedikt, CFO

Agenda Central Functions

Overview Central Function targets

IT Strategy roadmap

Human Resources

Corporate Communications

Finance & Controlling

■ 30

Overview Central Function targets

• Maintain and improve EBIT margin• Investment ROI tracking• Maintain strong OCF

• Develop HR Strategy• Implement Global HR Business Partner team

• Develop Global Communication strategy• Implement Global Communication organization

• Develop IT strategy• Implement Global IT organization• Move IT from run to built >> business enabler

Activities

© Pfeiffer Vacuum • Capital Markets Day 2018 • Nathalie Benedikt • November 28, 2018

IT 1

Finance & Controlling 2

HR 3

Global Communication 4

EBIT margin, ROI project tracing, OCF

Finalize strategy paper; install new organization

Conceivable KPIs

Finalize strategy paper; install new organization

Finalize strategy paper; install new organization

Agenda Central Functions

Overview Central Function targets

IT Strategy roadmap

Human Resources

Corporate Communications

Finance & Controlling

■ 32

IT Strategy roadmap

Global IT organization

Strong IT budget

One global ERP system! Today 5 ERP with many interfaces

Standardization of processes to lower the cost

IT needs to be fast (standardized), flexible (cloud/outsourcing) and business focused.

© Pfeiffer Vacuum • Capital Markets Day 2018 • Nathalie Benedikt • November 28, 2018

■ 33© Pfeiffer Vacuum • Capital Markets Day 2018 • Nathalie Benedikt • November 28, 2018

Application scoping phase has started in Q3/2018

Whole strategy implementation will need 4 to 6 years

Appl

icat

ions

ERP: SAP R3, proAlpha,MyFactory, Syteline, Sage

CAD: proEngineer, Inventor, SolidWorks, Catia

Sales: Saratoga CRM

HR: Lumesse, SAP, SD Works

Service: ERP, IBM, VSM

ONE ERP

One CAD

One CRM

One HR

One Service

IT Strategy roadmap

TODAY: TOMORROW:

■ 34

Key drivers of our IT Strategy:

Enable the Company to achieve the Digital Transformation

Optimize operational costs

Focus on high-impact business solutions

Cloud first

One tool for one task managed by one team

Allow people to collaborate in a flexible and simple way

© Pfeiffer Vacuum • Capital Markets Day 2018 • Nathalie Benedikt • November 28, 2018

IT Strategy roadmap

Agenda Central Functions

Overview Central Function targets

IT Strategy roadmap

Human Resources

Corporate Communications

Finance & Controlling

Implement new agile, team oriented „Group Spirit“

New ‘Global HR Business Partner’ organization to support entities

and ensure best practice

Significantly improve ‘HR Development’, ‘Employer Branding &Hiring’

Increase social media activities

Strong future CSR footprint

HR Strategy: Core elements

Ram

p up

act

iviti

es s

tart

ing

2019

with

n

ew G

loba

l HR

Sup

port

Org

aniz

atio

n

Agenda Central Functions

Overview Central Function targets

IT Strategy roadmap

Human Resources

Corporate Communications

Finance & Controlling

Global communication strategy: What‘s new ? Building up Global Communication team

Stronger promotion of the cutting-edge technologybrand

Considering country specific marketingcommunication needs(Internet presence/Advertising/Social Media...)

Create modern + creative customer contact points

Boost internal communication to support companytransformation

Collaboration … Communication

Agenda Central Functions

Overview Central Function targets

IT Strategy roadmap

Human Resources

Corporate Communications

Finance & Controlling

■ 40

Strategy SUMMARY:

Production capacity

Leading innovations

IT & Industry 4.0

Market share growth

China footprint

Global operations

Agile, flat company culture

Strong number 2 ! EBIT > 20 %

Finance & Controlling: Financial outlook

Guidance 2018 expected to be achieved at lower end

Overall Pfeiffer Vacuum is in a transforming period

Margins in the next 2 to 3 years will be impacted by investments and higherOPEX because of all strategy implementations

During the transformation no significant margin improvement expected

BUT: Transformation has the clear target :

1. To become a strong number 2 in the vacuum industry

2. To achieve EBIT margins > 20 % in the next 3 to 5 years

© Pfeiffer Vacuum • Capital Markets Day 2018 • Nathalie Benedikt • November 28, 2018

GLOBAL OPERATIONS

Capital Markets Day 2018 Frankfurt am Main, November 28

Dr. Matthias Wiemer, Member of the Management Board

Agenda Global Operations

Global Footprint: Today / Strategy / Perspective 2021

Global Procurement: Trends & Strategy development

Global Operations: Summary & Key projects

■ 44

Production Footprint today

Annecy / France

Asslar / Germany Goettingen / Germany

Cluj / Romania

Asan / Korea

Indianapolis / USA

Yreka / USA

Ho Chi Minh City / Vietnam

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

■ 45

General objectives:

Increase capacity based on the current business plan

Reduce manufacturing and transportation costs (Asia Europe)

