Governmental Accounting in Colonial Massachusetts

12

Governmental Accounting in Colonial Massachusetts Author(s): William Holmes Source: The Accounting Review, Vol. 54, No. 1 (Jan., 1979), pp. 47-57 Published by: American Accounting Association Stable URL: http://www.jstor.org/stable/246233 . Accessed: 18/06/2014 23:08 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. . American Accounting Association is collaborating with JSTOR to digitize, preserve and extend access to The Accounting Review. http://www.jstor.org This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PM All use subject to JSTOR Terms and Conditions

-

Upload

william-holmes -

Category

Documents

-

view

213 -

download

0

Transcript of Governmental Accounting in Colonial Massachusetts

Governmental Accounting in Colonial MassachusettsAuthor(s): William HolmesSource: The Accounting Review, Vol. 54, No. 1 (Jan., 1979), pp. 47-57Published by: American Accounting AssociationStable URL: http://www.jstor.org/stable/246233 .

Accessed: 18/06/2014 23:08

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

American Accounting Association is collaborating with JSTOR to digitize, preserve and extend access to TheAccounting Review.

http://www.jstor.org

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

THE ACCOUNTING REVIEW Vol. LIV, No. 1 January 1979

Governmental Accounting in Colonial

Massachusetts

William Holmes

ABSTRACT: This paper traces advances in the art of governmental accounting in Massachusetts to approximately 1800. The material studied as a basis for the paper was drawn, for the most part, from original source documents in the Massachusetts Archives, supplemented by readings from Boston town records. The advances noted appear to follow an evolutionary process, culminating in a double-entry appropriation system in use in the colony in the years 1754-1775. Boston appears to have been using a double-entry system by the 1780s. The paper also makes note of a double-entry appropriation system for use by municipalities described in The Town Officer [Freeman, 1791]. The systems encountered appear to be in advance of systems used in Europe during this same period.

A CCOUNTING historians, for the most part, have not been overly im- pressed with the state of the art as

practiced in colonial America. The "Ital- ian Method" is almost entirely lacking in early commercial records, and the wide- spread single-entry bookkeeping in use, with few exceptions, is rudimentary and full of inaccuracies.

Baxter, in his interesting and thought- provoking article "Accounting in Co- lonial America" [Baxter, 1956], offered some plausible reasons for this state of affairs that provided a measure of solace to American historians, but colonial accountants were still constrained to seat ourselves "below the salt" at any serious gathering of international accounting historians. However, some recent dis- coveries by this writer in the Massa- chusetts State Archives suggest that in accounting related to government, the American colonial accountant more than held his own. The Treasurer of the Col- ony of Massachusetts was using double- entry budgetary accounting in 1754.

Baxter [1956] pointed out that the colonial merchant did not need double-

entry bookkeeping. He had no particular need to determine "profit" at regular intervals; he was accountable in terms of income to no taxing authority; his "net worth" was in terms of acres of land, livestock, bushels of grain, shares in shipping joint ventures, and a variety of claims due from and to other people. Only to a limited extent was any part capable of being turned into quick cash. His single-entry bookkeeping enabled him to keep track of what was not physi- cally at hand, namely his accounts with his debtors and creditors, and, even if rudimentary, it worked well enough subject to an occasional adjustment "to agree his balance with my balance."

It occurred to me that if there is a con- nection between accountability and the state of the accounting art, the account- ing historian in America has been looking under the wrong stones. The account- ability factor, missing in the commercial

William Holmes is a Manager with Peat, Marwick, Mitchell & Co., Boston.

Manuscript received April, 1978. Accepted May, 1978.

47

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

48 The Accounting Review, January 1979

arena, was present in the governmental fiscal system-and uniquely so in Massa- chusetts from the earliest days.

The Massachusetts Bay Company was incorporated in 1629 as a business enter- prise-a joint stock company account- able to its English stockholders. Its Court of Assistants (Board of Directors) managed the company and reported quarterly to the "Generalitie" of stock- holders in "General Court." The ac- counts were "audited" by duly ap- pointed "auditors" in London before the first planters sailed for New England. The form was similar to that underlying the other English colonizing ventures of the times-The Viriginia Company, the Plymouth Company, etc.-but The Mas- sachusetts Bay Company was unique in one respect. The "Management" and Charter were effectively moved to Mas- sachusetts almost immediately, and over the years 1630-1640, as the old com- mercial venture took on the attributes of a self-sustaining civilian entity, much of the old business relationship between the Generalitie and the Court of Assistants carried over to the structure of the Civil government. In 1645, to help strengthen the fiscal relationship between the "Man- agement" and the evolving towns, which through taxation were providing the bulk of the revenues, the General Court ap- proved the creation of the post of Auditor General and wrote a lengthy job-descrip- tion to fit the post. Each town sent its deputies to the General Court and through these representatives, was en- titled to an on-the-spot accounting each year.

The actual books of account for the province prior to 1753 are missing, but the Massachusetts State Archives have the reports of the treasurers back to the 1650s. I propose to examine the advances made in the provincial accounts during the hundred years prior to the revolution

by looking at the Treasurer's Report for 1675-1679, the accounts rendered in the 1740s, and the actual accounting records for the year 1754. I will also consider the accounts for the town of Boston in the 1790s.

