GORO - What You Need to Know

34

Gold Resource Corp (GORO) What You Should Know July 2011 1

-

Upload

gorotruth1608 -

Category

Documents

-

view

891 -

download

1

Transcript of GORO - What You Need to Know

Gold Resource Corp (GORO)

What You Should Know

July 2011

1

2

INDEX

Gold Resource Corp (GORO)

What You Should Know

1) Insiders selling millions of shares without public disclosure

a. Only small percentage of insider sales have been disclosed

publicly

b. Insiders sold significant shares before Barron’s inquiry was public

2) Claiming that GORO is generating substantial cash AND that this cash is

funding the dividend

a. Actual cash flow has been negative every single quarter since

inception

b. Paying out private placement proceeds as dividends in Ponzi-like

scheme

3) Claiming to produce gold–equivalent ounces at “zero cost”

Calculation does not reflect royalties, G&A, construction, development,

exploration and or capital expenditures – all of which are necessary expenses

to build and sustain a mine - including these expenses results in GORO’s Q1

2011 cost per ounce exceeding $2,000 versus just the $87 they claimed

4) Claiming to have “one of the highest grade deposits in the world”

a. No one outside of Bill Reid’s family circle has verified the geology

b. Others who did their own drilling (Apex & Canyon) or were

present while GORO was doing drilling that led to production

decision (Heemskirk) have previously passed on the sites

c. Production resulting out of these mines has been far below

expectations – for example, open pit was supposed to produce 70K

ounces and only did <18K

5) Troubling corporate governance practices

a. Tightly controlled by small group

b. Acting lead independent director (Bill Conrad) is being paid richly

and selling shares

c. Failed to hire a full-time and/or mining-experienced CFO

d. Using non-major auditing firm

6) Pattern of deception on wide range of issues

a. Never ending delays and escalating costs

b. Misleading investors to expect “IRR>100%” – but every

project has a hugely negative IRR

c. Deception about mgmt’s experience levels – GORO has

everyone parroting that managers have strong experience

but they have never produced positive cash flow from any

mine in >30 years

d. Deception about danger levels in Mexico – locals won’t

bite the hand that feeds them but it may be a different

story if actual “zero cost gold” was being mined

e. Misleading statements on capitalizing of costs

f. Manufacturing a GAAP profit despite a cash loss

g. Misleading statements on shareholder dilution– in

actuality GORO has raised money with private placements

on more than 20 separate occasions and granted more

than 13MM shares to mgmt, etc

h. Deception on ownership of mining properties

7) Additional concerns and details

a. Odd circumstances concerning sales

b. Hochschild’s involvement with GORO

c. Superficial research coverage

d. Details on John Doody of Gold Stock Analyst

e. Don’t be fooled by 43-101

f. What to make of GORO’s new “acquisition”

g. Other facts that give one pause

h. What did GORO’s CEO say?

8) Applying Lessons from Bre-X

Conclusions for GORO

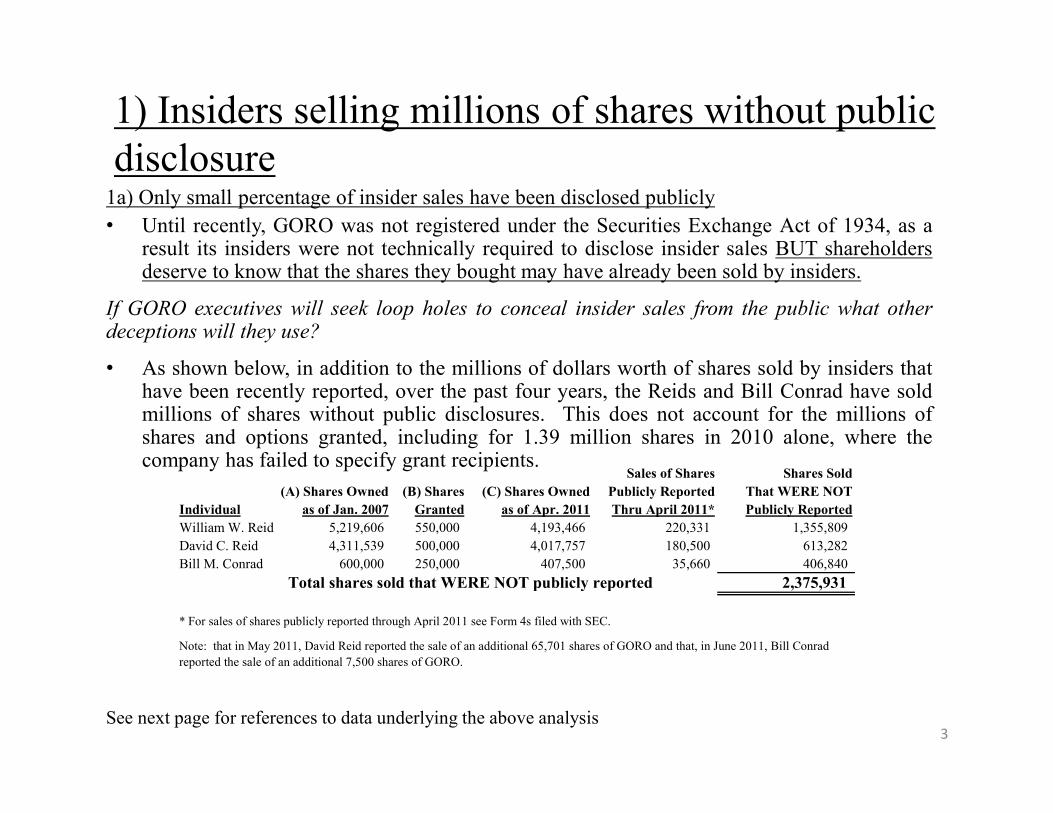

1) Insiders selling millions of shares without public

disclosure1a) Only small percentage of insider sales have been disclosed publicly

• Until recently, GORO was not registered under the Securities Exchange Act of 1934, as aresult its insiders were not technically required to disclose insider sales BUT shareholdersdeserve to know that the shares they bought may have already been sold by insiders.

If GORO executives will seek loop holes to conceal insider sales from the public what otherdeceptions will they use?

