Greece’s Debt Crisis Alan (51583329) Brain (51544666) Colman (51694712 ) Tang Chi Ming (50545419)

51

Greece’s Debt Crisis Alan (51583329) Brain (51544666) Colman (51694712) Tang Chi Ming (50545419)

-

Upload

homer-gregory -

Category

Documents

-

view

215 -

download

2

Transcript of Greece’s Debt Crisis Alan (51583329) Brain (51544666) Colman (51694712 ) Tang Chi Ming (50545419)

Greece’s Debt CrisisAlan (51583329)

Brain (51544666)

Colman (51694712)

Tang Chi Ming (50545419)

Contents

Story of Greece Debt Crisis Background Timeline EU / IMF Rescue Plan Current Status

Discussion Interest / Currency Swap Lesson Learned / Take Home

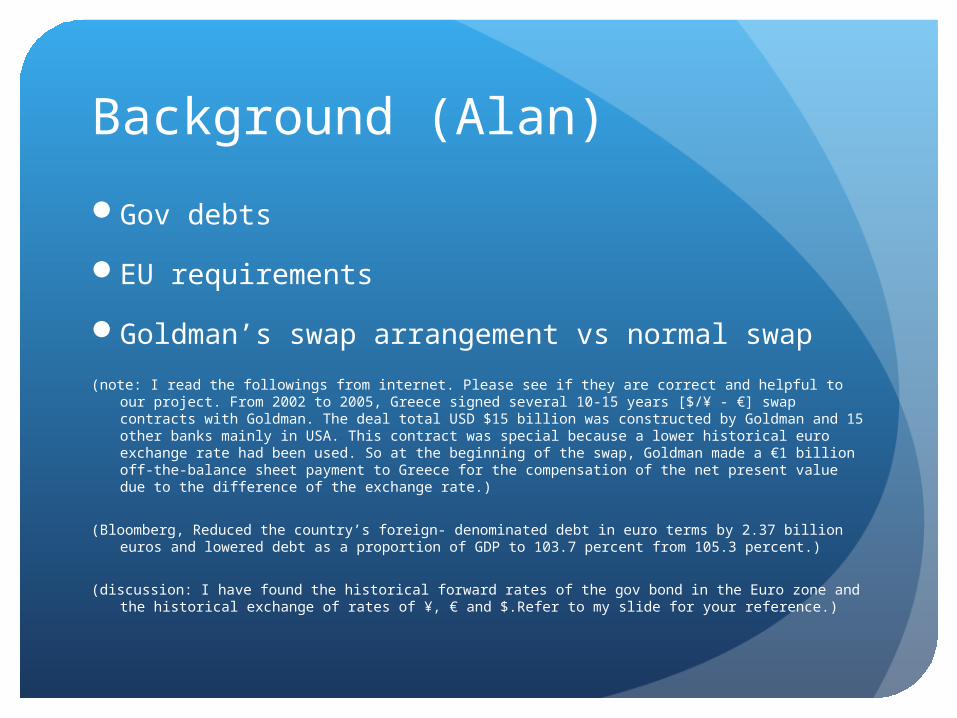

Background (Alan)

Gov debts

EU requirements

Goldman’s swap arrangement vs normal swap

(note: I read the followings from internet. Please see if they are correct and helpful to our project. From 2002 to 2005, Greece signed several 10-15 years [$/¥ - €] swap contracts with Goldman. The deal total USD $15 billion was constructed by Goldman and 15 other banks mainly in USA. This contract was special because a lower historical euro exchange rate had been used. So at the beginning of the swap, Goldman made a €1 billion off-the-balance sheet payment to Greece for the compensation of the net present value due to the difference of the exchange rate.)

(Bloomberg, Reduced the country’s foreign- denominated debt in euro terms by 2.37 billion euros and lowered debt as a proportion of GDP to 103.7 percent from 105.3 percent.)

(discussion: I have found the historical forward rates of the gov bond in the Euro zone and the historical exchange of rates of ¥, € and $.Refer to my slide for your reference.)

Background -

Global financial crisis in fall 2008Greece’s government borrowed heavily

from abroad to fund substantial government budget and current account deficits

Outbreak of crisis -

Between 2000 and 2002, its deficit average 3.8% of GDP

In 2009, its nearly doubling the existing estimate of 6.7% of GDP to 12.7% of GDP

Attempted to obscure debt levels through complex financial instruments

Greek 10-year bond yields were surged to 400 basis points in January 2010

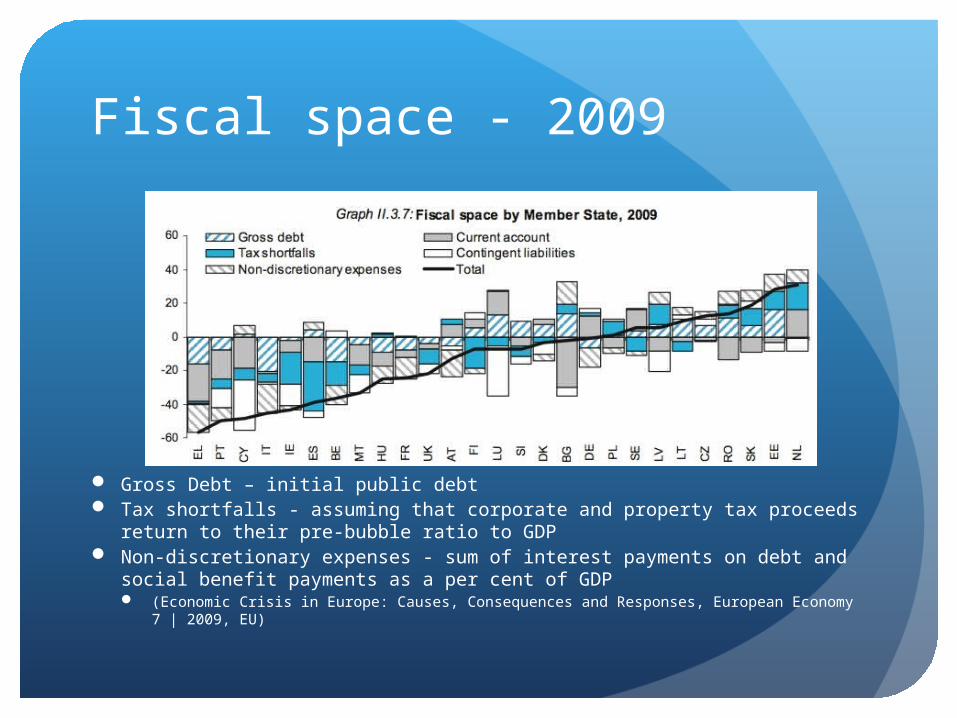

Fiscal space - 2009

Gross Debt – initial public debt Tax shortfalls - assuming that corporate and property tax proceeds return to their pre-

bubble ratio to GDP Non-discretionary expenses - sum of interest payments on debt and social benefit

payments as a per cent of GDP (Economic Crisis in Europe: Causes, Consequences and Responses, European Economy 7 | 2009, EU)

Possible cause of Greece’s crisis -

Mix of domestic and international factorsDomestic-

High government spending Structural rigidities Tax evasion Corruption

International- Adoption of euro as its national currency Lax enforcement of European Union (EU) rules

European Union (EU) requirement-

Buget deficit ceilings of 3% of GDPExternal debt ceilings of 60% of GDP25 out of 27 EU member states were exceed

these limits

Eurozone finance ministers and IMF agreed a 3 years loan program

Totaling €110 billion provided by Eurozone (€80 billion) and IMF(€30 billion)

Eurozone provide a bilateral loan at a market-based interest rate

IMF disburse the loan in tranches if Greece fulfill the reformation of economy policy

Eurozone and IMF Assistance -

Greece’s Policy reform - Implement a several packages of fiscal austerity

measures Deficit down from 13.6% of GDP in 2009 to below 3% by

2014 Deep cuts to public spending Enhanced revenue growth via tax increase Cracked down on tax and social security contribution

evasion

Goldman Sachs’s currency swap-

Arrange a special kind of cross currency swaps with frictional exchange rates

Issued 10 billion of debt in yen, dollar or Swiss francs1 billion in an up-front payment from Goldman to

