Globefish European Fish Price Report. Issue 8/2015 · Index for prices Groundfish 9 Flatfish 10...

25

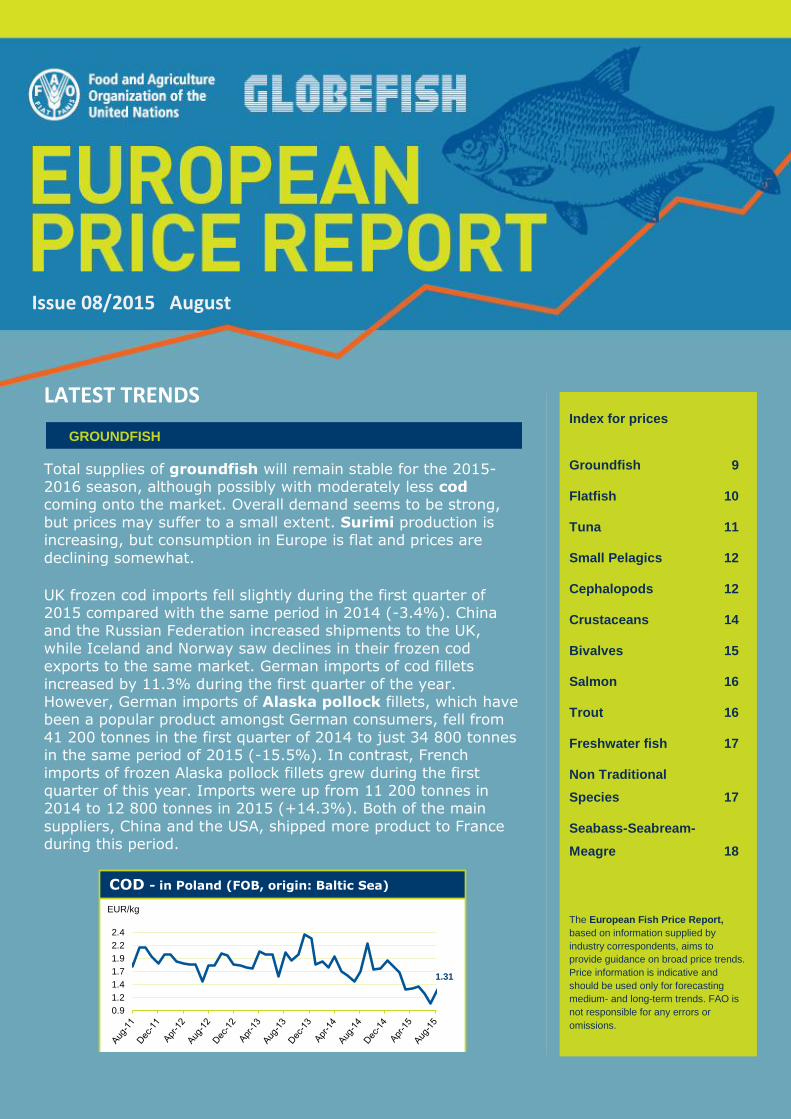

Index for prices Groundfish 9 Flatfish 10 Tuna 11 Small Pelagics 12 Cephalopods 12 Crustaceans 14 Bivalves 15 Salmon 16 Trout 16 Freshwater fish 17 Non Traditional Species 17 Seabass-Seabream- Meagre 18 The European Fish Price Report, based on information supplied by industry correspondents, aims to provide guidance on broad price trends. Price information is indicative and should be used only for forecasting medium- and long-term trends. FAO is not responsible for any errors or omissions. LATEST TRENDS Total supplies of groundfish will remain stable for the 2015- 2016 season, although possibly with moderately less cod coming onto the market. Overall demand seems to be strong, but prices may suffer to a small extent. Surimi production is increasing, but consumption in Europe is flat and prices are declining somewhat. UK frozen cod imports fell slightly during the first quarter of 2015 compared with the same period in 2014 (-3.4%). China and the Russian Federation increased shipments to the UK, while Iceland and Norway saw declines in their frozen cod exports to the same market. German imports of cod fillets increased by 11.3% during the first quarter of the year. However, German imports of Alaska pollock fillets, which have been a popular product amongst German consumers, fell from 41 200 tonnes in the first quarter of 2014 to just 34 800 tonnes in the same period of 2015 (-15.5%). In contrast, French imports of frozen Alaska pollock fillets grew during the first quarter of this year. Imports were up from 11 200 tonnes in 2014 to 12 800 tonnes in 2015 (+14.3%). Both of the main suppliers, China and the USA, shipped more product to France during this period. GROUNDFISH 1.31 0.9 1.2 1.4 1.7 1.9 2.2 2.4 EUR/kg COD - in Poland (FOB, origin: Baltic Sea) Issue 08/2015 August

Transcript of Globefish European Fish Price Report. Issue 8/2015 · Index for prices Groundfish 9 Flatfish 10...

Index for prices

Groundfish 9

Flatfish 10

Tuna 11

Small Pelagics 12

Cephalopods 12

Crustaceans 14

Bivalves 15

Salmon 16

Trout 16

Freshwater fish 17

Non Traditional

Species 17

Seabass-Seabream-

Meagre 18

The European Fish Price Report,

based on information supplied by

industry correspondents, aims to

provide guidance on broad price trends.

Price information is indicative and

should be used only for forecasting

medium- and long-term trends. FAO is

not responsible for any errors or

omissions.

LATEST TRENDS

Total supplies of groundfish will remain stable for the 2015-2016 season, although possibly with moderately less cod coming onto the market. Overall demand seems to be strong,

but prices may suffer to a small extent. Surimi production is increasing, but consumption in Europe is flat and prices are

declining somewhat.

UK frozen cod imports fell slightly during the first quarter of 2015 compared with the same period in 2014 (-3.4%). China and the Russian Federation increased shipments to the UK,

while Iceland and Norway saw declines in their frozen cod exports to the same market. German imports of cod fillets

increased by 11.3% during the first quarter of the year. However, German imports of Alaska pollock fillets, which have been a popular product amongst German consumers, fell from

41 200 tonnes in the first quarter of 2014 to just 34 800 tonnes in the same period of 2015 (-15.5%). In contrast, French

imports of frozen Alaska pollock fillets grew during the first quarter of this year. Imports were up from 11 200 tonnes in 2014 to 12 800 tonnes in 2015 (+14.3%). Both of the main

suppliers, China and the USA, shipped more product to France during this period.

GROUNDFISH

1.31

0.9

1.2

1.4

1.7

1.9

2.2

2.4

Fresh gutted

EUR/kg

COD - in Poland (FOB, origin: Baltic Sea)

Issue 08/2015 August

2

FLATFISH

TUNA - BILLFISHES

Seasonal demand for flatfish was very strong in August. Prices were also high,

in view of the extremely low availability of wild flatfish. Farmed 1 kg turbot is

expected to sell at around EUR 15.00/kg, with prices expected to decline again in September when the tourist season

comes to a close.

August is the traditional month of the closure of the Spanish and Italian tuna

canneries, so there is no demand from these buyers for tuna products. Prices

went up for fresh tuna on the European market, however, driven by demand

from restaurants in the southern part of the continent offering tuna steaks and other products.

Fishing in the Western and Central Pacific

continues to be poor during the FAD closure period, while Thai canneries continue to report moderate raw material inventories and production activities.

The two-month IATTC ‘veda’ closure began on 29 July in the Eastern Pacific. About 40% of the

vessels will be tied up during this period. Local canneries continue to report moderate raw material inventory levels. However, as a result of tightening supply from both WCPO and ETP, skipjack and yellowfin prices continue to rise.

Fishing is being affected by bad weather and continues to be poor in the Indian Ocean. Raw

material inventories at local canneries have decreased to the low-to-moderate level. As a result, skipjack prices continue to increase while yellowfin prices remain stable.

6.40

10.65

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

Fresh - whole, cultured 0.5-1kg/pc2-3 kg/pc

EUR/kg

TURBOT (farmed) - in Spain, origin: Spain

1.50

1.45 0.5

1.0

1.5

2.0

2.5

3.0

Skipjack Bangkok CFRSkipjack Ecuador, ex-vessel

USD/kg

TUNA - Pacific Ocean

3

SMALL PELAGICS

Catches in the Atlantic Ocean have improved slightly but continue to be affected by poor

weather. Raw material inventories at local canneries remain at the low-to-moderate level. Both skipjack and yellowfin prices have dropped due to the reduced demand from Europe.

