Grain marketing strategies 2 - Marty Hibbs, Grain Merchandiser

Upload

dhagenmaierCategory

view

146download

0

Marketing Basics1

Mark NelsonKansas Farm Bureau

(785) [email protected]

www.kfb.org

Marketing 101February 5, 2015

http://futuresfundamentals.com/basics-introduction-to-risk.html

Marketing Basics2

Marketing 101February 5, 2015

http://futuresfundamentals.com/basics-introduction-to-risk.html

$1.00

Futures and Futures Markets

Cash Bids/BasisPreharvest PricingShort Futures

Hedge & Forward Contracts

Marketing Basics3

1) Futures Prices (market determined)2) Cash Bids/Basis (an industry determined

relationship to futures)

Basis = cash bid – futures Quality: test weight, protein, oil content

Marketing 101: Understanding Prices

Storage

$4.35 – $4.55 ($0.20) =

+ ($0.20) =

Supply & Demand

Marketing Basics4

Become a “Student of Basis”

B ($0.35)A ($0.80)

D ($0.50)Mill $0.05

C ($0.10)KCBT $6.50

? Sell Where ?

Marketing Basics

5

Futures MarketsWhere all market participants are represented, underlying commodity information is shared and debated, and

. . . . . . . . . . commodity price is discovered. The CBT (1848) & KCBT (1856) were initially “cash” markets. “Standardized” forward contracts soon followed.

Trading floor of the KCBT, 1877

Marketing Basics6

In the 1860’s, the first Futures Contracts were developed

. . . . and because of this an important secondary function of futures markets evolved,

. . . . . . . the management of price risk;which separated price establishment from grain delivery.

• A binding commitment to deliver (sell) or receive (buy) at a standard location (i.e. KC)

• A standardized amount (i.e. 5,000 bu.)• Of a standardized quality (i.e. #2 HRW)• During a standardized delivery month (for

wheat; Jul, Sep, Dec, Mar or May)• With price determined by open outcry

• Or more likely, Electronic Trading Technology

Futures Contract

Marketing Basics7

Using the Futures Market(to manage price risk)

Clearing Members

LowHigh

Futures contracts are “time certain;” i.e. the July KCBT wheat futures contract expires in the month of July.

If you initially “sold” a July KCBT wheat futures contract; then prior to expiration, you need to “buy” a July contract back.

If you initially “bought” a July KCBT wheat futures contract; then prior to expiration, you need to “sell” a July contract back.

We do this by placing orders through clearing members.

Marketing Basics8

Trading FuturesAs futures prices change,

the “value” of your position also changes. (Buy Low; Sell High)

Let’s assume we initially Sold @ $6.60

And then prices fell to $5.60; we’d be up $1.00; or $5,000/contract

($33,000 - $28,000).

@ $6.20, are we up or down from our initial position?

What if we’d initially “bought”

@ $6.60?

Marketing Basics9

Q-T 1. Studying the Effects of Futures Price ChangesPart 1

Initial Current Gain orPosition Price Loss

sell @ $3.50 3.00$ $ 0.50sell @ $3.50 4.00$ $_______sell @ $2.85 2.60$ $_______sell @ $2.85 2.90$ $_______sell @ $64.25 63.00$ $_______buy @ $78.15 79.15$ $_______buy @ $78.15 80.15$ $_______

