Goods and Services Tax (GST) Seminar 2016

15

1 © 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Goods and Services Tax (GST) Seminar 2016 Thursday, 15 September 2016

Transcript of Goods and Services Tax (GST) Seminar 2016

1© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Goods and Services Tax (GST) Seminar 2016Thursday, 15 September 2016

2© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Question 1: Asset disposal - AnswersAnswers:

I. Output tax to be accounted for by XYZ

– 7% x $30,000 = $2,100

II. Is ABC required to deem any supplies arising from transactions in items (a) and (b) above?

(a) To account for output tax on sale – 7% x $3,000 = $210

(b) To account for deemed output tax on free computers given

away – 7% x $150 = $10.5

3© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

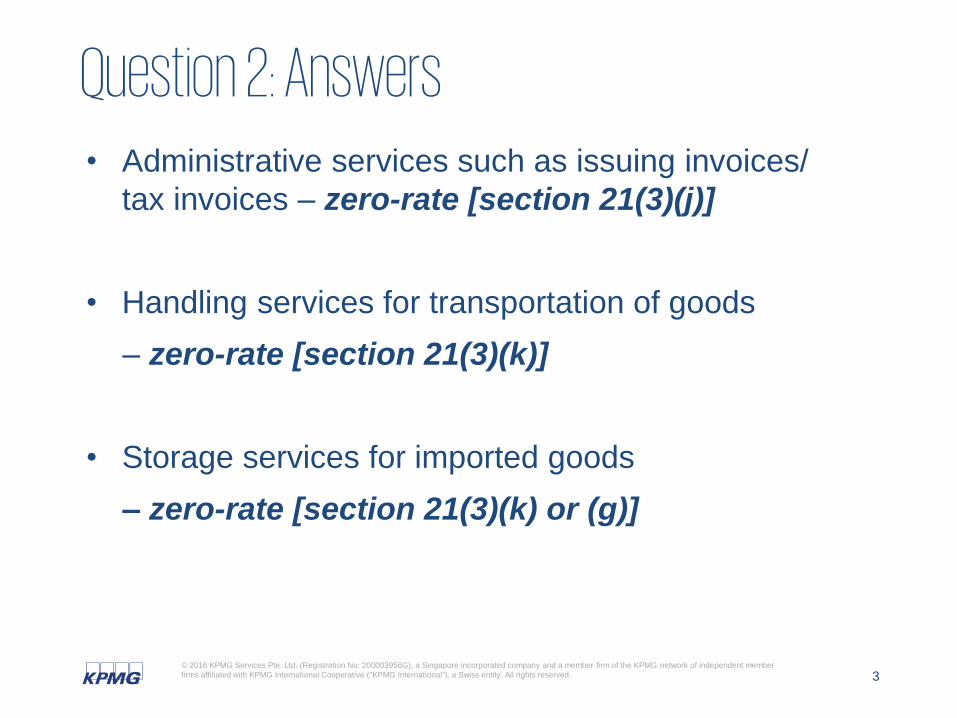

Question 2: Answers• Administrative services such as issuing invoices/

tax invoices – zero-rate [section 21(3)(j)]

• Handling services for transportation of goods

– zero-rate [section 21(3)(k)]

• Storage services for imported goods

– zero-rate [section 21(3)(k) or (g)]

4© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

(i)

(ii) To the extent that the training relates to highly specialised industry (e.g. pilot

training services) where training syllabus and contents are controlled but

Co.C has flexibility to customise method of training

- No comprehensive control exists

Question 3: AnswersCo. B Co. C

No Yes

5© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

(i) No. Total aggregate period (i.e. 183 days) does not exceed 183 days

(ii) No. Mr Lee’s personal visit was after cessation of his work – not counted

(iii) Company B will be regarded as having an FE in Singapore for entire supply

of installation services since period threshold of 183 days will be breached.

If the contracted sum exceeds S$1million, Company B is liable to register

for GST.