GreeceDisguised its debt legally through swaps

Greece – Goldman’s Swaps

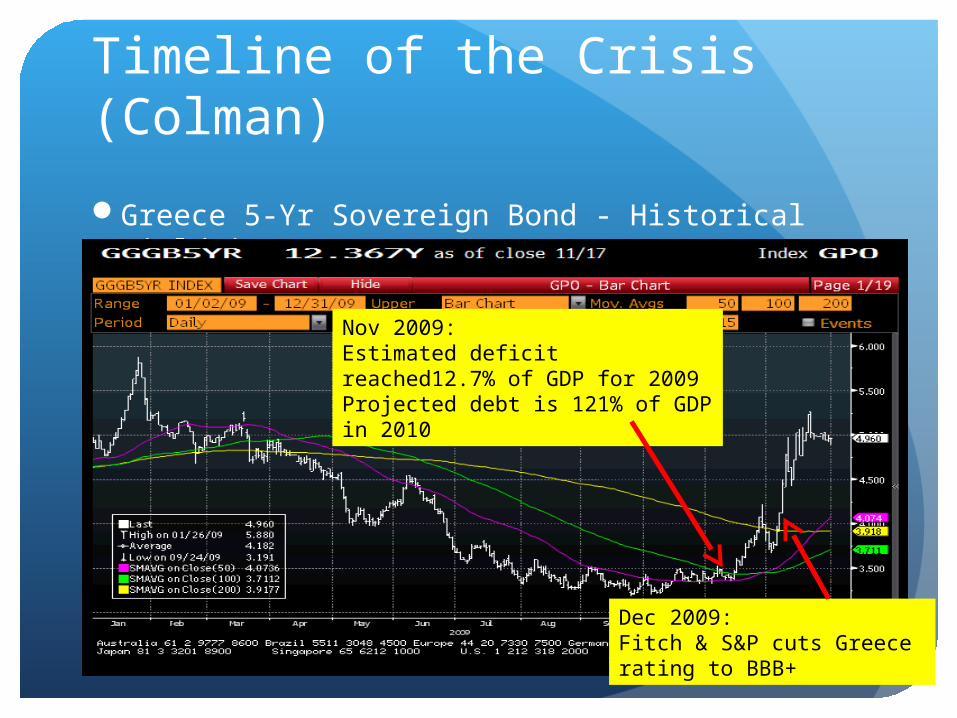

Timeline of the Crisis (Colman)

Greece 5-Yr Sovereign Bond - Historical Yield in 2009

Historical YieldNov 2009:Estimated deficit reached12.7% of GDP for 2009Projected debt is 121% of GDP in 2010

Dec 2009:Fitch & S&P cuts Greece rating to BBB+

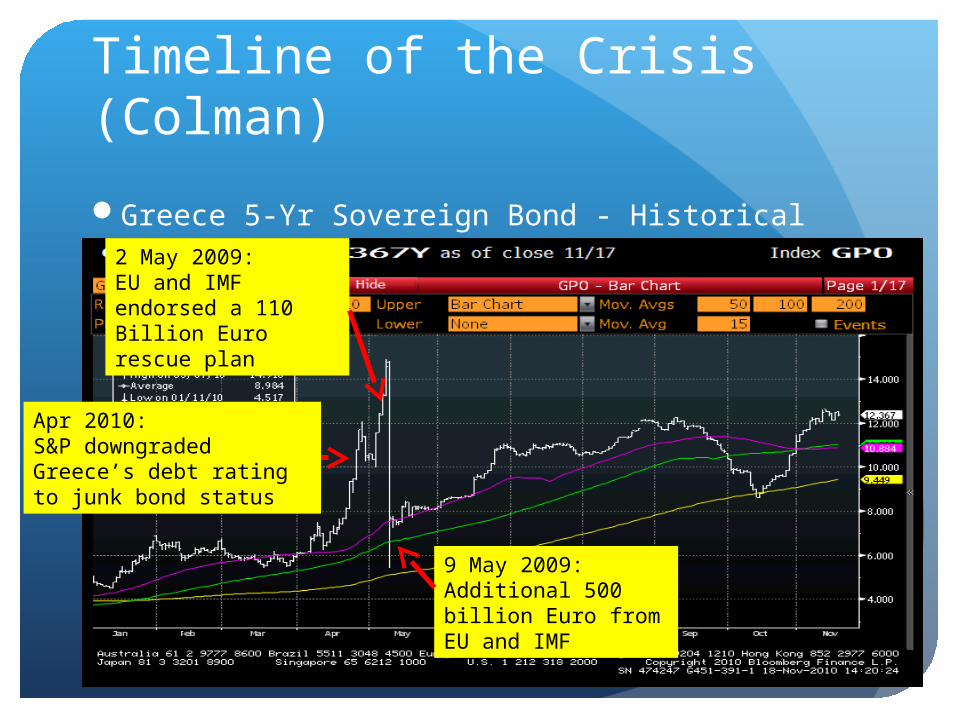

Timeline of the Crisis (Colman)

Greece 5-Yr Sovereign Bond - Historical Yield in 2010

Apr 2010:S&P downgraded Greece’s debt rating to junk bond status

2 May 2009:EU and IMF endorsed a 110 Billion Euro rescue plan

9 May 2009:Additional 500 billion Euro from EU and IMF

Timeline of the Crisis (Colman)

Bond rates / Yields changes

Things done before the rescue plan

(note: I read the followings from internet. Please see if they are correct and helpful to our project. In Jan, Greece issued €8 billion 10-yr gov bond at 7.2% (396 basis point higher than the German gov bond). In Feb, CDS hedging (318+ basis point than normal). In Mar, €6.8 billion 5-yr gov bond at 6.3%. The same month, strike began to see in the country. In April, €10 billion, 10-yr gov bond at 7.1% (400+ basis point higher than Germany’s. S&P downgraded Greece from BBB+ to BB+. EU together with IMF started the rescue plan in April and May. In July, €1.5 billion gov bond at 4.04%.)

(discussion: I have found the historical 10-yr Greek gov bond’s yield. Refer to my slide for your reference. In terms of the structure of the swap (i.e. cash flow, interest rate, etc) and liquidity, what options did Greece has done or considered.)

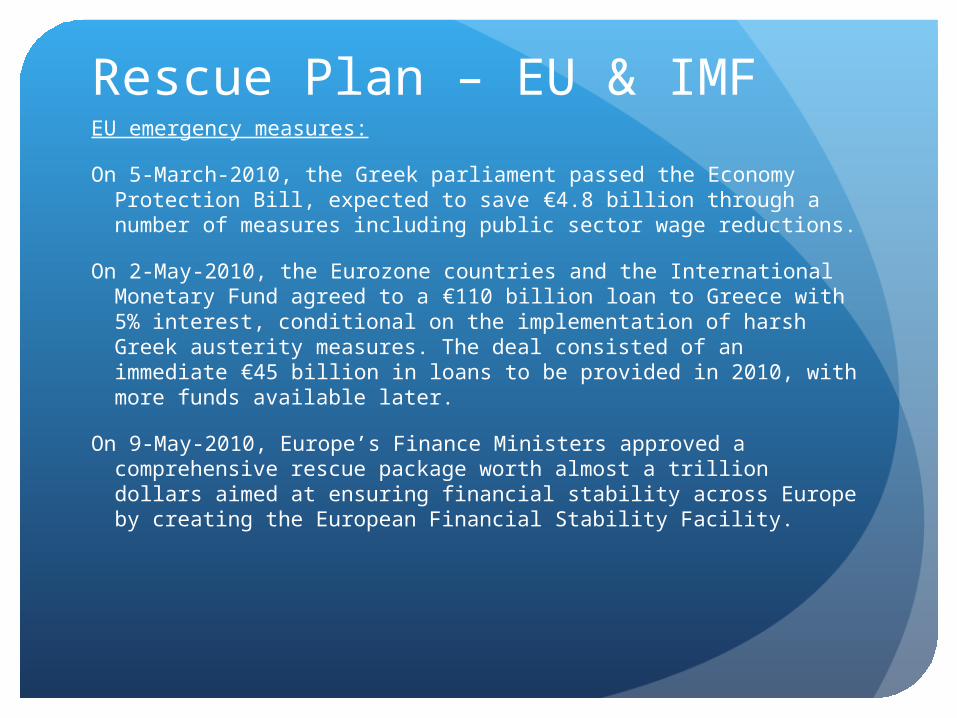

Rescue Plan – EU & IMFEU emergency measures:

On 5-March-2010, the Greek parliament passed the Economy Protection Bill, expected to save €4.8 billion through a number of measures including public sector wage reductions.

On 2-May-2010, the Eurozone countries and the International Monetary Fund agreed to a €110 billion loan to Greece with 5% interest, conditional on the implementation of harsh Greek austerity measures. The deal consisted of an immediate €45 billion in loans to be provided in 2010, with more funds available later.

On 9-May-2010, Europe’s Finance Ministers approved a comprehensive rescue package worth almost a trillion dollars aimed at ensuring financial stability across Europe by creating the European Financial Stability Facility.

