Government Financial Management World - ICGFM | · 3 ICGFM’s Three-Year Training Program 4 Miami...

12

2 2004 Miami Conference in Review 3 ICGFM’s Three-Year Training Program 4 Miami Sights & Scenes 5 ICGFM Membership Application 6 Millennium Challenge Corporation 9 PSC Update 11 Government Financial Management World ICGFM The International Consortium on Governmental Financial Management June 2004 • Vol. 13 No. 1 In This Issue T he annual conference was very successful with several interesting observations. 1. The focus for many countries has evolved to performance reporting reflecting inputs and outputs. Financial and compliance reporting has not been replaced but an increasing number of countries are report- ing on performance. 2. A topic closely tied to the performance reporting is the emphasis on moving from cash basis accounting to accrual, or at least, modified accrual accounting. Several countries are interested in learning how others have implemented this change. Moving to accrual will make performance reporting easier since cost information will be more accessible. 3. While there was considerable discussion about the problem of corruption, it is clear that there are tools available to assist countries in dealing with corrupt prac- tices. To provide some information about this issue, the ICGFM will undertake a survey dealing with Anti-Corruption. The survey will develop information about the facets of corruption; document the percep- tion of finance managers from around the world; analyze and report on the findings and suggest practicable recommendations. The timeline on this project is to have a final report available for the annual conference in 2005. 4. While each country thinks that the issues they have are unique to them, the discus- sion suggests that the problems are simi- lar worldwide. The networking and inter- action of the conference participants is one of the primary benefits of attending our conference. I hope that each of the atten- dees took something away from the meet- ing that was immediately useful to their job. I know that I was able to use the per- formance reporting information as well as the cash versus accrual discussion. I look forward to the information available from the conference next year. The Executive Committee of the ICGFM recommended that there should be a search for a part time Executive Director to handle the administrative aspects of the association. Lin Weeks has agreed to accept the position on an interim basis until a suitable candidate can be found. The Committee also agreed to develop a Strategic Plan for the association. This plan would then be submitted to the sponsoring organizations to seek financial support for the continued operation of the association. This plan is expected to be com- pleted by September 1st and given to the various organizations hoping for responses by the end of the year. The hope is that fund- ing can be obtained from the organizations to provide for some permanent part-time staff. While the volunteer members have provided significant support for many years, the future of ICGFM requires more attention than the past and some staff is necessary. As the strategic plan is developed we will pro- vide for comments from the members. I look forward to working with each of you to maximize the contribution that ICGFM can make for international financial management by governments throughout the world. The President’s Message ICGFM President Relmond Van Daniker

Transcript of Government Financial Management World - ICGFM | · 3 ICGFM’s Three-Year Training Program 4 Miami...

2

2004 MiamiConference in Review

3

ICGFM’s Three-YearTraining Program

4

Miami Sights &Scenes

5

ICGFM MembershipApplication

6

Millennium ChallengeCorporation

9

PSC Update 11

Government Financial Management World

ICGFM The International Consortium on Governmental Financial Management June 2004 • Vol. 13 No. 1

In This Issue

The annual conference was very successful with several interestingobservations.

1. The focus for many countries has evolvedto performance reporting reflecting inputsand outputs. Financial and compliancereporting has not been replaced but anincreasing number of countries are report-ing on performance.

2. A topic closely tied to the performancereporting is the emphasis on moving fromcash basis accounting to accrual, or atleast, modified accrual accounting. Severalcountries are interested in learning howothers have implemented this change.Moving to accrual will make performancereporting easier since cost informationwill be more accessible.

3. While there was considerable discussionabout the problem of corruption, it is clearthat there are tools available to assistcountries in dealing with corrupt prac-tices. To provide some information aboutthis issue, the ICGFM will undertake asurvey dealing with Anti-Corruption. Thesurvey will develop information about thefacets of corruption; document the percep-tion of finance managers from around the

world; analyze and report on the findingsand suggest practicable recommendations.The timeline on this project is to have afinal report available for the annual conference in 2005.

4. While each country thinks that the issuesthey have are unique to them, the discus-sion suggests that the problems are simi-lar worldwide. The networking and inter-action of the conference participants is oneof the primary benefits of attending ourconference. I hope that each of the atten-dees took something away from the meet-ing that was immediately useful to theirjob. I know that I was able to use the per-formance reporting information as well asthe cash versus accrual discussion. I lookforward to the information available fromthe conference next year.The Executive Committee of the ICGFM

recommended that there should be a searchfor a part time Executive Director to handlethe administrative aspects of the association.Lin Weeks has agreed to accept the positionon an interim basis until a suitable candidatecan be found. The Committee also agreed todevelop a Strategic Plan for the association.This plan would then be submitted to thesponsoring organizations to seek financialsupport for the continued operation of theassociation. This plan is expected to be com-pleted by September 1st and given to thevarious organizations hoping for responsesby the end of the year. The hope is that fund-ing can be obtained from the organizationsto provide for some permanent part-timestaff. While the volunteer members haveprovided significant support for many years,the future of ICGFM requires more attentionthan the past and some staff is necessary. Asthe strategic plan is developed we will pro-vide for comments from the members.

I look forward to working with each ofyou to maximize the contribution thatICGFM can make for international financialmanagement by governments throughoutthe world.

The President’s Message

ICGFM President Relmond Van Daniker

2

Government Financial Management World

International Consortium on Governmental FinancialManagement: 2004 Conference and Training

During the last week in April, pub-lic and private sector representa-tives from around the world gath-

ered in Miami, Florida to discuss strate-gies for “Promoting Development byEradicating Corruption, EnhancingSecurity, Improving Transparency andStrengthening Accountability.” Duringthe conference and in the training pro-gram, leaders in governmental financialmanagement shared their experiencesand expertise, responded to the partici-pants’ questions, and discussed strategiesto promote and strengthen good gover-nance. The delegates from Argentina,Barbados, Bolivia, Bosnia-Herzegovina,Cameroon, Canada, Colombia, CostaRica, Dominican Republic, El Salvador,Guatemala, Haiti, Honduras, Hungary,India, Macedonia, Mexico, Mongolia,New Zealand, Nicaragua, Pakistan,Paraguay, Peru, Philippines, SlovakRepublic, St. Kitts, Tanzania, Trinidadand Tobago, Uganda, United Kingdom,and the United States also enjoyed infor-mal opportunities to exchange ideas withtheir colleagues. The presentations can beviewed by downloading pertinent filesfrom the www.icgfm.org website.

