![Yazdani, G. - Ajanta. Part III [Cave VI,VII,IX,X,XI,XII,XV,XVI,XVII] (73p).pdf](https://static.fdocuments.us/doc/165x107/55cf969e550346d0338cb4fc/yazdani-g-ajanta-part-iii-cave-viviiixxxixiixvxvixvii-73ppdf.jpg)

Yazdani, G. - Ajanta. Part III [Cave VI,VII,IX,X,XI,XII,XV,XVI,XVII] (73p).pdf

Graduate Course

B.Com. (Hons.) III Year

Paper XVI : Management Accounting

Contents :

UNIT : 5

1. Management Decision Making

2. Marginal Costing and Decision Making

3. Differential Cost Analysis

UNIT : 6

1. Responsibility Accounting

2. Divisional Performance “Measurement : Financial Measures:

Editor :

Dr. N.K. Aggarwal

SCHOOL OF OPEN LEARNING UNIVERSITY OF DELHI

5, CAVALRY LANE

DELHI-110007

SESSION 2007-08 ( Copies)

© School of Open Leaning

Published by the Executive Director, School of Open Learning,

University of Delhi, 5 Cavalry Lane, Delhi-110007.

Laser typeset : S.O.L. Computer Centre

Printed at

1

UNIT 5

1

MANAGEMENT DECISION MAKING

Smriti Chawla Shri Ram College of Commerce

University of Delhi

Meaning of Decision Making

Decision-making is the process of choosing the best course of action from among

available alternative courses of action. Choice between alternative courses is an all pervading

managerial function. Managers of business concern discharge their functions only by making

decisions. Every manager regardless of level in which he operates is a decision maker. For

example cost of product is Rs.45 per unit. An export order is received at Rs. 40 per unit. Should

this order be accepted or not? The decision to be taken will be affected by cost and other factors

and cost accountant must use all information at his disposal to help management make right

decision.

Here, we are concerned with short term operating decisions such as whether to make a

component or buy it from outside supplier or whether or not to sell product at below cost. For

this marginal costing and differential cost analysis are two valuable techniques which are used

for short-term business decisions.

Steps Involved in Decision Making

The various steps involved in decision making process are:

Identify the problem or subject matter of decision:

A problem may be defined as a gap between existing or forecast condition and desired

condition. It may arise either because of an external event or an event purely internal to

business. Once the problem is known it becomes necessary to classify the same and

ascertain the relevant facts in order to make the right decision.

CHAPTER OBJECTIVES

Meaning of decision making Steps involved in Decision making Costs for Decision Making Decision making and Marginal Costing

o Fixation of Selling Prices o Effect of change in price o Maintaining a desired level of profit

(with Illustrations)

2

Identify alternative courses of action

There are various ways of achieving organisational objectives. Each of these is an

alternative. If for instance, profit is considered to be margin between sale price and cost,

the decision maker should not jump to conclusion that only way of increasing

profitability is to cut down costs. He must think of other alternatives to increase profits

such as change in product mix or make or buy a product or exploring new market etc.

The decision maker must make exhaustive list of all alternatives available.

Evaluation of alternatives

Identify the cost and benefit of each available alternative and make comparison between

them.

Selecting the best alternative and making it effective

Select the alternative which generates net maximum benefit. Moreover, people in the

organisation must be informed about the decision in order to make it effective.

Costs for Decision Making

The following are the important cost concepts used in decision-making:

(1) Relevant Costs: A relevant cost is a cost that is affected by a managerial decision.

Relevance means pertinent to decision in hand. Relevant costs for decision-making are

expected future costs that will differ under various alternatives. For example, if a decision

is to be taken whether idle capacity should be utilized or not. The costs that are relevant

in this decision are the additional cost that will be incurred for utilizing idle capacity. The

costs that are already incurred will be irrelevant costs and will be ignored for taking

decisions. Examples of relevant cost are marginal or variable cost, specific cost,

incremental costs, opportunity cost, out of pocket costs etc.

(2) Irrelevant Costs: Costs that are not affected by managerial decisions and hence are

ignored while taking decisions. Examples of irrelevant costs are general or absorbed

fixed cost, committed costs, sunk costs etc.

(3) Sunk Costs: Sunk Cost are historical costs incurred in past that cannot be changed and

over which management has no control. These costs are not relevant for decision making

about the future but they are frequently analysed in detail before decisions about future

courses of action are made. For example, in case of decision relating to replacement of a

machine, the written down value of existing machine is a sunk cost and therefore not

considered.

(4) Differential (Incremental and Decremental) Cost: It refers to the change (increase or

decrease) in total cost that occurs due to change in activity level, technology, process or

method of production etc. This cost is regarded as the difference in total cost resulting

from contemplated change.

(5) Marginal Cost: It is the additional cost of producing one additional unit and it is the

same thing as variable cost. Marginal costing is a technique of charging only variable

3

costs to products and helps in decisions like make or buy pricing of products, selection of

sales mix etc. Hence, this cost concept is of great relevance in managerial decision-

making.

(6) Imputed Costs: These are hypothetical costs which are specially computed outside the

accounting system for the purpose of decision-making. Interest on capital, rent of

premises payment for which is not actually made are examples of imputed cost.

(7) Opportunity costs: It is cost that measures the benefit that is lost or sacrificed when the

choice of one course of action requires that other alternative course of action be given up.

It is pure decision-making cost. For example, a company deposited Rs.1 lakh in bank at

10% p.a interest. Now it considers to invest this amount in debentures where yields is

17%. If company decides to invest in debentures it will have to forego bank interest of

Rs. 10000 p.a which is an opportunity cost.

(8) Replacement Cost: It is current market cost of replacing assets. For example: a

machinery purchased in 1990 at Rs. 10000 is discarded in 1998 and new machinery of

same type is purchased for Rs.15000. So, the replacement cost of machinery is Rs.15000.

(9) Out of pocket costs: out of pocket costs ate those costs that involve cash outlays which

may be either fixed or variable. It is frequently used as an aid in make or buy decisions,

price fixation during depression. Examples are wages, material cost, and insurance.

Depreciation on plant and machinery does not involve any cash outlay.

Decision Making and Marginal Costing

Marginal costing technique is used in providing assistance to the management in vital

decision making, especially in dealing with the problems requiring short-term decisions where

fixed costs are excluded. The following are important areas where managerial problems are

simplified by the use of the marginal costing.

Fixation of selling price

Effect of change in price

Maintaining desired level of profit

Key or Limiting Factor

Make or Buy Decision

Selection of Suitable product mix

Closing down or suspending activities

Alternative methods of production

Fixation of Selling Price

Although prices are more controlled by market conditions and other economic factors

than by decisions of management yet fixation of selling prices is one of the most important

functions of management. This function is to be performed:

a) Under normal circumstances

b) In times of competition

c) In times of trade depression

4

d) In accepting additional orders for utilizing idle capacity

e) In exporting and exploring new markets

In normal circumstances the price fixed must cover total cost, as otherwise profits cannot

be earned but under other circumstances, products may have to be sold at a price below total

cost, if such a step is necessary to meet the situation arising due to competition, trade depression,

additional orders for utilising spare capacity, exploring new markets etc. Thus, in special

circumstances, price may be below total cost and it should be equal to marginal cost plus certain

amount (if possible).

Pricing in Depression: Prices fall during depression and product may be sold below total

cost. In case there is serious but temporary fall in the demand on account of depression leading to

the need for a drastic reduction in prices temporarily, the minimum selling price should be equal

to marginal cost. If the selling price at which the goods can be sold is equal to marginal cost or

more than marginal cost the product should be continued. Fixed expenses will be incurred even if

product is discontinued during depression for a short period. If the product can be sold at a price

which is little more than marginal cost, loss on account of fixed expenses will reduce because

price will recover fixed expenses to some extent.

If the selling price is below the marginal cost, loss will be more than the fixed costs

because variable expenses will not be recovered fully. Hence, efforts should be made to sell the

product at a price which is equal to marginal cost or more than marginal cost. Production should

be discontinued if the price obtained is below the marginal cost so that loss may not be more than

the fixed costs.

Selling Price Below the Marginal Cost

In the following circumstances production may be continued even if the selling price is

below the marginal cost.

1. When a new product is introduced in the market.

2. When foreign market is to be explored to earn foreign exchange.

3. When concern has already purchased large quantities of materials.

4. When sales of one product at a price below the marginal cost will push up the sales of

other profitable products.

5. When employees cannot be retrenched.

6. When competitors are to be eliminated from the market.

7. When the goods are of perishable nature.

Accepting Additional Orders, Exploring Additional Markets and Exporting

When additional orders are accepted or additional markets explored at a price below

normal price to utilise idle capacity, it should be very carefully seen that they will not affect the

normal market and goodwill of the company. The order from local merchant should not be

accepted at a price below normal price because it will affect relationship of concern with other

customers purchasing the goods at normal price. In case of foreign markets, goods may be sold at

a price below normal price keeping in view the direct and indirect benefits of exporting such as

import quotas, subsidies of government.

Factors to be considered before Launching a Product in the New Market

(1) Whether the firm has surplus capacity to meet the new demand.

(2) The price offered by the new market or expected to be realised should fully recover

variable cost plus additional expenditure to be incurred in launching product in the new

5

market. Over and above this price should earn a profit margin considered appropriate by

the producer depending on market conditions and marketing strategy.

(3) Lower price charged in the new market, domestic or foreign, should not adversely affect

price or demand in existing market. Goods sold at lower price in the new market should

not be dumped back in the existing market.

Illustration 1: MM Company Limited produces a single product. Its selling price and

production cost per unit as under:

Output 40,000 units

Rs.

Material cost 4.00

Labour cost 4.00

Variable overhead 2.00

Fixed expense 4.00

Total Cost 14.00

Due to depression, the company is not able to sell at the existing selling price of Rs.16 per unit.

However, it is possible to sell the total output of 40,000 units at Rs.12 per unit.

You are required to advise whether the company should sell at Rs.12 per unit or close the

factory.

Solution:

Profit Statement if output is sold at Rs. 12 per unit

Sales : 40000 @ Rs. 12 per unit 4,80,000

Less : Variable cost @ Rs.10 per unit

(Rs.4 + Rs. 4 + Rs.2) 4,00,000

Contribution 80,000

Less : Fixed cost

(40,000 x Rs.4) 1,60,000

Loss (80000)

If company sells at Rs.12 per unit it will suffer a loss of Rs.80,000. However, if the

company discontinues the production it will suffer a loss of Rs.160,000 on account of fixed costs

which cannot be avoided during the period of closure of factory. It is therefore advantageous to

sell at Rs.12 per unit even though it is below the total cost of Rs.14 per unit Any price above the

marginal cost will reduce loss and therefore should be acceptable.

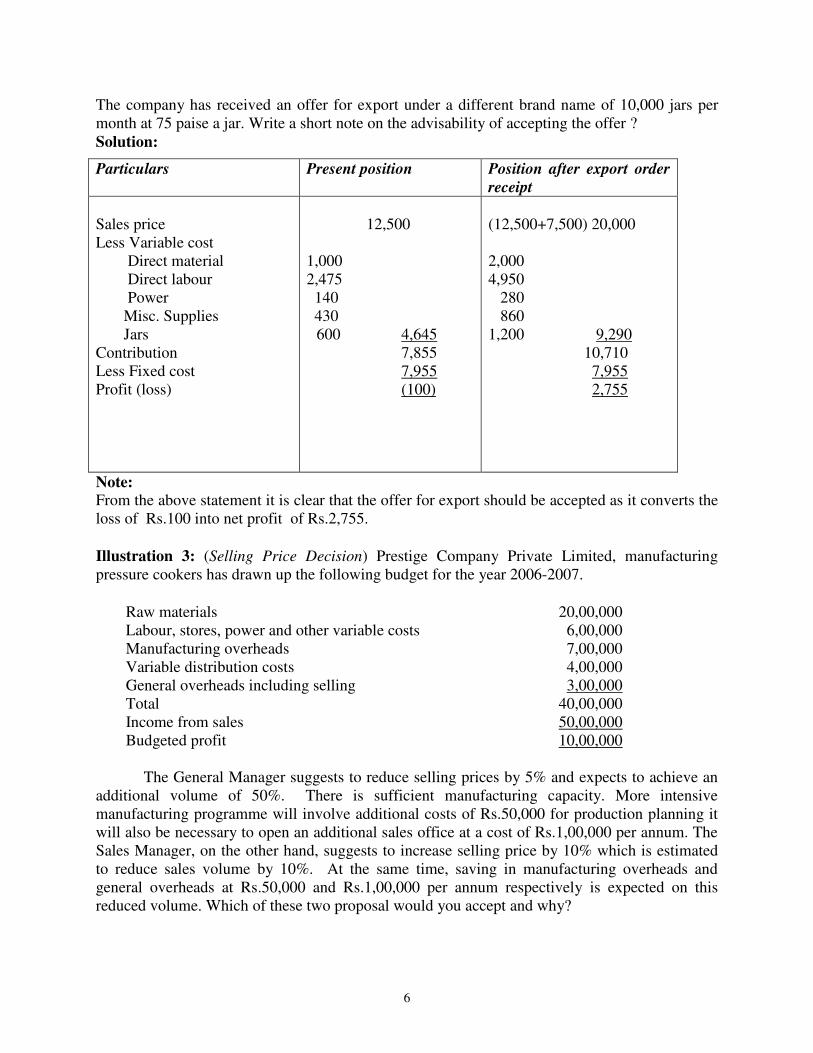

Illustration 2: The Everest Snow Company manufacturers and sells direct to customers

10,000 jars of ‘Everest Snow’ per month at Rs. 1.25 per jar. The company’s normal production

capacity is 20,000 jars and snow per month. Analysis is of cost for 10,000 jars show:

Direct Material 1,000

Direct Labour 2,475

Power 140

Misc. Expense 430

Jars 600

Fixed expenses of manufacturing,

Selling and administration 7,955

Total Rs. 12,600

6

The company has received an offer for export under a different brand name of 10,000 jars per

month at 75 paise a jar. Write a short note on the advisability of accepting the offer ?

