Gp consumer behaviour for third party at private banks

79

CONSUMER BEHAVIOR TOWARDS THIRD PARTY PRODUTS (TPP) IN INDIAN PRIVATE SECTOR BANKING A grand project report submitted in Partial Fulfillment of award of MBA degree Submitted by: Palak Khoda Roll No. 41 & Hetal Barot Roll No: 08 Project Guide: Prof. Pratima Prakash S.K.Patel Institute of Management & Computer Studies Gandhinagar, India 2006 1

-

Upload

hardik-sorathiya -

Category

Documents

-

view

39 -

download

0

Transcript of Gp consumer behaviour for third party at private banks

CONSUMER BEHAVIOR TOWARDS THIRD PARTY PRODUTS (TPP) IN

INDIAN PRIVATE SECTOR BANKING

A grand project report submitted in Partial Fulfillment of award of MBA degree

Submitted by:Palak KhodaRoll No. 41

&Hetal BarotRoll No: 08

Project Guide:Prof. Pratima Prakash

S.K.Patel Institute of Management & Computer StudiesGandhinagar, India

2006

1

CERTIFICATE

This is to certify that Miss. Hetal Barot and Miss. Palak Khoda the students of MBA 2nd year of S.K.Patel Institute of Management and Computer Studies Gandhinagar have completed their Grand Project “CONSUMER BEHAVIOR TOWARDS THIRD PARTY PRODUCTS IN INDIAN PRIVATE SECTOR BANKING” in the year 2004-2006 in partial fulfillment of Gujarat University requirements for the award of the degree of Master of Business Administration.

-------------------------- ----------------------------- ---------------------Prof. S.Chinnam Reddy Dr. S.G.Das Prof. Pratima PrakashDirector ` Co-ordinator Grand Project Guide

2

DECLARATION

We here by declare that the Grand Project title “Consumer Behavior towards Third Party Products in Indian Private Sector Banking” is our original work and has not been published elsewhere. This has been undertaken for the purpose of partial fulfillment of Gujarat University requirements for the award of the Degree of Master of Business Administration.

Student’s Name Signature

Palak KhodaHetal Barot

Date:

3

PREFACE

Today’s finicky customers will settle for noting less. The customer has come to realize somewhat belatedly that he is the king. The customer’s choice of one entity over another as his principal bank is determined by consideration of service quality rather than any other factor. He wants competitive loan rates but at the same time also wants his loan or credit card application processed in double quick time.

As the traditional system is concern Banks mean that where there is cash transactions are processing, where the receipts and payments or withdrawal and deposits are made. But, now in a modern context Banks becomes the Basket of products. Now a days, banks are offering the Third Party products like Mutual Funds, Insurance and other financial securities products like Demat Accounts etc. along with the Saving Accounts, Current Accounts, Fixed Deposits, Over-draft, Term Loans and Cash-Credit etc.

So, as the mind set of the customers are concern some still not accepted the concept of Banking with basket of products. Still there are banking customers who believe that Banking should be for the only cash transactions and taking and giving of money.

So, to know the consumer behavior towards this concept and the expectations of the consumers from the banks for the third party products and to analyze the perception gap we had taken 3 Private Sector Banks and analyze the products which they are offering and surveyed the Bank Consumers. The Products of Banks which we analyzed are

- Centurion Bank of Punjab- HDFC Bank- ICICI Bank

This is a some how new concept in the Indian Private Sector Banking so researches are made on it for the acceptance but here we tried to enlighten the expectations of the consumers plus also thrown the light on the perception gap exist for the same.

4

ACKNOWLEDGEMENT

It is really a matter of pleasure for us to get an opportunity to thank all the persons who contributed directly or indirectly for the successful completion of the project report “Consumer Behavior towards Third Party Products in Indian Private Sector Banking”.

First of all we are extremely helpful to our college S.K.PATEL INSTITUTE OF MANAGEMENT & COMPUTER STUDIES for providing us with this opportunity and for al its cooperation and contribution. We also express our gratitude to our honorable director Prof. S.Chinnam Reddy , and are highly thankful to our project guide Prof. Pratima Prakash for giving us the encouragement and freedom to conduct our project.

We are also grateful to our coordinator Dr.S.G.Das and all our faculty members for their valueable guidance and suggestions for our entire study.

We are greatly thankful to Mr. Dhaval Barot, Relationship Manager- Centurion Bank of Punjab, Ahmedabad, for providing us guidance and helping us for the entire study.

Last but not least we are thankful to all the friends and all other persons who directly or indirectly help us for this project.

Palak Khoda Hetal Barot

5

EXECUTIVE SUMMARY

The report “Consumer Behavior Towards Third Party Products in Indian Private Sector Banking” aims to the assimilate data about the various aspects of the consumers behavior regarding the behaviors of the consumers towards the Third Party Products of the Indian Private Sector Banking and to know the acceptance of and the expectations of the consumers from Third Party Products of the Indian Private Sector Banking.

For this we surveyed the consumers of 3 Banks viz.

HDFC Bank

ICICI Bank

Centurion Bank of Punjab

The report is a mixture of secondary and primary data with Questionnaires being our major instrument to collect primary data.

6

INDUSTRY PROFILE

7

INDIAN BANKING SECTOR

Banking in India has its origin as early as the Vedic period. It is believed that the

transaction from money lending to banking must have occurred even before

menu, the great Hindu jurist, who has devoted a section of his work to deposit

his advances and laid down rules relating to rest of interest. During the Mogul

period, the indigenous bankers played a very important role in lending money

and financing foreign trend commerce. During the day of east India Company, it

was the turn of the agency houses to carry on banking business. The general

bank of India was the first joint stock bank to t be established in the year

1786.the other which followed where the bank of Hindustan and Bengal bank.

The bank of Hindustan is reported to have continued till 1906 while the other

two failed in mean time. In the first half of the 19 century the east India company

established three bank, the bank of Bengal in 1809, the bank of Bombay in

1840,the bank of madras in 1843. This three banks also known as residency

bank, where independent units and functioned well. this tree banks where

amalgamated in 1920 and new bank, the imperial bank of India was established

on 27th jan,1921.with passing of the state bank of India act in 1955the

undertaking of the imperial bank of India was taken by the newly constituted

state bank of India. The reserve bank which is the central bank was creatsd in

1935 by passing reserve bank of India act 1934.in the wakw of the Swadeshi

movement, a numbers of banks with Indian management were established in the

country namely, Punjab national bank ltd, bank of India ltd. canara bank ltd,

Indian bank ltd,the bank of Baroda ltd, central bank of India ltd. On July

19,1969,14 major banks of the country were nationalized and 15th April 1980 six

more commercial private sector banks were also taken over by the government.

Today the commercial banking system in India may be distinguished into:

8

Public sector bank

a. state bank of India and its associated banks called the state bank group

b. 20 nationalized bank

c. regional rural banks mainly sponsored by public sector banks

Private sector banks

a. old generation private bank

b. new generation private banks

c. foreign banks in India

d. scheduled co-operation banks

e. non scheduled banks

Co operative sector

9

The co-operative banking sector has been developed in the country to the

supplement the village money lender. the co operative banking sector in India is

devided into 4 components:

1. State co-operative bank

2. Central co-operative bank

3. Primary agriculture credit societies

4. Land development bank

5. Urban co-operative banks

6. Primary Agriculture development banks

7. Primary land development banks

8. State land development banks

Development banks

10

1. Industrial finance corporation (IFCI)

2. Industrial development bank of India (IDBI)

3. Industrial investment bank of India (IIBI)

4. Industrial credit and investment corporation of India (ICICI)

5. Small industries development bank of India (SIDBI)

6. SCICI LTD.

7. National bank for agriculture and rural development (NABARD)

9. National housing bank

STATUS OF INDIAN BANKING INDUSTRY

11

It is useful to note some telling facts about the Indian banking industry

juxtaposed with other countries, recognizing the differences between the

developed and the emerging economies.

First, the structure of the industry: In the world’s top 1000 banks, the there are

many more large and medium-sized domestic banks from the developed

countries than from the emerging economies. Illustratively, according to The

Banker 2004, out of the top 1000 banks globally, over 200 are located in USA,

just above 100 in Japan, over 80 in Germany, over 40 in Spain and around 40 in

the UK. Even China has as many as 16 banks within the top 1000, out of which,

as many as 14 are in the 500, India, on the other hand, had 20 banks within the

top 500 banks. This is perhaps reflective of differences in size of economies and

of financial sectors.

Second, the share of bank assets in the aggregate financial sector assets: In most

emerging markets, banking sector assets comprise well over 80 per cents of total

financial sector assets, whereas these figures are much lower in the developed

economies. Furthermore, deposits as a share of total bank liabilities have

declined since 1990 in many developed countries, while in developing countries

public deposits continue to be dominant in banks. In India, the share of banking

assets is around 75 per cent, as of end-March 2004. There is, no doubt, merit in

recognizing the importance of diversification in the institutional and instrument

specific aspects of financial intermediation in the interest of wider choice,

competition and stability.

However, the dominant role of banks in financial intermediation in emergence

economies and particularly in India will continue in the medium term and the

12

banks will continue to be special for a long time. In this regard, it is useful t

emphasis the dominance of the banks in the developing countries in promoting

non-bank financial intermediaries and service including in development of debt

market. Even where role of banks is apparently diminishing in the emerging

markets, substantively, they continue to play a leading role in non-banking

financial activities, including the development of finance markets.