(0.50)0.25(0.05)1.251.002.00

Remember: Buy Low and Sell High

Marketing Basics10

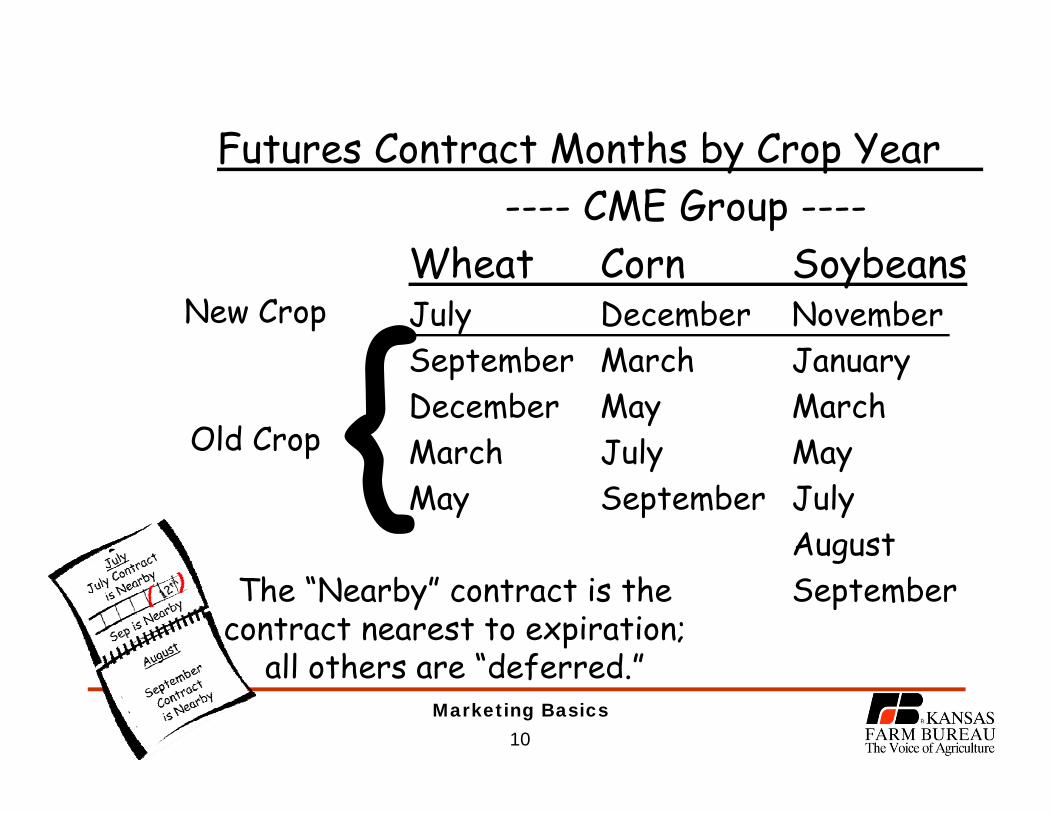

Futures Contract Months by Crop Year---- CME Group ----

Wheat Corn SoybeansJuly December November September March January December May MarchMarch July MayMay September July

AugustSeptember

Old Crop

The “Nearby” contract is the contract nearest to expiration;

all others are “deferred.”

New Crop

Marketing Basics11

Month – The contract delivery month.

Last – The last price traded (after trading hours, it is the day’s close or settlement.

Chg – The price change from the previous trading session’s close.

Open – The price traded when the market opened.

High/Low – The highest and lowest prices traded this trading session.

Futures Contract Terminology

Nearby >all others

are deferred

Marketing Basics12

Futures Market Participants

a) Hedgers (commercials), entities that use the futures market to manage price risk. Farmers/Ranchers/Feeders (Ag producers) Grain Elevators (handlers) Millers (wheat processors) Ethanol Plants (feedgrain processors) Importing and exporting companies/countries

b) Speculators (non-commercials), entities that accept price risk by buying and/or selling futures contracts in order to profit in the changes in price.

Marketing Basics13

New Participants: Hedge, Pension and Investment funds – While a very small percentage is invested in agriculture, it still represents 100’s of billions of dollars, and can impact markets.New Products: Commodity Price Indices – Fixed-

weight or weighted averages of selected commodity futures. Basically “investment” tools normally aimed at “buying

and holding” commodities. Example, S&P-GSCI – (Goldman Sachs Commodity

Index) 24 liquid, exchange-traded futures contracts including energy, metals, crops and livestock.

Marketing Basics14

Can We Trust Futures Exchanges and Contracts?

Futures exchanges regulate themselves by enforcing both federal laws & regulations, and exchange-based rules.CFTC provides market

surveillance along with enforcement of laws and regulations.

Yes, and it’s in our best interest to monitor and

maintain them.

Marketing Basics15

The BEST Synopsis of the Issues Not “political.”Great summary of the research and recent actions, with some analysis along with details, definitions and explanations.

