Global Seed Treatment Market 2012 - agrochemical...

24

Global Seed Treatment Market 2012 Global Seed Treatment Market 2012 Analysis and Opportunities A Presentation to: AgroChemEx 2012 Shanghai Everbright Convention & Exhibition Centre October 20, 2012 www.KlineGroup.com © 2012 Kline & Company

Transcript of Global Seed Treatment Market 2012 - agrochemical...

Global Seed Treatment Market 2012Global Seed Treatment Market 2012Analysis and Opportunities

A Presentation to:

AgroChemEx 2012Shanghai Everbright Convention & Exhibition Centre

October 20, 2012

www.KlineGroup.com

© 2012 Kline & Company

Today’s presentation

What is the current situation of the global seed treatment market?

What are some important trends driving the global seed treatment market?What are some important trends driving the global seed treatment market?

What is the outlook for the global seed treatment market?

© 2012 Kline & Company 1

Kline is a leading management consulting and market research firm specializing in the chemicals materials and energy sectorsfirm, specializing in the chemicals, materials, and energy sectors

Kline KlineKline Management Consulting

Kline Published Market

Research

Working with individual clients to resolve tough

issues and help implement solutions

Generating information and insights for multiple

clients through syndicated research

Managed flow of people, ideas and

data

© 2012 Kline & Company 2

Specialty pesticides is part of our Chemicals practice

Kline’s Seed Treatment 2012 Global Series is based on in-depth i t i ith t i i t t i d tinterviews with experts in nineteen countries and across ten crops

Region/country n/m

aize

bean

s

heat

atoe

s

Ric

e

arbe

ets

otto

n

flow

ers

anol

a

ghum

g y

Cor

n

Soyb Wh

Pota R

Suga Co

Sunf Ca

Sorg

NORTH AMERICACanada X XMexico X XUnited States X X X X X X X X

EUROPEFrance X X X X X XGermany X X X XItaly X XHungary X X XHungary X X XPoland X XRussia X X XSouth Africa X X X XUkraine X X XUnited Kingdom X X X X

SOUTH AMERICAArgentina X X X XBrazil X X X X

ASIA-PACIFICAustralia X X XJapan X

© 2012 Kline & Company 3

Japan XChina X X X X X XThailand XIndia X X X X X X

Today’s presentation

What is the current situation of the global seed treatment market?

What are some important trends driving the global seed treatment market?What are some important trends driving the global seed treatment market?

What is the outlook for the global seed treatment market?

© 2012 Kline & Company 4

Globally, North America is the largest seed treatment market by sales, and the US the largest single market

Global Overview

and the US the largest single marketSeed Treatment Sales by Region

Share of sales(Value)

Seed Treatment Sales by Country

Share of value

North

Asia-Pacific,

10% 40%

50%

( a ue)

America, 43%Europe-a,

23%

20%

30%

SouthAmerica,

24% 10%

20%

0%

© 2012 Kline & Company 5

a-Includes South Africa

Corn accounts for the largest share of global seed treatment sales

Global Overview

Corn/maize, wheat, and soybeans are the most widely planted crops in terms of

Seed Treatment Sales by Crop

All th

Comments

Share of valuemost widely-planted crops in terms of acreage – accounting for over 70% of acreageAll other crops include rice sunflower potatoes and sugar beets

Cotton, 5%

All others, 8%

rice, sunflower, potatoes, and sugar beetsCorn, 34%

Canola, 6%

Soybeans, 24%

Wheat, 23%

, 24%

© 2012 Kline & Company 6

Fungicides account for the largest share of acreage, but the smallest share of sales

Global Overview

share of salesSeed Treatment Sales by Pesticide Type

Share of sales Share of acreage

Fungicides, F i idInsecticides, or insecticide/Fungicides,

35%

Insecticides, or insecticide/fungicide combo,

Fungicides, 69%

insecticide/fungicide combo, 31%

65%

© 2012 Kline & Company 7

Carbendazim is the leading active ingredient sold, measured by i ht

Global Overview

weight

Share of sales(Quantity of active ingredient)