Optimize capital expenditure

Concentrate pump technologies Rotary Vane Pump (RVP)

Improve access to local procurement (see global sourcing strategy)

Establish a presence closer to major customers

Adapt structure of value added to market and sales mix

Improve FX exposure

Global Footprint strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

■ 46

Production Footprint perspective 2021 New production site for Dry Pumps in China

Annecy / France

Asslar / Germany Goettingen / Germany

Cluj / Romania

Asan / Korea

Indianapolis / USA

Yreka / USA

Ho Chi Minh City / Vietnam

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

NEW: Wuxi / China

■ 47

Production Footprint perspective 2021 New production site for Dry Pumps in China

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

37% 37%

26%

74%

12%

14%

Sales:

Value added:

2018 2021

33% 42%

25%

62%

25%

13%

Europe Amerika Asia

■ 48

Global Production strategy: established and based on the Group strategyand Group objectives

Asian market: above average growth => installed capacity in Asia will growfaster than in the EU

Major large production sites in Europe will be modernized

For Nor-Cal production sites new structure will be installed in order to supportthe profitable growth

Global production strategy supports growth strategy of both Business Units(AIR / Semi & Coating) and of Components & Solutions

Based on a group wide assessment of the supply chain a Global Operationstrategy will be developed

Global Production Footprint summary

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

Agenda Global Operations

Global Footprint: Today / Strategy / Perspective 2021

Global Procurement: Trends & Strategy development

Global Operations: Summary & Key projects

■ 50

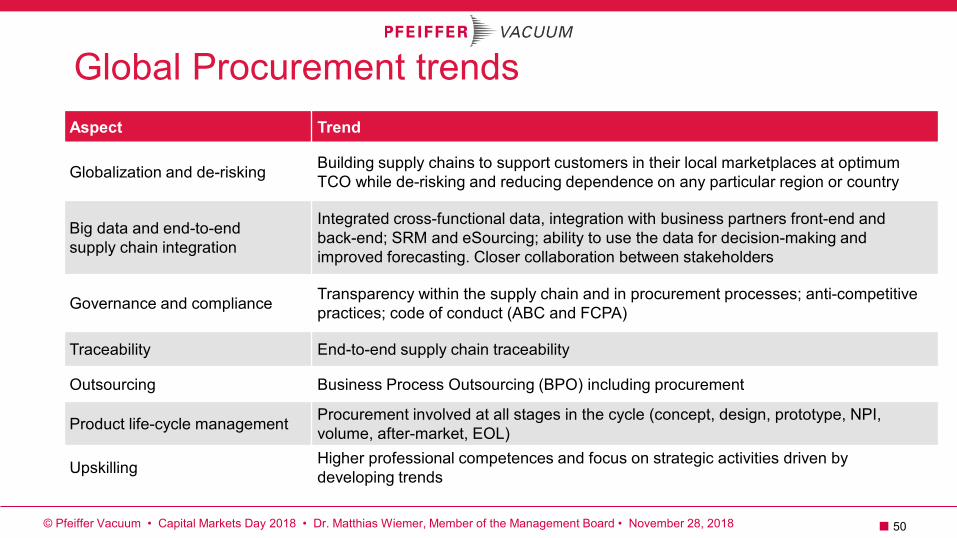

Global Procurement trends Aspect Trend

Globalization and de-risking Building supply chains to support customers in their local marketplaces at optimum TCO while de-risking and reducing dependence on any particular region or country

Big data and end-to-end supply chain integration

Integrated cross-functional data, integration with business partners front-end and back-end; SRM and eSourcing; ability to use the data for decision-making and improved forecasting. Closer collaboration between stakeholders

Governance and compliance Transparency within the supply chain and in procurement processes; anti-competitive practices; code of conduct (ABC and FCPA)

Traceability End-to-end supply chain traceability

Outsourcing Business Process Outsourcing (BPO) including procurement

Product life-cycle management Procurement involved at all stages in the cycle (concept, design, prototype, NPI, volume, after-market, EOL)

Upskilling Higher professional competences and focus on strategic activities driven by developing trends

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

■ 51

Procurement to become a strategic enabler aligning to Group strategy andGlobal Operations strategy

Create distinct procurement and supply chain competencies/organizations which focus onsupply/supplier management and supplier development respectively

Achieve optimum customer lead times & total cost of ownership by re-balancing the globalsupply chain to focus on proximity to point of consumption and customers locations. Createsignificant procurement capability in APAC and CEE

Intensity focus on design to cost by procurement, early stage supplier engagement anduse of supplier partnerships in new product development has potential to reduce product costat launch by 20%

Continuity of supply, supply chain sustainability and compliance need to be key elements ofprocurement operations to support business growth and profitability