Third, internationalization of banking operations: The foreign controlled banking

assets, as a proportion of total domestic banking assets, increased significantly in

several European countries (Austria, Ireland, Spain, Germany and Nordic

countries), but increases have been fairly small in some others (UK and

Switzerland). Amongst the emerging economies, while there was marked

increase of foreign controlled ownership in several Latin American economies,

the increase has, at best, been modest in the Asian economies. Available

evidence seems to indicate some correlation between the extent of liberalization

of capital account in the emerging markets and the share of assets controlled by

foreign banks. as per the evidence available, the form of branches, seem to enjoy

on par with domestic banks, as compared with most of the other developing

countries. Furthermore, the profitability of their operation in India is

considerably higher than the foreign banks operation in most other developing

countries. India continues to grant branch licenses more liberally than the

commitments made to the W.T.O

Fourth, the Share of state owned banks in total banking sector assets: Emerging

economies with predominantly government owned banks, tend to have much

13

higher state ownership of banks compared to their developed counterparts. while

many emerging countries choose to privatized their public sector banking

industries after a process of absorption of the overhang problems by the

government, we have encouraged state run banks to diversify ownership by

inducting private share capital through public offerings rather than by strategic

sales and still absorb the overhang problems. the process has helped reduced the

burden on the govt, enhance transparency, encourage market displined and

improved efficiency as reflected in stock market valuation promote efficient new

private sector banks, while drastically reducing the share of the wholly

government owned public sector banks is a good example of a dynamic mix of

public and privet ownership in banks.

A noteworthy feature of banking reforms in India is the growth of newly

licensed privet sector banks, some of which have attained globally best standards

in terms of technology, services and sophistically promoted banks have

surpassed branches of foreign banks in India. And could be a role model for

other banks.

14

BANK SYSTEM

Introduction

The reserve bank of India (RBI) is India’s central bank. Through the banking

industry is currently dominated by public sector banks, numerous privet and

foreign banks exist. India’s govt owned banks dominate the market. Their

performance has been mixed with a few being consistently profitable. Several

public sector banks are being restructured, and in some the govt either already

has or will reduce its ownership.

Private and foreign banks

The RBI has granted operating approval to a few privately owned domestic

banks; of these many commenced banking business. Foreign banks operate more

than 150 branches in India. The entry of foreign banks is based on reciprocity,

economic and political bilateral relations. An inter-departmental committee

approves applications for entry and expansion.

Capital adequacy norm

Foreign banks were required to achieve an 8% capital adequacy norm by march

1993, while Indian banks with overseas branches had until march 1995 to meet

that target. All other banks had to do so by march 1996. the banking sector is to

be use as a model for opening up of India’s insurance sector to privet domestic

and foreign participants, while keeping the insurance companies in operation.

Banking

India has an extension banking network, in both urban and rural areas. All large

Indian banks are nationalized, and all Indian financial institutes are in the public

sector.

RBI Bank

15

The reserve bank of India is the central banking institutions. It is the sole

authority for issuing bank notes and the supervisory for banking operations in

India.

It supervises and administers exchange control and banking regulations, and

administers the govt’s monitory policy. It is also responsible granting licenses

for new bank branches. 25 foreign banks operate in India with full banking

licenses. Several licenses for private bank have been approved. Despite fairly

broad banking coverage nation wide, the financial system remains inaccessible

to the poorest people in India.

Indian banking system

The banking system has three tiers. These are then scheduled commercial banks:

the regional rural banks which operate in rural areas not covered by the

scheduled banks;

And the cooperative and special rural banks.

Scheduled and scheduled banks

There are approximately 80 scheduled commercial banks, Indian and forign;

almost 200 regional rural banks; more than 350 central cooperatives banks,20

land development banks; and a number of primary agricultural credit societies

.in terms of business , the public sector banks, namely the state bank of India and

the nationalized banks, dominate the banking sector.

Logical financing

16

All sources of local financing are available to foreign-participation companies in

corporate in India, regardless of the extent of foreign participation. Under

foreign exchange regulations, foreigners and non-residents, including foreign

companies,

Require the permission of the reserv bank of India to borrow from a person or

company resident in india

17

THIRD PARTY PRODUCTS

18

Today Indian Private Sector Banks started to deal with the Third Party Products. Now a days Private Banks are selling the Third Party Products like Mutual Funds and Insurance mainly.

Let us see both the industry in detail.

MUTUAL FUNDSHistory of the Indian Mutual Fund Industry

The mutual fund industry in India started in 1963 with the formation of Unit Trust of India, at the initiative of the Government of India and Reserve Bank the. The history of mutual funds in India can be broadly divided into four distinct phases

First Phase – 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament. It was set up by the Reserve Bank of India and functioned under the Regulatory and administrative control of the Reserve Bank of India. In 1978 UTI was de-linked from the RBI and the Industrial Development Bank of India (IDBI) took over the regulatory and administrative control in place of RBI. The first scheme launched by UTI was Unit Scheme 1964. At the end of 1988 UTI had Rs.6,700 crores of assets under management. Second Phase – 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks and Life Insurance Corporation of India (LIC) and General Insurance Corporation of India (GIC). SBI Mutual Fund was the first non- UTI Mutual Fund established in June 1987 followed by Canbank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89), Indian Bank Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund (Oct 92). LIC established its mutual fund in June 1989 while GIC had set up its mutual fund in December 1990.

At the end of 1993, the mutual fund industry had assets under management of Rs.47,004 crores.

19

Third Phase – 1993-2003 (Entry of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian mutual fund industry, giving the Indian investors a wider choice of fund families. Also, 1993 was the year in which the first Mutual Fund Regulations came into being, under which all mutual funds, except UTI were to be registered and governed. The erstwhile Kothari Pioneer (now merged with Franklin Templeton) was the first private sector mutual fund registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and revised Mutual Fund Regulations in 1996. The industry now functions under the SEBI (Mutual Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual funds setting up funds in India and also the industry has witnessed several mergers and acquisitions. As at the end of January 2003, there were 33 mutual funds with total assets of Rs. 1,21,805 crores. The Unit Trust of India with Rs.44,541 crores of assets under management was way ahead of other mutual funds.

Fourth Phase – since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was bifurcated into two separate entities. One is the Specified Undertaking of the Unit Trust of India with assets under management of Rs.29,835 crores as at the end of January 2003, representing broadly, the assets of US 64 scheme, assured return and certain other schemes. The Specified Undertaking of Unit Trust of India, functioning under an administrator and under the rules framed by Government of India and does not come under the purview of the Mutual Fund Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered with SEBI and functions under the Mutual Fund Regulations. With the bifurcation of the erstwhile UTI which had in March 2000 more than Rs.76,000 crores of

20

assets under management and with the setting up of a UTI Mutual Fund, conforming to the SEBI Mutual Fund Regulations, and with recent mergers taking place among different private sector funds, the mutual fund industry has entered its current phase of consolidation and growth. As at the end of September, 2004, there were 29 funds, which manage assets of Rs.153108 crores under 421 schemes.

The graph indicates the growth of assets over the years.

GROWTH IN ASSETS UNDER MANAGEMENT

Note:Erstwhile UTI was bifurcated into UTI Mutual Fund and the Specified Undertaking of the Unit Trust of India effective from February 2003. The Assets under management of the Specified Undertaking of the Unit Trust of India has therefore been excluded from the total assets of the industry as a whole from February 2003 onwards.

Mutual Funds: An overview

21

Introduction

A Mutual Fund is a trust that pools the savings of a number of investors who share a common financial goal. The money thus collected is invested by the fund manager in different types of securities depending upon the objective of the scheme. These could range from shares to debentures to money market instruments. The income earned through these investments and the capital appreciation realized by the scheme are shared by its unit holders in proportion to the number of units owned by them (pro rata). Thus a Mutual Fund is the most suitable investment for the common man as it offers an opportunity to invest in a diversified, professionally managed portfolio at a relatively low cost. Anybody with an investible surplus of as little as a few thousand rupees can invest in Mutual Funds. Each Mutual Fund scheme has a defined investment objective and strategy.

A mutual fund is the ideal investment vehicle for today’s complex and modern financial scenario. Markets for equity shares, bonds and other fixed income instruments, real estate, derivatives and other assets have become mature and information driven. Price changes in these assets are driven by global events occurring in faraway places. A typical individual is unlikely to have the knowledge, skills, inclination and time to keep track of events, understand their implications and act speedily. An individual also finds it difficult to keep track of ownership of his assets, investments, brokerage dues and bank transactions etc.

A mutual fund is the answer to all these situations. It appoints professionally qualified and experienced staff that manages each of these functions on a full time basis. The large pool of money collected in the fund allows it to hire such staff at a very low cost to each investor. In effect, the mutual fund vehicle exploits economies of scale in all three areas - research, investments and transaction processing. While the concept of individuals coming together to invest money collectively is not new, the mutual fund in its present form is a 20th century phenomenon. In fact, mutual funds gained popularity only after the Second World War. Globally, there are thousands of firms offering tens of thousands of mutual funds with different investment objectives. Today, mutual funds collectively manage almost as much as or more money as compared to banks.