• As shown below, in addition to the millions of dollars worth of shares sold by insiders thathave been recently reported, over the past four years, the Reids and Bill Conrad have soldmillions of shares without public disclosures. This does not account for the millions ofshares and options granted, including for 1.39 million shares in 2010 alone, where thecompany has failed to specify grant recipients.

See next page for references to data underlying the above analysis3

Sales of Shares Shares Sold

(A) Shares Owned (B) Shares (C) Shares Owned Publicly Reported That WERE NOT

Individual as of Jan. 2007 Granted as of Apr. 2011 Thru April 2011* Publicly Reported

William W. Reid 5,219,606 550,000 4,193,466 220,331 1,355,809

David C. Reid 4,311,539 500,000 4,017,757 180,500 613,282

Bill M. Conrad 600,000 250,000 407,500 35,660 406,840

Total shares sold that WERE NOT publicly reported 2,375,931

* For sales of shares publicly reported through April 2011 see Form 4s filed with SEC.

Note: that in May 2011, David Reid reported the sale of an additional 65,701 shares of GORO and that, in June 2011, Bill Conrad

reported the sale of an additional 7,500 shares of GORO.

1) Insiders selling millions of shares without public

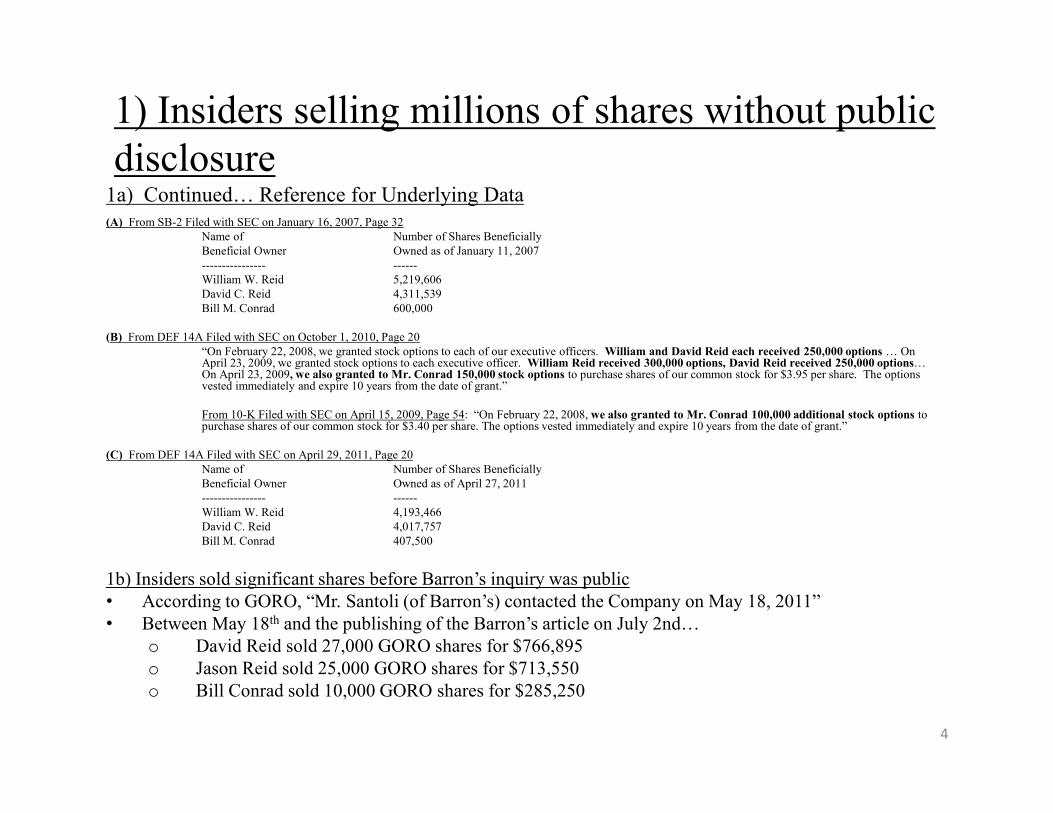

disclosure1a) Continued… Reference for Underlying Data(A) From SB-2 Filed with SEC on January 16, 2007, Page 32

Name of Number of Shares Beneficially

Beneficial Owner Owned as of January 11, 2007

---------------- ------

William W. Reid 5,219,606

David C. Reid 4,311,539

Bill M. Conrad 600,000

(B) From DEF 14A Filed with SEC on October 1, 2010, Page 20

“On February 22, 2008, we granted stock options to each of our executive officers. William and David Reid each received 250,000 options … On April 23, 2009, we granted stock options to each executive officer. William Reid received 300,000 options, David Reid received 250,000 options… On April 23, 2009, we also granted to Mr. Conrad 150,000 stock options to purchase shares of our common stock for $3.95 per share. The options vested immediately and expire 10 years from the date of grant.”

From 10-K Filed with SEC on April 15, 2009, Page 54: “On February 22, 2008, we also granted to Mr. Conrad 100,000 additional stock options to purchase shares of our common stock for $3.40 per share. The options vested immediately and expire 10 years from the date of grant.”

(C) From DEF 14A Filed with SEC on April 29, 2011, Page 20

Name of Number of Shares Beneficially

Beneficial Owner Owned as of April 27, 2011

---------------- ------

William W. Reid 4,193,466

David C. Reid 4,017,757

Bill M. Conrad 407,500

1b) Insiders sold significant shares before Barron’s inquiry was public

• According to GORO, “Mr. Santoli (of Barron’s) contacted the Company on May 18, 2011”

