Graphex Mining Limited ACN 610 319 769 Prospectus · Graphex Mining Limited . ACN 610 319 769 ....

225

Graphex Mining Limited ACN 610 319 769 Prospectus For an offer of up to 35,000,000 Shares at an issue price of $0.20 each to raise up to $7,000,000, with 1 free attaching Loyalty Option granted for every 3 Shares issued, each with an exercise price of $0.25 and expiry date 3 years from the Issue Date. This Prospectus has been issued to provide information on the offer of a minimum of 21,250,000 Shares and a maximum of 35,000,000 Shares to be issued at a price of $0.20 per Share to raise a total of a minimum of $4,250,000 and a maximum of $7,000,000 (before costs) (General Offer). Loyalty Options with an exercise price of $0.25 each and expiry date 3 years from the Issue Date will be issued free attaching on a 1 for 3 basis to every person issued Shares pursuant to this Prospectus. This Prospectus also incorporates a priority offer as part of the General Offer to shareholders of IMX Resources Limited registered on a record date of 8 April 2016 (IMX Offer). The General Offer and IMX Offer (together, Offers) pursuant to this Prospectus are conditional on ASX listing of the Company as outlined in Section 1.5 of this Prospectus. It is proposed that the IMX Offer will close at 5.00pm (WST) on 26 April 2016 and the General Offer will close at 5.00pm (WST) on 2 May 2016. The Directors reserve the right to close the Offers earlier or to extend these dates without notice. Applications must be received before that time. This is an important document and requires your immediate attention. It should be read in its entirety. Please consult your professional adviser(s) if you have any questions about this document. Investment in the Shares offered pursuant to this Prospectus should be regarded as highly speculative in nature, and investors should be aware that they may lose some or all of their investment. Refer to Section 5 for a summary of the key risks associated with an investment in the Shares. Joint Lead Managers

Transcript of Graphex Mining Limited ACN 610 319 769 Prospectus · Graphex Mining Limited . ACN 610 319 769 ....

Graphex Mining Limited ACN 610 319 769

Prospectus

For an offer of up to 35,000,000 Shares at an issue price of $0.20 each to raise up to $7,000,000, with 1 free attaching Loyalty Option granted for every 3 Shares issued, each

with an exercise price of $0.25 and expiry date 3 years from the Issue Date.

This Prospectus has been issued to provide information on the offer of a minimum of 21,250,000 Shares and a maximum of 35,000,000 Shares to be issued at a price of $0.20 per Share to raise a total of a minimum of $4,250,000 and a maximum of $7,000,000 (before costs) (General Offer).

Loyalty Options with an exercise price of $0.25 each and expiry date 3 years from the Issue Date will be issued free attaching on a 1 for 3 basis to every person issued Shares pursuant to this Prospectus.

This Prospectus also incorporates a priority offer as part of the General Offer to shareholders of IMX Resources Limited registered on a record date of 8 April 2016 (IMX Offer).

The General Offer and IMX Offer (together, Offers) pursuant to this Prospectus are conditional on ASX listing of the Company as outlined in Section 1.5 of this Prospectus.

It is proposed that the IMX Offer will close at 5.00pm (WST) on 26 April 2016 and the General Offer will close at 5.00pm (WST) on 2 May 2016. The Directors reserve the right to close the Offers earlier or to extend these dates without notice. Applications must be received before that time.

This is an important document and requires your immediate attention. It should be read in its entirety. Please consult your professional adviser(s) if you have any questions about this document.

Investment in the Shares offered pursuant to this Prospectus should be regarded as highly speculative in nature, and investors should be aware that they may lose some or all of their investment. Refer to Section 5 for a summary of the key risks associated with an investment in the Shares.

Joint Lead Managers

TABLE OF CONTENTS Section Page No

IMPORTANT INFORMATION ..................................................................... 3

CORPORATE DIRECTORY ........................................................................ 4

LETTER FROM THE BOARD ...................................................................... 5

KEY OFFER DETAILS .............................................................................. 7

INDICATIVE TIMETABLE .......................................................................... 8

INVESTMENT OVERVIEW ......................................................................... 9

1. Details of the Offers .................................................................. 27

2. Overview of the Company ........................................................... 41

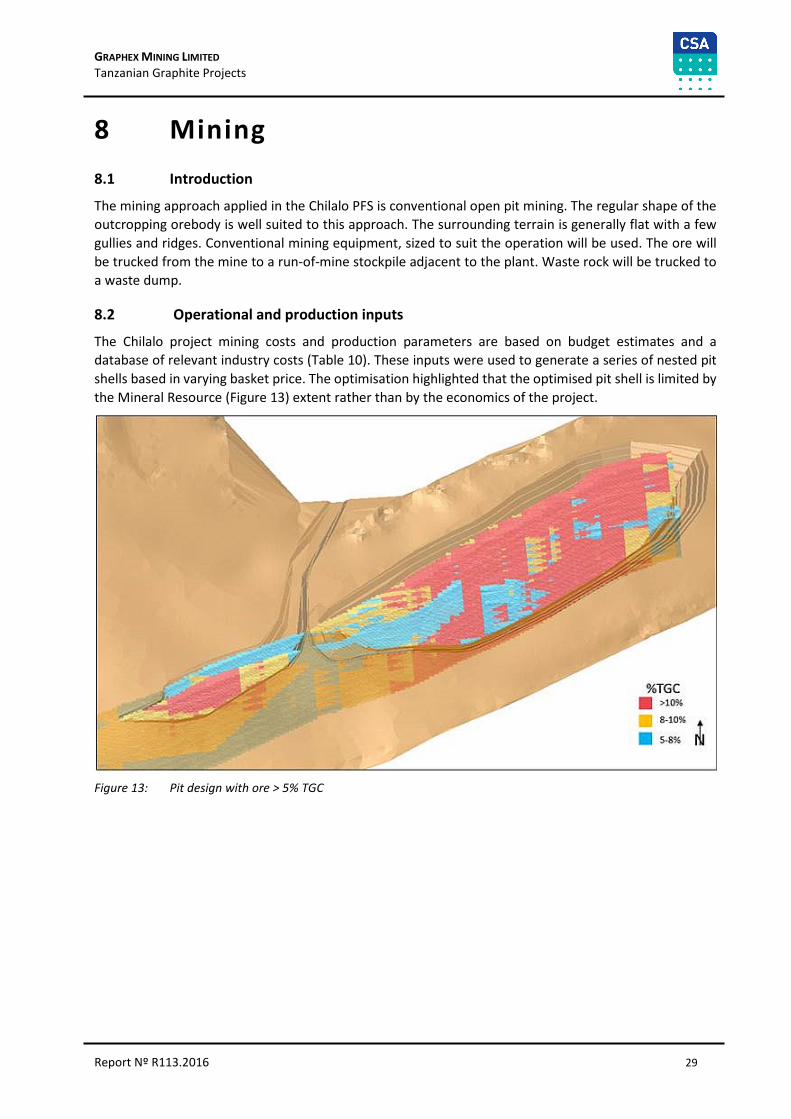

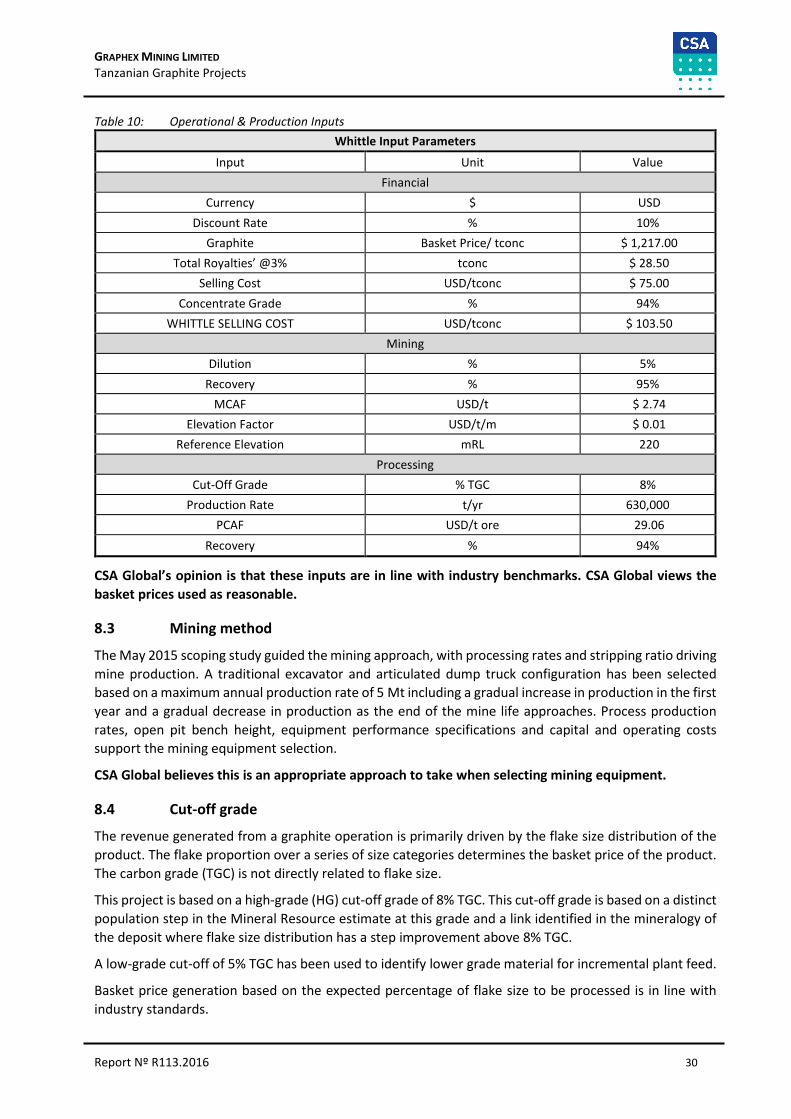

3. Overview of the Chilalo Graphite Project ........................................ 45

4. Overview of Tanzania ................................................................ 59

5. Risk Factors ............................................................................. 62

6. Independent Technical Assessment ................................................ 72

7. Independent Solicitor's Report ...................................................... 73

8. Financial information ................................................................. 74

9. Investigating Accountant's Report .................................................. 83

10. Directors, Key Management and Corporate Governance ...................... 84

11. Material Contracts ..................................................................... 92

12. Additional Information ............................................................... 98

13. Directors' Authorisation ............................................................ 113

14. Definitions ............................................................................ 114

Page 3

IMPORTANT INFORMATION

Prospectus

This Prospectus is dated 4 April 2016 and was lodged with ASIC on that date. ASIC, ASX and their respective officers do not take any responsibility for the contents of this Prospectus or the merits of the investment to which this Prospectus relates.

Within 7 days of the date of this Prospectus, the Company will make an application to ASX for the Shares offered pursuant to the Prospectus to be admitted for quotation on ASX.

Shares will not be issued pursuant to this Prospectus later than 13 months after the date of this Prospectus.