A draft offer document is to be prepared at the time of launching the fund. Typically, it pre specifies the investment objectives of the fund, the risk associated, the costs involved in the process and the broad rules for entry into and exit from the fund and other areas of operation. In India, as

22

in most countries, these sponsors need approval from a regulator, SEBI (Securities exchange Board of India) in our case. SEBI looks at track records of the sponsor and its financial strength in granting approval to the fund for commencing operations.

A sponsor then hires an asset management company to invest the funds according to the investment objective. It also hires another entity to be the custodian of the assets of the fund and perhaps a third one to handle registry work for the unit holders (subscribers) of the fund.

In the Indian context, the sponsors promote the Asset Management Company also, in which it holds a majority stake. In many cases a sponsor can hold a 100% stake in the Asset Management Company (AMC). E.g. Birla Global Finance is the sponsor of the Birla Sun Life Asset Management Company Ltd., which has floated different mutual funds schemes and also acts as an asset manager for the funds collected under the schemes.

23

BENEFITS OF MUTUAL FUNDS

Professional Management

Mutual Funds provide the services of experienced and skilled professionals, backed by a dedicated investment research team that analyses the performance and prospects of companies and selects suitable investments to achieve the objectives of the scheme.

Diversification

Mutual Funds invest in a number of companies across a broad cross-section of industries and sectors. This diversification reduces the risk because seldom do all stocks decline at the same time and in the same proportion. You achieve this diversification through a Mutual Fund with far less money than you can do on your own.

Convenient Administration

Investing in a Mutual Fund reduces paperwork and helps you avoid many problems such as bad deliveries, delayed payments and follow up with brokers and companies. Mutual Funds save your time and make investing easy and convenient.

Return Potential

Over a medium to long-term, Mutual Funds have the potential to provide a higher return as they invest in a diversified basket of selected securities.

Low Costs

Mutual Funds are a relatively less expensive way to invest compared to directly investing in the capital markets because the benefits of scale in brokerage, custodial and other fees translate into lower costs for investors.

24

Liquidity

In open-end schemes, the investor gets the money back promptly at net asset value related prices from the Mutual Fund. In closed-end schemes, the units can be sold on a stock exchange at the prevailing market price or the investor can avail of the facility of direct repurchase at NAV related prices by the Mutual Fund.

Transparency

You get regular information on the value of your investment in addition to disclosure on the specific investments made by your scheme, the proportion invested in each class of assets and the fund manager's investment strategy and outlook.

Flexibility

Through features such as regular investment plans, regular withdrawal plans and dividend reinvestment plans, you can systematically invest or withdraw funds according to your needs and convenience.

Affordability

Investors individually may lack sufficient funds to invest in high-grade stocks. A mutual fund because of its large corpus allows even a small investor to take the benefit of its investment strategy.

Choice of Schemes

Mutual Funds offer a family of schemes to suit your varying needs over a lifetime.

Well Regulated

All Mutual Funds are registered with SEBI and they function within theprovisions of strict regulations designed to protect the interests of investors. The operations of Mutual Funds are regularly monitored by SEBI.

25

Structure of the Indian mutual fund industry

The Indian mutual fund industry is dominated by the Unit Trust of India which has a total corpus of Rs700bn collected from more than 20 million investors. The UTI has many funds/schemes in all categories i.e equity, balanced, income etc with some being open-ended and some being closed-ended. The Unit Scheme 1964 commonly referred to as US 64, which is a balanced fund, is the biggest scheme with a corpus of about Rs200bn. UTI was floated by financial institutions and is governed by a special act of Parliament. Most of its investors believe that the UTI is government owned and controlled, which, while legally incorrect, is true for all practical purposes.

The second largest category of mutual funds are the ones floated by nationalized banks. Canbank Asset Management floated by Canara Bank and SBI Funds Management floated by the State Bank of India are the largest of these. GIC AMC floated by General Insurance Corporation and Jeevan Bima Sahayog AMC floated by the LIC are some of the other prominent ones. The aggregate corpus of funds managed by this category of AMCs is about Rs150bn.

The third largest category of mutual funds are the ones floated by the private sector and by foreign asset management companies. The largest of these are Prudential ICICI AMC and Birla Sun Life AMC. The aggregate corpus of assets managed by this category of AMCs is in excess of Rs250bn

26

Some of the AMCs operating currently are:

Name of the AMC Nature of ownership

Alliance Capital Asset Management (I) Private Limited

Private foreign

Birla Sun Life Asset Management Company Limited Private Indian

Bank of Baroda Asset Management Company Limited

Banks

Bank of India Asset Management Company Limited Banks

Canbank Investment Management Services Limited Banks

Cholamandalam Cazenove Asset Management Company Limited

Private foreign

Dundee Asset Management Company Limited Private foreign

DSP Merrill Lynch Asset Management Company Limited

Private foreign

Escorts Asset Management Limited Private Indian

First India Asset Management Limited Private Indian

GIC Asset Management Company Limited Institutions

IDBI Investment Management Company Limited Institutions

Indfund Management Limited Banks

27

ING Investment Asset Management Company Private Limited

Private foreign

J M Capital Management Limited Private Indian

Jardine Fleming (I) Asset Management Limited Private foreign

Kotak Mahindra Asset Management Company Limited

Private Indian

Kothari Pioneer Asset Management Company Limited

Private Indian

Jeevan Bima Sahayog Asset Management Company Limited

Institutions

Morgan Stanley Asset Management Company Private Limited

Private foreign

Punjab National Bank Asset Management Company Limited

Banks

Reliance Capital Asset Management Company Limited

Private Indian

State Bank of India Funds Management Limited Banks

Shriram Asset Management Company Limited Private Indian

Sun F and C Asset Management (I) Private Limited Private foreign

Sundaram Newton Asset Management Company Limited

Private foreign

Tata Asset Management Company Limited Private Indian

Credit Capital Asset Management Company Limited Private Indian

28

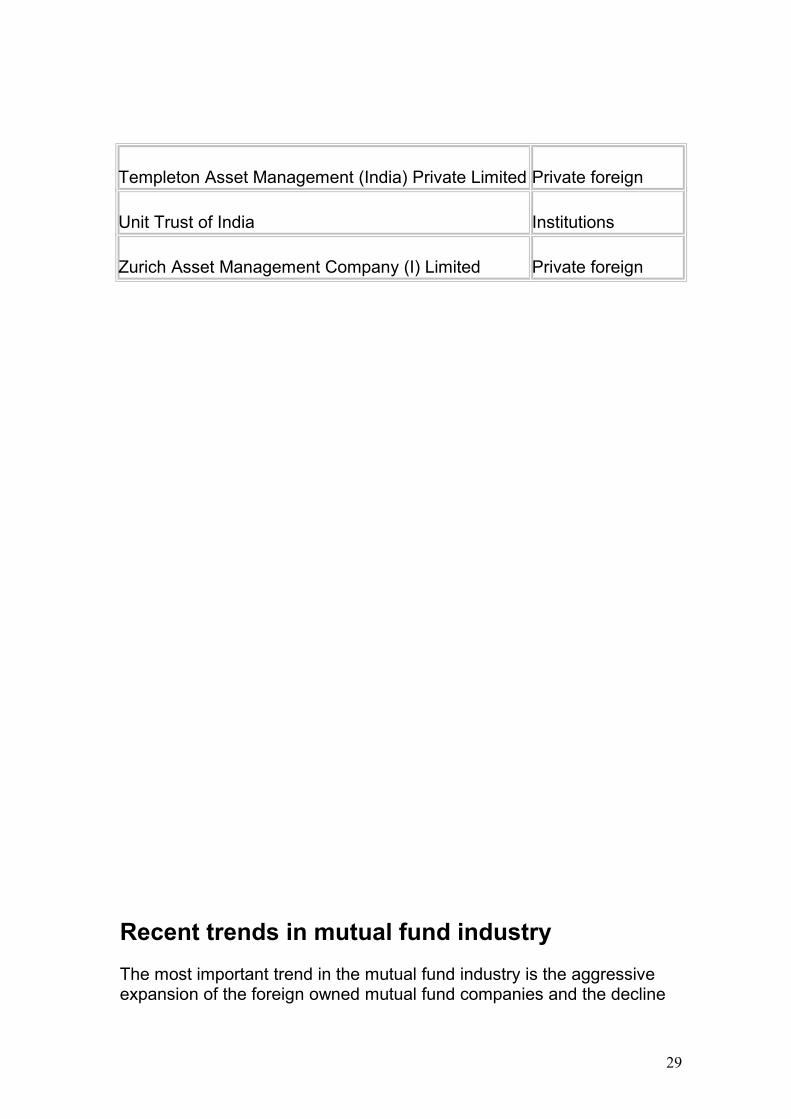

Templeton Asset Management (India) Private Limited Private foreign

Unit Trust of India Institutions

Zurich Asset Management Company (I) Limited Private foreign

Recent trends in mutual fund industry

The most important trend in the mutual fund industry is the aggressive expansion of the foreign owned mutual fund companies and the decline

29

of the companies floated by nationalized banks and smaller private sector players.

Many nationalized banks got into the mutual fund business in the early nineties and got off to a good start due to the stock market boom prevailing then. These banks did not really understand the mutual fund business and they just viewed it as another kind of banking activity. Few hired specialized staff and generally chose to transfer staff from the parent organizations. The performance of most of the schemes floated by these funds was not good. Some schemes had offered guaranteed returns and their parent organizations had to bail out these AMCs by paying large amounts of money as the difference between the guaranteed and actual returns. The service levels were also very bad. Most of these AMCs have not been able to retain staff, float new schemes etc. and it is doubtful whether, barring a few exceptions, they have serious plans of continuing the activity in a major way.