• Between May 18th and the publishing of the Barron’s article on July 2nd…

o David Reid sold 27,000 GORO shares for $766,895

o Jason Reid sold 25,000 GORO shares for $713,550

o Bill Conrad sold 10,000 GORO shares for $285,250

4

2) Claiming that GORO is generating substantial cash

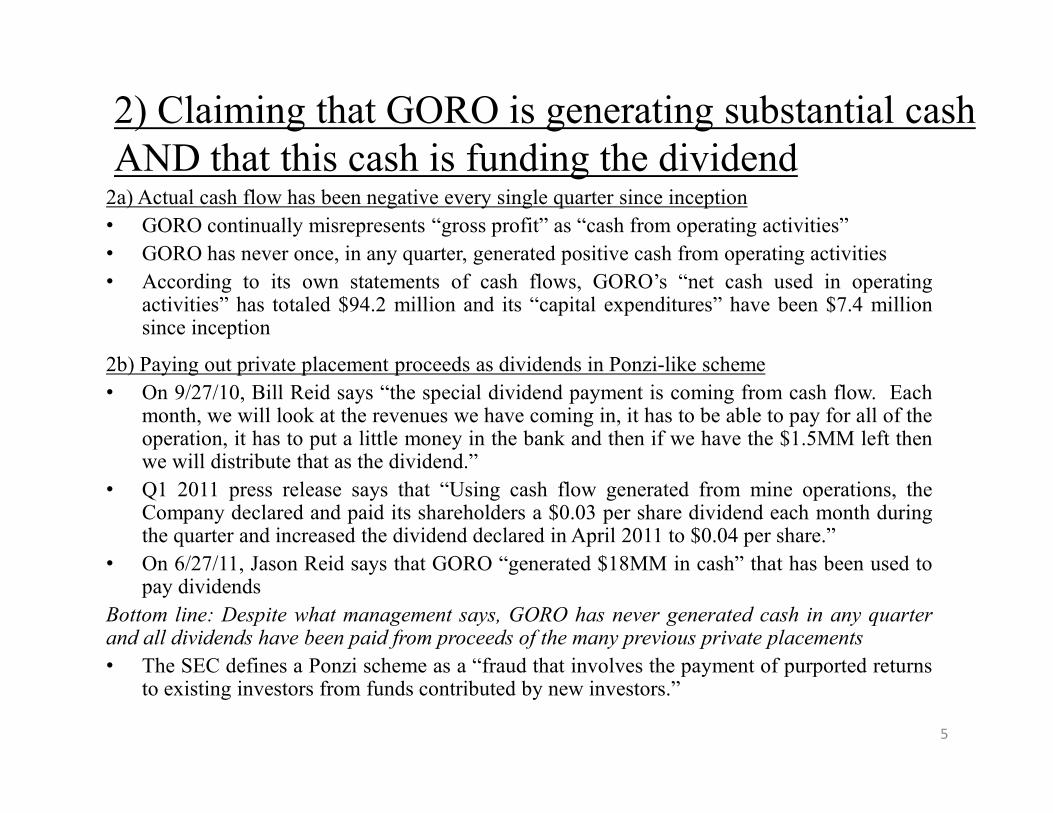

AND that this cash is funding the dividend2a) Actual cash flow has been negative every single quarter since inception

• GORO continually misrepresents “gross profit” as “cash from operating activities”

• GORO has never once, in any quarter, generated positive cash from operating activities

• According to its own statements of cash flows, GORO’s “net cash used in operatingactivities” has totaled $94.2 million and its “capital expenditures” have been $7.4 millionsince inception

2b) Paying out private placement proceeds as dividends in Ponzi-like scheme

• On 9/27/10, Bill Reid says “the special dividend payment is coming from cash flow. Eachmonth, we will look at the revenues we have coming in, it has to be able to pay for all of theoperation, it has to put a little money in the bank and then if we have the $1.5MM left thenwe will distribute that as the dividend.”

• Q1 2011 press release says that “Using cash flow generated from mine operations, theCompany declared and paid its shareholders a $0.03 per share dividend each month duringthe quarter and increased the dividend declared in April 2011 to $0.04 per share.”

• On 6/27/11, Jason Reid says that GORO “generated $18MM in cash” that has been used topay dividends

Bottom line: Despite what management says, GORO has never generated cash in any quarterand all dividends have been paid from proceeds of the many previous private placements

• The SEC defines a Ponzi scheme as a “fraud that involves the payment of purported returnsto existing investors from funds contributed by new investors.”

5

3) Inaccurately claiming to produce gold-equivalent

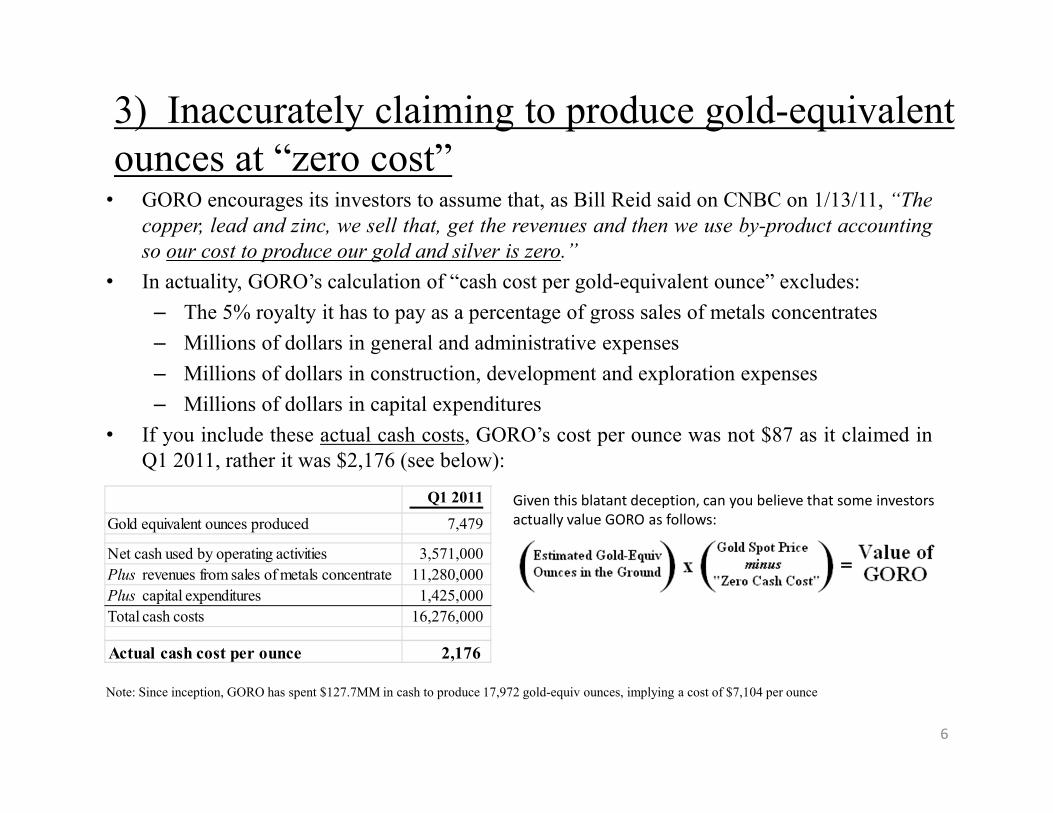

ounces at “zero cost”• GORO encourages its investors to assume that, as Bill Reid said on CNBC on 1/13/11, “The

copper, lead and zinc, we sell that, get the revenues and then we use by-product accounting

so our cost to produce our gold and silver is zero.”