Solution:

Particulars

Present position

Position after export order

receipt

Sales price

Less Variable cost

Direct material

Direct labour

Power

Misc. Supplies

Jars

Contribution

Less Fixed cost

Profit (loss)

12,500

1,000

2,475

140

430

600 4,645

7,855

7,955

(100)

(12,500+7,500) 20,000

2,000

4,950

280

860

1,200 9,290

10,710

7,955

2,755

Note:

From the above statement it is clear that the offer for export should be accepted as it converts the

loss of Rs.100 into net profit of Rs.2,755.

Illustration 3: (Selling Price Decision) Prestige Company Private Limited, manufacturing

pressure cookers has drawn up the following budget for the year 2006-2007.

Raw materials 20,00,000

Labour, stores, power and other variable costs 6,00,000

Manufacturing overheads 7,00,000

Variable distribution costs 4,00,000

General overheads including selling 3,00,000

Total 40,00,000

Income from sales 50,00,000

Budgeted profit 10,00,000

The General Manager suggests to reduce selling prices by 5% and expects to achieve an

additional volume of 50%. There is sufficient manufacturing capacity. More intensive

manufacturing programme will involve additional costs of Rs.50,000 for production planning it

will also be necessary to open an additional sales office at a cost of Rs.1,00,000 per annum. The

Sales Manager, on the other hand, suggests to increase selling price by 10% which is estimated

to reduce sales volume by 10%. At the same time, saving in manufacturing overheads and

general overheads at Rs.50,000 and Rs.1,00,000 per annum respectively is expected on this

reduced volume. Which of these two proposal would you accept and why?

7

Solution:

Comparative Statement of Budgeted Profit

Proposal I

Rs.

Proposal II

Rs.

Sales 71,25,000 49,50,000

Cost of Sales:

Raw materials

Labour, stores, power and other variable costs

Manufacturing overheads

Variable distribution cost

General overheads including selling

Total

30,00,000 18,00,000

9,00,000 5,40,000

7,50,000 6,50,000

6,00,000 3,60,000

4,00,000 2,00,000

56,50,000 35,50,000

Profit (Sales – Cost of sales) 14,75,000 14,00,000

Conclusion: Proposal I gives a larger profit of Rs.14,75,000 and thus should be accepted.

Working Notes

Sales: Proposal I Rs. 50,00,000 x 000,25,71.Rs100

150x

100

95

II Rs. 50,00,000 x 000,50,49.Rs100

90x

100

110

Raw material: Proposal I Rs. 20,00,000 + 50% = Rs. 30,00,000

II Rs. 20,00,000 - 10% = Rs. 18,00,000

Labour etc.: Proposal I Rs.6,00,000 + 50% = Rs. 9,00,000

II Rs. 6,00,000 - 10% = Rs. 5,40,000

Effect of Change in Sales Price

Management is confronted with the problem of cut in prices of products from time to time

on account of competition, expansion programmes or government regulations. It is therefore

necessary to know the effect of a cut in selling price per unit will be that contribution per unit

will reduce.

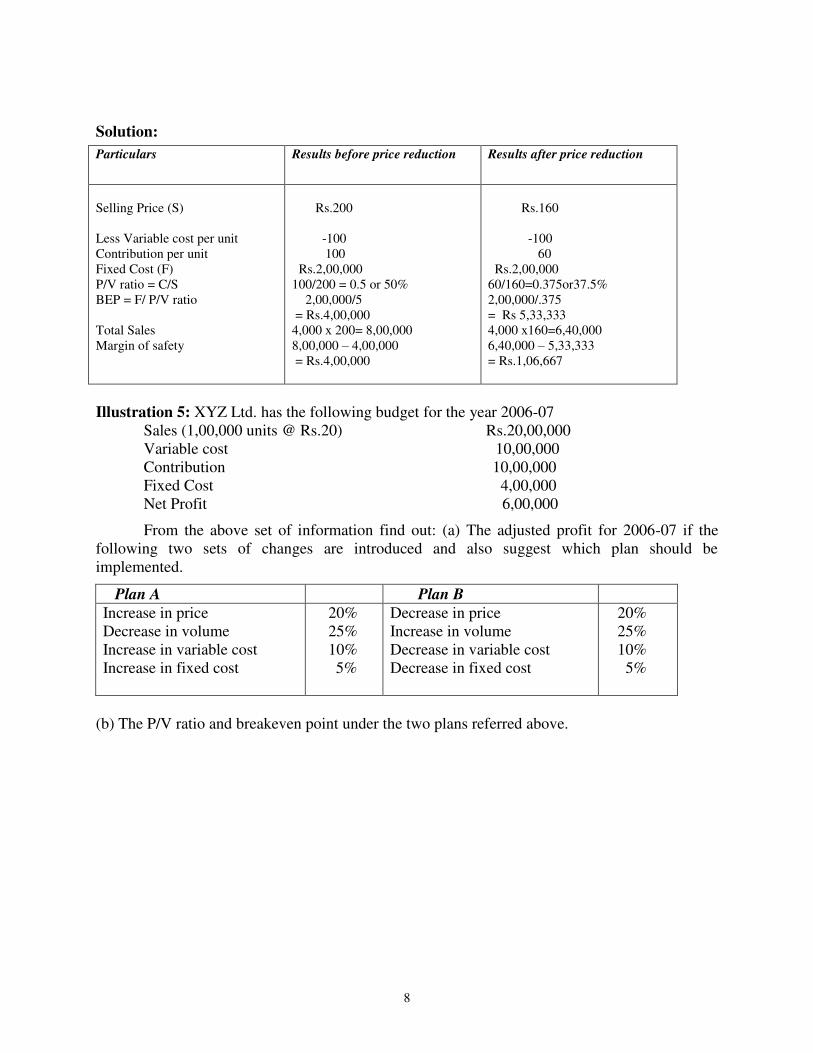

Illustration 4: The selling price of a product was Rs. 200 per unit, as against its variable

cost of Rs.100 per unit. Total fixed costs were Rs.2,00,000. Calculate the effect of a reduction in

price by Rs. 40 on the P/V ratio, break-even point and margin of safety, if 4000 units were

produced and sold.

8

Solution:

Particulars

Results before price reduction Results after price reduction

Selling Price (S)

Less Variable cost per unit

Contribution per unit

Fixed Cost (F)

P/V ratio = C/S

BEP = F/ P/V ratio

Total Sales

Margin of safety

Rs.200

-100

100

Rs.2,00,000

100/200 = 0.5 or 50%

2,00,000/5

= Rs.4,00,000

4,000 x 200= 8,00,000

8,00,000 – 4,00,000

= Rs.4,00,000

Rs.160

-100

60

Rs.2,00,000

60/160=0.375or37.5%

2,00,000/.375

= Rs 5,33,333

4,000 x160=6,40,000

6,40,000 – 5,33,333

= Rs.1,06,667

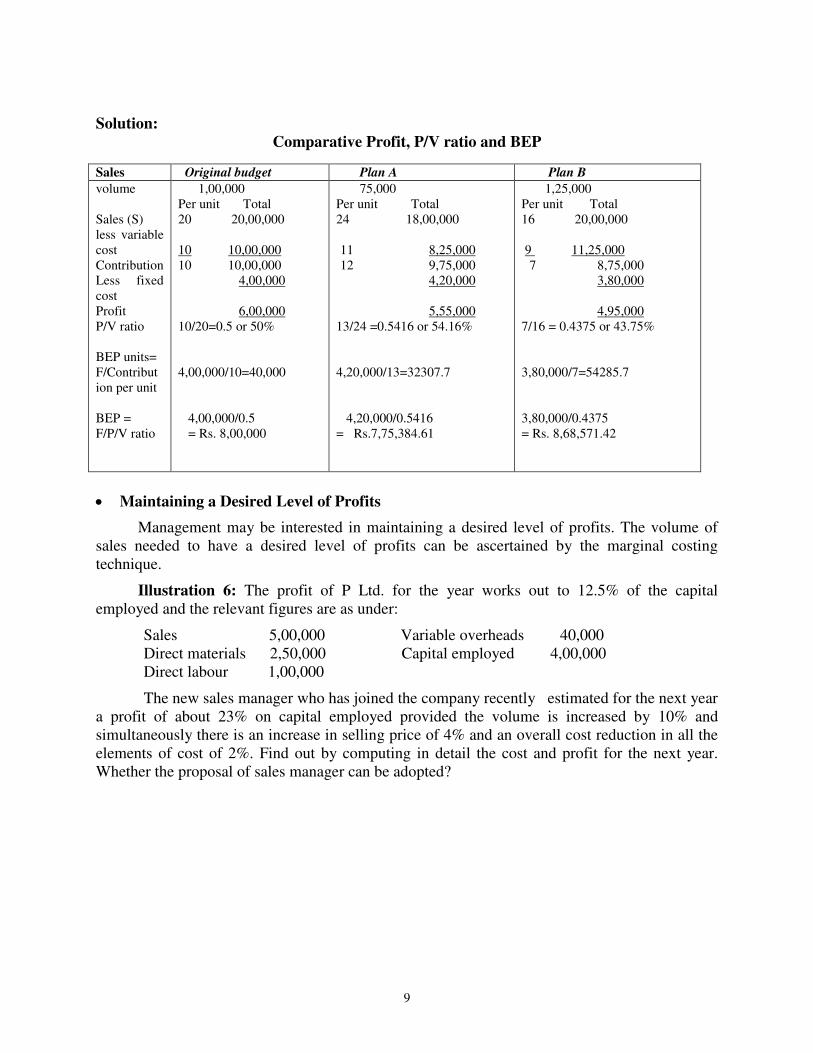

Illustration 5: XYZ Ltd. has the following budget for the year 2006-07

Sales (1,00,000 units @ Rs.20) Rs.20,00,000

Variable cost 10,00,000

Contribution 10,00,000

Fixed Cost 4,00,000

Net Profit 6,00,000

From the above set of information find out: (a) The adjusted profit for 2006-07 if the

following two sets of changes are introduced and also suggest which plan should be

implemented.

Plan A Plan B

Increase in price

Decrease in volume

Increase in variable cost

Increase in fixed cost

20%

25%

10%

5%

Decrease in price

Increase in volume

Decrease in variable cost

Decrease in fixed cost

20%

25%

10%

5%

(b) The P/V ratio and breakeven point under the two plans referred above.

9

Solution:

Comparative Profit, P/V ratio and BEP

Maintaining a Desired Level of Profits

Management may be interested in maintaining a desired level of profits. The volume of

sales needed to have a desired level of profits can be ascertained by the marginal costing

technique.

Illustration 6: The profit of P Ltd. for the year works out to 12.5% of the capital

employed and the relevant figures are as under:

Sales 5,00,000 Variable overheads 40,000

Direct materials 2,50,000 Capital employed 4,00,000

Direct labour 1,00,000

The new sales manager who has joined the company recently estimated for the next year

a profit of about 23% on capital employed provided the volume is increased by 10% and

simultaneously there is an increase in selling price of 4% and an overall cost reduction in all the

elements of cost of 2%. Find out by computing in detail the cost and profit for the next year.

Whether the proposal of sales manager can be adopted?

Sales Original budget Plan A Plan B

volume

Sales (S)

less variable

cost

Contribution

Less fixed

cost

Profit

P/V ratio

BEP units=

F/Contribut

ion per unit

BEP =

F/P/V ratio

1,00,000

Per unit Total

20 20,00,000

10 10,00,000

10 10,00,000

4,00,000

6,00,000

10/20=0.5 or 50%

4,00,000/10=40,000

4,00,000/0.5

= Rs. 8,00,000

75,000

Per unit Total

24 18,00,000

11 8,25,000

12 9,75,000

4,20,000

5,55,000

13/24 =0.5416 or 54.16%

4,20,000/13=32307.7

4,20,000/0.5416

= Rs.7,75,384.61

1,25,000

Per unit Total

16 20,00,000

9 11,25,000

7 8,75,000

3,80,000

4,95,000

7/16 = 0.4375 or 43.75%

3,80,000/7=54285.7

3,80,000/0.4375

= Rs. 8,68,571.42

10

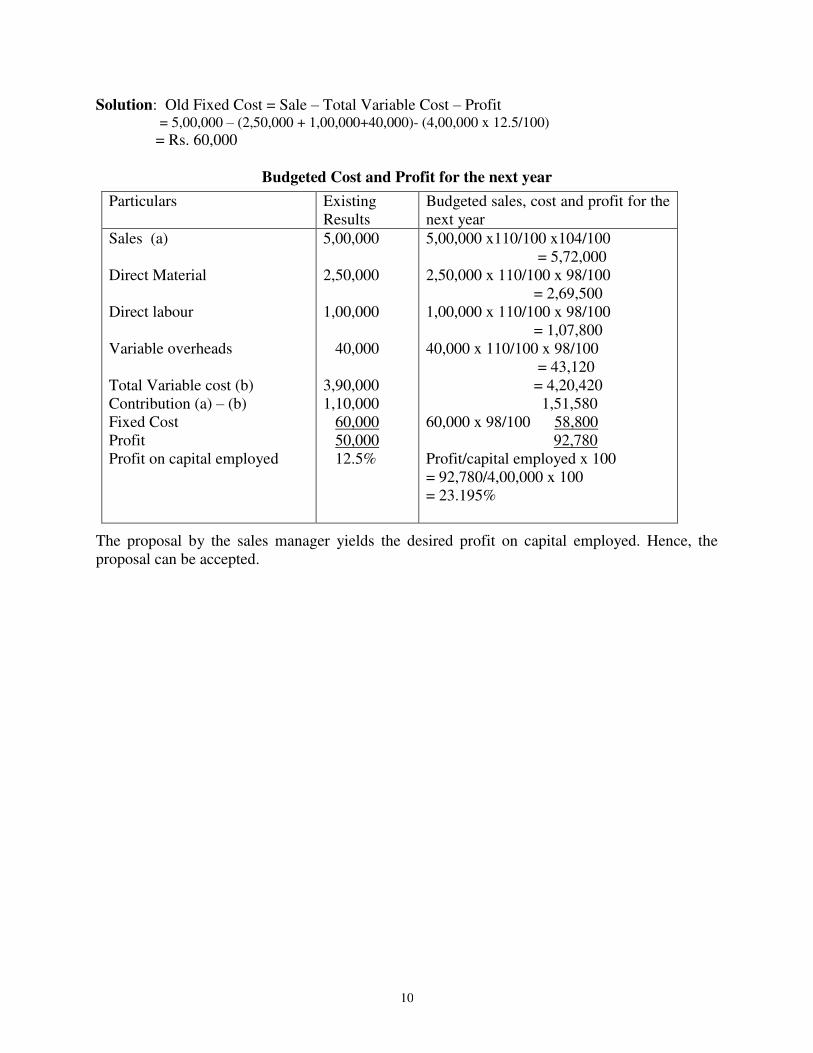

Solution: Old Fixed Cost = Sale – Total Variable Cost – Profit = 5,00,000 – (2,50,000 + 1,00,000+40,000)- (4,00,000 x 12.5/100)