Total imports of processed tuna from extern al countries into the EU

markets reached 167 447 tonnes during January-March 2015, valued

at USD 530.6 million. These figures reflect a reduction of 3.5% in volume and 24% in value compared with the

same time period last year. The top suppliers were Ecuador, Thailand, the

Philippines, Mauritius and China. Of the total imported, 24% (40 635 tonnes) was cooked loins imported

by Spain, Italy, France and Portugal. Imports of cooked loins declined in Spain by 56% but increased by 62% in Italy, making

total EU imports of loin 3.7% higher than the same period last year.

Of the individual markets for processed tuna in the EU, imports increased in the UK (+8%)

and in Germany (+4%), but declined in other EU markets.

During the first quarter of 2015, Norway registered a decline in exports of small pelagics.

The value of exports fell by 31% for herring and 17% for mackerel. Norway exported 47 543 tonnes of herring at an FOB value of NOK 498 million during this period, and 50 094 tonnes of mackerel at an FOB value of NOK 544 million. The average export price per kg

for mackerel fell by 12%, while for herring it increased by almost 20%. Ukraine was the largest market for Norwegian herring during the first quarter, while Turkey was the largest

market for Norwegian mackerel. China and the Republic of Korea remained important markets for Norwegian mackerel, while Nigeria dropped from the second largest market in the first quarter of 2014 to only the fifth in 2015. Indeed, Norwegian mackerel exports to

Nigeria dropped from 7 500 tonnes in the first quarter of 2014 to just half of that in the same period in 2015.

Tighter supplies of small pelagics are expected to see more herring going to direct human

consumption in 2015 than in 2014. It was estimated that roughly 50 000 tonnes of herring was used for reduction purposes (meal and oil) in 2014 as supplies were high and prices low. This year, however, the situation is reversed, as supplies are tighter and prices higher,

making it more profitable to sell herring for human consumption.

1.80

1.15

0.5

1.0

1.5

2.0

2.5

3.0

Yellowfin > 10 kg, Spain CFRSkipjack main sizes, Spain CFR

EUR/kg

TUNA - Spanish canneries

4

CEPHALOPODS

CRUSTACEANS

Squid catches in South Africa are around

250kg per boat per day - still very low. Some scientists said that the possible

reasons for continuing poor catches were the effects of El Nino and that the Agulhas

Current is flowing particularly strongly.

Vessel owners in Galicia, Spain, have asked authorities to extend the octopus fishery ban

in order to allow the resource to recover and rebuild. Owners have further requested that

the ban be implemented for the trawling fleet as well as for those operating traps.

Italian octopus imports rebounded during the first quarter of 2015, after having been relatively stable in 2014. Imports grew from 10 100 tonnes in the first quarter of 2014 to 13 400 tonnes

during the same period in 2015. Morocco strengthened its position as the number one supplier, and Spain and Indonesia both registered increases in export volumes to Italy. Spanish imports of octopus were even stronger, as imports during the first quarter increased by almost 53%,

from 9 100 tonnes in 2014 to 13 900 tonnes in 2015. Again, Morocco was the largest supplier by far, accounting for 59% of total Spanish octopus imports. Mauritania was the second largest

supplier, with 2 400 tonnes, and Portugal came in third place with 1 200 tonnes. Italian squid imports declined during the first three months of the year. Total imports dropped

from 17 600 tonnes to 15 800 tonnes (-10%). Spain, and particularly Thailand, saw reductions in their shipments to Italy. Spanish squid imports have been on a downward trend since 2012,

and this seems to be continuing in 2015. Total squid imports into Spain during the first quarter of 2015 declined by almost 2%, to 16 800 tonnes. The main suppliers were the Falkland Islands

(Malvinas), Morocco and India. While the Falkland Islands (Malvinas) showed a slight (+10%) increase in shipments, both Morocco and India shipped less squid to Spain in the beginning of this year compared with the same period last year.

Crab

Crab prices were firm in July and August due to lower landed volumes coupled with good demand. The fishing season is said to be a month late due to cold water temperatures in spring, and live crustacean stocks are lower as a result. With crab supplies entering the market

relatively late and demand very strong, prices have increased at all levels.

5.80

3.0

4.0

5.0

6.0

7.0

8.0

Squid - Whole, FAS, size M

EUR/kg

SQUID - in Italy, origin: South Africa

5

Lobster

Demand for lobster is very strong,

while the Canadian lobster season is closed and set to reopen in autumn. Consequently, European producers of

lobster have enjoyed an excellent business climate recently. While it is

typical for prices of European lobster to decline during the summer months, this year prices remained relatively

high and are even exhibiting further upward tendencies.

Shrimp

Falling prices of shrimp from exporting countries resulted in import growth in the

European market, with first quarter imports at their highest level in four years. India has overtaken Ecuador as

the number one supplier, with a 2.5% rise in exports to the EU. Compared with

the same period last year, supplies from Ecuador fell by 16%.

Summer demand in Europe has started to improve with better sales being seen,

particularly in the southern regions (Spain, Italy, Portugal and France ), where traditionally the tourist industry

demands large quantities of shrimp for restaurant consumption. Import inquiries

were low in May/July, however, possibly because there were already sufficient

stocks on the market. Importers, who still consider the present market price to be high, are expecting further price

discounts with the anticipated rise in production during July-September.

16.50 10.0

15.0

20.0

25.0

30.0

35.0

400-600/600-800 gr/pc

EUR/kg

EUROPEAN LOBSTER - in Europe, origin: Ireland

8.70

7.40

7.10 6.90

3.0

4.5

6.0

7.5

9.0

10.5

> 10-20 pc/kg > 20-30 > 30-40 > 40-60

EUR/kg

ARGENTINA RED SHRIMP - origin: Argentina

EUR/kg

ARGENTINA RED SHRIMP - origin: Argentina

8.20

6.70

5.60

4.40 3.3

4.8

6.3

7.8

9.3

10.8

30-40 pc/lb 40-50 60-70 100-120

EUR/kg

WHITELEG SHRIMP - origin: Central America

6

BIVALVES

SALMON

During the first quarter of 2015, EU imports of mussels declined by 9% compared with the

same period the year before, down to 42 600 tonnes. This reflects a continued import decline trend.

The French Bouchot mussel season was well under way by the end of July and these mussels

are being featured as a promotional item in many supermarket catalogues.

EU scallop imports during the first quarter period totaled 10 000 tonnes, the lowest ever

observed over the past five year period. The peak was noted in 2010’s first quarter with 14 200 tonnes imported. Imports into France, the EU’s top importer, dropped by 17% during

the first quarter compared with the same time period last year. This decline points to an overall weakening in household demand, likely due to the price rise. EU imports from external EU suppliers have declined relatively more (-14%) compared with internal EU

trade (-5%) when comparing the first quarter 2015 with the first quarter of 2014.

Large-sized oysters are relatively abundant this year due to a warm autumn in 2014 and as a result of the Russian embargo. Summer survival rates will be paramount in orientating the fourth quarter market, although latest reports indicate a more stable situation than previous

years.

An appreciation of the euro versus the krone and a reduction in harvest volumes at Norwegian farms has seen prices for Norwegian Atlantic salmon maintained at levels significantly higher than those seen in the same period in 2014. According to the NASDAQ salmon index, the

average price of fresh whole Atlantics exported from Norway in week 31 was NOK 44.25/ kg, more than 22% higher than the same week last year. This price increase has been driven by

reduced biomass following the clearing of what was a relative surplus of fish in the pens in the first half of the year together with currency shifts favouring exporters and slower growth rates resulting from lower sea temperatures. In particular, large fish, which were plentiful in the first

half of 2015, are now in short supply, and prices for these sizes have been pushed sharply upwards. For 8-9kg fish, the NASDAQ index recorded prices approaching NOK 60/kg in week 31.