Global Procurement strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

■ 52

Strategy development Global Procurement

Tim

ing

/ Pha

sing

COMPETITIVENESS

PROCUREMENT STRATEGY

Global and local supplier approach

Early design engagement

Secure continuity of supply

Collaboration

Common Process

Common Philosophy

Tactical execution

Strategic enabler

Group strategy

Global Operations strategy

Global Procurement strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

Agenda Global Operations

Global Footprint: Today / Strategy / Perspective 2021

Global Procurement: Trends & Strategy development

Global Operations: Summary & Key projects

■ 54

Strategy focal points Global Operations

Providing the necessary capacity 1

2

Establish a presence closer to major customers 3

4

5

Operational excellence 6

Adapt structure of value added to market and sales mix

Modernizing existing sites

Improve access to local procurement

Group strategy

Global Operations strategy

Global Procurement strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

■ 55

Global Operations and machining strategy development Strategy, costs, benefits, organization, KPI’s, planning & timelines

Global Procurement & Supply chain strategy development Strategy, costs, benefits, organization, KPI’s, planning & timelines

Semi/Coating BU service performance improvement

Nor-Cal product and supply chain migration planning from Yreka & US to APAC

AIR and C&S procurement and supply chain organizational planning,roles & responsibilities

APAC presence and capability

Key projects Global Operations

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Matthias Wiemer, Member of the Management Board • November 28, 2018

BUSINESS DEVELOPMENT SEMICONDUCTOR & COATING

Capital Markets Day 2018 Frankfurt am Main, November 28

Dr. Eric Taberlet, CEO

Agenda Business Development Semiconductor & Coating

BU Semi & Coating key figures

BU Semi & Coating key applications & drivers

BU Semi & Coating business key value propositions

Summary

■ 58

BU Semi & Coating sales development – 9 months

2017 2018

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

261 M

219 M YOY growth driven by: • Solar technology investments• Smart phones packaging• China

YOY growth driven by: • Intensive Capex spending• Memory DRAM and 3D NAND• China

Coating

Semi

+ 19 %

■ 59

Asia Asia

China China

Amercias

Amercias

EMEA

EMEA

2017 2018

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

261 M

219 M + 19 %

YOY growth driven by:

• New development of China• Market share gain in semi/US• Nor-Cal acquisition in the US• Strong dynamic in Europe

Regions

BU Semi & Coating sales development – 9 months

■ 60

Turbopumps Turbopumps

Instruments &

Components

Instruments &

Components

Backing pumps

Backing pumps

Service

Service Systems

Systems

2017 2018

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

261 M

219 M + 19 %

YOY growth driven by: • Nor-Cal acquisition (Components) • Backing pumps (Semiconductor, Solar) • Systems and Service (Semiconductor) • Turbo (Coating)

Products

BU Semi & Coating sales development – 9 months

Agenda Business Development Semiconductor & Coating

BU Semi & Coating key figures

BU Semi & Coating key applications & drivers

BU Semi & Coating business key value propositions

Summary

■ 62

Major growth drivers Significant growth drivers in Semi & Coating

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Business units Growth drivers

Semiconductor and Coating

Digitalization (Big Data) Energy Electromobility

Analytics, Industry and R&D

Health/Life-science Security Materials

Display size / resolution / 3D etc.

Mobility Energy etc.

■ 63

$8.5B

$29B

$80B

$100B

$270B

$500B

$1,500+B

Healthcare

New human machine interface

Hyperscale data centers

Industry 4.0 & industrial IoT

5G

Mobile

Smart automotive

Electronic megatrends

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Estimated $2 500B in 2021

Source: Yole Development 2018

■ 64

From megatrends to Pfeiffer Vacuum Market drivers

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Our target markets are key contributors in major mega trends Shaping the next decades

Our industry at a turning point

…

Energy transition

Semiconductor Display Green Energy

• OLED, Flex• Large TVs, Gen 10+

• Solar PERC/CIGS• LED• Energy storage

• Memory/3D NAND• Foundry• Patterning/ EUV

China China China

■ 66

What we see and believe… Short term assumption:

Nobody knows: downturn, flat, ramp up ??

Message across the board from our customers: be prepared for anyscenario because…

Mid-/long-term assumption: Semi industry changing:

Scale: higher capacity needed to long term semi market potential

It’s no longer about increasing speed just through smallertransistors, it’s all about new ways of for more advanced chips