= Rs. 60,000

Budgeted Cost and Profit for the next year

Particulars

Existing

Results

Budgeted sales, cost and profit for the

next year

Sales (a)

Direct Material

Direct labour

Variable overheads

Total Variable cost (b)

Contribution (a) – (b)

Fixed Cost

Profit

Profit on capital employed

5,00,000

2,50,000

1,00,000

40,000

3,90,000

1,10,000

60,000

50,000

12.5%

5,00,000 x110/100 x104/100

= 5,72,000

2,50,000 x 110/100 x 98/100

= 2,69,500

1,00,000 x 110/100 x 98/100

= 1,07,800

40,000 x 110/100 x 98/100

= 43,120

= 4,20,420

1,51,580

60,000 x 98/100 58,800

92,780

Profit/capital employed x 100

= 92,780/4,00,000 x 100

= 23.195%

The proposal by the sales manager yields the desired profit on capital employed. Hence, the

proposal can be accepted.

11

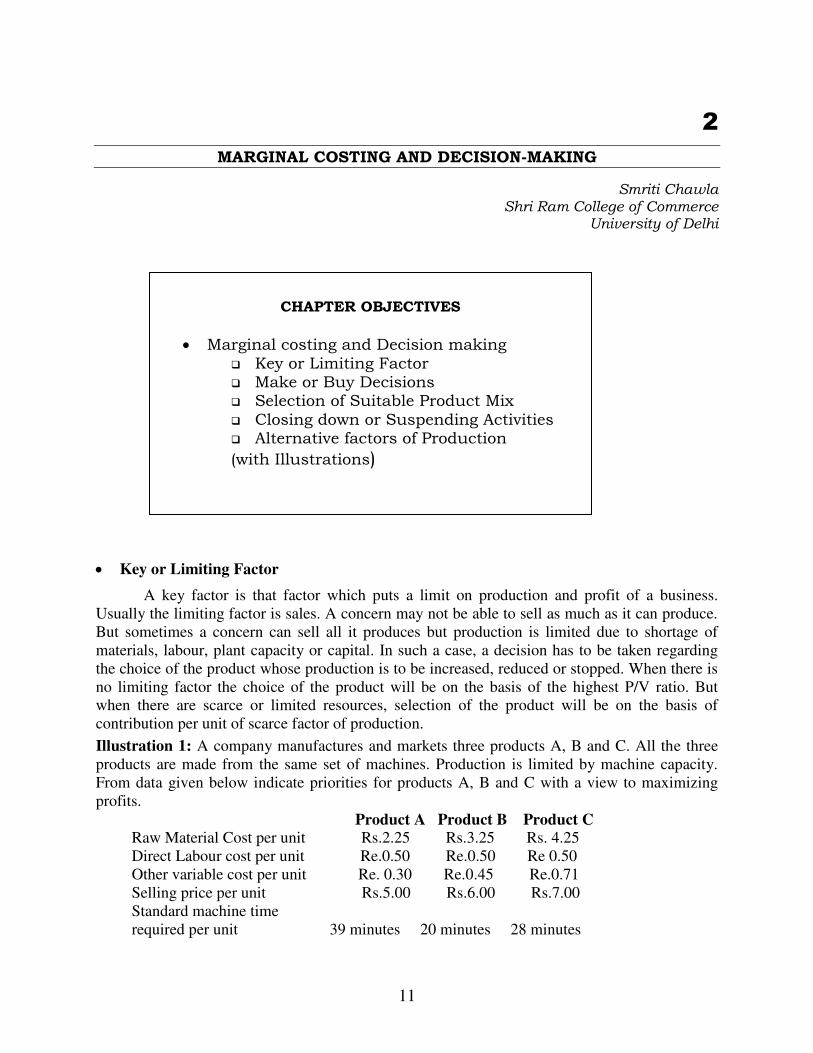

2

MARGINAL COSTING AND DECISION-MAKING

Smriti Chawla Shri Ram College of Commerce

University of Delhi

Key or Limiting Factor

A key factor is that factor which puts a limit on production and profit of a business.

Usually the limiting factor is sales. A concern may not be able to sell as much as it can produce.

But sometimes a concern can sell all it produces but production is limited due to shortage of

materials, labour, plant capacity or capital. In such a case, a decision has to be taken regarding

the choice of the product whose production is to be increased, reduced or stopped. When there is

no limiting factor the choice of the product will be on the basis of the highest P/V ratio. But

when there are scarce or limited resources, selection of the product will be on the basis of

contribution per unit of scarce factor of production.

Illustration 1: A company manufactures and markets three products A, B and C. All the three

products are made from the same set of machines. Production is limited by machine capacity.

From data given below indicate priorities for products A, B and C with a view to maximizing

profits.

Product A Product B Product C

Raw Material Cost per unit Rs.2.25 Rs.3.25 Rs. 4.25

Direct Labour cost per unit Re.0.50 Re.0.50 Re 0.50

Other variable cost per unit Re. 0.30 Re.0.45 Re.0.71

Selling price per unit Rs.5.00 Rs.6.00 Rs.7.00

Standard machine time

required per unit 39 minutes 20 minutes 28 minutes

CHAPTER OBJECTIVES

Marginal costing and Decision making Key or Limiting Factor Make or Buy Decisions Selection of Suitable Product Mix Closing down or Suspending Activities Alternative factors of Production

(with Illustrations)

12

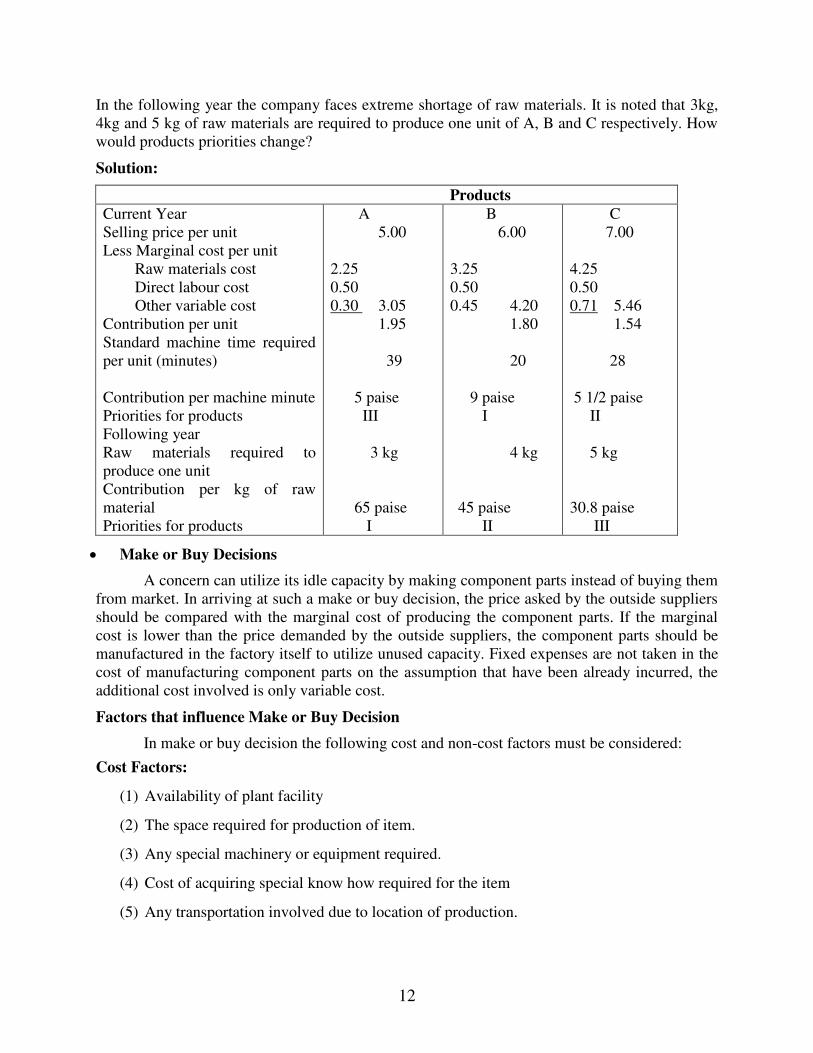

In the following year the company faces extreme shortage of raw materials. It is noted that 3kg,

4kg and 5 kg of raw materials are required to produce one unit of A, B and C respectively. How

would products priorities change?

Solution:

Products

Current Year

Selling price per unit

Less Marginal cost per unit

Raw materials cost

Direct labour cost

Other variable cost

Contribution per unit

Standard machine time required

per unit (minutes)

Contribution per machine minute

Priorities for products

Following year

Raw materials required to

produce one unit

Contribution per kg of raw

material

Priorities for products

A

5.00

2.25

0.50

0.30 3.05

1.95

39

5 paise

III

3 kg

65 paise

I

B

6.00

3.25

0.50

0.45 4.20

1.80

20

9 paise

I

4 kg

45 paise

II

C

7.00

4.25

0.50

0.71 5.46

1.54

28

5 1/2 paise

II

5 kg

30.8 paise

III

Make or Buy Decisions

A concern can utilize its idle capacity by making component parts instead of buying them

from market. In arriving at such a make or buy decision, the price asked by the outside suppliers

should be compared with the marginal cost of producing the component parts. If the marginal

cost is lower than the price demanded by the outside suppliers, the component parts should be

manufactured in the factory itself to utilize unused capacity. Fixed expenses are not taken in the

cost of manufacturing component parts on the assumption that have been already incurred, the

additional cost involved is only variable cost.

Factors that influence Make or Buy Decision

In make or buy decision the following cost and non-cost factors must be considered:

Cost Factors:

(1) Availability of plant facility

(2) The space required for production of item.

(3) Any special machinery or equipment required.

(4) Cost of acquiring special know how required for the item

(5) Any transportation involved due to location of production.

13

(6) As to labour factors like availability of required labour, sheet required and other must be

kept in view.

(7) As to overhead expenses, adoption of lease for apportioning them must be taken into

consideration including other factors.

Non-Cost Factors:

(1) In favour of making, the factors like:

Secrecy of company production

Ideal facility available

Tax considerations

Quality and stability of market supply

(2) In favour of buying factors:

Lack of capital required

Wide selection

Passing know how to suppliers or not

Uneven production of end product.

(3) The outside supplier should not be competitor.

(4) In case there are large fluctuation in demand, it is better to purchase from outside, but if

demand is likely to increase substantially own production may lead to lower cost latter.

Illustration 2: A radio manufacturing company finds that while it costs Rs.62.50 to make

component X 273 Q, the same is available in market at Rs. 57.50 each with an assurance of

continued supply. The break down of the cost is:

Cost per unit

Material 27.50

Labour 17.50

Variable overhead 5.00

Depreciation and other fixed costs 12.50

62.50

(a) Should the company make or buy the component?

(b) What would be your decision, if supplier offered the component at Rs. 48.50 each?

Solution: Compare the marginal cost of making the component with the cost of buying. It is

done below:

The marginal cost of manufacturing the component:

Material 27.50

Labour 17.50

Variable overhead 5.00

50.00

Cost of buying the component 57.50

Disadvantage in buying: Rs.57.50 – Rs.50 = Rs.7.50 per unit. Hence, the company should

make the component instead of buying. Here fixed cost are sunk cost and irrelevant for decision.

14

(b) If the component is available at Rs. 48.50 each then the option to buy will be profitable as it

will result in the saving of Rs. 1.50 per unit (Rs. 50 marginal cost of manufacture less Rs. 48.50

purchase price)

Illustration 3: (Make or Buy Decision) Auto Parts Ltd. has an annual production of

90,000 units for a motor component. The component cost structure is as below:

Materials Rs. 270 per unit

Labour (25% fixed) 180 per unit

Expenses:

Variable 90 per unit

Fixed 135 per unit

Total 675 per unit

(a) The purchase manager has an offer from a supplier who is willing to supply the component at

Rs.540. Should the component be purchased and production stopped?

(b) Assume the resources now used for this component's manufacture are to be used to produce

another new product for which the selling price is Rs.485.In the latter case the material price will

be Rs.200 per unit. 90,000 units of this product can be produced at the same cost basis as above

for labour and expenses. Discuss whether it would be advisable to divert the resources to

manufacture that new product, on the footing that the component presently being produced

would, instead of being produced, be purchased form the market.

Solution Rs.