18th Conference on NewDevelopments in GovernmentalFinancial Management

ICGFM President, Dr. Relmond VanDaniker’s opening remarks highlightedthe continuing attention directed towardcombating fraud and corruption and therole governmental financial managersplay in promoting transparency andenhancing good governance. Speakers,representing all disciplines within thefinancial management arena, reflectedthis theme in the presentations through-out the three-day conference.

During the conference, presentersfrom several national audit offices exam-ined a variety of accountability and

transparency issues. Dr. Paul Posner,from the U.S. General Accounting Office(USGAO), spoke about transparency inthe budget process. Dr. Arpad Kovacs,President of the Hungarian State AuditOffice, focussed attention on governmentcontracting. Dr. Generao Matute,Comptroller General of Peru and chair ofthe International Organization ofSupreme Audit Institution’s MoneyLaundering Task force, opened an after-noon session exploring approaches to“Stopping Money Laundering,Combating Corruption” that included apanel presentation moderated byUSGAO Director, Ms. Davi D’Agostino.In another session, Pakistan’s DeputyAuditor General, Mr. MuhammadMohsin Kahn, discussed anti-corruptionstrategies in his country, and keynotespeeches delivered by Dr. NijemounMama, Auditor General of Cameroon,and Ms. Jacquie Williams-Bridgers of theUSGAO, delved into evolving strategiesbeing implemented by their offices.

Other speakers directed attention toinitiatives undertaken by developmentand finance institutions and non-govern-mental organizations. Monday’s keynotespeaker, Mr. Stephen Zimmerman, repre-senting the Inter-American DevelopmentBank, highlighted several social andinstitutional reform projects. In openingprograms on the second day, Mr. FredShieck, Deputy Administrator of the U.S.Agency for International Developmentspoke of links between USAID projectsand poverty reduction and democraticreforms. Later in Tuesday’s program, Mr.Andy Wynne, of the Association ofChartered Certified Accountants in theUnited Kingdom, described projects andnew approaches associated withTransparency International and theUnited Nations Development Program.In another session, Mr. Albert Hrabak,from International Business andTechnical Consultants, Inc., describedevolving best practices in poverty-reduc-tion programs. Mr. David Nummy pre-sented details about the new MillenniumChallenge Corporation and its strategy toprovide assistance to countries that rulejustly, invest in their people and encour-age economic freedom.

Tuesday afternoon sessions examinedseveral specific programs in Central andSouth America. Ms. Luz Marleny OspinaR_a presented an internal control modelbeing introduced in Colombia, and Mr.Miguel Garcia-Gosalvez discussed recentexperiences introducing a control selfassessment model in El Salvador, Mexico,and Colombia. These presentations werefollowed by a panel discussion moderat-ed by Mr. Patrico Maldonado from

Casals and Associates’ America’sAccountability/Anti-corruption Project.The panelists explored integrating finan-cial management systems at the munici-pal level in Central America. Mr. JoseAntonio Perez described the work doneby the Federation of Municipalities of theCentral American Isthmus (FEMICA) topromote integrated financial manage-ment systems in the region, and Mr. JuanElvir Martel described his experiencesintroducing an integrated financial man-agement system in Santa Rosa de Copan,Honduras.

Standards, technology and developingtrends were central themes onWednesday. Mr. Richard Chambers, theacting President of the Institute ofInternal Auditors, discussed the role ofinternal auditors and the newly revised“International Standards for theProfessional Practice of InternalAuditing.” Mr. John Radford, Presidentof the National Association of StateAuditors, Comptrollers, and Treasurersin the United States, moderated the dis-cussion on implementing accountingstandards that included presentations byMr. Lusvsan-Ochir Dondog, President ofMongolia’s Institute of Certified PublicAccountants and Mr. Gert VanderLindefrom The World Bank. Mr. Luvsan-OchirDondog later joined Mr. Luc Ladouceur,Director of the Guyana EconomicManagement Program, to report on pro-jects using technology to measure perfor-mance, improve technology, andstrengthen accountability in a sessionchaired by FreeBalance’s President, Mr.Bruce Lazenby. One of the concludingpresentations by Dr. Van Daniker and Mr.Dick Willett, from Grant Thornton,encouraged delegates to participate in anICGFM sponsored study to documentefforts to fight corruption and enhancetransparency.

For the first time at the Miami confer-ence, the program included a luncheonspeaker. On Tuesday, former U.S.Ambassador Sally Shelton-Colby sharedher observations about strategies toinvolve citizens in building cooperativeinternational partnerships to promote economic development.

In comments about the conference,attendees remarked that they also bene-fited from informal discussions with col-leagues. During breaks, at lunches andduring the banquet hosted by Casals andAssociates delegates could be seenengaging in lively and animated debatesand discussions.

2004

Miami

Conference

in Review

3

Government Financial Management World

Upcoming Events

September 1, 2004

DC Forum Luncheon

October 6, 2004

DC Forum Luncheon

November 3, 2004

DC Forum Luncheon

December 1, 2004

DC Forum Luncheon

Contact Tanya Grayson [email protected] for information about the DCForum Luncheons.

Feb. 7–8, 2005

AGA’s Third Annual NationalLeadership Conference,Washington, D.C.Contact: Ada Phillips [email protected]: www.agacgfm.org/nlc Phone: 800.AGA.7211, ext. 204Fax: 703.548.9367

May 2005 (date to come)

ICGFM’s 19th Conference inGovernmental FinancialManagement, Miami, FL.Watch the website atwww.icgfm.org for updates or e-mail the ICGFM at [email protected]

July 10-13, 2005

AGA’s 54th Annual ProfessionalDevelopment Conference &Exposition, Orlando, FL.Contact: Ada Phillips [email protected]: www.agacgfm.org/nlc Phone: 800.AGA.7211, ext. 204Fax: 703.548.9367

Editor’s Note: If you have implemented a policy or proce-dure that you believe would bebeneficial to others, please writeit down and send it by email tothe Publications Editor, Dr. Jesse

Building a Strong FinancialManagement Framework: Puttingthe Pieces Together—Part 2 in theICGFM’s Three-Year TrainingProgram

On April 22-23, 100 participants from29 countries remained in Miami toparticipate in the second part of an

innovative 3-year training program. Thetraining last year highlighted budgetingand accounting; participants in this year’straining learned more about tools, tech-niques and best practices in buildingfinancial management systems. The thirdsession, to be offered next year, will directattention to auditing and accountability.

