Global Mobility Services: Taxation of International Assignees – … · 2019-07-15 · after the...

22

Global Mobility Services Taxation of International Assignees – Lithuania www.pwc.com/lt/en People and Organisation Global Mobility Country Guide

Transcript of Global Mobility Services: Taxation of International Assignees – … · 2019-07-15 · after the...

Global Mobility Services

Taxation of International Assignees – Lithuania

www.pwc.com/lt/en

People and Organisation

Global Mobility Country Guide

Last Updated: June 2019

This document was not intended or written to be used, for the purpose of avoiding tax penalties that may be imposed on the taxpayer.

Global Mobility Country Guide (Folio) 3

Country - Lithuania Introduction ....................................................................................................................................... 4

International assignees working in Lithuania ................................................................................ 4

Step 1 ............................................................................................................................................... 5

Understanding basic principles ..................................................................................................... 5

Step 2 ............................................................................................................................................... 7

Understanding the Lithuanian tax system .................................................................................... 7

Step 3 ............................................................................................................................................. 12

What to do before you arrive in Lithuania ................................................................................... 12

Step 4 ............................................................................................................................................. 14

What to do when you arrive in Lithuania .................................................................................... 14

Step 5 ............................................................................................................................................. 15

What to do when you leave Lithuania ......................................................................................... 15

Step 6 ............................................................................................................................................. 16

Other matters requiring consideration ........................................................................................ 16

Appendix A ..................................................................................................................................... 17

Typical tax computation .............................................................................................................. 17

Appendix B ..................................................................................................................................... 18

Double-taxation agreements....................................................................................................... 18

Appendix C ..................................................................................................................................... 19

Countries whose citizens do not require visas ........................................................................... 19

Appendix D ..................................................................................................................................... 21

Lithuania contacts and offices .................................................................................................... 21

Additional Country Folios can be located at the following website: Global Mobility Country Guides

People and Organisation 4

Introduction International assignees working in Lithuania PwC is the world's leading provider of professional services. The People and Organisation network works together with its clients to find solutions for the challenges they encounter when transferring people from one country to another.

This brochure is intended to inform foreign nationals and their employers about tax, social security and immigration issues in Lithuania.

This guide is not exhaustive and cannot be regarded as a substitute for professional advice addressing individual circumstances. Nevertheless, answers will be found to most of the questions raised by an expatriate or his/her employer. More detailed advice should be sought before any specific decisions are made about these issues.

More information can be obtained from our Lithuanian office specializing in People and Organisation’s Global Mobility Services (see Appendix E).

Global Mobility Country Guide (Folio) 5

Step 1 Understanding basic principles

The tax year 1. The tax year is the calendar year. Income is taxed in

the year in which it is actually received

Taxation base 2. Lithuanian tax residents are taxed on their worldwide

income. Lithuanian tax non-residents are taxed on the following Lithuanian-sourced income:

– Interest, except for interest received on the Lithuanian Government’s bonds;

– Income from distributed profits and payments to the members of the Board or Supervisory Board;

– Royalties;

– Employment related income;

– Income from sporting and performing activities;

– Income from the sale/lease of immovable property located in Lithuania;

– Proceeds from the sale or other transfer with title of movable property if that property is subject to legal registration in Lithuania and is (or must be) registered in Lithuania;

– Compensation for infringement of copyright or related rights;

– Income from individual activity performed through a permanent base in Lithuania.

Determination of residence 3. A Lithuanian tax resident shall be deemed to be any

of the following:

– An individual whose permanent place of residence during the tax period is in Lithuania, or

– An individual whose centre of personal, social or economic interests during the tax period is considered to be in Lithuania rather than in a foreign country, or

– An individual who stays in Lithuania, continuously or intermittently, for 183 or more days during the tax period, or

– An individual who stays in Lithuania, continuously or intermittently, for 280 or more days during two successive tax periods and who stayed, during one of such periods in Lithuania, continuously or intermittently, for 90 or more days.

General remarks 4. All income, according to the tax payment procedure,

is divided into two classes: Class A and Class B.

5. Income of Class A includes income received from Lithuanian enterprises, foreign enterprises through their permanent establishments and non-residents of Lithuania through their permanent base (except for certain other exceptions determined by the law), also some kind of income received from a Lithuanian resident. Tax on such kind of income has to be calculated and paid by the party, which makes the payments.

6. Income of Class B includes all other income not included in Class A. The tax on Class B income has to be calculated and paid by the individual.