So far, it appears that demand has not been overly affected by high prices and core markets in the EU are performing well. France, which has been a somewhat challenging market for

Norwegian exporters over recent years, posted an 8% increase in import volumes in June at prices almost 11% higher than the same month in 2014. According to the Norwegian Seafood

Council, the total value of salmon exports in July was NOK 3.8 billion, 9% higher than the same month last year. The EU as a whole absorbed 373 000 tonnes of salmon worth NOK 16 billion in

the first half of 2015. The US and Asian markets are also in good shape, importing 20% and 38% more salmon in volume terms in the first half of the year, although at lower prices. The UK farmed salmon industry, however, has not fared as well, posting total export volumes for the

7

TROUT

FRESHWATER FISH

first half of 2015 around 20% lower than the same period last year, despite a drop in price.

Significantly lower imports by China and the US was the primary reason for the reduced volumes, with the US now increasingly looking to Norway and Canada for its supply of fresh

salmon. The seasonal drop in prices following end-of-summer harvesting can still be expected to occur,

but the outlook for the rest of the year is positive for prices. Fish Pool forward prices are now in the low NOK 40s for the majority of the second two quarters, as lower total biomass and smaller

fish in the pens suggest there is not currently much scope for an increase in supply.

The Russian ban on Western food imports continues to negatively affect the Norwegian trout

industry. The price for fresh whole trout for the first half of 2015 was 13% lower than for the same period of 2014, while total export volume was some 18% down. Exports to Belarus have

increased significantly since the entering into force of the embargo, although Russian authorities have recently expressed concern that this may include fish that subsequently enter the Russian

market.

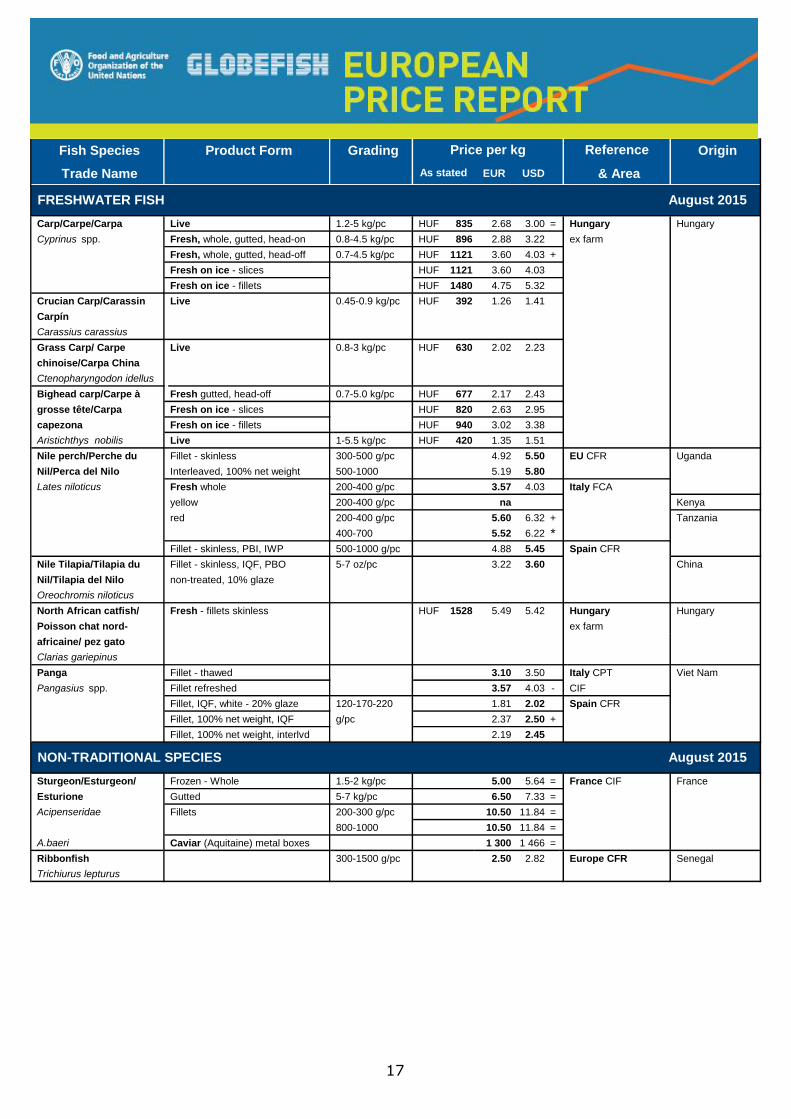

An increase in catches of Nile perch in Lake Victoria has led to good supply on the European fresh fish market. Prices

have started to trend downwards, and some supermarkets are offering Nile

perch at reduced prices. In addition, the devaluation of the Tanzanian currency has permitted lower offer prices.

In Hungary, both supply and demand for

carp have significantly decreased, as is typical for the mid-summer. Prices are

temporarily unstable.

Tilapia demand has improved and prices picked up from their low level reached in June

Pangasius demand from the European has weakened despite the price level which has remained relatively moderate.

3.30

2.90

1.5

2.0

2.5

3.0

3.5

Trout: Salmo spp Rainbow Trout: Oncorhynchus mykiss

EUR/kg

TROUT - Ex-farm prices in Italy

8

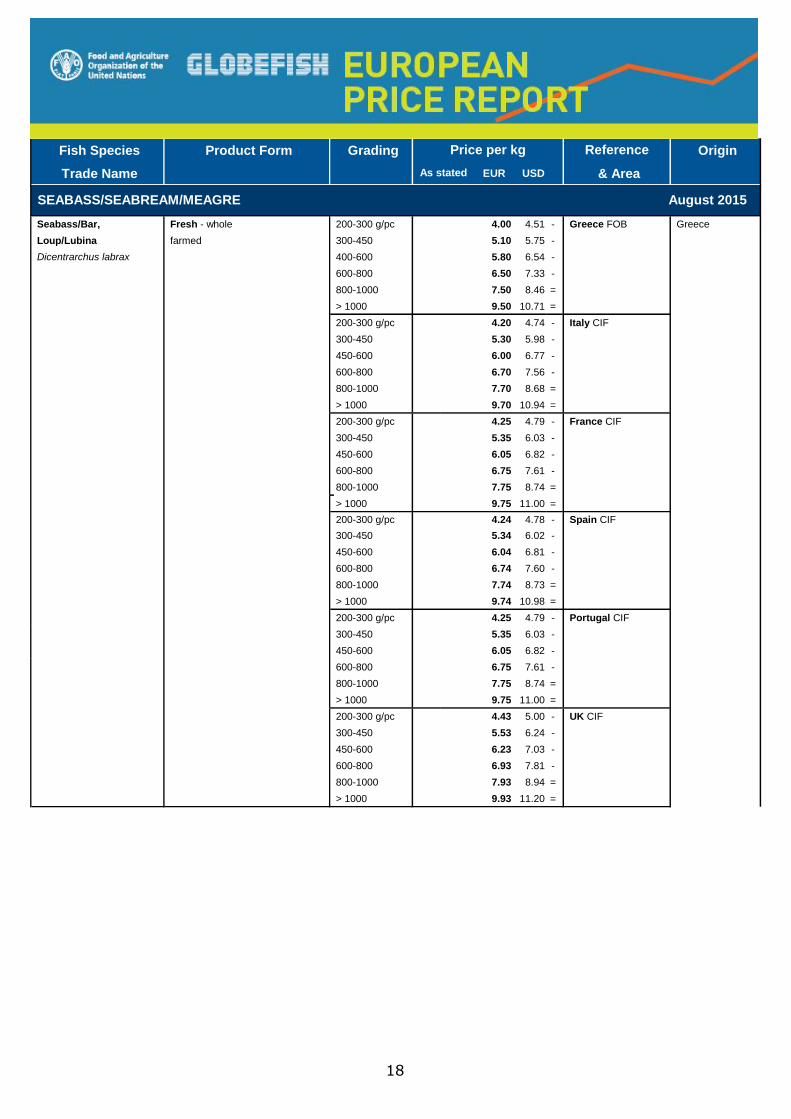

SEABASS – SEABREAM - MEAGRE

In general seabass prices tended downward over the last month, but

remain relatively high. In the Orbetello (Italy) area seabass and seabream had

to be harvested as an emergency action in view of extremely high water temperatures and low oxygen content.

As a result small seabass and seabream were widely available on the market. On

the other hand, large seabass, bigger than 2 kg, were selling at higher prices, as it is a preferred fish for restaurants

and is sometimes even sold as wild species, generally commanding higher prices.

