Government –scal policies and redistribution in Asian...

61

Motivation Redistributive scal policies Tax incidence Expenditure incidence Empirical estimates Taxation Government expenditures Fiscal policies in Asia Summary and conclusions Government scal policies and redistribution in Asian countries Iris Claus Treasury Guest Lecture 28 February 2012 Treasury Guest Lecture 1 / 61

-

Upload

vuongthuan -

Category

Documents

-

view

216 -

download

0

Transcript of Government –scal policies and redistribution in Asian...

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Government fiscal policies and redistribution inAsian countries

Iris Claus

Treasury Guest Lecture

28 February 2012

Treasury Guest Lecture 1 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Acknowledgement and disclaimer

• This work is joint with Jorge Martinez-Vazquez andVioleta Vulovic (Georgia State University).

• The views expressed are our own and do not necessarilyreflect the views or policies of the Asian DevelopmentBank or its board of governors or the governments theyrepresent.

Treasury Guest Lecture 2 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Motivation of paper

• There are many reasons why countries adopt redistributivepolicies

• . . . to pursue social justice• . . . to achieve effi ciency with equity (i.e. to grow the pieby cutting it more fairly)

• Redistribution may be achieved through taxation andgovernment expenditures.

Treasury Guest Lecture 3 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Purpose of this paper

• Assess the impact of government fiscal policies on incomedistribution in Asia

- Review the international literature on the role andeffectiveness of redistributive fiscal policies- Quantify the impact of taxation and governmentexpenditures on income disparity in Asia- Discuss how the effectiveness of fiscal policies inAsia may be improved

Treasury Guest Lecture 4 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax and expenditure incidence analysis

• ... assesses the impact of fiscal policies on incomedistribution and on the poor.

• ... is an effective tool to review whether policies have thedesired impact.

• Who pays a tax is often different from who is legally liableto make the payment (e.g. payroll taxes and socialsecurity contributions).

• Not all expenditures benefit people of different incomelevels to the same extent.

• E.g. more spending on primary education and less oncollege education should benefit the poor.

• But the effects may be mitigated by the lack of access ofthe poor in rural areas to schools.

Treasury Guest Lecture 5 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax incidence

• Tax incidence analysis needs to take into account:

- different types of tax- tax expenditures (exemptions, rebates, deductions,tax credits, special tax rates)- negative income taxes (cash transfers)- in-kind transfers (food stamps, voucher programs)

• It is diffi cult to measure.• Agents can shift the burden of taxes, e.g. via changes inprices charged to consumers, wages paid to workers.

• Taxes impose costs beyond the amounts collected bygovernments (excess burden or deadweight losses).

• What is the appropriate counterfactual to use as abenchmark?

Treasury Guest Lecture 6 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax incidence: three methodologies

1 Microsimulation models. . . make certain assumptions about taxes and allocate taxburdens to different income groups.

2 General equilibrium models. . . contain less detail on different income groups. Taxincidence is determined by the structure of the economy.

3 Regression based estimates. . . use time series analysis for particular country, crosscountry and panel data sets.

Treasury Guest Lecture 7 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Microsimulation models

• ... use household or consumer income and expendituresurveys and tax administrative data.

• For each tax, a portion of the total revenues collected isimputed as tax burden to each income group.

• E.g. excise taxes on tobacco are allocated to differentincome groups in proportion to their relative share in theconsumption of tobacco products.

• The incidence for each tax is calculated for each incomegroup and added up across all taxes to give a total taxburden for each income group

• ... expressed as an average total tax rate, i.e. theproportion of income paid in taxes by each income group.

Treasury Guest Lecture 8 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Microsimulation models: assumptions

• ... must make explicit assumptions about shifting and finalincidence of taxes based on theory and/or estimation.

• Typically there is agreement on the assumptions used forthe different taxes

• ... and where there is no consensus, sensitivity analysis isperformed.

• Personal income taxes are typically assumed not to beshifted and to be paid by the recipients of income.

• With progressive tax rates, this tax usually has aprogressive incidence.

• Payroll and social security taxes are typically assumed tobe fully shifted to workers.