THE TREASURER's REPORT 1675/1679

The Treasurer prepared a single report covering the years 1675 to 1679, from the commencement of King Philip's War to about 18 months beyond the official close of the war on February 12, 1678 [Mass. Archives]. The additional time probably allowed for submission of all charges and collection of the various "Rates" against the towns for revenues to pay the bills.

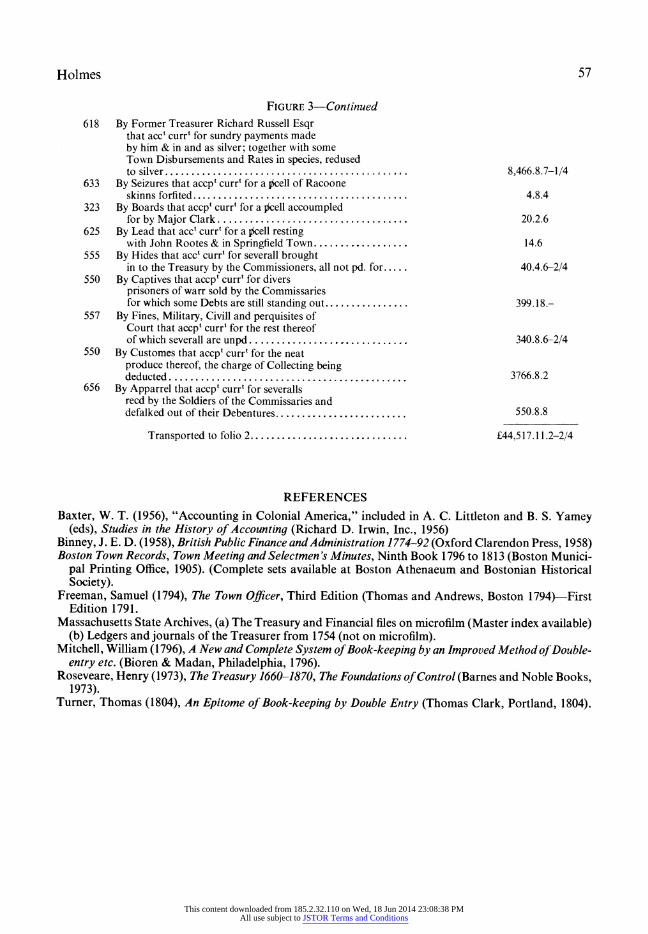

The Report consists of four double- folio pages, the left folio showing "debits" representing expenditures, and the right "folio" showing "credits," representing income. The usual "To" and "By" pre- fixes are used to round out the double- entry format. Each of the 73 classified line items comprising the expenditures is cross-referenced to what is almost cer- tainly a supporting ledger page, and the amount brought into the Report for each line item appears to be the total of the detail set forth on the ledger pages. Figures 1 and 2 of the Appendix show the debit and credit sides of the first double-folio page. Note also that the line items in the Report do not follow the sequence of the ledger pages. Like items were grouped together into ten major expenditure classifications and subtotals derived for each of these classes. Revenues were similarly classified into logical groupings.

The stark realities of the Indian War come down to us in one laconic entry, an "accopt currt" (account current) in- cluded in "payments to persons"

"To Scalps, that accopt currt for allowances to several for slaying sculking Indians ?21.2

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

Holmes 49

FIGURE 1 Condensed Report 1675/1679

To payments to persons ?34,672. 9.11 By assessments ?30,914.17. 10 To disburst for provant (food) 2,723.10. 5 By former Treasurer 8,466. 8. 7 To disburst for clothing 1,762. 6. 6 By captives-proceeds of sale 339.18. 0 To disburst for magazine (guns, etc.) 1,038.15. 3 By fines 340. 8. 6 To disburst for the traine (supplies) 428.16. 2 By customs, net 3,766. 8. 2

By apparel, sold 550. 8. 8 Total charge of the warr, as afore 40,625.18. 3 Bysundrysales 314. 0. 5

To disbursements relating to Civill Goverment 8,917.13. 8 By sundries 630.12. 0

To disbursment relating both By amount due by County of York 305.13. 2 to the warr and Civill Goverment as afore 2,304. 6. 7 By military re-imbursements 1,000. 0. 0

To fodder 91. 0. 0 By mint coinage 80. 0. 0 To several towns (abatements) 472. 2. 4 By several towns 3,869.12. 8 To remaining accounts receivable By miscellaneous (seven items) 127.10. 4 for which Treasurer is to be 127.18. 5 By balance due to Tr:asurer 1,773. 0.11

accountable ?52,538.19. 3 ?52,538.19. 3

Indian captives were sold into slavery in the West Indies, which explains the revenue item

"By captives-proceeds of sale ?399.18.0

Figure 1 is a condensed version which has been prepared to show the overall format. Individual line items of expendi- tures have been omitted but the subtotal for each related grouping is shown. Seven small classifications of revenues have been combined as "Miscellaneous."

There are several features of the Report that are worth noting:

1. It is not a cash receipts and disburse- ments account. Total assessments (?30,914.17.10) are accrued and, to the extent not collected, subse- quently abated (f472.2.4). The last debit entry charges the Treasurer with amounts still to be collected.

2. The income items are credits, and the expenditures debits, compatible with postings to "fictitious" ac- counts in a double-entry system.