Seed Treatment Sales by Active Ingredient

Many active ingredients are sold in combination with other active ingredients

Comments

30%

40%

(Qua t ty o act e g ed e t) combination with other active ingredientsSeven active ingredients account for two-thirds of salesThe top four active ingredients account for o er 50% of sales

20%

over 50% of sales

10%

0%

© 2012 Kline & Company 8

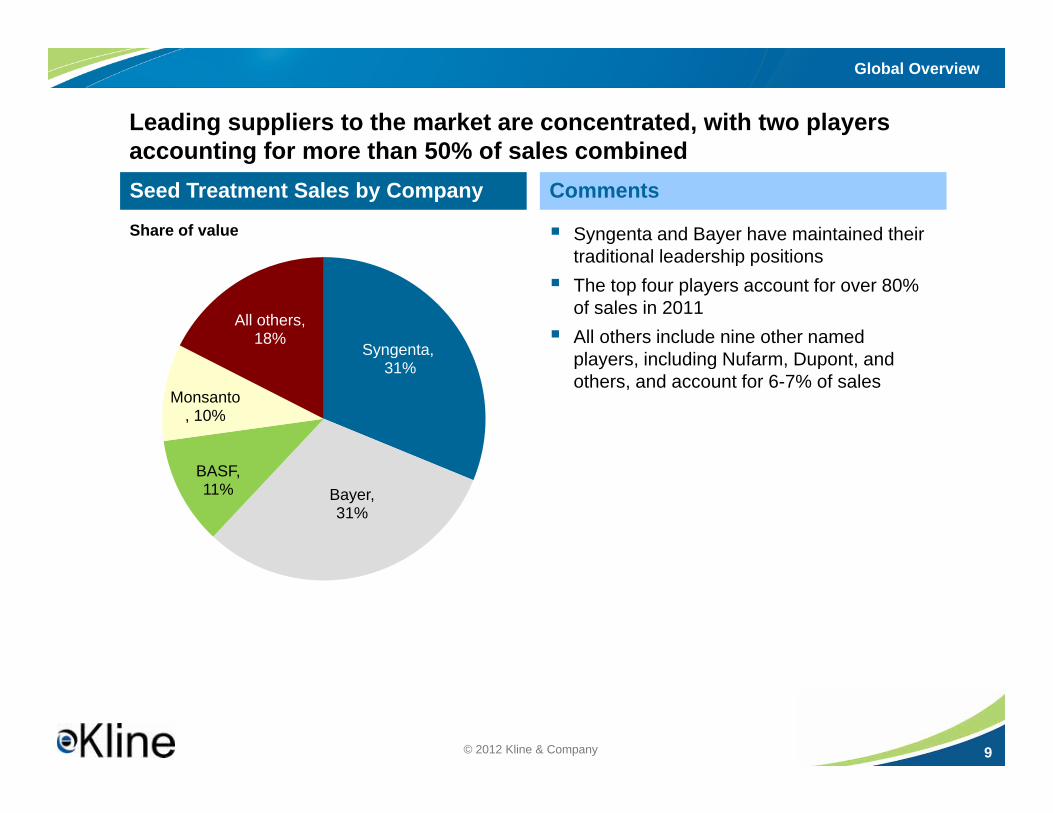

Leading suppliers to the market are concentrated, with two players accounting for more than 50% of sales combined

Global Overview

accounting for more than 50% of sales combined

Syngenta and Bayer have maintained their traditional leadership positions

Seed Treatment Sales by Company Comments

Share of valuetraditional leadership positionsThe top four players account for over 80% of sales in 2011All others include nine other named pla ers incl ding N farm D pont andSyngenta,

All others, 18%

players, including Nufarm, Dupont, and others, and account for 6-7% of sales

y g ,31%

Monsanto, 10%

Bayer, 31%

BASF, 11%

© 2012 Kline & Company 9

Today’s presentation

What is the current situation of the global seed treatment market?

What are some important trends driving the global seed treatment market?What are some important trends driving the global seed treatment market?

What is the outlook for the global seed treatment market?