• In the presence of a cap on income for contributions, itsincidence is regressive.

Treasury Guest Lecture 9 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Microsimulation models: assumptions

• For corporate income taxes a variety of shiftingassumptions have been proposed and analyzed(i) no shifting at all so that shareholders pay the full tax(ii) shifting to all capital owners through an equalizationof after-tax rates of return for all capital(iii) backward shifting to workers in the form of lowerwages(iv) forward shifting to consumers in the form of higherconsumer prices (depending on the degree of monopoly powerin markets)

• Typically, half of the tax burden was assumed to be paidby all owners of capital and the other half by consumers.

• With more open economies and mobile capital, asignificant part of the tax is now assumed to be paid byworkers.

Treasury Guest Lecture 10 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Microsimulation models: assumptions

• Taxes on goods and services (sales taxes, value addedtaxes, excises) are typically assumed to be regressive andshifted forward to consumers.

• The incidence of sales taxes is complicated by the presenceof cascading and multiple rates and exemptions.

• The regressivity of value added taxes may be reduced withdifferential rates (lower for necessities and higher forluxury items) or exemptions for basic commodities andnecessities.

• Value added and excise taxes have been found to be lessregressive or even neutral when analyzed over a longer timeframe or on life time basis rather than current income.

Treasury Guest Lecture 11 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Microsimulation models: assumptions

• Excise taxes can have a progressive impact as in the caseof luxury goods (gasoline, cars, expensive liquor, perfumes)

• ... and also a regressive impact (kerosene fuel used forcooking, tobacco products or cheap liquor).

• Taxes on imports are typically assumed to have the sameregressive incidence as sales and value added taxes for lackof better information.

• Property tax incidence is more controversial.• Some studies assume no shifting with the tax paid by theowners of the property or shifted to all owners of capital,in which case the tax is progressive.

• Others assume the forward shifting of property taxes torenters or users of the property, in which case they can beregressive.

Treasury Guest Lecture 12 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Microsimulation models: pros and cons

• The methodology is relatively simple and easy toimplement.

• The underlying assumptions are transparent and theimplications of alternative assumptions can be easilycompared.

• The analysis can include large samples of taxpayers.• But good information on income (and expenditure)distribution is not always available.

• Second round feedback effects are typically ignored whenassessing tax policy changes.

• Most importantly, the shifting assumptions have beencriticized for “stipulating” the incidence of various taxes.

Treasury Guest Lecture 13 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

General equilibrium models

• ... were pioneered by Harberger (1962).• Computable general equilibrium models are numericallysolved using data from the national accounts, householdexpenditure surveys and taxpayer data.

• ... analyze the incidence of taxes within the economy,without making explicit assumptions about the finalshifting of taxes.

• Tax incidence depends on the values of several criticalparameters in the economy (capital-labor ratios in differentsectors, elasticities of substitution in production among thedifferent factors).

• It is measured by the differences in the vector ofequilibrium prices before and after a tax change.

Treasury Guest Lecture 14 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

General equilibrium models: pros and cons

• General equilibrium models employ an explicit structuralmodel of the economy with utility/demand functions andproduction/supply functions.

• They offer transparency in how incidence results are linkedto assumptions on fundamental parameters.

• They take into account indirect or second round feedbackeffects of taxation (or government expenditure) changes.

• But they are operationally intensive and the number oftaxpayers represented needs to be small.

• And even though this approach does not “stipulate”incidence results

• ... it does “stipulate” critical parameters.

Treasury Guest Lecture 15 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Regression based estimates

• A limited number of recent studies have used multivariateeconometric analysis

• ... to investigate the impact of taxes on the distribution ofincome (typically measured by gini coeffi cients) acrosscountries.

• Cross-section or panel data

Treasury Guest Lecture 16 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Regression based estimates: pros and cons

• The econometric approach allows analyzing the impact oflarge variations in the level and structure of taxes acrosscountries,

• ... variations that are unlikely observed within the contextof a single economy.

• But the impact of the different elements of the taxstructure on income distribution cannot be examined inany detail,

• ... at least not to the extent allowed by the generalequilibrium approach and especially microsimulationmodels.