Material 270

Labour (75% of Rs.180) 135

Variable expenses 90

Total variable cost when component is produced 495

Suppliers price 540

Excess of purchase price over variable cost = 540 – 495 = Rs.45 (a) Fixed expenses are

not affected whether the component is made or purchased. Thus company should make the

component itself because if purchased from outside it will have to pay Rs.45 per unit more and

on 90,000 units @ Rs.45 it comes to Rs.40,50,000.

(b) Cost implications of proposal to divert available production facilities for a new product:

15

Rs.

Selling price of per unit of new product 485

Less: Variable costs - Material 200

Labour 135

Expenses 90 425

Contribution per unit 60

Loss if present component is purchased = 540 – 495 = Rs.45.

If company diverts the resources for the production of a new product, it will benefit by

Rs.15 (i.e. Rs.60 – 45) per unit. On 90,000 units it will save @ Rs.15 i.e. Rs.13,50,000. Thus, it

is advisable to divert the production facilities in the manufacture of the new product and the

component presently being manufactured should be bought from outside. This will result in

additional profit of Rs.13,50,000.

Selection of Suitable product mix When a factory manufactures more than one product, a problem is faced by management as

to which product mix will give maximum profits. The best product mix is that which yields the

maximum contribution. The products which give the maximum contribution are to be retained

and their production should be increased. The products, which give comparatively less

contribution, should be reduced or closed down altogether. The effect of sales mix can also be

seen by comparing the P/V ratio and break even point. The new sales mix will be favourable if it

increases P/V ratio and reduced the break even point.

Illustration 4: A manufacturer with an overall capacity of one lakh machine hours

(interchangeable among products) has so far been producing a standard mix of 15,000 units of

product A, 10,000 units of Product B and C each. The total expenditure exclusive of fixed

charges is Rs. 2.09 lakhs and variable cost ratio among the products approximates

1:1.5:1.75respectively per unit. The fixed charges came to Rs. 2.00 per unit. When the unit

selling prices are Rs. 6.25 for A, Rs 7.50 for B and Rs. 10.50 for C, he incurs a loss. He desires

to change the product mix as under:

Mix 1 Mix 2 Mix 3

A

B

C

18,000

12,000

7,000

15,000

6,000

13,000

22,000

8,000

8,000

As an accountant what mix will you recommend ?

16

Solution:

(i) Computation of variable cost per unit

Total variable cost of Rs. 2,09,000 will be apportioned among the three products in the

following ratio:

A 15,000 x 1= Rs.15000: B 10,000 x 1.5 = Rs. 15000 C 10,000 x 1.75 = Rs. 17,500 or

6:6:7

Hence, total variable cost of each product will be

A : 2,09,000 x 6/19 = Rs.66,000

B : 2,09,000 x 6/19 = Rs.66,000

C : 2,09,000 x 7/19 = Rs.77,000

And per unit variable cost of each product:

A : 66,000/15000= Rs. 4.40 per unit

B : 66,000/10,000 = Rs.6.60 per unit

C : 77,000/ 10,000 = Rs. 7.70 per unit

(ii) Computation of contribution per unit of each product:

Product A Product B Product C

Selling price

Variable cost

Contribution

6.25

4.40

1.85

7.50

6.60

0.90

10.50

7.70

2.80

(iii) It is assumed that the fixed cost of Rs. 70,000 (35,000 unit of present mix at Rs. 2)

remains constant for all proposed mixes.

Comparative profitability statement to evaluate here product mixes.

Product

Contribu-

tion rate

per unit

Mix 1 Mix 2 Mix 3

Units Total

contribution

Units Total

contribution

Units Total

contribution

A

B

C

Contribution

Less fixed

charges

Profit(loss)

1.85

0.90

2.80

18,000 33,300

12,000 10,800

7,000 19,600

63,700

70,000

(6300)

15,000 27,750

6,000 5,400

13,000 36,400

69,550

70,000

(450)

22,000 40,700

8,000 7,200

8,000 22,400

70,300

70,000

300

17

Note : It is evident from the above statement that Mix 3 gives the maximum total

contribution and gives a net profit of Rs.300 after recovering fixed cost hence Mix 3 is

recommended.

Closing Down or Suspending Activities:

Sometimes, it become necessary for firm to temporarily suspend or close the activities of the

particular product, factory or department as a whole due to trade recession. The decision to close

down or suspend it activities will depend on whether product are making contribution towards

fixed cost or not. If products are making contribution towards fixed cost it is preferable not to

close business or suspend its activities to minimise the losses. If business is closed down there

may be certain fixed cost which could be avoided but there will be certain expenses which will

have to be incurred at the time of closing the operation like redundancy payments, maintenance

of plant etc. Such cost are associated with closing down of the business and must be taken into

consideration before taking any decision. Fixed cost may be general or specific. General fixed

cost may or may not remain constant while specific cost will be directly affected by closing

down of operation.

In addition to cost consideration, there may be some non-cost considerations which may

weigh in taking the decision to close down or suspend its activities or not. The following non-

cost considerations are relevant in this respect:

Once business is closed down, competitors may establish their products and our business

may be lost. It may be difficult to recapture the lost market again.

Fear of retrenchment of workers. If workers are discharged it may be difficult to get

experienced and skilled workers again at the restart of business.

Plant may become obsolete with the closure of business and heavy capital expenditure

may have to be incurred on restart of the business.

Reputation of the firm may suffer if some activities are closed down or suspended.

Temporary closing down or suspending activities may not be desirable if the relationship

with the suppliers is adversely affected.

Alternative Methods of Production:

Marginal costing is helpful in comparing alternative method of production, i.e., machine

work or handwork. The method which gives the greatest contribution (assuming fixed expense

remaining same) is to be adopted keeping, of course the limiting factor in view. Where, however,

fixed expenses change, the decision will betaken on the basis of profit contributed by each.

Illustration 5: Product X can be produced either by machine A or machine B. Machine A

can produce 100 units of X per hour and machine B 150 units per hour. Total machine hours

available during the year are 2,500. Taking into account the following data determine the

profitable method of manufacture. Per unit of product X

Machine A (Rs) Machine B(Rs)

Marginal cost 5 6

Selling price 9 9

Fixed cost 2 2

18

Solution:

Profitability Statement

Machine A (Rs.) Machine B (Rs.)

Selling price per unit 9 9

Less marginal cost 5 6

Contribution per unit 4 3

Output per hour 100 units 150 units

Contribution per hour 400 450

Machine hours per year 2500 2500

Annual contribution 10,00,000 11,25,000

Hence, production by machine B is more profitable.

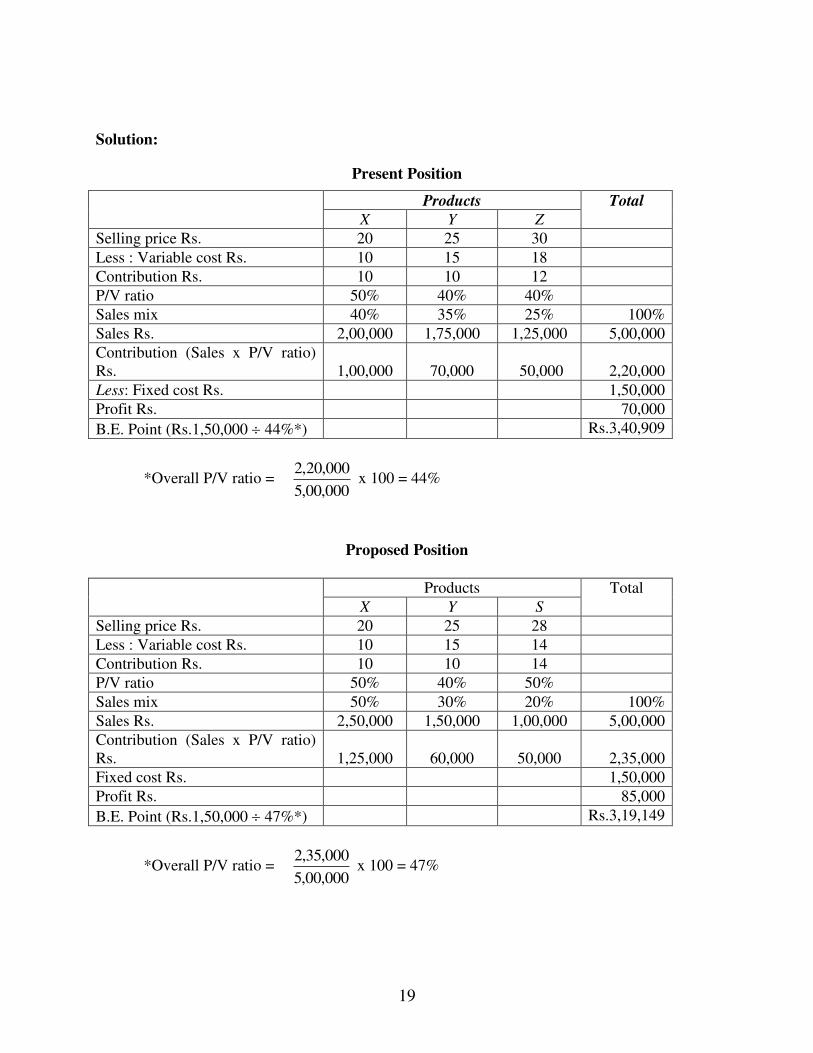

Illustration 6: (Sales Mix Decision). A multi-product company provides the following costs

and output data for the last year.

Products

X Y S

Sales mix 40% 35% 25%

Rs. Rs. Rs.

Selling price 20 25 30

Variable cost per unit 10 15 18

Total fixed cost 1,50,000

Total sales 5,00,000

The company proposes to replace Product Z by Product S. Estimated cost and output data are:

Products

X Y Z

Sales mix 50% 30% 20%

Rs. Rs. Rs.

Selling price 20 25 28

Variable cost per unit 10 15 14

Total fixed cost 1,50,000

Total sales 5,00,000

Analyses the proposed change and suggest what decision the Company should take.

19

Solution:

Present Position

Products Total

X Y Z

Selling price Rs. 20 25 30

Less : Variable cost Rs. 10 15 18

Contribution Rs. 10 10 12

P/V ratio 50% 40% 40%

Sales mix 40% 35% 25% 100%

Sales Rs. 2,00,000 1,75,000 1,25,000 5,00,000

Contribution (Sales x P/V ratio)

Rs.

1,00,000

70,000

50,000

2,20,000

Less: Fixed cost Rs. 1,50,000

Profit Rs. 70,000

B.E. Point (Rs.1,50,000 44%*) Rs.3,40,909

*Overall P/V ratio = 000,00,5

000,20,2 x 100 = 44%

Proposed Position

Products Total

X Y S

Selling price Rs. 20 25 28

Less : Variable cost Rs. 10 15 14

Contribution Rs. 10 10 14

P/V ratio 50% 40% 50%

Sales mix 50% 30% 20% 100%

Sales Rs. 2,50,000 1,50,000 1,00,000 5,00,000

Contribution (Sales x P/V ratio)

Rs.

1,25,000

60,000

50,000

2,35,000

Fixed cost Rs. 1,50,000

Profit Rs. 85,000

B.E. Point (Rs.1,50,000 47%*) Rs.3,19,149

*Overall P/V ratio = 000,00,5

000,35,2 x 100 = 47%

20

Conclusion: It may thus, be concluded that the proposed change should be acceptable

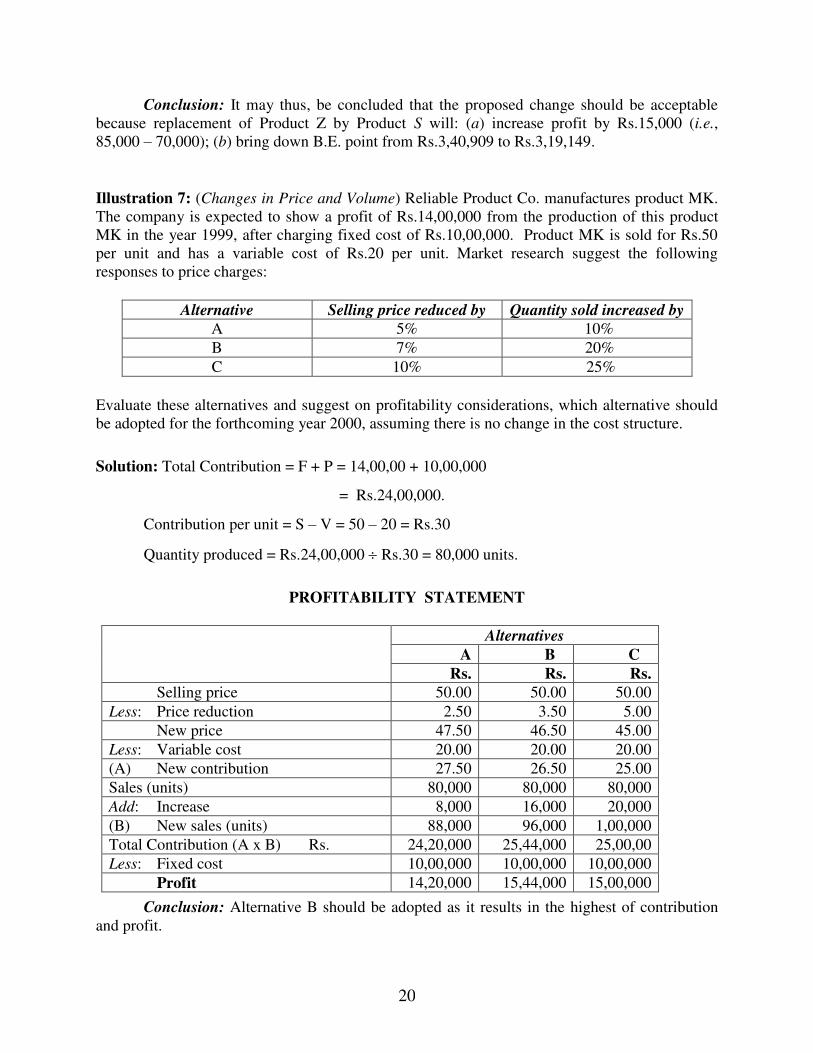

because replacement of Product Z by Product S will: (a) increase profit by Rs.15,000 (i.e.,

85,000 – 70,000); (b) bring down B.E. point from Rs.3,40,909 to Rs.3,19,149.