The experience of some of the AMCs floated by private sector Indian companies was also very similar. They quickly realized that the AMC business is a business, which makes money in the long term and requires deep-pocketed support in the intermediate years. Some have sold out to foreign owned companies, some have merged with others and there is general restructuring going on.

The foreign owned companies have deep pockets and have come in here with the expectation of a long haul. They can be credited with introducing many new practices such as new product innovation, sharp improvement in service standards and disclosure, usage of technology, broker education and support etc. In fact, they have forced the industry to upgrade itself and service levels of organizations like UTI have improved dramatically in the last few years in response to the competition provided by these.

Regulatory Aspects

30

Schemes of a Mutual Fund

• The asset management company shall launch no scheme unless the trustees approve such scheme and a copy of the offer document has been filed with the Board.

• Every mutual fund shall along with the offer document of each scheme pay filing fees.

• The offer document shall contain disclosures which are adequate in order to enable the investors to make informed investment decision including the disclosure on maximum investments proposed to be made by the scheme in the listed securities of the group companies of the sponsor A close-ended scheme shall be fully redeemed at the end of the maturity period. "Unless a majority of the unit holders otherwise decide for its rollover by passing a resolution".

• The mutual fund and asset management company shall be liable to refund the application money to the applicants,-

(i) If the mutual fund fails to receive the minimum subscription amount referred to in clause (a) of sub-regulation (1);

(ii) If the moneys received from the applicants for units are in excess of subscription as referred to in clause (b) of sub-regulation (1).

• The asset management company shall issue to the applicant whose application has been accepted, unit certificates or a statement of accounts specifying the number of units allotted to the applicant as soon as possible but not later than six weeks from the date of closure of the initial subscription list and or from the date of receipt of the request from the unit holders in any open ended scheme.

Rules Regarding Advertisement:

31

• The offer document and advertisement materials shall not be misleading or contain any statement or opinion, which are incorrect or false.

Investment Objectives And Valuation Policies:

• The price at which the units may be subscribed or sold and the price at which such units may at any time be repurchased by the mutual fund shall be made available to the investors.

General Obligations:

• Every asset management company for each scheme shall keep and maintain proper books of accounts, records and documents, for each scheme so as to explain its transactions and to disclose at any point of time the financial position of each scheme and in particular give a true and fair view of the state of affairs of the fund and intimate to the Board the place where such books of accounts, records and documents are maintained.

• The financial year for all the schemes shall end as of March 31 of each year. Every mutual fund or the asset management company shall prepare in respect of each financial year an annual report and annual statement of accounts of the schemes and the fund as specified in Eleventh Schedule.

• Every mutual fund shall have the annual statement of accounts audited by an auditor who is not in any way associated with the auditor of the asset management company.

Procedure for Action In Case Of Default:

• On and from the date of the suspension of the certificate or the approval, as the case may be, the mutual fund, trustees or asset management company, shall cease to carry on any activity as a mutual fund, trustee or asset management company, during the period of suspension, and shall be subject to the directions of the Board with regard to any records, documents, or securities that may be in its custody or control, relating to its activities as mutual fund, trustees or asset management company.

Restrictions On Investments:

32

• A mutual fund scheme shall not invest more than 15% of its NAV in debt instruments issued by a single issuer, which are rated not below investment grade by a credit rating agency authorized to carry out such activity under the Act. Such investment limit may be extended to 20% of the NAV of the scheme with the prior approval of the Board of Trustees and the Board of asset management company.

• A mutual fund scheme shall not invest more than 10% of its NAV in unrated debt instruments issued by a single issuer and the total investment in such instruments shall not exceed 25% of the NAV of the scheme. All such investments shall be made with the prior approval of the Board of Trustees and the Board of asset management company.

• No mutual fund under all its schemes should own more than ten per cent of any company's paid up capital carrying voting rights.

• Such transfers are done at the prevailing market price for quoted instruments on spot basis.The securities so transferred shall be in conformity with the investment objective of the scheme to which such transfer has been made.

• A scheme may invest in another scheme under the same asset management company or any other mutual fund without charging any fees, provided that aggregate interscheme investment made by all schemes under the same management or in schemes under the management of any other asset management company shall not exceed 5% of the net asset value of the mutual fund.

• The initial issue expenses in respect of any scheme may not exceed six per cent of the funds raised under that scheme.

• Every mutual fund shall buy and sell securities on the basis of deliveries and shall in all cases of purchases, take delivery of relative securities and in all cases of sale, deliver the securities and shall in no case put itself in a position whereby ithas to make short sale or carry forward transaction or engage in badla finance.

• Every mutual fund shall, get the securities purchased or transferred in the name of the mutual fund on account of the concerned scheme, wherever investments are intended to be of long-term nature.

• Pending deployment of funds of a scheme in securities in terms of investment objectives of the scheme a mutual fund can invest the funds of the scheme in short term deposits of scheduled commercial banks.

• No mutual fund scheme shall make any investment in;

33

i. Any unlisted security of an associate or group company of the sponsor; or

ii. Any security issued by way of private placement by an associate or group company of the sponsor; or

The listed securities of group companies of the sponsor which is in excess of 30% of the net assets [of all the schemes of a mutual fund]

• No mutual fund scheme shall invest more than 10 per cent of its NAV in the equity shares or equity related instruments of any company. Provided that, the limit of 10 per cent shall not be applicable for investments in index fund or sector or industry specific scheme.

• A mutual fund scheme shall not invest more than 5% of its NAV in the equity shares or equity related investments in case of open-ended scheme and 10% of its NAV in case of close-ended scheme.

Types of Mutual Funds

34

Mutual fund schemes may be classified on the basis of its structure and its investment objective.

By Structure:

Open-ended Funds

An open-end fund is one that is available for subscription all through the year. These do not have a fixed maturity. Investors can conveniently buy and sell units at Net Asset Value ("NAV") related prices. The key feature of open-end schemes is liquidity.

Closed-ended Funds

A closed-end fund has a stipulated maturity period which generally ranging from 3 to 15 years. The fund is open for subscription only during a specified period. Investors can invest in the scheme at the time of the initial public issue and thereafter they can buy or sell the units of the scheme on the stock exchanges where they are listed. In order to provide an exit route to the investors, some close-ended funds give an option of selling back the units to the Mutual Fund through periodic repurchase at NAV related prices. SEBI Regulations stipulate that at least one of the two exit routes is provided to the investor.

Interval Funds

Interval funds combine the features of open-ended and close-ended schemes. They are open for sale or redemption during pre-determined intervals at NAV related prices.

By Investment Objective:

Growth Funds

The aim of growth funds is to provide capital appreciation over the medium to long- term. Such schemes normally invest a majority of their corpus in equities. It has been proven that returns from stocks, have outperformed most other kind of investments held over the long term. Growth schemes are ideal for investors having a long-term outlook seeking growth over a period of time.

Income Funds

35

The aim of income funds is to provide regular and steady income to investors. Such schemes generally invest in fixed income securities such as bonds, corporate debentures and Government securities. Income Funds are ideal for capital stability and regular income.

Balanced Funds

The aim of balanced funds is to provide both growth and regular income. Such schemes periodically distribute a part of their earning and invest both in equities and fixed income securities in the proportion indicated in their offer documents. In a rising stock market, the NAV of these schemes may not normally keep pace, or fall equally when the market falls. These are ideal for investors looking for a combination of income and moderate growth.

Money Market Funds

The aim of money market funds is to provide easy liquidity, preservation of capital and moderate income. These schemes generally invest in safer short-term instruments such as treasury bills, certificates of deposit, commercial paper and inter-bank call money. Returns on these schemes may fluctuate depending upon the interest rates prevailing in the market. These are ideal for Corporate and individual investors as a means to park their surplus funds for short periods.

Load Funds

A Load Fund is one that charges a commission for entry or exit. That is, each time you buy or sell units in the fund, a commission will be payable. Typically entry and exit loads range from 1% to 2%. It could be worth paying the load, if the fund has a good performance history.

No-Load Funds

A No-Load Fund is one that does not charge a commission for entry or exit. That is, no commission is payable on purchase or sale of units in the fund. The advantage of a no load fund is that the entire corpus is put to work.

Other Schemes:

36

Tax Saving Schemes

These schemes offer tax rebates to the investors under specific provisions of the Indian Income Tax laws as the Government offers tax incentives for investment in specified avenues. Investments made in Equity Linked Savings Schemes (ELSS) and Pension Schemes are allowed as deduction u/s 88 of the Income Tax Act, 1961. The Act also provides opportunities to investors to save capital gains u/s 54EA and 54EB by investing in Mutual Funds, provided the capital asset has been sold prior to April 1, 2000 and the amount is invested before September 30, 2000.

Special Schemes

• Industry Specific Schemes

Industry Specific Schemes invest only in the industries specified in the offer document. The investment of these funds is limited to specific industries like InfoTech, FMCG, Pharmaceuticals etc.

• Index Schemes

Index Funds attempt to replicate the performance of a particular index such as the BSE Sensex or the NSE 50

• Sectoral Schemes

Sectoral Funds are those, which invest exclusively in a specified industry or a group of industries or various segments such as 'A' Group shares or initial public offerings.

