Goods Compliance Update June 2017 - abf.gov.auVictorian company loses customs depot licence for...

26

Goods Compliance Update June 2017 | 1 Goods Compliance Update June 2017

Transcript of Goods Compliance Update June 2017 - abf.gov.auVictorian company loses customs depot licence for...

Goods Compliance Update June 2017 | 1

Goods Compliance Update June 2017

Goods Compliance Update June 2017 | 2

Message from Commander Customs Compliance 3

Asbestos 5 Importing a vehicle to Australia 5 Asbestos statistics 6

Industry Summit 2017 7

Review of all customs licensing arrangements 8 Purpose of the review 8 Final Report - May 2017 8

Anti-Dumping 9 Dumping definitions 9What is dumping? 10 What is anti-dumping 10 How to find confidential instructions 11 Tariff Concession Orders (TCO) – Exemption from dumping duties is not automatic 11 Importers must be aware 11 The use of exemption codes is monitored by the ADC and the ABF 11

Update on China-Australia Free Trade Agreement 12 Using the Correct Certificate of Origin 12 For further information 13

Tariff Advice System 14 Further Information 14

What is in your cider? 15 Information for importers and their brokers 15

C8DAP

Typewritten Text

Goods Compliance Update June 2017 | 3

Reminder to store high-risk goods safely 16

Former customs broker sentenced to jail 17

Victorian company loses customs depot licence for repeated breaches 17

Newsroom Alerts 18

Compliance Programme Results 1 July 2016 – 31 May 2017 19 The Infringement Notice Scheme 19 Value of Revenue Understatements 21 Cargo Control and Accounting 21 Administration of the Refund Scheme 22 Administration of the Duty Drawback Scheme 22 Compliance Monitoring Programme 23

Import Declarations 23 Export Declarations 24 Cargo Reporting 25

Useful points of contact 26

Goods Compliance Update June 2017 | 4

Message from Commander Customs Compliance Welcome to the second edition of the Goods Compliance Update (GCU) for 2017.

Customs Compliance continues to work with industry across a wide range of forums. This year Customs Compliance officers have delivered accredited Continuing Professional Development presentations at a number of industry conferences around Australia. I am encouraged by the positive feedback received from industry members about these presentations and I appreciate the opportunities provided by our industry partners to participate.

Customs Compliance was also represented at the recent Industry Operational Training Session in Melbourne. I note an important theme for this event was the role that trusted entities in the trading community have in maintaining supply chain integrity. While the integrity of the supply chain is fundamental to effective border management and a healthy Australian economy, efficient and secure trade is also key to a competitive and prosperous industry sector. Therefore it is essential that we continue to work together to promote compliance.

The minutes from the March 2017 meeting of the Trade and Goods Compliance Advisory Group (CAG) are available for you to view online. At the June CAG meeting, the Export Council of Australia presented on the topic of export reporting and members identified a number of practical options to improve compliance. The outcomes of this discussion will be included in the minutes which will be published on the Department’s website and we will further consider how to best apply the valuable input from members to improve export reporting compliance. It was also encouraging to hear from CAG members at this meeting that the GCU is providing a useful communication tool to inform the trading community about compliance issues, initiatives, and recent activities. We remain committed to the GCU and would value your feedback on ways we can improve our communications. Please contact us through [email protected].

Erin Dale Commander Customs Compliance Australian Border Force

Goods Compliance Update June 2017 | 5

Asbestos

Importing a vehicle to Australia

The ABF is urging people to be aware of the risk of asbestos in cars and parts they plan to bring to Australia.

Since 31 December 2003, the Australian Government has prohibited the importation of goods that contain asbestos, and placed a ban on the domestic manufacture and use of all types of asbestos and products containing asbestos. The ABF actively targets products suspected of containing asbestos, including vehicles and vehicle parts. ABF activities are not designed to cause inconvenience to importers, but are part of the Australian Government’s arrangements to protect the public from the significant dangers of asbestos.

To date, asbestos has been detected in a range of motor vehicles and parts such as clutch linings, brake pads and gaskets. Recent examples, which have been imported into Australia from a variety of countries, include five Ford Mustangs, including a Shelby GT350 (brake line insulation and pads, manifold gasket, air-conditioning compressor gasket, windscreen surrounds and wiper scuttle panel); two of Lincoln Continentals (drum brakes and brake pads) and a Porsche 911 (brake pads). Over the same period, classic motorcycles marques from, Honda, Kawasaki, Ducati, Yamaha, Vincent, AJS and Enfield have tested positive along with vintage Lambretta, IWL and Vespa motor scooters and even new vehicles, such as a consignment of ATVs and go-karts.

In a number of countries, unlike Australia, there are few to no restrictions on the use and supply of asbestos. Local standards in some countries may even classify goods as ‘asbestos-free’ where they meet a certain low level of asbestos content. In Australia, a product found with any level of asbestos, regardless of age, is prohibited for import or use. The person importing the vehicle must show proof that the imported car or parts do not contain any asbestos.

One way to show this is by testing the vehicle or parts using a National Association of Testing Authorities (NATA) accredited laboratory. If proof cannot be shown, the goods will be held at the border until sampling and testing for asbestos is done. This can mean long delays and additional cost.

People who want to have a sample of their goods tested in Australia, before importing them, must first seek permission from the Minister of Employment to import a sample for analysis, through the Asbestos Safety and Eradication Agency. The samples must be from the actual shipment to be imported and the testing must be done by an Australian testing laboratory that is NATA accredited.