Illustration 7: (Changes in Price and Volume) Reliable Product Co. manufactures product MK.

The company is expected to show a profit of Rs.14,00,000 from the production of this product

MK in the year 1999, after charging fixed cost of Rs.10,00,000. Product MK is sold for Rs.50

per unit and has a variable cost of Rs.20 per unit. Market research suggest the following

responses to price charges:

Alternative Selling price reduced by Quantity sold increased by

A 5% 10%

B 7% 20%

C 10% 25%

Evaluate these alternatives and suggest on profitability considerations, which alternative should

be adopted for the forthcoming year 2000, assuming there is no change in the cost structure.

Solution: Total Contribution = F + P = 14,00,00 + 10,00,000

= Rs.24,00,000.

Contribution per unit = S – V = 50 – 20 = Rs.30

Quantity produced = Rs.24,00,000 Rs.30 = 80,000 units.

PROFITABILITY STATEMENT

Alternatives

A B C

Rs. Rs. Rs.

Selling price 50.00 50.00 50.00

Less: Price reduction 2.50 3.50 5.00

New price 47.50 46.50 45.00

Less: Variable cost 20.00 20.00 20.00

(A) New contribution 27.50 26.50 25.00

Sales (units) 80,000 80,000 80,000

Add: Increase 8,000 16,000 20,000

(B) New sales (units) 88,000 96,000 1,00,000

Total Contribution (A x B) Rs. 24,20,000 25,44,000 25,00,00

Less: Fixed cost 10,00,000 10,00,000 10,00,000

Profit 14,20,000 15,44,000 15,00,000

Conclusion: Alternative B should be adopted as it results in the highest of contribution

and profit.

21

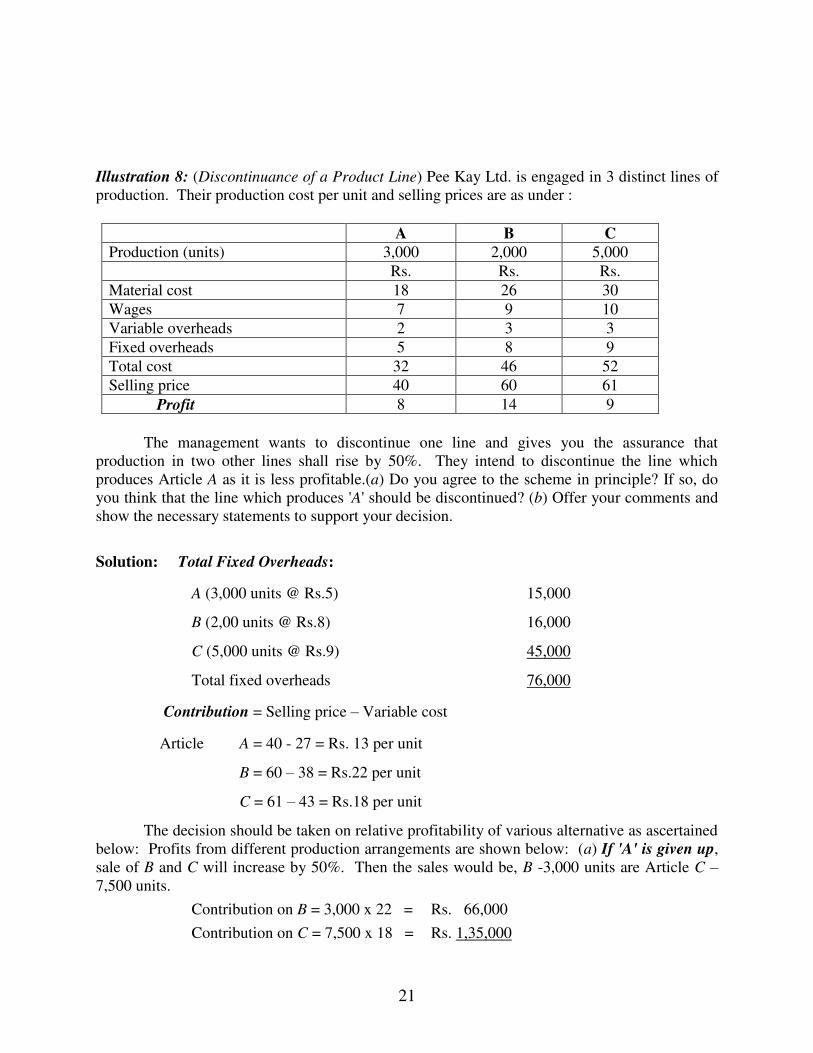

Illustration 8: (Discontinuance of a Product Line) Pee Kay Ltd. is engaged in 3 distinct lines of

production. Their production cost per unit and selling prices are as under :

A B C

Production (units) 3,000 2,000 5,000

Rs. Rs. Rs.

Material cost 18 26 30

Wages 7 9 10

Variable overheads 2 3 3

Fixed overheads 5 8 9

Total cost 32 46 52

Selling price 40 60 61

Profit 8 14 9

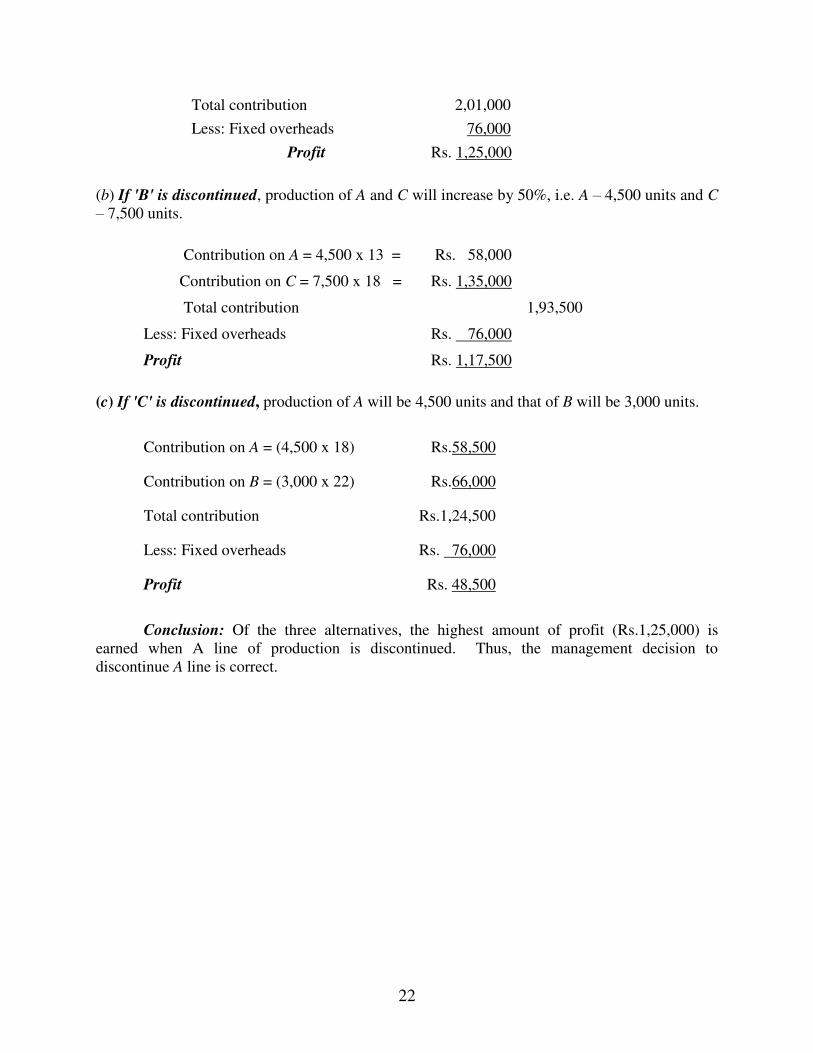

The management wants to discontinue one line and gives you the assurance that

production in two other lines shall rise by 50%. They intend to discontinue the line which

produces Article A as it is less profitable.(a) Do you agree to the scheme in principle? If so, do

you think that the line which produces 'A' should be discontinued? (b) Offer your comments and

show the necessary statements to support your decision.

Solution: Total Fixed Overheads:

A (3,000 units @ Rs.5) 15,000

B (2,00 units @ Rs.8) 16,000

C (5,000 units @ Rs.9) 45,000

Total fixed overheads 76,000

Contribution = Selling price – Variable cost

Article A = 40 - 27 = Rs. 13 per unit

B = 60 – 38 = Rs.22 per unit

C = 61 – 43 = Rs.18 per unit

The decision should be taken on relative profitability of various alternative as ascertained

below: Profits from different production arrangements are shown below: (a) If 'A' is given up,

sale of B and C will increase by 50%. Then the sales would be, B -3,000 units are Article C –

7,500 units.

Contribution on B = 3,000 x 22 = Rs. 66,000

Contribution on C = 7,500 x 18 = Rs. 1,35,000

22

Total contribution 2,01,000

Less: Fixed overheads 76,000

Profit Rs. 1,25,000

(b) If 'B' is discontinued, production of A and C will increase by 50%, i.e. A – 4,500 units and C

– 7,500 units.

Contribution on A = 4,500 x 13 = Rs. 58,000

Contribution on C = 7,500 x 18 = Rs. 1,35,000

Total contribution 1,93,500

Less: Fixed overheads Rs. 76,000

Profit Rs. 1,17,500

(c) If 'C' is discontinued, production of A will be 4,500 units and that of B will be 3,000 units.

Contribution on A = (4,500 x 18) Rs.58,500

Contribution on B = (3,000 x 22) Rs.66,000

Total contribution Rs.1,24,500

Less: Fixed overheads Rs. 76,000

Profit Rs. 48,500

Conclusion: Of the three alternatives, the highest amount of profit (Rs.1,25,000) is

earned when A line of production is discontinued. Thus, the management decision to

discontinue A line is correct.

23

23

3

DIFFERENTIAL COST ANALYSIS

Smriti Chawla Shri Ram College of Commerce

University of Delhi

Meaning

Differential cost is the change in the costs which may take place due to increase or

decrease in output, change in sales volume, alternate method of production, make or buy

decisions, change in product mix etc. So, differential cost is the result of an alternative course

of action. For example, difference in costs may arise because of replacement of labour by

machinery and difference in costs of two alternative courses of action will be the differential

cost.

If change in cost occurs due to change in level of activity, differential cost is referred to

as incremental cost in case of increase in output and decremental cost in case of decrease in

output.

In differential cost analysis costs are calculated on the basis of absorption or total

costing technique, but in marginal costing technique, costs are calculated on the basis of

variable costs only and fixed costs are not taken. But if the alternate course of action does not

CHAPTER OBJECTIVES

Meaning

Characteristics of Differential Cost

Difference between Differential Cost Analysis and Marginal Costing

Practical Applications of Differential Cost Analysis Determination of Optimum level of

production Accept or Reject Decision Adding or Dropping a Product line Make or buy decisions Sell or process decisions Introduction of Additional shift

(with Illustrations)

24

involve any extra fixed costs change in variable costs will become differential costs and there

will be no difference between marginal costs and differential costs.

Differential cost is the change in cost which may result from the adoption of an alternate

course of action or change in the level of activity. Change in cost may take place due to change

in fixed costs and variable costs, so differential cost is the aggregate of changes in fixed costs

and variable costs which take place due to the adoption of an alternate course of action or

change in the level of output.

Characteristics of Differential Cost

The following are the essential characteristics of differential costs:

1. Differential cost analysis is not made within the accounting records rather it is made

outside the accounting records. Differential costs may, however, be incorporated in the

flexible budgets because they budget costs at various levels of activity.

2. Total differential costs are considered in differential cost analysis. Cost per unit is not

taken into consideration.

3. Total differential revenues are compared with total differential costs before advocating

an alternate course of action. A change in course of action is recommended only if

differential revenues exceed differential costs.

4. The items of cost which do not change for the alternatives under consideration are

ignored, only the difference in items of costs are considered because differential costs

analysis is concerned with changes in costs.

5. The changes in costs are measured from a common base point which may be a present

course of action or present level of production.

6. Differential cost analysis is related to the future course of action or future level of

output, so it deals with future costs. Historical costs or standard cots may be used but

they should be suitably adjusted to future conditions.

7. For making a choice among the various alternatives, the alternative which gives the

maximum difference between the incremental revenue and incremental cost is

recommended to be adopted.

Difference Between Differential Cost Analysis and Marginal Costing

Differential costs are often confused with marginal costs; so it is better to compare the

two to remove the confusion. The points of similarity and difference between the two are

summarized as follows:

25

Similarity

1. Both are techniques of cost analysis and cost presentation.

2. Both are used for taking managerial decisions such as effect on profits by following

changes in sales volume, product mix, price or method of production.

3. Marginal costs and differential costs are the same when there is no change in fixed costs on

account of increase or decrease in output.

Difference

1. Under marginal costing technique, fixed costs are not added to get the marginal cost of a

product whereas differential cost analysis takes into consideration changes in fixed costs

due to change in output.

2. Differential cost analysis is helpful in taking the managerial decisions and is not

incorporated in accounting records. In other words, differential costs are calculated

separately as analysis statements. On the other hand, marginal costs may be incorporated

in the accounting records.

3. Marginal costs are calculated on the basis of contribution approach whereas differential

costs may be ascertained on the basis of both absorption costing as well as marginal

costing.