Greek exports of bass and bream for the first half of 2015 were down around 10% in volume terms, as farm production levels are throttled back this year. This has had an overall positive

effect on prices, as expected, particularly for bream. Due to a surplus of Turkish fish on the market in the first half of the year, the price increase was somewhat delayed, but going into the

2nd quarter it is clearly evident in core markets such as Italy. Recent news suggesting a new bailout deal for Greece is close to being agreed will provide some further relief for Greek aquaculture companies, who have been struggling with a range of difficulties related to the

unstable economic situation. Turkish producers, meanwhile, have been benefitting from favourable exchange rates, rapid expansion in old and new markets and the recent firming of

prices. The only significantly worse performer out of Turkish bass and bream importers was Russia, where a poor economic environment has harmed consumer spending. Supply in Turkey is also expected to tighten in the second two quarters of 2015 following relatively high export

volumes in the first six months, and this should see prices remain seasonally high following the typical post-summer drop in demand.

5.30

5.70

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Seabass fresh whole 300-450 gr/pc Seabream fresh whole 300-450 gr/pc

EUR/kg

SEABASS/SEABREAM - in Italy origin: Greece

EUR/kg

SEABASS/SEABREAM - in Italy origin: Greece

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

Cod/Cabillaud, Morue/ Fresh gutted 1.17 1.31 + Poland FOB Baltic Sea

Bacalao IQF portion, single frozen 100-150 g/pc 7.05 7.95 - Italy CIF Iceland

Gadus morhua Fresh - fillet 100-200 g/pc 3.94 4.44 CPT Denmark

200-400 6.00 6.77

Fresh - Whole 1-2 kg/pc 5.28 5.96

2-4 5.83 6.57

Single frozen Europe DDP Norway

Industrial block

Fillet - light salted, skin-on, IQF 500-1000 g/pc 3.80 4.25 CFR China

100% net weight

Minced - baby food grade

Fillet - wet salted - 1st quality 700-1000 g/pc 9.00 10.15 = Italy DDP Iceland

produced from fresh raw material

Stockfish 700 g/pc 22.50 25.37 = Norway

Fillet skinless 300-600 g/pc 7.30 8.23 Spain CIF

400-600 9.30 10.49

600-800 9.75 11.00

900-1300 12.45 14.04 * DDP

900-1300 13.05 14.72 * Netherlands

Gadus macrocephalus Fillet - wet salted - 1st quality 400-700 g/pc 7.90 8.91 + Italy CIP Denmark

produced from frozen raw material

Hake/Merlu/Merluza Minced block 1.58 1.78 = Namibia FOB Namibia

Merluccius capensis for Spanish market

H&G, IWP 100-200 g/pc Spain FOB

350-500

500-800

Fillet skin on 2-4 oz/pc 2.80 3.16 - DDP

4-6 3.20 3.61 -

6-8 3.45 3.89 -

8-12 3.75 4.23 -

IQF portion, trapeze 90-110 g/pc 5.95 6.71 + Italy CIF

Merluccius hubbsi H&G 150-250 1.58 1.78 Argentina

Fillet - skinless 80-120 g/pc 3.06 3.45

skin-on 2.98 3.36

Merluccius merluccius Fresh - whole 100-200 g/pc 3.70 4.17 CPT Croazia

200-300 4.70 5.30

Fresh - gutted 300-400 5.56 6.27

Merluccius productus Fillet, PBO 2.15 2.40 = Spain CIF USA

Alaska pollack/Lieu Industrial block single frozen na Europe CFR

de l'Alaska/Colín Industrial block double frozen na China

de Alaska Fillet, IQF 2-4 oz

Theragra chalcogramma Fillet, baby food quality 3.49 3.94 + DDP USA

H&G >25 1.21 1.36 Russian Fed.

>30 1.30 1.47 wholesale Vladivostok

>30 1.53 1.73 wholesale Moscow

Surimi (Alaska pollack) Stick - Paprika 250 g/pc 2.46 2.77 France CFR Spain

Hoki H&G 100-300 g/pc 1.63 1.84 Spain FOB

Macruronus magellanicus 300-500 1.63 1.84

500-900 1.63 1.84

Saithe/Lieu noir/ Fillet - interleaved 200-400 g/pc Europe CIF Faroe Islands

Carbonero (Pollock, Coley)

Pollachius virens Fillet - skinless, PBI, interleaved 16-32 oz/pc 5.30 5.98 = Spain DDP Iceland

Reference

August 2015

Price per kg

As stated

GROUNDFISH

no quotation

no quotation

no quotation

no quotation

9

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Monkfish/Baudroie/ Fresh - Tail < 0.3 kg/pc 6.29 7.10 Italy CPT UK

Rape 0.3-0.5 7.87 8.87

Lophius spp. 0.5-1 10.25 11.56

1-2 11.54 13.02

> 2 13.02 14.68

Tails, skinless 100-250 g/pc 5.75 6.48 = Spain DDP Namibia

Frozen at land 250-500 6.75 7.61 =

100% net weight 500-1000 8.25 9.30 +

> 1000 9.25 10.43 +

Haddock/Eglefin/Eglofino H&G < 0.8 kg/pc NOK 14.00 1.54 1.72 = Sweden FCA Norway

Melanogrammus Fresh 1-1.5 kg/pc 5.20 5.86 * Spain DDP

aeglefinus > 1.5 3.30 3.72 *

> 2 3.70 4.17 *

Ling/Lingue franche/ Fillet - wet salted 1-1.5 kg/pc 4.95 5.58 + Italy DDP Faeroe Islands

Maruca Produced from fresh raw material

Molva molva 1st quality

John Dory/ Frozen skin-on 60-100 g/pc 4.07 4.55 Germany CFR China

Sainte Pierre IQF, 20% glaze 100-150 4.38 4.90

Pez de San Pedro 150-200 4.74 5.30

Zeus faber 200-300 4.92 5.50

300-400 5.23 5.85

1000-2000 20.05 22.61 * Spain DDP Spain

2000-3000 22.25 25.09 *

Headless Small 2.10 2.37 Mauritania FOB Mauritania

Medium 3.30 3.72 for European market

Large 3.50 3.95

Turbot/Rodaballo Fresh - whole 0.5-1 kg/pc 6.40 7.22 Spain CIF Spain

Psetta maxima cultured 1-2 7.90 8.91

2-3 10.65 12.01

3-4 16.90 19.06

Fresh - whole < 0.5 kg/pc 6.70 7.56 + Netherlands

wild 0.4-0.6 na

0.5-1 11.10 12.52 +

1-2 18.00 20.30 +

2-3 18.80 21.20 +

3-4 23.20 26.16 +

4-6 25.15 28.36 +

Fresh - whole 0.4-0-6 kg/pc 5.66 6.38 Italy CPT Spain/Portugal

0.8-1 6.00 6.77

1-1.5 6.00 6.77

1.5-2 7.90 8.91

2-2.5 10.90 12.29

2.5-3 11.00 12.40

3-4 16.80 18.95

wild 0.3-0.5 kg/pc 5.04 5.68 Netherlands

0.5-1 7.74 8.73

0.7-1 7.73 8.72

1-2 10.42 11.75

2-3 12.05 13.59

> 4 14.00 15.79

FLATFISH

GROUNDFISH (cont.) August 2015

August 2015

10

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Sole/Sole/ Fresh - whole < 170 g/pc 12.15 13.70 + Spain CIF Netherlands

Lenguado wild 170-220 14.15 15.96 +

Solea vulgaris 200-300 15.25 17.20 +

300-400 21.85 24.64 +

400-500 22.95 25.88 +

500-600 29.55 33.32 +

Fresh - whole No. 2 19.50 21.99 Italy CPT

No. 3 12.45 14.04

No. 4 11.45 12.91

Fresh - gutted No. 2 17.48 19.71 +

No. 3 14.04 15.83 +

No. 4 13.50 15.22 +

No. 5 na

Fresh - whole No. 2 14.91 16.81 CIF

No. 3 14.15 15.96

No. 4 9.92 11.19

European plaice/ Fresh - whole 300-400 g/pc 3.40 3.83 * Spain CIF

Plie d'Europe/ 400-600 3.70 4.17 *

Solla europea > 600 4.50 5.07 *

Pleuronectes platessa IQF, white skin-on, 25% glaze No. 2 4.65 5.24 + Netherlands FOB