3. The expenditures in the Report in- volve 73 classified line items, each

referenced to a ledger page. The classification is not carried to ex- tremes as evidenced by the follow- ing item:

To Miscellaneous that accpt currt for severalls ax mixed and rated together as not well to be placed to distinct accp"s ?54.2.0

I have written confidently of "ledgers," although I do not assert these were necessarily part of a double-entry system. The confidence is based on the wording of the extremely interesting Audit Certifi- cate written on the last pages which reads:

In Obedience to an order of ye Honored Gent Court, Dated May 19th, 1680 wee ye Sub- scribers mett at ye time Appointed to peruse ye Country Treasurers Accompts, & accord- ingly proceeded soo farr as we thought nessesary unless long time given for Examin- ing of it in ye particulars, ye Accot being very Voluminous Comprised in ffower large Leagers. But soo farr as wee Examined, and Upon consideracon of ye whole wee judge ye Accot to be just, & Capt Hull & Capt Honibs- man making Oath thereto may be allowed by this honoured Court, the Ballance due to ye Treasurt per said Accot is Seaventeen hundred Seventy three-pounds, elevenpence money.

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

50 The Accounting Review, January 1979

The said Treasurr informs vt Severall Townes are in Arreares for their rates, though Creditt be given for ye whole, as also there is one hundred twenty six pounds eighteen shillings four pence due to ye Country for fines cap- tives, etc. We finde Capt Hull hath chargd ffity two pounds per Annum for ffour years as Captt Honibsmans Salary for keeping ye books, but nothing for himself & servants.

All Wch wee present to this Honered Court seated in Boston. October ye 21, 1680

Humphry Davie John Richards II James Russell Anthony Stoddard"

So there were indeed flowerr large Leagers." The following analysis of the cross references to ledger pages appearing in the Report also tells a story:

Ledger Page Reference Range Numbers of References

200to300 2 301 to 400 3 401 to 500 5 501 to 600 36 601 to 700 49

95

A reasonable guess would be that the small numbers of references in the ranges 200 to 500 indicate the bookkeeper was using up some remaining empty pages in old ledgers brought forward from prior years.

It will be noticed that the auditors audited only "soo farr as we thought necessary." The "certificate" as written was presented first to the House of Magistrates-the upper house of the Legislature-and they appended their approval as follows:

This return of the Treasurer is Accepted by the magistry, their brethern the Deputies have to Consent

Edwd Rawson Secretary 25th October 1680

The Deputies-the lower house-were not, however, satisfied with the offhand

way the auditors had gone about their job and annotated their disapproval:

The Deputies Consent not hereto William Torrey, Clerk

On the Contra page appears the fol- lowing:

But the Deputies do consent provided such account as per overhead given be verified and do therefore apoynt Capt. Hutchinson, Capt. Tho. Brattle, Capt. Johnson further to im- prove that matter and what they find bring to the above attention

Jo Cooke per order 2.9.80

All apparently went well with the verification" and the final entry reads: passed by the Deputies 2 November 1680 Consented to by the magistry Edwd Rawson Secretary

All of the original auditors and subse- quent appointees were prominent Bos- tonians and active in the civil and mercan- tile life of the Town.

THE TREASURER'S REPORT IN THE 1 740s

The Treasurer's Reports in the 1740s are in the traditional form of an account of charge and discharge, quite unlike the "Income and Expenditure" format de- scribed above for the years 1675 through 1679. However, the content does not differ materially. Full assessments for tax revenues from the towns continue to be accrued and expenditures are classified under logical headings. However, there is one important difference. Each sub- total for the expenditures is related to an Appropriation authorized by the General Court. Those for the year 1647-48 are as follows:

Total expended Appropriation for Defense ?42,863. 2. 0 Appropriation for Forts

and Garrisons 16,917. 5. 5 Appropriation for Grants 12,352.14. 5 Appropriation for Repress'