Agility again and again will be key differentiator

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

© Intel/Micron

3D-NAND

■ 67

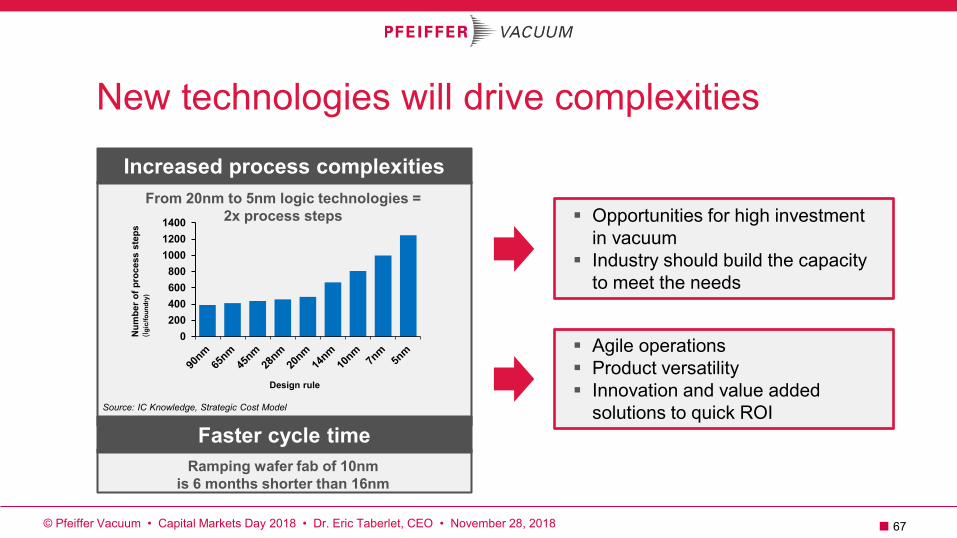

Ramping wafer fab of 10nm is 6 months shorter than 16nm

From 20nm to 5nm logic technologies = 2x process steps

Increased process complexities

Faster cycle time

New technologies will drive complexities

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Opportunities for high investmentin vacuum

Industry should build the capacityto meet the needs

Agile operations Product versatility Innovation and value added

solutions to quick ROI

0200400600800

100012001400

Num

ber o

f pro

cess

ste

ps

(lgic

/foun

dry)

Design rule

Source: IC Knowledge, Strategic Cost Model

■ 68

Materials will drive the innovation

Material innovation will drive the semidevices roadmap: new dielectric, metals(Tantalum, Manganese..), low-k…

3D Structures (NAND) require betterconformality and selectivity: innovativeprocesses (Epi, Etch , ALD, ALE ..)

Faster devices: Interconnect

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Source: Entegris

?

65 45 28 20 14 10 7

Rel

ativ

e im

pact

on

devi

ce

perf

orm

ance

Node in nm

ScalingDesignMaterials

■ 69

Vacuum

Integrated Subsystems

Power

Fluid Management

Wafer Handling

Other Subsystems

Thermal

Integrated Process Diagnostics

0,0 0,5 1,0 1,5 2,0 2,5 3,0 3,5

Vacuum shows highest growth between 2018-2022

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Critical Subsystems Revenues, $Bn Semiconductor Vacuum pumps counting

the highest growth:

more vacuum steps inthe new technologyinflections and morecapital expenditure inthe memory sector

By 2023 the market forvacuum subsystemscould reach 3 B USDfor semi

2017

2023

Source: VLSI Research Inc.

Agenda Business Development Semiconductor & Coating

BU Semi & Coating key figures

BU Semi & Coating key applications & drivers

BU Semi & Coating business key value propositions

Summary

BU Semi & Coating key figures

■ 71

Gauges & Valves

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Turbopumps

Integrated Dry Pumps

Process Dry Pumps

Leak Detectors

Contamination Control Systems

Gas Abatement Systems

Semi / Coating product offer CLEANROOM

SUB-FLOOR

BASEMENT

■ 72

Products robustness handling:More powder formation, more corrosivegases

Product flexibility handling mixed chemistryEtch, Clean, CVD ..

Total cost of ownership Agile operations Close cooperation with customer for quick

product adaptation

Our response and value proportion

High process flexibility requirements New process requirements /

quick adaptations New materials requirements /

quick adaptation Shorter time to ramp up => maximizing

ROI on Capital intensive cycles

Customer critical needs

Technical inflections: Pfeiffer Vacuum value proposition

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 73

Agility in production, development and service solution

Close to customer location with dedicated application and support teams

New opportunities on Products/service offers: The great value of data (the new oil) !! Turning data into economic value will be a key differentiator

Our response and value proportion

Implement solutions into high volume manufacturing: fast

A partnership with extended development capability to meet the fast changing environment

Moving toward yield prediction value

Customer critical needs

Industry shift 4.0: Pfeiffer Vacuum value proposition

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

■ 74

Global service capabilities close to customers

Advanced service solutions development Innovative solutions:

Mobility and data mining

Our response and value proportion

Maintaining installed base: high utilization

High utilization rate of infrastructures => higher uptime constraints

Continues adaptation of the products to process evolutions => strong application support and quick development process

Prediction becoming key

Customer critical needs

Service value proposition

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Agenda Business Development Semiconductor & Coating

BU Semi & Coating key figures

BU Semi & Coating key applications & drivers

BU Semi & Coating business key value propositions

Summary

■ 76

Summary

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Eric Taberlet, CEO • November 28, 2018

Our Goal: A solid disruptive N°2 in the vacuum industry

Our Vision

Innovations in vacuum solutions will enable technologies shaping the future

Our Mission

Leading the industry transformation, innovating in solutions and business models to enable customers success