Samples may also be tested outside Australia by a laboratory that is accredited by international accreditation authorities that are NATA-recognised equivalents. The local testing authority must be a signatory to a Mutual Recognition Arrangement (MRA) with NATA and have a valid scope of

Goods Compliance Update June 2017 | 6

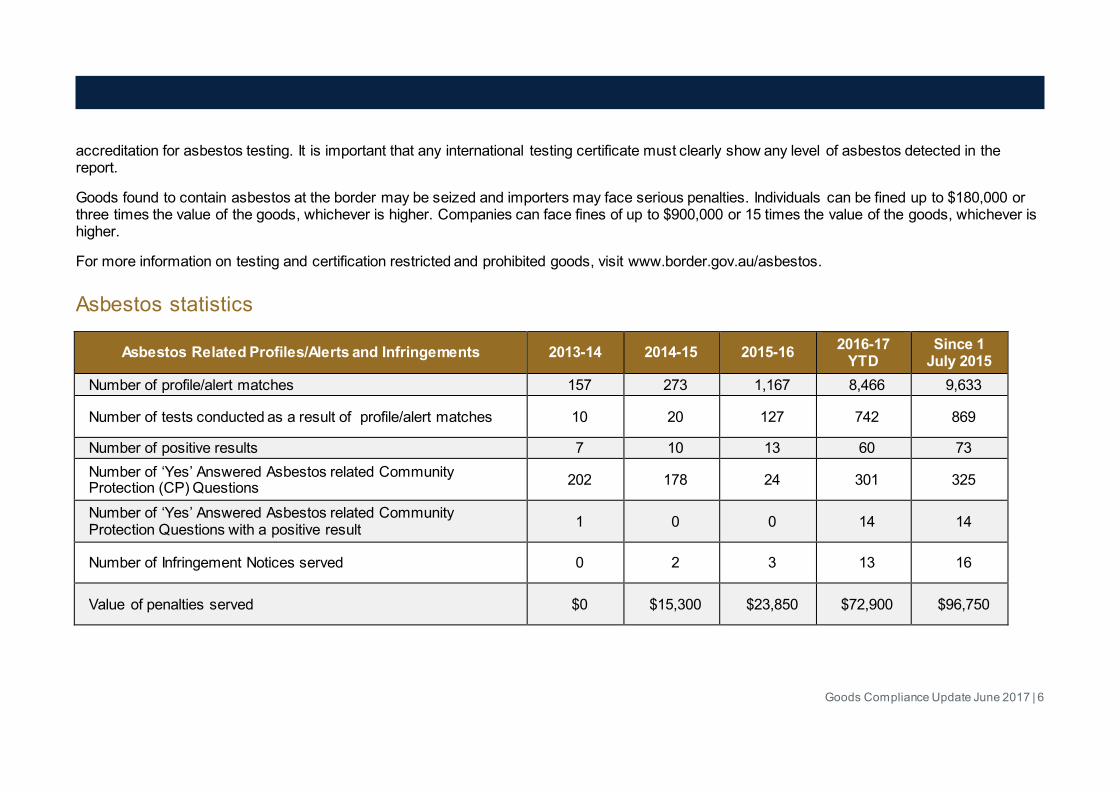

accreditation for asbestos testing. It is important that any international testing certificate must clearly show any level of asbestos detected in the report.

Goods found to contain asbestos at the border may be seized and importers may face serious penalties. Individuals can be fined up to $180,000 or three times the value of the goods, whichever is higher. Companies can face fines of up to $900,000 or 15 times the value of the goods, whichever is higher.

For more information on testing and certification restricted and prohibited goods, visit www.border.gov.au/asbestos.

Asbestos statistics

Asbestos Related Profiles/Alerts and Infringements 2013-14 2014-15 2015-16 2016-17 YTD

Since 1 July 2015

Number of profile/alert matches 157 273 1,167 8,466 9,633

Number of tests conducted as a result of profile/alert matches 10 20 127 742 869

Number of positive results 7 10 13 60 73 Number of ‘Yes’ Answered Asbestos related Community Protection (CP) Questions 202 178 24 301 325

Number of ‘Yes’ Answered Asbestos related Community Protection Questions with a positive result 1 0 0 14 14

Number of Infringement Notices served 0 2 3 13 16

Value of penalties served $0 $15,300 $23,850 $72,900 $96,750

Goods Compliance Update June 2017 | 7

Industry Summit 2017 The annual Industry Summit is an opportunity for industry and the Department to have a conversation about strategic trade, travel and migration issues. The Industry Summit 2017 will be hosted in Melbourne on 31 July and its theme is Border innovation: strengthening our nation’s economy, security and society. The Summit will explore ways to create opportunities for collaboration, co-design and co-investment in technologies and business processes that will help us respond to the changing global trade, traveller and migration environment. Industry representatives will hear from the Department’s leaders, including the Secretary of the Department and Commissioner of the Australian Border Force, about our strategic direction and priorities for the future. By participating in the Industry Summit workshops, industry representatives can influence the Department’s plans to continue improving our processes, policies and programs. Those unable to attend the Industry Summit can follow online via Twitter (@AusBorderForce), as keynote speeches will be live streamed. You can also join the conversation using our hashtag #DIBPIndustrySummit. The event is by invitation only. For more information email [email protected]. Read more and see previous Industry Summit results at www.border.gov.au/industrysummit.