Persons wishing to apply for Shares pursuant to the Offers must do so using the applicable Application Form attached to or accompanying this Prospectus. Before applying for Shares potential investors should carefully read the Prospectus so that they can make an informed assessment of:

• the rights and liabilities attaching to the Shares and Loyalty Options; • the assets and liabilities of the Company; and • the Company's financial position and performance, profits and losses, and prospects.

Investors should carefully consider these factors in light of their own personal financial and taxation circumstances.

No person is authorised to give any information or to make any representation in relation to the Offers which is not contained in this Prospectus. Any information or representation not so contained may not be relied upon as having been authorised by the Company or the Directors in relation to the Offers.

Risks

Any investment in the Company should be considered highly speculative. Before deciding to invest in the Company, potential investors should read the entire Prospectus and, in particular, in considering the prospects of the Company, potential investors should consider the risk factors that could affect the financial performance and assets of the Company. Investors should carefully consider these factors in light of their personal circumstances (including financial and taxation issues). The Shares offered by this Prospectus should be considered highly speculative. Please refer to Section 5 for details relating to risk factors. Persons considering applying for Shares pursuant to the Prospectus should obtain professional advice from an accountant, stockbroker, lawyer or other adviser before deciding whether to invest. No guarantee is given as to the success of the Company, the repayment of capital, the payment of dividends, or the price at which the Shares will trade on ASX.

Offer outside Australia

The offer of Shares made pursuant to this Prospectus is not made to persons to whom, or places in which, it would not be lawful to make such an offer of Shares. No action has been taken to register the Offers under this Prospectus in any jurisdiction outside Australia. The distribution of this Prospectus in jurisdictions outside Australia may be restricted by law in those jurisdictions and therefore persons who come into possession of this Prospectus should seek advice on and observe any of these restrictions. Failure to comply with these restrictions may violate securities laws.

See Section 1.16 for further information on Hong Kong, Mauritius, Singapore and the UK.

Forward-looking statements

This Prospectus contains forward-looking statements which incorporate an element of uncertainty or risk, such as 'intends', 'may', 'could', 'believes', 'estimates', 'targets' or 'expects'. These statements are based on an evaluation of current economic and operating conditions, as well as assumptions regarding future events. These events, as at the date of this Prospectus, are expected to take place, but there is no guarantee that such

will occur as anticipated or at all given that many of the events are outside the Company's control.

Accordingly, the Company cannot and does not give any assurance that the results, performance or achievements expressed or implied by the forward-looking statements contained in this Prospectus will actually occur. Further, the Company may not update or revise any forward-looking statement if events subsequently occur or information subsequently becomes available that affects the original forward-looking statement.

Exposure Period

This Prospectus will be circulated during the Exposure Period. The purpose of the Exposure Period is to enable this Prospectus to be examined by market participants prior to applying for Shares. This examination may result in the identification of deficiencies in this Prospectus and, in those circumstances, any Application that has been received may need to be dealt with in accordance with section 724 of the Corporations Act. Applications for Shares under the Offers set out in this Prospectus will not be processed by the Company until after the expiry of the Exposure Period. No preference will be conferred on Applications lodged prior to the expiry of the Exposure Period.

Conditional Offers

The Offers contained in this Prospectus are conditional on certain events occurring. If these events do not occur, the Offer will not proceed and investors will be refunded their Application Monies without interest. Please refer to Section 1.5 for further details on the conditions attaching to the Offers.

Electronic Prospectus

If you have received this Prospectus as an electronic Prospectus, please ensure that you have received the entire Prospectus accompanied by the applicable Application Form. If you have not, please contact the Company at +61 8 9200 4960 and the Company will send you, at no cost, either a hard copy or a further electronic copy of the Prospectus or both. Alternatively, you may obtain a copy of the Prospectus from the Company's website at www.graphexmining.com.au.

The Company reserves the right not to accept an Application Form from a person if it has reason to believe that when that person was given access to the electronic Application Form, it was not provided together with the electronic Prospectus and any relevant supplementary or replacement prospectus or any of those documents were incomplete or altered.

Diagrams

Diagrams used in this Prospectus may not be drawn to scale.

Miscellaneous

All references to "$", "A$", "AUD", "dollar" and "cents" are references to Australian currency unless otherwise stated.

All references to time relate to the time in Perth, Western Australia unless otherwise stated.

A number of terms and abbreviations used in this Prospectus have defined meanings which appear in Section 14.

Page 4

CORPORATE DIRECTORY

Directors Mr Stephen Dennis Mr Philip Hoskins Mr Grant Davey Company Secretary Mr Stuart McKenzie Registered Office Suite 4, Level 1 2 Richardson Street WEST PERTH WA 6005 Telephone: +61 8 9200 4960 Facsimile: +61 8 9200 4961 Email: [email protected] Website www.graphexmining.com.au Proposed Stock Exchange Listing Australian Securities Exchange (ASX) Proposed ASX Code: GPX Share Registry* Computershare Investor Services Pty Limited Level 11, 172 St Georges Terrace PERTH WA 6000 Telephone (within Australia): 1300 850 505 (outside Australia): +61 3 9415 4000 Facsimile: +61 3 9473 2500 Auditor* PricewaterhouseCoopers Brookfield Place 125 St Georges Terrace PERTH WA 6000

Australian Legal Adviser Bellanhouse Legal Ground Floor, 11 Ventnor Avenue WEST PERTH WA 6005 Investigating Accountant KPMG Financial Advisory Services (Australia) Pty Ltd 235 St Georges Terrace PERTH WA 6000 Telephone: +61 8 9263 7171 Facsimile: +61 8 9263 7129 Independent Technical Assessor CSA Global Level 2, 3 Ord Street WEST PERTH WA 6005 Independent Solicitor East African Law Chambers Plot No. 18 Rukwa Street Masaki Dar es Salaam TANZANIA Joint Lead Managers Palladion Partners Pty Ltd Level 14, 234 George Street SYDNEY NSW 2000 Telephone: +61 2 9002 5410 RM Corporate Finance Pty Ltd AFSL 315235 Level 1, 143 Hay Street SUBIACO WA 6008 Telephone: +61 8 6380 9200

* This entity is included for information purposes only. It has not been involved in the preparation of this Prospectus.

Page 5

LETTER FROM THE BOARD

Dear Investor,

On behalf of the Directors, I look forward to welcoming you as a shareholder of Graphex Mining Limited (Company). The Company is a graphite-focused company with a clear strategy of fast-tracking the development of the Chilalo Graphite Project in Tanzania.

The Company was incorporated by its current parent company IMX Resources Limited (IMX) in January 2016, following a strategic review by the IMX board of its assets and a decision by the IMX board to dispose of its graphite assets into the Company. Subject to IMX shareholder approval and satisfaction of various other conditions (see Section 11.2), the Company will acquire the Chilalo Graphite Project and IMX will distribute approximately 16,454,000 Graphex Shares to its shareholders.

A recently completed Pre-Feasibility Study by IMX confirmed the emergence of the Chilalo Graphite Project as a technically sound project, with low capital intensity and attractive returns. Testwork has demonstrated Chilalo is capable of producing a high quality product with excellent flake size distribution and expansion ratios. The Pre-Feasibility Study demonstrates Chilalo's proximity to existing infrastructure and high resource grade contribute to low operating costs and capital intensity.

The Company is presently in discussions with large Chinese companies, China Gold Group Investment Co Ltd (China Gold Investment) and CN Docking Joint Investment and Development Co. Ltd (a wholly owned subsidiary of China National Building Material Group Corporation) (CN Docking). IMX has an existing memorandum of understanding (MOU) with China Gold Investment and CN Docking, pursuant to which the parties agreed to an exclusive negotiation and due diligence period with respect to the Chilalo Project, ceasing on 31 July 2016. Providing a binding agreement is reached with China Gold Investment and CN Docking, the Board believes a relationship with China Gold Investment and CN Docking has potential to:

1. provide the Chilalo Project with a credible offtake partner;

2. inject significant expertise in the development and construction of graphite projects; and

3. provide project financing via both procurement of project-level debt and contribution of equity to construction of graphite projects.

The Company has assembled a balanced Board of Directors who have extensive skills in capital markets, project finance and development, mining operations, corporate transactions, operating in Tanzania and Africa more generally, as well as having previous experience in undertaking business with China. The Board is excited about the potential of the Chilalo Graphite Project, and the predicted future growth in demand for high quality flake graphite.

Upon listing, implementation of the Company's strategy will be led by Managing Director Phil Hoskins and supported by the management team responsible for the Project's rapid development to date. The management team is expected to be complemented by experienced consultants (previously engaged by IMX) with experience in African project development and strategic Chinese relationships.

The Board believes that graphite is shaping to be a commodity of the future. The next 12-18 months will be critical in determining which of the graphite developers can successfully transition to profitable graphite operations. We are confident that we have the asset, the team and the strategic relationships to ensure that we can be one of the success stories.

Page 6

The purpose of this Offer is to expand the Company's shareholder base, potentially introducing one or two cornerstone investors to the Company's shareholder register, raise sufficient funds to commence a definitive feasibility study on the Chilalo Graphite Project, and at the same time, as a condition of the Offer, seek a listing of the Company on ASX.

I encourage you to read the Prospectus, request that you consider the risks of investment in Section 5, and invite you to become a shareholder in the Company, which I believe has great potential.

Yours faithfully

Stephen Dennis Chairman Graphex Mining Limited

Page 7

KEY OFFER DETAILS

Pro forma capital structure

Offer Price per Share $0.20 per Share

Shares offered under the Offers

- Minimum Subscription

- Maximum Subscription

21,250,000 Shares

35,000,000 Shares

Cash raised under the Offers (before expenses)

- Minimum Subscription

- Maximum Subscription

$4,250,000

$7,000,000

Pre-Offer Shares on issue* 20,000,000 Shares

Total number of Shares on issue following the Offers

- Minimum Subscription

- Maximum Subscription

41,250,000 Shares

55,000,000 Shares

*As at the date of this Prospectus the Company has 100 Shares on issue. Pursuant to the Acquisition Agreement, at or around the Issue Date the Company will issue a further 19,999,900 Shares as part consideration for the acquisition of the Chilalo Graphite Project. Of these, approximately 16,454,000 will be transferred to IMX Shareholders pursuant to a proposed In-specie Distribution and 3,546,000 will be transferred to MMG Exploration Holdings Limited (MMG) under an existing joint venture agreement. See Section 11.2 for further details on the Acquisition Agreement.

Note: Please refer to Section 1.6 for further details relating to the proposed capital structure of the Company.