(Representatives) Pay 4,418. 5. 0

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

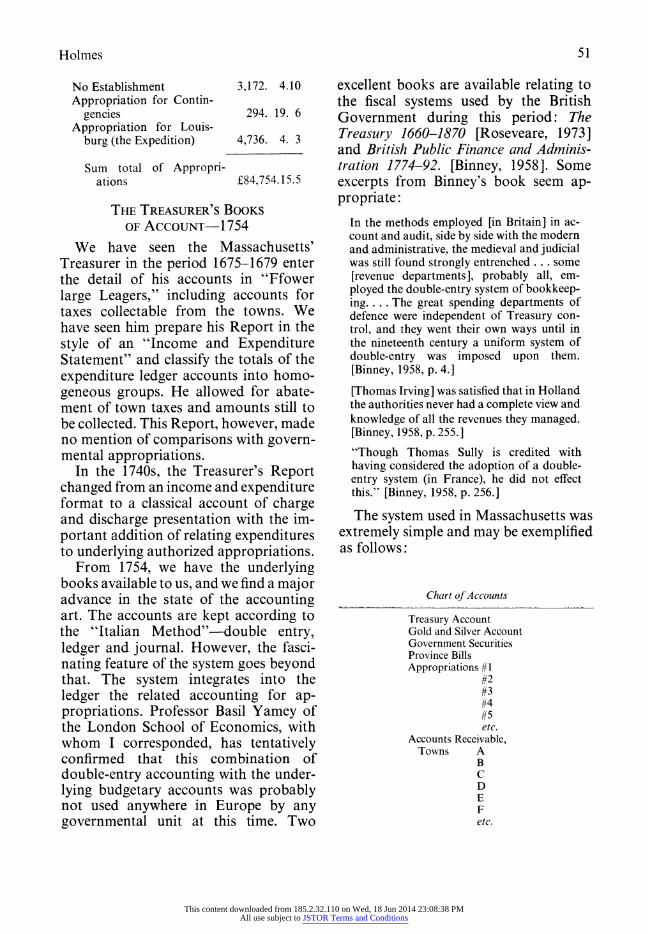

Holmes 51

No Establishment 3,172. 4.10 Appropriation for Contin-

gencies 294. 19. 6 Appropriation for Louis-

burg (the Expedition) 4,736. 4. 3

Sum total of Appropri- ations ?84,754.15.5

THE TREASURER'S BOOKS OF ACCOUNT- 1754

We have seen the Massachusetts' Treasurer in the period 1675-1679 enter the detail of his accounts in "Ffower large Leagers," including accounts for taxes collectable from the towns. We have seen him prepare his Report in the style of an "Income and Expenditure Statement" and classify the totals of the expenditure ledger accounts into homo- geneous groups. He allowed for abate- ment of town taxes and amounts still to be collected. This Report, however, made no mention of comparisons with govern- mental appropriations.

In the 1740s, the Treasurer's Report changed from an income and expenditure format to a classical account of charge and discharge presentation with the im- portant addition of relating expenditures to underlying authorized appropriations.

From 1754, we have the underlying books available to us, and we find a major advance in the state of the accounting art. The accounts are kept according to the "Italian Method"-double entry, ledger and journal. However, the fasci- nating feature of the system goes beyond that. The system integrates into the ledger the related accounting for ap- propriations. Professor Basil Yamey of the London School of Economics, with whom I corresponded, has tentatively confirmed that this combination of double-entry accounting with the under- lying budgetary accounts was probably not used anywhere in Europe by any governmental unit at this time. Two

excellent books are available relating to the fiscal systems used by the British Government during this period: The Treasury 1660-1870 [Roseveare, 1973] and British Public Finance and Adminis- tration 1774-92. [Binney, 1958]. Some excerpts from Binney's book seem ap- propriate:

In the methods employed [in Britain] in ac- count and audit, side by side with the modern and administrative, the medieval and judicial was still found strongly entrenched .. . some [revenue departments], probably all, em- ployed the double-entry system of bookkeep- ing.... The great spending departments of defence were independent of Treasury con- trol, and they went their own ways until in the nineteenth century a uniform system of double-entry was imposed upon them. [Binney, 1958, p. 4.]

[Thomas Irving] was satisfied that in Holland the authorities never had a complete view and knowledge of all the revenues they managed. [Binney, 1958, p. 255.]

"Though Thomas Sully is credited with having considered the adoption of a double- entry system (in France), he did not effect this." [Binney, 1958, p. 256.]

The system used in Massachusetts was extremely simple and may be exemplified as follows:

Chart of Accounts

Treasury Account Gold and Silver Account Government Securities Province Bills Appropriations #1

#2 #3 #4 #5 etc.

Accounts Receivable, Towns A

B C D E F etc.

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

52 The Accounting Review, January 1979

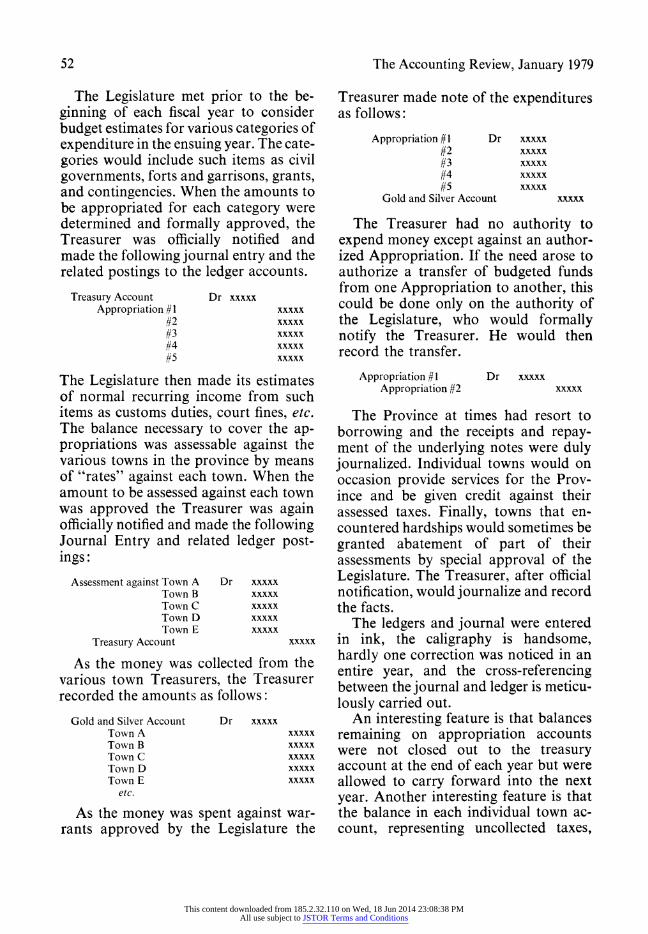

The Legislature met prior to the be- ginning of each fiscal year to consider budget estimates for various categories of expenditure in the ensuing year. The cate- gories would include such items as civil governments, forts and garrisons, grants, and contingencies. When the amounts to be appropriated for each category were determined and formally approved, the Treasurer was officially notified and made the following journal entry and the related postings to the ledger accounts.