4. In marginal costing, margin of contribution, contribution per unit of limiting factor and

profit-volume ratio are the main yardsticks for evaluating the managerial decisions

whereas in differential cost analysis, differential costs are compared with the differential

revenues of determine whether alternate course of action should be followed or not.

Practical Applications of Differential Costs

Many managerial decisions involving problems of alternative choices are made with the

help of differential cost analysis. Such decisions include the following:

(1) Determination of the Optimum Level of Production

The optimum level is that level of production where profit is the maximum. In order to

arrive at a decision of this type, the differential costs are compared with incremental revenue at

various levels of output. So long as the incremental revenue exceeds differential costs, it is

profitable to increase the output. But as soon as the differential cost equals or exceeds

increments revenue, it is no more profitable to increase the volume of output.

Illustration 1: A company has a capacity of producing 1,00,000 units of a certain product in a

month. The sales department reports that the following schedule of sale prices is possible:

26

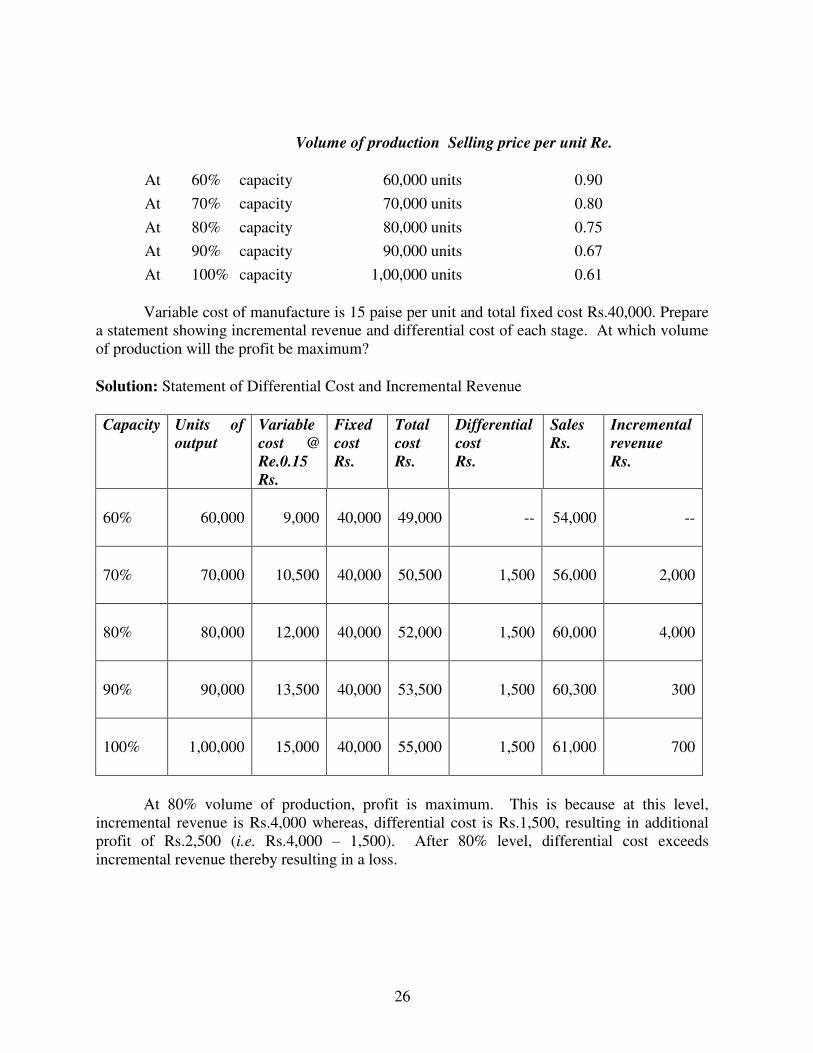

Volume of production Selling price per unit Re.

At 60% capacity 60,000 units 0.90

At 70% capacity 70,000 units 0.80

At 80% capacity 80,000 units 0.75

At 90% capacity 90,000 units 0.67

At 100% capacity 1,00,000 units 0.61

Variable cost of manufacture is 15 paise per unit and total fixed cost Rs.40,000. Prepare

a statement showing incremental revenue and differential cost of each stage. At which volume

of production will the profit be maximum?

Solution: Statement of Differential Cost and Incremental Revenue

Capacity Units of

output

Variable

cost @

Re.0.15

Rs.

Fixed

cost

Rs.

Total

cost

Rs.

Differential

cost

Rs.

Sales

Rs.

Incremental

revenue

Rs.

60% 60,000 9,000 40,000 49,000 -- 54,000 --

70% 70,000 10,500 40,000 50,500 1,500 56,000 2,000

80% 80,000 12,000 40,000 52,000 1,500 60,000 4,000

90% 90,000 13,500 40,000 53,500 1,500 60,300 300

100% 1,00,000 15,000 40,000 55,000 1,500 61,000 700

At 80% volume of production, profit is maximum. This is because at this level,

incremental revenue is Rs.4,000 whereas, differential cost is Rs.1,500, resulting in additional

profit of Rs.2,500 (i.e. Rs.4,000 – 1,500). After 80% level, differential cost exceeds

incremental revenue thereby resulting in a loss.

27

(2) Accept or Reject Decision

Sometimes a concern may receive special offers from its regular customers to sell its

regular products. Special offers may be received from the home customers for one time

quantity sales or sales to foreign customers. Such offers generally are received at lesser prices

than the usual customary prices. The decision to accept or reject special offers is based entirely

on differential cost and the contribution margin approach. The point to be considered is

whether incremental revenue is more than the differential costs to be incurred. The use of

absorption costing is not preferred as it may show misleading results. While deciding about

special offers rejection or acceptance the following factors should be taken into consideration:

(i) The impact on future earnings of temporarily reduction in he selling price.

(ii) The effect of reducing selling prices on the existing customers when it comes to their

knowledge.

(iii) The possibility of selling additional units to the new customers beyond the special offer.

(iv) The reliability of cost estimates associated with the offer.

(v) The effect on current and future capacity in terms of an expansion of plant, personnel,

financial requirements and other capacity constraints.

Illustration 1(Continued): If there is a bulk offer for export at 50 paise per unit for the balance

capacity over the maximum profit volume and the price quoted will not affect the internal sales,

will you advise accepting this bid and why?

Solution:

Internal Market

(80,000 units)

Special Order for

export (20,000

units)

Total

(1,00,000 units)

Rs. Rs. Rs.

Variable cost @

15 paise per unit

12,000 3,000 15,000

Fixed cost 40,000 ------- 40,000

Total Cost 52,000 3,000 55,000

Sales 60,000 10,000 70,000

Profit 8,000 7,000 15,000

It is advisable to accept the bulk offer @ Re.0.50 per unit for the balance capacity of 20,00

units (i.e. 1,00,000 – 80,000) for export as it will result in an increase of profit by Rs.7,000.

28

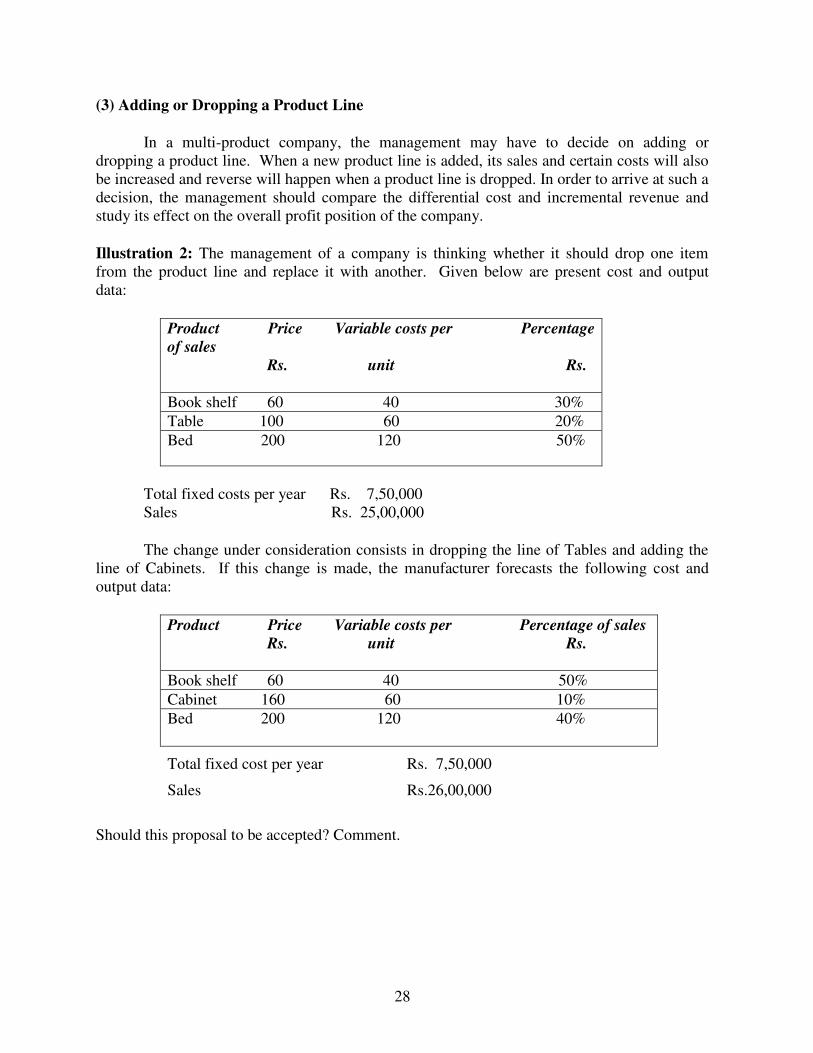

(3) Adding or Dropping a Product Line

In a multi-product company, the management may have to decide on adding or

dropping a product line. When a new product line is added, its sales and certain costs will also

be increased and reverse will happen when a product line is dropped. In order to arrive at such a

decision, the management should compare the differential cost and incremental revenue and

study its effect on the overall profit position of the company.

Illustration 2: The management of a company is thinking whether it should drop one item

from the product line and replace it with another. Given below are present cost and output

data:

Product Price Variable costs per Percentage

of sales

Rs. unit Rs.

Book shelf 60 40 30%

Table 100 60 20%

Bed 200 120 50%

Total fixed costs per year Rs. 7,50,000

Sales Rs. 25,00,000

The change under consideration consists in dropping the line of Tables and adding the

line of Cabinets. If this change is made, the manufacturer forecasts the following cost and

output data:

Product Price Variable costs per Percentage of sales

Rs. unit Rs.

Book shelf 60 40 50%

Cabinet 160 60 10%

Bed 200 120 40%

Total fixed cost per year Rs. 7,50,000

Sales Rs.26,00,000

Should this proposal to be accepted? Comment.

29

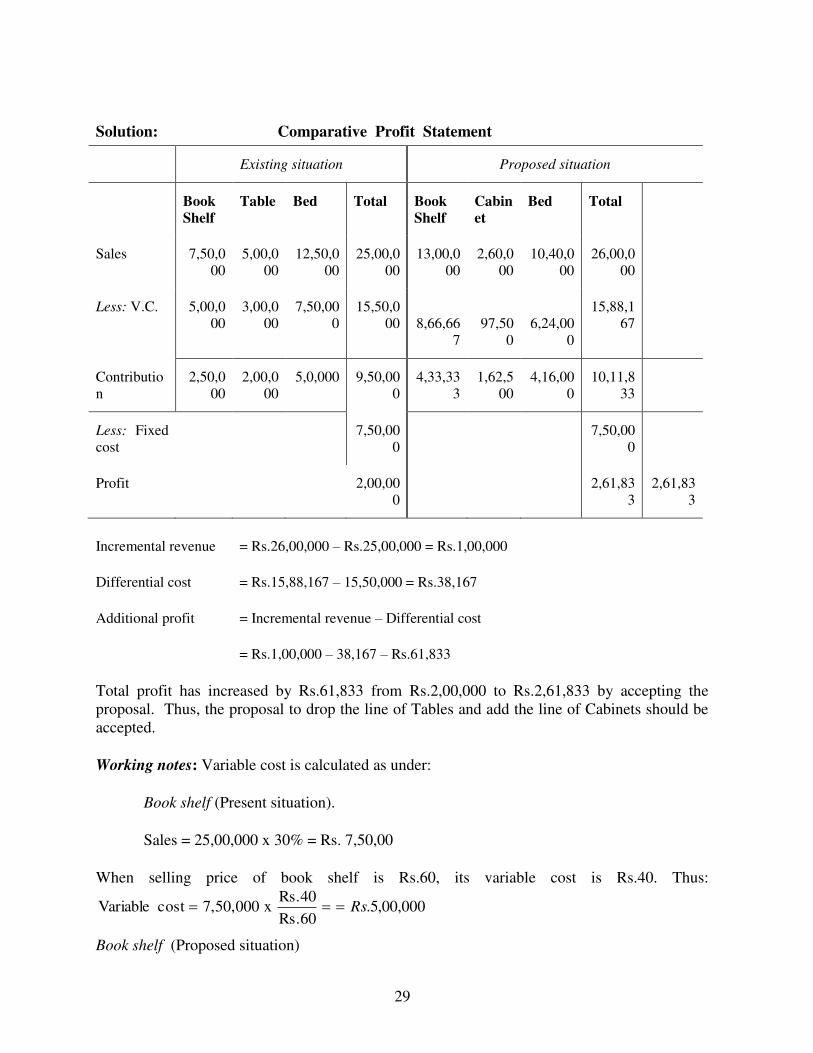

Solution: Comparative Profit Statement

Existing situation Proposed situation

Book

Shelf

Table Bed Total Book

Shelf

Cabin

et

Bed Total

Sales 7,50,0

00

5,00,0

00

12,50,0

00

25,00,0

00

13,00,0

00

2,60,0

00

10,40,0

00

26,00,0

00

Less: V.C. 5,00,0

00

3,00,0

00

7,50,00

0

15,50,0

00

8,66,66

7

97,50

0

6,24,00

0

15,88,1

67

Contributio

n

2,50,0

00

2,00,0

00

5,0,000 9,50,00

0

4,33,33

3

1,62,5

00

4,16,00

0

10,11,8

33

Less: Fixed

cost

7,50,00

0

7,50,00

0

Profit 2,00,00

0

2,61,83

3

2,61,83

3

Incremental revenue = Rs.26,00,000 – Rs.25,00,000 = Rs.1,00,000

Differential cost = Rs.15,88,167 – 15,50,000 = Rs.38,167

Additional profit = Incremental revenue – Differential cost

= Rs.1,00,000 – 38,167 – Rs.61,833

Total profit has increased by Rs.61,833 from Rs.2,00,000 to Rs.2,61,833 by accepting the

proposal. Thus, the proposal to drop the line of Tables and add the line of Cabinets should be

accepted.