Page 8

INDICATIVE TIMETABLE

Event Date

Lodgement of this Prospectus with ASIC 4 April 2016

IMX Offer Record Date 8 April 2016

IMX Offer Opening Date 11 April 2016

IMX Offer Closing Date 26 April 2016

General Offer Opening Date 11 April 2016

General Offer Closing Date 2 May 2016

Completion of Acquisition Agreement 9 May 2016

Record date for In-specie Distribution 11 May 2016

Completion of In-specie Distribution 12 May 2016

Issue of Shares and Loyalty Options under the Offers 13 May 2016

Despatch of holding statements 13 May 2016

Expected date for Shares to commence trading on ASX 18 May 2016

Note: The dates shown above are indicative only and may vary subject to the Corporations Act, the Listing Rules and other applicable laws. In particular, the Company reserves the right to vary the opening dates and the closing dates without prior notice, which may have a consequential effect on the other dates. Applicants are therefore encouraged to lodge their Application Form as soon as possible after the relevant opening date if they wish to invest in the Company. The Company also reserves the right not to proceed with any of the Offers at any time before the issue of Shares to applicants.

Page 9

INVESTMENT OVERVIEW

This Section is not intended to provide full information for investors intending to apply for Securities offered pursuant to this Prospectus. This Prospectus should be read and considered in its entirety. The Securities offered pursuant to this Prospectus carry no guarantee in respect of return of capital, return on investment, payment of dividends or the future value of the Securities.

Topic Summary More information

Introduction

Who is the Company and what does it do?

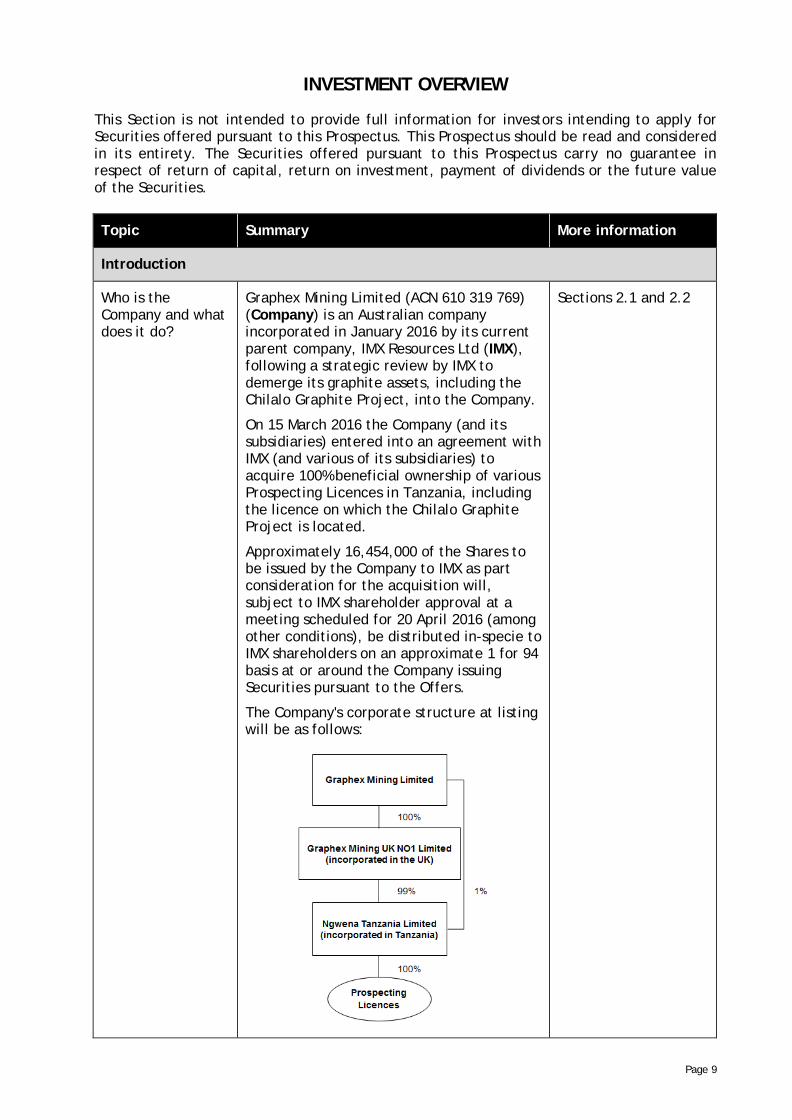

Graphex Mining Limited (ACN 610 319 769) (Company) is an Australian company incorporated in January 2016 by its current parent company, IMX Resources Ltd (IMX), following a strategic review by IMX to demerge its graphite assets, including the Chilalo Graphite Project, into the Company.

On 15 March 2016 the Company (and its subsidiaries) entered into an agreement with IMX (and various of its subsidiaries) to acquire 100% beneficial ownership of various Prospecting Licences in Tanzania, including the licence on which the Chilalo Graphite Project is located.

Approximately 16,454,000 of the Shares to be issued by the Company to IMX as part consideration for the acquisition will, subject to IMX shareholder approval at a meeting scheduled for 20 April 2016 (among other conditions), be distributed in-specie to IMX shareholders on an approximate 1 for 94 basis at or around the Company issuing Securities pursuant to the Offers.

The Company's corporate structure at listing will be as follows:

Sections 2.1 and 2.2

Page 10

Topic Summary More information

Other than as disclosed in this Prospectus, the Company has not undertaken any activities since incorporation.

What are the Company's projects?

Upon completion of the Acquisition Agreement and listing on ASX, the Company (through its wholly owned subsidiary Ngwena Tanzania Limited) will own a 100% interest in six Prospecting Licences in south-east Tanzania, including the Prospecting Licence on which the flagship Chilalo Graphite Project is located.

Details of the Prospecting Licences are set out in the table below:

Project area Licence no.

Chilalo PL 6073/2009

PL 6158/2009

PL 9929/2014

PL 9946/2014

Noli PL 8628/2012

PL 5447/2008

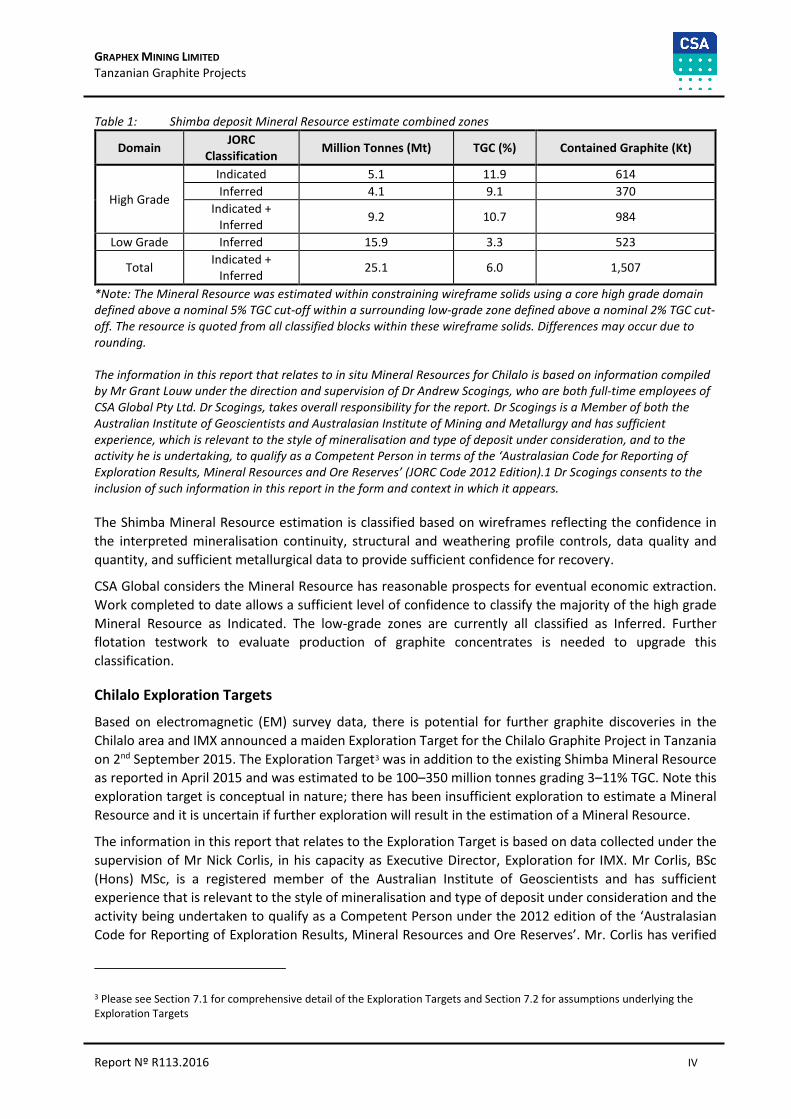

The Project has an existing Indicated and Inferred Mineral Resource Estimate of 25.1Mt at 6% TGC for 1,507Kt of contained graphite.

IMX recently completed a pre-feasibility study (PFS) on the Chilalo Graphite Project, which confirmed the emergence of the Project as a technically sound project, with low capital intensity and attractive returns. The Board believes the results of the PFS strongly support the Company's strategy of focusing its efforts on advancing Chilalo as a near-term development opportunity.

Sections 2.3, 3 and 6

What is the Company's financial position?

The Company was incorporated in January 2016 and has not traded, therefore the Company has not earned any revenue or incurred any expenses from its activities (other than the expenses of the Offers).

Section 8 contains historical financial

Section 8

Page 11

Topic Summary More information

information for the Company.

The Board is satisfied that upon completion of the Offers, the Company will have sufficient working capital to meet its stated objectives.

What is the proposed capital structure of the Company?

Following completion of the Offers under this Prospectus and completion of the Acquisition Agreement, the proposed capital structure of the Company is as set out in Section 1.6.

Section 1.6

What is the proposed use of funds raised under the Offers?

Graphex proposes to use the funds raised from the Offers to purchase the Chilalo Project from IMX, conduct marketing activities targeted to reaching agreements for offtake and project financing (the completion of which is expected to allow for commencement of a definitive feasibility study on a Minimum Subscription basis), to cover the costs of the Offers, and for administration and general working capital.

Sections 1.7 and 3.4

What is the Company's strategy?

Following completion of the Offers under this Prospectus and completion of the Acquisition Agreement, the Company's immediate priority is to further advance the development of the Chilalo Graphite Project by obtaining a mining licence, securing binding offtake agreements, completing a definitive feasibility study, progressing project financing negotiations and eventually constructing the Project.

Section 2.4

Summary of key risks

Prospective investors should be aware that subscribing for Shares in the Company involves a number of risks. The risk factors set out in Section 5, and other general risks applicable to all investments in listed securities, may affect the value of the Shares in the future. Accordingly, an investment in the Company should be considered highly speculative. This Section summarises the key risks which apply to an investment in the Company and investors should refer to Section 5 for a more detailed summary of the risks.

Future capital requirements

The Company has no operating revenue and is unlikely to generate any operating revenue unless and until the Chilalo Graphite Project is successfully developed and production commences. Exploration and development costs and pursuit of its business plan will reduce the Company's current cash reserves and the amount raised under the Offers. Therefore, in order to successfully develop the Chilalo Graphite Project and for production to commence, the Company will require further financing

Section 5.1(a)

Page 12

Topic Summary More information

in the future, in addition to amounts raised pursuant to the Offers (particularly if only the Minimum Subscription is met).