Treasury Account Dr xxxxx Appropriation #1 xxxxx

#2 xxxxx #3 xxxxx #4 xxxxx #5 xxxxx

The Legislature then made its estimates of normal recurring income from such items as customs duties, court fines, etc. The balance necessary to cover the ap- propriations was assessable against the various towns in the province by means of "rates" against each town. When the amount to be assessed against each town was approved the Treasurer was again officially notified and made the following Journal Entry and related ledger post- ings:

Assessment against Town A Dr xxxxx Town B xxxxx Town C xxxxx Town D xxxxx Town E xxxxx

Treasury Account xxxxx

As the money was collected from the various town Treasurers, the Treasurer recorded the amounts as follows:

Gold and Silver Account Dr xxxxx Town A xxxxx Town B xxxxx Town C xxxxx Town D xxxxx Town E xxxxx

etc.

As the money was spent against war- rants approved by the Legislature the

Treasurer made note of the expenditures as follows:

Appropriation #1 Dr xxxxx #2 xxxxx #3 xxxxx #4 xxxxx #5 xxxxx

Gold and Silver Account xxxxx

The Treasurer had no authority to expend money except against an author- ized Appropriation. If the need arose to authorize a transfer of budgeted funds from one Appropriation to another, this could be done only on the authority of the Legislature, who would formally notify the Treasurer. He would then record the transfer.

Appropriation #I Dr xxxxx Appropriation #2 xxxxx

The Province at times had resort to borrowing and the receipts and repay- ment of the underlying notes were duly journalized. Individual towns would on occasion provide services for the Prov- ince and be given credit against their assessed taxes. Finally, towns that en- countered hardships would sometimes be granted abatement of part of their assessments by special approval of the Legislature. The Treasurer, after official notification, would journalize and record the facts.

The ledgers and journal were entered in ink, the caligraphy is handsome, hardly one correction was noticed in an entire year, and the cross-referencing between the journal and ledger is meticu- lously carried out.

An interesting feature is that balances remaining on appropriation accounts were not closed out to the treasury account at the end of each year but were allowed to carry forward into the next year. Another interesting feature is that the balance in each individual town ac- count, representing uncollected taxes,

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

Holmes 53

was periodically aged on the ledger page by year of assessment. To facilitate this process receipts from collectors were "aged"as posted. It may also be noted that the system used for revenues is still used by Massachusetts municipalities and referred to as the "modified accrual method." Under this method the major tax assessments eventually paid by the townspeople were accrued and most of the "indirect" taxes-customs duties, fines, etc.-were kept on a cash basis. The only major step missing in the colonial accounts present in today's system was that "encumbrances" against appropri- ations were not recognized at year-end.

Despite what appears to be a complete double-entry system the financial report rendered annually to the Legislature con- tinued to be in account of charge and discharge format. The information to construct this report could, of course, be derived with relative ease from the ledger accounts. Also the records so far have not disclosed a trial balance book, al- though trial balances might have been prepared annually on separate sheets of paper.

The Treasurer in 1753 was Harrison Gray, who had just been appointed to the office and held the post until 1775. A summary review of the ledger and jour- nals during this period seems to indicate that the system described above was in force during this entire period. However, Gray was a Loyalist, and with the defeat of the British forces in the revolution, he moved his family from Massachusetts to England.

Some intriguing questions remain. Did Gray inherit the system from earlier Treasurers whose ledgers and journals are not available to us? If so, who in- vented the system and how far back does it go? If the system was introduced during Gray's period of office, did he himself keep the books or did some un-

named knowledgeable clerk do the actual record keeping?

Harrison Gray himself was a well- established merchant, having taken over a successful ropework business. My guess (and it is only that) is that Gray introduced the system. After he left for England in 1775, a new Treasurer ap- pointed by the revolutionary government took over the office. If Gray himself was the brains behind the accounting system, it is unlikely that his successor would be equally knowledgeable. It will be inter- esting to examine the records beyond 1775 to see whether the new Treasurer was able to sustain the accounting stan- dards set by Gray.

TOWN ACCOUNTS

This article has dealt thus far with the accounts of the Province of Massachu- setts. However, at a lower level of govern- ment, an equally interesting matter war- rants attention. In 1791 Samuel Freeman, a lawyer resident in Portland, Maine, published the first edition of his book The Town Officer [Freeman, 1791] deal- ing with the duties of the Selectmen, Town Clerks, Town Treasurers, Assess- ors, etc. However, one of the late chapters sets forth in 27 pages "A Plain and Regu- lar Method to Keep Accounts of the Expenditures of Monies voted by a Town; upon an Inspection of which, the State of its Finances may at any time be known." The system described is double- entry and, like the Massachusetts system, includes the accounting for the annual appropriations as an integral part of the system. The chapter provides a full "set" of accounts, journal and ledger, based on normal transactions within a town during the year.

