Global Wealth Management Trends An EY Point of View June 2015.

17

Global Wealth Management Trends An EY Point of View June 2015

-

Upload

beryl-golden -

Category

Documents

-

view

216 -

download

1

Transcript of Global Wealth Management Trends An EY Point of View June 2015.

Global Wealth Management Trends

An EY Point of View June 2015

Page 2 Global Wealth Management Trends

Some key observations around Wealth

ASIA, LATAM AND

AFRICA ARE

GROWING FASTER

PRIVATE WEALTH OF

GEN-Y

(MILLENIALS) WILL

DOMINATE BY 2020

CURRENTLY WEALTH IS

CONCENTRATED

AROUND DEVELOPED

COUNTRIES

GLOBALLY THE

RICH ARE

GETTING RICHER

BUT ASIA IS FAST

CATCHING UP

Page 3

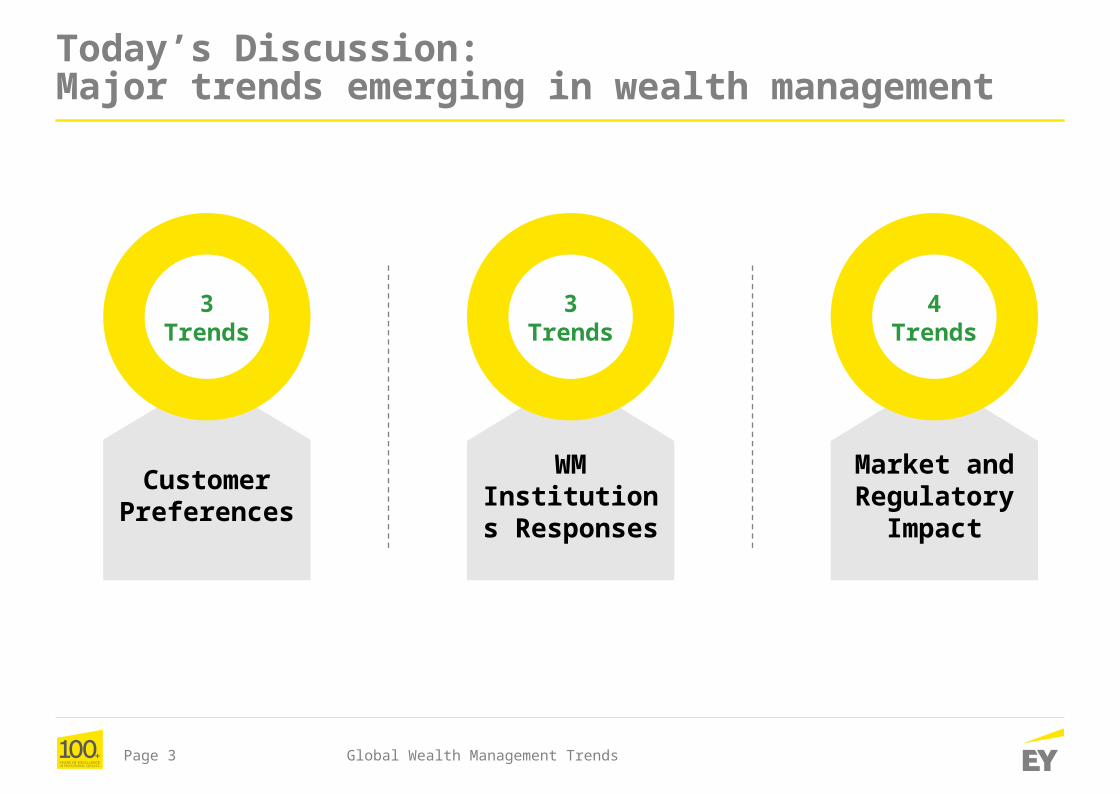

Today’s Discussion: Major trends emerging in wealth management

Global Wealth Management Trends

Customer Preferences

3 Trend

s

WM Institutions Responses

3 Trend

s

Market and Regulatory

Impact

4 Trend

s

Page 4

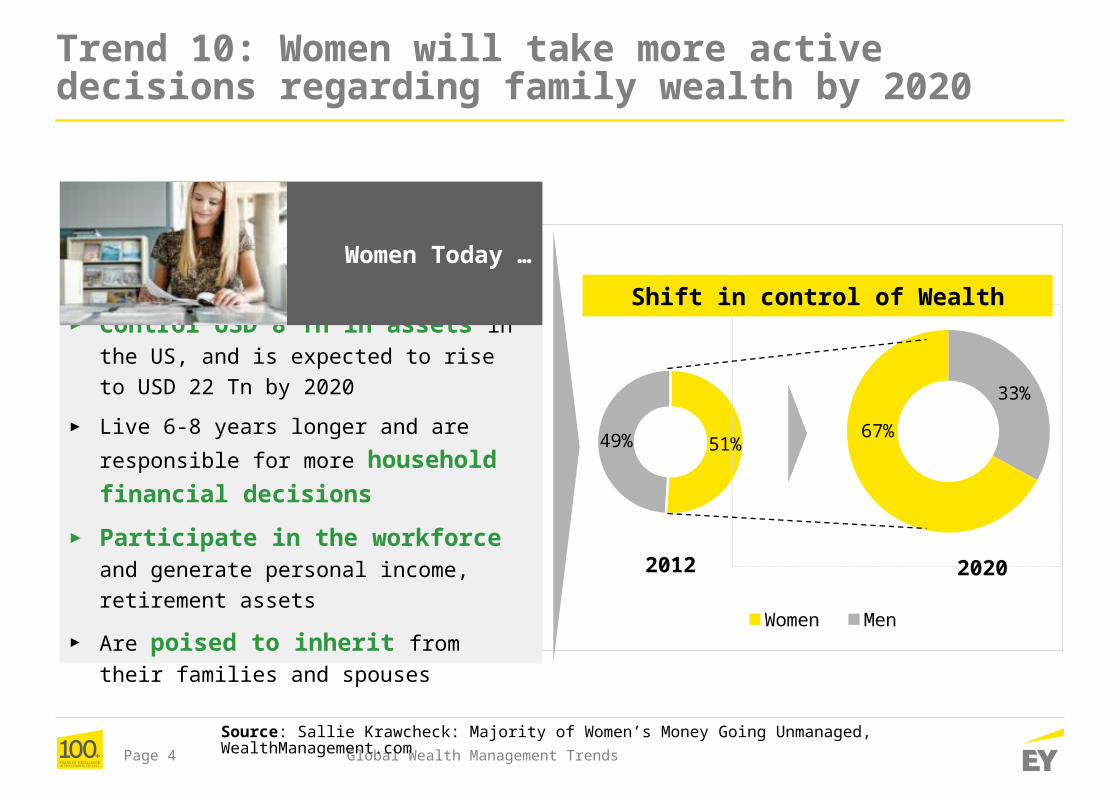

Trend 10: Women will take more active decisions regarding family wealth by 2020

51%49%

Women Men

33%

67%

2012 2020

Shift in control of Wealth► Control USD 8 Tn in assets in the

US, and is expected to rise to USD 22 Tn by 2020

► Live 6-8 years longer and are

responsible for more household financial decisions

► Participate in the workforce and

generate personal income, retirement assets

► Are poised to inherit from their

families and spouses

Global Wealth Management Trends

Women Today …

Source: Sallie Krawcheck: Majority of Women’s Money Going Unmanaged, WealthManagement.com

Page 5

Trend 9: Millennials are conservative

Cash52%

Fixed Income

7%

Stocks28%

Others13%

Care more about Risk than anything else…

Distrustful of Wall Street

Hold a lot of Cash

Cautious

Current Asset MixInvestment philosophy

Global Wealth Management Trends

Source: UBS “Think you know the Next Gen investor? Think again” 1Q 2014

The financial crisis has shaped their behaviour

Page 6

Trend 8: Your advisor is growing old

Age of the financial advisor increasing across

the globe

Next Gen to the job

► Average age of advisors is 50.9 years

► In US 43% of the advisors are over the age of 55

► Only 11% are under the age of 35

Global Wealth Management Trends

Source: Understanding and Addressing a More Sophisticated Population, Cerulli Associates