37

Market Trends

A lone UTI with just one scheme in 1964, now competes with as many as 400 odd products and 34 players in the market. In spite of the stiff competition and losing market share, UTI still remains a formidable force to reckon with.

Last six years have been the most turbulent as well as exiting ones for the industry. New players have come in, while others have decided to close shop by either selling off or merging with others. Product innovation is now passé with the game shifting to performance delivery in fund management as well as service. Those directly associated with the fund management industry like distributors, registrars and transfer agents, and even the regulators have become more mature and responsible.

The industry is also having a profound impact on financial markets. While UTI has always been a dominant player on the bourses as well as the debt markets, the new generation of private funds which have gained substantial mass are now seen flexing their muscles. Fund managers, by their selection criteria for stocks have forced corporate governance on the industry. By rewarding honest and transparent management with higher valuations, a system of risk-reward has been created where the corporate sector is more transparent then before.

Funds have shifted their focus to the recession free sectors like pharmaceuticals, FMCG and technology sector. Funds performances are improving. Funds collection, which averaged at less than Rs100bn per annum over five-year period spanning 1993-98 doubled to Rs210bn in 1998-99. In the current year mobilization till now have exceeded Rs300bn. Total collection for the current financial year ending March 2000 is expected to reach Rs450bn.

What is particularly noteworthy is that bulk of the mobilization has been by the private sector mutual funds rather than public sector mutual funds. Indeed private MFs saw a net inflow of Rs. 7819.34 crore during the first nine months of the year as against a net inflow of Rs.604.40 crore in the case of public sector funds.

Mutual funds are now also competing with commercial banks in the race for retail investor’s savings and corporate float money. The power shift

38

towards mutual funds has become obvious. The coming few years will show that the traditional saving avenues are losing out in the current scenario. Many investors are realizing that investments in savings accounts are as good as locking up their deposits in a closet. The fund mobilization trend by mutual funds in the current year indicates that money is going to mutual funds in a big way. The collection in the first half of the financial year 1999-2000 matches the whole of 1998-99.

India is at the first stage of a revolution that has already peaked in the U.S. The U.S. boasts of an Asset base that is much higher than its bank deposits. In India, mutual fund assets are not even 10% of the bank deposits, but this trend is beginning to change. Recent figures indicate that in the first quarter of the current fiscal year mutual fund assets went up by 115% whereas bank deposits rose by only 17%. (Source: Thinktank, The Financial Express September, 99) This is forcing a large number of banks to adopt the concept of narrow banking wherein the deposits are kept in Gilts and some other assets which improves liquidity and reduces risk. The basic fact lies that banks cannot be ignored and they will not close down completely. Their role as intermediaries cannot be ignored. It is just that Mutual Funds are going to change the way banks do business in the future.

Banks v/s Mutual Funds

BANKS MUTUAL FUNDS

Returns Low Better

Administrative exp.High Low

Risk Low Moderate

Investment options Less More

Network High penetration Low but improving

Liquidity At a cost Better

Quality of assets Not transparent Transparent

39

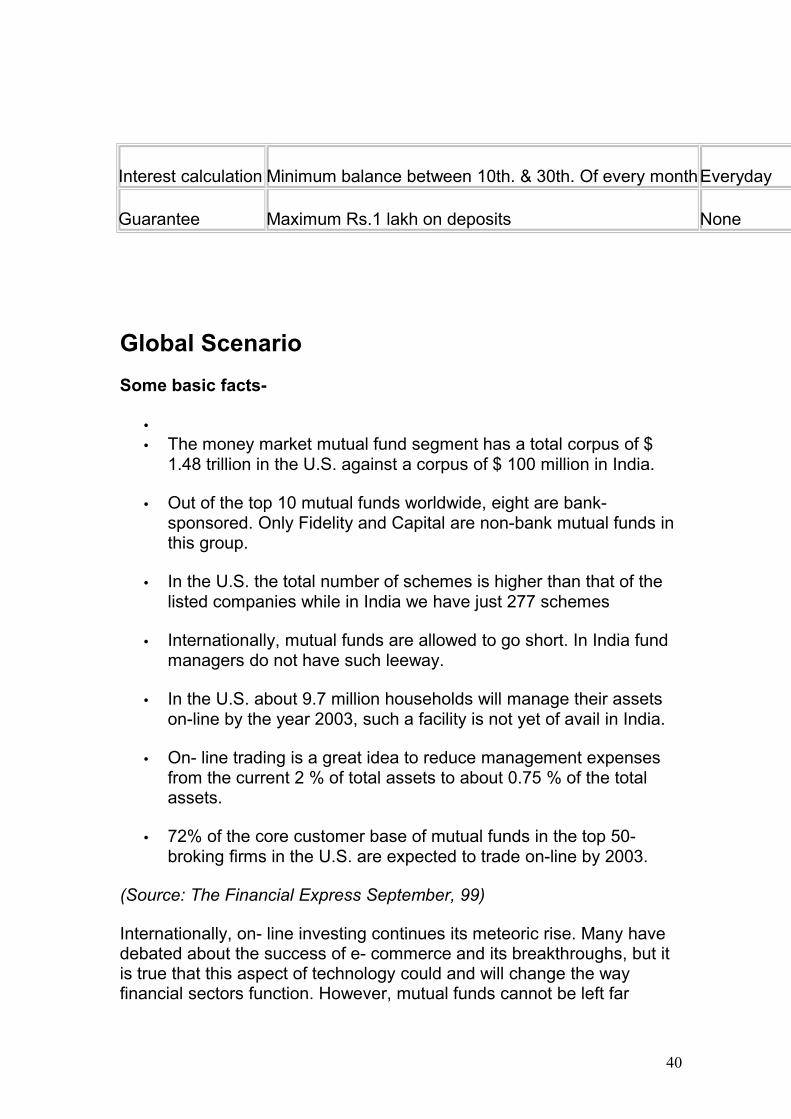

Interest calculation Minimum balance between 10th. & 30th. Of every monthEveryday

Guarantee Maximum Rs.1 lakh on deposits None

Global Scenario

Some basic facts-

•• The money market mutual fund segment has a total corpus of $

1.48 trillion in the U.S. against a corpus of $ 100 million in India.

• Out of the top 10 mutual funds worldwide, eight are bank- sponsored. Only Fidelity and Capital are non-bank mutual funds in this group.

• In the U.S. the total number of schemes is higher than that of the listed companies while in India we have just 277 schemes

• Internationally, mutual funds are allowed to go short. In India fund managers do not have such leeway.

• In the U.S. about 9.7 million households will manage their assets on-line by the year 2003, such a facility is not yet of avail in India.

• On- line trading is a great idea to reduce management expenses from the current 2 % of total assets to about 0.75 % of the total assets.

• 72% of the core customer base of mutual funds in the top 50-broking firms in the U.S. are expected to trade on-line by 2003.

(Source: The Financial Express September, 99)

Internationally, on- line investing continues its meteoric rise. Many have debated about the success of e- commerce and its breakthroughs, but it is true that this aspect of technology could and will change the way financial sectors function. However, mutual funds cannot be left far

40

behind. They have realized the potential of the Internet and are equipping themselves to perform better.

In fact in advanced countries like the U.S.A, mutual funds buy- sell transactions have already begun on the Net, while in India the Net is used as a source of Information.

Such changes could facilitate easy access, lower intermediation costs and better services for all. A research agency that specializes in internet technology estimates that over the next four years Mutual Fund Assets traded on- line will grow ten folds from $ 128 billion to $ 1,227 billion ; whereas equity assets traded on-line will increase during the period from $ 246 billion to $ 1,561 billion. This will increase the share of mutual funds from 34% to 40% during the period.

(Source: The Financial Express September ,99)

Such increases in volumes are expected to bring about large changes in the way Mutual Funds conduct their business.

Here are some of the basic changes that have taken place since the advent of the Net.

• Lower Costs: Distribution of funds will fall in the online trading regime by 2003 . Mutual funds could bring down their administrative costs to 0.75% if trading is done on- line. As per SEBI regulations , bond funds can charge a maximum of 2.25% and equity funds can charge 2.5% as administrative fees. Therefore if the administrative costs are low , the benefits are passed down and hence Mutual Funds are able to attract mire investors and increase their asset base.

• Better advice: Mutual funds could provide better advice to their investors through the Net rather than through the traditional investment routes where there is an additional channel to deal with the Brokers. Direct dealing with the fund could help the investor with their financial planning.

• In India , brokers could get more Net savvy than investors and could help the investors with the knowledge through get from the Net.

• New investors would prefer online : Mutual funds can target investors who are young individuals and who are Net savvy, since servicing them would be easier on the Net.

41

• India has around 1.6 million net users who are prime target for these funds and this could just be the beginning. The Internet users are going to increase dramatically and mutual funds are going to be the best beneficiary. With smaller administrative costs more funds would be mobilized .A fund manager must be ready to tackle the volatility and will have to maintain sufficient amount of investments which are high liquidity and low yielding investments to honor redemption.

• Net based advertisements: There will be more sites involved in ads and promotion of mutual funds. In the U.S. sites like AOL offer detailed research and financial details about the functioning of different funds and their performance statistics. a is witnessing a genesis in this area . There are many sites such as indiainfoline.com and indiafn.com that are doing something similar and providing advice to investors regarding their investments.