Any additional equity financing may be dilutive to Shareholders, may be undertaken at lower prices than the Offer Price or may involve restrictive covenants which limit the Company's operations and business strategy. Debt financing, if available, may involve restrictions on financing and operating activities.

Although the Directors believe that additional capital can be obtained, no assurances can be made that appropriate capital or funding, if and when needed, will be available on terms favourable to the Company or at all. If the Company is unable to obtain additional financing as needed, it may be required to reduce the scope of its activities and this could have a material adverse effect on the Company's activities and could affect the Company's ability to continue as a going concern.

The Company may undertake additional offerings of Shares and of securities convertible into Shares in the future. The increase in the number of Shares issued and outstanding and the possibility of sales of such shares may have a depressive effect on the price of Shares. In addition, as a result of such additional Shares, the voting power of the Company's existing shareholders will be diluted.

Conditionality of Offers

The obligation of the Company to issue the Shares under the Offers is conditional on certain matters, as set out in Section 1.5. If the Conditions are not satisfied, the Company will not proceed with the Offers. Failure to complete the Offers may have a material adverse effect on the Company's financial position.

Section 5.1(b)

Potential for dilution

On completion of the Offers, assuming completion of the In-specie Distribution and the Maximum Subscription is reached, the number of Shares in the Company will increase from 20,000,000 to up to 55,000,000. This means the number of Shares on issue will increase by approximately 275% on completion of the Offers. On this basis, IMX Shareholders participating in the In-specie Distribution should note that if they do not participate in

Section 5.1(c)

Page 13

Topic Summary More information

the Offers (and even if they do), their holdings may be considerably diluted (as compared to their holdings and number of Shares on issue as at the date of this Prospectus).

Key personnel Recruiting and retaining qualified personnel are important to the Company's success. The number of persons skilled in the exploration and development of mining properties is limited and competition for such persons is strong. There can be no assurance given that there will be no detrimental impact on the Company if one or more key employees leave the Company.

Section 5.1(d)

Emerging markets The Company's main assets will be located in Tanzania. When conducting operations on foreign assets in emerging markets such as Tanzania, ASX listed entities may face a number of additional risks that companies with operations wholly within Australia may not face. For example, the ability to implement effective internal control and risk management systems and good corporate governance principles, having regard to the separation of executive management and the board from the location of the projects and the need to rely on consultants and professional advisors in those jurisdictions.

Section 5.1(e)

Joint venture parties, agents and contractors

The Directors are unable to predict the risk of financial failure or default by a participant in any joint venture to which the Company is or may become a party. Further, the Company is unable to predict the risk of insolvency or managerial failure by any of the contractors used by the Company in any of its activities or the insolvency or other managerial failure by any of the other service providers used by the Company for any activity. The effects of such failures may have an adverse effect on the Company's activities.

Section 5.1(f)

Termite administration

As announced by IMX to ASX on 21 September 2015, IMX received a letter of demand from the liquidators of Termite Resources NL (In liquidation) (Termite), which provided notice of a potential claim against directors and officers of Termite (some of whom are also IMX directors and officers), as well as against IMX itself.

Termite was wholly owned by an

Section 5.1(g)

Page 14

Topic Summary More information

incorporated joint venture entity in which IMX held a 51% interest. Termite held the joint venture's interests in the Cairn Hill iron ore mine in South Australia. On 19 June 2014, IMX announced the appointment of voluntary administrators to Termite. In September 2014, Termite's creditors voted to place it in liquidation.

IMX has previously announced the quantum of the potential claim is put in the alternative as the amount of the unsatisfied liabilities to unsecured creditors at the date of administration (mostly made up of damages claims from long term logistics creditors for early termination of their contracts on appointment of the administrators) said to be estimated at $75 million, alternatively about $46 million plus interest (being the amount repaid to the joint venture entity).

As at the date of this Prospectus the Termite liquidator has neither commenced proceedings against, nor given notice under the standstill agreement (see IMX announcement of 19 January 2016) of an intention to commence proceedings against IMX. IMX maintains that the potential claim by the liquidators is unlikely to succeed, and has determined to proceed with the entry into the Acquisition Agreement. Based on disclosures made by IMX and separate due diligence undertaken by the Company in relation to this matter, the Company has also determined to proceed with the entry into the Acquisition Agreement and the lodgement of this Prospectus.

The Company notes that as at the date of this Prospectus, there is no current or threatened civil litigation, arbitration proceedings or administrative appeals, or criminal or governmental prosecutions of a material nature in which the Company or its subsidiaries is directly or indirectly concerned which is likely to have a material adverse effect on the business or financial position of the Company or its subsidiaries.

Insurance risks The Company intends to put in place an insurance program aligned to the scale of its activities and in accordance with industry practice. However, there is no guarantee that such insurance or any future necessary coverage will be available to the Company at economically viable premiums (if at all)

Sections 5.1(h) and 5.1(i)

Page 15

Topic Summary More information

or that, in the event of a claim, the level of insurance carried by the Company now or in the future will be adequate, or that a liability or other claim would not materially and adversely affect the Company's business. Further, the occurrence of an event that is not covered or fully covered by insurance could have a material adverse effect on the business, financial condition and results of the Company.

Litigation risk The Company is subject to litigation risks. All industries, including the minerals exploration industry, are subject to legal claims, with and without merit. Defence and settlement costs of legal claims can be substantial, even with respect to claims that have no merit.

Due to the inherent uncertainty of the litigation process, the resolution of any particular legal proceeding to which the Company is or may become subject could have a material effect on its financial position, results of operations or the Company's activities.

Section 5.1(k)

Liquidity risk There can be no guarantee that there will be an active market for Shares or that the price of Shares will increase. There may be relatively few buyers or sellers of Shares on ASX at any given time. This may affect the volatility of the market price of Shares. It may also affect the prevailing market price at which Shareholders are able to sell their Shares. This may result in Shareholders receiving a market price for their Shares that is less or more than the price paid under the Offers.

Section 5.1(j)

Country risk The Prospecting Licences are for prospects located in Tanzania and the Company will be subject to the various political, economic and other risks and uncertainties associated with operating in that country. There are risks attached to exploration and mining operations in a developing country like Tanzania which are not necessarily present in a developed country like Australia, including: economic, social or political instability or change, hyperinflation, currency non-convertibility or instability and changes of law affecting government participation, taxation, working conditions, rates of exchange, exchange control, exploration licensing, export duties,

Section 5.2(a)

Page 16

Topic Summary More information

environmental protection, mine safety, labour relations as well as government control over mineral properties or government regulations that require the employment of local staff or contractors or require other benefits to be provided to local residents.

Logistics and infrastructure

The Chilalo Graphite Project in Tanzania is subject to logistical risk of a long supply line should there be a requirement to import materials and equipment from outside the continent of Africa. The Project is located in a remote area of south-eastern Tanzania where there are some infrastructure deficiencies.

While the Company intends to have access to the Mtwara port, which is 220km by road from Chilalo and the nearby Nachingwea airport is suitable for the transport of people and consumables, the Company will need to establish reliable road transport and sources of power and water in order for mining operations to be viable, none of which can be assured.

Owing to a shortage of skilled local personnel, the Company will engage expatriate workers to perform certain functions in Tanzania. In order to develop the Project, the Company will need to establish the facilities and material necessary to support operations in the remote location in which it is situated. The remoteness of the properties will also affect the potential viability of mining operations, as the Company will also need to establish more significant sources of power, water, physical plant and transport infrastructure in the area. The lack of availability of such sources may adversely affect mining feasibility and may, in any event, require the Company to arrange financing, locate adequate supplies and obtain necessary approvals from national and regional governments, none of which can be assured.

Section 5.2(b)

Tenement title Rights in relation to mining rights in Tanzania are governed by Tanzanian legislation. They are evidenced by the granting of licences. Each licence is for a specific term and carries with it annual expenditure and reporting commitments, as well as other conditions requiring compliance. Consequently, the Company,

Section 5.2(c)

Page 17

Topic Summary More information

through its subsidiary Ngwena Tanzania Limited, could lose title to or its interest in tenements if the licence conditions are not met or if insufficient funds are available to meet expenditure commitments as and when they arise, in line with the Tanzanian Mining legislation.

Tenements to be held by the Company or its subsidiaries are subject to periodic renewal. Renewal, although straightforward, is not automatic, and is subject to approval, which approval can be denied where a default notice has been issued. If any of the Prospecting Licences are not renewed, the Company may suffer significant damage through loss of the opportunity to develop any mineral resources on that licence.

Occupier's consent The title to mineral rights to be held by the Company may also be affected by the provisions of law which provide for the protection of lawful occupiers of the area. Where a mineral right granted to an applicant is over an area of land inhabited by lawful occupiers then the Company as holder of such a mineral right is required to obtain the lawful occupier's written consent, following necessary consultation, prior to exercising any of the rights conferred under its mineral right. Failure to obtain the lawful occupier's prior written consent would not invalidate the licence holder's mineral right but the lawful occupier may make a claim against the licence holder.

Section 5.2(d)

Environment and other regulatory risks

Environmental laws in Tanzania are strict. Every activity from exploration through to development and mining require compliance with the regulations for environmental protections by virtue of section 81 of the Environmental Management Act, 2004. Under section 81 an Environmental Impact Assessment Report is a mandatory requirement and the outcome of the assessment may be negative. It is expected that the Company's activities will have an impact on the environment, particularly at the time of advanced exploration and any mine development.

Environmental laws are dynamic and can change over time. The Company is unable to predict the effect of additional environmental laws and regulations that may be adopted in the future. Additional

Section 5.2(e)

Page 18

Topic Summary More information

laws or regulations may materially increase the Company's cost of doing business or affect its operations. The cost and complexity of complying with any additional environmental laws and regulations may prevent the Company from being able to develop potentially economically viable mineral deposits.

The Company and/or its subsidiaries will require other various governmental approvals and permits in Tanzania from time to time in connection with various aspects of its activities. To the extent such approvals or permits are required and not obtained, or are delayed, the Company may experience delays affecting its scheduled project development.

Exploration, development, mining and processing risks

The Chilalo Graphite Project is at the development stage, with a PFS completed in November 2015. The prospects of Graphex should be considered in light of the risks, expenses and difficulties frequently encountered by companies at this stage of development, particularly in the African region.

The business of mineral exploration, project development and production, by its nature, contains elements of significant risk with no guarantee of success. Ultimate and continuous success of these activities is dependent on many factors.

Despite the level of Mineral Resources currently estimated for the Project and the PFS providing the Company with confidence as to the potential of the Project, there can be no assurance that the Project will be brought into commercial production or that any additional exploration of the Prospecting Licences will result in the discovery of an economic mineral deposit. Even if a mineral deposit is identified, there is no certainty that it can be economically exploited. If exploration is successful, there will be additional costs and processes involved in transitioning to the development phase.

In the event that exploration development and exploration programmes prove to be unsuccessful, this could lead to a diminution in the value of the licences, a reduction in the base reserves of the Company and possible relinquishment of the licences.

