![Green Bonds - - EESL PPT Gaurav.pdf · 4 Leading Green Bonds in Asia [1/2] Thought Leadership in Green bonds in Asia India Green Bonds Market Development Council: In recognition of](https://static.fdocuments.us/doc/165x107/5b93665609d3f2d9098d351d/green-bonds-eesl-ppt-gauravpdf-4-leading-green-bonds-in-asia-12-thought.jpg)

Green and social bonds: what’s at stake for investors? · As the market for green and social...

13

www.mirova.com 1 Green and social bonds: what’s at stake for investors? Written on 29/09/2014 EXECUTIVE SUMMARY As the market for green and social bonds takes off, attracting ever more attention from the financial community and from agents engaged in promoting the development of a more sustainable economy, we intend to revisit some larger questions that this market raises. How far along have we come in the market’s development? What controversies does it provoke? What is valuable about this market and how should we be thinking about its future development? I. Green and social bonds have carved out a place for themselves in the fixed-income market A green or social bond is one that, in addition to its ‘usual’ characteristics (maturity, coupon, etc) is designed to finance projects that offer environmental and/or social benefits. A market experiencing vigorous growth in many directions The year 2013 was full of questions raised by the rising tide of ‘green and social bonds’ or ‘sustainability bonds’. Was the market witnessing an exceptionally good year or the start of a sustained trend? This autumn, as the harvest gets underway, 2014 promises to be an excellent year and appears to confirm that green and social bonds are here to stay, creating a new sub class within fixed income. Indeed, by the end of August 2014, the total issuance for the year was close to USD 20 billion, 1.6 times that of 2013, which was itself more or less a threefold increase compared to the ‘birth’ of this market in 2006. “ The market for green and social bonds has more than tripled in a few short years Obviously, despite this impressive growth, green and social bonds represent only a minute part of all bonds issued at the moment (less than 1% of the bond market). Nonetheless, qualitative indicators beyond this sustained growth encourage us to believe that the trend is likely to continue. Hervé Guez, Director of Responsible Investment Research Emmanuelle Ostiari, SRI analyst Marc Briand, Head of Fixed Income Chris Wigley, Senior Portfolio manager

Transcript of Green and social bonds: what’s at stake for investors? · As the market for green and social...

www.mirova.com

1

Green and social bonds: what’s at stake for investors?

Written on 29/09/2014

EXECUTIVE SUMMARY

As the market for green and social bonds takes off, attracting ever more attention from the financial community and from agents engaged in promoting the development of a mo re sustainable economy, we intend to revisit some l arger questions that this market raises. How far along have we come in the market’s development? What controversies do es it provoke? What is valuable about this market and how should w e be thinking about its future development?

I. Green and social bonds have carved out a place for themselves in the fixed-income market

A green or social bond is one that, in addition to its ‘usual’ characteristics (maturity, coupon, etc) is designed to finance projects that offer environmental and/or social benefits.

A market experiencing vigorous growth in many directions

The year 2013 was full of questions raised by the rising tide of ‘green and social bonds’ or ‘sustainability bonds’. Was the market witnessing an exceptionally good year or the start of a sustained trend? This autumn, as the harvest gets underway, 2014 promises to be an excellent year and appears to confirm that green and social bonds are here to stay, creating a new sub class within fixed income.

Indeed, by the end of August 2014, the total issuance for the year was close to USD 20 billion, 1.6 times that of 2013, which was itself more or less a threefold increase compared to the ‘birth’ of this market in 2006.

“ The market for green and

social bonds has more than tripled in a

few short years

Obviously, despite this impressive growth, green and social bonds represent only a minute part of all bonds issued at the moment (less than 1% of the bond market). Nonetheless, qualitative indicators beyond this sustained growth encourage us to believe that the trend is likely to continue.

Hervé Guez, Director of Responsible Investment Research Emmanuelle Ostiari, SRI analyst

Marc Briand, Head of Fixed Income Chris Wigley, Senior Portfolio manager

www.mirova.com

2

Figure 1. Total number and value of sustainability bond issues greater than USD 200 million, as

at 31 August 2014

Source: Mirova / Natixis Global Market Research, 2014.

First, 2014 was the year that corporate issuers arrived in full force. Whereas the market had previously been completely dominated by supranational organizations, development banks and international agencies, corporate issuances, which first

appeared in 2013, grew from 17% to reach nearly 50% of the global volume of bonds issued at the end of August, 2014.

Figure 2. Distribution of sustainability bonds greater than USD 200 M by issuer type – as at

31 August 2014

Source: Mirova / Natixis Global Market Research, 2014.

Another interesting feature of the market’s growth has been the noticeable increase in social bonds. This remains a narrow market segment, however, the last few months bear witness to a significant inroad made by bond issues with a social impact.

“ While 2014 was a year for

tremendous growth in the green bond

market, there remain several steps if

this success is to continue

It is fair to say that the market for green and social bonds achieved a number of breakthroughs in 2014, however, the chapter is by no means closed, and, beyond increasing volume, there are several steps needed for this market to realize its potential. As we see it, there are four significant challenges ahead: i) ensuring more corporate bonds with a broader variety of ratings (BBB and HY issuers); ii) attracting more North-American and Asian issuers; iii) fostering activity by sovereign issuers, and iv) growing the number of issues by current issuers in order to produce meaningful issuer yield curves.