Goods Compliance Update June 2017 | 8

Review of all customs licensing arrangements

Purpose of the review

The focus of the review into licensing regimes under the Customs Act 1901 (as announced in November 2015) was to work with industry and other government departments to identify opportunities to streamline, improve and deregulate the existing licensing regimes. The purpose of the review was to:

• review the role played by licensing in today's border management environment, and consider whether there are other, more efficient, ways to achieve the same objectives for border management;

• assess the efficiency and effectiveness of the current licensing regimes; • assess the regulatory burden of the current licensing regimes and identify opportunities to reduce this burden and align application processes

between administrations; and • recommend whether the current licensing regimes should be retained with improvements/enhancements or replaced.

Final Report - May 2017

The Review of Customs Licensing Regimes Final Report was formally submitted to Comptroller-General of Customs on the 31 March 2017. We appreciate the contributions made to the Review, particularly submissions, feedback on the Issues Paper, and attendance at the workshops.

The Final Report outlines the findings of the Review and sets out the 15 recommendations. The first recommendation is that the current licensing regime be retained for customs brokers, depots and warehouses, as no suggested model would be more efficient in meeting the objectives for border management than the existing one. The remaining 14 recommendations are intended to strengthen integrity and streamline processes underpinning the licensing regime for the Department, industry and other government agencies that also license customs brokers, depots and warehouses (for example, the Australian Taxation Office).

Goods Compliance Update June 2017 | 9

The Department will continue to work with stakeholders during the implementation of the recommendations.

For any queries regarding the Final Report, please contact [email protected].

Anti-Dumping Customs Compliance has recently encountered a number of compliance issues related to anti-dumping. We have provided some important information in relation to anti-dumping to assist industry in complying with their reporting requirements and eliminate any common misconceptions of the system.

Dumping definitions Normal Value (NV) - is usually based on the price paid for like goods (to those on which a dumping action is initiated) that are sold in the domestic market of the country of export. It is one of the variable factors used in determining a dumping margin.

Non-Injurious FOB Price (NIFOB)/Non-Injurious Price (NIP) - under Customs legislation there is provision for final duty rates to be less than the dumping margin, if that rate is sufficient to remove the injury to the Australian industry. In determining what that rate is, the Anti-Dumping Commission (ADC) must determine the non-injurious price. Where the NIP is less than the normal value the lesser margin may be imposed. The NIFOB and/or NIP is another variable factor. NIFOBS refers to measures imposed before 1993 and NIPS to those imposed after Jan 1 1993.

Production/export subsidy - where an exporter is the recipient of a benefit or financial contribution from the government of the exporting country then that benefit is considered to be a subsidy and becomes countervailable under our legislative provisions. The production and export subsidy variables are two such benefits identified as a result of previous ADC investigations.

Undertaking export price - as an alternative to imposing duties after an investigation, the Assistant Minister for Industry, Innovation & Science may accept a written undertaking from an exporter to conduct future export trade to Australia at a price that will not cause injury to the Australian industry - this is known as a Price Undertaking.

Ascertained export price (AEP) - is the export price established by the ADC after inquiries locally and overseas during the investigation. The ADC examines all exports of goods to Australia and makes deductions to prices (where necessary) to reach the FOB level - the AEP is then compared with

Goods Compliance Update June 2017 | 10

either the normal value and or NIFOB/NIP in order to determine what if any is the dumping margin. The AEP is the third of the variable factors ascertained during the investigation. Non-injurious price (NIP) - see above

Dumping Security Amount - during the course of an investigation, the ADC may establish that dumping has occurred. In this case, provisional dumping duties may be imposed on future exports. These provisional measures are taken in the form of securities.

Countervailing Security Amount - same as dumping security amount but refers to an investigation where a countervailable subsidy has been identified during an investigation.

Interim Dumping Duty (IDD) - these are the measures imposed at the completion of an investigation. The IDD amount payable represents the dumping margin, that is, the difference between the AEP and the NV and or the NIFOB/NIP.

Interim Countervailing Duty - represents the amount of subsidy as identified in the investigation.

What is dumping?

Dumping occurs when goods exported to Australia are priced lower than their ‘normal value’, which is usually the comparable price in the ordinary course of trade in the exporter’s domestic market. Anti-dumping duties may be imposed when dumping causes, or threatens to cause, material injury to an Australian industry. Dumping duty is payable when goods are being imported at a price that is lower than the normal value of the goods in the country of export.

What is anti-dumping?

Anti-dumping is the imposition of a measure by the Australian government, in the form of an additional duty on imports and/or a minimum export price, to remedy material injury to Australian manufacturers caused by dumping. For further information regarding anti-dumping measures, please see the ADC. The ADC administers Australia’s anti-dumping and countervailing (anti-subsidy) system. Upon application by the Australian industry setting out prima facie evidence of the dumping or subsidy and the injury the ADC commences an investigation and reports to the Minister, whether anti-dumping or countervailing duties should be imposed on goods from the countries named in the application.

Goods Compliance Update June 2017 | 11

How to find confidential instructions

The IDD ad valorem rate and the AEP for each dumping specification number (DSN) are considered confidential and will not be published. Importers of these goods are required to substantiate their commercial relationship with an exporter/supplier of their goods by providing evidence of:

• A previous trading history with nominated exporter/supplier of the goods. Evidence of a trading history would take the form of at least commercial invoices, packing list and bills of lading from previous shipments; or

• In the absence of a trading history, an offer or a quotation from an exporter/supplier of goods subject to dumping/countervailing measures. The offer or quotation must be on the exporter/supplier’s company letterhead.