Section 5.3(a)

Page 19

Topic Summary More information

Commodity price volatility and exchange rate risk

If the Company achieves success leading to mineral production, the revenue it will derive through the sale of product exposes the potential income of the Company to commodity prices and exchange rate risks. Commodity prices fluctuate and are affected by many factors beyond the control of the Company. Such factors include supply and demand for minerals, technological advancements, forward selling activities and other macro-economic factors.

In addition, unlike the majority of base and precious metals, there is no internationally recognised market for graphite nor is graphite an exchange traded commodity. As a result, there is a lack of market transparency associated with the price of graphite and there can be no assurance that the pricing included in the PFS represents a true market price.

Furthermore, prices of various commodities and services may be denominated in United States dollars or Tanzanian shillings, whereas the income and expenditure of the Company are and will be taken into account in Australian currency, exposing the Company to the fluctuations and volatility of the rate of exchange between the United States dollar and the Australian dollar and the Tanzanian shilling and the Australian dollar as determined in international markets.

Section 5.3(b)

Estimation of Mineral Resources and Ore Reserves

There is a degree of uncertainty to the estimation of Mineral Resources and Ore Reserves and corresponding grades being mined or dedicated to future production. Until Mineral Resources or Ore Reserves are actually mined and processed, the quantity of Mineral Resources and Ore Reserves must be considered as estimates only. In addition, the grade of Mineral Resources and Ore Reserves may vary depending on, among other things, graphite prices. Any material change in quantity and grades of Mineral Resources, Ore Reserves, or stripping ratio may affect the economic viability of the properties. There can be no assurance that metal recoveries in small-scale laboratory tests will be duplicated in larger scale tests under on-site conditions or during production.

Fluctuation in the price of graphite, results

Section 5.3(d)

Page 20

Topic Summary More information

of drilling, metallurgical testing and the evaluation of mine plans subsequent to the date of any mineral resource estimate may require revision of such estimate. Any material reductions in estimates of Mineral Resources and/or Ore Reserves, could have a material adverse effect on the Company's financial condition.

Directors, Related Party Interest and Substantial Holders

Who are the Directors?

The Directors are:

(a) Philip Hoskins – Director (and proposed Managing Director upon Listing);

(b) Stephen Dennis – Non-Executive Director and Chairman; and

(c) Grant Davey – Non-Executive Director.

"Corporate Directory" and Section 10.1

What experience do the Directors have?

Phil Hoskins is presently IMX's managing director, having been appointed to that role in October 2015 after a period of time serving as IMX's chief executive officer. Mr Hoskins will step down as IMX's managing director prior to the Company's admission to the official list of ASX. He is a senior executive with 14 years of broad finance and commercial experience across resources exploration, project development and production as well as large-scale property developments requiring debt and equity financing.

Stephen Dennis has been actively involved in the mining industry for over 30 years. He has held senior management positions at MIM Holdings Limited, Minara Resources Limited and Brambles Australia Limited. Until recently, Mr Dennis was the chief executive officer and managing director of CBH Resources Limited, the Australian subsidiary of Toho Zinc Co., Ltd of Japan.

Grant Davey holds a BSc Mining Engineering degree and has over 20 years of senior management and operational experience in the construction and operation of gold, platinum and coal mines in Africa, Australia, South America and Russia. More recently he has been involved in venture capital investments in several Canadian and

Section 10.2

Page 21

Topic Summary More information

Australian listed exploration and mining projects. He was the managing director of Cradle Resources Limited and founder and managing director of the Panda Hill niobium project in Tanzania which is expected to go into construction during 2016.

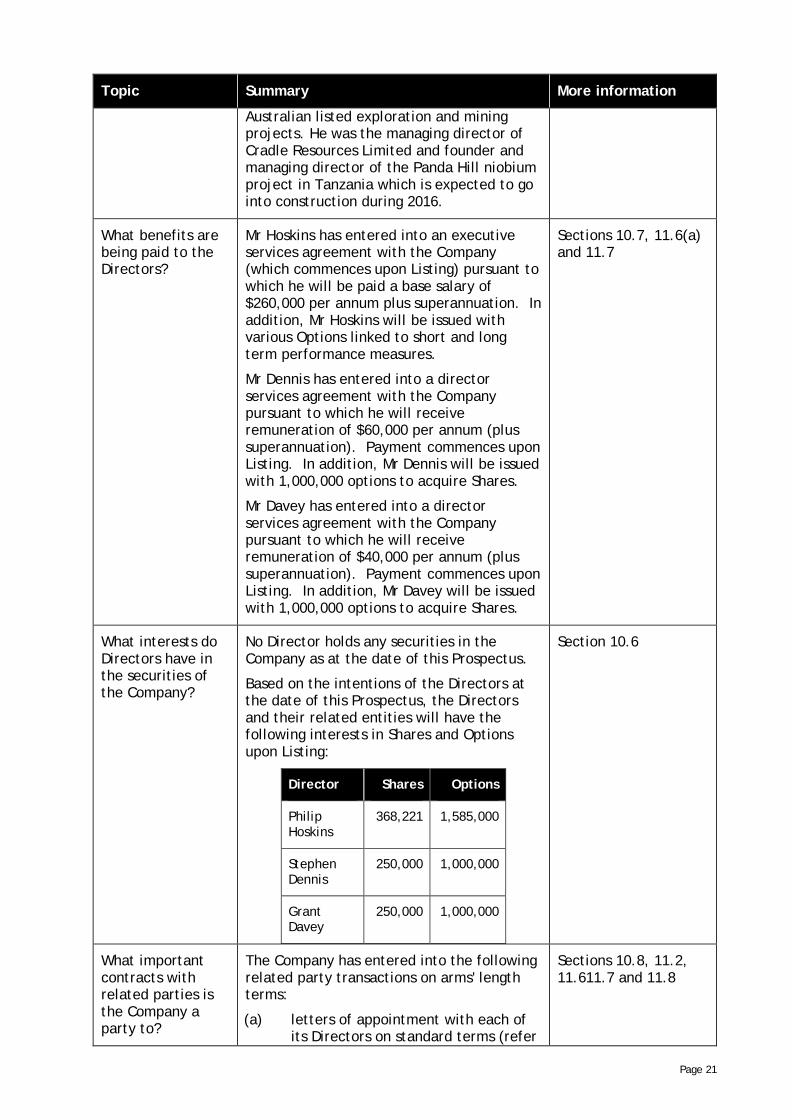

What benefits are being paid to the Directors?

Mr Hoskins has entered into an executive services agreement with the Company (which commences upon Listing) pursuant to which he will be paid a base salary of $260,000 per annum plus superannuation. In addition, Mr Hoskins will be issued with various Options linked to short and long term performance measures.

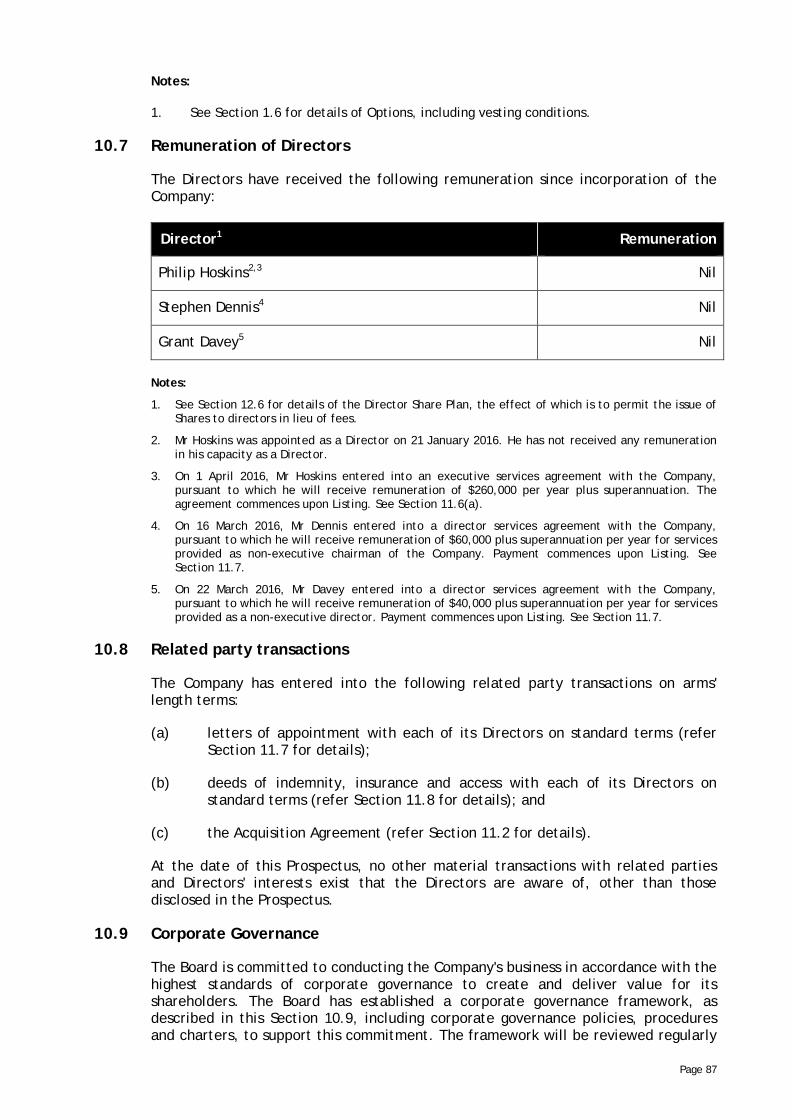

Mr Dennis has entered into a director services agreement with the Company pursuant to which he will receive remuneration of $60,000 per annum (plus superannuation). Payment commences upon Listing. In addition, Mr Dennis will be issued with 1,000,000 options to acquire Shares.

Mr Davey has entered into a director services agreement with the Company pursuant to which he will receive remuneration of $40,000 per annum (plus superannuation). Payment commences upon Listing. In addition, Mr Davey will be issued with 1,000,000 options to acquire Shares.

Sections 10.7, 11.6(a) and 11.7

What interests do Directors have in the securities of the Company?

No Director holds any securities in the Company as at the date of this Prospectus.

Based on the intentions of the Directors at the date of this Prospectus, the Directors and their related entities will have the following interests in Shares and Options upon Listing:

Director Shares Options

Philip Hoskins

368,221 1,585,000

Stephen Dennis

250,000 1,000,000

Grant Davey

250,000 1,000,000

Section 10.6

What important contracts with related parties is the Company a party to?

The Company has entered into the following related party transactions on arms' length terms:

(a) letters of appointment with each of its Directors on standard terms (refer

Sections 10.8, 11.2, 11.611.7 and 11.8

Page 22

Topic Summary More information

Section 11.7 for details);

(b) deeds of indemnity, insurance and access with each of its Directors on standard terms (refer Section 11.8 for details);

(c) the Acquisition Agreement (refer Section 11.2 for details).

Who are the additional key management personnel?