• In actuality, GORO’s calculation of “cash cost per gold-equivalent ounce” excludes:

– The 5% royalty it has to pay as a percentage of gross sales of metals concentrates

– Millions of dollars in general and administrative expenses

– Millions of dollars in construction, development and exploration expenses

– Millions of dollars in capital expenditures

• If you include these actual cash costs, GORO’s cost per ounce was not $87 as it claimed in

Q1 2011, rather it was $2,176 (see below):

Note: Since inception, GORO has spent $127.7MM in cash to produce 17,972 gold-equiv ounces, implying a cost of $7,104 per ounce

Q1 2011

Gold equivalent ounces produced 7,479

Net cash used by operating activities 3,571,000

Plus revenues from sales of metals concentrate 11,280,000

Plus capital expenditures 1,425,000

Total cash costs 16,276,000

Actual cash cost per ounce 2,176

Given this blatant deception, can you believe that some investors

actually value GORO as follows:

6

4) Claiming to have “one of the highest grade

deposits in the world”

4a) No one outside of the Reid family has verified GORO’s claims with independent drilling

• GORO’s geological reports note that geological work was both performed by and checked

by David Reid

• No one else has verified these claims with an independent drilling study…

• Not Hochschild

• Not Michael Dudas of Jeffries

• Not John Hathaway of Toqueville Gold Fund

• Not John Doody of Gold Stock Analysts

• No one else period.

• Bre-X Minerals had a similar “take our word for it” attitude in claiming to have found world

class mineralization on sites previously passed over by others - until independent drilling

studies confirmed that management's claims were fraudulent

7

4) Claiming to have “one of the highest grade

deposits in the world” (cont.)

4b) Other companies that have independently drilled on the site have passed

Apex Minerals

• GORO leased the El Aguila site in 2002 shortly after the lease was cancelled by Apex

Mining Corporation

• Over the four years that Apex leased El Aguila, it carried out exploration “involving

geologic mapping, surface sampling and a drilling program spanning over 4,000 feet”

• Apex cancelled its lease on El Aguila when the site “did not meet its expectations”

• Apex was run by Thomas Kaplan, the billionaire that BusinessWeek Magazine dubbed

“Gold’s Evangelist” due to his high conviction for gold

• In stark contrast to Apex, GORO claims to have instantly found material amounts of

gold onsite…

o In speaking about El Aguila, GORO’s CEO Bill Reid explained “we were

impressed right from the beginning… (there was) ore grade mineralization

sticking right out of the ground.”

o He went onto to claim that the “very first” hole that GORO drilled on the site

“yielded 55 grams of gold per tonne and 700 grams of silver per tonne.”

8

4) Claiming to have “one of the highest grade

deposits in the world” (cont.)4b) Other companies that have independently drilled on the site have passed (cont.)

Canyon Resources

• After leasing the El Aguila property, GORO entered into an “exploration agreement” withpublicly-traded Canyon Resources Corporation

• Canyon Resources subsequently spent $500,000 exploring the property including drillingnearly 13,000 feet of survey holes

• Following the review of this drilling data, Canyon Resources passed on the opportunity toacquire 50% of the property for $3,500,000.

Heemskirk

• In July 2005, Heemskirk became GORO’s largest outside shareholder and acquired the “firstright to acquire all or part of any securities offered by (GORO) in the future” and the “firstright of refusal to acquire any or all of (GORO’s) interest in mining properties located inMexico” should GORO sell the properties. By contract, these rights lasted through August2008.

• During this three year period, GORO issued many press releases announcing “continuedhigh-grade drill intercepts.” In April 2007, GORO announced that, based on its confidencein the project, the Board had decided to put the El Aguila project into production

• Though they were GORO’s largest shareholder during this period where GORO’smanagement became confident enough to begin putting the sites into production, Heemskirkwas not impressed as reflected in its decision to sell its GORO shares years ago at a fractionof current prices 9

4) Claiming to have “one of the highest grade

deposits in the world” (cont.)4c) Production resulting from GORO’s mines has been far below forecasts

Management’s Forecast for El Aguila Open Pit

• “We discovered our open pit deposit, which we are presently mining with our very first drill

hole. We knew we had something very special after this discovery.” - Bill Reid, Commodity Stocks,

10/31/09

• We are focused on quality ounces, which at El Aguila indicate a capital payback of ~ 6

months… first year production is targeted at 70,000 ounces of gold which would come

solely from open pit mineralization.” - Bill Reid, Company Press Release, 4/11/07

• “El Aguila Open Pit… mineralized material: company estimate of 330,000 tonnes @ Au 7.5

grams/tonne and Ag 63 grams/tonne” - GORO Corporate Presentation 1/21/11

• “Targeting 60,000 to 70,000 ounces gold at El Aguila open pit.” - GORO Corporate Presentation 1/21/11

Actual Production Result for El Aguila Open Pit

• Completion of mining of El Aguila open pit, and including “initial processing of the

underground ore” resulted in the reported sale of $26.0 million in “metals concentrate,”

including 17,972 ounces of gold at a cost, net of all revenues, of $96.2 million.