Succession planning and

training of advisors is slowing which

will lead to a shortfall of advisors

Page 7

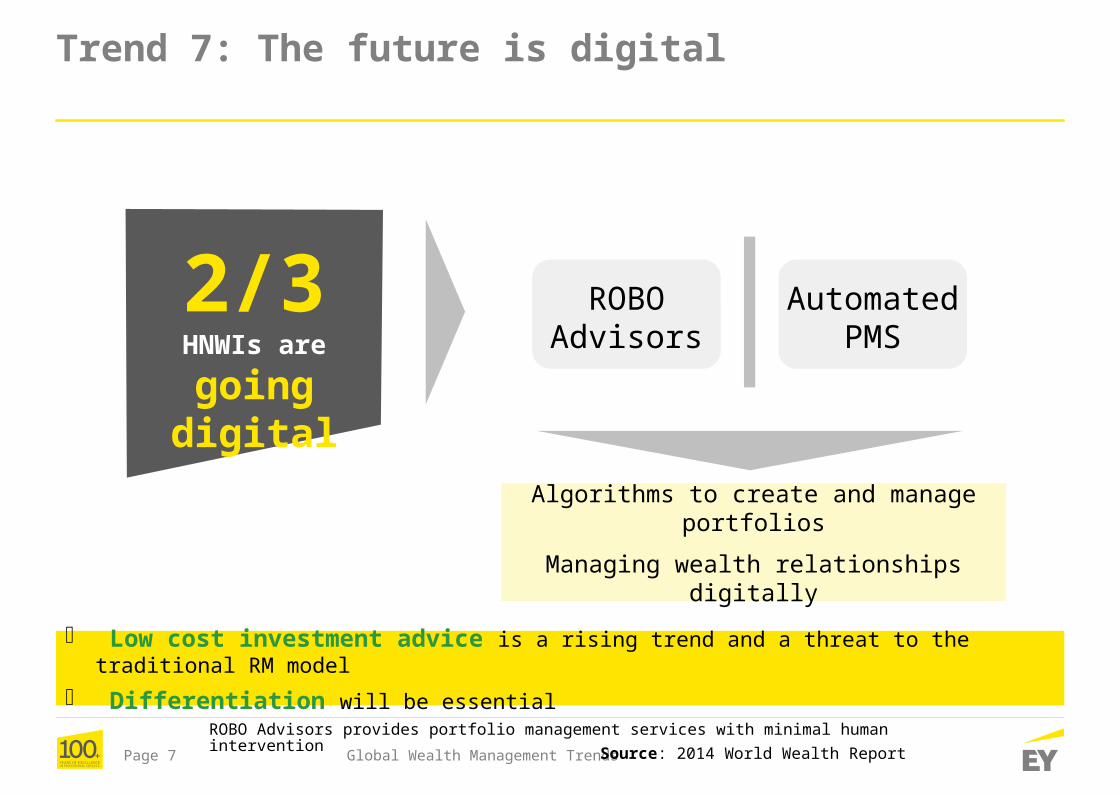

Trend 7: The future is digital

2/3 HNWIs are

going digital

ROBO Advisors

Automated PMS

Algorithms to create and manage portfolios

Managing wealth relationships digitally

Low cost investment advice is a rising trend and a threat to the traditional RM model

Differentiation will be essentialROBO Advisors provides portfolio management services with minimal human intervention