The market takes shape

The number of new issues remains the most visible indicator for measuring the size and momentum of a bond market. But it is worth remarking on how the market structure is evolving and contributing to a growing sense that green and social bonds are here to stay as an asset class in their own right.

Looking first at the microeconomic level, the number of dedicated structuring and originating teams has increased. In Europe, this market was initially the exclusive realm of teams such as the SEB (Skandinaviska Enskilda Banken) and Crédit Agricole CIB, Merrill Lynch, etc. Today, BNP and HSBC have announced that they will be earmarking resources dedicated to this asset class. Such investments in human resources constitute a particularly strong signal.

Investors, for their part, are also getting organized. In addition to Mirova, which, having been an important early supporter of green bonds in its fixed income funds, recently announced the creation of an open fund devoted to green bonds, Zurich Insurance has also positioned itself as a leading player with two portfolios of €1 billion each in green bonds (the first

consisting of agencies and supranational organizations, and the second corporate bonds).

Well aware of this momentum, service providers are also developing dedicated products and services. Hard on the heels of S&P Dow Jones, MSCI and Barclays have announced the launch of their own Green bond indices. Meanwhile, extra-financial ratings agencies are beginning to offer specialized services to supply second opinions.

The Green Bond Principles (GBP), created with the intention of structuring the market, come on top of these many micro-economic aspects. Since clearly a green bond ought not to be classified as such on the say-so of its issuer, so the market needs a framework if it is to develop over time, and four banks1 jointly published the GBP in January of 2014. Since then, the governance of this initiative has been broadened and strengthened. In terms of reinforcement, it will now come under the aegis of the ICMA (International Capital Markets Association). Its greater breadth takes the form of an executive committee drawn from three groups: banks, issuers and investors, with six members from each. The GBP now stand at 62 members in all, with several institutions (NGOs, service providers) granted the status of “observers.”

Figure 3. Breakdown of GBP members by category

Source: Mirova / ICMA, 2014.

1 Bank of America Merrill Lynch, Citigroup, Crédit Agricole CIB, J.P. Morgan Chase &

Co.

The GBP aim to provide guidelines for what constitute the elements needed before a bond issuance can be considered Green, with the dual goal of helping issuers design their green bonds and assisting investors in evaluating the environmental impact achieved by such bonds.

Rather than precisely defining the environmental impact sought, the GBP focus on the governance criteria a bond needs to use in order meet the definition of a green bond. This framework is structured around:

- The types of credit instruments that can be considered green. In theory, the framework accommodates any type of bond; practically, however, most issuance has involved ‘senior unsecured’ bonds.

- The characteristics of the security, meaning:

1) a description of the use of proceeds that makes

clear, as part of the bond’s legal documentation,

the types of projects eligible for funding,2

2) an evaluation and selection process that applies

to projects meeting the bond’s eligibility criteria

(examination and decision procedures, measures

for determining impact, documentation required

for verifying projects’ eligibility);

3) management of funds, including a dedicated

portfolio or internal audit process for tracking

funds, and an external auditor who confirms the

veracity of the information reported;

4) disclosure, in the form of a dedicated annual

report, of the projects and/or impact produced

consequent to the bond issue, using quantitative

and/or qualitative performance indicators;

- The type of assurances such bonds should offer,

such as an independent expert’s second opinion

regarding criteria for project eligibility and, more

importantly, a third opinion, with this one being from

an independent audit firm.

2 Here, the GBP propose a non-exhaustive list of environmental categories, including

renewable energy, energy efficiency, waste management, sustainable soil

management, protection for biodiversity, clean transport and management of

drinking water.

This framework, designed to provide green bonds with a structure that will guarantee their credibility is supported by all members; however, implementation of these recommendations remains voluntary at this time, and the level of adherence to these guidelines varies considerably, including among GBP member organizations. Common sense suggests that this flexibility is warranted by the embryonic nature of the market, where players may have very different levels of maturity; thus pragmatism advises that we let time do its work, and regularly revise these principles—indeed, a drafting committee, on which Mirova sits, has just been named within the executive board—without doing anything to radically upset the market’s momentum. But beyond the issue of adherence to the principles enumerated above, there are three concerns that remain all but absent from the GBP:

- Defining what green is, and what is green. Here,

given the complexity of the issue and lack of

consensus on the matter, we do not expect much

progress from the GBP in the immediate future.

- What exactly can green bonds fund? Can external

growth be financed using green bonds? Should

issuers operating solely in the domain of renewable

energy be subject to fewer requirements? And so

on…While it is difficult to secure a consensus on such

issues, we believe that the GBP are in a position to

offer guidance.

- Lastly, the desired quality of reporting remains

somewhat hazy, even if outlines have been sketched.

Here again, progress could be made through the

GBP.

“ The credibility of this new

market will depend on its capacity to

reinforce its standards

It is clear to see that the credibility of this new market will depend on its capacity to offer satisfactory responses to these questions. It is equally clear, in light of current debates on the subject, that a broad consensus on these topics is not likely in the immediate future. Nonetheless, we believe that in order for a consensus to appear, debate there must be, and that

participants need to take a stance on these issues, even though this means adjusting their positions as their experience increases and the market evolves; only then can a consensus coalesce around shared principles, ideally taking shape as a label.