Conclusions:1)Index funds have caused structural changes in OI and composition.

2)CFTC, the exchanges and market participants are adapting and volatility is easing.

3)Time and more research is necessary.

Are Futures Markets Manipulated?

Marketing Basics16

Questions About Futures?

Marketing Basics17

Basis, the Cash minus Futures Relationship

June 20th

KC HRW + Basis = CashJuly $5.00 ($0.25) $4.75 September $5.10 ($0.35) $December $5.20 ($0.45) $March $5.30 ($0.55) $May $5.40 ($0.65) $July $5.20 ($0.25) $4.95

Marketing Basics18

KSU’s Ag Manager Great source of data Multiple yearsMultiple locationsMultiple commodities “Wednesday-basis” 48 week year “Nearby Basis”

(contract “nearest” to expiration)

Marketing Basics19

<= Mar =><= May =><= Jul =><= Sep =><= Dec =>< MarFut. Fut.

“Strong Basis:” cash bids are greater

relative to futures than AVG

“Weak Basis,” cash bids are less relative to futures than AVG

“Nearby Basis” (Cash Bid – Futures Price Nearest to Expiration)

__ __ _ __ __

Marketing Basics20

Basis Convergence

Transport.

S torage Cos ts

($0.50)

($0.40)

($0.30)

($0.20)

($0.10)

$0.00

Harvest ==> Contract Expiration

Transportation, QualityVolatility & Delivery Costs

------- March, KCBT Wheat -------

Basis Convergence: The concept that cash bids and futures prices will converge (i.e. basis will become nearly zero) at the contract delivery point during contract expiration. Why? Because sellers have the “opportunity to deliver” on their futures contract (only 3%).

. . . at other locations, basis will still reflect transportation, quality, volatility and the costs associated with delivery.

Marketing Basics

Marketing 101: Pricing AlternativesForward Cash ContractA contract to deliver a negotiated amount of grain to a

specific location for a negotiated price (futures & basis) at a specified time in the future.Eliminates both futures price and basis riskAllows for forward pricing over a longer periodThe amounts contracted can varyNo margin account or maintenance requiredDifficult to get out of (deliver, buy out, roll forward)Commits you to a specific buyer and locationNot always available; what if the buyer fails?

* Unsecured Creditor

Marketing Basics

Forward Cash Contract – Example Assume that you are a wheat producer and it is January

15. You call your local elevator and they tell you that the current forward contract bid is $6.40/bu. You accept the bid and agree to deliver 1,500 bushels at harvest.

a) On June 25, you deliver your grain and receive $6.40/bu. The current bid is $4.50/bu. Was the forward cash contract a success? Why or why not?

b) On June 25, you deliver your grain and receive $6.40/bu. The current bid is $8.50/bu. Was the forward cash contract a success? Why or why not?