Requests and evidence must be sent to [email protected].

Tariff Concession Orders (TCO) – Exemption from dumping duties is not automatic An Exemption Instrument based on the TCO must be in place to use the exemption code. In the dumping system, for the TCO, there are two separate pieces of legislation in play therefore it is not a case of straightforward transfer of the exemption. TCOs are concessional instruments under the Customs Tariff Act 1995 that allow concessional rates of Customs Duty. Information on exemptions can be found on the ADC website.

Importers must be aware

Throughout any investigation, review or inquiry, the ADC provides contemporaneous information on cases on the public record (which is made available on the ADC website) throughout the entirety of the case and the onus is on interested parties to familiarise themselves with the duties payable. Interested parties should check the website to obtain current information regarding investigations, reviews and inquiries that are in progress.

The use of exemption codes is monitored by the ADC and the ABF

The onus is ultimately on the importer. The importer must be prepared to provide sufficient evidence to the ABF of the entry into home consumption and that the goods had not simply been transhipped for each circumstance where a country exemption is used and when a compliance audit is carried out. If the goods are determined to be transhipped, any unpaid duty liability will need to be paid and there may also be administrative penalties for a false declaration applicable.

Goods Compliance Update June 2017 | 12

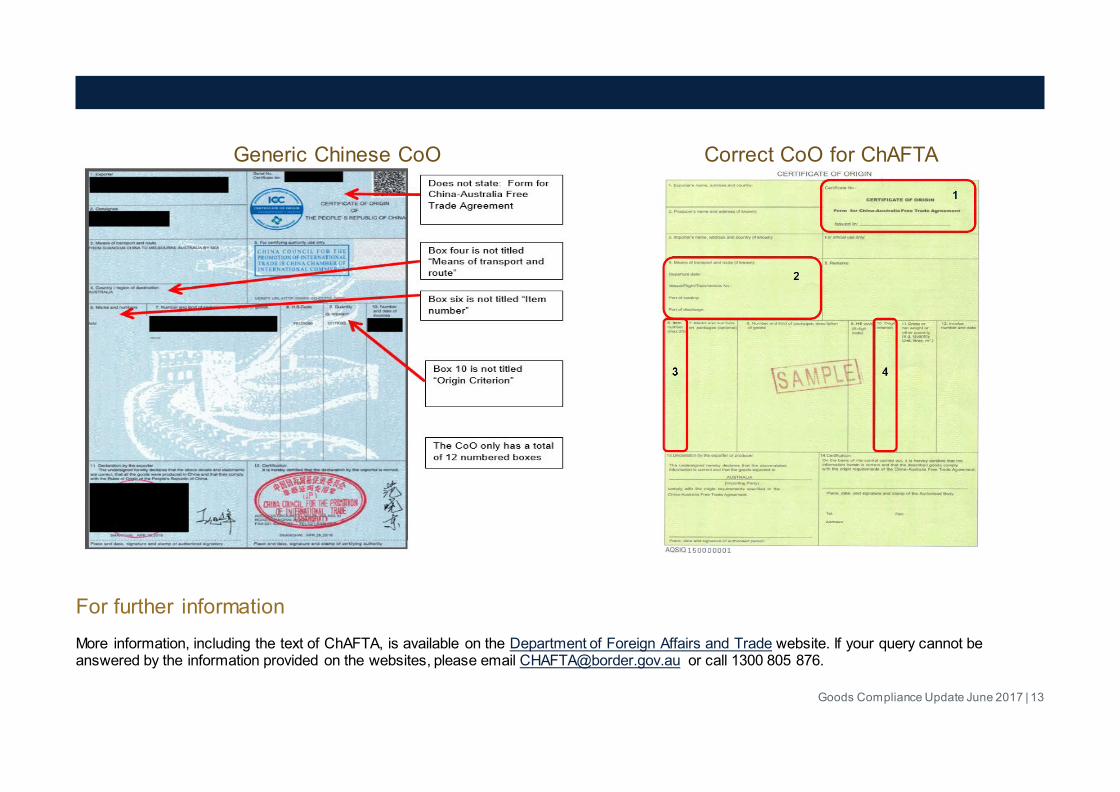

Update on China-Australia Free Trade Agreement Since the China-Australia Free Trade Agreement (ChAFTA) entered into force on 20 December 2015, the Origin and Verification team located within Customs Compliance has been asked to clarify which Certificate of Origin (CoO) can be used to claim preferential treatment under ChAFTA regulations. In a number of cases, incorrect CoOs have been used when trying to claim preferential tariff treatment.

Using the Correct Certificate of Origin

To claim preferential treatment under ChAFTA, the correct CoO must be used. The correct CoO for ChAFTA must:

1. state “Form for China-Australia Free Trade Agreement” in the top right hand corner

2. have a box four titled “Means of Transport and route”

3. have a box six titled “Item number”

4. have a box ten titled “Origin criterion”

5. contain 14 numbered boxes

6. be completed in English

7. be stamped and signed by an authorised body of exporting country

8. be completed as per the ChAFTA Annex 3-A instructions.

The China Council for the Promotion of International Trade issues a generic CoO for goods exported from China. The generic CoO cannot be used to claim preferential treatment under ChAFTA as it has deficient boxes and information. For example, the generic CoO has only 12 boxes, does not state it is for ChAFTA, and does not have a box for the Origin Criterion. A comparison of the correct CoO for ChAFTA and the generic CoO is provided below.