Treasury Guest Lecture 17 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax incidence: international evidence

1 Tax systems tend to be progressive even though sometaxes within them are regressive.

2 Incidence analysis needs to be performed within the bigpicture (revenue mobilization, excess burden,administration and compliance costs).

3 Overall, tax systems do not have a large impact on thedistribution of income.

Treasury Guest Lecture 18 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Expenditure incidence

• . . . is diffi cult to measure.• Public goods and services are often provided withoutdirect charges and there are no market prices to infer themarginal benefits.

• Even when a fee is charged, this price cannot beinterpreted as the marginal benefit for individuals

• . . . because the supply of most public goods and servicesis subsidized or rationed and does not respond directly todemand.

Treasury Guest Lecture 19 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Expenditure incidence: three approaches

1 Benefit incidence. . . measures by how much the income of a householdwould have to be raised if the household had to pay forthe subsidized public services at full cost.

2 Behavioral approach. . . estimates demand functions for public goods andservices to generate price elasticities and marginalwillingness to pay.

3 Regression based estimates. . . use time series analysis for a particular country, crosscountry and panel data sets.

Treasury Guest Lecture 20 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Benefit incidence

• ... measures by how much the income of a householdwould have to be raised if the household had to pay forthe subsidized public goods and services at full cost.

• ... uses information on the costs of publicly providedgoods and services and on their uses by different incomegroups to arrive at estimates of the distribution of benefits.

• Information on individual or household use of the publicgoods and services is typically obtained from surveys.

• Benefit incidence has been estimated for three maincategories: education, health and some types ofinfrastructure.

Treasury Guest Lecture 21 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Benefit incidence: pros and cons

• The approach provides simplicity and transparency ofestimation procedures.

• It allows studying which public expenditures are mosteffective in reaching and improving the status of the poor.

• But the cost measures may not be a good approximationof the true benefits or marginal valuations of the publicgoods and services provided.

• It cannot incorporate changes in the behavior ofindividuals in response to changes in public expenditure.

• The analysis is limited to public expenditure programs forwhich private beneficiaries can be identified.

• It can also ignore important interaction effects with theprivate sector.

Treasury Guest Lecture 22 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Behavioral approach

• ... takes people’s preferences to derive marginal willingnessto pay as the measure of benefit from public expenditures.

• ... uses econometric methods to exploit variations inbehavior in the use of public goods and services, prices,incomes and other household characteristics acrossindividuals and time

• ... to derive demand functions,• ... price elasticities and willingness to pay.• With that information one can estimate the incidence ofpublic spending programs

• ... and the response to any changes in costs associatedwith the use of a public good or service.

Treasury Guest Lecture 23 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Behavioral approach: pros and cons

• The approach is more theoretically sound with clearfoundations in microeconomics.

• It allows the estimation of incidence for publicexpenditures for which specific users cannot be identified.

• It incorporates individual behavioral responses• ... and thus provides guidance for policy reform and betterdesign and targeting of public policies to the poor.

• But it is more data intensive and methodologically morecomplex.

Treasury Guest Lecture 24 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Regression based estimates

• A limited number of recent studies have used multivariateeconometric analysis

• ... to investigate the impact of government expenditureson the distribution of income (typically measured by ginicoeffi cients) across countries.

• Cross-section or panel data

Treasury Guest Lecture 25 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Regression based estimates: pros and cons

• The econometric approach allows analyzing the impact oflarge variations in the level and composition ofgovernment spending across countries,

• ... variations that are unlikely observed within the contextof a single economy.

• But it does not allow analyzing the specific details ofpolicies and institutions

• ... that can make a significant difference on theeffectiveness and overall impact of public expenditurepolicies.

Treasury Guest Lecture 26 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Expenditure incidence: international evidence

1 Spending programs on social welfare and the social sectorscan significantly reduce income inequality.

2 More effective redistributional policies, especially for thepoor, can be implemented with government expenditurethan with taxes.