II. Mirova’s current position

Concerning these three central questions, namely, how to assess the green qualities of projects, the possible objects of allocation, and the desirable quality of reporting, Mirova offers the following analysis.

A methodology for evaluation consistent with Mirova’s overall approach to measuring the environmental and/or social contribution of an investment

For Mirova, Responsible Investment aims to achieve economic, social and environmental performance by directing savings towards the entities, initiatives, and projects that contribute to sustainable development. We are convinced that extra-financial dimensions constitute a crucial component of any investment strategy that aims to create value.

Consequently, Mirova seeks first and foremost to identify entities or projects designed to seize opportunities associated with the transition of our economy toward a more sustainable society, while ensuring that potential environmental, social and governance (ESG) risks are taken into account.

This philosophy is implemented as a two-tiered ESG evaluation:

1. A review of opportunities designed to determine how well an activity (product service, project etc.) meets the challenges of sustainable development. The level of exposure is calculated in terms of the environmental or social benefits an activity presents in comparison to a business as usual scenario, and is expressed using a four-point scale: ‘high exposure’, ‘significant exposure’, ‘low or no exposure’ and ‘negative exposure’. Negative exposure occurs, for instance, when the nature of the

activity itself represents a significant risk to sustainable development.

2. A review of ESG risks to determine each actor’s responsiveness to the ESG issues raised by the way they do business. This evaluation is made on a three-point scale: ‘Positive’, ‘Neutral’, or ‘Risk’.

Figure 4. Indicative matrix of the elaboration of the Mirova

Sustainability Opinions

Source: Mirova, 2014

This matrix (Figure 4) provides a five-point scale (Figure 5) that

runs from Committed down to Negative and forms the basis for

Mirova’s sustainability opinions.

“ A methodology for evaluation with two distinct levels: one to identify sustainable development opportunities

and another to assess ESG risks

=

Schéma 5. Opinions Développement Durable Mirova

Source : Mirova, 2014

This methodology is applied, with suitable adjustments, for each of the asset classes Mirova manages, including equities, fixed-income securities and infrastructure.

Applied to green bonds, this evaluation framework would ideally analyse the underlying projects, making no exclusions a priori as to issuers, except as concerns those in flagrant violation of the fundamental principles of the Global Compact and OECD’s Guiding Principles.3

In practice, the current levels of documentation for green and social bond issues do indeed allow us to analyse the environmental and/or social benefits of underlying projects using our in-house grid (presented below). However, the information provided at this time does not make it possible for us to judge how the environmental and/or social risks associated with underlying projects are handled. In the absence of data specific to the project, the risk review segment of the analysis will rely on information concerning the issuer’s management of risk.

Thus our evaluation of green and social bonds has two components: on the one hand the anticipated contributions to sustainable development from underlying projects, and on the other a review of ESG risks, primarily those of the issuer.

3 OECD Guidelines for Multinational Enterprises.

Environmental and/or social benefits ensuing from the use of proceeds

Evaluating the environmental and/or social benefits associated with the projects underlying green bonds obviously requires transparency as to the use of funding and clear, verifiable, criteria for determining projects’ eligibility to receive financing.

Once an issuer publishes information about a project, the first task is to review how well its intended goal meets the challenges of sustainable development.

The analysis of a project’s contribution must address the following concerns:

- Which sustainable development issues does the project offer solutions to?

- Will this project have a significant impact on the sustainable development issue it aims to address?

- Does the project really go beyond business as usual practices?