The ICGFM and the Graduate School,USDA’s Government Audit TrainingInstitute co-sponsor the training. In hisopening remarks, Mr. Peter Aliferis,USDA’s Dean of Curriculum forGovernment Auditing, Accounting,Budgeting and Financial Management atthe Graduate School, encouraged partici-pants to take advantage of the training tolearn from each other as well as from theexperts leading the training. He also suggested that they share the trainingmaterials with others in their offices—inessence to take what they learn and teachothers.

Dr. Jesse Hughes, the ICGFM TrainingCoordinator, developed the training pro-gram, brought in expert lecturers andpractitioners, and guided the discussionsessions. After reviewing key points fromthe 2003 training, Dr. Hughes introducedDr. Michael Parry, Chair of InternationalManagement Consultants, Ltd. Dr. Parryset out the basis for subsequent discus-sions as he spoke about “Establishing aConceptual Foundation: WhyGovernments Need Integrated FinancialManagement Systems.” In later sessions,Mr. Scott Vickland intro-duced a case study fromBosnia-Herzegovina tohighlight issues in“Strengthening FinancialManagement throughAccounting Reform.” Mr.Toni Dimovski (Budget)and Mr. Mende Micevski(Treasury) presentedadditional applicationexperiences from theMinistry of Finance inMacedonia. Mr. LionelVareille, described theFrench experience inmoving to an accrual-based governmentaccounting approach.

During three discus-sion group sessions, par-ticipants exchanged ideas

and experiences as they responded toquestions related to the formal presenta-tions. The language-based “breakout”groups of 10-40 persons promoted freeflowing discussions. A facilitator was des-ignated for each breakout group, and atthe conclusion of their discussions a“reporter” shared the group’s thoughtsand conclusions with the entire assembly.Facilitators included: Mr. Miguel Luiña(Bolivia), Ms. Lorena Segura de Aguilar(Honduras), Mr. Hugh Stephenson(Nicaragua), Ms. Carmela S. Perez(Philippines), and Ms. Blandina Nyoni(Tanzania).

Participants were extremely enthusias-tic about the discussion group sessionsand the translated training materials pro-vided in English, Spanish, and French.They expressed great interest in nextyear’s concluding session on auditing andaccountability. If regional groups are inter-ested in providing training on govern-mental financial management issues,speakers can be arranged by contactingICGFM at [email protected]. ■

Interim Executive Director

Mrs. Linda L. Weeks has beennamed as the interim ExecutiveDirector for the ICGFM to man-

age the Consortium’s day-to-day opera-tions while the Executive Committeeworks to identify an individual to assumethis role on a permanent basis. She will beworking part-time in space provided bythe National Association of State Auditors,Comptrollers and Treasurers, at 444 NorthCapitol Street, NW – Suite 234,Washington, DC 20001, USA. Lin may bereached at ++202-624-5651, or via email [email protected] (please note, ICGFMmust be entered in upper case letters).

The National Association of State Budget Officers is one of theICGFM’s newest organizational members. In Miami, ScottPattison, the NASBO’s Executive Director, introduced Dr. Kovacs,President of the Hungarian State Audit Office.

4

Government Financial Management World

Conference delegates enjoyed opportunities to informallyexchange information and ideas during the coffee breaks.Pictured here, Alberta Ellison, Program Manager for the U.S.General Accounting Office, chats with Mohammed Mohsin Khan,Deputy Auditor General of Pakistan.

Casals and Associates, an ICGFM Sustaining Member, supportedthe Miami conference in many ways. Prior to the conference Ms.Sylvia Rodriguez, Casals’ Governance Programs Manager, direct-ed conference registration for the Spanish speaking delegations.During the conference Ms. Mariela Lanzas, an associate withCasals, staffed the registration desk and assisted delegates andspeakers. Mr. Patrico Maldonado, Director of Casals andAssociates’ America’s Accountability/Anti-corruption Project is pictured above introducing panelists for the session he moderated.

Ms. Beatriz Casals, pictured above,introducing the special luncheonspeaker also hosted Tuesdayevening’s banquet.

In the two-day training program presenters shared their experi-ences introducing integrated financial management systems andparticipants also had opportunities to meet in small groups toshare their own experiences. Pictured above, left-right,ToniDimovski, from the Budget Office in the Ministry of Finance inMacedonia, shares his observations from a budgeting perspec-tive. Sitting are Dr. Jesse Hughes, ICGFM Training Coordinator,and Mende Micevski, from the Treasury in the Ministry ofFinance in Macedonia.

The discussion group pictured here included representativesfrom Argentina, Bolivia, Columbia, the Dominican Republic and Peru. Miguel Luin´a, at the far left facilitated this group’sconversations.