3 But the impact of policies depends crucially on thetargeting of expenditures to the poor and lower incomegroups.

Treasury Guest Lecture 27 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Empirical estimation: evidence for Asia

• To quantify the impact of taxation and governmentexpenditures on income inequality in Asia, measured bygini coeffi cients

• Panel data analysis uses 150 countries with data between1970 and 2009.

• 23 Asian countries are included.• Taxes and government expenditures are consideredindividually and jointly.

• Asia specific tax and government expenditure effects areidentified using dummy variables.

Treasury Guest Lecture 28 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

All regressions

• . . . include lagged inequality• ... dummy variables to account for differences in thecomputation of gini coeffi cients across countries (gross/netincome, expenditure)

• ... a set of control variables that are commonly used in theliterature to explain income inequality (population growth,youth dependency, old-age dependency, a globalization index,per capita GDP, long-term unemployment, perception ofcorruption, schooling and size of government)

• ... and inflation.

Treasury Guest Lecture 29 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Fiscal variables: tax

• Tax variables include personal income taxes, corporateincome taxes, social security contributions and payrolltaxes, general taxes on goods and services, excises andcustoms duties, all measured as a percent of GDP, and aprogressivity measure.

• The progressivity measure is Sabirianova Peter, Buttrickand Duncan’s (2010) average rate progression variable.

• It is based on countries’personal income tax system(statutory tax rates, tax brackets, country-specific taxlegislation, basic allowances, standard deductions, tax credits,national surcharges and local taxes).

Treasury Guest Lecture 30 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Fiscal variables: progressivity measure

• Average tax rates are computed for each country for eachyear at 100 different levels of pre-tax income, which areevenly spread in the range from 4 to 400 percent of acountry’s GDP per capita.

• The average rates (for each country and each year) arethen regressed on the log of the 100 pre-tax income datapoints that are formed around per capita GDP.

• A country’s tax structure in a particular year is interpretedas progressive, neutral or regressive if the estimated slopecoeffi cient is positive, zero or negative.

Treasury Guest Lecture 31 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Fiscal variables: public spending

• Government expenditures include spending on socialprotection, education, health and housing, all measured asa percent of GDP.

• Ideally, subcomponents would have been included (e.g.basic education, primary health).

• But internationally comparable disaggregated data are notavailable.

Treasury Guest Lecture 32 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Personal income taxes

Estimated marginal impact on inequality (percentage points)Asia Rest of the world

Personal income tax -0.573 -0.041Personal income tax * progressivity -0.002 -0.005

• Personal income taxation reduces income inequality.• The effect is significantly larger in Asia than in othercountries.

• The greater effect in Asia may be due to a larger numberof people not paying income tax.

• The impact of progressive income tax scales is modest andsomewhat smaller in Asia than in the rest of the world.

Treasury Guest Lecture 33 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Corporate income taxes

Estimated marginal impact on inequality (in percentage points)Asia Rest of the world

Corporate income tax 0.598 -0.338Corporate income tax * globalization -0.017 0.005

• Corporate income taxes (CIT) reduce income disparity inthe rest of the world but is regressive in Asia.

• ... possibly due to larger tax concessions and subsidies forAsian firms.

• CIT interacted with globalization lowers inequality in Asia• ... which is the opposite from what is expected and whatis observed in the rest of the world

• ... possibly due to higher effective tax rates for foreignfirms in Asia compared to domestic firms and than in therest of the world.

Treasury Guest Lecture 34 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Social security contributions and payroll taxes

Estimated marginal impact on inequality (in percentage points)Asia Rest of the world

Social security and payroll taxes 1.324 0.165

• . . . are typically shifted to employees in the form of lowerwages and capped at higher incomes, increasing incomeinequality.

• . . . are found to be particularly harmful in Asia.• The estimated adverse effect on income inequality is eighttimes larger than in the rest of the world.