The key management personnel are:

(a) Stuart McKenzie – Commercial Manager and Company Secretary;

(b) Nicholas Corlis – General Manager Technical; and

(c) Christopher Knee – Chief Financial Officer.

Sections 10.3 and 10.4

Who will be the substantial holders of the Company?

As at the date of this Prospectus the Company is a wholly-owned subsidiary of IMX.

Based on the information known as at the date of this Prospectus, and assuming the Minimum Subscription is achieved, on Admission only MMG Exploration Holdings Limited will have an interest in 5% or more of the Shares on issue, with a holding of approximately 8.60%.

Investors should note the details above do not include any IMX Shareholder who participates in the IMX Offer.

Section 12.7

What are the Offers?

What are the Offers?

This Prospectus is for a conditional initial public offering of a minimum of 21,250,000 and up to a maximum of 35,000,000 fully paid ordinary shares in the Company.

The offers comprise a public General Offer, which also incorporates the IMX Offer to Eligible IMX Shareholders (together, Offers).

Loyalty Options with an exercise price of $0.25 each and an expiry date 3 years from the Issue Date will be issued free attaching on a 1 for 3 basis to every person issued Shares under the General Offer.

The Shares being offered will represent approximately 51.5% of the issued capital of the Company at Admission on a Minimum Subscription basis and approximately 64% of the issued capital of the Company at Admission on a Maximum Subscription basis.

Sections 1.1, 1.2 and 1.6

Page 23

Topic Summary More information

What is the Offer Price?

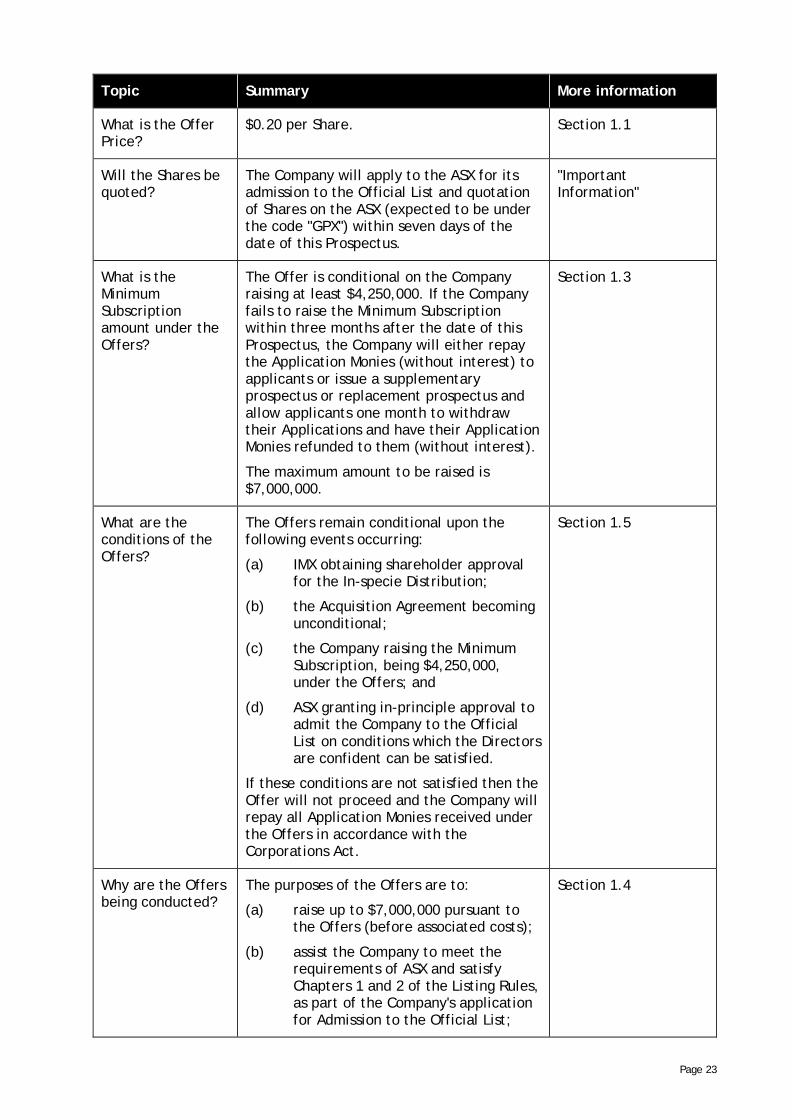

$0.20 per Share. Section 1.1

Will the Shares be quoted?

The Company will apply to the ASX for its admission to the Official List and quotation of Shares on the ASX (expected to be under the code "GPX") within seven days of the date of this Prospectus.

"Important Information"

What is the Minimum Subscription amount under the Offers?

The Offer is conditional on the Company raising at least $4,250,000. If the Company fails to raise the Minimum Subscription within three months after the date of this Prospectus, the Company will either repay the Application Monies (without interest) to applicants or issue a supplementary prospectus or replacement prospectus and allow applicants one month to withdraw their Applications and have their Application Monies refunded to them (without interest).

The maximum amount to be raised is $7,000,000.

Section 1.3

What are the conditions of the Offers?

The Offers remain conditional upon the following events occurring:

(a) IMX obtaining shareholder approval for the In-specie Distribution;

(b) the Acquisition Agreement becoming unconditional;

(c) the Company raising the Minimum Subscription, being $4,250,000, under the Offers; and

(d) ASX granting in-principle approval to admit the Company to the Official List on conditions which the Directors are confident can be satisfied.

If these conditions are not satisfied then the Offer will not proceed and the Company will repay all Application Monies received under the Offers in accordance with the Corporations Act.

Section 1.5

Why are the Offers being conducted?

The purposes of the Offers are to:

(a) raise up to $7,000,000 pursuant to the Offers (before associated costs);

(b) assist the Company to meet the requirements of ASX and satisfy Chapters 1 and 2 of the Listing Rules, as part of the Company's application for Admission to the Official List;

Section 1.4

Page 24

Topic Summary More information

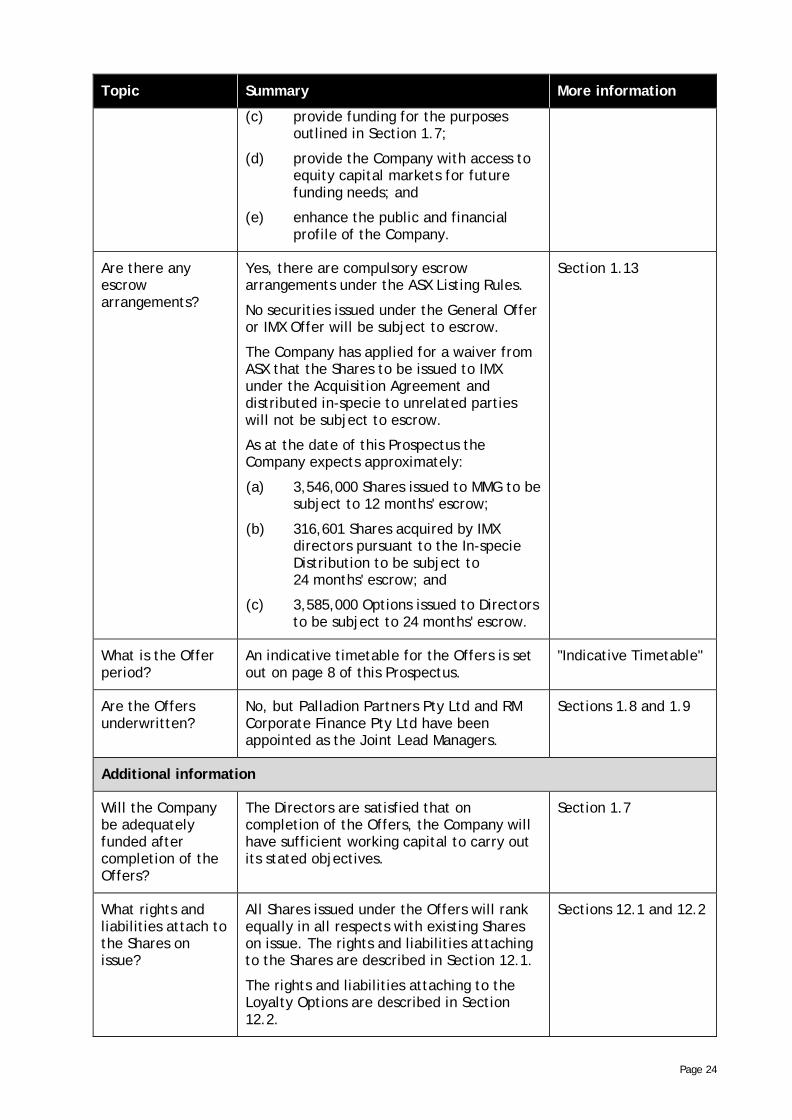

(c) provide funding for the purposes outlined in Section 1.7;

(d) provide the Company with access to equity capital markets for future funding needs; and

(e) enhance the public and financial profile of the Company.

Are there any escrow arrangements?

Yes, there are compulsory escrow arrangements under the ASX Listing Rules.

No securities issued under the General Offer or IMX Offer will be subject to escrow.

The Company has applied for a waiver from ASX that the Shares to be issued to IMX under the Acquisition Agreement and distributed in-specie to unrelated parties will not be subject to escrow.

As at the date of this Prospectus the Company expects approximately:

(a) 3,546,000 Shares issued to MMG to be subject to 12 months' escrow;

(b) 316,601 Shares acquired by IMX directors pursuant to the In-specie Distribution to be subject to 24 months' escrow; and

(c) 3,585,000 Options issued to Directors to be subject to 24 months' escrow.

Section 1.13

What is the Offer period?

An indicative timetable for the Offers is set out on page 8 of this Prospectus.

"Indicative Timetable"

Are the Offers underwritten?

No, but Palladion Partners Pty Ltd and RM Corporate Finance Pty Ltd have been appointed as the Joint Lead Managers.

Sections 1.8 and 1.9

Additional information

Will the Company be adequately funded after completion of the Offers?

The Directors are satisfied that on completion of the Offers, the Company will have sufficient working capital to carry out its stated objectives.

Section 1.7

What rights and liabilities attach to the Shares on issue?

All Shares issued under the Offers will rank equally in all respects with existing Shares on issue. The rights and liabilities attaching to the Shares are described in Section 12.1.

The rights and liabilities attaching to the Loyalty Options are described in Section 12.2.

Sections 12.1 and 12.2

Page 25

Topic Summary More information

What are the tax implications of investing in Securities under the Offers?

The tax consequences of any investment in Securities under the Offers will depend upon your particular circumstances.

Prospective investors should obtain their own tax advice before deciding to invest.

Section 1.18

Who is eligible to participate in the Offers?

The General Offer is open to all investors with a registered address in Australia and certain qualifying investors in Hong Kong, Mauritius, Singapore and the UK to whom such an offer can be lawfully made.

The IMX Offer is open to IMX Shareholders registered on a record date of 8 April 2016.

Sections 1.1 and 1.16

How do I apply for Shares under the Offers?