Miami Sights& Scenes

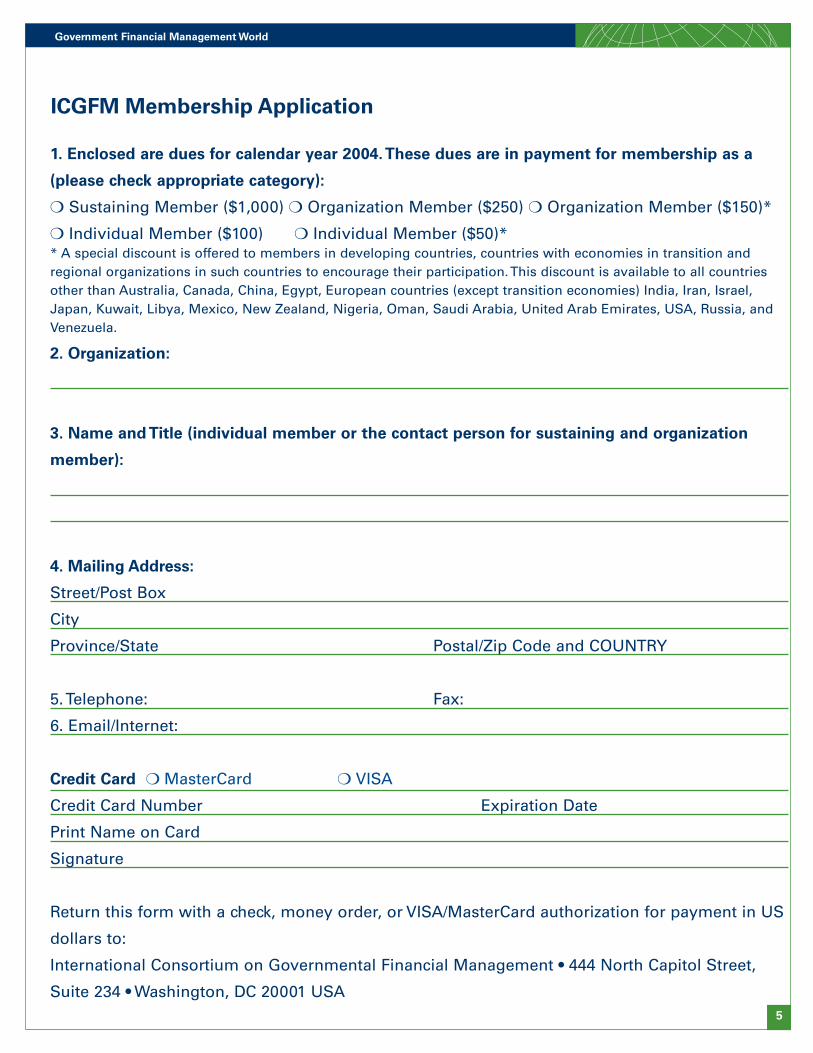

1. Enclosed are dues for calendar year 2004.These dues are in payment for membership as a

(please check appropriate category):

❍ Sustaining Member ($1,000) ❍ Organization Member ($250) ❍ Organization Member ($150)*

❍ Individual Member ($100) ❍ Individual Member ($50)** A special discount is offered to members in developing countries, countries with economies in transition andregional organizations in such countries to encourage their participation. This discount is available to all countriesother than Australia, Canada, China, Egypt, European countries (except transition economies) India, Iran, Israel,Japan, Kuwait, Libya, Mexico, New Zealand, Nigeria, Oman, Saudi Arabia, United Arab Emirates, USA, Russia, andVenezuela.

2. Organization:

3. Name and Title (individual member or the contact person for sustaining and organization

member):

4. Mailing Address:

Street/Post Box

City

Province/State Postal/Zip Code and COUNTRY

5. Telephone: Fax:

6. Email/Internet:

Credit Card ❍ MasterCard ❍ VISA

Credit Card Number Expiration Date

Print Name on Card

Signature

Return this form with a check, money order, or VISA/MasterCard authorization for payment in US

dollars to:

International Consortium on Governmental Financial Management • 444 North Capitol Street,

Suite 234 • Washington, DC 20001 USA5

Government Financial Management World

ICGFM Membership Application

Professional development was a majortopic discussed at the April 19, 2004,Board of Directors’ meeting, and the

Board agreed to explore options for expand-ing ICGFM-sponsored training.

The ICGFM and the Graduate School,USDA training programs have been wellreceived and may be expanded. Participantswere enthusiastic about 2003 program thatexamined issues in budgeting and account-ing. The training received very positive feed-back, and 100 persons registered for the 2004training exploring challenges in establishingfinancial management systems. TheGraduate School, USDA’s GovernmentAudit Training Institute (GATI) has agreedto continue its partnership with the ICGFMand co-sponsor a third training program inconjunction with the 2005 Miami conference.This session will direct attention to auditingand accountability. At the Board meeting,GATI agreed to discuss additional futureopportunities to partner with the ICGFM toprovide additional financial managementtraining programs.

During the Board meeting, Directors alsodiscussed the possibility of co-sponsoringtraining or conferences with other organiza-tions. Several Directors suggested cooperat-ing with IFAC in presenting programs inconjunction with meetings of IFAC’s PublicSector Committee, and Dr. Jesse Hughes andMrs. Lin Weeks are pursuing the possibilityof working with colleagues in India to deliv-er a program there in November.

If you have suggestions or ideas aboutfuture professional development programs,please send your comments to Dr. Hughesand Mrs. Weeks at the new email [email protected] (note: ICGFM must be inupper case letters).

A Special Note of

Appreciation

Throughout the year the NationalAssociation of State Auditors,Comptrollers, and Treasurers provides

administrative support to the InternationalConsortium on Governmental FinancialManagement. They played a critical part inassisting ICGFM in preparing for and deliv-ering the 18th International Conference.Special appreciation goes to Ms. CorneliaChebinou, Ms. Tanya Grayson, Ms. KathleenHoward, and Ms. Glenda Johnson for theirexemplary contributions to the conference.

Millennium Challenge

CorporationNotice of Report on the Selection of Eligible

Countries for FY 2004SUMMARY: Section 608(d) of the

Millennium Challenge Act of 2003, Pub. L.108-199 (Division D) requires theMillennium Challenge Corporation to pub-lish a report that lists the countries deter-mined by the Board of Directors of theCorporation to be eligible for assistance forFiscal Year 2004. The report is set forthbelow.

Report: The Act authorizes the provisionof assistance to countries that enter intocompacts with the United States to supportpolicies and programs that advance theprospects of such countries to achieve lastingeconomic growth and poverty reduction.The Act requires the Millennium ChallengeCorporation (MCC) to take a number ofsteps to determine the countries that, basedon their demonstrated commitment to justand democratic governance, economic free-dom and investing in their people, will beeligible to receive Millennium ChallengeAccount (MCA) assistance during a fiscalyear. These steps include the submission ofreports to appropriate congressional commit-tees and the publication of notices in theFederal Register that identify:1. The “candidate countries” for MCA

assistance (Section 608(a) of the Act);2. The eligibility criteria and methodology

that the MCC Board of Directors (theBoard) will use to select “eligible coun-tries” from among the “candidate coun-tries” (Section 608(b) of the Act); and

3. The countries determined by the Board tobe “eligible countries” for a fiscal year, thecountries on the list of eligible countrieswith which the Board will seek to enterinto MCA “Compacts” and a justificationfor such decisions (Section 608(d) of theAct).This is the third of the above-described

reports. It identifies the countries deter-mined by the Board to be eligible for MCAassistance in FY 2004 (other than underSection 616 of the Act) and those that theBoard will seek to enter into MCACompacts, and the justification for such decisions.