Treasury Guest Lecture 35 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

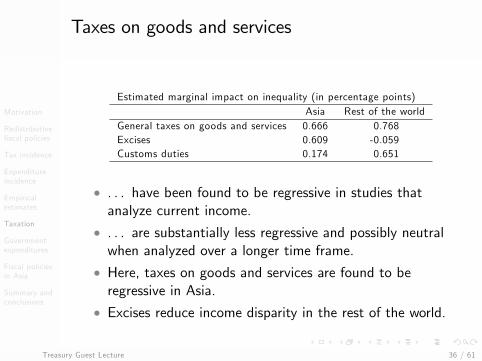

Taxes on goods and services

Estimated marginal impact on inequality (in percentage points)Asia Rest of the world

General taxes on goods and services 0.666 0.768Excises 0.609 -0.059Customs duties 0.174 0.651

• . . . have been found to be regressive in studies thatanalyze current income.

• . . . are substantially less regressive and possibly neutralwhen analyzed over a longer time frame.

• Here, taxes on goods and services are found to beregressive in Asia.

• Excises reduce income disparity in the rest of the world.

Treasury Guest Lecture 36 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Social protection spending

Estimated marginal impact on inequality (in percentage points)Asia Rest of the world

Social protection 0.490 -0.276

• . . . has the expected negative sign in the rest of the world.• . . . is found to increase income inequality in Asia.• . . . consists of (i) services and transfers provided toindividuals and households, and (ii) expenditures onservices provided on a collective basis.

• Asian countries provide relatively few services andtransfers (first component).

• The second component (formulation and administration ofgovernment policy, formulation and enforcement of legislationand standards for providing social protection, and appliedresearch and experimental development into social protectionservices) is likely to dominate.

Treasury Guest Lecture 37 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Social protection spending

Estimated marginal impact on inequality (in percentage points)Asia Rest of the world

Social protection 0.490 -0.276

• For the few services and transfers that Asian countriesprovide there may be a narrow benefit coverage and a lackof targeting to the poor.

• E.g. unemployment benefits are typically restricted topeople in formal employment.

• Pension systems in Asian countries, outside the OECD,can be generous (due to early retirement ages and relativelyhigh pension levels)

• ... but they are typically only available to a privilegedminority.

Treasury Guest Lecture 38 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Government expenditure on housing, health andeducation

Estimated marginal impact on inequality (in percentage points)Asia Rest of the world

Housing 2.162 -0.614Health -0.241 -0.330Education -0.486 -0.034

• Government expenditure on housing reduced incomeinequality in the rest of the world but increases it in Asia.

• Health spending in Asia has a similar negative effect onincome inequality as in other countries.

• Education expenditure has a somewhat larger negativeimpact.

Treasury Guest Lecture 39 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Improving the effectiveness of fiscal policies in Asia

• Taxation is a less effective tool for redistributing incomethan public spending.

• But it is crucial for raising government expenditure toachieve distributional objectives.

• Effectiveness of tax systems and tax administration incollecting tax revenue in Asia

• Brief discussion of government spending policies oneducation, health and social protection to throw more lighton our econometric findings

Treasury Guest Lecture 40 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

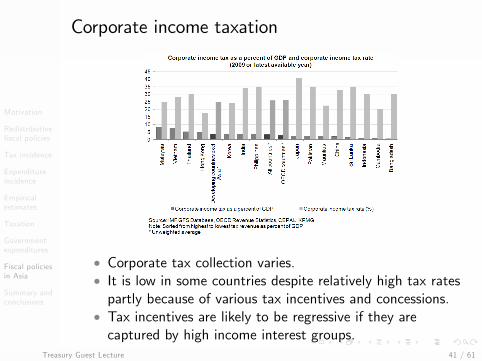

Corporate income taxation

• Corporate tax collection varies.• It is low in some countries despite relatively high tax ratespartly because of various tax incentives and concessions.

• Tax incentives are likely to be regressive if they arecaptured by high income interest groups.

Treasury Guest Lecture 41 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

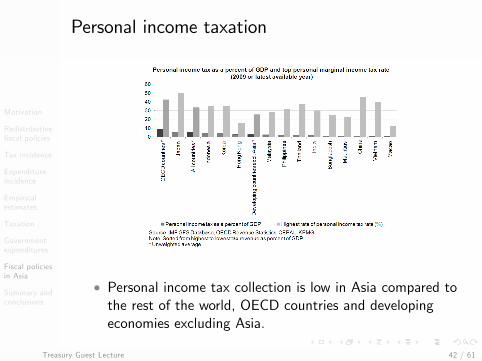

Personal income taxation

• Personal income tax collection is low in Asia compared tothe rest of the world, OECD countries and developingeconomies excluding Asia.