BUSINESS DEVELOPMENT ANALYTICS, INDUSTRY AND R&D

Capital Markets Day 2018 Frankfurt am Main, November 28 Dr. Ulrich von Huelsen, Member of the Management Board

Agenda BU Analytics, Industry and R&D

Pfeiffer Vacuum AIR business

Major growth drivers

Business Unit Analytics

Strategy map

Summary

■ 79

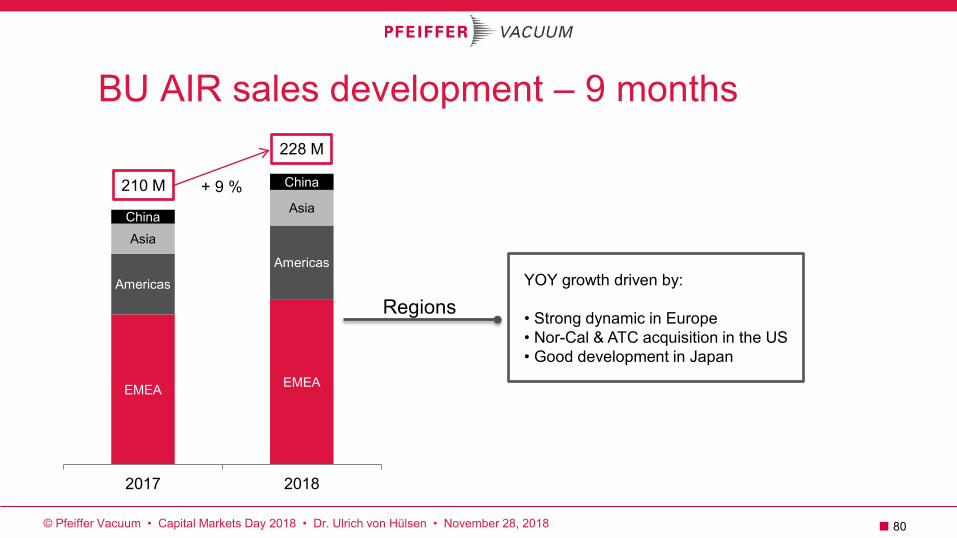

BU AIR sales development – 9 months

2017 2018

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

228 M

210 M

YOY growth driven by: • North America, Asia • Focus applications • New customers YOY growth driven by: • Mass spectrometry • Electron microscopy • Leak detection • New customers

Industry

Analytics

+ 9 % R & D

YOY growth driven by: • North America, Europe, Asia • Nor-Cal

■ 80

BU AIR sales development – 9 months

EMEA EMEA

Americas Americas

Asia

Asia China

China

2017 2018

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

228 M

210 M + 9 %

YOY growth driven by: • Strong dynamic in Europe • Nor-Cal & ATC acquisition in the US • Good development in Japan

Regions

■ 81

BU AIR sales development – 9 months

Turbopumps Turbopumps

Instruments &

Components

Instruments &

Components

Backing pumps

Backing pumps Service

Service Systems

Systems

2017 2018

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

228 M

210 M + 9 %

YoY growth driven by: • Nor-Cal acquisition (components) • ATC acquisition (components) • Leak detectors (Industry, Analytics) • Turbo (Analytics)

Products

Agenda BU Analytics, Industry and R&D

Pfeiffer Vacuum AIR business

Major growth drivers

Business Unit Analytics

Strategy map

Summary

■ 83

Major growth drivers Significant growth drivers in Analytics, Industry and R&D

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

Business units Growth drivers

Semiconductor and Coating

Digitalization (Big Data) Energy Electromobility

Analytics, Industry and R&D

Health/Life-science Security Materials

Display size / resolution / 3D etc.

Mobility Energy etc.