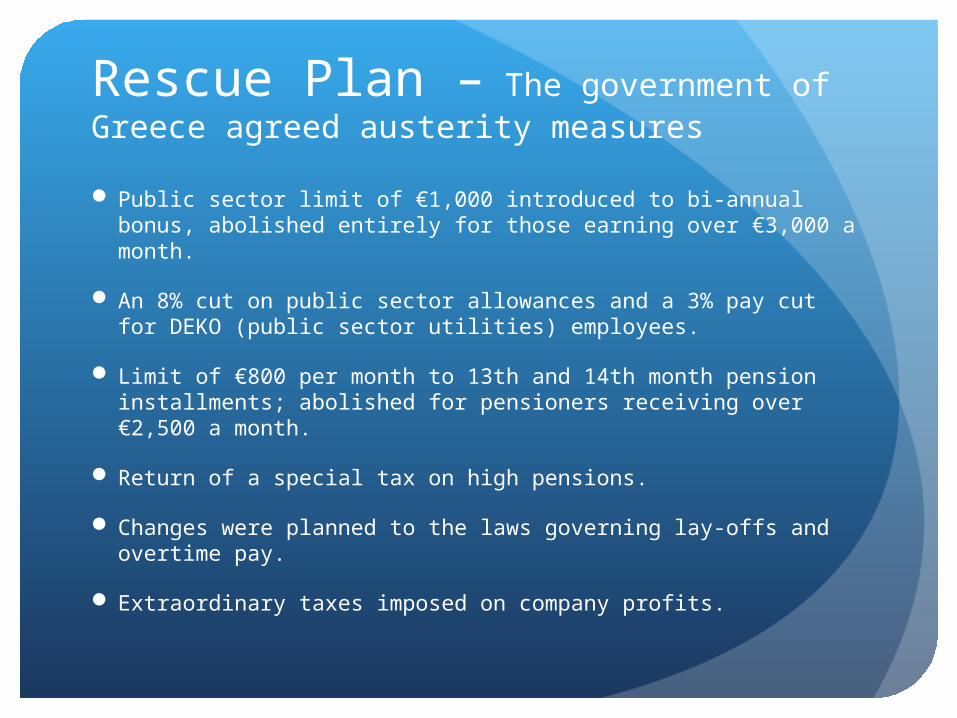

Rescue Plan – The government of Greece agreed austerity measures

Public sector limit of €1,000 introduced to bi-annual bonus, abolished entirely for those earning over €3,000 a month.

An 8% cut on public sector allowances and a 3% pay cut for DEKO (public sector utilities) employees.

Limit of €800 per month to 13th and 14th month pension installments; abolished for pensioners receiving over €2,500 a month.

Return of a special tax on high pensions.

Changes were planned to the laws governing lay-offs and overtime pay.

Extraordinary taxes imposed on company profits.

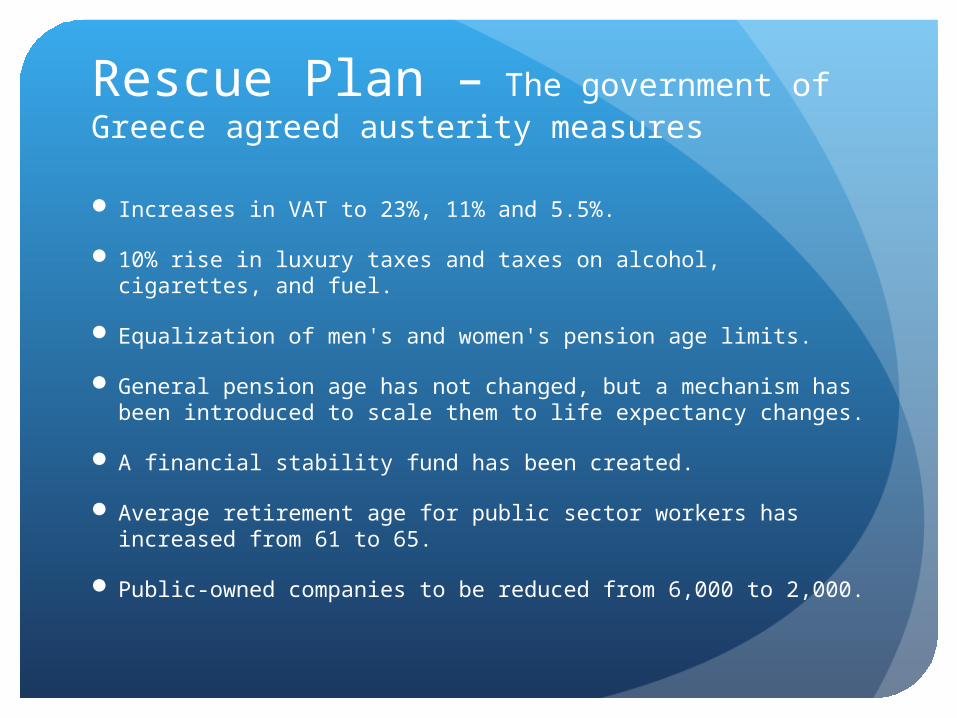

Rescue Plan – The government of Greece agreed austerity measures

Increases in VAT to 23%, 11% and 5.5%.

10% rise in luxury taxes and taxes on alcohol, cigarettes, and fuel.

Equalization of men's and women's pension age limits.

General pension age has not changed, but a mechanism has been introduced to scale them to life expectancy changes.

A financial stability fund has been created.

Average retirement age for public sector workers has increased from 61 to 65.

Public-owned companies to be reduced from 6,000 to 2,000.

Rescue Plan – EU & IMF

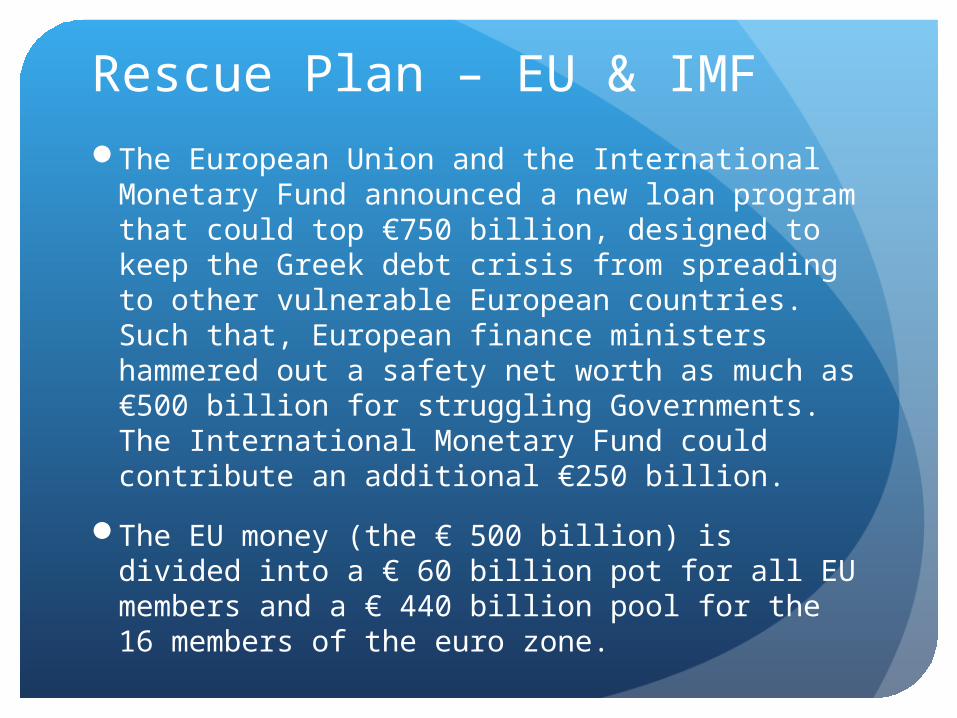

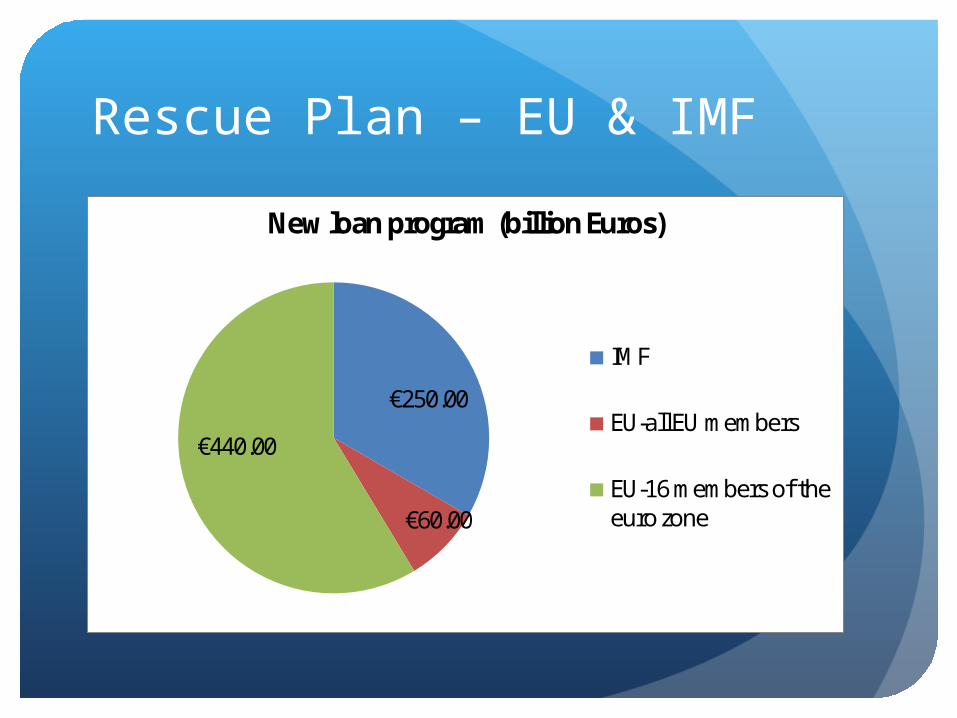

The European Union and the International Monetary Fund announced a new loan program that could top €750 billion, designed to keep the Greek debt crisis from spreading to other vulnerable European countries. Such that, European finance ministers hammered out a safety net worth as much as €500 billion for struggling Governments. The International Monetary Fund could contribute an additional €250 billion.