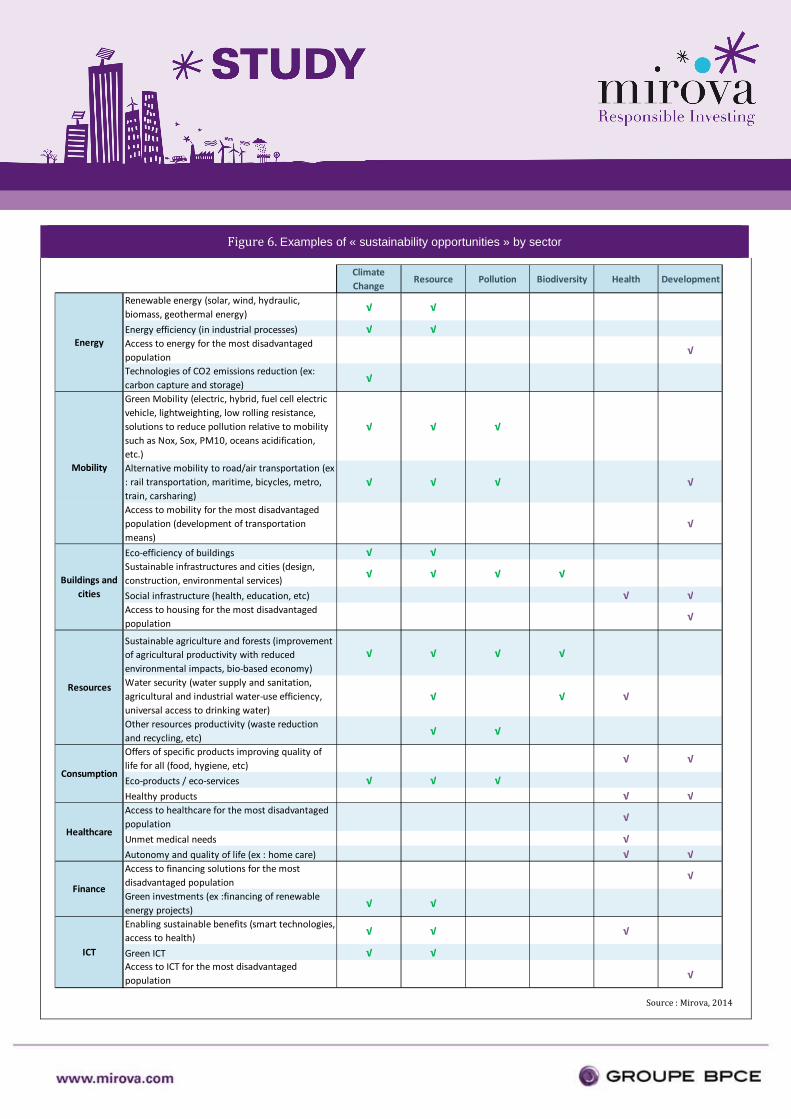

The intent here is to determine to what extent underlying projects offer sustainable development solutions. Mirova’s opportunities grid considers six challenges: climate change, resources, pollution, biodiversity, health, and development. Each project may address one or several of these basic sustainable development challenges.

Figure 6. Examples of « sustainability opportunities » by sector

Source : Mirova, 2014

Climate

ChangeResource Pollution Biodiversity Health Development

Renewable energy (solar, wind, hydraulic,

biomass, geothermal energy)√ √

Energy efficiency (in industrial processes) √ √

Access to energy for the most disadvantaged

population√

Technologies of CO2 emissions reduction (ex:

carbon capture and storage)√

Green Mobility (electric, hybrid, fuel cell electric

vehicle, lightweighting, low rolling resistance,

solutions to reduce pollution relative to mobility

such as Nox, Sox, PM10, oceans acidification,

etc.)

√ √ √

Alternative mobility to road/air transportation (ex

: rail transportation, maritime, bicycles, metro,

train, carsharing)

√ √ √ √

Access to mobility for the most disadvantaged

population (development of transportation

means)

√

Eco-efficiency of buildings √ √

Sustainable infrastructures and cities (design,

construction, environmental services)√ √ √ √

Social infrastructure (health, education, etc) √ √

Access to housing for the most disadvantaged

population√

Sustainable agriculture and forests (improvement

of agricultural productivity with reduced

environmental impacts, bio-based economy)

√ √ √ √

Water security (water supply and sanitation,

agricultural and industrial water-use efficiency,

universal access to drinking water)

√ √ √

Other resources productivity (waste reduction

and recycling, etc)√ √

Offers of specific products improving quality of

life for all (food, hygiene, etc)√ √

Eco-products / eco-services √ √ √

Healthy products √ √

Access to healthcare for the most disadvantaged

population√

Unmet medical needs √

Autonomy and quality of life (ex : home care) √ √

Access to financing solutions for the most

disadvantaged population√

Green investments (ex :financing of renewable

energy projects)√ √

Enabling sustainable benefits (smart technologies,

access to health)√ √ √

Green ICT √ √

Access to ICT for the most disadvantaged

population√

Finance

ICT

Energy

Mobility

Buildings and

cities

Resources

Consumption

Healthcare

8

For each bond, all the projects identified are reviewed in light of these six issues. To be considered a green or social bond, the underlying projects must meet the following conditions:

- Have at least one ‘Significant Exposure’ rating for one of the issues, that is, offer demonstrably improved practices that exceed business as usual, as well as a positive impact in the area under consideration.

- Not exhibit negative exposure to any of the six issues.

We hope to enrich this basic framework for analysis as our knowledge and expertise of the standards and best practices prevailing in each sector progresses. A continuous learning and adjustment process is crucial if this new financial vehicle is to establish credibility as having genuine environmental and social value.

Green bonds have ESG risks too!

Every project, every activity, however beneficial it may be with respect to the challenges of sustainable development, carries with it negative social and environmental externalities that vary over the course of its life cycle (supply chain, development, construction, operations, end-of-life). As we see it, responsible investors should be taking these risks into account.

Where green and social bonds are concerned, current documentation practices, unlike those prevailing in the area of infrastructure finance, do not make it possible to determine as precisely how environmental and social risks associated with underlying projects are handled.

For lack of this information, we rely on available data on the issuer’s handling of these risks. On the assumption that if an issuer is responsible about controlling for potentially negative social and environmental externalities in its activities overall, there is a strong chance that the projects underlying its green bond will be at least as well managed as the balance of its activities.

Nonetheless, some best practices stand out. We could point to the EDF’s green bond, which finances only projects that respect a specific set of criteria established by Vigeo in order to guarantee the responsible management of projects. These include taking into account health and security issues affecting employees, management of relationships with suppliers. In this way, beyond the intent of the underlying projects (renewable energy), which contribute to the energy transition, the issuer provides investors with assurances that social and environmental externalities are taken into account. However, this level of detail remains a rarity for the moment.