In the U.S. most mutual funds concentrate only on financial funds like equity and debt. Some like real estate funds and commodity funds also take an exposure to physical assets. The latter type of funds are preferred by corporate’s who want to hedge their exposure to the commodities they deal with.

For instance, a cable manufacturer who needs 100 tons of Copper in the month of January could buy an equivalent amount of copper by investing in a copper fund. For Example, Permanent Portfolio Fund, a conservative U.S. based fund invests a fixed percentage of it’s corpus in Gold, Silver, Swiss francs, specific stocks on various bourses around the world, short –term and long-term U.S. treasuries etc.

In U.S.A. apart from bullion funds there are copper funds, precious metal funds and real estate funds (investing in real estate and other related assets as well.).In India, the Canada based Dundee mutual fund is planning to launch a gold and a real estate fund before the year-end.

In developed countries like the U.S.A there are funds to satisfy everybody’s requirement, but in India only the tip of the iceberg has been explored. In the near future India too will concentrate on financial as well as physical funds.

42

INSURANCE

Today concept of Banc assurance is getting very common, selling Insurance of another company to the Bank customers.

Lets see the Banc assurance in detail.

Bancassurance

Introduction

With the opening up of the insurance sector and with so many players entering the Indian insurance industry, it is required by the insurance companies to come up with innovative products, create more consumer awareness about their products and offer them at a competitive price. New entrants in the insurance sector had no difficulty in matching their products with the customers' needs and offering them at a price acceptable to the customer.

But, insurance not being an off the shelf product and one which requiring personal counseling and persuasion, distribution posed a major challenge for the insurance companies. Further insurable population of over 1 billion spread all over the country has made the traditional channels of the insurance companies costlier. Also due to heavy competition, insurers do not enjoy the flexibility of incurring heavy distribution expenses and passing them to the customer in the form of high prices.

With these developments and increased pressures in combating competition, companies are forced to come up with innovative techniques to market their products and services. At this

43

juncture, banking sector with it's far and wide reach, was thought of as a potential distribution channel, useful for the insurance companies. This union of the two sectors is what is known as Bancassurance.

What is Bancassurance?

Bancassurance is the distribution of insurance products through the bank's distribution channel. It is a phenomenon wherein insurance products are offered through the distribution channels of the banking services along with a complete range of banking and investment products and services. To put it simply, Bancassurance, tries to exploit synergies between both the insurance companies and banks.

Bancassurance if taken in right spirit and implemented properly can be win-win situation for the all the participants' viz., banks, insurers and the customers.

Advantages to banks

• Productivity of the employees increases.• By providing customers with both the services under one

roof, they can improve overall customer satisfaction resulting in higher customer retention levels.

• Increase in return on assets by building fee income through the sale of insurance products.

• Can leverage on face-to-face contacts and awareness about the financial conditions of customers to sell insurance products.

• Banks can cross sell insurance products Eg: Term insurance products with loans.

44

Advantages to insurers

• Insurers can exploit the banks' wide network of branches for distribution of products. The penetration of banks' branches into the rural areas can be utilized to sell products in those areas.

• Customer database like customers' financial standing, spending habits, investment and purchase capability can be used to customize products and sell accordingly.

• Since banks have already established relationship with customers, conversion ratio of leads to sales is likely to be high. Further service aspect can also be tackled easily.

Advantages to consumers

• Comprehensive financial advisory services under one roof. i.e., insurance services along with other financial services such as banking, mutual funds, personal loans etc.

• Enhanced convenience on the part of the insured

• Easy access for claims, as banks are a regular go.

• Innovative and better product ranges

Bancassurance in India

Bancassurance in India is a very new concept, but is fast gaining ground. In India, the banking and insurance sectors are

45

regulated by two different entities (banking by RBI and insurance by IRDA) and bancassurance being the combinations of two sectors comes under the purview of both the regulators. Each of the regulators has given out detailed guidelines for banks getting into insurance sector. Highlights of the guidelines are reproduced below:

RBI guideline for banks entering into insurance sector provides three options for banks. They are:

• Joint ventures will be allowed for financially strong banks wishing to undertake insurance business with risk participation;

• For banks which are not eligible for this joint-venture option, an investment option of up to 10% of the net worth of the bank or Rs.50 crores, whichever is lower, is available;

• Finally, any commercial bank will be allowed to undertake insurance business as agent of insurance companies. This will be on a fee basis with no-risk participation.

The Insurance Regulatory and Development Authority (IRDA) guidelines for the bancassurance are:

• Each bank that sells insurance must have a chief insurance executive to handle all the insurance activities.

• All the people involved in selling should under-go mandatory training at an institute accredited by IRDA and pass the examination conducted by the authority.

• Commercial banks, including cooperative banks and regional rural banks, may become corporate agents for one insurance company.

46

• Banks cannot become insurance brokers.

Some of the Bancassurance tie-ups in India are:

Insurance Company Bank

Birla Sun Life Insurance Co. Ltd.

Bank of Rajasthan, Andhra Bank, Bank of Muscat, Development Credit Bank, Deutsche Bank and Catholic Syrian Bank

Dabur CGU Life Insurance Company Pvt. Ltd

Canara Bank, Lakshmi Vilas Bank, American Express Bank and ABN AMRO Bank

HDFC Standard Life Insurance Co. Ltd.

Union Bank of India

ICICI Prudential Life Insurance Co Ltd.

Lord Krishna Bank, ICICI Bank, Bank of India, Citibank, Allahabad Bank, Federal Bank, South Indian Bank, and Punjab and Maharashtra Co-operative Bank.

Life Insurance Corporation of India

Corporation Bank, Indian Overseas Bank, Centurion Bank, Satara District Central Co-operative Bank, Janata Urban Co-operative Bank, Yeotmal Mahila Sahkari Bank, Vijaya Bank, Oriental Bank of Commerce.

Met Life India Insurance Co. Ltd.

Karnataka Bank, Dhanalakshmi Bank and J&K Bank

SBI Life Insurance Company Ltd.

State Bank of India

Bajaj Allianz General Insurance Co. Ltd.

Karur Vysya Bank and Lord Krishna Bank

47

National Insurance Co. Ltd.

City Union Bank

Royal Sundaram General Insurance Company

Standard Chartered Bank, ABN AMRO Bank, Citibank, Amex and Repco Bank.

United India Insurance Co. Ltd.

South Indian Bank

Issues to be tackled

Given the roles and diverse skills brought by the banks and insurers to a Bancassurance tie up, it is expected that road to a successful alliance would not be an easy task. Some of the issues that are to be addressed are:

1. The tie-ups need to develop innovative products and services rather than depend on the traditional methods. The kinds of products the banks would be allowed to sell are another major issue. For instance, a complex unit-linked life insurance product is better sold through brokers or agents, while a standard term product or simple products like auto insurance, home loan and accident insurance cover can be handled by bank branches

2. There needs to be clarity on the operational activities of the bancassurance i.e., who will do the branding, will the insurance company prefer to place a person at the bank branch, or will the bank branch train and put up one of its own people, remuneration of these people.

3. Even though the banks are in personal contact with their clients, a high degree of pro-active marketing and skill is required to sell the insurance products. This can be addressed through proper training.

4. There are hazards of direct competition to conventional banking products. Bank personnel may become resistant

48

to sell insurance products since they might think they would become redundant if savings were diverted from banks to their insurance subsidiaries.

Factors that appear to be critical for the success of bancassurance are

1. Strategies consistent with the bank's vision, knowledge of target customers' needs, defined sales process for introducing insurance services, simple yet complete product offerings, strong service delivery mechanism, quality administration, synchronized planning across all business lines and subsidiaries, complete integration of insurance with other bank products and services, extensive and high-quality training, sales management tracking system for reporting on agents' time and results of bank referrals and relevant and flexible database systems.

2. Another point is the handling of customers. With customer awareness levels increasing, they are demanding greater convenience in financial services.

3. The emergence of remote distribution channels, such as PC-banking and Internet-banking, would hamper the distribution of insurance products through banks.

4. The emergence of newer distribution channels seeking a market share in the network.

49

Conclusion

With huge untapped market, insurance sector is likely to witness a lot of activity - be it product innovation or distribution channel mix. Bancassurance, the emerging distribution channel for the insurers, will have a large impact on Indian financial services industry. Traditional methods of distributing financial services would be challenged and innovative, customized products would emerge.

Banks will bring in customer database, leverage their name recognition and reputation at both local and regional levels, make use of the personal contact with their clients, which a new entrant cannot, as they are new to the industry.

In customer point of view, a plethora of products would be available to him. More customized products would come into existence and that too all within a hands reach.

Finally Success of the bancassurance would mostly depend on how well insurers and banks understand each other's businesses and seize the opportunities presented, weeding out differences that are likely to crop up.

Insurance industry, earlier comprised of only two state insurers.

50

Life Insurers ie Life Insurance Corporation of India (LIC) and General Insurers ie General Insurance Corporation of India (GIC) GIC had four subsidary companies.

With effect from Dec'2000, these subsidaries have been de-linked from parent company and made as an independent insurance companies. Oriental Insurance Company Limited, New India Assurance Company Limited, National Insurance Company Limited and United India Insurance Company Limited.