Eligible CountriesThe MCC Board of Directors met on May

6, 2004, to select countries that will be eligi-ble for FY 2004 MCA assistance (other thanunder Section 616 of the Act) and will beinvited to submit proposals for such assis-tance. The Board determined the followingcountries eligible for FY 2004 assistance:Armenia, Benin, Bolivia, Cape Verde,Georgia, Ghana, Honduras, Lesotho,Madagascar, Mali, Mongolia, Mozambique,Nicaragua, Senegal, Sri Lanka, and Vanuatu.

6

ICGFM to Explore

Expanding Training

Options

Government Financial Management World

In our November 2003 NewsletterI gave you some facts, figuresand things to think about related

to ICGFM membership. Many ofyou have been talking to othersabout the Consortium, and I ampleased to report that we are receiv-ing inquiries from organizationsand individuals interested in joiningus in programs to enhance govern-mental financial management prac-tices at all levels. I was delightedthat my end-of-the-year report tothe Board of Directors reflected ourexpanding membership, and I hopethis trend will continue into 2004.

In March, we mailed out theinvoices for the 2004 dues, and sev-eral individuals and organizationsbecame new members during theMiami conference. If you are amember but you have not receivedyour 2004 invoice, please let meknow. If you have received yourinvoice, but have not sent in yourdues – please send your payment assoon as possible. If you havealready sent in your 2004 dues –THANK YOU!

I can be reached at the ICGFMoffice. The email address [email protected], the fax is ++202-624-5473.

In the November 2004 NewsletterI will once again list our members –and I hope that you and your orga-nization will be included.

A Brief Note from

the Membership

Committee from

Lin Weeks, Chair

MCC, continued on next page

7

Government Financial Management World

In accordance with the Act and with MCC’s “Criteria andMethodology for Determining the Eligibility of CandidateCountries for Millennium Challenge Account Assistance in FY2004," submitted to the Congress on March 2, 2004, selection wasbased on a country’s overall performance in relation to threebroad policy categories: Ruling Justly, Encouraging EconomicFreedom, and Investing in People. The Board relied on sixteenpublicly available indicators to assess policy performance as thepredominant basis for determining which countries would beeligible for assistance. Where appropriate, the Board also consid-ered other data and quantitative information as well as qualita-tive information to determine whether a country performed sat-isfactorily in relation to its peers in a given category, includingperformance with respect to investing in their people, particular-ly women and children, economic policies that promote privatesector growth, the sustainable management of natural resources,and human and civil rights, including the rights of people withdisabilities. The Board also considered whether any adjustmentsshould be made for data gaps, lags, trends, or strengths or weak-nesses in particular indicators.

The following countries were selected because (i) they per-formed above the median in relation to their peers on at leasthalf of the indicators in each of the three policy categories, (ii)they performed above the median on corruption, (iii) they didnot perform substantially below average on any indicator, and(iv) the supplemental information available to the Board sup-ported their selection: Armenia, Benin, Ghana, Honduras,Madagascar, Mali, Mongolia, Nicaragua, Senegal, and Vanuatu.

Three of the countries performed above the median in rela-tion to their peers on at least half of the indicators in each of thethree policy categories and above the median on corruption,though they were substantially below average on one indicator:Cape Verde, Lesotho and Sri Lanka. The following is some of theinformation that was available to the Board in making its eligi-bility determinations that suggested that each of these countrieswas taking measures to address these shortcomings:

Cape Verde—Although Cape Verde received a low score onthe ``Trade Policy’’ indicator, its score did not capture improve-ments resulting from a recent shift to a Value Added Tax thatreduced Cape Verde’s reliance on revenue from import tariffs.Cape Verde is also making good progress in its efforts towardWorld Trade Organization accession.

Lesotho—Although Lesotho scores substantially below themedian on the ``Days to Start a Business” indicator, it recentlyestablished a one-stop shop to facilitate new business formation.It also performs very well overall in the “Economic Freedom”category and the other categories. Lesotho also performs well onother measures of starting a business; for example, it costs 68%of per capita income to start a business in Lesotho, versus a sub-Saharan Africa average of 256%, and Lesotho’s minimum capitalrequirement for new businesses is only a tenth of the sub-Saharan average.

Sri Lanka—Although Sri Lanka’s score on the “Fiscal Policy”indicator falls substantially below the median, the deficit hasdeclined each year since 2001, reflecting a positive trend over thepast several years. Additionally, Sri Lanka’s non-concessionalborrowing in 2004 is expected to be less than half of the 2002level.

Finally, three countries were determined by the Board to beeligible despite the fact that they (i) were not above the medianin relation to their peers on at least half of the indicators in oneof the three policy categories and/or (ii) were at or below themedian on the corruption indicator. The Board made a positiveeligibility determination on these countries in light of thenotable actions taken by their governments and positive trends

contained in supplemental information available to the Board.The following is some of the information that was available tothe Board that suggested the policy performance of each of thesecountries was better than was reflected in the indicator data:

Bolivia—Bolivia is right at the median on the “Corruption”indicator and is above the median on all of the other indicatorsin the “Ruling Justly” category; however, its current score on the“Corruption” indicator does not reflect changes made sincePresident Mesa assumed power in October 2003. For instance,President Mesa has created a cabinet-level position to coordinateanti-corruption efforts as well as establishing an office to pro-vide for the swift investigation of police corruption.

Georgia—Although Georgia is at or below the median onmore than half of the “Ruling Justly” categories, including the“Corruption” indicator, this data does not capture the substan-tial progress made by the newly elected Georgian government inonly three months time. The Government of Georgia has, amongother things, created an anti-corruption bureau, a new bureau toinvestigate and prosecute corruption cases, a single treasuryaccount for all government revenue to ensure transparency andaccountability, and has started revamping procurement legisla-tion to ensure an open and competitive process.

Mozambique—The trends and supplemental information thatfilled in data lags for Mozambique’s “Investing in People” indi-cators demonstrated Mozambique’s progress and achievementthat were not reflected in the indicators. Primary education com-pletion rates, for example, have been steadily rising inMozambique, and this positive trend is backed by the fact thatenrollment rates have increased to over 90% in 2000, from 60%in 1995. Girls’ primary school enrollment rates increased by 60%between 1995 and 2000. Although Mozambique scores above themedian in four of the six “Ruling Justly” categories, it fallsbelow the median on the World Bank’s anti-corruption indicator.However, certain indications suggest that this data is lagged andthat Mozambique is making significant progress to fight corrup-tion. Mozambique has passed new legislation to fight corruptionand has created a special Anti-Corruption Unit that is conduct-ing numerous investigations. These recent improvements on cor-ruption are in fact reflected in another source—TransparencyInternational’s anti-corruption index--a more up-to-date indica-tor, in which it scored well above the median (74th percentile).