Also, there remains, beyond concerns regarding how environmentally or socially beneficial a project is, the question of what kind of projects may be financed.

Use of proceeds

From investor’s point of view, the function of this market is to provide an opportunity to contribute to the ecological transition, by providing the capital necessary to the development of business models offering social or environmental benefits. Such rational altruism seeks to ensure that our model of development becomes sustainable by transforming its core, convinced that this is the only way to guarantee long term returns and, thus, to stabilize long term liabilities.

From this perspective, there is, beyond the ‘green’ or ‘social’ quality of the underlying project, an additional question, which is the nature of the project; and this, it seems, presents itself in somewhat different terms for a creditor than it would for an equity holder.

When one purchases shares in a business concern, it requires one to take a global approach to social and environmental analysis. After all, one becomes the owner of indivisible portions of the company and responsible for both its assets and its liabilities. A creditor is often in a somewhat different position. When an issuer uses the market to raise debt capital for ‘general corporate purposes’ its creditors are in the same position as shareholders: there is no alternative but to consider the environmental and social qualities of the issuer in their entirety. Such an approach inevitably results in placing off-limits certain companies present in the equities and bond markets. Regardless of the methodology employed assessment is inevitably based on comparison, and almost every SRI approach entails some exclusion, whether this is done ex ante or ex post, on a sector basis or based on normative criteria. The great strength of the green bond concept is to tie investment to specific underlying projects. Thus, no company is left out in the cold, as long as it has a viable project for transformation to offer the market. The counterpart to this inclusiveness is a stringent demand for clarity as to the use of proceeds to finance investments that induce the promised transformation. And, as we know, capital markets are quite simply organized to ensure that debt instruments are as fungible as possible. Green and social bonds are at odds with this attitude, since their function is to bind together financing and investment. One might summarize the rational of this market as follows: using green debt to finance green or social assets. The corollary of this principle is that there cannot be more green or social bonds than there are

9

green or social assets on the issuer’s balance sheet, meaning that such bonds may not be used to cover operational losses, share buybacks, or to refinance existing debt, even if such losses, shares or debt were to belong to green or social companies.

“ The great strength of the

green bond concept is to tie

investment to specific underlying

projects.

The most controversial issue is probably the possible financing of ‘green goodwill’ using ‘green debt’. For instance, is it acceptable to use green bonds to finance the acquisition of a renewable energy manufacturer? Issuers are tempted to answer in the affirmative. From their point of view, a euro, whether allocated to organic or external growth, involves much the same process: what difference is there between investing in the construction of a wind farm and buying one that’s already built? Only the question of financial profitability, based on a firm’s internal technical competencies will determine the best choice. However, it is perfectly clear that for society at large the difference is considerable. In the one case new capacity is created, while in the other, there is simply a change in capital ownership. In one case it is possible to objectively identify gains compared to a reference scenario, while in the other there is no change in the scenario underway. For this reason we do not believe that green debt should be used to back green goodwill. This does not close all doors to the possibility of refinancing green assets as part of external growth: however, only unamortized green assets can be backed by green debt, not goodwill, which is merely a financial return collected by the original capital investors, and not a new investment. One might object that the acquisition price in fact reflects the new value of these assets, and therefore goodwill should be eligible for refinancing under principles that combine backing green assets and debt. To this, we respond that i) from a theoretical perspective, goodwill is a residual ensuing from an acquisition, thus cannot be attributed to an asset ex ante, and ii) in practical terms there has been no end to the number of cases in which goodwill has suffered accelerated or sudden impairment because it failed to demonstrate ex-post justification.

This consideration of asset/debt relations is also interesting insofar as it applies also to the financing of green or social debt that can be securitized. While practically non-existent at this juncture, we expect a bright future for this market in the coming years.

Financing the ecological transition also means financing the investments of consumers, especially assets like homes and vehicles, which are often the leading items of both their household budgets and carbon footprints! Consequently, there is every reason to expect financial solutions, such as mechanisms to refinance debt associated with energy-efficient renovations, a major environmental concern if ever there was one.

Clarity of the dedicated reporting scheme

Even the greatest mastery of these elements, from the quality of environmental or social components, to the traceability of projects’ funding, is to no avail if lacking a high degree of transparency and gestures of commitment on the part of issuers, and this at several levels.

- Eligibility criteria: transparency as to the evaluation of

projects’ environmental and/or social quality, consultation

with independent experts and third party assurance of

veracity.

- Traceability as to use of proceeds

- Reporting on outcomes:

• regular updates (at least annual) on the projects

actually financed with proceeds, including the

capital allocated to each;

• qualitative and quantitative performance indicators

for measuring the real impact of investments with

respect to sustainable development goals (for

instance, tonnes of CO2 avoided by a green bond,

number of individuals gaining access to a health

service for a social bond etc.), and

• third party assessment confirming the veracity of

information provided.

To take an example, Nordic Investment Bank (NIB) publishes a

complete list of each and every project financed through its

green bonds, and updates this inventory every time a project is

added. Information provided includes the goal of the project, its

10

duration and the companies participating. A separate list tracks

the CO2 emissions avoided yearly thanks to these bond issues.

This level of transparency concerning project funding, which

still rare today, is essential for maintaining the value-added of

sustainability bonds for investors, which resides in the

measure of impact that they offer.