Global Wealth Management TrendsSource: 2014 World Wealth Report

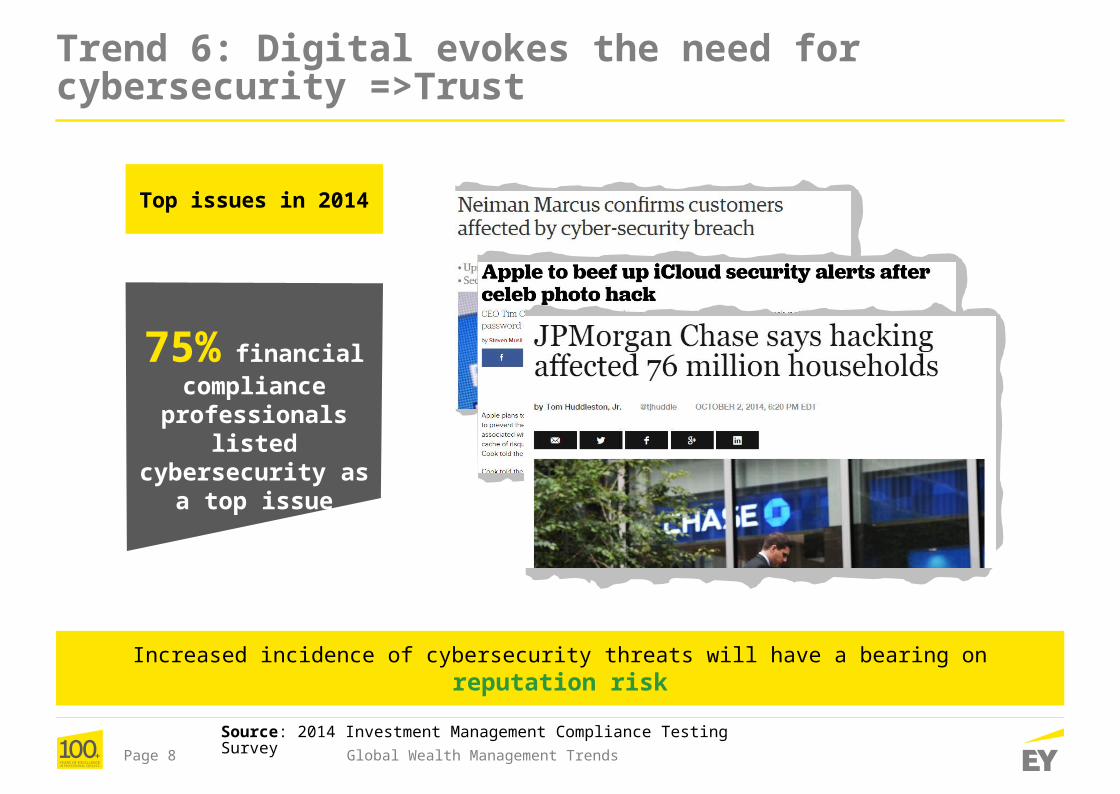

Page 8

75% financial compliance

professionals listed

cybersecurity as a top issue

Trend 6: Digital evokes the need for cybersecurity =>Trust

Increased incidence of cybersecurity threats will have a bearing on reputation risk

Top issues in 2014

Global Wealth Management Trends

Source: 2014 Investment Management Compliance Testing Survey

Page 9

Trend 5: Celebrities fail without good financial advisor

Celebrity lives are always magnified

They need good financial advise because their time is money

Today’s high profile and rich make mistakes

Global Wealth Management Trends

Celebrities need a trusted advisor to help them manage wealth while dealing with lifestyle challenges

Celebrities fail to plan and protect their wealth for events that erode their wealth such as:

► Divorce

► Death

► Law Suits and other Legal trouble

Financial planning for life events

M C Hammer

Dionne Warwick

Larry King

Page 10

Trend 4: Domicile preferences

Australia & New

Zealand

Russia & CIS

Over 60% likely to send children

abroad for secondary education

Only 4% HNWIs considering move out

of country

33% HNWIs considering to move

out of country

Tax is the main reason globally UHNWI consider moving to different country

In Russia, education and political issues are the main reasons

Globally 27% send kids abroad for

secondary education

China

42%3%

Global Wealth Management Trends

Source: Knight Frank report, 2015

12% HNWIs considering to move

out of country

Page 11

78

71

67

66

61

60

53

54

51

80

72

67

66

61

61

54

53

52

Technology

Automotive

Food & Beverage

Consumer packaged goods

Pharma

Energy

Banks

Financial services

Media

Trend 3: Trust will be new wealth mantra

Global Wealth Management Trends

Source: Edelman Trust Barometer

2014 2015

Banks and Financial services have lowest trust among industries

Page 12 Global Wealth Management Trends

Trend 2: Mass affluent is the new sweet spot for wealth managers

44% of mass affluent does not consider primary bank as a potential provider of investment

services. Addressing this perception problem will unlock more opportunities for banks

Mass Market

Mass Affluent

Mass market segment, a core driver

of revenue, is

marginally profitable at best

Mass Affluent are 6- 10 times more

profitable than mass

market

Constitute 20-30% of

retail divisions in banks

HNWI segment though profitable, is too

small to drive enough growth and

revenue

Source: Rising to the challenge of the rising mass affluent, BAI

HNWIs

Millionaires

UHNWI

Billionaires

Centa- millionaires

Page 13

Trend 1: The wealthier take more risks

Growing trends of acquiring stakes in

unlisted companies

Offshore investments have

caught on

Attractiveness of Real estate as an

asset class is coming down

Equity has taken over from real estate as the

preferred option, commercial Real estate

and lease rental discounting are helping

push investments in Real Estate

Kids going abroad, diversification,

currency movement are pushing offshore investment

High growth potential opportunities in these firms

are attracting HNWIs attention

Global Wealth Management Trends

Source: EY Analysis

Page 14

Globally the rich are getting richer…How can wealth management firms work to build their wealth?

What have these guys

done right to build their

wealth?