Working notes: Variable cost is calculated as under:

Book shelf (Present situation).

Sales = 25,00,000 x 30% = Rs. 7,50,00

When selling price of book shelf is Rs.60, its variable cost is Rs.40. Thus:

000,00,5.Rs.60

Rs.40x7,50,000costVariable Rs

Book shelf (Proposed situation)

30

Sales = 26,00,000 x 50% = Rs.13,00,000

667,66,8.Rs.60

Rs.40x,00,00031costVariable Rs

Similar calculations are made for other lines of products.

(4) Make or Buy Decisions

In assembly type concerns, different components parts are assembled in order to

manufacture the product. Such component parts can be manufactured in the concern or these

can be purchased from external suppliers. If the concern has idle capacity and idle workers that

can be used to make component parts, it is preferable to make and realize cost savings. If there

is no idle capacity, the parts can be purchased from the outside. The other uses of idle capacity

should be examined before reaching a final decision as the available facilities have to be put to

best utilisation. Differential costing technique an be used for solving make or buy problem.

Costs associated with buying and making is to be compared. The sum of purchase price plus

transportation, insurance and ordering cost represents the amount applicable to the buying

alternative. On the other hand costs associated with the make alternative include the

differential variables to make the component parts such as materials, labour and variable

overheads. Allocated fixed costs remain unchanged in aggregate when components are made,

cannot be relevant to make or buy decisions. While making decision not only the present cost

but projections for future costs are to be taken into consideration.

In addition to the quantitative factors discussed above, the qualitative factors which are

taken into consideration to influence the make or buy decision are as follows:

(i) Quality of goods supplied by the supplier.

(ii) Uninterrupted supply by the supplier meeting the delivery dates.

(iii) If secrecy is to be maintained and manufacturing know-how is not to be passed on to the

supplier of the component part, the decision will be to manufacture part even though the

manufacturing cost may be more than the price to be charged by the supplier.

(iv) Any adverse effect on labour relations if it is decided to buy from outside instead of

making.

(v) The facility of wider selection in case of buy-decision.

(5) Sell or Process Decisions

A product can be sold by a company when it has been partially processed or of

processing it further and then selling it. When a product passes through a series of

manufacturing operations, it may be a saleable product at a number of different points along the

way. Thus a company has an option to sell he product at various physical stages of completion.

31

For example in petroleum refinery, the refinement of oil can be stopped a several points during

the process and can be sold as fuel oil, diesel oil, kerosene or gasoline as market exists or all

these intermediate semi-manufactured products. In sell or process decision incremental

analysis provides the solution. In all alternatives incremental revenue is to be compared with

incremental costs after the decision point as all costs incurred before the sell or process further

decision must be treated as sunk costs. The alternative which gives more benefit (incremental

revenue – incremental cost) must be adopted.

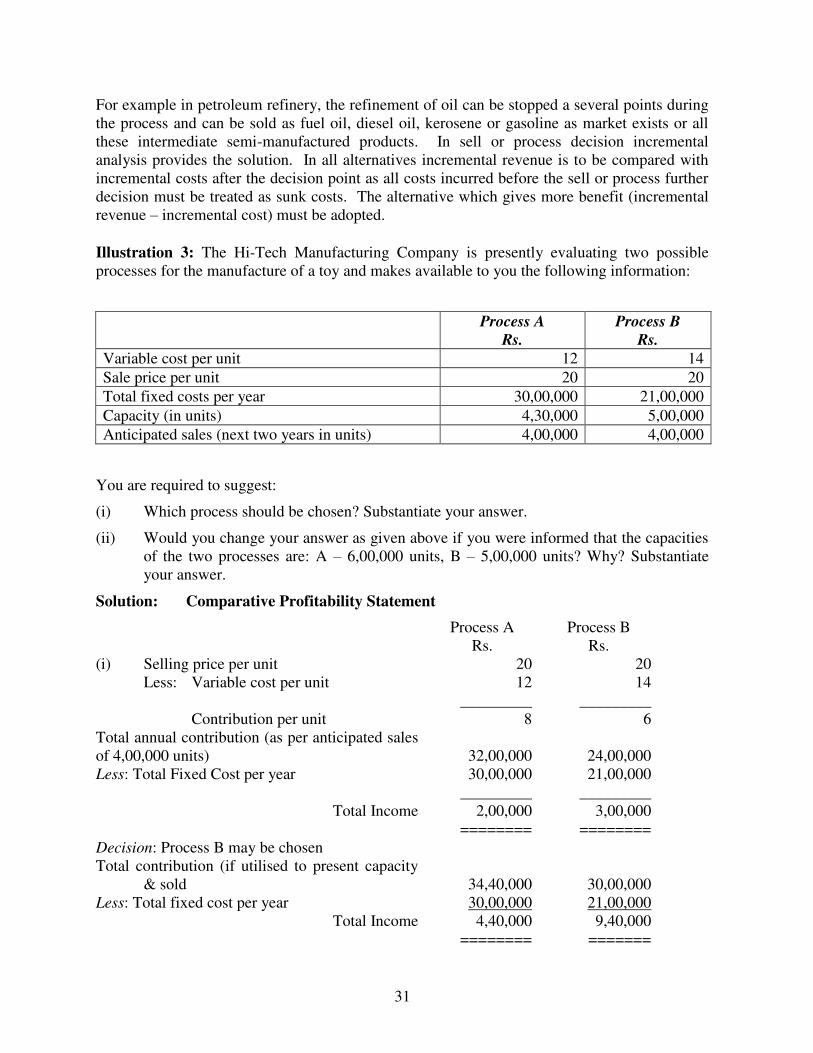

Illustration 3: The Hi-Tech Manufacturing Company is presently evaluating two possible

processes for the manufacture of a toy and makes available to you the following information:

You are required to suggest:

(i) Which process should be chosen? Substantiate your answer.

(ii) Would you change your answer as given above if you were informed that the capacities

of the two processes are: A – 6,00,000 units, B – 5,00,000 units? Why? Substantiate

your answer.

Solution: Comparative Profitability Statement

Process A

Rs.

Process B

Rs.

(i) Selling price per unit

Less: Variable cost per unit

Contribution per unit

Total annual contribution (as per anticipated sales

of 4,00,000 units)

Less: Total Fixed Cost per year

Total Income

20

12

_________

8

32,00,000

30,00,000

_________

2,00,000

20

14

_________

6

24,00,000

21,00,000

_________

3,00,000

======== ========

Decision: Process B may be chosen

Total contribution (if utilised to present capacity

& sold

Less: Total fixed cost per year

34,40,000

30,00,000

30,00,000

21,00,000

Total Income 4,40,000 9,40,000

======== =======

Process A

Rs.

Process B

Rs.

Variable cost per unit 12 14

Sale price per unit 20 20

Total fixed costs per year 30,00,000 21,00,000

Capacity (in units) 4,30,000 5,00,000

Anticipated sales (next two years in units) 4,00,000 4,00,000

32

Decision – Process B may be chosen

(ii) Total contribution (if capacity of A 6,00,000

units and of B 5,00,000 units)

Less: Fixed cost per year

48,00,000

30,00,000

30,00,000

21,00,000

Total Income 18,00,000 9,00,000

Decision: Process A may be chosen

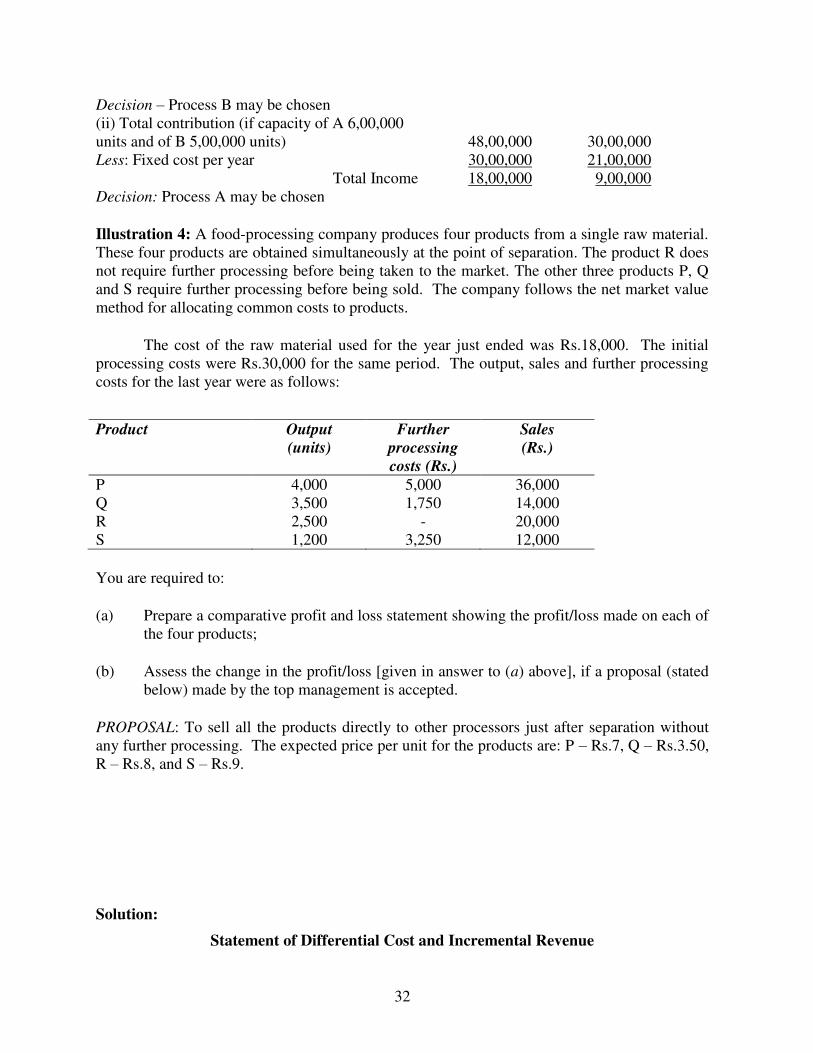

Illustration 4: A food-processing company produces four products from a single raw material.

These four products are obtained simultaneously at the point of separation. The product R does

not require further processing before being taken to the market. The other three products P, Q

and S require further processing before being sold. The company follows the net market value

method for allocating common costs to products.

The cost of the raw material used for the year just ended was Rs.18,000. The initial

processing costs were Rs.30,000 for the same period. The output, sales and further processing

costs for the last year were as follows:

Product Output

(units)

Further

processing

costs (Rs.)

Sales

(Rs.)

P 4,000 5,000 36,000

Q 3,500 1,750 14,000

R 2,500 - 20,000

S 1,200 3,250 12,000

You are required to:

(a) Prepare a comparative profit and loss statement showing the profit/loss made on each of

the four products;

(b) Assess the change in the profit/loss [given in answer to (a) above], if a proposal (stated

below) made by the top management is accepted.

PROPOSAL: To sell all the products directly to other processors just after separation without

any further processing. The expected price per unit for the products are: P – Rs.7, Q – Rs.3.50,

R – Rs.8, and S – Rs.9.

Solution:

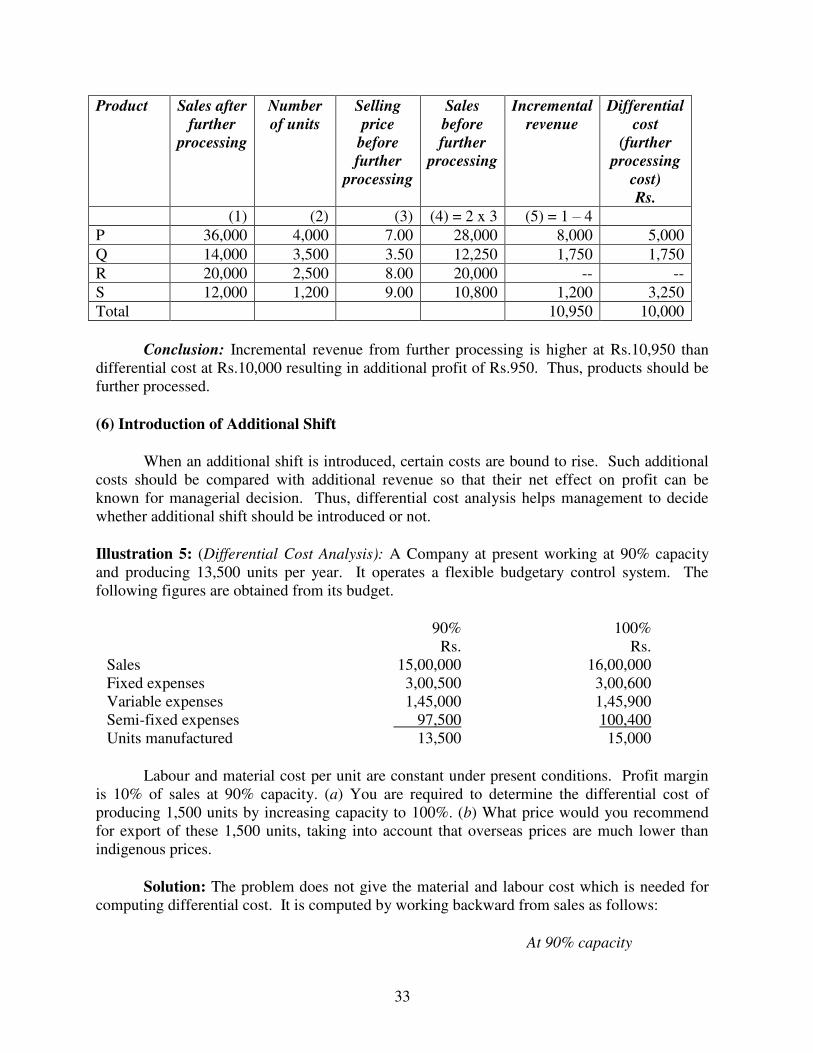

Statement of Differential Cost and Incremental Revenue

33

Product Sales after

further

processing

Number

of units

Selling

price

before

further

processing

Sales

before

further

processing

Incremental

revenue

Differential

cost

(further

processing

cost)

Rs.