Each of these elements contributes to the establishment of a

credible market, and is thus championed by Mirova in all our

exchanges with issuers, although they are not qualifying

features per se in our analysis process at this time. This is a

requirement whose stringency will evolve alongside our

experience and observation of best practices.

These requirements are not, in fact cumulative, and are

assessed globally. We recognize that reporting elements of

this type can be onerous and time consuming to set up for

issuers. In order to lighten this load to a strict minimum at

issue, we encourage companies to move toward an integrated

reporting model (cf. the Integrated Reporting Initiative, to which

Mirova is also deeply committed). Such a model would make it

possible to fairly easily provide, as an appendix to the report, a

detailed description of green or social assets and liabilities. If

issuers committed to ensuring that such liabilities do not

exceed assets, investors would doubtlessly be significantly

less demanding concerning segregated accounting, second

opinions and ex ante descriptions of projects, as secure in their

certitude that all significant information would be available ex

post as part of the audited and certified annual report.

III. What makes this market attractive?

To be sure, contributing to a more sustainable economy ought to be a sufficient goal in and of itself. After all, without a sustainable economy we are constantly facing the risk of a Collapse, to borrow the title of Jared Diamond’s work, which would, de facto, result in severe losses for all economic agents. By investing in and for a sustainable economy we help to ensure long term prosperity for all, something that ought to be worth a few short-term opportunity costs by way of a trade-off. Absolutely. However, we believe that the outcome of this short versus long-term cost/benefit calculation can and should be reinforced by creating a market infrastructure based on a win-win approach. This is possible because the economy is not a zero-sum game (even, or rather especially, when the time

dimension comes into play), which is just as well, because however mistaken and dangerous it is to design a market theory based entirely on greed, it is delusional, and likely just as dangerous, to try an found it on altruism alone. Human nature being what it is, it is better to design incentives that attempt to reconcile and overcome our contradictory tendencies, rather than ignore them.

But before we come back to the mechanisms that might allow us to resolve these contractions, let us consider what interests this market holds for its two principal participants: issuers and investors.

The market’s appeal from an investor standpoint

To date, the green and social bond market seems to offer nothing but upside from an investor perspective. Issuers have more or less entirely abandoned the idea of structured products with variable coupons contingent on environmental or social goals, and have largely floated ‘vanilla’ instruments on the market. Returns are determined by the overall credit rating of the issuer. Thus investors receive the same rate of return, for a given issuer, whether the bond is green or social or neither. This explains why these issues have met with such great success; outside the space of SRI investors, conventional investors also subscribe on the basis of ordinary risk/return calculations. While especially high levels of demand at issuance can sometimes create a slightly less attractive spread than traditional bonds exhibit, its effect is generally minimal, with little impact on their overall yield.

Thus we are currently witnessing the development of a market that offers investors environmental and social benefits without sacrificing financial returns.

To an issuer-by-issuer analysis, it is worthwhile to add an overview of the market as a whole. The underlying question remains: ‘if, as an investor, I allocate part of my holdings to this new asset class consisting of green and social bonds, what is likely to change about the overall return I can expect from the bond markets?’

The following snapshot, which we offer here in response to this question, dates from 15 September, and is presented by way of example only. In addition to changes in general market conditions, we have already made clear that the market for sustainability bonds is rapidly evolving, and that we should expect the snapshot we might take a year from now to look extremely different.