© 2012 Kline & Company 10

Increasing interest in risk protection is a key driver of demand in seed t t t d i i l t b hi h i t t l l

Market Drivers and Trends

treatment, driven in large part by higher investment levels …Driver Description Impact

Prices of seeds increasing in individual crop segmentsSeeds a major input cost

Farmers reducing seeding ratesIncreasing importance of seed treatment to prevent plant loss

Higher seedcosts Seeds a major input cost to prevent plant loss

Weather and crop prices increasingly volatileFarmers increasingly risk averse

Growing interest in practices to reduce risk, e.g., adapting to weather conditions after sowing that make seedlings more

costs

Volatility in prices and Farmers increasingly risk averse g g

vulnerable to soil diseases and insects

Steady increase in farm sizes leads to new management practicesFarmers planting earlier to sow all their

Increasing seedling damage potentialmakes risk management increasingly important

Increasing farm sizes

pweather

Farmers planting earlier to sow all their acreage, but conditions not optimal (e.g. cool, wet conditions)

importantYoung seedlings need protection against pathogen and insect attack

Crop rotation has been the traditional means of reducing soil pathogens

Greater build-up of pathogens increasing the risk of seedling loss

farm sizes

Shortening g p gIncreased pressure on crop land, and greater focus on prices of crops

g gShortening crop rotations

© 2012 Kline & Company 11

… and increasingly enabled by suppliers and other players along the l h i

Market Drivers and Trends

value chainDriver Description Impact

One product (multi-component) to coverwider range of insects and diseasesTrend to buy hybrid seeds better suited

Opportunity to include, or offer seed treatment as an optionIncreasing

use of multi Trend to buy hybrid seeds – better-suited to treatment – in Europe, US, and Brazil

Seed companies adding value with Increasing application of overtreatments

use of multi-component

Seed companies adding value withunique treatmentsTreaters and retailers investing in seed treatment equipment

Increasing application of overtreatmentsfor control of broader spectrum, or higher level and longer-lasting control in high infestation situationsIncreasing application of base treatments and overtreatments by local

New seed revenuestreams

ytreaters

© 2012 Kline & Company 12

Seed application point differs by crop and is still evolving for top 6 global seed treatment crops

Market Drivers and Trends

global seed treatment crops

Crop seed Traditional seed where applied

Trend in where applied Expected change

Corn Seed company Seed company -Corn Seed company Seed company

Wheat Bin run seed; treated by grower if treated

More certified seed; treated by seed channel

More certified seed, so more channel treating

Soybeans Not treated; nematode resistant seed purchased

Seed companies treating More seed company treatment

Canola Seed channel Seed channel -

Cotton Seed company Seed company plus overtreatment by channel

-

Rice Grower and seed channel Grower, seed companyand channel

-and channel

Potatoes Grower Grower Grower, channel

© 2012 Kline & Company 13

2011 saw a number of new products launches, but basically no new active ingredients

Market Drivers and Trends

active ingredientsCompany Product Description

Adds control of nematodes to existing CruiserMaxx Beans product

New fungicide, part of new class of succinatedyhydrogenase inhibitorsBroad spectrum activity, and particularly effective against Rhizoctoniaeffective against Rhizoctonia

Launches combination product for corn in 2011 – for soybeans and cotton in 2012Clothianidin plus biological combination offers control of early season insects and broadcontrol of early season insects and broad range of nematodesAddition of Votivo increased corn yields by 7.1 bushels/acre

Introduces seed treatment products with pactive ingredients licenced from different manufacturers for use in proprietary combinations in their own seed brands

Expanded to include corn, sorghum, and other

© 2012 Kline & Company

cereals, in addition to barley and wheat

14

Today’s presentation

What is the current situation of the global seed treatment market?

What are some important trends driving the global seed treatment market?What are some important trends driving the global seed treatment market?

What is the outlook for the global seed treatment market?