Applications for Shares under the Offers must be made by completing the relevant Application Form in accordance with the instructions.

Applicants for Shares under the General Offers may pay by cheque only and payments must be in Australian dollars for the full amount of the Application, being the number of Shares applied for multiplied by $0.20 per Share.

Applicants for Shares under the IMX Offer may pay by BPAY® or by cheque and payments must be in Australian dollars for the full amount of the Application, being the number of Shares applied for multiplied by $0.20 per Share.

Investors are not required to take any action to receive Loyalty Options.

Section 1.10

What is the allocation policy?

Whilst priority will be given to Eligible IMX Shareholders, the Directors will allocate Shares at their sole discretion with a view to ensuring an appropriate Shareholder base for the Company going forward.

There is no assurance that any applicant will be allocated any Shares, or the number of Shares for which it has applied.

Section 1.11

When will I receive confirmation that my Application has been successful?

It is expected that holding statements will be sent to successful applicants by post on or about 13 May 2016.

"Indicative Timetable"

What is the Company's dividend policy?

The Company does not expect to pay dividends in the near future as its focus will primarily be on using cash reserves to develop the Chilalo Project.

Section 2.4

Page 26

Topic Summary More information

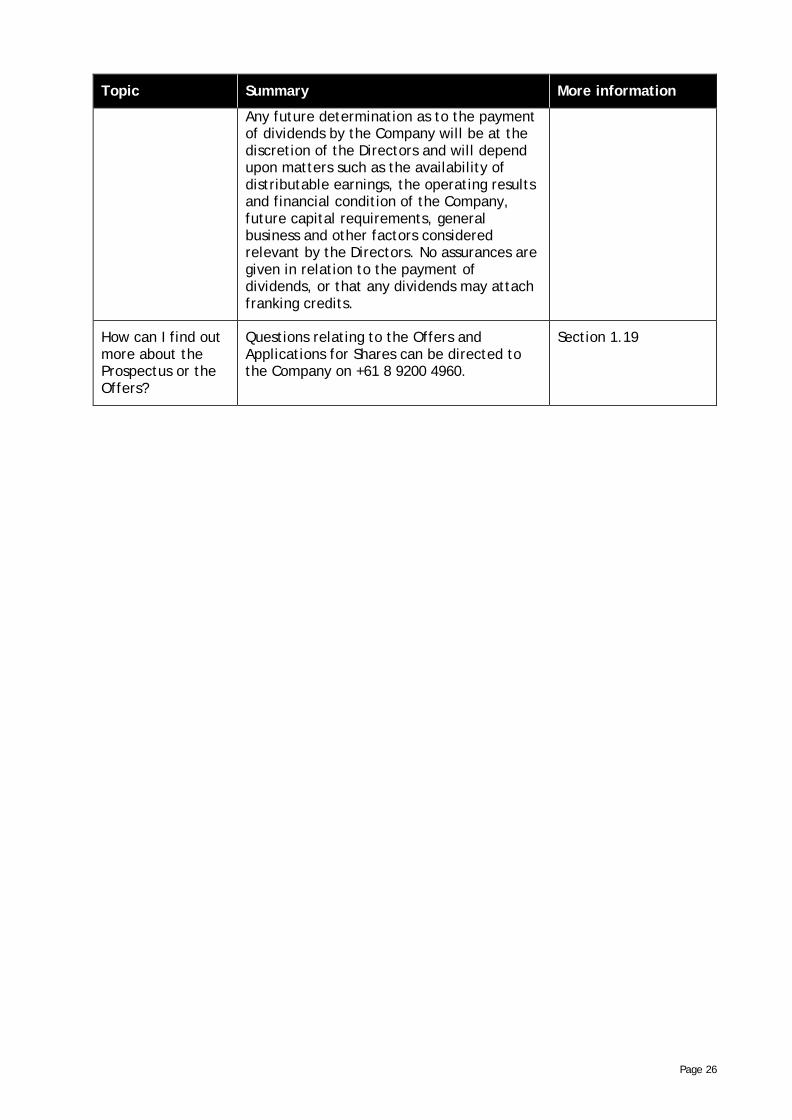

Any future determination as to the payment of dividends by the Company will be at the discretion of the Directors and will depend upon matters such as the availability of distributable earnings, the operating results and financial condition of the Company, future capital requirements, general business and other factors considered relevant by the Directors. No assurances are given in relation to the payment of dividends, or that any dividends may attach franking credits.

How can I find out more about the Prospectus or the Offers?

Questions relating to the Offers and Applications for Shares can be directed to the Company on +61 8 9200 4960.

Section 1.19

Page 27

1. Details of the Offers

1.1 General Offer and IMX Offer

This Prospectus invites potential investors to apply for up to 35,000,000 Shares at an issue price of $0.20 each to raise up to $7,000,000 (before associated costs).

The Offers comprise a public General Offer, which also incorporates the IMX Offer to Eligible IMX Shareholders (together, Offers).

The Company is offering Eligible IMX Shareholders the opportunity to subscribe for Graphex Shares through a priority offer (IMX Offer). Whilst priority will be given to Eligible IMX Shareholders, the Directors will allocate Shares at their sole discretion with a view to ensuring an appropriate Shareholder base for the Company going forward. While it is intended that as many Eligible IMX Shareholders as possible receive at least the minimum allocation of 10,000 Shares ($2,000) under the IMX Offer, there is no guarantee that all Eligible IMX Shareholders will have their Applications accepted in full. Eligible IMX Shareholders are encouraged to submit an IMX Offer Application Form as soon as possible.

Applications from Eligible IMX Shareholders which are not accepted by the Company by the IMX Offer Closing Date will be issued to applicants under the General Offer. The IMX Offer closes five days before the General Offer closes, to facilitate this process.

The Shares to be issued pursuant to the Offers are of the same class and will rank equally in all respects with the existing Shares in the Company. The rights and liabilities attaching to the Shares are further described in Section 12.1 of the Prospectus.

Applications for Shares under the General Offer must be made on the General Offer Application Form accompanying this Prospectus and received by the Company on or before the General Offer Closing Date. Persons wishing to apply for Shares under the General Offer should refer to Section 1.10(a) for further details and instructions.

Applications for Shares under the IMX Offer must be made on the IMX Offer Application Form accompanying this Prospectus and received by the Company on or before the IMX Offer Closing Date. Persons wishing to apply for Shares under the IMX Offer should refer to Section 1.10(b) for further details and instructions.

1.2 Loyalty Options

The Company is issuing 1 free Loyalty Option for every 3 Shares issued pursuant to this Prospectus. For the avoidance of doubt IMX Shareholders who will receive Shares pursuant to the In-specie Distribution will not and are not entitled to receive Loyalty Options.

Fractional entitlements will be rounded down to the nearest whole number.

The issue of Loyalty Options will be made to those investors who are issued Shares pursuant to the Offers. Those investors are not required to take any action to receive Loyalty Options. The Loyalty Options will be issued to those investors on the Issue Date.

The Loyalty Options are subject to a vesting condition that the Loyalty Option holder hold Shares on the 'Vesting Date' (being the date that is 3 months following the

Page 28

commencement of trading of Graphex's Shares on ASX), with the number vesting equal to the lesser of:

(a) the number of Loyalty Options held on the Vesting Date; and

(b) the number of Shares held on the Vesting Date divided by 3,

(Vesting Condition).

Unvested Loyalty Options will lapse on the Vesting Date.

An illustration of how the Vesting Condition operates with various examples of transactions undertaken by Loyalty Option holders prior to the Vesting Date is set out below:

No. Shares held on Issue Date

90,000 90,000 90,000 90,000 90,000

No. Loyalty Options issued

30,000 30,000 30,000 30,000 30,000

Transactions completing before Vesting Date

No transactions

Shareholder purchases

10,000 Shares before

Vesting Date

Shareholder sells 30,000

Shares before the

Vesting Date

Shareholder sells 45,000 Shares then purchases

45,000 Shares before

Vesting Date

Shareholder sells 40,000 Shares then purchases

10,000 Shares before

Vesting Date

No. Shares held on Vesting Date

90,000 100,000 60,000 90,000 60,000

No. of Loyalty Options that vest

30,000 30,000 20,000 30,000 20,000

No. Loyalty Options that lapse

Nil Nil 10,000 Nil 10,000

Reason Same number of Shares held therefore all Loyalty Options vest.

Shareholders who purchase additional Shares such that their shareholding at the Vesting Date is greater than their holding at the Issue Date are not entitled to

Number of Shares held divided by 3 is now less than number of Loyalty Options on Vesting Date.

Same number of Shares held therefore all Loyalty Options vest.

Number of Shares held divided by 3 is now less than number of Loyalty Options on Vesting Date.

Page 29

additional Loyalty Options.

Up to the Vesting Date the Loyalty Options are non-transferable. Following the Vesting Date the Loyalty Options will become transferable.

The rights and liabilities of the Loyalty Options issued under this Prospectus are set out in Section 12.2.

1.3 Minimum Subscription

The minimum level of subscription for the Offers is 21,250,000 Shares to raise $4,250,000 (before costs) (Minimum Subscription).

None of the Shares offered under this Prospectus will be issued if Applications are not received for the Minimum Subscription. Should Applications for the Minimum Subscription not be received within three months from the date of this Prospectus, the Company will either repay the Application Monies (without interest) to applicants or issue a supplementary prospectus or replacement prospectus and allow applicants one month to withdraw their Applications and have their Application Monies refunded to them (without interest).

1.4 Purpose of the Offers

This Prospectus has been issued for the purposes of:

(a) raising up to $7,000,000 pursuant to the Offers (before associated costs);

(b) assisting the Company to meet the requirements of ASX and satisfy Chapters 1 and 2 of the Listing Rules, as part of the Company's application for Admission to the Official List;

(c) providing funding for the purposes outlined in Section 1.7;

(d) providing the Company with access to equity capital markets for future funding needs; and

(e) enhancing the public and financial profile of the Company.

1.5 Conditional

The Offers under this Prospectus are conditional upon the following events occurring:

(a) IMX obtaining shareholder approval for the In-specie Distribution;

(b) the Acquisition Agreement becoming unconditional;

(c) the Company raising the Minimum Subscription, being $4,250,000, under the Offers (refer to Section 1.3); and

(d) ASX granting in-principle approval to admit the Company to the Official List on conditions which the Directors are confident can be satisfied.

Page 30

If these conditions are not satisfied then the Offers will not proceed and the Company will repay all Application Monies received under the Offers in accordance with the Corporations Act.