Agenda BU Analytics, Industry and R&D

Pfeiffer Vacuum AIR business

Major growth drivers

Business Unit Analytics

Strategy map

Summary

■ 85

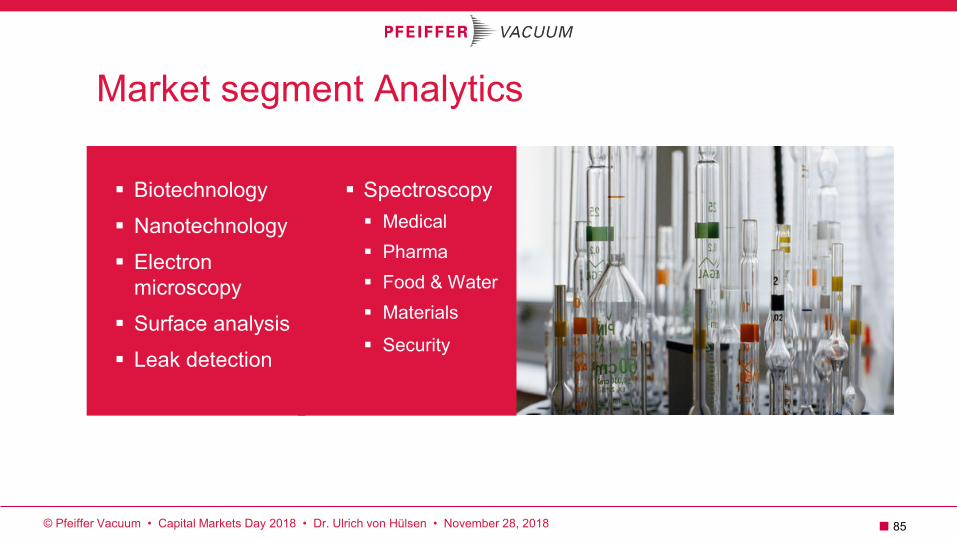

Market segment Analytics

Biotechnology

Nanotechnology

Electron microscopy

Surface analysis

Leak detection

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

Spectroscopy Medical Pharma Food & Water Materials

Security

■ 86

Pfeiffer Vacuum is market leader in the Analytic market – Why?

Q QUALITY

Highest reliability

T TECHNOLOGY

Performance Lowest vibrations

C COMPETENCE Customer specific

solutions

E EXPERIENCE Our know-how for your applications

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

■ 87

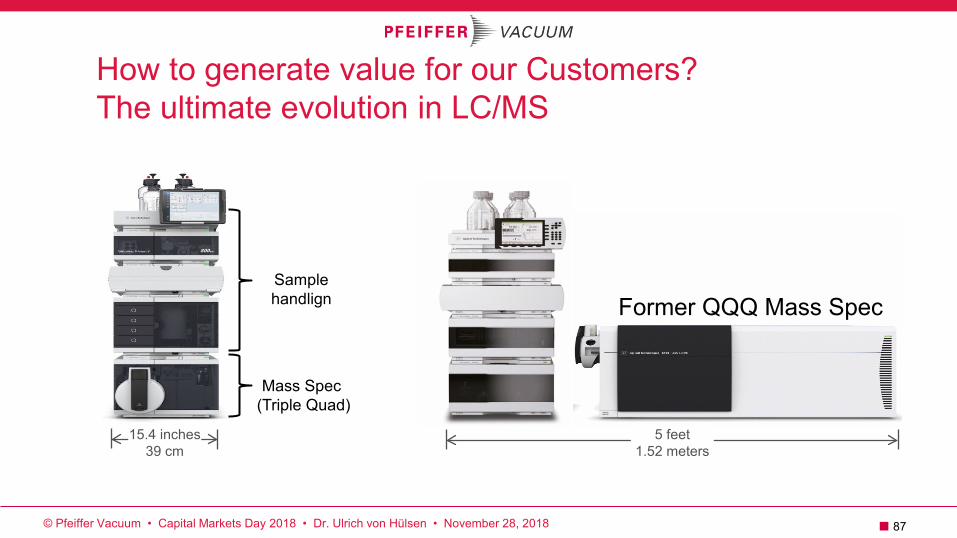

How to generate value for our Customers? The ultimate evolution in LC/MS

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

5 feet 1.52 meters

Former QQQ Mass Spec

Mass Spec (Triple Quad)

Sample handlign

15.4 inches 39 cm

■ 90 ■ 90

Vacuum solutions for the AIR business

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

Pharmaceutical industry Container Closure Integrity Testing (CCIT)

Analytical industry Portable mass spectrometer systems

Mobile dry high Vacuum systems Light weight

Small installation footprint

Low power input for long battery operation

Insensitivity of vacuum equipment to external shock vibration

Leak detection and leak testing Tracer gas leak detectors with helium / hydrogen

Micro-flow leak testing with air

Optical emission spectroscopy

Agenda BU Analytics, Industry and R&D

Pfeiffer Vacuum AIR business

Major growth drivers

Business Unit Analytics

Strategy map

Summary

■ 92

Strategy map Extend market share Generate differentiation for our OEM-customers Partner of choice for new analytics applications

Analytics

Select and focus the right applications Transfer analytics success to Industry OEMs Focus on fastest, high quality service

Industry

Unmatched reputations due to performance and reliability Synergies from acquisition Increased sales focus

R&D

Capacity increase Digitalization Global service presence

AIR strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

■ 93

Strategy map Extend market share Generate differentiation for our OEM-customers Partner of choice for new analytics applications

Analytics

Select and focus the right applications Transfer analytics success to Industry OEMs Focus on fastest, high-quality service

Industry

Unmatched reputations due to performance and reliability Synergies from acquisition Increased sales focus

R&D

Capacity increase Digitalization Global service presence

AIR strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

■ 94

Strategy map Extend market share Generate differentiation for our OEM-customers Partner of choice for new analytics applications

Analytics

Select and focus the right applications Transfer analytics success to Industry OEMs Focus on fastest, high quality service

Industry

Unmatched reputations due to performance and reliability Synergies from acquisition Increased sales focus

R&D

Capacity increase Digitalization Global service presence

AIR strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

■ 95

Strategy map Extend market share Generate differentiation for our OEM-customers Partner of choice for new analytics applications