• GORO management now claims that the open pit was mined primarily to obtain waste rock

to build a tailings damn

10

5) Troubling corporate governance practices

5a) Tightly controlled by small group

• GORO has only five full-time U.S. employees and four are family members

– CEO is Bill Reid

– President Jason Reid is Bill’s Son

– VP David Reid is Bill’s brother

– Corporate Development Officer Greg Patterson is Bill’s son-in-law

5b) Acting lead independent director (Bill Conrad) is being paid richly and selling shares

• As an “Independent” Director Bill Conrad is able to serve as Chairman of both the Audit

and Compensation Committees. He has held these posts since 2006

• Over the past five years, Conrad has been granted 850,000 GORO shares or 1.6% of total

shares, in the form of restricted stock and options

• Conrad has sold 450,000 GORO shares BUT has only reported publicly the sale of 43,160

shares. Conrad and the board have permitted the Reids to sell millions of GORO shares

without public disclosures

• In 2010, Conrad received $260,000 in cash compensation from GORO compared to just

$126,000 for Isac Burstein and $80,500 (annualized) for Tor Falck. Monty Jennings was

paid just $215,889 for acting as part-time CFO during all of 2010

• In 2010, as Chairman of the Compensation Committee, Conrad approved massive salary

and bonus increases for the Reids bringing the cash compensation of Bill, David and Jason

Reid to a total of $2,320,000 in 2010 from just $662,000 in 2009 11

5) Troubling corporate governance practices (cont.)

5c) Failed to hire a full-time and/or mining-experienced CFO

• On 6/16/11, GORO announced the hiring of Paul Oberman as part-time CFO

• He “will be compensated at an hourly rate” and his contract “is terminable by either party

upon 30 days’ notice.” The company also agreed to indemnify Mr. Oberman

• In seeking to replace their former part-time CFO Monty Jennings, the company had said

that Monty “has mining experience but specializes in oil and gas… (and) we are searching

for a mining experienced CFO.”

• According to Paul’s own Linked-In page, his 42-year career included just 4 years in the

mining industry where he served as a controller from 1977 to 1981. Over the last 15 years,

over 90% of Paul’s documented experience has been in the office furniture, auto service

center, IT consulting and jewelry industries

• Paul’s actual employer, Catapult CFO Partners, describes itself as “the premier source in the

Rocky Mountain region for interim and part-time CFOs.”

5d) Using a non-major public auditing firm

• GORO continually promises that it will switch to a major public auditing firm. But the

company continues to employ the small regional firm of StarkSchenkein LLP

With a ten figure market cap, $25MM+ in annual dividend payments and large salaries paid to

the Reids and Bill Conrad, what is it about GORO’s accounting that prevents it from finding and

funding a full-time mining CFO and using a major public auditing firm?12

6a) Never ending delays and escalating costs

• In 2007, GORO was targeting 2008 as its “start-up” year for the Aguila open pit project with

necessary infrastructure expected to cost $20 million and “CAPEX payback in 6 months”

• In 2008, GORO said that “start-up” for El Aguila was being targeted for 2009 and that the

project may cost as much as $26 million

• In 2009, GORO moved the “start-up” for El Aguila to 2010 and disclosed that it had

committed to spending $35.5 million to complete the project

• In 2010, after it had declared “commercial production” at El Aguila, GORO said that it had

spent $47.6 million to complete the “majority” of the project but that additional capital

expenditures would be required to finish it. GORO also indicated that the project “has not

yet reached its designed targets.”

13

6b) Misleading investors to expect “IRR>100%” –

while every project has a hugely negative IRRPromotion

• “We have an internal rate of return 100% as a hurdle, in other words we have to pay back

our capital in less than one year or we won’t do a project. This particular project (El

Aguila), we will pay back its capital in less than one year.” - GORO CEO Bill Reid Interview on

GoldSeek.com, 2/11/09

• For years GORO has promised that all of its projects will “payback CAPEX less than 1

year”

• In 2007, GORO targeted 2008 as the “start-up year” for the Aguila open pit project

with “CAPEX payback in 6 months”

Reality

• GORO has never had positive cash flow and as of March 2011 had consumed over $100MM

in cash

14

6c) Deception about mgmt’s experience levels

Promotion

• “(GORO’s) founders, who have experienced a long and successful career in discovering,

developing and monetizing precious metals deposits…” - Michael Dudas of Jeffries on 1/5/11 – Firm was

paid $3.6MM by GORO

• “The tremendous success of US Gold Corp. is a strong asset for the Reid’s resume and will

bring additional confidence and interest into (GORO).” - Peter Spina of GoldSeek.com on 1/31/07– At the

time, Spina was a paid employee of GORO and GORO still advertises on GoldSeek.com

• “Regarding GORO, the current management has a strong track record in terms of

developing and growing US Gold Corp. prior to starting GORO.” - Waheed Hasan Wasserman Morris

on 1/17/07 – Firm was paid $25.5K by GORO

• “Gold Stock Analyst normally wouldn't cover (GORO) due to no indep feasibility study,

but, knowing Reid family’s mine building history” (we made an exception). - John Doody, Gold Stock Analyst on 10/1/10

Reality

• “Since our inception in 1979, we have never been profitable and we have not generated

revenue from operations since 1990.” U.S. Gold Corp. 2009 10-K

• To this day, the Reids, whether at U.S. Gold Corp. or GORO or any where else, have yet to

produce positive cash flow from any mine in any quarter

15

6d) Deception about danger levels in Mexico

Promotion

• “We’re in the southern state of Oaxaca, Mexico, it’s a beautiful place with very nice people,

we are very pleased to be there… most of the danger (in Mexico) is in the northern border

area or certain states… but in our area, we don’t see that problem… it’s a very nice area.”- GORO CEO Bill Reid, CNBC 1/13/11

Reality

• “Our business operations may be adversely affected by social and political unrest in

Oaxaca… Oaxaca City, the capital of the State of Oaxaca, experienced a period of social

and political unrest in 2006. Certain civilian groups seeking political reform staged protests

and demonstrations in various locations in Oaxaca City, including schools, government

offices and major roadways. Although our property is roughly a 90 minute drive from

Oaxaca City and the civil disturbances appear to have dissipated, these events may still

negatively impact our business operations if Oaxaca experiences another such event.”- GORO’s SEC Filings

16

6e) Misleading statements on capitalizing of costs

Promotion

• On the Q1 2011 conference call, Bill Reid said “We are an exploration stage company with

regards to accounting and the SEC primarily because we do not have proven and probable

reserves and because of that our accounting requires us to expense all capital having to do

with the mine. We don’t mind that, we think its actually very positive, its much closer to

cash and that’s really the way things work.”