Marketing 101: Pricing Alternatives

Marketing Basics

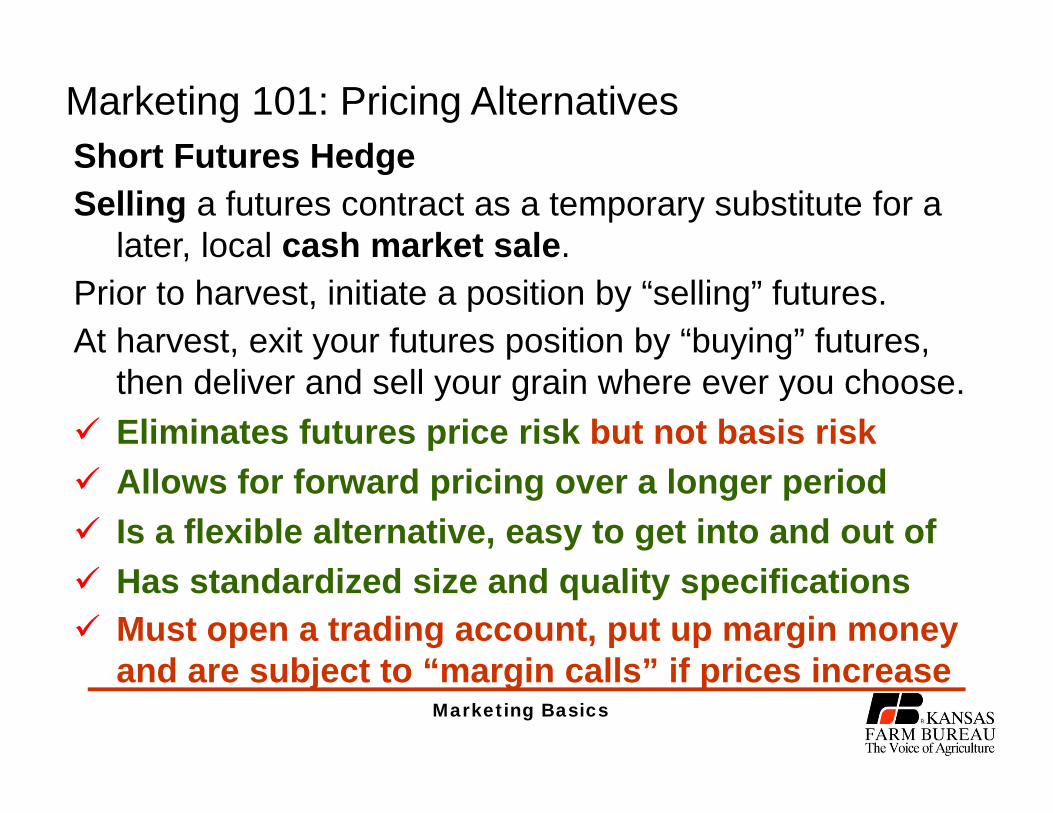

Short Futures HedgeSelling a futures contract as a temporary substitute for a

later, local cash market sale.Prior to harvest, initiate a position by “selling” futures.At harvest, exit your futures position by “buying” futures,

then deliver and sell your grain where ever you choose. Eliminates futures price risk but not basis risk Allows for forward pricing over a longer period Is a flexible alternative, easy to get into and out of Has standardized size and quality specifications Must open a trading account, put up margin money

and are subject to “margin calls” if prices increase

Marketing 101: Pricing Alternatives

Marketing Basics

Short Futures Hedge – Margin ExampleMargin Account Balance For One DEC 2008 Corn Futures Sell Hedge

Placed on January 2, 2008

-$5,000

$0

$5,000

$10,000

$15,000

$20,000

1/2/20

08

2/2/20

08

3/2/20

08

4/2/20

08

5/2/20

08

6/2/20

08

7/2/20

08

8/2/20

08

9/2/20

08

10/2/

2008

Date

Mar

gin

bala

nce,

$/c

ontr

act

Sell one contract @ $4.80 ¼ Initial margin = $1,500 $4.09 ½ (10/30/08)

Market topped @ $7.88 (6/26/08)126 acres irrigated180 bu./ac. = 22,680 bushels

or 4.5 contracts4 x $15,000 = $60,000

Marketing Basics

Know What the Market’s OfferingShort Futures Hedge

Examining Your Pricing Opportunities - Harvest Delivery

1. Futures Cont. Mo: JUL 15 Wheat Expected Basis ($0.10) Today's Date 2/3/15 Exit Date 6/30/152. Futures Price $5.55

3. Expected Commissions $0.00 Normally around $0.0154. ENSP* $5.45

5. Forward Cash Contract $5.30 JUL 16 Wheat 5.92$ ENSP 5.82$

* ENSP = Expected Net Selling Price = Futures + Basis - Commissions

My expectation of what I would “net;” IF I sell futures today.

(?)

Marketing Basics26

<= Mar =><= May =><= Jul =><= Sep =><= Dec =>< MarFut. Fut.

($0.10) may be a good “estimate” for 2015

__ __ _ __ __

Focus on the basis for the date you expect to deliver/sell

Marketing Basics

Example 1a: Short Hedge, Prices DownCash Market Futures Market BasisInitiation 2/3/15 Sell JUL 15 Wheat 5.55$ ($0.10)

expectedExit 6/30/15Buy JUL 15 Wheat 4.05$ ($0.10)Sell Cash 3.95$ actualEvaluation

$3.95 $1.50NET $5.45

What Happens as prices Change?