The first batch of licenses were issued by the Insurance Regulatory and Development Authority (IRDA) in 2001. At present following are the players in the Indian Market:

LIFE INSURERS:

1. ALLIANZ BAJAJ LIFE INSURANCE CO. LTD.

2. AMP SANMAR ASSURANCE CO. LTD.

3. BIRLA SUN LIFE INSURANCE CO. LTD.

4. DABUR CGU LIFE INSURANCE COMPANY PVT.LTD.

5. HDFC STANDARD LIFE INSURANCE CO. LTD.

6. ICICI PRUDENTIAL LIFE INSURANCE CO.LTD.

7. ING VYSYA LIFE INSURANCE CO. PVT. LTD.

8. LIFE INSURANCE CORPORATION OF INDIA

51

9. MAX NEW YORK LIFE INSURANCE CO. LTD.

10. METLIFE INDIA INSURANCE CO. PVT. LTD.

11. OM KOTAK MAHINDRA LIFE INSURANCE CO. LTD.

12. SBI LIFE INSURANCE CO.LTD.

13. TATA AIG LIFE INSURANCE CO. LTD.

NON-LIFE INSURERS:

1. BAJAJ ALLIANZ GENERAL INSURANCE CO.

2. ICICI LOMBARD GENERAL INSURANCE CO.

3. IFFCO TOKYO GENERAL INSURANCE CO.

4. NATIONAL INSURANCE CO.

5. NEW INDIA ASSURANCE CO.

6. ORIENTAL INSURANCE CO.

7. RELIANCE GENERAL INSURANCE CO.

8. ROYAL SUNDARAM ALLIANCE INSURANCE CO.

52

9. TATA AIG LIFE INSURANCE CO.

10. UNITED INDIA INSURANCE CO.

REINSURERS:

GENERAL INSURANCE CORPORATION OF INDIA.

Relevance of Bancassurance in the Indian financial sector

• Integration of the financial service industry in terms of banking, securities business and insurance is a growing worldwide phenomenon. The Universal Banking is evolving on these lines in India.

• Banks are the key pillars of India’s financial system. Public have immense faith in banks.– Share of bank deposits in the total financial assets of

households has been steadily rising (presently at about 40%).

• Indian Banks have immense reach to households.

– Total of 65700 branches of commercial banks, each branch serving an average of 15,000 people.

• Banks enjoy considerable goodwill and access in the rural regions. – There are 32600 branches in rural India (about 50% of total),

and 14400 semi-urban branches, where insurance growth has been most buoyant.

53

– 196 exclusive Regional Rural Banks in deep hinterland

• Banks have enormous retail customer base.

– Total of 406 million accounts with aggregate deposits of Rs.700,000 crore as at Sept 2000.

– Share of `individuals’ as a category in bank accounts is steadily increasing.

– Rural and semi-urban bank accounts constitute close to 60% in terms of number of accounts, indicating the number of potential lives that could be covered by insurance with the frontal involvement of banks.

• Banks world over have realized that offering value-added services such as insurance, helps to meet client expectations.

– Competition in the Personal Financial Services area is getting `hot’ in India.

– Banks seek to retain customer loyalty by offering them a vastly expanded and more sophisticated range of products.

• Banks world over have realized that offering value-added services such as insurance, helps to meet client expectations.

– Competition in the Personal Financial Services area is getting `hot’ in India.

– Banks seek to retain customer loyalty by offering them a vastly expanded and more sophisticated range of products.

• Insurance distribution helps to increase the fee-based earnings of banks to a considerable extent.

– Internationally, insurance activities contribute significantly to banks’ total domestic retail revenues.

• Fee-based selling helps to enhance the levels of staff productivity in banks. – This is vitally important to bring higher motivation levels in

banks in India.

54

• Banks can put their energies into the `small-commission customers’ that insurance agents would tend to avoid.– Banks’ entry in distribution helps to enlarge the insurance

customer base rapidly. This helps to popularize insurance as an important financial protection product.

• Bancassurance helps to lower the distribution costs of insurers.– Acquisition cost of insurance customer through banks is low.

Selling insurance to existing mass market banking customers is far less expensive than selling to a group of unknown customers.

– Experience in Europe has shown that bancassurance firms have a lower expense ratio. This benefit could go to the insured public by way of lower premiums.

• Banks have an important role to play in the pension sector when deregulated. – Low cost of collecting pension contributions is the key

element in the success of developing the pension sector. Money transfer costs in Indian banking is low by international standards.

– Portability of pension accounts is a vital requirement which banks can fulfill in a credible framework.

• Banks can play a major role in developing a viable healthcare programme in India.– Only 2.5 million people have access to healthcare facilities.

There is a growing demand for healthcare products which banks can distribute (and facilitate administration).

55

Bancassurance: Patterns of Distribution alliances

• Banks selling products of their insurance subsidiary exclusively.• Banks selling products of an insurance affiliate on an exclusive

basis.

• Banks offering products of several insurance companies as `super market’.

Distribution alliances in bancassurance:Key Regulatory issues

• Corporate Agency model– Issues and responsibilities.

– How relevant in the case of banks?

• Corporate Broker model– Banks as brokers.

– Regulatory and operational issues.

Implementing Bancassurance: Key Challenges in the Indian context

• Creating an environment of top level involvement of bank management.

• Bringing relevance, motivation and skill development at the operating level at bank branches.

• Resolving possible conflicts of interest between the bank and the insurer.

• Setting up distribution procedures consistent with the manual systems in most banks.

56

• Establishing credible service level agreements between the bank and the insurer.

57

COMPANY PROFILE

58

HDFC BANK

The Housing Finance Corporation Limited

59

RESEARCH DESIGN

60

Objectives of the Project:

- To know the Acceptance of TPP in Banking by Customers- To get the knowledge about the Expectations of the customers

from Banking sector towards TPP- To get knowledge about the Management of Customer

Relationship towards TPP in different Private Sector Banks- To know the Satisfaction Level of the Customers from the TPP - To get the knowledge of the Perception Gap related to TPP

Research Methodology:

Data Collection Sources:

Primary Data: Primary data was collected by means of the survey. Questionnaires were prepared and customers of the three banks were approached to fill up these questionnaires.

Secondary Data: In order to have a proper understanding of Third Party Products in Private Sector Banking an in depth study was done from the various books, magazines, articles written on the subject. A lot of data has also been collected from these and also from the various websites on the topic as also from the web sites of the all the three banks.

Sample Unit:Ahmedabad Area was surveyed i.e. the branches of the Ahmedabad city.

Sample Size:100 Samples from the all three banks are to be surveyed and analysed

Sampling Technique:Convenience Sampling was used to collect the data from the various banks and from the various bank customers.

61

LIMITATIONS:

- The sample size was restrictedxc with in the area of Ahmedabad.- Further it was a convenience sampling.- There were time and cost limitations.- The three banks selected have been considered as

representatives of the banking sector. Also, the opinions have been generalized to the public.

- This project has been done for academic purpose and not done as a professional researcher for the company.

62

ANALYSIS

63

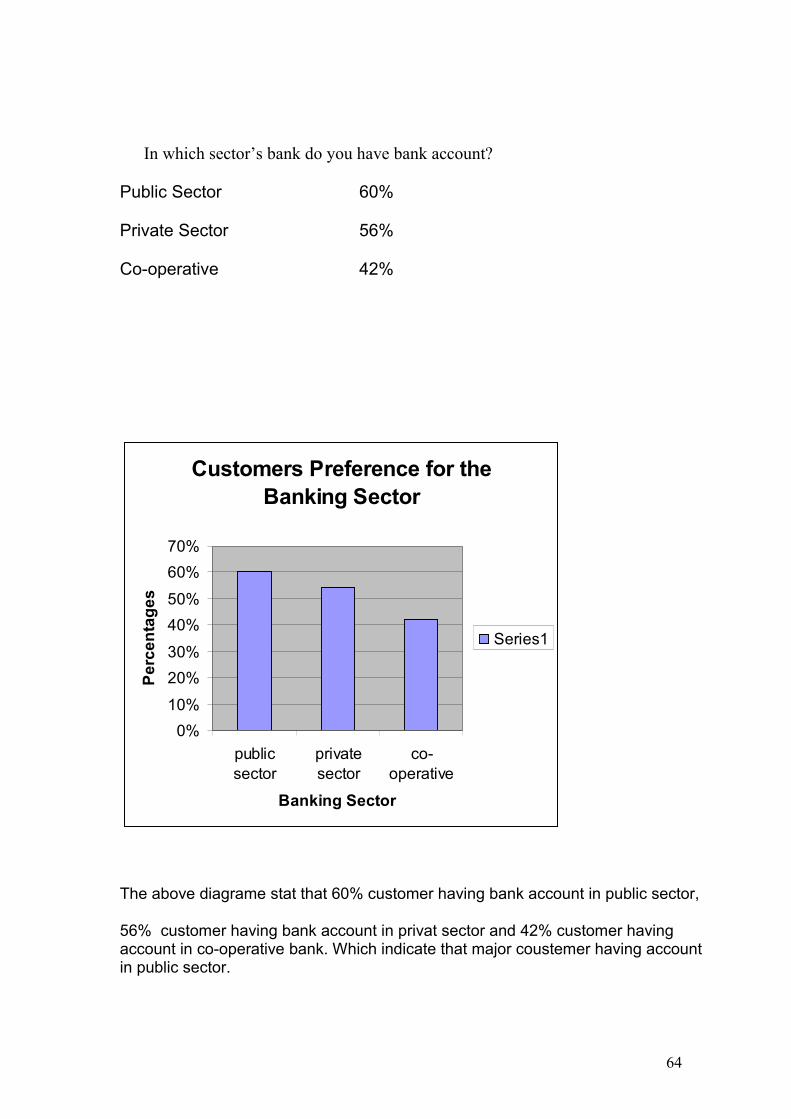

In which sector’s bank do you have bank account?