The EU money (the € 500 billion) is divided into a € 60 billion pot for all EU members and a € 440 billion pool for the 16 members of the euro zone.

Rescue Plan – EU & IMF

€250.00

€60.00

€440.00

New loan program (billion Euros)

IMF

EU-all EU members

EU-16 members of the euro zone

Rescue Plan – EU & IMF

The guarantees for the 60 billion euros are shared by all EU members.

The guarantees for the 440 billion euros are divided between euro zone countries on the basis of their holdings of capital in the ECB, as is the case with the multilateral bailout package extended to Greece.

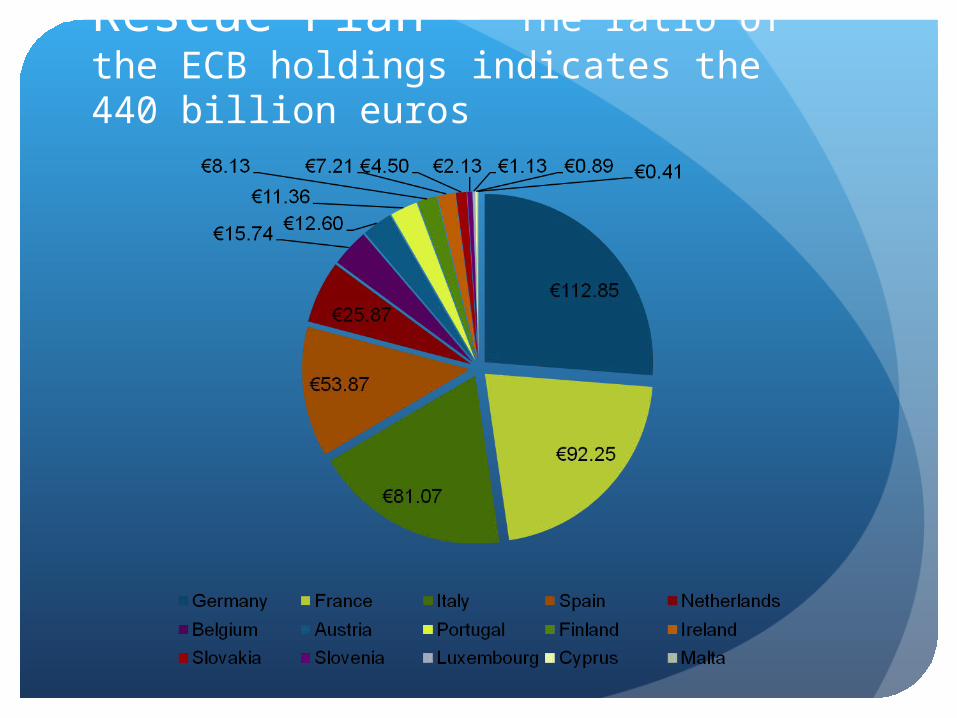

Rescue Plan – The ratio of the ECB holdings indicates the 440 billion euros

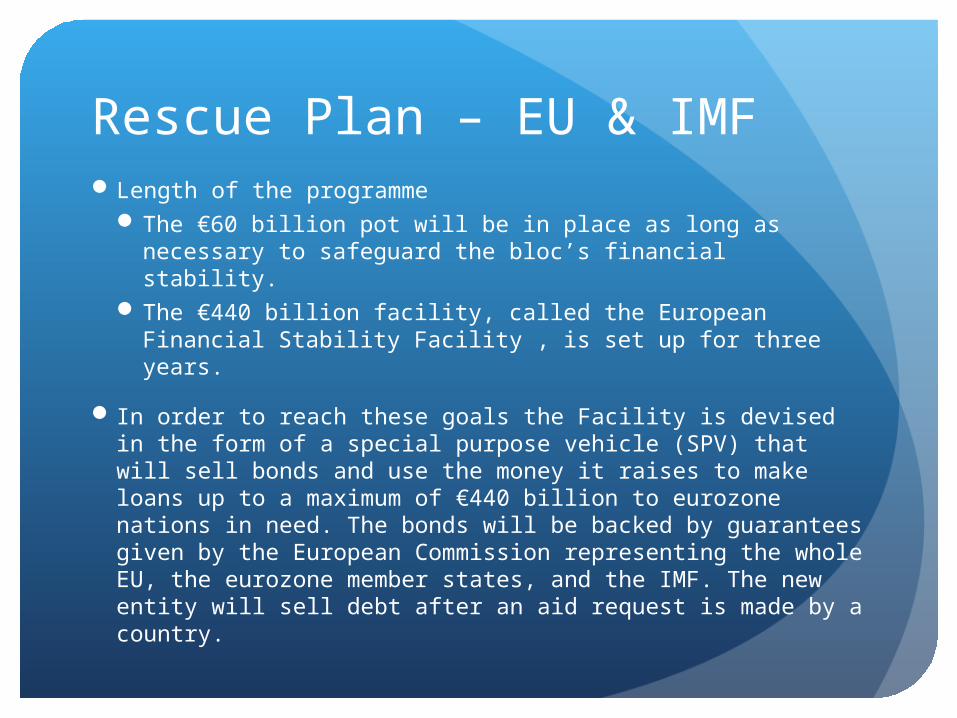

Rescue Plan – EU & IMFLength of the programme

The €60 billion pot will be in place as long as necessary to safeguard the bloc’s financial stability.

The €440 billion facility, called the European Financial Stability Facility , is set up for three years.

In order to reach these goals the Facility is devised in the form of a special purpose vehicle (SPV) that will sell bonds and use the money it raises to make loans up to a maximum of €440 billion to eurozone nations in need. The bonds will be backed by guarantees given by the European Commission representing the whole EU, the eurozone member states, and the IMF. The new entity will sell debt after an aid request is made by a country.

Rescue Plan – The European Financial Stability Facility (EFSF)

The EFSF is operated in June-2010.

The bonds the European Financial Stability Facility (EFSF) issues would be guaranteed by all euro zone member states proportionately to their share in the capital of the European Central bank. The bonds could be of whatever maturity is seen as best and would not be limited by the envisaged 3-year life-span of the SPV itself.

Rescue Plan – Central banks reopen US dollar swap linesAccording to the US Federal Reserve, the Bank

of Canada, the Bank of England, the European Central Bank, and the Swiss National Bank was “in response to the re-emergence of strains in US dollar short-term funding market in Europe.”

To help contain the European fiscal crisis, the facility will enable central banks to lend US dollars to banks in their respective countries that needed dollar funding.

On 10-May-10, Japan’s central bank also joined the five major global counterparts for the actions.

Rescue Plan – Long-term solutionsEuropean Union leaders have made two major

proposals for ensuring fiscal stability in the long term.

The first proposal is the creation of the European Financial Stability Facility.

The second is a single authority responsible for tax policy oversight and government spending coordination of EU member countries, temporarily called European Treasury. The stability facility us financially backed by the EU and the IMF. The European Parliament, the European Council, and especially the European Commission, can all provide some support for the treasury while it is still being built.

EU rescue fund wins top credit rating

The three main credit agencies have given their highest rating to a €440bn fund to help eurozone countries in the event that they face difficulties in accessing capital market.

Mood’s, Standard and Poor’s and Fitch Ratings on 20-Sep-10 all assigned triple-A ratings to the vehicle, which is based in Luxembourg and will act as a backstop to any eurozone country facing problems tapping the bond markets. In return, governments would have to adopt rigorous economic policies agreed with the IMF, European Central Bank and the European Commission.

The outlook on the provisional rating is stable, according to Moody’s, in line with the rating outlooks of 15 of the 16 participating countries.