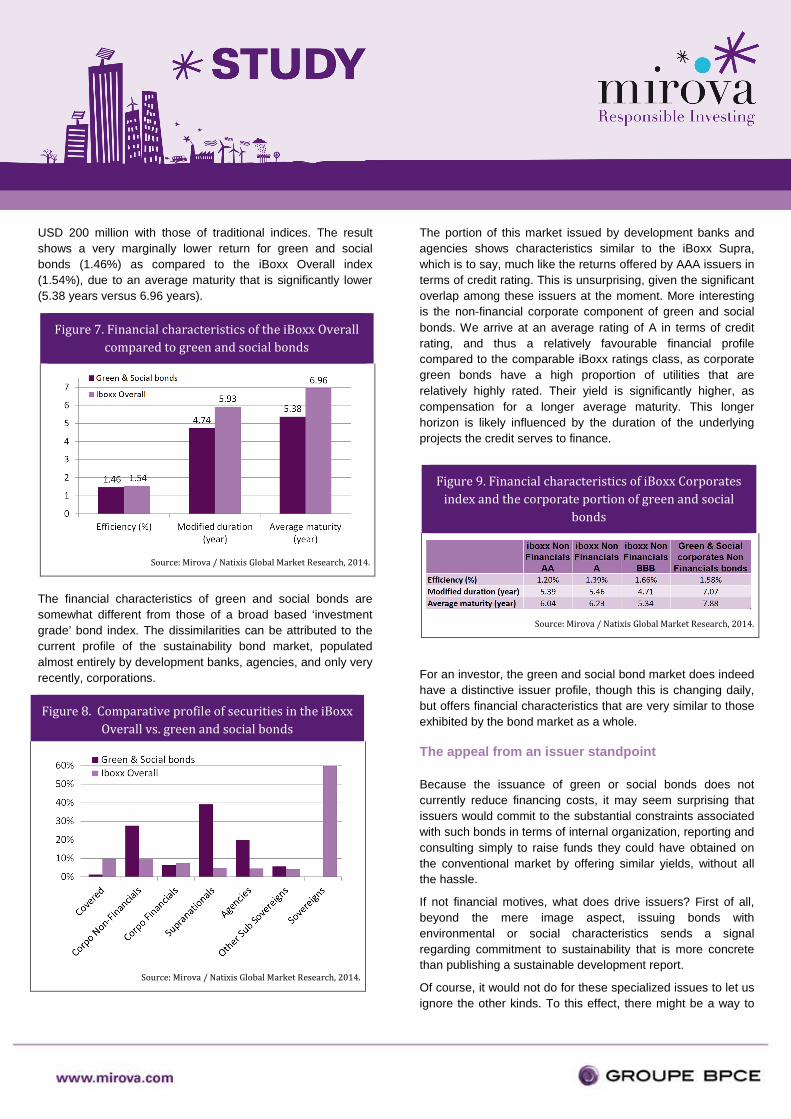

These precautionary statements notwithstanding, it is interesting to compare the financial characteristics of the current supply of green and social bond issues greater than

11

USD 200 million with those of traditional indices. The result shows a very marginally lower return for green and social bonds (1.46%) as compared to the iBoxx Overall index (1.54%), due to an average maturity that is significantly lower (5.38 years versus 6.96 years).

The financial characteristics of green and social bonds are somewhat different from those of a broad based ‘investment grade’ bond index. The dissimilarities can be attributed to the current profile of the sustainability bond market, populated almost entirely by development banks, agencies, and only very recently, corporations.

The portion of this market issued by development banks and agencies shows characteristics similar to the iBoxx Supra, which is to say, much like the returns offered by AAA issuers in terms of credit rating. This is unsurprising, given the significant overlap among these issuers at the moment. More interesting is the non-financial corporate component of green and social bonds. We arrive at an average rating of A in terms of credit rating, and thus a relatively favourable financial profile compared to the comparable iBoxx ratings class, as corporate green bonds have a high proportion of utilities that are relatively highly rated. Their yield is significantly higher, as compensation for a longer average maturity. This longer horizon is likely influenced by the duration of the underlying projects the credit serves to finance.

For an investor, the green and social bond market does indeed have a distinctive issuer profile, though this is changing daily, but offers financial characteristics that are very similar to those exhibited by the bond market as a whole.

The appeal from an issuer standpoint

Because the issuance of green or social bonds does not currently reduce financing costs, it may seem surprising that issuers would commit to the substantial constraints associated with such bonds in terms of internal organization, reporting and consulting simply to raise funds they could have obtained on the conventional market by offering similar yields, without all the hassle.

If not financial motives, what does drive issuers? First of all, beyond the mere image aspect, issuing bonds with environmental or social characteristics sends a signal regarding commitment to sustainability that is more concrete than publishing a sustainable development report.

Of course, it would not do for these specialized issues to let us ignore the other kinds. To this effect, there might be a way to

Figure 7. Financial characteristics of the iBoxx Overall

compared to green and social bonds

Source: Mirova / Natixis Global Market Research, 2014.

Figure 8. Comparative profile of securities in the iBoxx

Overall vs. green and social bonds

Source: Mirova / Natixis Global Market Research, 2014.

Figure 9. Financial characteristics of iBoxx Corporates

index and the corporate portion of green and social

bonds

Source: Mirova / Natixis Global Market Research, 2014.

12

encourage development banks to adopt a methodology whereby they only issue sustainability bonds, which would be consistent with their mission.

The second motive, while not strictly financial, involves a calculated effort on the part of issuers not to cut themselves off from certain investors. SRI investors employ environmental and social standards, and thus sustainability bonds are a way of attracting investment to fund specific projects that a company would not have been eligible for with a general corporate purpose issue.

Thus, while certain investors do not wish to finance nuclear power or fossil fuels, issuers with a presence in these sectors may still be able to reach out to them by offering such investors an opportunity to finance only the company’s development of renewable energy.

Some observers have criticised green bonds for this very reason, saying they might become a means for certain players to secure SRI financing that they would otherwise not be eligible for. We disagree. First of all, the reasoning doesn’t apply to equity funds, for which project finance is irrelevant. Secondly, because if green and social bonds work for these issuers as for any other, this will eventually translate in the market as a difference in financing costs. Capital that can be raised from the entire pool of investors becomes less costly than financing that can draw on only a subset of them. If so, the market will have accomplished its fundamental role: it will assign a price (indirectly and not directly as does a Carbon Exchange) to social and environmental benefits. By reducing the cost of financing green and social projects, this process will lower the profitability required of them as compared to other types, thereby contributing to the development of a sustainable economy. Rather than fret about possible negative effects, socially responsible investors should be doing everything they can to support the healthy development of this market; the more it grows, the greater its positive impact on the financing costs for projects of social and environmental benefit will be.

Moving towards a win-win situation

To place issuers and investors head to head is to invite a confrontation between contradictory attitudes. Issuers are hoping for their green or social projects to be financed at a lesser cost than other kinds, whereas investors are looking to hold out for comparable returns. Meanwhile, investors make considerable demands in terms of reporting in order to forestall the risk of weak issuance through due diligence procedures. The most demanding among them ask issuers to quantify,

where possible, the social and/or environmental benefits resulting from the underlying projects. Issuers, on the other hand, may be reluctant to incur large additional reporting costs.