It should be noted that Freeman's book is dated five years before A New and Complete System of Bookkeeping, published in Philadelphia in 1796 [Mitch-

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

54 The Accounting Review, January 1979

ell, 1796]. The obvious question is how a lawyer would have been knowledgeable enough to devise such a system. Free- man's second edition was published in Boston in 1793 and he undoubtedly had connections in Massachusetts. Was he familiar with the Massachusetts system of accounts and did he adapt it to town finances? There is a further possibility. The third book on bookkeeping pub- lished in America was Thomas Turner's An Epitome of Bookkeeping by Double Entry, also published, in 1804, in Port- land, Maine [Turner, 1804]. Could there have been some arrangement between Freeman and Turner for the accounting chapters in Freeman's book?

BOSTON TOWN ACCOUNTING IN THE 1790s

The move towards public account- ability is noted also in the minutes of the Boston Town Meetings in 1798 and 1799. In 1798 the "Committee Appointed to Audit the Town Treasurer Account" after reporting that they found the last year's accounts "well Vouched and right cast" reported also that "They annex Gen' Account of the Treasurer and a tryall Balance of his Books." More sig- nificantly, however, they go on:

Your Committee recommend that the Town desire the Selectmen to procure a Book and order the Town Clerk to keep Accounts agree- able to the Appropriations as above and in their Drafts on the Treasurer it will be proper to designate the Appropriation; they also Recommend that the Treasurer be ordered to Open as many Accounts in his Books as will conform to said Appropriations & charge each agreeable to the Selectmen's Drafts-so that in future the Town may know which & how much they fall short of the Sums granted.

This was basically the system recom- mended in The Town Officer. The Boston Treasurer was apparently already using double-entry. Now he was being asked to

integrate the appropriation breakdown into his ledger classifications. The detail in his ledger should agree with that in the Selectmen's "Book."

The town went one step farther the following year at the May 14, 1799, town meeting.

"A schedule of the Town expences was re- ported and on motion, Voted that the same be printed & delivered to the Inhabitants."

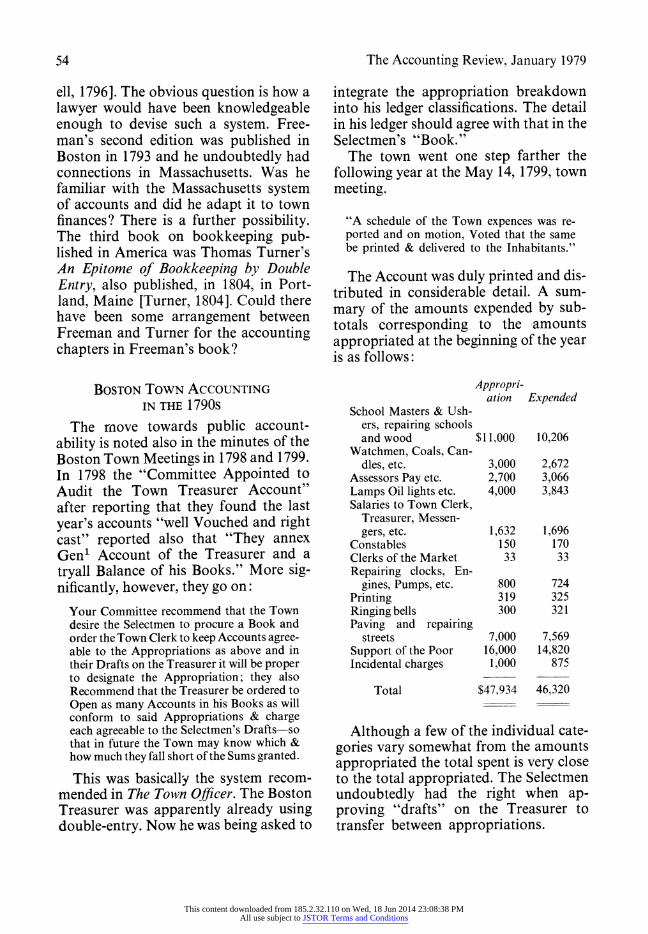

The Account was duly printed and dis- tributed in considerable detail. A sum- mary of the amounts expended by sub- totals corresponding to the amounts appropriated at the beginning of the year is as follows:

Appropri- ation Expended

School Masters & Ush- ers, repairing schools and wood $11,000 10,206

Watchmen, Coals, Can- dles, etc. 3,000 2,672

Assessors Pay etc. 2,700 3,066 Lamps Oil lights etc. 4,000 3,843 Salaries to Town Clerk,

Treasurer, Messen- gers, etc. 1,632 1,696

Constables 150 170 Clerks of the Market 33 33 Repairing clocks, En-

gines, Pumps, etc. 800 724 Printing 319 325 Ringing bells 300 321 Paving and repairing

streets 7,000 7,569 Support of the Poor 16,000 14,820 Incidental charges 1,000 875

Total $47,934 46,320

Although a few of the individual cate- gories vary somewhat from the amounts appropriated the total spent is very close to the total appropriated. The Selectmen undoubtedly had the right when ap- proving "drafts" on the Treasurer to transfer between appropriations.

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

Holmes 55

CONCLUSION

Much remains to be done to resolve all the questions posed above. The most immediate step, as I have pointed out, is to analyze the Massachusetts records beyond 1775. The second is to check the systems in use in adjoining New England colonies at the same period. The records of the other original colonies-Virginia, the Carolinas, New York, and Pennsyl- vania-should also be examined.