IQF skin-off, 25% glaze 4.95 5.58 - for Italian market

European Flounder/ Fresh - fillets skin-on Large 4.18 4.71 Italy CPT

Flet d'Europe/ skinless Large 5.01 5.65

Platija europea 1.68 1.89 FCA

Platichthys flesus Fresh - whole 0.31 0.35 + Poland FOB Baltic Sea

Greenland Halibut/ Fillet - skinoff, boneless, Denmark FOB Greenland

Reinhardtius blockfrozen

hippoglossoides

Tuna/Thon/Atún Skipjack - whole main size 1.34 1.50 + Bangkok CFR Western/Central

Thunnus spp. Pacific Ocean

Skipjack - whole 1.30 1.45 + Ecuador Eastern Tropical

Yellowfin - whole 1.52 1.70 + ex-vessel Pacific Ocean

Skipjack - whole main size 1.25 1.41 + Seychelles Indian Ocean

Yellowfin - whole 1.70 1.92 = FOB

Skipjack - whole 1.00 1.13 + Abidjan Atlantic Ocean

Yellowfin - whole > 10 kg 1.65 1.86 - ex-vessel

Skipjack - whole 1.8-3.4 kg/pc 1.15 1.30 + Spanish Various origins

Yellowfin - whole > 10 kg 1.80 2.03 = Canneries CFR

Skipjack - cooked & cleaned double cleaned 3.89 4.35 = Italy DDP Solomon Islands

loins - vacuum packed

Yellowfin - cooked & cleaned double cleaned 5.37 6.00 = Kenya/Mauri-

loins - vacuum packed tius/Solomon Is.

Yellowfin - whole 3-10 kg 1.38 1.52 Spain DAT Indian Ocean

Bigeye - whole > 10 kg 1.60 1.76

Yellowfin - whole > 10 kg 1.85 2.04 Atlantic Ocean

Skipjack - whole > 3.5 kg 1.10 1.21

Yellowfin - frozen loins 4.50 4.96 DDP Eastern Pacific

Skipjack - frozen loins 3.60 3.97 Ocean

Bigeye - frozen loins 3.80 4.19

Skipjack > 1.8 kg/pc 1.28 1.41 Tunisia CFR France

TUNAS/BILLFISHES

No quotations

FLATFISH (cont.) August 2015

August 2015

11

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Tuna/Thon/Atún Skipjack - pre-cooked loins 4.43 4.95 + Europe CFR Ecuador

Thunnus spp. Yellowfin - pre-cooked loins double cleaned 5.46 6.10 +

single cleaned 5.37 6.00 +

Skipjack - whole 1.9-3.4 kg/pc 0.89 1.00 Ecuador FOB

3.5-5 0.98 1.10

Skipjack - pre-cooked loins 4.43 4.95 +

Swordfish/Espadon/ Frozen at sea, DWT 30-50 kg/pc 7.30 8.23 + Spain FOT Spain

Pez espada 100% net weight 50-70 7.20 10.00 +

Xiphias gladius Fresh - whole < 12 kg/pc 9.49 13.18 Italy FCA

Mediterranean 13-18 9.63 13.38

19-25 9.63 13.38

Atlantic 26-35 9.04 12.56

36-50 9.04 12.56

> 50 8.09 11.24

Mackerel/Maquereau/ Fresh - whole 4-6 pc/kg 2.50 2.82 Italy CPT France

Caballa Fresh - Fillets 4.20 4.74

Scomber scombrus butterfly cut

Whole 200-400 g/pc Netherlands/Poland UK

300-500 FOB

H&G > 200 g/pc na for Eastern Europe Greenl./Faroe. I

Whole 3-4 pc/kg 1.05 1.18 Spain FOB Spain

Whole 1-3 pc/kg 0.87 0.98 Tunisia FOB Tunisia

for European market

Herring/Hareng/Arenque Fresh - fillet 2.62 2.95 Italy CPT Denmark

Clupeidae 250-300 g/pc 1.03 1.16 Russian Fed. Russian Fed.

> 300 1.21 1.36 wholesale Moscow

>250 0.99 1.12 wholesale Vladivostok

>300 1.15 1.30

Fresh - whole 70-100 g/pc 0.14 0.16 - Poland FOB Baltic

Sprat/Sprat/Espadín 0.14 0.16 =

Sprattus sprattus

Sardine/Sardine/Sardina Fresh - whole 1.00 1.13 Italy CPT Croatia

Sardina pilchardus 1.15 1.30 Italy

IQF 9-10.5 cm na Tunisia FOB Tunisia

for European market

CEPHALOPODS

Squid/Encornet/Calamar Whole S (< 18 cm) 5.60 6.32 = Italy CIF South Africa

Loligo spp. M (18-25) 5.80 6.54 +

L (25-30) 5.90 6.65 -

XL (>30) 5.90 6.65 -

Loligo gayi Whole 18-22 cm 4.95 5.58 Spain FCA Falkland/

15-18 4.95 5.58 Malvinas Is.

12-16 4.95 5.58

Loligo vulgaris Whole 2 small 5.20 5.86 Mauritania FOB Mauritania

3 small 4.50 5.07 for European market

4 small 4.00 4.51

small 5.70 6.43

medium 6.00 6.77

large 6.10 6.88

August 2015

SMALL PELAGICS August 2015

TUNAS/BILLFISHES (cont.)

August 2015

No quotations

12

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Squid/Encornet/Calamar Whole cleaned, < 10 3.58 4.00 Germany CFR India

Loligo duvacelli 2 kg blocks -20% glaze 11-20 3.31 3.70

Loligo chinensis < 3 4.16 4.65 China

3-6 3.40 3.80

6-10 2.95 3.30

10-15 2.59 2.90

15-20 2.24 2.50

Dosidicus gigas Raw fillet 2-4 kg/pc 0.89 0.99 Europe CFR Chile

0.94 1.05 Peru

Raw tentacle 1-2, 2-3 kg/pc 0.89 0.99 Chile

0.92 1.03 Peru

Raw wings 0.54 0.60 Chile

whole without cartilage 0.67 0.75 Peru

Necks 0.58 0.65 Chile

open with cartilage 0.76 0.85 Peru

Darum membraneless 1.70 1.90

Boiled wings - skin-on 0.91 1.02

Squid rings - thawed 2.41 2.72 Italy CPT

Squid stripes - thawed 1.50 1.69

Tentacles 1.70 1.92

Octopus/Poulpe/Pulpo Whole - FAS T1 9.25 10.43 Morocco FOB, Morocco

Octopus vulgaris T2 8.25 9.30 for Spanish market

T3 7.05 7.95

T4 6.45 7.27

T5 5.65 6.37

IQF, 10% glazing T3 8.00 8.82 for Italian market

T4 7.40 8.16

T5 7.10 7.83

T6 6.40 7.06

T7 5.60 6.18

Sushi slice 7 g/pc 12.79 14.30 = Europe CFR Indonesia

100% net weight 9 g 12.79 14.30 =

boiled cut 7.92 8.85 +

100% net weight

Flower type 1-2 kg/pc 4.38 4.90 +

90% net weight >2 4.65 5.20 +

Cuttlefish/Seiche/ Whole, cleaned, IQF < 10 pc/kg 3.94 4.40 Germany CFR India

Sepia 20% glaze 11-20 3.27 3.65

Sepia spp. Fresh - whole 100-200 g/pc na Italy CPT France/UK

200-300 4.15 4.68

500-1000 3.92 4.42

600-1200 3.25 3.67

trap caught 500-1000 3.45 3.89

August 2015 CEPHALOPODS (cont.)