Analytics

Select and focus the right applications Transfer analytics success to Industry OEMs Focus on fastest, high quality service

Industry

Unmatched reputations due to performance and reliability Synergies from acquisition Increased sales focus

R&D

Capacity increase Digitalization Global service presence

AIR strategy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

Agenda BU Analytics, Industry and R&D

Pfeiffer Vacuum AIR business

Major growth drivers

Business Unit Analytics

Strategy map

Summary

■ 97

Summary

© Pfeiffer Vacuum • Capital Markets Day 2018 • Dr. Ulrich von Hülsen • November 28, 2018

Success in Analytics is continuing Industry strategy is getting traction

Our goal is to grow significantly faster than the market

R&D sales initiatives are getting traction Goal: Extend leadership to more and more applications Key investments

Capacity R&D Digitalization

Key enablers mentioned in Group strategy

CHINA DEVELOPMENT FOCUS

Capital Markets Day 2018 Frankfurt am Main, November 28 Mrs. Hind Beaujon, VP Business Unit Semiconductor & Coating

■ 99 © Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

Who has ever tried to drink from a hose?

■ 100 © Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

Huge opportunities

China 13th plan National policies

Competitiveness

Trade war

Intensive expansions

Made in China 2025

………….. IPs

That’s how it feels working with China

■ 101

What to do with all of that ?

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

To be able to drink from this hose... we need a filter: A strategy

1. Identify core areas of growth for Pfeiffer Vacuum

2. Define a focused strategy for long-term development in China

3. Define the way to execute this target

4. Assess the risks and try to manage them the best we can and stay flexible

■ 102

The growth engine of the global economy

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

China has become the largest and the fastest growing market in the world

13%

18%

20%

23%

27%

30%

0% 5% 10% 15% 20% 25% 30% 35%

Ultramobile

STB

TV

Desktop PC & Notebook

Mobile phone

Light vehicle

China unit shipments in 2016 as % of worldwide share

~28M units

~501M units

~51M units

~61M units

~55M units

~27M units

Source: Gartner, HIS, Team estimations, 1H17

■ 103

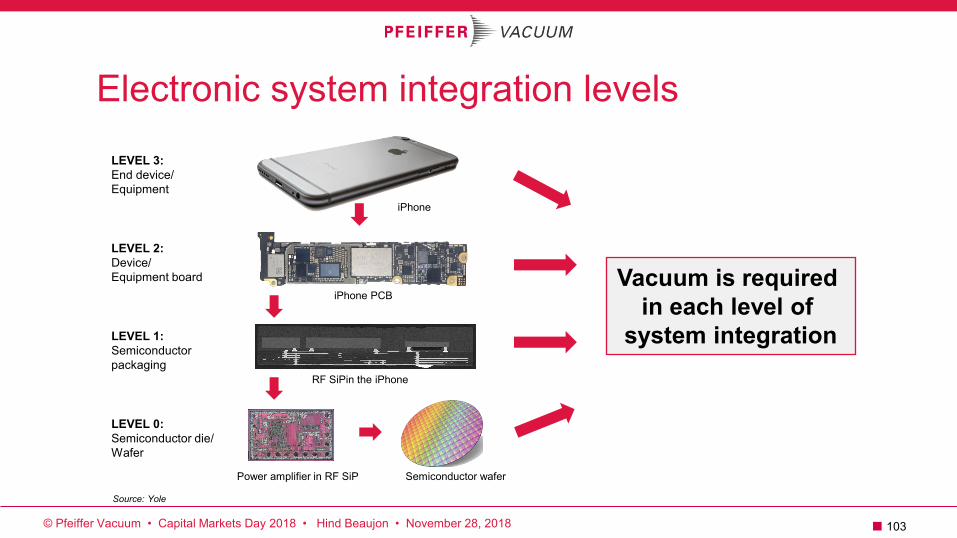

Electronic system integration levels

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

Vacuum is required in each level of

system integration

LEVEL 3: End device/ Equipment

LEVEL 2: Device/ Equipment board

LEVEL 1: Semiconductor packaging

LEVEL 0: Semiconductor die/ Wafer

Semiconductor wafer Power amplifier in RF SiP

RF SiPin the iPhone

iPhone PCB

iPhone

Source: Yole

■ 104

China smart phone OEM’s / 5G

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

Xiaomi

■ 105

IoT – Increasing needs of vacuum

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

Reliability x Power consumption

2017

Front 3D camera

Front 3D camera

Front 3D camera Rear 3D camera

Front 3D camera Rear 3D camera

2018 2019 2020

Development of 3D imaging in mobile devices

Source: Yole

■ 106

Greater China’s role in IoT growth

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

There will be more than 40 billion wireless connected devices

>20% of those devices will be in Greater China

Greater China IoT market to reach 10 Trillion (CNY)