At the municipal level, the Boston records should be researched. These are now in the custody of the rare book room at the Copley Square branch of the Bos-

ton Public Library. However, they have not yet been indexed or catalogued and currently are not being made available for research. I was able to make a cursory examination of one journal and ledger and it is apparent the town was using a double-entry system about 1780, perhaps earlier.

All in all, early governmental account- ing appears to be a fertile field for the American colonial accounting historian to cultivate. We must

Copy fair what time hath blurred Reedeem truth from his jaws.

(Herbert 1800)

APPENDIX

FIGURE 2

MASSACHUSETTS COLONY Treasurer's Report-1675/1679

1675 662 Massachusetts Goverment Dr Cash Cash

June 643 To Military Service, that accpt currt for Stipends to Comanders, Officers, and Souldiers .............? . ? 16,270.19.10-3/4

646 To portage, that accpt currt for posts, Guids, scouts, pilots, and Interpretors ........................... f 81.19 2-3/4

549 To Gards, that accpt currt for Convoughs, Cartg Ligherterg, porters........?....................... ? 196. 2 9-3/4

630 To Maritim Disbursments that accpt Currt for wages to Seamen and frait........................ ? 578.18.3

657 To wounded men, that accpt currt for payments to Doc"s, Chirurgeons, Maimed souldiers, and accommodations ..........?.. .. ... ? 568.14.8-2/4

656 To Contingencies that accpt currant for Journies, allowances, gratuities, serches & .? 668.14.-3/4

623 To Indian service that accptcurrt for payments to the Native souldiers .? 566.8.6-2/4

637 To Mixt Disbursments that accpt currt for charges brought in by the severall Townes for Hors, Armes Ammunition, provant & of which that certified to be pd by the Former Treasurer, that accpt currt hath Credit for as p Contra..............?.. . ? 14,830.10.3-1/4

626 To Ferriage that accptcurrt forTransportingoverpasses.. ? 34.11.7 658 To Accountable payments that accpt currt for money

recd. by severall persons to pay Souldiers on which rests on accpt on returns. ? 79.2.1

556 To Scalps that accpt currt for allowances to severall for slaying skulking Indians ....................... ? 21.2.-

540 To Eastern Expedition that accpt currt for severalls sent to these parts for supply of the Army and Inhaby tants there..................?............... ? 303.13.9 2/4

544 To Discountments that accpt currt for the Debits of plymouth Colony, Conecticott Colony and United

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

56 The Accounting Review, January 1979

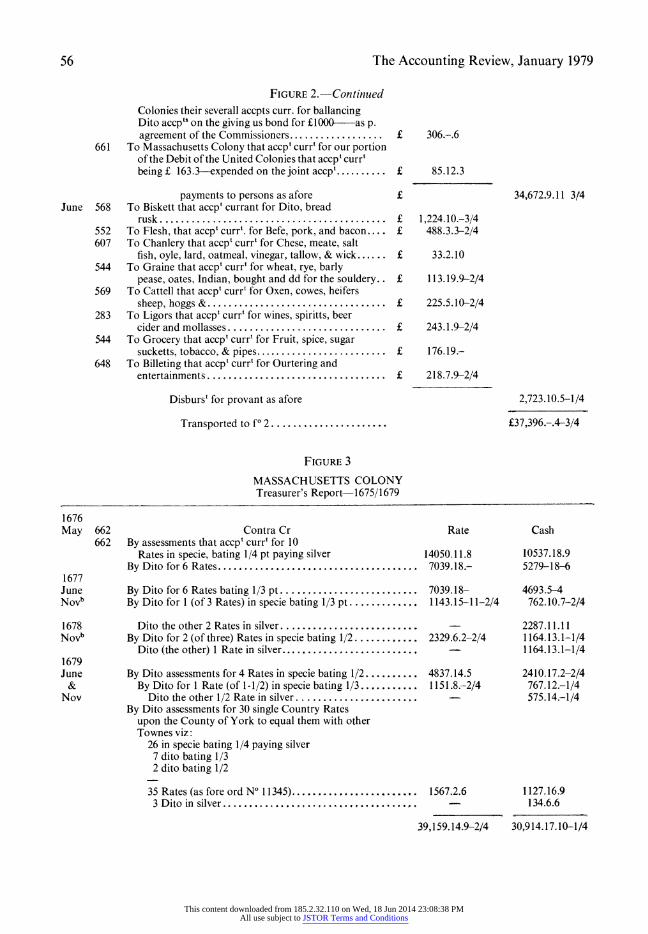

FIGURE 2.-Continued

Colonies their severall accpts curr. for ballancing Dito accpts on the giving us bond for ?1000-as p. agreement of the Commissioners .?. t 306.-.6