Did the hedge work? Why?

Marketing Basics

Example 1b: Short Hedge, Prices UPCash Market Futures Market BasisInitiation 2/3/15 Sell JUL 15 Wheat $5.55 ($0.10)

expectedExit 6/30/15Buy JUL 15 Wheat $7.05 ($0.10)Sell Cash $6.95 actualEvaluation

$6.95 ($1.50)NET $5.45

What Happens as prices Change?

Did the hedge work? Did you incur a margin call?

Marketing Basics

Example 1c: Short Hedge, Prices Down, WEAK BasisCash Market Futures Market BasisInitiation 2/3/15 Sell JUL 15 Wheat $5.55 ($0.10)

expectedExit 6/30/15Buy JUL 15 Wheat $4.05 ($0.50)Sell Cash $3.55 actualEvaluation

$3.55 $1.50NET $5.05

What Happens as prices Change?

Did the hedge work? Versus Forward Contract?

Marketing Basics

Example 1d: Short Hedge, Prices UP, WEAK BasisCash Market Futures Market BasisInitiation 2/3/15 Sell JUL 15 Wheat $5.55 ($0.10)

expectedExit 6/30/15Buy JUL 15 Wheat $7.05 ($0.50)Sell Cash $6.55 actualEvaluation

$6.55 ($1.50)NET $5.05

What Happens as prices Change?

Did the hedge work? Versus a Forward Contract?

Marketing Basics

What Happens as prices Change?

Did the hedge work? Versus a Forward Contract?

Example 1e: Short Hedge, Prices Down, STRONG BasisCash Market Futures Market BasisInitiation 2/3/15 Sell JUL 15 Wheat $5.55 ($0.10)

expectedExit 6/30/15Buy JUL 15 Wheat $4.05 $0.30Sell Cash $4.35 actualEvaluation

$4.35 $1.50NET $5.85

Marketing Basics

Comparing Pricing AlternativesPrices Prices Price Down

Alternative Up Down Weak BasisNo Action, sell @ harvest (speculating) $6.95 $3.95 $3.55Forward Contract $5.30 $5.30 $5.30Short Futures Hedge $5.45 $5.45 $5.05Short Options Hedge $6.65 $6.65 $6.25Option Fence $6.75 $6.75 $6.35Which alternative reduces price risk the most?Which reduces price risk the least?Which are susceptible to margin calls?Which are adversely affected by weaker than expected

basis?

Marketing Basics

Implementing Your Plan

1) Start Small, Go Slow and Build as your Knowledge Increases

2)Make Incremental Sales within Pricing Windows• Preharvest vs. postharvest• i.e. Up to 30% in 10% increments

3)Build and Utilize a “Marketing Team”4)Learn from the Past but Focus on the Future

and your next Marketing Decision

Marketing Basics

http://www.kfb.org/

USDA Reports Trip to Washington DCAugust 10-13, 2015

Registration: noon - 4/6/15

Futures Trip to Chicago

Spring 2016

Marketing Basics35

Questions?

Marketing Basics

When Hedging: Your basis estimate should reflect both the time you plan on selling or delivering the cash commodity; AND your expectation of the factors that will likely be impacting your commodity.

Homework: What is our basis estimate for harvest sales of corn?

($0.25)

Nearby Basis DataManhattan Corn ------------- Basis ------------ 3 Year

Week 2011 2012 2013 Avg BasisSeptember 33 ($0.33) ($0.18) $0.76 $0.08

Week 2 34 ($0.29) ($0.20) ($0.34) ($0.28) Week 3 35 ($0.26) ($0.20) ($0.11) ($0.19) Week 4 36 ($0.26) ($0.19) ($0.35) ($0.27)

October 37 ($0.26) ($0.20) ($0.39) ($0.28) Week 2 38 ($0.25) ($0.20) ($0.32) ($0.26) Week 3 39 ($0.19) ($0.18) ($0.39) ($0.25) Week 4 40 ($0.22) ($0.16) ($0.34) ($0.24)