(1) (2) (3) (4) = 2 x 3 (5) = 1 – 4

P 36,000 4,000 7.00 28,000 8,000 5,000

Q 14,000 3,500 3.50 12,250 1,750 1,750

R 20,000 2,500 8.00 20,000 -- --

S 12,000 1,200 9.00 10,800 1,200 3,250

Total 10,950 10,000

Conclusion: Incremental revenue from further processing is higher at Rs.10,950 than

differential cost at Rs.10,000 resulting in additional profit of Rs.950. Thus, products should be

further processed.

(6) Introduction of Additional Shift

When an additional shift is introduced, certain costs are bound to rise. Such additional

costs should be compared with additional revenue so that their net effect on profit can be

known for managerial decision. Thus, differential cost analysis helps management to decide

whether additional shift should be introduced or not.

Illustration 5: (Differential Cost Analysis): A Company at present working at 90% capacity

and producing 13,500 units per year. It operates a flexible budgetary control system. The

following figures are obtained from its budget.

90%

Rs.

100%

Rs.

Sales

Fixed expenses

Variable expenses

Semi-fixed expenses

Units manufactured

15,00,000

3,00,500

1,45,000

97,500

13,500

16,00,000

3,00,600

1,45,900

100,400

15,000

Labour and material cost per unit are constant under present conditions. Profit margin

is 10% of sales at 90% capacity. (a) You are required to determine the differential cost of

producing 1,500 units by increasing capacity to 100%. (b) What price would you recommend

for export of these 1,500 units, taking into account that overseas prices are much lower than

indigenous prices.

Solution: The problem does not give the material and labour cost which is needed for

computing differential cost. It is computed by working backward from sales as follows:

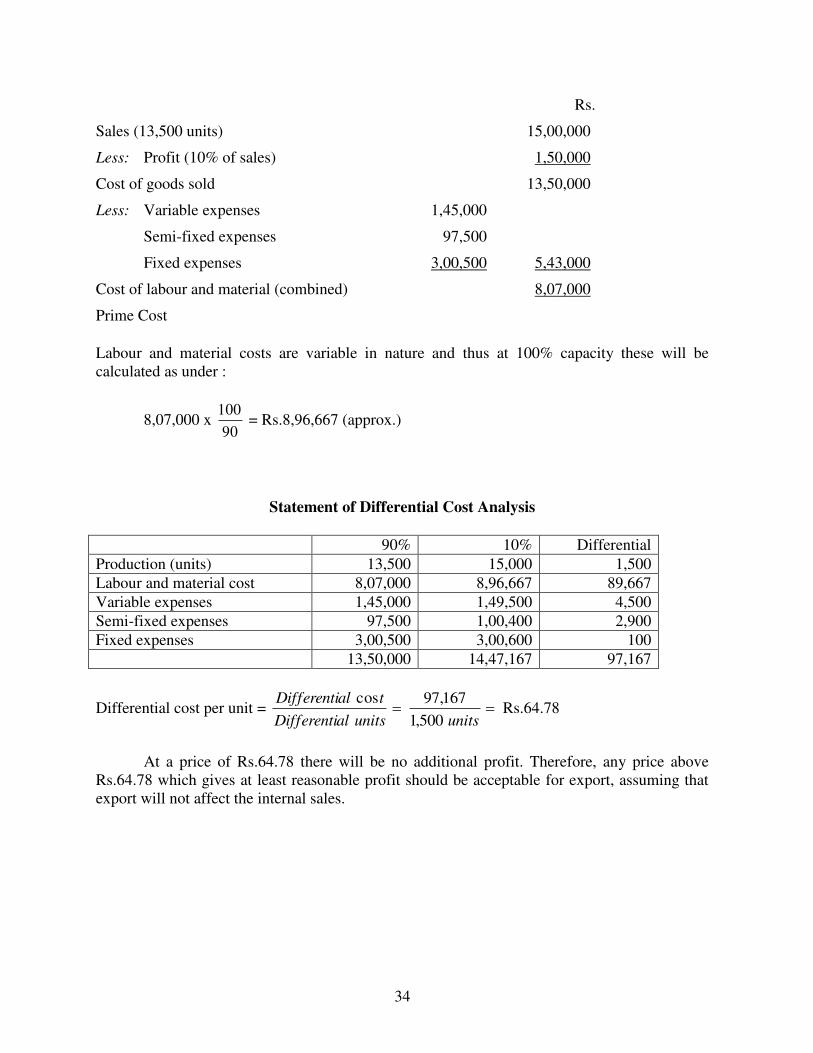

At 90% capacity

34

Rs.

Sales (13,500 units) 15,00,000

Less: Profit (10% of sales) 1,50,000

Cost of goods sold 13,50,000

Less: Variable expenses 1,45,000

Semi-fixed expenses 97,500

Fixed expenses 3,00,500 5,43,000

Cost of labour and material (combined) 8,07,000

Prime Cost

Labour and material costs are variable in nature and thus at 100% capacity these will be

calculated as under :

8,07,000 x 90

100 = Rs.8,96,667 (approx.)

Statement of Differential Cost Analysis

90% 10% Differential

Production (units) 13,500 15,000 1,500

Labour and material cost 8,07,000 8,96,667 89,667

Variable expenses 1,45,000 1,49,500 4,500

Semi-fixed expenses 97,500 1,00,400 2,900

Fixed expenses 3,00,500 3,00,600 100

13,50,000 14,47,167 97,167

Differential cost per unit = unitsunitsalDifferenti

talDifferenti

500,1

167,97cosRs.64.78

At a price of Rs.64.78 there will be no additional profit. Therefore, any price above

Rs.64.78 which gives at least reasonable profit should be acceptable for export, assuming that

export will not affect the internal sales.

35

UNIT 6

1

RESPONSIBILITY ACCOUNTING

Smriti Chawla Shri Ram College of Commerce

University of Delhi

Meaning and Definition of Responsibility Accounting

One of the fundamental functions of management accounting is facilitating managerial

control. Various devices are used by the management in performing this important function.

Responsibility accounting is one of the most recent developments in this field. The concept of

responsibility accounting is closely related to the systems of budgetary control and standard

costing.

Responsibility accounting is a system of control where responsibility is assigned for the

control of costs. The persons are made responsible for the control of costs. Proper authority is

given to the persons so that they are able to keep up their performance. In case the performance

is not according to the predetermined standards then the persons who are assigned this duty will

be personally responsible for it. In responsibility accounting the emphasis is on men rather than

on systems.

CHAPTER OBJECTIVES

Meaning and Definition of Responsibility Accounting

Essential Features of Responsibility Accounting Steps involved in Responsibility Accounting

Advantages of Responsibility Accounting Limitations of Responsibility Accounting Responsibility Centres

Types of Responsibility Centres o Cost Centre o Profit Centre

o Revenue Centre o Investment Centre

Transfer Prices Lets Sum Up Questions

36

Charles T. Hongreen. “Responsibility accounting is a system of accounting that recognizes various decision centres throughout an organization and traces costs to the individual

managers who are primarily responsible for making decisions about the costs in question”. Louderback and Dominiak, “Responsibility accounting is the name given to that

respect of the managerial process dealing with the reporting of information to facilitate control of

operations and evaluation of performance.”

Institute of Cost and Works Accountants of India, “Responsibility Accounting is a system of management accounting under which accountability is established according to the

responsibility delegated to various levels of management and a management information and

reporting system instituted to give adequate feedback in terms of delegated responsibility. Under

this system divisions or units of an organization under a specified authority in a person are

developed responsibility centres and evaluated individually for their performance.”

Hence, responsibility accounting focuses main attention on responsibility centres. The

managers of different activity centres are responsible for controlling the costs of their centres.

Information about costs incurred for different activities is supplied to the persons incharge of

various centre. The performance is constantly compared to the standards set and this process is

very useful in exercising cost control. Responsibility accounting is different from cost

accounting is different from cost accounting in the sense that the future lays emphasis on cost

control whereas the latter lays emphasis on cost ascertainment.

Essential Features of Responsibility Accounting

An analysis of the definitions given above reveals the following important features or

fundamental aspects of responsibility accounting-

(a) Inputs and outputs or Costs and Revenues: The implementation and maintenance of

responsibility accounting system is based upon information relating to inputs and

outputs. The physical resources utilized in an organization such quantity of raw material

used, labour hours consumed are termed as inputs. These inputs expressed in monetary

terms are known as costs. Similarly output expressed in monetary terms are called

revenue.

(b) Planned and Actual Information or Use of Budgeting: Effective responsibility

accounting requires both planned and actual financial information. It is not only

historical cost and revenue data but also planned future data which is essential for

implementation of responsibility accounting system. It is through budgets that

responsibility for implementing plans is communicated to each level of management.

(c) Identification of Responsibility Centres: The responsibility centres represent the sphere

of authority or decision points in an organisation. However, for effective control a large

firm is divided into meaningful segments, departments or divisions, which are called

responsibility centres. A responsibility center is under the control of an individual who is

responsible for control of activities of that sub unit of the organisation.

(d) Relationship Between Organisation Structure and Responsibility Accounting System:

Responsibility accounting system must be so designed as to suit the organization

structure of organization. It must be founded upon existing authority responsibility

relationship in organization. In fact, responsibility accounting system should parallel the

37

organisation structure and provide financial information to evaluate actual results of each

individual responsible for a function.

(e) Performance Reporting: Responsibility accounting is a control device. A control

system to be effective should be such that deviations from the plans must be reported at

earliest so as to take corrective action for future. The deviations can be known only when

performance is reported. Thus, responsibility accounting system is focused on

performance reports also known as ‘responsibility reports’, prepared for each responsibility unit.

(f) Participative Management: The function of responsibility accounting system becomes

more effective if participative style of management is followed, wherein, the plans are

laid according to mutual consent and decisions reached after consulting the subordinates.

It provides motivation to workers by ensuring their participation and self imposed goals.

(g) Management by Exception: An effective responsibility accounting system must provide

for management by exception i.e, it should focus attention of management on significant

deviations and not burden them with all kinds of routine matters, rather condensed

reports requiring their attention must be sent to them particularly at higher levels of

management.

(h) Human Aspect of Responsibility Accounting. To ensure success of responsibility

accounting system it must look into human aspect also by considering needs of

subordinates, developing mutual interests, providing information about control measures

and adjusting according to requirements.

(i) Transfer Pricing Policy: In a large-scale enterprise having decentralised divisions, there

is common practice of transfering goods and services from one segment of organization

to other. In such situations, there is a need to determine the price at which the transfer

should take place so that costs and revenues could be properly assigned. The significance

of the transfer price can well be judged from the fact that for the transfering division it

will be source of revenue, whereas for division to which transfer is made it will be

element of cost. Hence, there is need of having proper transfer policy for successful

implementation of responsibility accounting system.

Steps involved in Responsibility Accounting

Responsibility accounting is used as a control device. The aim of responsibility is to help

management in achieving organisational goals. The following steps are involved in responsibility

accounting:

1. The organisation is divided into various responsibility centres. Each responsibility

centre is put under charge of responsibility manager. The managers are responsible

for the performance of their departments.

2. The targets of each responsibility centre are set in. The targets are set in consultation

with manager of responsibility centre so that he may be able to give full information

about his department. The goals of the responsibility centres are properly

communicated to them.

38

3. The actual performance of each responsibility centre is recorded and communicated

to executive concerned and actual performance is compared with goals set and it

helps in assessing the work of these centres.

4. If the actual performance of a department is less than the standard set, then variances

are conveyed to the top management.

5. Timely action is taken to take necessary corrective measures so that work does not

suffer in future. The directions of top-level management are communicated to

concerned responsibility centre so that corrective measures are initiated at earliest.

Significance of Responsibility Accounting

Responsibility is very important in every type of business. The following are some of the

advantages of responsibility accounting.

1. Assigning of Responsibility: Each and every individual in organisation is assigned some

responsibility and they are accountable for their work. Everybody knows what is

expected of him. No body can shift responsibility to anybody else if something goes

wrong. So, under this system responsibility is assigned individually.

2. Improves Performance: The persons incharge for different activities know that their

performance will be reported to top management. They will try to improve their

performance. On the other hand, it acts as a deterrent for low performance also because

persons know that they are accountable for their work and they will have to explain for

their low performance.

3. Helpful in cost planning: Under system of responsibility accounting full information is

collected about costs and revenues. This data is helpful in planning of future costs and

revenues, fixing of standards and preparing of budgets.

4. Delegation and Control: This system enables the management to delegate authority

while retaining overall control. The authority is delegated according to requirements of