13

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

CRUSTACEANS

Whiteleg shrimp/ PD, chemical treatment 31-40 pc/lb 9.39 10.50 + Europe CFR Indonesia

Crevette pattes 100% net weight 41-50 8.59 9.60 +

blanches/Camarón treated with non-phosphate 51-60 8.32 9.30 +

patiblanco 61-70 7.60 8.50 +

Penaeus vannamei 71-90 7.43 8.30 +

91-120 7.07 7.90 +

Raw, PD 16-20 pc/lb 7.96 8.90 India

IQF, 20% glaze 21-25 6.98 7.80

26-30 6.53 7.30

31-40 5.90 6.60

41-50 5.59 6.25

51-60 5.37 6.00

61-70 5.19 5.80

C&P, deveiled, tail-off 41-60 pc/lb 6.35 7.10 Viet Nam

IQF, 20% glaze 61-80 6.08 6.80

Head-on, shell-on 20-30 pc/kg 9.39 10.50 Central

30-40 7.34 8.20 America

40-50 5.99 6.70

50-60 5.46 6.10

60-70 5.01 5.60

70-80 4.47 5.00

80-100 4.25 4.75

100-120 3.94 4.40

120-140 3.49 3.90

Head-on, shell-on 30-40 pc/kg 7.51 8.40 South/Central

40-50 6.26 7.00 America FOB

50-60 5.37 6.00 for European main

60-70 5.10 5.70 ports

70-80 4.56 5.10

80-100 3.94 4.40

> 100 3.85 4.30

Argentine red shrimp/ Head-on, shell-on 10-20 pc/kg 8.70 9.81 = Spain EXW Argentina

Salicoque rouge/ 20-30 7.40 8.34 =

d'Argentine/Camarón 30-40 7.10 8.01 =

langostín argentino 40-60 6.90 7.78 =

Pleoticus muelleri

Black tiger/Crevette Headless 8-12 pc/lb 9.39 10.50 - Europe/ Bangladesh

tigrée/Camarón tigre 20% glaze, IQF 13-15 8.77 9.80 - Russian Fed.

Penaeus monodon 16-20 6.98 7.80 - CFR

21-25 6.04 6.75 -

Head-On, Shell on 8-12 pc/lb 10.56 11.80 * Germany CFR

20% glaze semi IQF 13-15 9.48 10.60 *

16-20 7.34 8.20 *

21-30 5.19 5.80 *

31-40 4.83 5.40 *

Headless, Shell on, easy peel 8-12 pc/lb 11.18 12.50 *

20% glaze, IQF 13-15 8.36 9.35 *

16-20 6.62 7.40 *

Common shrimp/ Fresh 28.50 32.14 + Spain CIF Netherlands

Crevette grise/Quisquilla

Crangon crangon

August 2015

14

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Norway lobster/ 4X1.5 kg 4-7 26.80 28.51 - Spain CIF Netherlands

Langoustine/Cigala 6-9 21.85 23.24 -

Nephrops norvegicus 8-12 20.20 21.49 -

11-15 18.00 19.15 -

16-20 15.20 17.14 +

21-30 14.10 15.90 +

31-40 10.30 11.62 -

41-50 7.55 8.51 -

Tails 40-60 13.60 15.34 -

Whole 00 12.38 13.96 Scotland

0 10.38 11.71

1 9.38 10.58

2 8.38 9.45

3 7.38 8.32

4 6.38 7.19

5 5.15 5.81

Fresh - whole 6-9 pc/kg 16.73 18.87 Italy CPT Denmark/

11-15 13.00 14.66 UK

16-20 10.70 12.07

21-30 8.50 9.59

41-50 4.92 5.55

European lobster/ Live - bulk 400-600 g/pc 17.00 19.17 + France delivered Ireland

Homard européen/ 600-800 17.00 19.17 + to French vivier

Bogavante Fresh - whole Large 16.00 18.04 Italy CPT UK

Homarus gammarus small 20.00 22.55 France

American lobster/ Live > 800 g/pc 16.24 18.31 Canada

Homard américain/ Fresh 250-350 12.22 13.78

Bogavante americano Popsicle < 450 g/pc CAN 17.20 14.00 12.55 Canada FOB

Homarus americanus (canner size) for European mkt

> 450 CAN 18.20 14.00 12.55

(market size)

Whole cooked netted lobster canners CAN 16.70 12.85 11.52

market CAN 17.95 13.81 12.38

Edible crab/Tourteau/ Live T2 2.60 2.93 + France Auction France

Buey de mar 13-16 cm

Cancer pagurus

BIVALVES

Oyster/Huître/Ostra Live No. 3 4.50 6.09 = France prod. Price/ Ireland/France

Crassostrea gigas average export price

60-100 g/pc 14.00 18.95 * Spain DDP Netherlands

Mussel/Moule/Mejillón Live - Bottom mussel 2.10 2.37 = France wholesale France

Mytilus edulis 1.80 2.03 = Netherlands

Mytilus galloprovincialis Live - Rope 60-80 pc/kg 2.00 2.26 = Spain

Mytilus chilensis IQF - shell-off, 7% glaze 200-300 pc/kg 4.40 4.96 + Italy CIF Chile

Cooked mussel meat IQF 100-200 pc/kg 2.91 3.25 France CIF

200-300 2.82 3.15

300-500 2.77 3.10

Cooked mussel whole shell, IQF 80-100 pc/kg 1.97 2.20

Razor shell/Couteau/ Live S 8.55 9.64 - Spain CIF Ireland

Navajas - Solenidae M 7.65 8.63 -

10-12 cm 4.10 4.62 * DDP Netherlands

CRUSTACEANS (cont.)

August 2015

August 2015

15

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

SALMON

Atlantic salmon/ Fresh - gutted, head-on 2-3 kg/pc 3.80 4.29 France CIF Scotland

Saumon de l'Atlantique/ Superior quality 3-4 5.30 5.98

Salmón del Atlántico 4-5 5.30 5.98

Salmo salar 5-6 5.10 5.75

> 6 5.10 5.75

Fresh - gutted, head-on 2-3 kg/pc 4.30 4.85 Norway

Superior quality 3-4 4.70 5.30

4-5 4.70 5.30

5-6 4.70 5.30

> 6 4.70 5.30

gutted, head-on 4-5 kg/pc 4.90 5.53 Tunisia CFR

5-6 4.90 5.53

Fresh - salmon cubes 8x8x8 9.73 10.97 Europe CFR

IQF - salmon slices 9.90 11.16

Fresh - Whole - Superior 2-3 kg/pc na Italy FCA

3-4 4.64 5.23

4-5 4.68 5.28

5-6 4.68 5.28

6-7 4.57 5.15

7-8 4.43 5.00

8-9 na

9-10 na

3-4 5.32 6.00 CIF

4-5 5.45 6.15

5-6 5.35 6.03

IQF portion 100-150 g/pc 10.10 11.39 = Denmark

Head-on, gutted, grade 1 6-7 kg/pc 5.08 5.73 Denmark DDP Chile

Fillet, interleaved 1-2 lb/pc 4.87 5.49

2-4 4.17 4.70

Fillet, VAC 1-2 lb/pc 6.10 6.88

3-4 6.15 6.94

Fillet, IQF 2-3 lb/pc 6.15 6.94

4-5 6.88 7.76

Bits and pieces 5.81 6.50 Europe CIF

scapped meat 4.20 4.70

TROUT

Trout/Truite/Trucha Whole, gutted, fresh on ice 0.25-0.4 kg/pc HUF 1332 4.28 4.78 * Hungary ex-farm Hungary

Salmo trutta Fillet - farmed 200-400 g/pc 7.90 8.91 + Italy ex-farm Italy

Live - farmed 500-700 g/pc 3.40 3.83 +

Rainbow trout/ Live - farmed 250-400 g/pc 2.90 3.27 =

Truite arc-en-ciel/ Gutted 250-400 g/pc 4.10 4.62 +

Trucha arco iris

Oncorhynchus mykiss

August 2015

August 2015

16

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Carp/Carpe/Carpa Live 1.2-5 kg/pc HUF 835 2.68 3.00 = Hungary Hungary

Cyprinus spp. Fresh, whole, gutted, head-on 0.8-4.5 kg/pc HUF 896 2.88 3.22 ex farm