Goods Compliance Update June 2017 | 13

Generic Chinese CoO Correct CoO for ChAFTA

For further information

More information, including the text of ChAFTA, is available on the Department of Foreign Affairs and Trade website. If your query cannot be answered by the information provided on the websites, please email [email protected] or call 1300 805 876.

Goods Compliance Update June 2017 | 14

Tariff Advice System Recent compliance checks have identified importers changing brokers after provision of an unfavourable tariff advice, and not providing the new broker with information as to the existence of a decision. Investigation into these cases may include further examination of the importer, issue of demands for unpaid duty and application of infringement notices.

A tariff advice is a private and binding ruling that allows importers to seek a formal ruling on the classification of specific goods before importation. The tariff advice system is designed to assist importers in making business decisions about future imports of specific goods prior to committing to importation. The importer may apply directly to the ABF or may engage a broker to lodge the application on their behalf.

The National Trade Advice Centre (NTAC) is responsible for issuing a tariff advice and also review existing classifications. In 42% of cases, the tariff advice or clarification will change the classification or the tariff concession claimed. Once an advice is given, the classification of the goods will be recognised for five years from the date of application, unless withdrawn or voided. When a tariff advice is granted, it must be followed if the goods (subject to the tariff advice) are imported.

Post import verification is conducted on imports where a tariff advice has been provided, and goods are not classified accordingly. As a tariff advice is a private, binding ruling, it cannot be disregarded if it is unfavourable to the applicant. Should the applicant be dissatisfied with the decision, a review may be requested. Information on how to apply for a review is given will all decisions.

Further Information

For further information on the Tariff Advice System can be found here.

Goods Compliance Update June 2017 | 15

What is in your cider? Recently the ABF has been reviewing the importation of cider products including flavoured, apple and pear ciders. The findings across 26 importers have indicated that this is an area of significant non-compliance and misunderstanding for both brokers and importers. Genuine ciders are classified to tariff 2206.00.30. They are duty free and attract Wine Equalisation Tax (WET). The products must however satisfy the conditions of Chapter 22 Note 5 (d) of the Customs Tariff Schedule and not have added to it, at any time, any liquor or substance that gives the cider its colour and/or flavour. WET is payable at the border or can be deferred, passed on at the retail level or paid following domestic sales. Brokers and importers need to consult with the manufacturer and obtain the ingredient lists, to satisfy themselves that imported ciders meet Australia’s legislative requirements. Importers must be aware that not all imported ciders brewed overseas are the same. That is not all imported ciders are brewed to comply with Australia’s legislative requirements. This is particularly the case with parallel imports of ciders imported and distributed by parallel importers. Parallel imports of the same brand do not provide the assurance that they have the same exact ingredients as the authorised products. Authorised cider products are brewed specifically for distribution within Australia and comply with Australia’s legislative requirements. Parallel imports are brewed for other markets and other countries which often do not have the same level of regulatory oversight.

Information for importers and their brokers

Where there is uncertainty as to the ingredients of parallel imports and or confirmation of the ingredients from the manufacturer(s) cannot be obtained, cider must be classified to 2206.00.92. There is an approximate fivefold difference between WET and duty/excise, which can translate into a costly error when considering the possible application of the Infringement Notice Scheme. Breaches of s243T of the Customs Act 1901 resulting in the short-payment of duty, presently provides for 45 penalty units or 75% of the short-paid duty, whichever is higher.

Goods Compliance Update June 2017 | 16

Reminder to store high-risk goods safely There has recently been an increase in the number of licensed premises failing to store high-risk goods safely, in particular firearms. The failure to store these goods appropriately places the community at serious risk, and is a breach of licence conditions.

The obligations of a licence holder to store high-risk goods safely are prescribed in the Customs Act 1901 (the Act) and outlined in Australian Customs and Border Protection Notice 2013/56. High risk items such as firearms are to be stored in the deadhouse (additional licence condition 26), which must be kept locked (additional licence condition 11). Licence holders must review their policy and procedures to ensure that their staff are aware of and follow all licence requirements.

Licence holders must also assess their deadhouse to ensure it is of sufficient size to accommodate any consignments of firearms received by the licensed premises. Failure to store high-risk goods such as firearms appropriately is an offence under section 36(1), 36(2) and 77R (1) of the Act.

Sections 36(1), 36(2) - Failure to keep goods safely or failure to account for goods

Failure to provide the required safeguards for high-risk goods causes undue risks to the wider community. An offence under these provisions does not require the goods to have been moved, altered or interfered with. An offence against section 36(2) is one of strict liability.

Section 77R (1) – Breach of conditions of depot licence Storing firearms, or other high risk goods outside the deadhouse and / or failing to lock the deadhouse are offences under 77R (1) as they amount to breaches of conditions imposed under section 77Q. An offence against 77R (1) is one of strict liability.

Failure to adhere to licence obligations may result in the issuing of an infringement notice, suspension or cancellation of your license or prosecution.

Licensed establishment operators must be aware that there may be additional obligations under State or Territory law relating to the safe storage of firearms that need to be observed.

Goods Compliance Update June 2017 | 17

Former customs broker sentenced to jail A former customs broker has been handed a four-year prison sentence after being found guilty of falsifying importation documents and pocketing more than $700,000. Daniel Larosa, 48, was charged with one count of obtaining a financial advantage by deception and one count of attempting to obtain a financial advantage by deception after the ABF uncovered he had made 318 fraudulent claims for duty on goods that were not entitled to be duty free.