© 2012 Kline & Company 15

Under our most likely forecast, global sales will grow by 3% per year from 2011 to 2016

Global Outlook

from 2011 to 2016

Baseline growth a result ofE di f d t t t b f

Seed Treatment Market Scenarios

10%4 000Value CAGR

Comments

− Expanding use of seed treatment by farmers, channel and seed companies

− Increased crop acreage− Increased use of higher-value insecticides− Move from generic products to proprietary

10%

3 000

4,000

Move from generic products to proprietary chemistries

Pessimistic cased grounded in− A shift away from biofuel support – lower grain

and oilseed prices lead to reduced planted areaR d i i i l l i d

5.9%

5%2 000

3,000

− Reductions in agricultural price support due economic difficulties in major crop producing countries – farming becoming more cyclical, and lower investment in inputs, by some farmers

Optimistic case driven by3.0%

5%

1 000

2,000

− Faster growth in area planted in lesser developed regions

− Faster uptake of seed treatments in grain crops, especially insecticide seed treatments

− Increased use of high-cost/high-value products0.3%0%0

1,000

© 2012 Kline & Company

Increased use of high cost/high value products (e.g., combinations and/or nematicides)

− Continued strong grain and oilseed markets in the developed regions

16

0%0Pessimistic Likely Optimistic

Canola will experience the fastest sales growth to 2016, while corn will remain the largest crop in terms of sales

Global Outlook

remain the largest crop, in terms of sales

Canola

Seed Treatment Sales Growth by Crop

8% 8%100%

Seed Treatment Sales by Crop

Soybeans

Canola

6% 7%5% 5%

8% 8%

80%

Wh t

Cotton

24%

23% 23%

60%

Corn

Wheat 24% 24%40%

0% 1% 2% 3% 4% 5% 6%

All others34% 32%

0%

20%

© 2012 Kline & Company 17

0% 1% 2% 3% 4% 5% 6%

Sales CAGR 2011-16(Value)

2011 2016

North America will remain the largest region by sales in 2016, but will experience the slowest growth

Global Outlook

experience the slowest growth

10 4% 11 0%100%

Seed Treatment Sales by Region Seed Treatment Sales Growth by Reg.

23.1% 23.0%

10.4% 11.0%

80%

South America

23.5% 25.2%

60%Asia Pacific

43 0%

40% Europe-a

43.0% 40.8%

0%

20%

0% 1% 2% 3% 4% 5%

North America

© 2012 Kline & Company 18

2011 20160% 1% 2% 3% 4% 5%

Sales CAGR 2011-16(Value)