November 41 ($0.20) ($0.17) ($0.35) ($0.24) Week 2 42 ($0.19) ($0.16) ($0.35) ($0.23) Week 3 43 ($0.18) ($0.14) ($0.34) ($0.22) Week 4 44 ($0.15) ($0.16) ($0.32) ($0.21)

Marketing Basics

WORKSHEET 1: What's the Market Offering?Today's Date: Expected1. Futures Contract Month: ____________ Basis $______

2. Futures Price $______

3. Expected Commissions $__0__

4. ENSP* $______ (ENSP) = Expected Net Selling Price = Futures + Expected Basis - Commissions

What’s the ENSP?

December Corn

4.68

2/25/14(0.25)

4.43

Marketing Basics

Short Futures Hedge Evaluation - 1.1Cash Futures Basis

Hedge InitiationDate:Futures Action: SELL $ $Hedge Exit/HarvestDate:Futures Action: BUY $ $Sell Cash Commodity $ Futures Gain (Loss)* $ Net Price** ==> $

*Futures Gain (Loss) = Futures Sell Price - Futures Buy Price **Net Price = Cash Commodity Price + Futures Gain (Loss)

What’s the Net Price Received?

2/14/144.60 (0.25)

10/17/144.00

3.80(0.20)

0.604.48

Marketing Basics

Short Futures Hedge Evaluation - 1.2Cash Futures Basis

Hedge InitiationDate:Futures Action: SELL $ $Hedge Exit/HarvestDate:Futures Action: BUY $ $Sell Cash Commodity $ Futures Gain (Loss)* $ Net Price** ==> $

*Futures Gain (Loss) = Futures Sell Price - Futures Buy Price **Net Price = Cash Commodity Price + Futures Gain (Loss)

What’s the Net Price Received?

2/14/144.60 (0.25)

10/17/144.80

4.50(0.30)

(0.20)4.38

Marketing Basics40

Questions?

Thanks!

Marketing Basics

Developing Your Marketing Plan

Job 1: WhenIdentify Pricing Windows“Deadlines for Action”

PreplantPreharvestAt HarvestPostharvestDate Specific

Based Upon Your KnowledgeComfort Resources

Marketing Basics

Developing Your Marketing Plan

Job 2: HowWhat’s In Your Toolbox?

PreharvestForward Cash ContractShort Futures HedgeShort Options HedgeBasis ContractsSell for Cash at HarvestOthers

Marketing Basics

Developing Your Marketing Plan

Job 3: WhySet Price Targets

What’s a “Good” Price?

My Cost of Production? a % above costs

A % Above CurrentPrice Levels?

Historical Levels?

Marketing Basics

Developing Your Marketing Plan

Job 4: Put It All TogetherIdentify Quantitative Amounts to

Price within each Window and, with each Marketing Alternative

How Much Preharvest?How Much with Forward ContractsHow Much with Futures (Options)

How Much At HarvestHow Much will you Store

Marketing Basics45

Incremental Pricing(Your Marketing Plan)

1) Identify pricing windows (i.e. preharvest and post harvest).

2)Set quantitative pricing targets (i.e. a range from 20-80%).

3)Utilize a mix of pricing alternatives (i.e. forward contracts, futures, hedge-to-arrive contracts).

4)Make incremental sales within each predetermined window & range.

Based Upon Your: KnowledgeComfort Resources

Marketing Basics

1. Prices Down – is considered a “worst case” scenario2. Versus Inaction – compares each alternative to inaction

or “doing nothing.”3. Over 1 Contract – compares it over 5,000 bushels

Prices Versus Over 1Alternative Down Inaction Contract

No Action - Speculating $5.08 ------ ------Forward Contract $6.48 $1.40 $7,000Short Futures Hedge $6.58 $1.50 $7,500

Comparing Pricing AlternativesWorst Case Scenario

Marketing Basics47

Mark NelsonDirector of

CommoditiesKansas Farm Bureau

(785) 587-6103

www.kfb.org

Marketing 101SUMMARY

K now What the Market is Offering

I ncrementally PriceS tudy/Understand BasisS tudy/Understand Your

Marketing Alternatives

Marketing Basics48

Basis Convergence

Transport.