Question 4: Answers

6© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

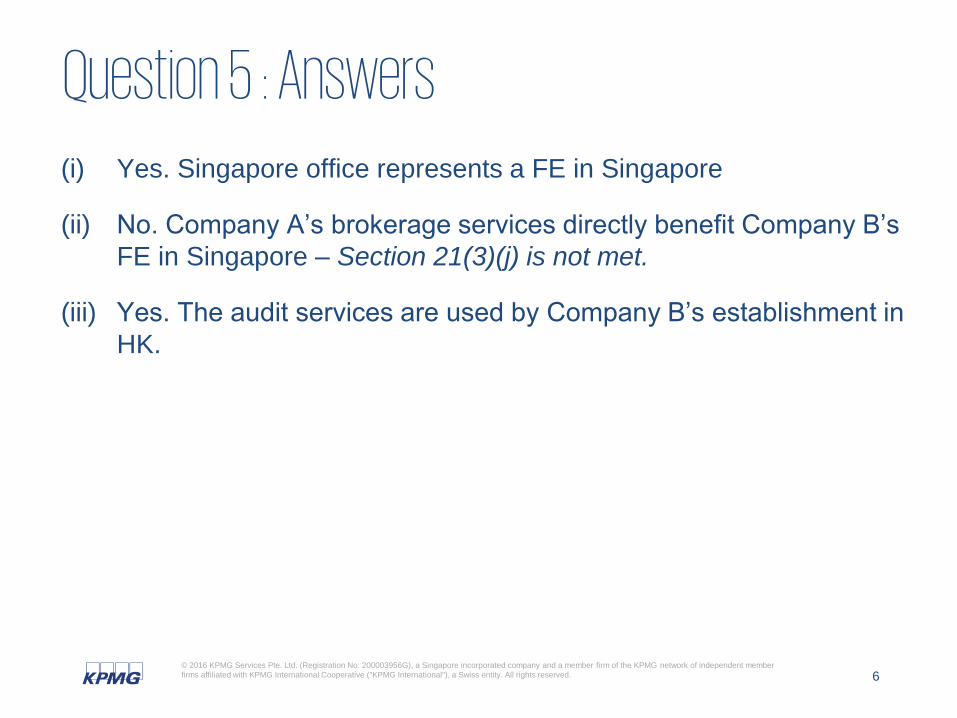

(i) Yes. Singapore office represents a FE in Singapore

(ii) No. Company A’s brokerage services directly benefit Company B’s

FE in Singapore – Section 21(3)(j) is not met.

(iii) Yes. The audit services are used by Company B’s establishment in

HK.

Question 5 : Answers

7©2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-

vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Question 6: AnswerWhether GST treatment should be determined per each expense

- No, since expenses are recovered as basis of charge for

primary service of management support provided to B

• If B belongs in Singapore – standard-rate

• If B belongs outside Singapore – zero-rate

8©2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-

vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Question 7: Answer

Whether Seconding Co is entitled to claim input tax on

seconded staff’s expenses

- No, if the secondment of staff satisfies the qualifying

conditions to be treated as not a supply

9© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

Question 8: AnswersI. Commission received by MNO from FC

– 7% GST

II. GST incurred on MNO’s tax invoice for purchase of new

car

- Claimable in full by FC

III GST incurred on FC’s tax invoice for purchase of new car

- Not claimable by HIJ – blocked input tax under regulation

27

10© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

No.

- More for staff’s personal benefit.

Question 9: Answer

11© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

Yes.

- Similar benefits are provided at other staff meetings in

general

Question 10: Answer

12© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

Yes.

- Solely for paying purchases made on behalf of

company and business entertainment

Question 11: Answer

13© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

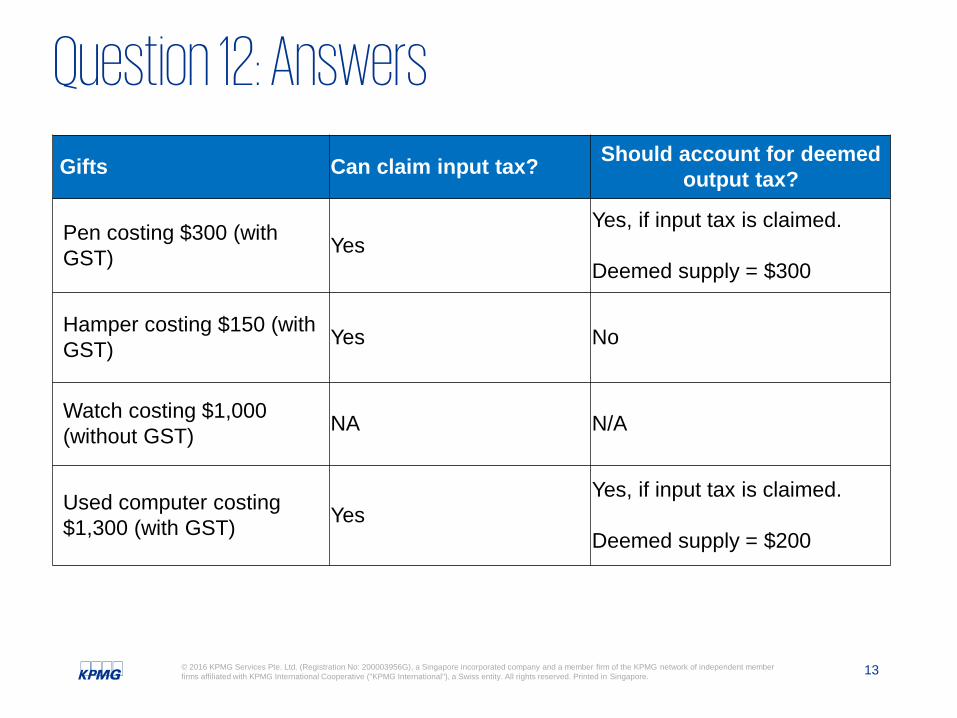

Gifts Can claim input tax? Should account for deemed

output tax?

Pen costing $300 (with

GST) Yes

Yes, if input tax is claimed.

Deemed supply = $300

Hamper costing $150 (with

GST) Yes No

Watch costing $1,000

(without GST) NA N/A

Used computer costing

$1,300 (with GST) Yes

Yes, if input tax is claimed.

Deemed supply = $200

Question 12: Answers

14© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

Gifts Can claim input tax? Should account for deemed

output tax?

Meal allowance of $20 No No

Lease of F&F of $500 (with

GST) per month

Yes (for April and May)

No (from June onwards)

Yes, deemed supply = $500

(for April and May)

No (from June onwards)

Maintenance fee of the

serviced apartment of $150

(with GST) per month

Yes (for April and May)

No (from June onwards)

N/A

Chalet rental of $600 Yes No

Question 12: Answers (Cont’d)

kpmg.com/socialmedia kpmg.com/app

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2016 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.