a-Includes South Africa

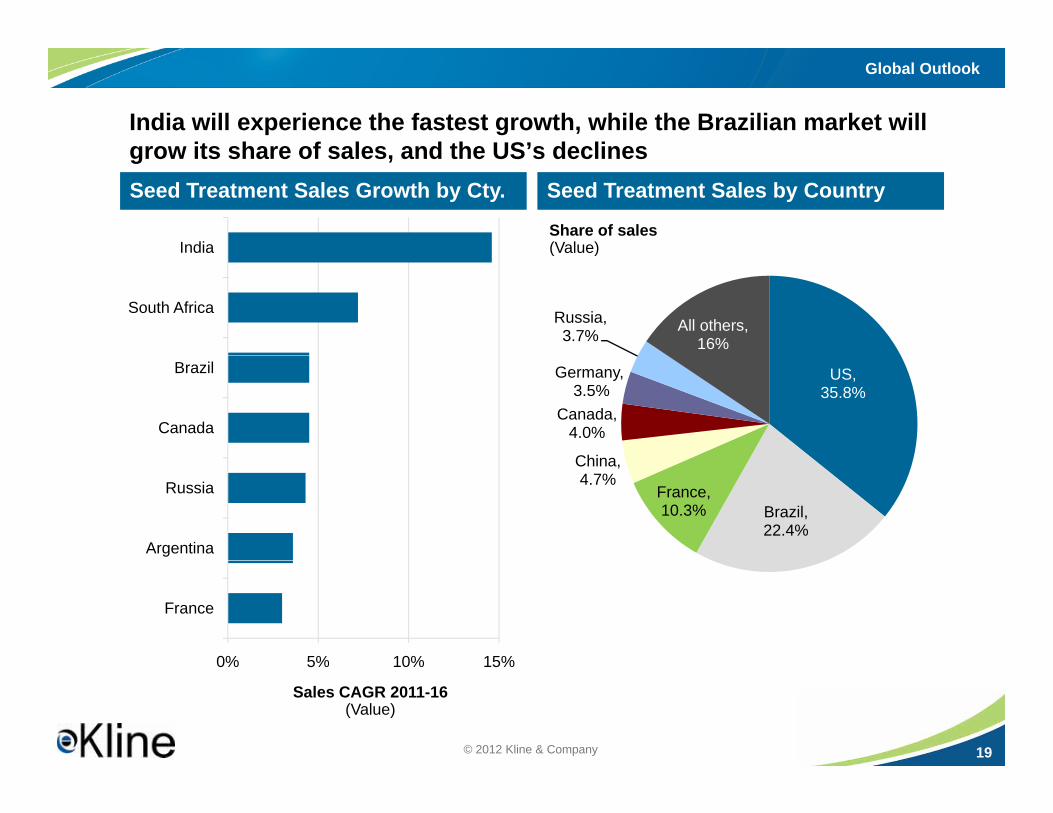

India will experience the fastest growth, while the Brazilian market will grow its share of sales and the US’s declines

Global Outlook

grow its share of sales, and the US s declinesSeed Treatment Sales Growth by Cty.

India

Seed Treatment Sales by Country

Share of sales(Value)

South Africa

d a

Russia, 3.7% All others,

16%

( a ue)

Canada

Brazil US, 35.8%

China

Canada, 4.0%

Germany,3.5%

Argentina

RussiaBrazil, 22.4%

France, 10.3%

China, 4.7%

0% 5% 10% 15%

France

© 2012 Kline & Company 19

0% 5% 10% 15%

Sales CAGR 2011-16(Value)

Today’s presentation

Thank you for attending today’s presentationThank you for attending today s presentation

© 2012 Kline & Company 20

D t i thi t ti i d fData in this presentation is sourced from:“Seed Treatment 2012 Global Series”

Regional coverage:− North America− Europe and Africa− South America− Asia-Pacific

The report includes:− Estimates of market sizes and outlook for key seed

treatment crops in 19 countries − A highly reliable and independent assessment of the

competitive positions of the major seed treatment suppliers in terms of product sales and market share

− Management-level insights into the reasons for treatment, the key insects and diseases being treated, and the leading products in each segment

− An assessment of strengths and weaknesses for current products and a tabulation of unmet needs provided by our respondents

− An overview of the cultural practices used by

© 2012 Kline & Company

p ygrowers to produce their crops, the role of seed treatment, and opportunities to establish or increase market penetration

21

Kline’s emphasis on primary research and rigorous analysis methodology lt i hi h lit d i i htf l tresults in high quality and insightful reports

PRIMARY RESEARCHUnstructured interviews with:

DealersConsultantsCrop advisorsSeed companiesSeed companiesGrowersDistributorsGovernment agencies

SECONDARY RESEARCHTrade journalsAnalysis of public dataCorporate financial reports and literature Non-confidential data from Kline’s databases

RIGOROUS ANALYSIS/CROSS CHECK

© 2012 Kline & Company

AmericasKline is a worldwide consulting and research firm dedicated ____________

Asia

to providing the kind of insight and knowledge that helps companies find a clear path to success. The firm has served the management consulting and market research needs of organizations in the chemicals, materials, energy, life sciences and consumer products industries for over 50 ___________

Europe___________

If you require additional information about the contents of this document or the services that Kline provides, please contact:

sciences, and consumer products industries for over 50 years. For more information, visit www.KlineGroup.com.

Li WangManaging Director, Kline [email protected]

Rob Field-MarshamManager, Kline [email protected]

Kristina ZableckeAccount Manager, EMEA , Asia+32-(2)[email protected]

Kline Global Headquarters

Kline & Company, Inc.35 Waterview Blvd.Suite 305Parsippany, NJ 07054

China

Kline AsiaCITIC Square, Suite 912B1168 Nanjing Xi LuShanghai, 200041, Chinay

Phone: +1-973-435-6262Fax: +1-973-435-6291

www.KlineGroup.com

g , ,Phone: +86-21 5292-5353