Fresh, whole, gutted, head-off 0.7-4.5 kg/pc HUF 1121 3.60 4.03 +

Fresh on ice - slices HUF 1121 3.60 4.03

Fresh on ice - fillets HUF 1480 4.75 5.32

Crucian Carp/Carassin Live 0.45-0.9 kg/pc HUF 392 1.26 1.41

Carpín

Carassius carassius

Grass Carp/ Carpe Live 0.8-3 kg/pc HUF 630 2.02 2.23

chinoise/Carpa China

Ctenopharyngodon idellus

Bighead carp/Carpe à Fresh gutted, head-off 0.7-5.0 kg/pc HUF 677 2.17 2.43

grosse tête/Carpa Fresh on ice - slices HUF 820 2.63 2.95

capezona Fresh on ice - fillets HUF 940 3.02 3.38

Aristichthys nobilis Live 1-5.5 kg/pc HUF 420 1.35 1.51

Nile perch/Perche du Fillet - skinless 300-500 g/pc 4.92 5.50 EU CFR Uganda

Nil/Perca del Nilo Interleaved, 100% net weight 500-1000 5.19 5.80

Lates niloticus Fresh whole 200-400 g/pc 3.57 4.03 Italy FCA

yellow 200-400 g/pc na Kenya

red 200-400 g/pc 5.60 6.32 + Tanzania

400-700 5.52 6.22 *Fillet - skinless, PBI, IWP 500-1000 g/pc 4.88 5.45 Spain CFR

Nile Tilapia/Tilapia du Fillet - skinless, IQF, PBO 5-7 oz/pc 3.22 3.60 China

Nil/Tilapia del Nilo non-treated, 10% glaze

Oreochromis niloticus

North African catfish/ Fresh - fillets skinless HUF 1528 5.49 5.42 Hungary Hungary

Poisson chat nord- ex farm

africaine/ pez gato

Clarias gariepinus

Panga Fillet - thawed 3.10 3.50 Italy CPT Viet Nam

Pangasius spp. Fillet refreshed 3.57 4.03 - CIF

Fillet, IQF, white - 20% glaze 120-170-220 1.81 2.02 Spain CFR

Fillet, 100% net weight, IQF g/pc 2.37 2.50 +

Fillet, 100% net weight, interlvd 2.19 2.45

Sturgeon/Esturgeon/ Frozen - Whole 1.5-2 kg/pc 5.00 5.64 = France CIF France

Esturione Gutted 5-7 kg/pc 6.50 7.33 =

Acipenseridae Fillets 200-300 g/pc 10.50 11.84 =

800-1000 10.50 11.84 =

A.baeri Caviar (Aquitaine) metal boxes 1 300 1 466 =

Ribbonfish 300-1500 g/pc 2.50 2.82 Europe CFR Senegal

Trichiurus lepturus

FRESHWATER FISH August 2015

August 2015 NON-TRADITIONAL SPECIES

17

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Seabass/Bar, Fresh - whole 200-300 g/pc 4.00 4.51 - Greece FOB Greece

Loup/Lubina farmed 300-450 5.10 5.75 -

Dicentrarchus labrax 400-600 5.80 6.54 -

600-800 6.50 7.33 -

800-1000 7.50 8.46 =

> 1000 9.50 10.71 =

200-300 g/pc 4.20 4.74 - Italy CIF

300-450 5.30 5.98 -

450-600 6.00 6.77 -

600-800 6.70 7.56 -

800-1000 7.70 8.68 =

> 1000 9.70 10.94 =

200-300 g/pc 4.25 4.79 - France CIF

300-450 5.35 6.03 -

450-600 6.05 6.82 -

600-800 6.75 7.61 -

800-1000 7.75 8.74 =

> 1000 9.75 11.00 =

200-300 g/pc 4.24 4.78 - Spain CIF

300-450 5.34 6.02 -

450-600 6.04 6.81 -

600-800 6.74 7.60 -

800-1000 7.74 8.73 =

> 1000 9.74 10.98 =

200-300 g/pc 4.25 4.79 - Portugal CIF

300-450 5.35 6.03 -

450-600 6.05 6.82 -

600-800 6.75 7.61 -

800-1000 7.75 8.74 =

> 1000 9.75 11.00 =

200-300 g/pc 4.43 5.00 - UK CIF

300-450 5.53 6.24 -

450-600 6.23 7.03 -

600-800 6.93 7.81 -

800-1000 7.93 8.94 =

> 1000 9.93 11.20 =

SEABASS/SEABREAM/MEAGRE August 2015

18

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Seabass/Bar, Fresh - whole 200-300 g/pc 4.27 4.82 - Germany CIF Greece

Loup/Lubina farmed 300-450 5.37 6.06 -

Dicentrarchus labrax 450-600 6.07 6.85 -

600-800 6.77 7.63 -

800-1000 7.77 8.76 =

> 1000 9.77 11.02 =

200-300 g/pc 4.40 4.96 = Italy CIF

300-450 5.80 6.54 -

450-600 6.50 7.33 =

600-800 6.90 7.78 -

800-1000 9.00 10.15 =

1000-1500 10.50 11.84 -

> 1500 12.00 13.53 -

> 2000 15.50 17.48 +

200-300 g/pc 4.40 4.96 Spain CIF Canary Island

300-400 4.70 5.30 (Spain)

400-600 5.70 6.43

600-800 7.91 8.92

800-1000 10.21 11.51

Fresh - whole - wild 1000-2000 g/pc 23.50 26.50 Italy FCA Morocco

Atlantic > 2000 24.50 27.63

> 3000 24.00 27.06

Fresh - whole - wild 400-600 g/pc na CPT Egypt

Mediterranean 600-800 12.72 14.34

800-1000 12.92 14.57

1000-2000 13.00 14.66

> 2000 13.14 14.82

> 3000 13.33 15.03

Farmed - Orbetello Large 10.70 12.07 FCA Italy

Medium 9.70 10.94

Small na

August 2015 SEABASS/SEABREAM/MEAGRE (cont.)