The top 1% own almost 40% of wealth. And the top 10% hold almost 90%

Global Wealth Management Trends

Source: The Economist

A. Invest in their Businesses

B. Diversification of investments

Page 15

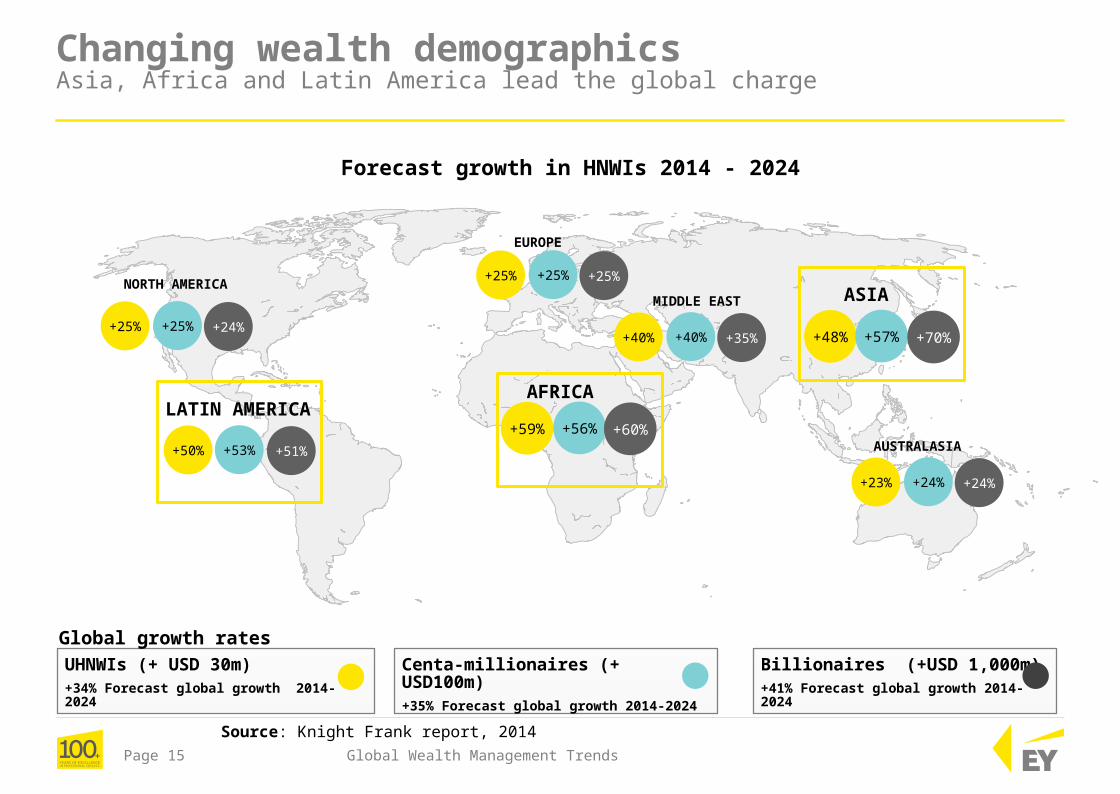

Centa-millionaires (+ USD100m)+35% Forecast global growth 2014-2024

UHNWIs (+ USD 30m)+34% Forecast global growth 2014-2024

Billionaires (+USD 1,000m)+41% Forecast global growth 2014-2024

Global growth rates

+25%

+25%

+24%

NORTH AMERICA

EUROPE

MIDDLE EAST

AFRICA

ASIA

AUSTRALASIA

Forecast growth in HNWIs 2014 - 2024

LATIN AMERICA

Changing wealth demographics Asia, Africa and Latin America lead the global charge

+25%

+25%

+25%

+23%

+24%

+24%

+59%

+56%

+60%

+40%

+40%

+35%

+50%

+53%

+51%

+48%

+57%

+70%

Global Wealth Management Trends

Source: Knight Frank report, 2014

Page 16 Global Wealth Management Trends

Where is wealth concentrated today

Source: Knight Frank report, 2015

Europe, 29%

North America,

25%

Australasia, 2%

Asia, 32%

Rest of the World,

12%

HNWIs wealth distribution

J apan, 26%India, 5%

China, 31%

Singapore, 17%

Rest of Asia, 21%

Ernst & Young LLP

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in.

Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata – 700016

© 2015 Ernst & Young LLP. Published in India. All Rights Reserved.

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.