Reality

• In fact, GORO did capitalize, rather than expense, significant amounts. In all, capitalized

expenses in Q1 2011 totaled $6.1MM including $2.5MM for “materials and supplies,”

$2.1MM for “ore stockpiles and metals concentrates” and $1.2MM for “machinery and

equipment”

• If these costs had been expensed rather than capitalized, GORO’s Q1 2011 $2.0MM GAAP

profit would have been a loss of $4.1MM

Even Worse… when it is in their interest, GORO will publicly promote that they are

capitalizing expenses. On 6/20/11, in defending the open pit mine (which was supposed to

produce 70K gold ounces and only did <18K) Jason Reid said that using the open pit to “get us

into production in the shortest amount of time” allowing GORO to start “capitalizing expenses”

rather than taking “operating costs”

17

6f) Manufacturing a GAAP profit despite a cash loss

What happened to “Earnings are opinion, cash is fact”?

• On GORO’s Q1 2011 conference call Bill Reid said “we are pleased to report our first

profitable quarter, we consider this an important milestone in the history of the company.”

If this profit was real than why did GORO’s cash balance decrease by $9.8MM during the

quarter?

• As GORO warns, investors should be weary of GAAP profits, like the one GORO just

reported, and look at the cash flow statement to see what really happened…

• In Q1 2011, GORO reported operating cash flow of negative $3.6MM as well as $1.4MM in

capital expenditures. Adding the resulting negative $5.0MM in “free cash flow” to the

$4.8MM in dividends that GORO paid to shareholders sums to the $9.8MM reduction in

cash during the quarter

• Note that GORO had $1.4MM in “stock-based compensation” during the quarter, had these

employees been paid in cash and not stock, the cash balance would have declined a total of

$12.2MM on the quarter

With GORO being tightly controlled by a small group, not having a dedicated CFO, being

audited by a non-major public accounting firm and having only one customer (who happens to

be private and not release financials itself) – investors should be weary of GORO’s accounting.

→Put another way, would you trust financials certified by a CEO who uses loopholes to

conceal the sales of millions of shares by insiders?18

6g) Misleading statements on shareholder dilution

Promotion

• GORO’s corporate presentation indicates that the company has a “disciplined capital

structure” that “limits shareholder dilution”

Reality

• GORO has been extremely dilutive carrying out more than 20 separate private placements

in its short history

• Additionally, GORO has granted more than 13,000,000 shares and options to management,

employees, external “investor relations consultants,” etc.

• While the vast majority of the grants have been to the Reids and Bill Conrad, over 550,000

shares have been granted to outside “investor relations consultants”

• GORO was once more honest about its highly dilutive practices disclosing that…

“Since we have not generated any cash from operations, we have been forced to rely on sale of

equity to pay our expenses.” GORO Prospectus Filed 2/11/08

• Though GORO has never “generated any cash from operations,” the company no longer

includes the above sentence in its filings

19

6h) Deception on ownership of mining properties

Promotion

• “(GORO’s) Mining unit consists of 100% interest in 5 potential high-grade gold and silver

properties in Mexico” - GORO Corporate Presentation 1/21/11

Reality

• “Effective October 14, 2002, we leased three mining concessions, El Aguila, El Aire and La

Tehuana, from a former consultant to our company. The lease agreement is subject to a 4%

net smelter return royalty where production is sold in the form of gold/silver dore and 5% for

production sold in concentrate form… the lessor may terminate it if we fail to fulfill any of

our obligations… (In) February 2007, we leased a property known as the Solaga (that)… is

subject to a 4% net smelter return royalty on any production… In 2010, we acquired two

additional concessions, each of which require a 2% royalty to the former owner…The

requirement to pay royalties to the owner of the concessions… will reduce our profitability

from production of gold or other precious metal.” - GORO 10-K 2010

• As previously detailed (Point 3), GORO does not include these royalty charges in its own

calculation of “cash cost per ounce”

• In 2010, GORO cancelled 70,000 restricted shares, valued at over $2.0 million, that had

previously been granted to an employee or consultant for the company. Shareholders deserve

to know the identity of this individual and what that person did to warrant the cancellation of

these shares. What if it is the former consultant who owns these properties?

20

7a) Odd circumstances concerning sales

• In every financial statement ever filed with the SEC through June 2010, GORO’s

income statement began with a line item reading “Gold Sales” with zeros

following it to reflect the fact that GORO was not selling any gold

• After declaring “commercial production” in July 2010, GORO changed that top

line item from “Gold Sales” to “Sales of Metals Concentrate”

• On the third quarter 2010 conference call where GORO CEO Bill Reid was

announcing his first “sales of metals concentrate” in over twenty years, he was

asked to provide the average prices for the gold and silver sold during the quarter.

Incredibly, he responded “I, I, I really don’t have those figures, we worked really

late into the night to get our financials and I don’t really have them.”

• Also, one may think that a company claiming to control such “rich” amounts of

resources would actively bargain with many purchasers to achieve the best prices.

However, GORO has entered into an agreement to sell all of its “metals

concentrate” to just one buyer, privately-held Trafigura Group

21

7b) Hochschild’s involvement with GORO…

• In 2006, Hochschild goes public, IPO raises $616MM. Like GORO, Hochschild is very

dilutive carrying out additional private placements through 2009 to raise another $325MM.

Until shortly before IPO, Hochschild was small company with revenues below $100MM

• In 2008, Hochschild’s earnings decline 70%+ due to lower than expected grades and higher

than expected costs. Biggest issue is that its mines are reaching exhaustion. Names new

CEO and begins explaining that it will pursue an M&A strategy to build a future pipeline

• Over remainder of 2008 and into early 2010, Hochschild uses proceeds from debt issuance

and additional equity offerings to invest $500MM across a range of mining projects and

companies. Invests ~13% of this M&A budget into GORO

• In announcing the investment, Hochschild said “GORO has a highly experienced

management team and we look forward to working with them to develop the significant

potential of the El Aguila property as well as the other properties in their impressive project

pipeline.”