MCC will closely monitor the continued progress of thesecountries in these and other policy areas between the time ofthis report and the presentation to the Board of any proposedMCA Compact, and anticipates continued performance andimprovement in these areas will be part of the Compacts themselves.

Selection for Compact NegotiationThe Board also authorized the MCC to seek to negotiate an

MCA Compact, as described in Section 609 of the Act, with eachof the eligible countries identified above that develops a propos-al that justifies beginning such negotiations. MCC will initiatethe process by inviting eligible countries to submit program pro-posals to MCC. MCC has posted guidance on the MCC Web site(www.mcc.gov) regarding the development and submission ofMCA program proposals, and will soon begin outreach visits toeach of the eligible countries where this and related informationon developing their proposals for MCA assistance will be dis-cussed.

Submission of a proposal is not a guarantee that MCC willfinalize a Compact with an eligible country. MCC will evaluateproposals and make funding decisions based on the potential forimpacting economic growth and other considerations. The quali-ty of the initial proposal--including how well the country hasdemonstrated the relationship between the proposed priority

MCC, continued from previous page

MCC, continued on next page

Government Financial Management World

MCC, continued from page 7

Extracts from IFAC E-Newsletter:

5. IFAC Explores Issues Pertaining to theImplementation of International Standards

The IFAC Board has requested that Peter Wong from HongKong (a former IFAC Board member) lead a project toobtain the views of individuals and various groupings of

professional accountants and other stakeholders on the extent towhich they have seen challenges and successes in the implemen-tation of International Standards on Auditing (ISAs), issued bythe IAASB, and International Financial Reporting Standards,issued by the International Accounting Standards Board.

IFAC leadership and management are in the process of con-ducting a series of focus groups and interviews with membersof regional accountancy organizations as well as with profes-sional accountants from different backgrounds (large firms,medium-sized firms, small firms, members in business, nationalaccounting and auditing standard setters), as well as regulators,users and other interested parties. Individuals who would liketo provide input should send an email to [email protected].

6. Latest International Auditing and EthicsPronouncement Available in Several Formats

The 2004 Handbook of International Auditing, Assurance, andEthics Pronouncements, featuring all pronouncements issued bythe International Auditing and Assurance Standards Board(IAASB) and the Ethics Committee through December 31, 2003,is now available in print and in a new fully searchable, interac-tive electronic format. The pronouncements in this new edition

of the handbook have been restructured by the IAASB to betterreflect the services covered by them. Additions to this year’shandbook include the new audit risk standards, assurance stan-dards, assurance framework, and an interpretation to IFAC’sCode of Ethics for Professional Accountants.

7. Compendium of International Public SectorAccounting Standards Now Available

The 2004 Handbook of International Public Sector AccountingPronouncements is available at no charge in a downloadable PDFand print format. It features International Public SectorAccounting Standards (IPSASs) 1-20, along with a glossary ofterms, summary of occasional papers and studies, and a selectedbibliography. For information about Public Sector Committee(PSC) activities, view the latest PSC Update, which is availablein English, French and Spanish.

8. IFAC Addresses Anti-Money Laundering and theRole of Accountants

Governments, regulators and the global business communityare increasingly calling on accounting practitioners to contributeto the battle against money laundering. A new IFAC paper, Anti-Money Laundering 2nd Edition, addresses the increased expec-tations of legislators and regulators with respect to the profes-sion’s role in detecting money laundering and the implementa-tion of controls and safeguards against it.

This paper and other documents mentioned above may bedownloaded at no charge from the IFAC website: www.ifac.org.

area(s) and economic growth and poverty reduction--will bea determining factor. An eligible country’s commitment andcapacity will also be a factor in determining how quickly MCCcan begin substantive discussions with a country on a Compactand will likely influence the speed with which a Compact canbe negotiated as well as the amount and timing of any MCAassistance approved by the Board.

Any MCA assistance (other than certain types of technicalassistance or assistance provided under Section 616 of the Act)will be contingent on the successful negotiation of a mutuallyagreeable Compact between the eligible country and MCC, andapproval of the Compact by the Board.Dated: May 11, 2004.Paul V. Applegarth,Chief Executive Officer, Millennium Challenge Corporation.[FR Doc. 04-10980 Filed 5-13-04; 8:45 am]

This Newsletter, as well as prior issues,

can be found at www.icgfm.org. Other

Newsletters of interest published by a cou-

ple of our sustaining members can be found

at www.agacgfm.org (Association of

Government Accountants—US) and

www.cpaaustralia.org (CPA Australia).

PSC Update 11

The PSC Update is prepared by staff after each meeting ofthe PSC with the aim of providing a timely report on theprogress of PSC projects. The views expressed in this docu-

ment may not necessarily reflect the final views of theCommittee or of individual members.

1. IntroductionThe Public Sector Committee (PSC) met in Buenos Aires,

Argentina in March 2004. This Update summarizes the majorfeatures of the meeting. Background papers for this meeting areavailable on the PSC page of the IFAC web-site. In conjunctionwith this meeting, the PSC and the Federación Argentina deConsejos Profesionales de Ciencias Económicas (FACPCE) joint-ly hosted a seminar which was attended by approximately twohundred public sector accountants from Argentina and LatinAmerica. Mr. René Ricol, President of IFAC and Dr. Ian Ball,Chief Executive of IFAC, attended part of the PSC meeting. Mr.Ricol addressed the PSC, noting the significant contribution thePSC makes to the mission of IFAC.

2. Chair and Membership of the PSCThis was the first meeting under new Chair Philippe

Adhémar, the PSC member from France, and Vice ChairMike Hathorn, the PSC member from the United Kingdom.

New members attending their first meeting were WayneCameron (Australia), Zvi Chalamish (Israel), Ryoko Shimizu(Japan) and Greg Schollum (New Zealand).