Treasury Guest Lecture 42 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Personal income taxation

• Personal income tax collection is low partly because of ahigher tax free (minimum exempt) thresholds ...

Treasury Guest Lecture 43 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Personal income taxation

• ... and a higher threshold of income above which the topmarginal personal income tax rate applies.

Treasury Guest Lecture 44 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

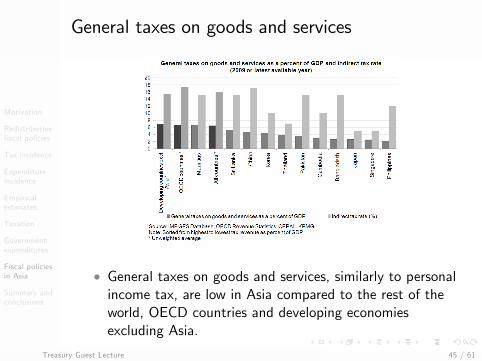

General taxes on goods and services

• General taxes on goods and services, similarly to personalincome tax, are low in Asia compared to the rest of theworld, OECD countries and developing economiesexcluding Asia.

Treasury Guest Lecture 45 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

VAT effi ciency

• An effi ciency ratio can be calculated as VAT revenues toGDP divided by the VAT rate (in percent).

• A low effi ciency ratio suggests erosion by exemptions,reduced rates within the tax law and/or low taxpayercompliance.

Treasury Guest Lecture 46 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

VAT registration threshold

• Relatively high registration thresholds are contributing tolow VAT effi ciency in some countries.

Treasury Guest Lecture 47 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax administration costs

• Tax administration costs in Asia are relatively low, at leastin the countries for which data are available,

• ... partly because of less revenue collection

Treasury Guest Lecture 48 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax administration costs

• ... and effi cient tax collection in some countries.

Treasury Guest Lecture 49 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

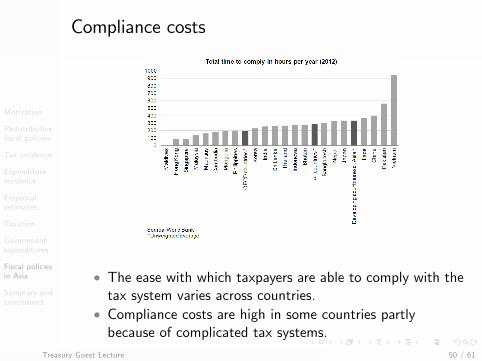

Compliance costs

• The ease with which taxpayers are able to comply with thetax system varies across countries.

• Compliance costs are high in some countries partlybecause of complicated tax systems.

Treasury Guest Lecture 50 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax reform in Asia

• The tax systems in several Asian countries arecharacterized by relatively high tax rates and narrow bases.

• There seems to be greater reliance on corporate incometaxation, which tends to be more distortionary (because ofinternationally mobile capital) than personal incometaxation and value added taxes.

• Tax reform should focus on lowering income tax rateswhile broadening the tax base.

• This would reduce the economic, compliance andadministrative costs of taxation and likely lead to increasesin tax revenue.

• A broad base, low rate tax system may be seen as fairer.

Treasury Guest Lecture 51 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Tax reform in Asia

• Further gains could be achieved in some countries byshifting the tax burden from income taxation to valueadded taxes

• ... and by broadening the value added tax base.• VAT exemptions and/or reduced tax rates are often usedto address the potential regressivity of value added taxes.

• They are costly and not well targeted to the poor.• A more effective policy would be direct cash transferpayments.

Treasury Guest Lecture 52 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Government expenditure: education and health

• Asia has made considerable progress in improvingeducation and health outcomes and toward achieving themillennium development goals (MDGs) and targets.

• Primary school enrollment and the number of studentswho start grade one and reach the last grade of primaryeducation have been rising.

• Literacy rates in Asia are high.• These achievements are likely to be contributing to ourfinding that education expenditure is reducing incomeinequality in Asia

• ... as government spending on primary education has beenfound to be progressive.