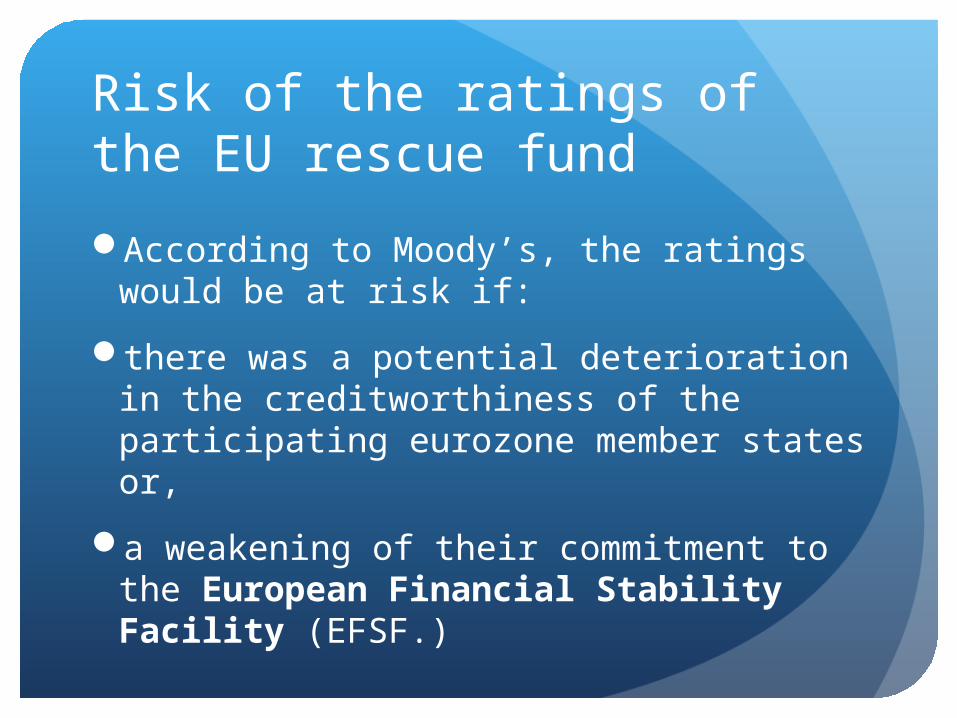

Risk of the ratings of the EU rescue fund

According to Moody’s, the ratings would be at risk if:

there was a potential deterioration in the creditworthiness of the participating eurozone member states or,

a weakening of their commitment to the European Financial Stability Facility (EFSF.)

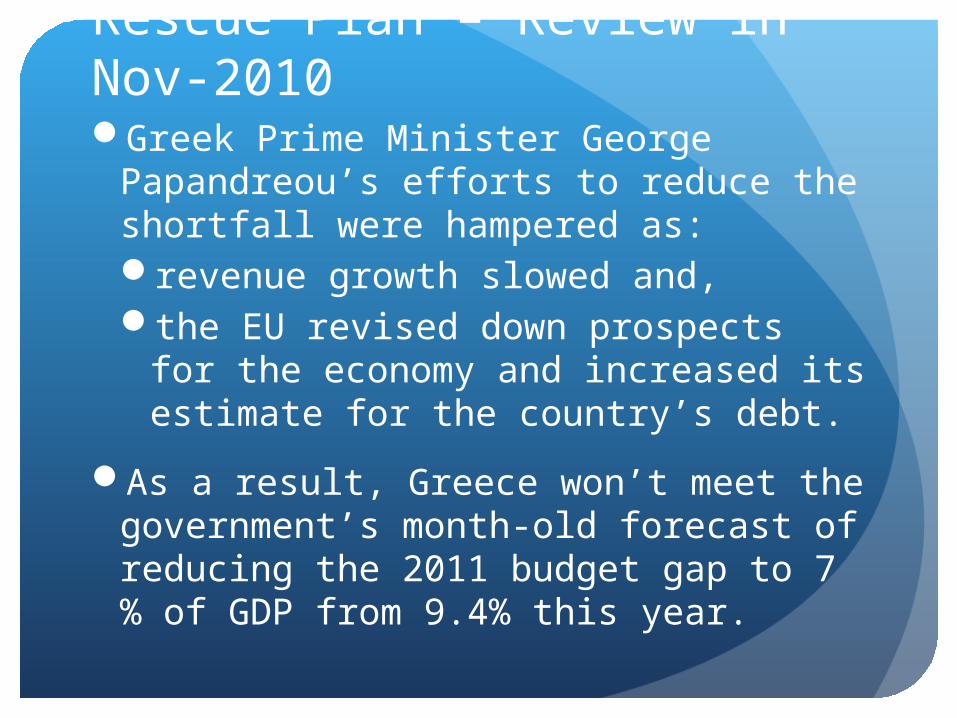

Rescue Plan – Review in Nov-2010Greek Prime Minister George

Papandreou’s efforts to reduce the shortfall were hampered as:revenue growth slowed and,the EU revised down prospects for

the economy and increased its estimate for the country’s debt.

As a result, Greece won’t meet the government’s month-old forecast of reducing the 2011 budget gap to 7 % of GDP from 9.4% this year.

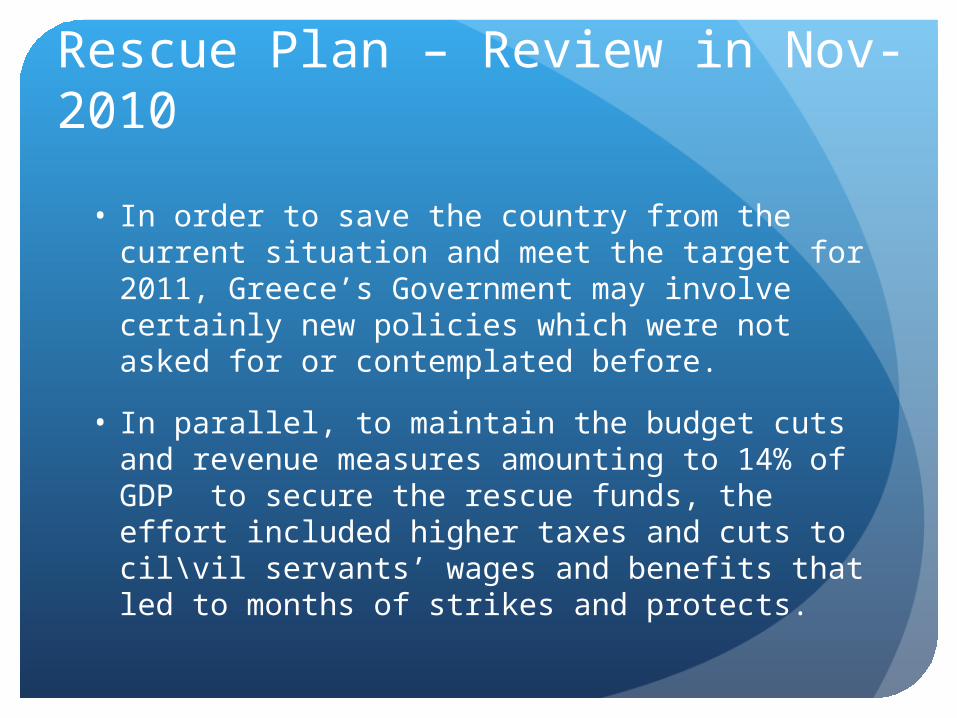

Rescue Plan – Review in Nov-2010

• In order to save the country from the current situation and meet the target for 2011, Greece’s Government may involve certainly new policies which were not asked for or contemplated before.

• In parallel, to maintain the budget cuts and revenue measures amounting to 14% of GDP to secure the rescue funds, the effort included higher taxes and cuts to cil\vil servants’ wages and benefits that led to months of strikes and protects.

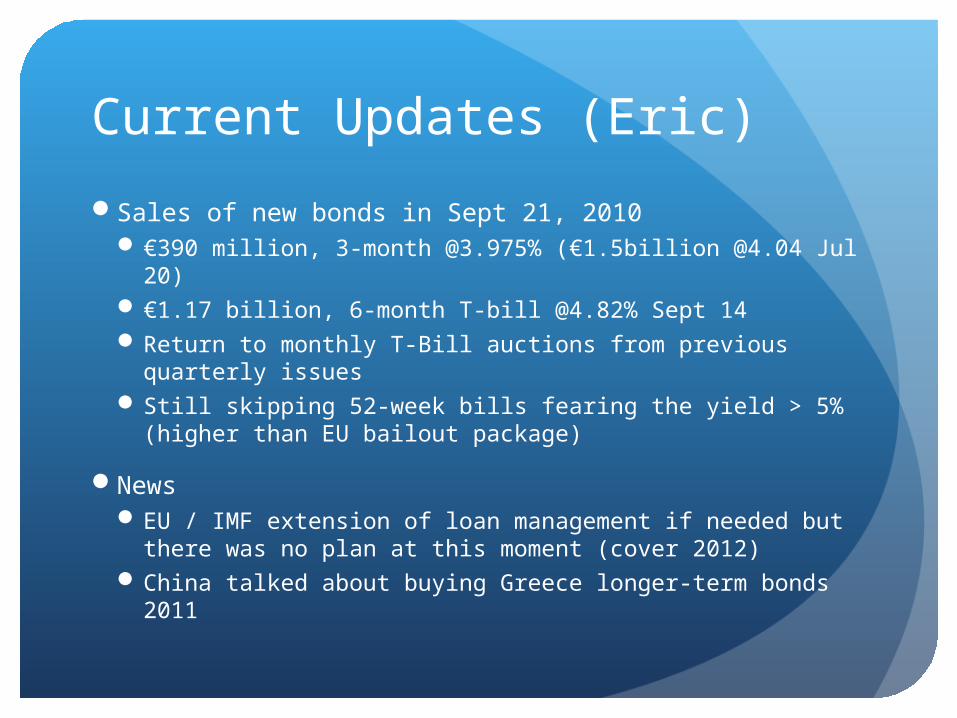

Current Updates (Eric)