1.6 Capital structure

The proposed pro forma capital structure of the Company following completion of the Offers is as follows:

No. of Shares (Minimum

Subscription)

% of Shares

No. of Shares (Maximum

Subscription)

% of Shares

Shares issued to IMX Shareholders pursuant to the In-Specie Distribution

16,454,000 39.9% 16,454,000 30.0%

Shares issued to MMG* 3,546,000 8.6% 3,546,000 6.0%

Shares to be issued pursuant to the Offers

21,250,000 51.5% 35,000,000 64.0%

Total Shares on issue at the listing date

41,250,000 100% 55,000,000 100%

* MMG is a party to a joint venture agreement with IMX, pursuant to which it holds a 14.12% interest in the Company’s tenement holdings (including the Prospecting Licences, which are the subject of the Acquisition Agreement) on the Nachingwea Property in Tanzania. MMG currently holds its interest in such tenement holdings, through its shareholding in a UK incorporated joint venture company (UK JV Co). On completion of the Offers and Acquisition Agreement, MMG will no longer hold its interest in the Prospecting Licences through UK JV Co, but will hold its interest through a shareholding in Graphex of 3,546,000 Shares. In accordance with the Listing Rules, the Shares issued to MMG will be subject to a 12 month escrow period. See Sections 3.1(a) and 11.2 for further information.

No. of Options (Minimum

Subscription)

% of Options

No. of Options

(Maximum Subscription)

% of Options

Options on issue as at the date of the Prospectus

Nil 0% Nil 0%

Loyalty Options to be issued pursuant to this Prospectus

7,083,333 39% 11,666,667 49%

Adviser Options to be issued1

4,440,921 25% 5,927,359 25%

Director and Employee Options to be issued2

6,437,957 36% 6,437,957 27%

Total Options on issue at the listing date

17,962,211 100% 24,031,983 100%

Page 31

Notes:

1. Unquoted options exercisable at $0.25 each and expiring 3 years from the date of issue to be issued to the Joint Lead Managers and the Corporate Advisor. See Section 12.3 for the terms of issue of the Advisor Options.

2. Unquoted options to be issued to Directors and employees as follows:

(i) 1,000,000 options exercisable at $0.20 each and expiring 3 years from the date the Company is admitted to the Official List, to be issued to director Stephen Dennis;

(ii) 1,000,000 options exercisable at $0.20 each and expiring 3 years from the date the Company is admitted to the Official List, to be issued to director Grant Davey;

(iii) 350,000 options exercisable at $0.20 each and expiring 3 years from the date the Company is admitted to the Official List, to be issued to director Phil Hoskins;

(iv) 650,000 options exercisable at $0.20 each and expiring 3 years from the date the Company is admitted to the Official List, to be issued to executives and employees;

(v) 520,000 options with a nil exercise price, expiring 3 years from the date the Company is admitted to the Official List and vesting on 1 July 2017, subject to performance against KPIs relating to health and safety, securing of offtake and financing agreements, delivery of a DFS in accordance with board approved budget and timeline, completion of Project permitting and ensuring the Company is sufficiently funded to deliver on its strategy, to be issued to director Phil Hoskins as short term incentives for the period to 30 June 2017;

(vi) 594,319 options with a nil exercise price, expiring 3 years from the date the Company is admitted to the Official List and vesting on 1 July 2017, subject to performance against KPIs relating to health and safety, securing of offtake and financing agreements, delivery of a DFS in accordance with board approved budget and timeline, completion of Project permitting and ensuring the Company is sufficiently funded to deliver on its strategy, to be issued to executives and employees as short term incentives for the period to 30 June 2017;

(vii) 715,000 options with a nil exercise price, expiring 5 years from the date the Company is admitted to the Official List, with one third vesting on each of 1 July 2017, 1 July 2018 and 1 July 2019, subject to achievement of key project milestones including execution of binding offtake and project financing agreements, commencement of commercial production and share price performance, to be issued as long term incentives to director Phil Hoskins; and

(viii) 1,608,638 options with a nil exercise price, expiring 5 years from the date on which the Company is admitted to the Official List, with one third vesting on each of 1 July 2017, 1 July 2018 and 1 July 2019, subject to achievement of key project milestones including execution of binding offtake and project financing agreements, commencement of commercial production and share price

Page 32

performance, to be issued as long term incentives to executives and employees.

1.7 Proposed use of funds

Following the Offers, it is anticipated that the following funds will be available to the Company:

Source of funds Minimum Subscription

$ million

Maximum Subscription

$ million

Existing cash as at the date of this Prospectus - -

Proceeds from Offers 4.25 7.00

Total funds available 4.25 7.00

The Company intends to apply the funds raised from the Offers as follows:

Use of funds Minimum Subscription

$ million

Maximum Subscription

$ million

Cash purchase price payment to IMX 1.00 1.00

Transaction costs1 0.56 0.74

Corporate and administration costs 0.97 0.97

Tenement costs 0.05 0.05

Feasibility costs 1.08 3.30

Offtake marketing costs 0.30 0.40

Working capital 0.29 0.54

TOTAL 4.25 7.00

Notes:

1. Expenses paid or payable by the Company in relation to the Offers are set out in Section 12.11.

The above table is a statement of current intentions as at the date of this Prospectus. Investors should note that, as with any budget, the allocation of funds set out in the above table may change depending on a number of factors, including the outcome of offtake marketing and development activities, studies, regulatory developments and market and general economic conditions. In light of this, the Board reserves the right to alter the way the funds are applied.

The Board is satisfied that upon completion of the Offers, the Company will have sufficient working capital to meet its stated objectives. The Minimum Subscription is based on the Company's minimum working capital requirements in order to execute its planned strategy for the next 12 months, which includes securing binding offtake

Page 33

agreements and the commencement of a definitive feasibility study (DFS). The use of funds is based on known actual salary costs and administration costs, a high-level third party-prepared estimate of DFS costs, exploration plans and known transaction and broker costs based on executed mandates.

The variance in the use of funds is due to the following factors:

(a) the Minimum Subscription is based on the Company's minimum working capital requirements in order to execute its planned strategy for the next 12 months, however if the Maximum Subscription is raised this is expected to exceed 12 months; and

(b) under the Maximum Subscription the Company is funded to complete a DFS, however the Company does not expect to commence a DFS in either the Minimum Subscription or Maximum Subscription scenario unless and until offtake and financing agreements for the development of the Chilalo Project are in place. Should such offtake and/or financing agreements include provision for third party funding of a DFS, the Company may not be required to use funds from the Maximum Subscription for the DFS, with those additional funds likely to be directed to working capital or eventually towards Project construction.

The use of further equity funding may be considered by the Board where it is appropriate to accelerate a specific project or strategy.

In the event the Company raises between the Minimum and Maximum Subscription, funds will be apportioned on a pro-rata basis.

1.8 Underwriting

The Offers are not underwritten.

1.9 Joint Lead Managers

Palladion Partners Pty Ltd and RM Corporate Finance Pty Ltd have been appointed as Joint Lead Managers to the Offers on the terms and conditions summarised in Section 11.3 of this Prospectus.

1.10 Applications

(a) General Offer

(i) Payment by cheque

Applications for Shares under the General Offer can be made using the General Offer Application Form accompanying this Prospectus. The General Offer Application Form must be completed in accordance with the instructions set out on the form.

Applications under the General Offer must be for a minimum of 10,000 Shares ($2,000) and then in increments of 2,500 Shares ($500). No brokerage, stamp duty or other costs are payable by applicants. Cheques must be made payable to "Graphex Mining Limited – Application Account" and should be crossed "Not Negotiable". All Application Monies will be paid into a trust account.

Page 34

Completed General Offer Application Forms and accompanying cheques must be received by the Share Registry before 5.00pm WST on the General Offer Closing Date by post to the following address:

By post Computershare Investor Services Pty Limited GPO BOX 52 Melbourne Victoria 3001 Australia

Applicants are urged to lodge their General Offer Application Forms as soon as possible as the General Offer may close early without notice.

An original, completed and lodged General Offer Application Form together with a cheque for the Application Monies, constitutes a binding and irrevocable offer to subscribe for the number of Shares specified in the General Offer Application Form. The General Offer Application Form does not need to be signed to be valid. If the General Offer Application Form is not completed correctly or if the accompanying payment is for the wrong amount, it may be treated by the Company as valid. The Directors' decision as to whether to treat such an Application as valid and how to construe amend or complete the General Offer Application Form is final; however an applicant will not be treated as having applied for more Shares than is indicated by the amount of the cheque for the Application Monies.

It is the responsibility of applicants outside Australia to obtain all necessary approvals for the allotment and issue of Shares pursuant to this Prospectus. The return of a completed General Offer Application Form will be taken by the Company to constitute a representation and warranty by the applicant that all relevant approvals have been obtained.

(b) IMX Offer

Applications for Shares under the IMX Offer can only be made using the IMX Offer Application Form, which will be mailed to the IMX Shareholders who are registered as an IMX Shareholder on the IMX Offer Record Date, and therefore eligible to participate in the IMX Offer. The IMX Offer is not renounceable and it cannot be transferred.

The IMX Offer is not a rights issue or entitlement offer. IMX Shareholders on the Record Date may apply for as many Graphex Shares as they wish, noting the minimum application amount of $2,000 and that final allocations will be subject to Board discretion.

Whilst priority will be given to Eligible IMX Shareholders, the Directors will allocate Shares at their sole discretion with a view to ensuring an appropriate Shareholder base for the Company going forward. While it is intended that as many Eligible IMX Shareholders as possible receive at least the minimum allocation of 10,000 Shares ($2,000) under the IMX Offer, there is no guarantee that all Eligible IMX Shareholders will have their Applications

Page 35

accepted in full. Eligible IMX Shareholders are encouraged to submit an IMX Offer Application Form as soon as possible.

Any Shares which are not applied for by Eligible IMX Shareholders by the IMX Offer Closing Date and accepted by the Company, will be issued to applicants under the General Offer. The IMX Offer closes five days before the General Offer closes, to facilitate this process.

The IMX Offer Application Form must be completed in accordance with the instructions set out on the form.

IMX Offer Application Forms must not be circulated to prospective investors unless accompanied by a copy of this Prospectus.

Applications under the IMX Offer must be for a minimum of 10,000 Shares ($2,000) and then in increments of 2,500 Shares ($500). No brokerage, stamp duty or other costs are payable by applicants.

Eligible IMX Shareholders may pay by BPAY® or cheques. Eligible IMX Shareholders are encouraged to pay by BPAY®.

(i) Payment by BPAY®

Eligible IMX Shareholders who elect to pay by BPAY® must follow the instructions for BPAY® described in the IMX Offer Application Form (which includes the biller code and your unique customer reference number). Please note that should you choose to pay by BPAY® payment:

(A) you do not need to submit the personalised IMX Offer Application Form but are taken to make the statements and declarations on that form; and

(B) you are deemed to have applied for such whole number of Shares which is covered in full by your application money.

When completing your BPAY® payment, please make sure to use the specific Biller Code and unique reference number provided on your personalised IMX Offer Application Form.

You should be aware that your own financial institution may implement earlier cut-off times with regard to electronic payment, and you should therefore take this into consideration when making payment. It is your responsibility to ensure that funds submitted through BPAY® are received by 5.00pm WST on the IMX Offer Closing Date.

(ii) Payment by cheque

Cheques must be made payable to "Graphex Mining Limited – Application Account" and should be crossed "Not Negotiable". All Application Monies will be paid into a trust account.