As a result of the deception, $728,188 was paid into Larosa’s personal bank account. Assistant Commissioner Investigations, Wayne Buchhorn, said the ABF’s investigation began after a routine check uncovered a number of inconsistencies in Larosa’s refund applications.

“Not only did Larosa abuse his position of trust as a licensed and authorised customs broker, he also demonstrated a planned and persistent act of offending and used the fraudulently obtained funds to support his own lifestyle,” Assistant Commissioner Buchhorn said.

At the time of the deception, Larosa was practising as a licensed customs broker which authorised him to act as an agent for the importation of goods into Australia. Once authorities became aware of the dishonest behaviour, his customs broker licence was suspended and subsequently cancelled.

To view the story in full, please visit our newsroom.

Victorian company loses customs depot licence for repeated breaches The ABF has cancelled the customs depot licence of a Victorian company for repeatedly breaching its licence conditions. The company was licensed under the Customs Act 1901 to hold goods prior to being customs cleared at its depot in Victoria.

On 28 March 2017, ABF officers executed monitoring warrants at the depot and associated offices and identified a total of 14 breaches of its licensing conditions.

The breaches included: • unpacking, moving and storing goods outside of the licenced area • failing to keep goods in a separate and distinct area from goods not subject to customs control • failing to provide commercial records relating to goods received into the depot • failing to maintain a depot log book providing details of people entering the licensed area • failing to maintain adequate fencing and gates

Goods Compliance Update June 2017 | 18

• failing to implement and maintain an effective accounting system.

ABF officers served the company with a Notice of Intended Cancellation and Suspension of the Customs Depot Licence pursuant to section 77V of the Customs Act 1901. This meant the depot had its licence immediately suspended with full cancellation taking effect on Tuesday, 11 April 2017.

Regional Commander Victoria, James Watson said this result sends a strong message to companies who do not comply with their licensing conditions. ”These depots are trusted to store and handle potentially dangerous goods and we won’t tolerate any breach of that trust,” Commander Watson said.

To view the story in full, please visit our newsroom.

Newsroom Alerts An ABF operation has resulted in the arrest of a Victorian man and a South Australian woman for allegedly importing more than nine tonnes of illicit tobacco into Melbourne and Adelaide. The ABF Tobacco Strike Team began investigating the individuals following the arrest of another syndicate member in August of last year. To view the story in full, please visit our newsroom. Three men associated with an Outlaw Motorcycle Gang (OMCG) have been charged following a major multi-agency drug operation resulting in the seizure of approximately 119 kilograms of crystal methamphetamine with an estimated street value of $119 million. To view the story in full, please visit our newsroom.

Goods Compliance Update June 2017 | 19

Compliance Programme Results 1 July 2016 – 31 May 20171

The Infringement Notice Scheme

Table 1 – Infringement Notice Scheme 2016-17 year to date (YTD)

Offence Number issued

Value of notices issued

33(2) – Moving altering or interfering with goods subject to Customs control without authority. 5 $18,900.00 33(3) – Moving altering or interfering with goods subject to Customs control without authority. 1 $8,100.00 33(6) – Moving, altering or interfering with goods subject to Customs control without authority. 181 $1,438,650.00 36(2) – Failure to keep goods safely or failure to account for goods. 1 $8,100.00 36(6) – Failure to keep goods safely or failure to account for goods. 9 $72,900.00 60(1) – Failure to bring ship or aircraft for boarding at appointed boarding station. 1 $2,700.00 64(13) – Failure to meet reporting requirements for the impending arrival of a ship or aircraft. 28 $123,750.00 64A(3) – Failure to answer questions or produce documents relating to a ship or aircraft, or its cargo, crew, passengers, stores or its voyage or flight. 2 $2,700.00

64AA(10) – Failure to meet reporting requirements for the arrival of a ship or aircraft. 1 $8,100.00 64AB(10) – Failure to meet reporting requirements for the report of cargo. 32 $257,400.00

1 The Compliance programme statistics were accurate at the time of publishing. Current system parameters may result in variances if published for the same timeframe in the future.