S torage Cos ts

($0.50)

($0.40)

($0.30)

($0.20)

($0.10)

$0.00

Harvest ==> Contract Expiration

Transportation, QualityVolatility & Delivery Costs

Marketing 201: “Crop Year Basis Strengthens”Basis generally is weakest (widest) at harvest and strengthens as the marketing year progresses, and supplies are “bid” out of storage (for a given contract).

------- March, KCBT Wheat -------

Marketing Basics49

Managing price risk over time In 1848 the CBT, and in 1856 the KCBT, were

established. Initially as “cash” markets with “standardized” forward contracts.

In the 1860’s, the first standardized “futures contracts” were developed.

In 1919 the CME was established. In 1972, the first “financial” contracts were traded

(i.e. futures on treasury notes, etc.). In 1992, the Globex, electronic trading platform was

developed. In 2007, the CME and CBT merged to become a

single entity, the CME Group

Marketing Basics

BASE PREHARVEST PLANPercentages to Price

Preplant PhasePreharvest PhaseHarvest PhasePost Harvest

Given CurrentInformation!

Mark’s TemplateForwardCash Fut/Opt Total

0/25% 0/50% 0/50%25/50% 25/75% 25/100%

Later DecisionLater Decision

Storage AvailabilityHave it? More OpportunitiesDon’t? May FC More

The Decision to Price (Incremental Pricing)

Marketing Basics51

Mark NelsonDirector of

CommoditiesKansas Farm Bureau

(785) 587-6103

www.kfb.org

Marketing 101

Keep I tS impleS______

K now What the Market is Offering

I ncrementally PriceS tudy/Understand BasisS tudy/Understand Your

Marketing Alternatives (future markets)

Marketing Basics52

Salina Osborne Diff1999 ($0.27) ($0.55) ($0.28)2000 ($0.27) ($0.41) ($0.14)2001 ($0.10) ($0.33) ($0.23)2002 $0.09 ($0.24) ($0.33)2003 ($0.10) ($0.36) ($0.26)2004 ($0.10) ($0.34) ($0.24)2005 $0.00 ($0.25) ($0.25)2006 ($0.07) ($0.39) ($0.32)2007 ($0.10) ($0.48) ($0.38)2008 ($0.30) ($0.85) ($0.55)2009 ($0.26) ($0.67) ($0.41)2010 ($1.00) ($1.33) ($0.33)2011 ($0.18) ($0.65) ($0.47)

Last 5-Yr ($0.37) ($0.80) ($0.43)W/out '10 ($0.21) ($0.66) ($0.45)

First 5-Yr ($0.13) ($0.38) ($0.25)

($1.40)

($1.20)

($1.00)

($0.80)

($0.60)

($0.40)

($0.20)

$0.00

$0.20

KS Wheat Basis Comparison(4th Wednesday of June)

SalinaOsborne

Marketing Basics

Study/Understand Marketing Alternatives

Basis Impacts on the Short Futures HedgeThe short futures hedge works well as a price risk

management tool when basis variability is minimal. Why? Because we more closely receive the net price we “expected.”

A much weaker or wider than expected basis hurts the short futures hedge (i.e. sell positions).

But a much stronger or narrower than expected basis helps the short futures hedge.

Marketing Basics54

1) Futures Prices (market determined)2) Cash Bids/Basis (an industry determined

relationship to futures)

Basis = cash bid – futuresQuality: test weight, protein, oil content

Study/Understand Basis

Storage

Marketing Basics55

Milo Dec Futures4th Wednesday of NovemberDodge

City Salina44th

Topeka($0.49) ($0.27) ($0.29) 1998($0.53) ($0.31) ($0.37) 1999($0.27) ($0.07) ($0.24) 2000