Sales of new bonds in Sept 21, 2010 €390 million, 3-month @3.975% (€1.5billion @4.04 Jul 20) €1.17 billion, 6-month T-bill @4.82% Sept 14 Return to monthly T-Bill auctions from previous quarterly

issues Still skipping 52-week bills fearing the yield > 5% (higher

than EU bailout package)

News EU / IMF extension of loan management if needed but

there was no plan at this moment (cover 2012) China talked about buying Greece longer-term bonds 2011

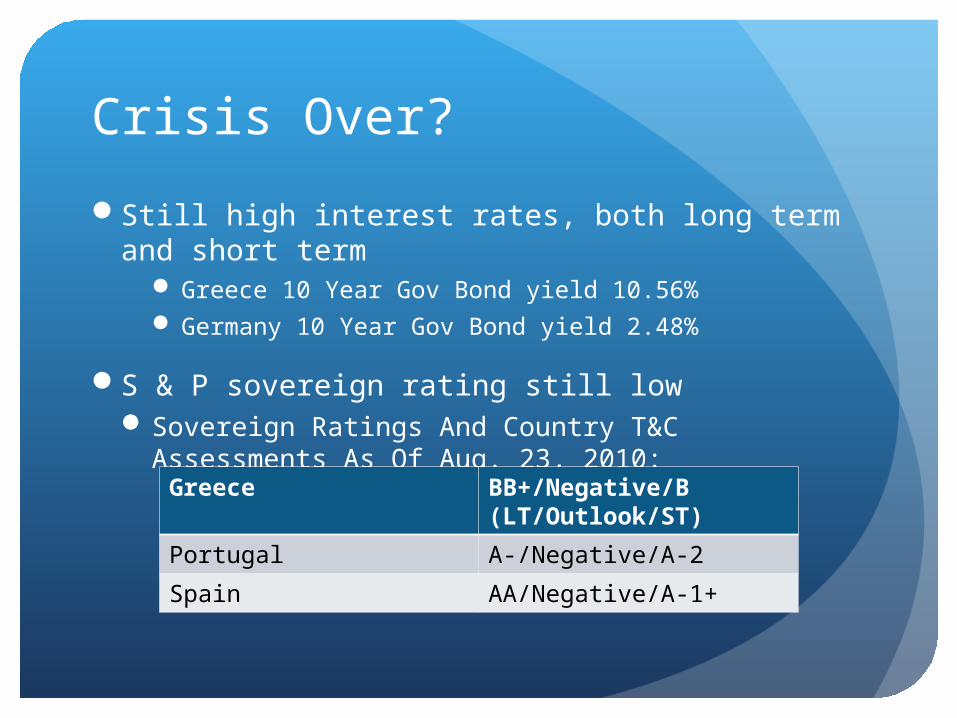

Crisis Over?

Still high interest rates, both long term and short term

Greece 10 Year Gov Bond yield 10.56% Germany 10 Year Gov Bond yield 2.48%

S & P sovereign rating still lowSovereign Ratings And Country T&C Assessments As

Of Aug. 23, 2010:Greece BB+/Negative/B

(LT/Outlook/ST)

Portugal A-/Negative/A-2

Spain AA/Negative/A-1+

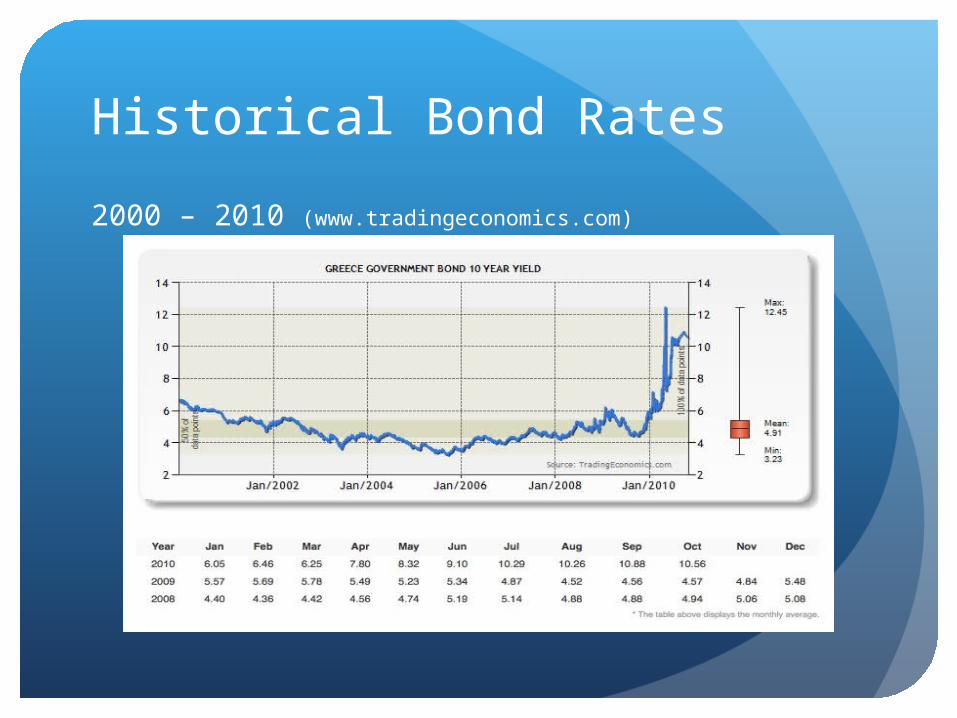

Historical Bond Rates

2000 – 2010 (www.tradingeconomics.com)

Historical Bond Rates

European Central Bank (www.ecb.int)

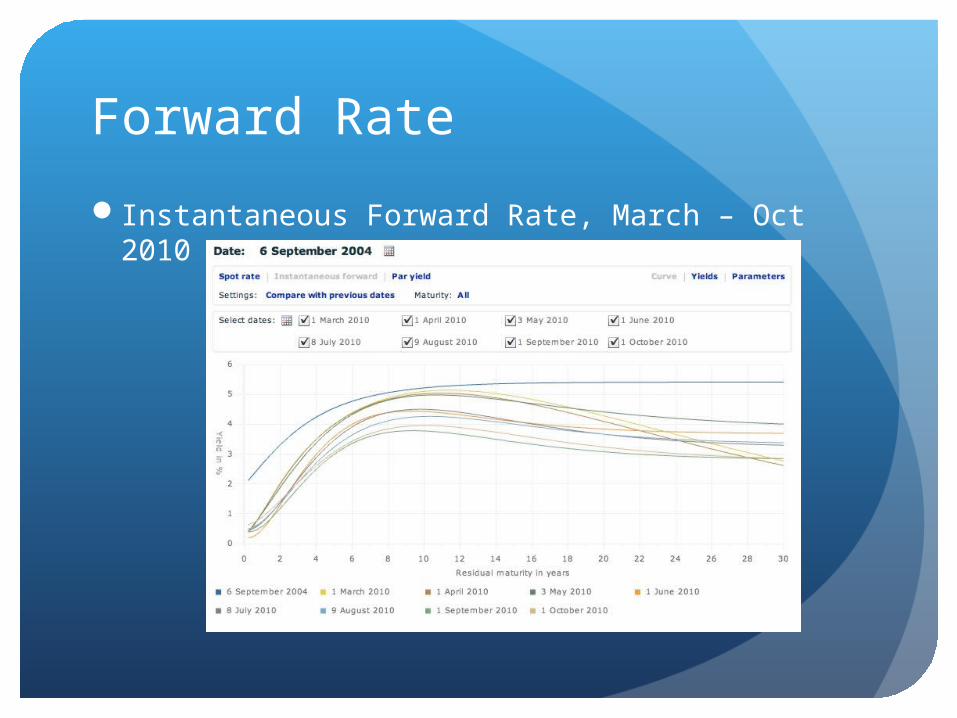

Estimates zero-coupon yield curves for the euro area and derives forward and par yield curves.

The forward curve shows the short-term (instantaneous) interest rate for future periods implied in the yield curve.

Sample contains "AAA-rated" euro area central government bonds, i.e. debt securities with the most favourable credit risk assessment.

Historical daily data going back to 6 September 2004 are now available.