661 To Massachusetts Colony that accp' curry' for our portion of the Debit of the United Colonies that accp'curr' being ? 163.3-expended on the joint accp'.......... ? 85.12.3

payments to persons as afore ? 34,672.9.11 3/4 June 568 To Biskett that accp' currant for Dito, bread

rusk ..? 1,224.10.-3/4 552 To Flesh, that accp' curr. for Befe, pork, and bacon ? 488.3.3-2/4 607 To Chanlery that accp' curry' for Chese, meate, salt

fish, oyle, lard, oatmeal, vinegar, tallow, & wick....?.. . 33.2.10 544 To Graine that accp' curry' for wheat, rye, barly

pease, oates, Indian, bought and dd for the souldery. ? 113.19.9-2/4 569 To Cattell that accp' curryt for Oxen, cowes, heifers

sheep, hoggs & ........? 225.5.10-2/4 283 To Ligors that accp' curry' for wines, spiritts, beer

cider and mollasses ..................?............ 243.1.9-2/4 544 To Grocery that accp' curryt for Fruit, spice, sugar

sucketts, tobacco, & pipes................... ? 176.19.- 648 To Billeting that accp' curry' for Ourtering and

entertainments . . . . ? 218.7.9-2/4

Disburst for provant as afore 2,723.10.5-1/4

Transported to fP 2. ?37,396.-.4-3/4

FIGURE 3

MASSACHUSETTS COLONY Treasurer's Report-1675/1679

1676 May 662 Contra Cr Rate Cash

662 By assessments that accp' curry' for 10 Rates in specie, bating 1/4 pt paying silver 14050.11.8 10537.18.9

By Dito for 6 Rates ......................... ......... 7039.18.- 5279-18-6 1677 June By Dito for 6 Rates bating 1/3 pt. . . 7039.18- 4693.5-4 NoVb By Dito for 1 (of 3 Rates) in specie bating 1/3 pt ....... 1143.15-11-2/4 762.10.7-2/4

1678 Dito the other 2 Rates in silver .. . . . .- 2287.11.11 NoVb By Dito for 2 (of three) Rates in specie bating 1/2 ...... . .. - 2329.6.2-2/4 1164.13.1-1/4

Dito (the other) 1 Rate in silver.-..... 1164.13.1-1/4 1679 June By Dito assessments for 4 Rates in specie bating 1/2 . 4837.14.5 2410.17.2-2/4

& By Dito for 1 Rate (of 1-1/2) in specie bating 1/3 ... .. . 1151.8.-2/4 767.12.-1/4 Nov Dito the other 1/2 Rate in silver .................... - 575.14.-1/4

By Dito assessments for 30 single Country Rates upon the County of York to equal them with other Townes viz:

26 in specie bating 1/4 paying silver 7 dito bating 1/3 2 dito bating 1/2

35 Rates (as fore ord N 11345)... 1567.2.6 1127.16.9 3 Dito in silver ......... ................ ......... 134.6.6

39,159.14.9-2/4 30,914.17.10-1/4

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions

Holmes 57

FIGURE 3-Continued 618 By Former Treasurer Richard Russell Esqr

that acc' currt for sundry payments made by him & in and as silver; together with some Town Disbursements and Rates in species, redused to silver .. . .. 8,466.8.7-1/4

633 By Seizures that accp' curry' for a Ocell of Racoone skinns forfited .......................................4.8.4

323 By Boards that accp' currt for a cell accoumpled for by Major Clark ...... . . . 20.2.6

625 By Lead that acc' currt for a Ocell resting with John Rootes & in Springfield Town ....... 14.6

555 By Hides that acc' currt for severall brought in to the Treasury by the Commissioners, all not pd. for 40.4.6-2/4

550 By Captives that accp' curry' for divers prisoners of warr sold by the Commissaries for which some Debts are still standing out ................ 399.18.-

557 By Fines, Military, Civill and perquisites of Court that accp' curry' for the rest thereof of which severall are unpd . 340.8.6-2/4

550 By Customes that accp' curry' for the neat produce thereof, the charge of Collecting being deducted............................... ....... 3766.8.2

656 By Apparrel that accp' currt for severalls recd by the Soldiers of the Commissaries and defalked out of their Debentures. 550.8.8

Transported to folio 2 ........ ....... ?44,517.11.2-2/4

REFERENCES

Baxter, W. T. (1956), "Accounting in Colonial America," included in A. C. Littleton and B. S. Yamey (eds), Studies in the History of Accounting (Richard D. Irwin, Inc., 1956)

Binney, J. E. D. (1958), British Public Finance and Administration 1774-92 (Oxford Clarendon Press, 1958) Boston Town Records, Town Meeting and Selectmen's Minutes, Ninth Book 1796 to 1813 (Boston Munici-

pal Printing Office, 1905). (Complete sets available at Boston Athenaeum and Bostonian Historical Society).

Freeman, Samuel (1794), The Town Officer, Third Edition (Thomas and Andrews, Boston 1794)-First Edition 1791.

Massachusetts State Archives, (a) The Treasury and Financial files on microfilm (Master index available) (b) Ledgers and journals of the Treasurer from 1754 (not on microfilm).

Mitchell, William (1796), A New and Complete System of Book-keeping by an Improved Method of Double- entry etc. (Bioren & Madan, Philadelphia, 1796).

Roseveare, Henry (1973), The Treasury 1660-1870, The Foundations of Control (Barnes and Noble Books, 1973).

Turner, Thomas (1804), An Epitome of Book-keeping by Double Entry (Thomas Clark, Portland, 1804).

This content downloaded from 185.2.32.110 on Wed, 18 Jun 2014 23:08:38 PMAll use subject to JSTOR Terms and Conditions