19

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

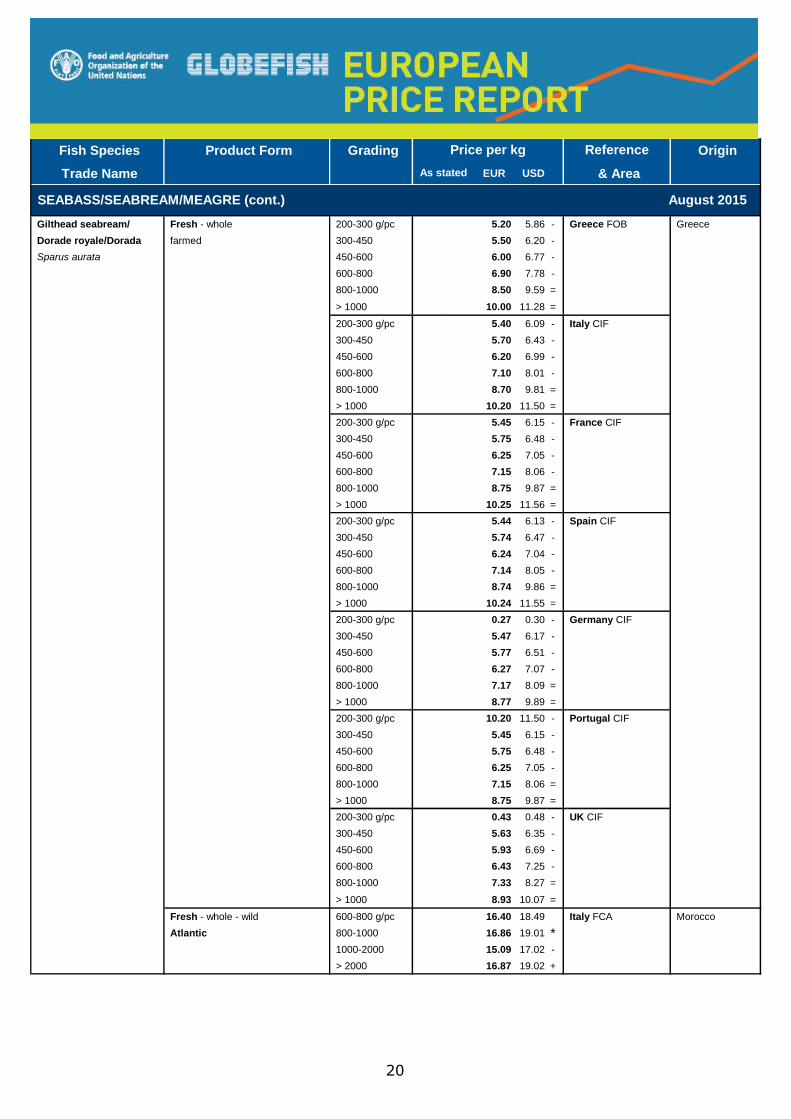

Gilthead seabream/ Fresh - whole 200-300 g/pc 5.20 5.86 - Greece FOB Greece

Dorade royale/Dorada farmed 300-450 5.50 6.20 -

Sparus aurata 450-600 6.00 6.77 -

600-800 6.90 7.78 -

800-1000 8.50 9.59 =

> 1000 10.00 11.28 =

200-300 g/pc 5.40 6.09 - Italy CIF

300-450 5.70 6.43 -

450-600 6.20 6.99 -

600-800 7.10 8.01 -

800-1000 8.70 9.81 =

> 1000 10.20 11.50 =

200-300 g/pc 5.45 6.15 - France CIF

300-450 5.75 6.48 -

450-600 6.25 7.05 -

600-800 7.15 8.06 -

800-1000 8.75 9.87 =

> 1000 10.25 11.56 =

200-300 g/pc 5.44 6.13 - Spain CIF

300-450 5.74 6.47 -

450-600 6.24 7.04 -

600-800 7.14 8.05 -

800-1000 8.74 9.86 =

> 1000 10.24 11.55 =

200-300 g/pc 0.27 0.30 - Germany CIF

300-450 5.47 6.17 -

450-600 5.77 6.51 -

600-800 6.27 7.07 -

800-1000 7.17 8.09 =

> 1000 8.77 9.89 =

200-300 g/pc 10.20 11.50 - Portugal CIF

300-450 5.45 6.15 -

450-600 5.75 6.48 -

600-800 6.25 7.05 -

800-1000 7.15 8.06 =

> 1000 8.75 9.87 =

200-300 g/pc 0.43 0.48 - UK CIF

300-450 5.63 6.35 -

450-600 5.93 6.69 -

600-800 6.43 7.25 -

800-1000 7.33 8.27 =

> 1000 8.93 10.07 =

Fresh - whole - wild 600-800 g/pc 16.40 18.49 Italy FCA Morocco

Atlantic 800-1000 16.86 19.01 *1000-2000 15.09 17.02 -

> 2000 16.87 19.02 +

SEABASS/SEABREAM/MEAGRE (cont.) August 2015

20

Fish Species Product Form Grading Origin

Trade Name EUR USD & Area

ReferencePrice per kg

As stated

Gilthead seabream/ Fresh - whole, culture 300-400 g/pc 6.00 6.77 - Italy CIF Greece

Dorade royale/Dorada wild 400-600 g/pc 13.00 14.66 CPT Egypt

Sparus aurata 600-800 13.00 14.66

800-1000 13.00 14.66

1000-2000 13.17 14.85

farmed Orbetello Large 10.70 12.07 FCA Italy

Medium 9.70 10.94

Small 7.60 8.57

Meagre/Maigre Fresh - Whole 500-1000 g/pc 4.30 4.85

commun/Corvina farmed 1000-2000 4.87 5.49

Argyrosomus regius > 2000 5.01 5.65

> 3000 4.30 4.85

> 2000 g/pc 7.00 7.89 = CIF Greece

wild 600-800 g/pc 8.50 9.59 CPT Egypt

800-1000 9.00 10.15

1000-2000 9.00 10.15

2000-4000 9.00 10.15

SEABASS/SEABREAM/MEAGRE (cont.) August 2015

21

http://infofish.org/index.php/pacific-tuna-forum-2015

Sofitel Resort, Denarau, Nadi, Fiji22 - 23 September 2015

As one of the Co-Organizers, GLOBEFISH will offer 20% off theregistration fee to all of its Associate

Members, Partners and Correspondents.Contact us at [email protected]

13

PRICE REFERENCE (INCOTERMS 2010)

CFR Cost and Freight

CIF Cost, Insurance and Freight

CIP Carriage and Insurance Paid To

CPT Carriage Paid To

DAT Delivered at Terminal

DAP Delivered at Place

DDP Delivered Duty Paid

EXW Ex Works

FCA Free Carrier

FAS Free Alongside Ship

FOB Free on Board

(DAF, DES, DEQ and DDU have been cancelled)

PRODUCT FORM

C&P Cooked and Peeled

FAS Frozen at Sea

H&G Headed and Gutted

HOG Head on Gutted (salmon)

IQF Individually Quick Frozen

IWP Individually Wrapped Pack

PBI Pinbone In

PBO Pinbone Off

PD Peeled and Deveined

PTO Peeled Tail On

PUD Peeled, Undeveined

SYMBOLS

+ Price increased in original currency since last report

- Price decreased in original currency since last report

= Updated but unchanged price

* New insertion

Not updated since last issue

CURRENCY RATES

USD EUR Canada CAD 1.30 1.45

Hungary HUF 278.42 311.27

Norway NOK 8.15 9.11 USA USD 1.12

EU EUR 0.89

Denmark DKK 6.68 7.46

Exchange Rates: 12/08/15

GLOBEFISH Market Reports are available from the GLOBEFISH web site: www.globefish.org

All rights reserved. No part of FAO/GLOBEFISH European Fish Price Report may be reproduced, stored in a retrieval system, or transmitted in any form or by any means (electronic, mechanical, photocopying or otherwise), without prior permission. Requests for use of this material (including purpose and extent) should be addressed to: GLOBEFISH - Fisheries and

Aquaculture Department - Food and Agriculture Organization, Viale delle Terme di Caracalla, 00153 Rome, Italy.

The European Fish Price Report is a monthly GLOBEFISH publication, prepared by Helga Josupeit and Felix Dent.

It can be ordered from the FISH INFONetwork:

FAO GLOBEFISH

(Network coordinator)

Viale delle Terme di Caracalla

00153 Rome - Italy

Tel: (39) 06 57055188

Fax: (39) 06 57053020

E-mail: [email protected]

Web site: www.globefish.org

INFOPECHE (Africa)

Tour C, 19éme étage, Cité

Administrative

Abidjan 01 - Côte d’Ivoire

Tel: (225) 20228980

Fax: (225) 20218054

E-mail: [email protected]

Web site: www.infopeche.ci

INFOPESCA

(Latin America)

Julio Herrera y Obes 1296

11200 Montevideo - Uruguay

Tel: (598) 2 9028701

Fax: (598) 2 9030501

E-mail: [email protected]

Web site: www.infopesca.org

INFOYU (China)

Room 514, Nongfeng Building

No. 96 East Third Ring Road

Chaoyang District

Beijing 100122 – P.R. China

Tel: (86-10) 59199614

Fax: (86-10) 59199614

E-mail: [email protected]

Web site: www.infoyu.net

EUROFISH

(Central and Eastern Europe)

H.C. Andersens Blvd 44-46

1553 Copenhagen - Denmark

Tel: (45) 33377755

Fax: (45) 33377756

E-mail: [email protected]

Web site: www.eurofish.dk

INFOSAMAK

(Arab Region)

71 blvd Rahal El Meskini

Casablanca 20 000 - Morocco

Tel: (212) 522540856

Fax: (212) 522540855

E-mail:

Web site : www.infosamak.org

INFOFISH (Asia/Pacific)

1st Floor, Wisma LKIM

Jalan Desaria - Pulau Meranti

47120 Puchong, Selangor DE

Malaysia

Tel: (603) 80609295/80609169

Fax: (603) 80603697

E-mail: [email protected]

Web site: www.infofish.org

INFOSA - sub-office

INFOPECHE (Southern Africa)

89, John Meinert Street- West

Windhoek -Namibia

Tel: (264) 61279430

Fax: (264) 61279434

E-mail:[email protected]

Web site: www.infosa.org.na

15

Food and Agriculture Organization of the United Nations

Fish Products and Industry Division

Viale delle Terme di Caracalla

00153 Rome, Italy

Tel +39 06 5705 3288

Fax +39 06 5705 3020

www.globefish.org

![Stock assessment form small pelagics - GFCM · Stock Assessment Form Small Pelagics ... 6th Geographical sub-area: [GSA_4] ... When an analytical assessment exists, ...](https://static.fdocuments.us/doc/165x107/5b4fb9c37f8b9a2f6e8cf273/stock-assessment-form-small-pelagics-stock-assessment-form-small-pelagics.jpg)