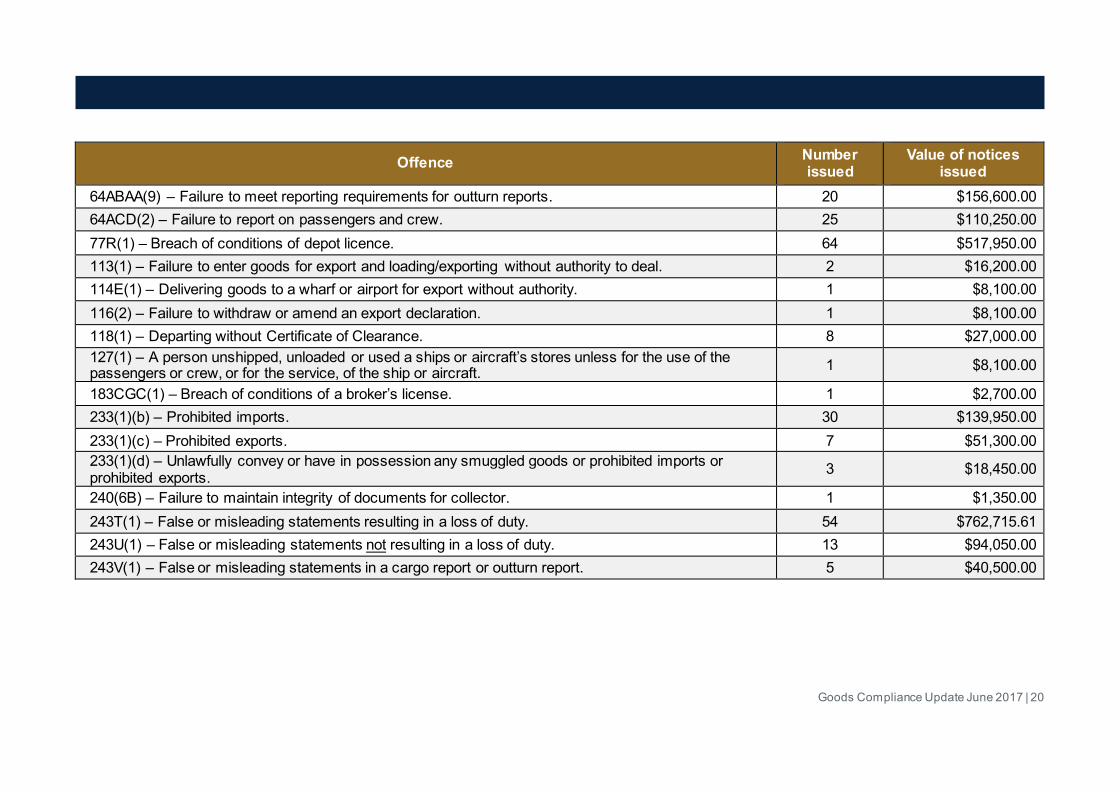

Goods Compliance Update June 2017 | 20

Offence Number issued

Value of notices issued

64ABAA(9) – Failure to meet reporting requirements for outturn reports. 20 $156,600.00 64ACD(2) – Failure to report on passengers and crew. 25 $110,250.00 77R(1) – Breach of conditions of depot licence. 64 $517,950.00 113(1) – Failure to enter goods for export and loading/exporting without authority to deal. 2 $16,200.00 114E(1) – Delivering goods to a wharf or airport for export without authority. 1 $8,100.00 116(2) – Failure to withdraw or amend an export declaration. 1 $8,100.00 118(1) – Departing without Certificate of Clearance. 8 $27,000.00 127(1) – A person unshipped, unloaded or used a ships or aircraft’s stores unless for the use of the passengers or crew, or for the service, of the ship or aircraft. 1 $8,100.00

183CGC(1) – Breach of conditions of a broker’s license. 1 $2,700.00 233(1)(b) – Prohibited imports. 30 $139,950.00 233(1)(c) – Prohibited exports. 7 $51,300.00 233(1)(d) – Unlawfully convey or have in possession any smuggled goods or prohibited imports or prohibited exports. 3 $18,450.00

240(6B) – Failure to maintain integrity of documents for collector. 1 $1,350.00 243T(1) – False or misleading statements resulting in a loss of duty. 54 $762,715.61 243U(1) – False or misleading statements not resulting in a loss of duty. 13 $94,050.00 243V(1) – False or misleading statements in a cargo report or outturn report. 5 $40,500.00

Goods Compliance Update June 2017 | 21

Value of Revenue Understatements

Table 2 – Understated Revenue for 2016-17 YTD

Post Transaction Verification $35,163,669.34 Pre-clearance Intervention $9,186,491.81 General Monitoring Programme $12,144,554.18 Voluntary Disclosures $31,326,576.07 Refunds refused $2,004,586.50

Cargo Control and Accounting Table 3 provides an overview of the cargo control and accounting results for 2016-17 YTD. The purpose of cargo control and accounting activity is to monitor the level of compliance of cargo terminal operators and licensed depots and warehouses with their respective legislated and licence conditions.

Table 3 – Cargo control and accounting activity for 2016-17 YTD

Number of customs cargo control and compliance activities 17,564 Proportion of breaches identified as against lines checked 2.71%