Treasury Guest Lecture 53 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Government expenditure: health

• Maternal death rates have fallen sharply with betterattendance at birth of trained health professionals andimproved antenatal care.

• Infant and child mortality rates are falling although only afew countries so far have reached the MDG target.

• The progress that has been made is likely to havebenefitted poor families.

• Infant and child mortality is closely related to householdwealth.

• But HIV/AIDS remains a problem.

Treasury Guest Lecture 54 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Social protection: employment

• Coverage remains relatively low in Asia and generally isonly available to formal sector workers.

• Few countries have income support systems for theunemployed

• ... with coverage rates in terms of the proportion ofunemployed who receive benefits being less than 10percent on average.

• Effective coverage of work related accidents and diseases islow with only a proportion of accidents being reported andcompensated.

• In the informal sector, unemployment coverage is virtuallynon-existent and working conditions and safety aretypically poor and work related diseases are widespread.

Treasury Guest Lecture 55 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Social protection: pensions

• The proportion of working age population covered bycontributory pension programs in countries with pensionsystems is low at around 20 percent.

• Few countries have social pensions to provide safety netretirement income for people who were not members of aformal scheme.

• Pension systems in Asian countries, outside the OECD, areoften quite generous.

• Replacement rates measure the value of a person’s pensionas the percentage of their earnings when working.

• They are well above OECD levels for men in Asia.

Treasury Guest Lecture 56 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Social protection: pensions

• Replacement rates are high partly because nearly alldefined-benefit schemes are based on final salaries ratherthan average earnings.

• Such schemes tend to be particularly regressive.• The higher paid typically have salaries that rise morerapidly with age, while the earnings of lower paid workersgenerally remain flat or rise less fast.

• The expected amount of time that people spend inretirement can be calculated by combining information onnational pension ages and life expectancy.

• It is relatively high in Asia because of low pensioneligibility ages.

Treasury Guest Lecture 57 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Government expenditure: explaining our results

• Education and health expenditures in Asia were found toreduce income inequality

• ... while social security spending has mainly benefittedhigher income people.

• Basic education and health services seem to be fairlyuniversally available.

• Social protection spending has been restricted to aminority already likely to be better off.

Treasury Guest Lecture 58 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Summary and conclusions: international evidence

• Most tax systems tend to show a mildly progressiveincidence impact.

• But overall taxes have not been an effective means ofredistributing income

• . . . partly because of large excess burdens or economiclosses associated with highly progressive tax systems.

• More effective redistributional policies can be achievedwith government expenditure.

• But the effective targeting can be diffi cult to design andimplement.

• Cash and in-kind transfers are particularly effective unlessthere are serious targeting problems.

• Spending programs in the social sectors are moreprogressive, the more is spent in relative and absoluteterms on the goods and services used by the poor.

Treasury Guest Lecture 59 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Summary and conclusions: findings for Asia

• Our empirical investigation confirms international resultsfor Asia.

• Government expenditure has a larger impact on incomedistribution than taxes.

• Education and health spending reduce income inequality inAsia and in other countries.

• But social protection expenditure in Asia appears toincrease income inequality, whereas it reduces it in the restof the world.

• Also adversely affecting the distribution of income in Asiancountries is government expenditure on housing.

Treasury Guest Lecture 60 / 61

Motivation

Redistributivefiscal policies

Tax incidence

Expenditureincidence

Empiricalestimates

Taxation

Governmentexpenditures

Fiscal policiesin Asia

Summary andconclusions

Summary and conclusions: findings for Asia

• For taxation, policies in Asia have a less distinctivedifferential distributive impact.

• Personal income taxes may be more progressive in Asiathan in the rest of the world, possibly because of a largernumber of people not paying income tax.

• Corporate income taxes may be less progressive possiblybecause of larger tax incentives, exemptions andconcessions for Asian firms.

• Overall, we are unable to conclude in any reliable mannerthat taxes are effective in redistributing income.

• At best, they may have a small impact both in Asia andthe rest of the world.

Treasury Guest Lecture 61 / 61