By 2020

Source: KPMG

■ 107

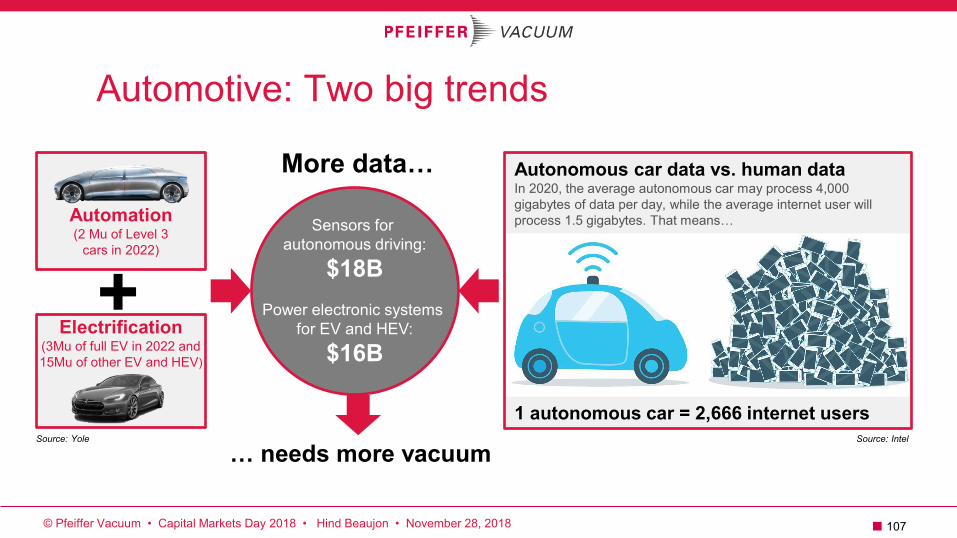

Source: Intel Source: Yole

Sensors for autonomous driving:

$18B

Power electronic systems for EV and HEV:

$16B

Automotive: Two big trends

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

… needs more vacuum

+

Automation (2 Mu of Level 3

cars in 2022)

Electrification (3Mu of full EV in 2022 and 15Mu of other EV and HEV)

More data… Autonomous car data vs. human data In 2020, the average autonomous car may process 4,000 gigabytes of data per day, while the average internet user will process 1.5 gigabytes. That means…

1 autonomous car = 2,666 internet users

■ 108

Greater China’s role in IoV growth

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

3,5

17,2

25,3

34,2

0

10

20

30

40

2005 2010 2015 2020

Greater China surpassed the U.S. in 2010 to become the #1 passenger car market

Passenger car sales in China

41%

35%

14%

10%

RoWGreater ChinaNorth AmericaEurope

By 2020, Greater China is expected to represent ~35% of new car sales

New car sales forecast: 2020

Source: Excolus / China Auto 2020

■ 109

Increasing memory needs Needs vacuum

Entering the data era... and China is a key market

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

Shanghai: 27M people (registered) in 2020 5 400 M GB data per day

2M 4M

40M 50M 50M

55M

Smart airplanes

Social media + other

Smart vehicles

Smart factories

Public safety systems

Smart buildings

Explosion of data generation In 2020, a city of 1M people will generate 200M GB of data per day.

Source: AMAT

■ 110

From mega to market trends = Focused markets

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

46% of WW IC market by 2020 >40 % of new investments in 2017-2020

49% of WW manufacturing capacity by 2020 >75% of new investments in 2017-2021

>60% of WW manufacturing capacity is Chinese >70 % of investments are in China or Chinese funds

Semiconductor Display Green Energy

• OLED, Flex • Large TVs, Gen 10+

• Solar PERC/CIGS • LED • Energy storage

• Memory/3D NAND • Foundry • Patterning/ EUV

China China China

■ 111

China opportunities: Pfeiffer Vacuum strategy Investment in China:

Industrial footprint/supply chain

Sales and support capacity

Products to address China market needs

Sourcing partnerships for targeted segments/products to enable:

Strategic partnership for market penetration acceleration

Industrial synergies for “2025 Made in China” plan

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

■ 112

China opportunities: Pfeiffer Vacuum strategy

2018 executions: Service operations capacity increasing

ongoing

First milestone for assembly localization for the Chinese market

Kick-off of local supply chain/sourcing

Development of the local application team

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

Wuxi

Wuxi

■ 113

Summary China, an opportunity and a challenge

China is part of Pfeiffer Vacuum’s 3-years plan and long-term development

Pfeiffer Vacuum is seeking innovation in:

Business model

Technology and products to address the Chinese market

Stay tuned...

© Pfeiffer Vacuum • Capital Markets Day 2018 • Hind Beaujon • November 28, 2018

CAUTIONARY STATEMENT Some statements herein are forward-looking and the actual outcome could be materially different. In addition to the factors explicitly commented upon, the actual outcome could be materially and adversely affected by other factors such as the effect of economic conditions, exchange-rate and interest-rate movements, political risks, the impact of competing products and their pricing, product development, commercialization and technological difficulties, supply disturbances, and major customer credit losses.

© Pfeiffer Vacuum • Capital Markets Day 2018 • Disclaimer • November 28, 2018