3. PSC External Review and FundingThe PSC received a report on the status of the review of its

operations. It was noted that to date 142 responses had beenreceived to the questionnaire issued by the Review Committeeand those responses indicate strong support for the PSC and itsactivities. The Review Committee is still developing its finalreport. When completed, the report will be circulated to PSCmembers for discussion at the PSC meeting in July and submit-ted to the IFAC Board.

4. PSC Consultative GroupThe PSC met with its Consultative Group and key Latin

American constituents to discuss the operations of theConsultative Group, strengthening PSC liaison with Latin

America and the PSC work program. The Consultative Grouprecommended that it continue to operate in its current form, butthat for each meeting the PSC identify the specific issues onwhich Consultative Group input is sought.

5. Work ProgramDraft papers related to the following projects were considered

by the PSC at this meeting.

Budget ReportingDr. Jesse Hughes made a presentation to the PSC on the

Research Report he was preparing and outlined his conclusionson the key research questions including: • whether establishing requirements for budget reporting was

within the mandate of the PSC; and, • if it was, issues to be addressed in developing such

requirements.Dr. Hughes noted that he had had valuable input from

Steering Committee members and others in the development ofthe Research Report but, the recommendations made in thereport were his alone. Members commended Dr. Hughes on thework completed, thanked Steering Committee members for their

contribution and agreed to provide further input to Dr. Hughesas he finalized the Research Report. The PSC agreed that theResearch Report should be finalized by Dr Hughes and madepublicly available from the PSC’s web page. The PSC also notedthat it was to be made clear that the Research Report and its rec-ommendations were those of Dr. Hughes, and not the PSC. ThePSC agreed to discuss in detail Dr. Hughes’ recommendations atthe next PSC meeting in July 2004, and at that time determinewhether to proceed to develop requirements on budget report-ing, and the nature of those requirements.

Accounting for Development Assistance Under the Cash Basis of Accounting

Mr. Ian Mackintosh, Chair of the Project Advisory Panel(PAP) and Mr. Charles Coe, consultant, were present at the meet-ing. Mr. Mackintosh advised the PSC that PAP members hadhad only limited time to consider the Key DecisionsQuestionnaire distributed in late 2003. The PSC consideredresponses to the KDQ received so far from PAP members andthe key components of an Exposure Draft (ED) identified by Mr.Coe. The PSC agreed that a draft ED reflecting issues andapproaches identified by Mr. Coe updated to reflect PSC com-ments thereon, is to be developed and provided to PAP mem-bers for comment.

That draft, together with PAP comments and any subsequentrevisions, is to be presented to the PSC for consideration at itsmeeting in July 2004.

Impairment of AssetsThe PSC undertook a preliminary review of responses to

Exposure Draft (ED) 23 Impairment of Assets. The PSC notedthat there was considerable support for the development of anInternational Public Sector Accounting Standard (IPSAS) basedon the ED, but that a significant number of respondents raisedconcerns about the definition of cash-generating assets andwhether: o property, plant and equipment carried at fair value inaccordance with IPSAS 17 Property, Plant and Equipmentshould be excluded from the scope of the proposed IPSAS; o adecline in market value should be excluded from the list of mini-mum indicators of impairment; and o it was necessary to identi-fy the depreciated replacement cost, restoration cost and serviceunits approaches to measurement of value-in-use as differentapproaches. The PSC agreed to amend the definition of cashgenerating assets and to strengthen the explanation of the PSC’sviews in the Basis for Conclusions, particularly where it wasproposed that the IPSAS differ from International AccountingStandard 36 Impairment of Asset (IAS 36). The PSC directed thata first draft IPSAS based on the proposals in ED 23 be preparedfor review at the next meeting. That review will include consid-eration of any amendments to the treatment of impairments inthe revised IAS 36 soon to be issued by the IASB, and the rela-tionship between the measurement of an impairment loss in ED23 and guidance on the measurement of fair value in IPSAS 17.

Harmonization with International Financial ReportingStandards (IFRSs) issued by the IASB

The PSC agreed to update the IPSASs based on IASs that hadbeen amended as part of the IASB’s recently completedImprovements Project, and commenced the review of the firstthree of those proposed revised IPSASs. The PSC also consid-ered a number of pervasive issues that would need to be dealtwith in any revision including: • adopting the principle of “equal authority” of all provisions

of an IPSAS and clarifying the intent of the PSC by the use ofappropriate language such as “shall” or “may”;

• inclusion of a Basis for Conclusions in all IPSASs and deletionof unnecessary definitions;

9

Government Financial Management World

PSC, continued on page 10

10

• the extent to which an IAS/IFRS should berelied on in selecting accounting policies inthe absence of an IPSAS; and o the need toupdate the Preface to International PublicSector Accounting Standards. Members agreed that it was important to

develop and make public the PSC’s policy forupdating IPSASs currently on issue and fordealing with IASs/IFRSs for which an IPSAShad not yet been issued. Members alsoagreed that it was important to identify andmake public the anticipated timing of issue ofproposed updated or new IPSASs, includedthose translated into French and Spanish.This would enable constituents to plan imple-mentation of IPSASs in an informed andorderly fashion. A strategy paper is to bedeveloped for consideration at the next PSCmeeting.

Convergence of IPSASs with GFS and ESA 95

Mr. Ian Mackintosh, Chair of WorkingGroup I of the Task Force on Harmonizationof Public Sector Accounts, provided a reportto the PSC on the February 2004 meeting ofthe Task Force. He also outlined the recom-mendations of Working Group I, whichincluded that the PSC should: • encourage or allow note disclosure of

financial information about the generalgovernment sector as defined by theGovernment Finance Statistics Manual2001 (GFSM 2001); and

• activate a project directed at developing acomprehensive report of financial perfor-mance which distinguishes between trans-actions and other economic flows asdefined in GFSM 2001. The PSC agreed to activate these projects

subject to resource availability. The PSC alsonoted that issues encompassed by the perfor-mance reporting project may be broader thanthose reflected in a decision to harmonizewith statistical reporting bases and that a sep-arate project proposal should be developedand discussed as a first step. Mr. Mackintoshnoted that the Working Group also recom-mended that the PSC require or allow: • the adoption of current values in IPSASs,

including adopting IAS 39 FinancialInstruments: Recognition andMeasurement; and

• inventories to be valued at current replace-ment cost when all other assets are valuedat fair value. The PSC noted that these rec-ommendations impacted on their IASBharmonization strategy already in progressand agreed to consider them and/or raisethem with the IASB as the harmonizationstrategy was further progressed.