True, the market appears to have found an equilibrium point at the moment: brand image benefits for both parties, financing costs that are identical or even slightly lower, along with reporting costs that are manageable for issuers, while investors receive yields around those of conventional bonds. This equilibrium makes us comfortable assuming that the market will continue to grow. However, it is not impossible that this growth may produce large spreads when green or social bonds are issued, or that the bond curve may come to favour issuers of this type of bond.

We are by no means there yet. But it is possible, right now, to design a market infrastructure that would allow us to overcome this easily anticipated obstacle and accelerate the market’s development. Since, green and social bonds contribute to the general interest by reducing systemic risks such as climate change, it seems appropriate that regulations, notably the Solvency Directive, move to treat them more favourably. By aligning the interests of society, those of corporations developing green or social projects, and those of socially responsible investors, new regulatory mechanisms would help to create a market infrastructure strongly tipped in favour of green and social bonds, and thus toward a multiplications of the investments they finance. Of course, such a programme cannot be envisaged without significant strengthening of market standards for the evaluation of environmental and social benefits; this could ultimately lead to a recognized label.

Is there a need for investments in transformation? Are there financing issues at hand? If established on firm footing, the green and social bond market can become an essential tool for financing the energy transition; and for this reason we predict that both its future and our own look brighter every day.

13

DISCLAIMER .

This information purpose only document is a non-contractual document intended only for professional/not-professional clients in accordance with MIFID. It may not be used for any purpose other than that for which it was conceived and may not be copied, distributed or communicated to third parties, in part or in whole, without the prior written consent of Mirova. No information contained in this document may be interpreted as being contractual in any way. This document has been produced purely for informational purposes. Mirova reserves the right to modify any information contained in this document at any time without notice. This document consists of a presentation created and prepared by Mirova based on sources it considers to be reliable. However, Mirova does not guarantee the accuracy, adequacy or completeness of information obtained from external sources included in this document. These simulations/assumptions are made/indicated for example, they do not constitute an undertaking from Mirova and Mirova does not assume any responsibility for such simulations/assumptions. Figures contained in this document refer to previous years. Past performance and simulations of past and future performances are not a reliable indicator and therefore do not anticipate future results. Reference to a ranking and/or a price does not indicate the future performance of the strategy or the fund manager. Under Mirova’s social responsibility policy, and in accordance with the treaties signed by the French government, the funds directly managed by Mirova do not invest in any company that manufactures sells or stocks anti-personnel mines and cluster bombs. Additional notes: Where required by local regulation, this material is provided only by written request. • In the EU (ex UK) Distributed by NGAM S.A., a Luxembourg management company authorized by the CSSF, or one of its branch offices. NGAM S.A., 2, rue Jean Monnet, L-2180 Luxembourg, Grand Duchy of Luxembourg. • In the UK Provided and approved for use by NGAM UK Limited, which is authorized and regulated by the Financial Conduct Authority. • In Switzerland Provided by NGAM, Switzerland Sàrl. • In and from the DIFC Distributed in and from the DIFC financial district to Professional Clients only by NGAM Middle East, a branch of NGAM UK Limited, which is regulated by the DFSA. Office 603 – Level 6, Currency House Tower 2, P.O. Box 118257, DIFC, Dubai, United Arab Emirates. • In Singapore Provided by NGAM Singapore (name registration no. 5310272FD), a division of Absolute Asia Asset Management Limited, to Institutional Investors and Accredited Investors for information only. Absolute Asia Asset Management Limited is authorized

by the Monetary Authority of Singapore (Company registration No.199801044D) and holds a Capital Markets Services License to provide investment management services in Singapore. Registered office: 10 Collyer Quay, #14-07/08 Ocean Financial Centre. Singapore 049315. R.O.C., license number 2012 FSC SICE No. 039, Tel. +886 2 2784 5777. • In Japan Provided by Natixis Asset Management Japan Co., Registration No.: Director-General of the Kanto Local Financial Bureau (kinsho) No. 425. Content of Business: The Company conducts discretionary asset management business and investment advisory and agency business as a Financial Instruments Business Operator. Registered address: 2-2-3 Uchisaiwaicho, Chiyoda-ku, Tokyo.

The above referenced entities are business development units of Natixis Global Asset Management, the holding company of a diverse line-up of specialised investment management and distribution entities worldwide. Although Natixis Global Asset Management believes the information provided in this material to be reliable, it does not guarantee the accuracy, adequacy or completeness of such information.

Mirova. Responsible Investing MIROVA Mirova is a subsidiary of Natixis Asset Management Limited liability company - Share capital € 7 461 327, 50 Regulated by AMF under n°GP 02-014 RCS Paris n°394 648 216 Registered Office: 21 quai d’Austerlitz - 75 013 Paris NATIXIS ASSET MANAGEMENT Limited Company - Share Capital: €50 434 604,76 Regulated by AMF: GP 90-009 RCS Paris n°329 450 738 Registered Office: 21 quai d’Austerlitz - 75634 Paris