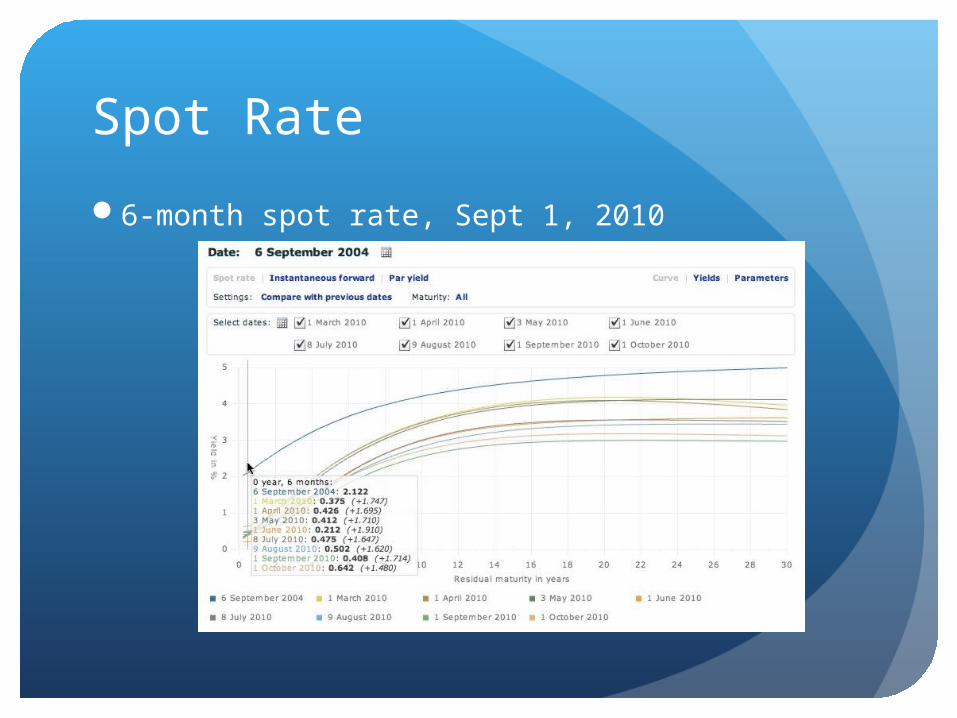

Spot Rate

6-month spot rate, Sept 1, 2010

Forward Rate

Instantaneous Forward Rate, March – Oct 2010

Discussion (group)

Lesson Learned

Implications

(discussion: I suggest when we all finished filling in the content we spend one afternoon to complete this part.)

Discussion – Interest Swap

Interest Swap – in general Periodic payment for an agreed period of time based upon a notional

amount of principal. Notional amount of principal is required in order to compute the

actual cash amounts. Cash flows to be exchanged under an interest rate swap on each

settlement date are typically "netted" (or offset) what is paid or received

For fixed-for-floating interest rate swap. The counterparty making fixed rate payments in a swap is predominantly the less creditworthy participant.

Forward interest rates is calculated to eliminate any arbitrage profit with spot interest rates. Floating rates of interest can be calculated by using forward yield curve.

Because the net present value of the swap is zero. Therefore, from above, the fixed rate payments can be calculated.

Discussion – Currency Swap

Currency swaps were originally conceived in the 1970s in UK. UK companies had to pay a premium to borrow in US Dollars. So they set up back-to-back loan agreements with US companies wishing to borrow Sterling

Cross-currency interest rate swaps were introduced by the World Bank in 1981 to obtain Swiss francs and German marks by exchanging cash flows with IBM.

Global financial crisis of 2008, the currency swap transaction structure was used by the United States Federal Reserve System to establish central bank liquidity swaps (A currency swap

should be distinguished from a central bank liquidity swap).

Ref.: http://en.wikipedia.org/wiki/Currency_swap

Discussion – Currency Swap

Foreign-exchange agreement between two parties to exchange principal and/or interest payments in one currency for equal net present value loan in another currency.

Three different ways in which swaps can exchange loans:

Principal only Agreed rate in the future – forward contract or futures (higher cost then alternative

derivatives)

Longer term up to 10 years – FX swap

Principal + interest interest cash flows are not netted before they are paid to the counterparty

each party borrows on the other's behalf – also known as a back-to-back loan

Interest payment only exchanged cash flows are in different denominations and so are not netted

known as a cross-currency interest rate swap, or cross-currency swap

ECB Rejects Request for Details

Nov, European Central Bank ECB turned down a request and an appeal by Bloomberg News “acute” risk of roiling markets refused to release two briefing documents:

“The impact on government deficit and debt from off-market swaps: the Greek case.”

The second reviews Titlos Plc, a securitization that allowed National Bank of Greece SA, the country’s biggest lender, to exchange swaps on Greek government debt for funding from the ECB.

The briefings give officials’ views on the impact of the swaps and analyze how the Titlos transaction would affect “the Eurosystem collateral framework, and associated risk control measures.”

Discussion – Interest Swap

Consider fixed-to-floating swap Fixed side – Greece, Floating side – Goldman Using a lower $/€ exchange rate Initial cash flow – off-the-balance sheet €1 billion to Greece

changed the fixed rate assume it was a one-time payment as the exchange rate

was rising during the period – lower government operation deficit

Cash flow from float decreased from 2007 – 2009 due to decreasing cash inflow from float

Contracts will terminate in: 2012(2002+10) / 2017(+15) – affected 3- & 7-Yr bond issues 2015 (2005+10) / 2020(+15) – affected 5- & 10-Yr bond issues

Discussion – Goldman’s Swaps

Greece / Goldman’s Swaps$/€ exchange rate:

Dec 2, 2002 = 1.0009 Sept 6, 2004 = 1.227

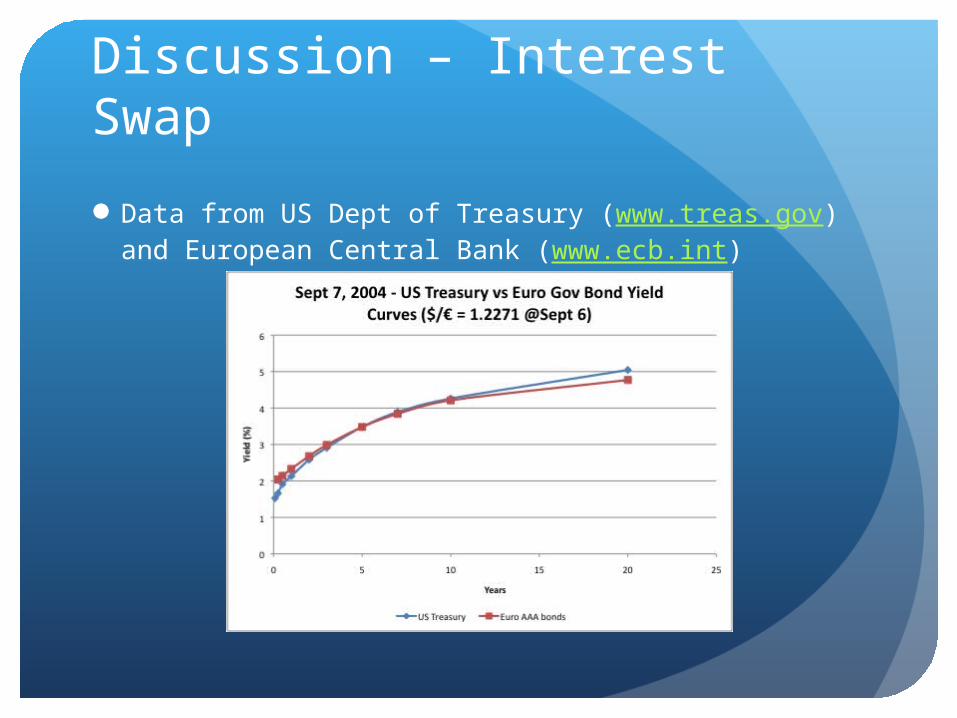

US Treasury vs Euro Gov Bond Yield, Sept 7, 2004 Short-term US’s was lower than Euro’s (1-month to 3-Yr) Long-term US’s was higher than Euro’s (10-Yr to 20-Yr)

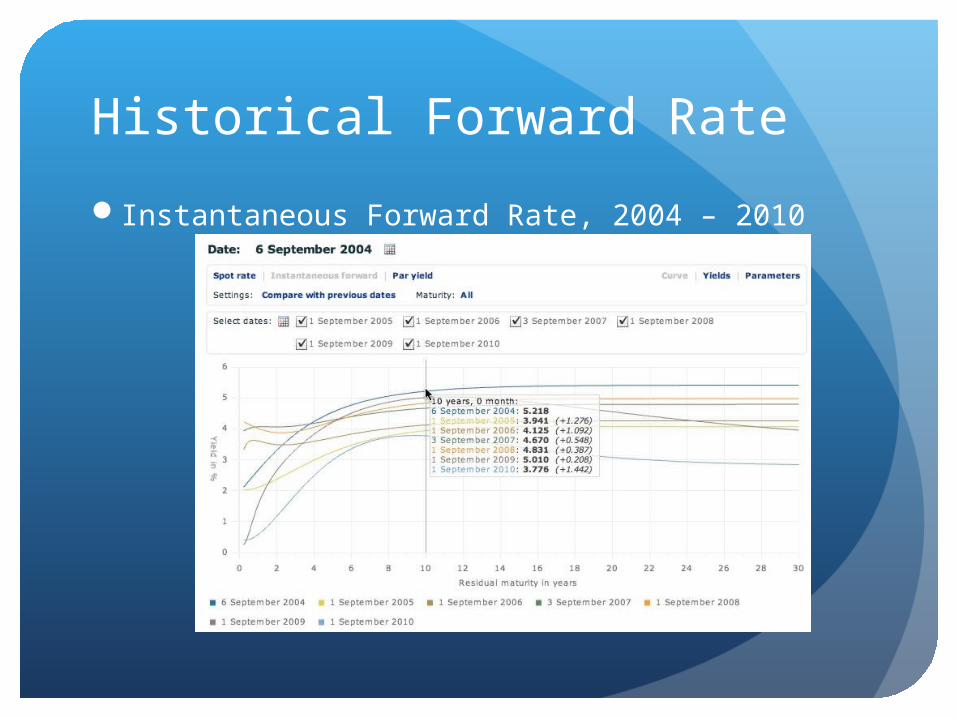

Historical Forward Rate

Instantaneous Forward Rate, 2004 – 2010

Discussion – Interest Swap

Data from US Dept of Treasury (www.treas.gov) and European Central Bank (www.ecb.int)