6. Next PSC Meeting: New York, USA, 5 – 7 July 2004

For further information please contact:Paul Sutcliffe, PSC Technical Director ([email protected]) or Jerry Gutu, PSCTechnical Manager ([email protected]).

7. PSC MEMBERS 2004FRANCE—Philippe Adhémar (Chair),Conseiller Maître à la Cour des Comptes. UNITED KINGDOM—Mike Hathorn (ViceChair), Partner, Moore Stephens, UnitedKingdom. ARGENTINA—Carmen Giachino Palladino,Consultant InterAmerican DevelopmentBank. AUSTRALIA—Wayne Cameron, Auditor-General, State of Victoria. CANADA—Rick Neville, Vice-President andChief Financial Officer, Royal Canadian Mint. GERMANY—Norbert Vogelpoth, Partner,PwC Deutsche. ISRAEL—Zvi Chalamish, DeputyAccountant General, Israeli Ministry ofFinance. JAPAN—Ryoko Shimizu, Partner, PwCJapan. MALAYSIA—Mohd. Salleh Mahmud,Deputy Accountant-General, Malaysia. MEXICO—Javier Pérez Saavedra,Subdirector de control de Calidad, PetroleosMexicano. NETHERLANDS—Peter Bartholomeus,Director, Government Audit PolicyDepartment, Ministry of Finance. NEW ZEALAND—Greg Schollum, ChiefFinancial Officer, Greater Wellington RegionalCouncil. NORWAY—Tom Olsen, Partner, PwCNorway. SOUTH AFRICA—Terence Nombembe,Deputy Auditor-General of South Africa andCEO of the Office of the Auditor-General ofSouth Africa. UNITED STATES OF AMERICA—RonPoints, Manager, Financial Management forEast Asia and Pacific Region, World Bank.

8. PSC OBSERVERS 2004Asian Development Bank (ADB),

European Union (EU), InternationalAccounting Standards Board (IASB),International Monetary Fund (IMF),International Organisation Of Supreme AuditInstitutions—Committee on AccountingStandards (INTOSAI-CAS), Organisation ForEconomic Co-Operation And Development(OECD), United Nations/United NationsDevelopment Programme (UN/UNDP) andthe World Bank.

Government Financial Management World

PSC, continued from page 9

11

Government Financial Management World

Don’t Miss the DC

Forum—Mark Your

Calendars for this Fall

On the first Wednesday each month,the International Consortium onGovernmental Financial

Management hosts a DC Forum inWashington, DC. Attendees at the luncheonevents at The Brookings Institution enjoythe opportunity to network with colleaguesand engage in discussions with guest speak-ers. Although the DC Forum “adjourns forthe summer,” regular meetings will resumeon Wednesday, September 1, when Dr.Howard E. McCurdy, Professor of PublicAffairs and Chair of the PublicAdministration Department at AmericanUniversity, will be our speaker.

Mark your calendars now for DC Forumluncheons on:

September 1October 6November 3December 1

Email announcements with details aboutthe topic and the speaker are sent out 2-3weeks before each event. If you have notbeen receiving the email announcements,and you would like to be added to the emaillisting, please send a message to TanyaGrayson at [email protected].

If you have suggestions for topics orspeakers, please send an email to Mrs. LinWeeks at [email protected].

June DC Forum

Megan Elder, Student InternTaylor University, Indiana

WA “Bill” Broadus Jr. spoke to mem-bers of the Consortium at the DCForum on June 2, 2004 regarding

China’s economic future. “It’s a very excit-ing time in China,” Broadus said. “We mustbe proactive.”

Consortium members discussed the goalsfor China’s economy over lunch at TheBrookings Institution. Broadus led the dis-cussion and presented his efforts to installimproved financial management programsin China with funding from the World Bankand help from the Association ofGovernment Accountants (AGA).

AGA is helping the Chinese to establishan organization in China similar to AGA. Itwill provide training, internships andresources inside of China and will operateas a separate entity from AGA. The two willoperate as “sister organizations,” Broadussaid.

The organization, to be based in Beijing,has 1.8 million potential members, Broadusestimated. He speculates possible chaptersin Shanghai and Hong Kong, but the overallumbrella in Beijing must first be established.Other countries are interested in launchinga similar program, specifically Vietnam.China will be the prototype for furtherinvolvement.

Another AGA goal is establishing a full-time South East Asia training center in Honolulu, Hawaii. It will address thefinancial management needs of 11 countries.

For the endeavor to be successful,Broadus and his associates learned thecountry must have an interest, he said. Healso learned the importance of patience. “InChina, they do things very fast or they dothings very slow,” he said. Although theeffort to establish an organization similar toAGA is progressing, it is not moving as fastas had been desired.

Honorary Chairman Emeritus

Elmer B. Staats, Former Comptroller Generalof the United States

President

Relmond Van Daniker, AGA

President-Elect

Vacant

Immediate Past President

Leroy E. Bookal, World Bank

Treasurer

Peter Aliferis, Graduate School-USDA

Secretary

Dick Willett, Grant Thornton

Vice Presidents

Mathew Andrews, World BankJacquie Williams Bridgers, GAOWilliam Taylor, Inter-American DevelopmentBank

ICGFM Publications EditorJesse Hughes, Consultant

Representatives of the Sustaining Members

AGA: Relmond P. Van DanikerCasals and Associates, Inc.: Beatriz CasalsCPA Australia: David ShandGATI: Peter V. AliferisIBTCI: Al HrabakIIA & IADB: Bill TaylorNASACT: Kinney PoynterUSAID: Everett Mosley/Toby JarmanU.S. GAO: Jacquie Williams Bridgers World Bank: J. Graham Joscelyne

Representatives of Member Organizations

Cameroon State Audit Office

Hungary State Audit Office

India Comptroller and Auditor General

International Monetary Fund

Pakistan Office of the Auditor General

Representatives of Individual Members

Blandina NyoniMortimer Dittenhofer James Hamilton Jesse Hughes Virginia RobinsonLinda Weeks

Government Financial Management World

International Consortium on Governmental

Financial Management (ICGFM)

444 North Capitol Street, Suite234Washington, DC 20001 USAwww.icgfm.org • [email protected]

ph: 202 624-8461

fx: 202 624 5473

ICGFM Officers