Goods Compliance Update June 2017 | 22

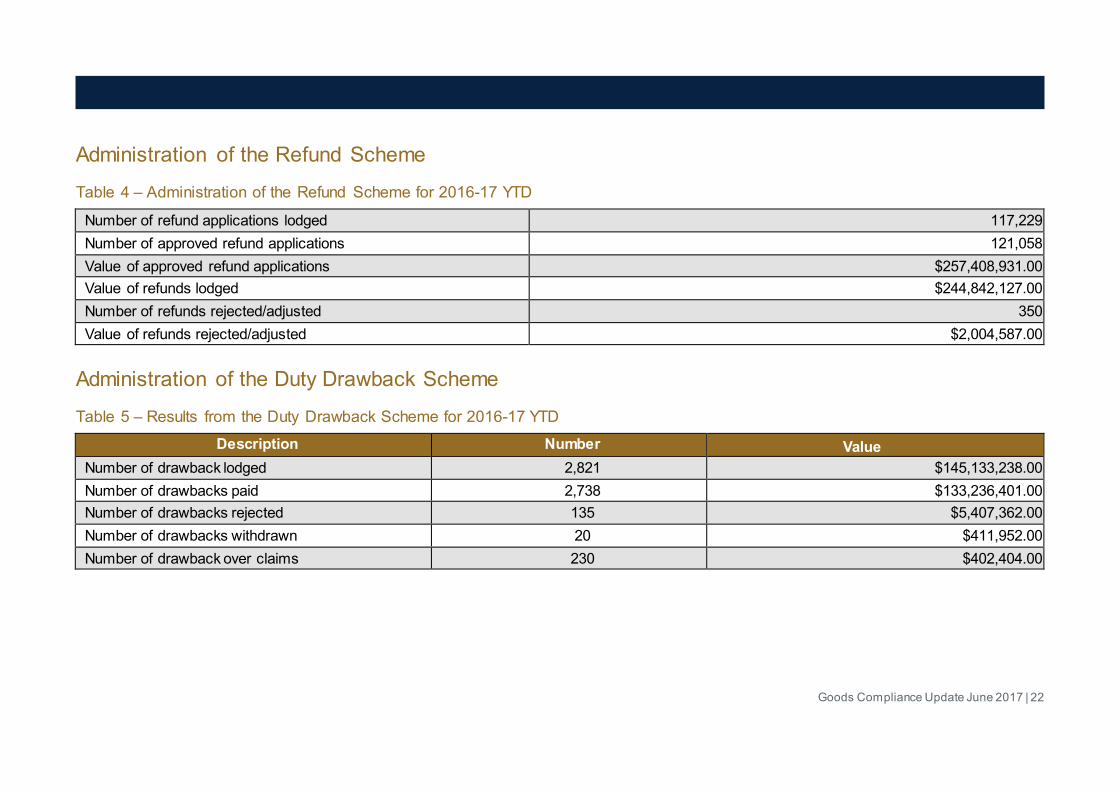

Administration of the Refund Scheme

Table 4 – Administration of the Refund Scheme for 2016-17 YTD

Number of refund applications lodged 117,229 Number of approved refund applications 121,058 Value of approved refund applications $257,408,931.00 Value of refunds lodged $244,842,127.00 Number of refunds rejected/adjusted 350 Value of refunds rejected/adjusted $2,004,587.00

Administration of the Duty Drawback Scheme

Table 5 – Results from the Duty Drawback Scheme for 2016-17 YTD

Description Number Value Number of drawback lodged 2,821 $145,133,238.00 Number of drawbacks paid 2,738 $133,236,401.00 Number of drawbacks rejected 135 $5,407,362.00 Number of drawbacks withdrawn 20 $411,952.00 Number of drawback over claims 230 $402,404.00

Goods Compliance Update June 2017 | 23

Compliance Monitoring Programme The Compliance Monitoring Programme (CMP) monitors the accuracy and quality of import and export declarations and cargo reports to assess overall levels of industry compliance. As a statistically valid sampling program, results from the CMP can indicate compliance behaviours across the cargo environment. Tables 6 to 11 show CMP results for 2016-17 YTD.

Import Declarations Table 6 – Compliance Monitoring Programme – import results for 2016-17 YTD

Number of lines checked 4,699 Number of lines detected to have error/s 1,319 Error rate (by number of lines) 28% Number of errors detected 1,720

Table 7 – Ten most common errors on import lines for 2016-17 YTD

Val – Valuation Date 280 Tariff Classification 175 Incorrect Delivery Address 159 Gross Weight 150 Val – Overseas Insurance 112 Val – Invoice Terms 107 Val – Related Transaction 100 Other 91 Val – Price (Invoice Total) 81 Val – Overseas Freight 72

Goods Compliance Update June 2017 | 24

Export Declarations

Table 8 – Compliance Monitoring Programme – Export Declaration results for 2016-17 YTD

Number of lines checked 820 Number of lines detected to have error/s 330 Error rate (by number of lines) 40.2% Number of errors detected 588

Table 9 – Top 10 most common errors on Export Declarations for 2016-17 YTD

FOB Value 164 Gross Weight 103 Net Quantity 68 AHECC - Misclassification 52 Origin 39 Other Export Data Inaccuracy 30 AHECC - Multi-Lines 24 Consignee Name 17 Consignee City 14 Declared Owner 13

Goods Compliance Update June 2017 | 25

Cargo Reporting Table 10 – Compliance Monitoring Programme – cargo report results for 2016-17 YTD

Number of lines checked 4,659 Number of cargo reports detected to have error/s 112 Error rate 2.4% Number of errors detected 120

Table 11 – The most common errors on cargo reports for the 2016-17 YTD

Gross Weight 47 Consignor Incorrect 19 Cargo Report Data Inaccuracy (Other) 16 Goods Description 15 Consignee Incorrect 14 Declared Value 3 Currency Code 2 Port of Destination 2 Origin Port of Loading 1

Goods Compliance Update June 2017 | 26

Useful points of contact General enquiries can be made through online forms available at the contact us page of our website. For referrals, including suspected revenue evasion, please contact Border Watch.

Purpose Phone Email Online

General enquiries NA (online form available) NA (online form available) General Enquiries Form

Referrals (Border Watch) Inside Australia: 1800 06 1800 Outside Australia: +61 2 6246 1325 NA (online form available) Border Watch

Cargo Support 1300 558 099 [email protected] Cargo Support

Tariff Concession Orders General Enquiries: 02 6229 3567 TAPIN help desk: 02 6275 6534 [email protected] Tariff Concession Orders

Tariff Advice 1800 053 016 [email protected] Tariff Advice

Duty Drawback Scheme 1300 304 322 [email protected] Duty Drawback Scheme

Voluntary Disclosures NA (email address only) [email protected] Voluntary Disclosures

ChAFTA enquiries 1300 805 876 [email protected] ChAFTA Enquiries

Origin enquiries 1300 805 876 [email protected] Free Trade Agreements

Australian Trusted Trader 1300 319 024 [email protected] Australian Trusted Trader