• Hochschild has NOT carried out its own independent drilling tests to verify GORO’s claims.

• December 2009, Hochschild’s “2010 Production Overview” explains that GORO “has a

stated production target of 70,000 ounces of gold in 2010.” Hochschild includes its shares

of these 70,000 ounces in its overall production target for 2010. As it turns out, GORO

produces just 10,493 ounces in 2010

• March 2010, Hochschild’s CEO and CFO resign from the company for “personal reasons”22

7b) Hochschild’s involvement with GORO (cont)…

• September 2010, Hochschild does not participate in Jeffries’ private placement where

GORO raises $55.6MM. At four cents a month, Hochschild stands to receive over $7MM a

year in dividends that GORO is paying out from the proceeds of that Jeffries offering

• March 2011, Hochschild reports that it produced 26.4MM silver-equivalent attributable

ounces, 9% below its 2010 Production Target of 29.0MM silver-equivalent ounces.

GORO’s lower than expected production accounts for 40% of this miss

• In March 2011, Hochschild announces that its 2011 Production Target is just 22.5MM

silver-equivalent attributable ounces compared to 26.4MM in 2010 and 28.0MM in 2009

• If GORO were to meet its own 2011 production target of 90K gold-equivalent ounces (most

likely it will not), Hochschild’s GORO-related silver-equivalent attributable ounces would

be 1.50MM compared to just 0.18MM in 2010

• In total, Hochschild has purchased 14.63MM GORO shares for $67MM (before

dividends received) at a cost of $4.58 per share. It’s incredible that others (John

Hathaway, John Doody etc.) use Hochschild’s investment at less than $5.00 to justify a

$30+ valuation for GORO

• April 2011, John Doody says publicly that he expects Hochschild will sell its GORO

position if/when the shares get Canadian listing

23

7c) Superficial research coverage

• GORO receives its primary “investment newsletter” coverage from John Doody

of Gold Stock Analyst and its primary “Wall Street” coverage from Michael

Dudas of Jeffries

• Neither party has conducted geological tests, specifically independent drilling, to

verify GORO’s claims

• Jeffries collected $3.6MM in fees from a GORO private placement in Sept 2010

• Both are bullish on GORO, neither has made its endorsement of GORO

contingent on the company “proving” its own mineral resource estimates

• To help justify GORO’s soaring market capitalization, both have resorted to using

dividend yield valuation metrics

• Bre-X received very positive coverage from the analyst community for years,

particularly from the firms that collected fees from raising cash for the company

24

7d) Details on John Doody of Gold Stock Analyst

• John Doody is a vocal advocate of GORO

• In promoting his newsletter, John Doody professes to use his trading in “penny stocks to

date women half (his) age” and warns that “unless (he is) looking at a chart of women’s

lingerie sizes – (he) usually avoids analyzing sets of data like (geological reports).”

• Doody also claims to “have a track record when it comes to revealing frauds” based on his

declaring Bre-X a fraud in Barron’s in early 1997

• On 4/5/97, Barron’s quoted John Doody as saying that Bre-X’s Busang mine was a fraud.

However, the following events preceded this quote:– 1/23/97, a mysterious fire in Busang’s administrative building destroys geological records.

– 2/17/97, Freeport geologists begin first independent drilling tests to test Bre-X’s claims for Busang.

– 3/12/97, Freeport geologists issue internal report saying their drilling has yielded only “insignificant gold values” for the

Busang project. Report is not yet released publicly.

– 3/19/97, Bre-X geologist Michael de Guzman plunges 800 feet from a helicopter and dies near Busang.

– 3/21/97, Indonesian press begins publicly speculating that Freeport-McMoran’s drilling tests had not found gold.

– 3/24/97, Graham Farquharson of Strathcona Minerals begins new drilling tests at Busang.

– 3/26/97 Graham Farquharson tells lawyers that there is a “strong possibility that the potential gold resources of the

Busang property have been overstated because of invalid samples and assaying.”

– 3/26/97, Freeport-McMoran’s conclusion that its own drilling results from Busang yield only “insignificant gold values”

is finally made public after weeks of speculation.

– 4/4/97, Canadian mining publication Northern Miner (which had previously praised the Busang discovery) publishes a

story titled “Bre-X’s Credibility Undermined As Suspicions Mount.” Story is based on report by Australian geological

consulting firm Normet Pty that was part of a resource report ordered by Bre-X. Normet’s report warned of anomalies in

Bre-X’s drill samples indicating salting. The report had been kept secret by Bre-X for ten months before Northern Miner

broke the story.

– 4/4/97, Bre-X stock, which had recently traded in excess of $25.00 CAD had fallen to just $3.20 CAD.25

7d) What is John Doody saying about GORO today

• Following GORO’s April 2011 announcement that, despite continuing negative cash flows,

the monthly dividend is being increased by 33% from 3 cents to 4 cents, John Doody

indicates that “Gold stocks’ typical 1% yield would justify a $48 shr price” for GORO’s

shares

• GORO may already be setting the stage for another large private placement and using John

Doody to condition investors. Consider the following quote from John Doody’s Gold Stock

Analyst newsletter on April 15, 2011: “Hauling 1,200 t/day ore to feed the Mill is approx 80

in/out truckloads and the traffic could ultimately present a problem in meeting Co’s 200K

oz/yr goal for 2013. If production moves deeper than 500 meters, GSA would expect Co to

build a $50+mil shaft to simplify haulage. Unknown are deeper ground conditions, so far

so good, but if conditions are more difficult than forecast, the ore’s rich grade allows for

extra support expense.”

o If this statement turns out to be accurate, regulators should ask… Why did John Doody

publish the statement before management communicated the issue publicly?

• The trend of John Doody possibly disclosing non-public information on GORO continued

on May 1, 2011 when his GSA newsletter announced that “GORO engaged well-known

Pincock, Allen, Holt (PAH) to calculate the 43-101 resource statement.”

26

7e) Don’t Be Fooled by a 43-101 Reserve Study…

• GORO does not have “proven or probable reserves” per SEC standards

• As a substitute, it may attempt a study to be able to report 43-101 reserves according to

Canadian standards

• John Doody has said that “Basically, GORO has done all the drilling necessary for a 43-101,

they just have to get an engineer to finish up all his calculations and put them into a form

that Canada wants to submit it.”