Public Sector 60%

Private Sector 56%

Co-operative 42%

Customers Preference for the Banking Sector

0%

10%

20%

30%

40%

50%

60%

70%

publicsector

privatesector

co-operative

Banking Sector

Pe

rce

nta

ge

s

Series1

The above diagrame stat that 60% customer having bank account in public sector,

56% customer having bank account in privat sector and 42% customer having account in co-operative bank. Which indicate that major coustemer having account in public sector.

64

Which type of Bank Account do you have?

Current Account 84%

Saving Account 76%

Fixed Deposits 42%

0%

20%

40%

60%

80%

100%

CurrentAccount

SavingAccount

FixedDeposits

Series1

65

Are you aware about the Third Party Products?

Yes 52%

No 48%

46%

47%

48%

49%

50%

51%

52%

yes no

Series1

66

If yes, then have you ever invested for the same?

Yes 85%

No 15%

0%

20%

40%

60%

80%

100%

yes no

Series1

67

If yes, then in which product had you invested?

Insurance 78%

Mutual Funds 64%

0%

20%

40%

60%

80%

insurance Mutual fund

Series1

68

Do you think Banks need to deal with Third Party Products?

Yes 72%

No 28%

0%

20%

40%

60%

80%

yes no

Series1

69

Which Criteria you consider before taking the decision of investment through particular Bank?

Service 44%

Credit worthiness 72%

Relations 62%

0%10%20%30%40%

50%60%70%80%

servise creditworthiness

relations

Series1

70

How will you rate the Satisfaction level from the services provided to you by the Bank through which you made your investment?

Highly Satisfied 34%

Satisfied 42%

Moderate 15%

Dissatisfied 5%

Highly Dissatisfied 4%

0%

10%

20%

30%

40%

50%

highlysatisfied

satisfied moderate dissatisfied highlydissatisfied

Series1

71

Are you satisfied with the products which are provided to you by your Bank?

Yes 82%

No 18%

0%

20%

40%

60%

80%

100%

yes no

Series1

72

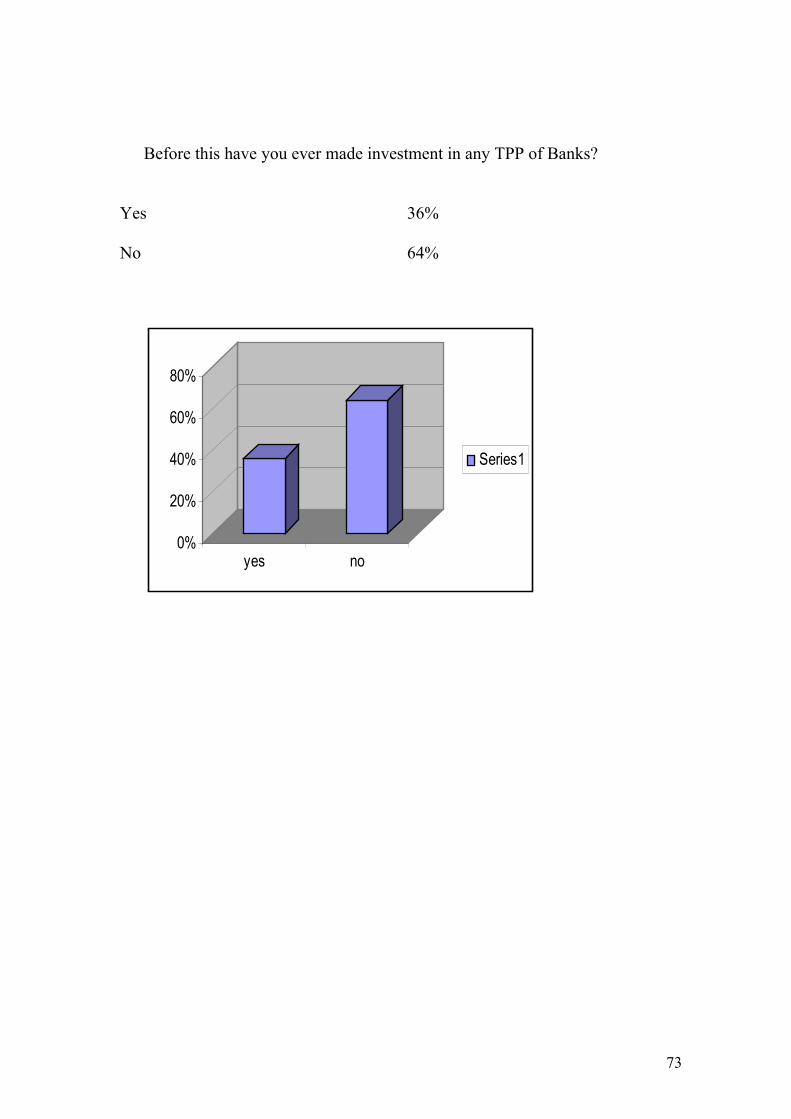

Before this have you ever made investment in any TPP of Banks?

Yes 36%

No 64%

0%

20%

40%

60%

80%

yes no

Series1

73

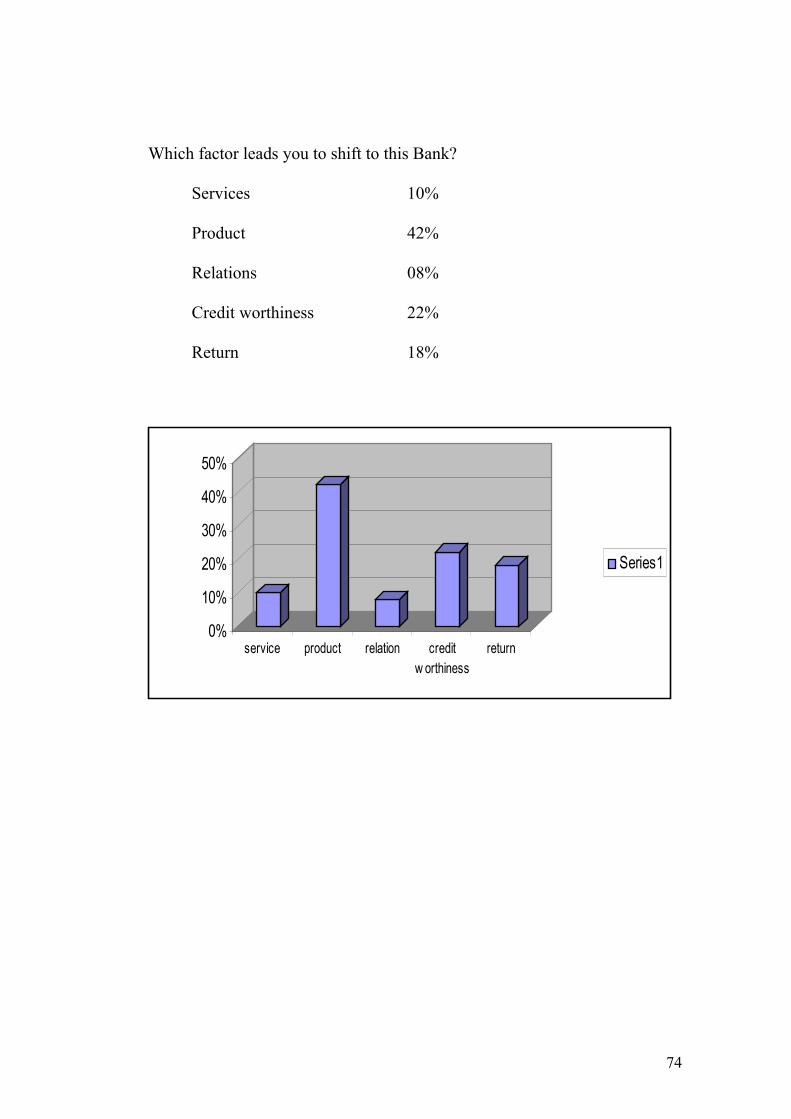

Which factor leads you to shift to this Bank?

Services 10%

Product 42%

Relations 08%

Credit worthiness 22%

Return 18%

0%

10%

20%

30%

40%

50%

service product relation creditw orthiness

return

Series1

74

Do you think you may shift to any other Bank for Investment in TPP in future?

Yes 68%

No 32%

0%

20%

40%

60%

80%

yes no

Series1

75

What factors might lead you to shift to some other bank?

Services 15%

Product 25%

Relations 18%

Credit worthiness 16%

Return 26%

0%

5%

10%

15%

20%

25%

30%

service product relation creditworthiness

return

Series1

76

Do you think you are getting the perceived product satisfaction?

Yes 52%

No 48%

46%

48%

50%

52%

yes no

Series1

77

If No, then in which features it differs from your perceived product features?

Return 54%

Management Pattern 16%

Trustworthiness 30%

0%

10%

20%

30%

40%

50%

60%

return managementpattern

trustworthiness

Series1

78

79