$0.04 ($0.10) 2001($0.07) $0.23 $0.14 2002($0.15) $0.15 $0.11 2003

2004($0.43) ($0.18) ($0.30) 2005($0.11) $0.13 $0.15 2006($0.40) ($0.05) ($0.10) 2007($0.80) ($0.71) ($0.70) 2008($0.80) ($0.50) ($0.74) 2009($0.75) ($0.51) ($0.35) 2010($0.28) $0.05 ($0.16) 2011

($0.61) ($0.32) ($0.42) AVG$0.261 $0.290 $0.283 Stdev

($0.80)

($0.60)

($0.40)

($0.20)

$0.00

$0.20

$0.40

Dec Fut ~ 4th Wed November

Kansas Grain Sorghum Basis

Dodge Salina Topeka

Historical BasisThe starting point for

deriving an expected basis

Marketing Basics56

Is the starting point for deriving an expected basis

Historical BasisFocusing on the date you

expect to deliver/sell

Wheat Jul KC Futures4th Wednesday of June

Dodge City Salina

24th Topeka

1998($0.55) ($0.27) ($0.23) 1999($0.46) ($0.27) ($0.27) 2000($0.32) ($0.10) ($0.15) 2001($0.19) $0.09 $0.12 2002($0.35) ($0.10) ($0.05) 2003($0.29) ($0.10) ($0.10) 2004($0.38) $0.00 $0.00 2005($0.36) ($0.07) $0.05 2006($0.45) ($0.18) $0.00 2007($0.65) ($0.30) ($0.30) 2008($0.55) ($0.26) ($0.15) 2009($1.20) ($1.00) ($0.85) 2010($0.39) ($0.18) ($0.20) 2011($0.46) ($0.15) ($0.10) 2012

($0.68) ($0.44) ($0.38) AVG$0.241 $0.254 $0.233 Stdev

Marketing Basics57

Corn Dec Futures4th Wednesday of October

Dodge City Salina

40th Topeka

($0.21) ($0.21) 1998($0.29) ($0.23) 1999($0.04) ($0.27) 2000$0.08 ($0.06) ($0.22) 2001$0.13 $0.08 $0.02 2002$0.10 $0.10 ($0.06) 2003$0.03 ($0.15) ($0.30) 2004

($0.10) ($0.30) ($0.38) 2005$0.15 ($0.02) 2006

($0.12) ($0.13) ($0.20) 2007($0.22) ($0.32) ($0.22) 2008($0.27) ($0.30) ($0.33) 2009($0.38) ($0.50) ($0.40) 2010$0.16 $0.20 $0.02 2011

($0.16) ($0.20) ($0.24) AVG$0.183 $0.221 $0.140 Stdev

($0.50)

($0.40)

($0.30)

($0.20)

($0.10)

$0.00

$0.10

$0.20

$0.30

Dec Fut ~ 4th Wed October

Kansas Corn Basis

Dodge Salina Topeka

Historical BasisThe starting point for

deriving an expected basis

Marketing Basics58

Beans Nov Futures4th Wednesday of OctoberDodge

City Salina40th

Topeka($0.60) ($0.23) ($0.29) 1998($0.51) ($0.17) ($0.37) 1999($0.45) ($0.12) ($0.24) 2000($0.40) ($0.21) ($0.10) 2001($0.24) ($0.06) $0.14 2002($0.38) ($0.15) $0.11 2003($0.61) ($0.26) 2004($0.69) ($0.41) ($0.30) 2005($0.59) $0.15 2006($1.05) ($0.80) ($0.10) 2007($1.05) ($0.60) ($0.70) 2008($0.96) ($0.31) ($0.40) 2009($0.97) ($0.61) ($0.61) 2010($0.95) ($0.41) ($0.30) 2011

($0.96) ($0.44) ($0.44) AVG$0.273 $0.222 $0.267 Stdev

($1.10)

($0.90)

($0.70)

($0.50)

($0.30)

($0.10)

$0.10

$0.30

Nov Fut ~ 4th Wed October

Kansas Soybean Basis

Dodge Salina Topeka

Historical BasisThe starting point for

deriving an expected basis

Marketing Basics59

Mark NelsonKansas Farm Bureau

(785) [email protected]

www.kfb.org

Marketing 101February 18, 2014

$1.00