• Investors should be weary of any 43-101 reserves reported by GORO as:

o The standard for SEC reserves is much higher than for 43-101 reserves, and

o GORO can continue to use its own drilling results, rather than being required to have a

truly independent drilling study to achieve 43-101 reserves

27

7e) 43-101 Reserve Study Concerns, Cont…

• According to John Doody’s Gold Stock Analyst May 1, 2011 report…“GORO engaged

well-known Pincock, Allen, Holt (PAH) to calculate the 43-101 resource statement.”

Should investors be comfortable with a reserve study performed by PAH?

Public details of a recent lawsuit suggests that the answer may be “NO”…

• In 2005 and 2006, PAH performed an “independent engineering evaluation” of the Hazelton

underground mine in Indiana for Bronco Energy Fund. Standard Bank made the mistake of

relying on the PAH report in financing Bronco’s acquisition of the mine

• When Bronco went bankrupt, Standard Bank lost $40MM

• Standard Bank later sued PAH for “professional negligence and negligent misrepresentation

in its independent engineer’s due diligence report”

• Standard Bank was unable to prevail in court as the Judge ruled that “because the

relationship of these parties is governed by a contract between PAH and Bronco (and not

directly between PAH and Standard Bank)… PAH had no duty to Standard Bank”

• GORO investors should realize that PAH will have no duty to them also

28

7f) What to make of GORO’s new “acquisition”…

• On June 20, 2011, GORO announced that it had “acquired” properties to “add to and

increase the size of the Aguila Project” and consolidate “a dominant land position”

• In fact, GORO did not “acquire” this property from a seller. Rather it “staked new claims”

to get it

• In an investor talk on the same day of the press release, Jason Reid explained that GORO

was able to obtain the claims because they expired. But he did not know who previously

owned them and he would not give the name of the “excellent man in the field” who told

GORO that the claims had become available

• Jason said that the fees to stake and maintain these claims are “very nominal”

• Does GORO really expect investors to believe…

1) GORO found “one of the highest grade deposits in the world” on lands where company’s

like Canyon Resources and Thomas Kaplan’s Apex Minerals failed to find compelling

mineralization AND…

2) That owners of neighboring claims on the same “trend” of this “world class… high grade

asset base” simply allowed the claims to lapse AND…

3) When the claims became available, GORO encountered no competition and was able to

obtain them for only “nominal fees”

29

7g) Other facts that give one pause

• GORO started construction of the mill in Mexico well over two years before the company

received a mining permit

• David Reid, who was responsible for the company’s geological work, quit GORO’s Board

in November 2010 without explanation

o David’s less-experienced nephew joined GORO’s boards near the time of David’s

leaving it but there is no reason that both could not serve on the board

• For years, GORO has promised that once gold production was underway they would start

paying dividends in custom gold dore GORO coins rather than “trash cash.” In early 2011,

GORO began showing the public the first such coin. However, the coin is actually made

from gold that GORO purchased and not gold that GORO mined

30

7h) What did GORO’s CEO say?...

• “For a month or so there has not been any drilling. But we have been doing a lot of work on

the ground and come up with some very exciting things but it will have to wait for a press

release before I talk about them. We have really embellished and are continuing to work on

our model which looks more exciting all the time.” - Bill Reid, GORO Conference Call, March 2009

• “We did not engineer this to death with a bunch of feasibility studies or critical paths.” - Bill

Reid, GORO Conference Call, June 2009

• “You will never see a private gold mining company because public gold mining companies

obtain much higher values for owners as each ounce of gold produced is given a value as

high as $20,000 or more, where private companies only get the price of gold.” - Bill Reid,

Various Investor Conversations

31

8) Applying Lessons from Bre-X…

• Similarities between Bre-X and GORO are numerous…

o Bre-X also claimed to have found “one of the highest grade deposits in the world” on

sites that had been previously surveyed and passed over by other miners

o Bre-X also conducted its own drilling tests the results of which were tightly controlled

by the three key executives of the company

o Bre-X’s management team also had a history of penny stock promotions and spent vast

majority of time in front of investors and very little time at the actual mines

o Bre-X had two separate companies provide “feasibility” studies that included resource

estimates but these were based on the drill test results conducted by Bre-X. Though

executives of Bre-X frequently mentioned these reports as evidence of the high grade

reserves on its properties, they kept the full reports under wraps so that the public

would not learn that portions of these feasibility studies recommended that the

geological work should be confirmed by an independent drilling study

• But GORO has additional red flags that Bre-X lacked like…

o Insiders concealing the sales of millions of shares from the public

o Paying out private placement proceeds as dividends to attract new investors

Investors learned from Bre-X the hard way and should not repeat the same mistakes with GORO

32

8) Number of potential victims could grow…

• The longer the Bre-X fraud lasted, the worse it became. The stock was even included in the

Toronto Stock Exchange’s TSE300 Index

• GORO was recently included in the Russell 2000 Index

• The number of investors that were victimized by the Bre-X fraud was very large due to high

number of private placements carried out by Bre-X

• GORO is a very dilutive company having carried out more than twenty separate private

placement transactions in its history

• GORO’s high level of cash consumption will require the company to raise more cash in

foreseeable future

33

Conclusions for GORO…

• Investors should not be duped by GORO’s own estimates. Investors should also

be wary of estimates resulting from any 43-101 resource studies that GORO may

produce in the future as such studies have significantly lower standards than SEC

proven and probable reserves and may also be based on GORO’s own drilling

tests anyway

• Investors should not let the Reid family convince them that independent drilling

tests are too expensive. The expense of such tests pale in comparison to the

billion dollar plus market capitalization of the company, the big salaries of its

management and the millions of dollars in dividends that this company is paying

despite no cash profits and no mineral reserves

• The massive Bre-X fraud occurred because no one, not investors or analysts or

regulators, required that management’s estimates of gold resources be verified by

independent third-party drilling tests

• The investment community should demand that independent drilling tests be

carried out on GORO’s mining properties

• Even those that trust that GORO has a “Midas Touch”

should insist on independent drilling studies to prove it34