Historical $/€ Rates

Min(Oct/00) 0.8412 Max(Jul/08) 1.5893Current(Nov/10)~1.4

(finance.yahoo.com)

Historical ¥/€ Rates

Min(Oct/00) 91.334 Max(Jul/08) 169.3582 Current(Nov/10)~112.075

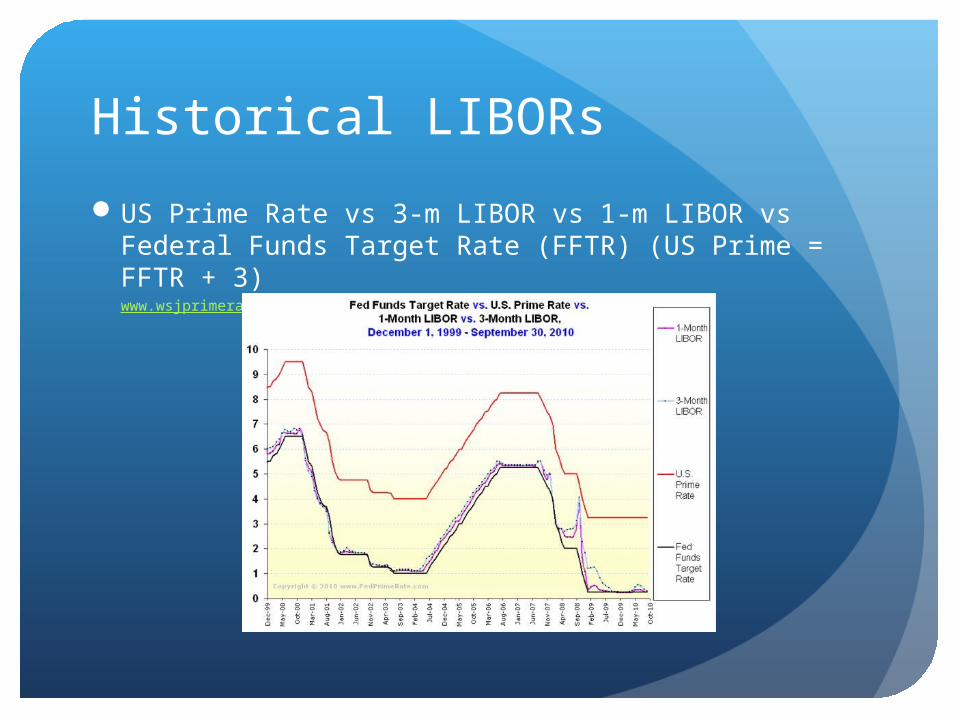

Historical LIBORs

US Prime Rate vs 3-m LIBOR vs 1-m LIBOR vs Federal Funds Target Rate (FFTR) (US Prime = FFTR + 3)www.wsjprimerate.us - chart updated on Oct 5, 2010

Lesson Learned

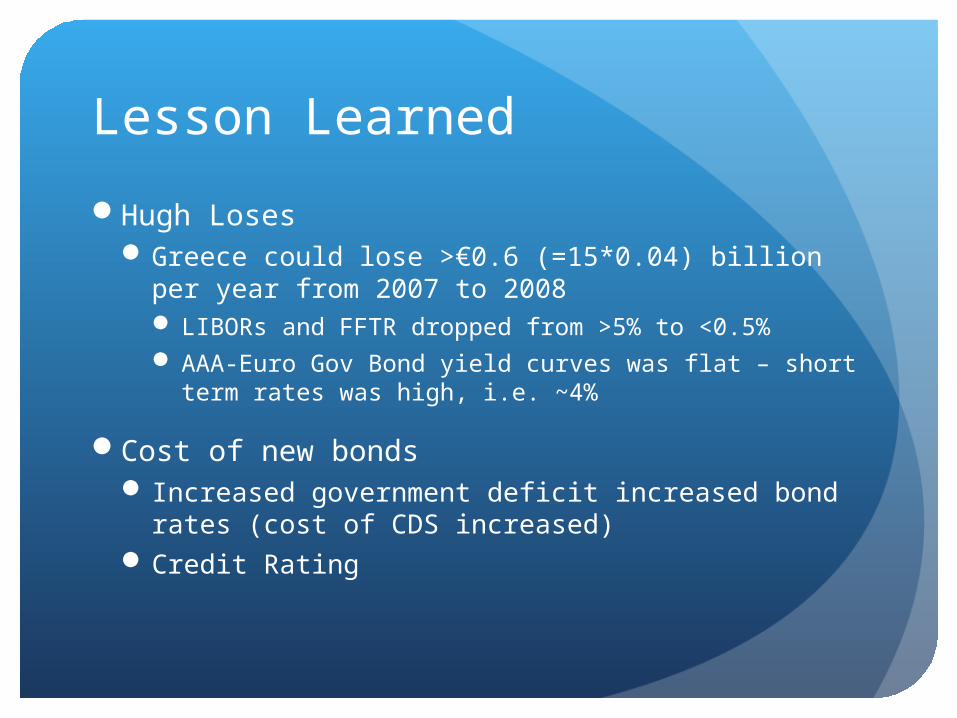

Hugh LosesGreece could lose >€0.6 (=15*0.04) billion per year

from 2007 to 2008 LIBORs and FFTR dropped from >5% to <0.5% AAA-Euro Gov Bond yield curves was flat – short term

rates was high, i.e. ~4%

Cost of new bonds Increased government deficit increased bond rates

(cost of CDS increased)Credit Rating

Lesson Learned

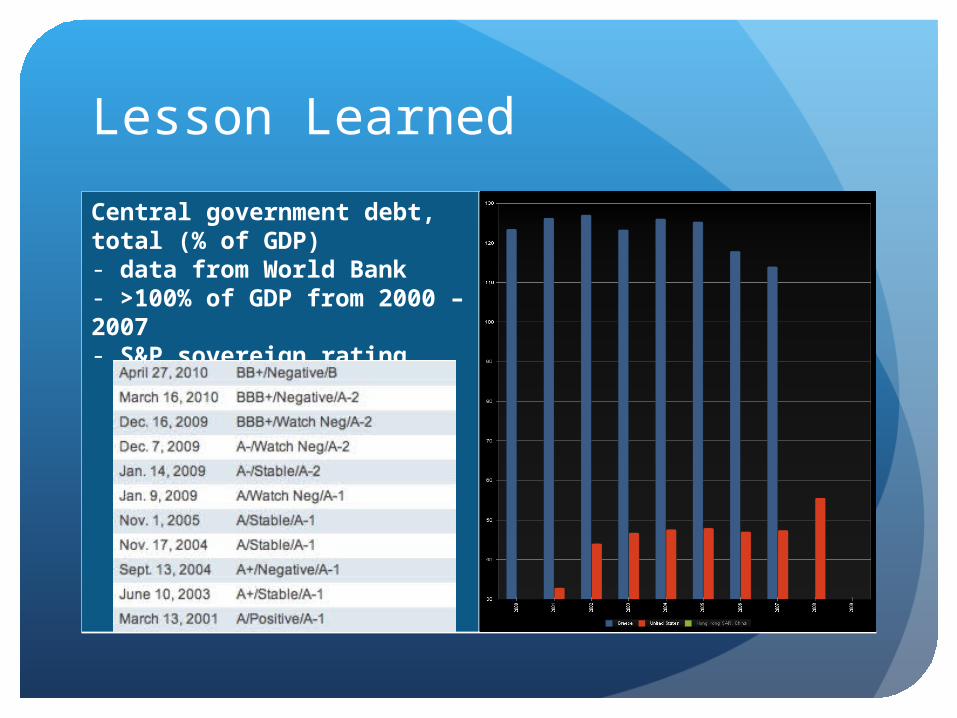

Central government debt, total (% of GDP)- data from World Bank- >100% of GDP from 2000 – 2007- S&P sovereign rating

Take Home - ‘Attractive’ Yield

“Investors could find 5.4 percent, the yield at which the six-month area on the Greek curve trades, rather attractive, given that Greek financing needs over that period will still be completely covered by the IMF-EU loan,” said Chiara Cremonesi, a market strategist at UniCredit SpA in London.

Moody’s Investors Service, which downgraded Greece’s credit rating to non-investment grade in June, said on Oct. 5 that it’s “impressed” with the country’s overhaul of its public finances. The risk to the country’s sovereign rating forecast “is to the upside,” assuming reforms continue, Moody’s said.