Current personal income tax rates 7. The rate of personal income tax is 20% and is

applied to income amounts not exceeding EUR 136,344 per calendar year in 2019 (this threshold is foreseen to be reduced for 2020 and 2021) and 27% for the exceeding part is applicable to:

– Employment related income;

– Payments to the members of the Board or Supervisory Board;

– Income derived under copyright agreements (when it is received from the company that is also the employer of individual);

People and Organisation 6

– Income under civil agreement received by a manger of small partnership who is a member of such small partnership.

8. Income from profit distribution (e.g. dividends) is taxable at a flat personal income tax rate of 15%.

9. Other income not specified above is taxed at a personal income tax rate of 15% (except for income from the sale of waste for which a reduced rate of 5% is applicable) if income amounts do not exceed EUR 136,344 per calendar year. A 20% personal income tax rate is applicable to income exceeding this threshold.

Global Mobility Country Guide (Folio) 7

Step 2 Understanding the Lithuanian tax system

Taxation of employment income 10. In principle, all employment related income, whether

in cash or in kind, is taxable. Employment income can be reduced by pre-determined tax-exempt amounts. Social security contributions are not deductible for personal income tax purposes.

11. If individuals are employed in Lithuanian entity or foreign entity acting through a permanent establishment in Lithuania, the employer on a monthly basis withholds 20% of personal income tax from employment related income. Individuals themselves have additionally to pay additional 7% of personal income tax on income exceeding EUR 136,344.

12. Individuals, whose employers are foreign entities without a permanent establishment in Lithuania, must pay personal income tax on received income themselves. In such a case Lithuanian tax residents have an annual personal income tax paying and reporting obligation (by 1 May of the following year), whereas Lithuanian tax non-residents have to pay and report personal income tax within 25 days from the receipt of income

Tax exempt amount 13. Tax exempt amount (TEA) is applied on a monthly

basis only to employment related income of Lithuanian tax residents:

– TEA of EUR 300 per month is applied to individuals whose employment related income does not exceed one minimum monthly salary amount which was in force as of 1 January of the current tax year (i.e. currently EUR 555 per month);

– TEA is proportionally reduced for larger amounts of income, and if income amounts to or exceeds EUR 2,555 per month, no TEA is applied.

14. Annual TEA is calculated at the end of the tax year taking into consideration not only employment related income but also other taxable income (except for

income taxed at 5% and derived under business certificates). Therefore, while applying for TEA, tax payers should take into consideration the fact that if it appears that the TEA applied on a monthly basis throughout 2019 in fact had to be lower, the individual will be obliged to file the annual personal income tax return and cover the income tax difference by 1 May 2020.

Taxation of self employment income 15. Self-employed individuals engaged in a limited

number of activities specified by the government can acquire a business certificate. Income derived from activities exercised under a business certificate not exceeding EUR 45,000 is taxed at a fixed rate determined by municipality councils.

16. Income exceeding EUR 45,000 derived from self-employment pursued having acquired a business certificate during a tax period and income from self-employment activities, which do not fall under the list of activities that could be undertaken under a business certificate, is taxed depending on the amount of income received. Personal income tax calculated at 15% flat rate on taxable income is reduced by applying a personal income tax credit, calculated as follows:

– 5% rate applies if income does not exceed EUR 20,000 per calendar year;

– Proportionally increasing rate ranging from 5% to 15% applies to income exceeding EUR 20,000 but lower than EUR 35,000 received per calendar year;

– 15% flat personal income tax rate is applied to income amount of EUR 35,000 and higher received per calendar year

People and Organisation 8

Taxation of self employment income

Non-taxable income provided by the employer 17. Contributions made by an employer on behalf of an

employee, such as life insurance premiums, additional (voluntary) health insurance contributions and pension contributions, provided that the total amount of such contributions does not exceed 25% of the employee’s annual employment related income (special conditions also apply);

18. The value of prizes and gifts received by an individual if the value of such prizes does not exceed EUR 200 during the tax period;

19. Railway or public transport tickets provided to an employee to commute to/from work;

20. Per diems (subject to certain limits and conditions) and other expenses related to business trips.

Capital gains from sale of financial instruments/derivatives 21. Capital gains from transfer of financial instruments or

realisation of derivatives not exceeding EUR 500 per tax year;

Interests 22. Interest received on (1) non-equity securities or (2)

non-equity government securities (i.e. government or municipal bonds, not necessarily of the EEA member states) or (3) deposits kept in banks and other credit institutions (not necessarily in the EEA member states), if the non-equity securities are acquired or the contracts of deposits are concluded after 1 January 2014 and the amount of such interest does not exceed EUR 500 per tax year;

23. Interest income received on consumer credits granted via peer-to-peer lending platforms or funds lend via crowdfunding platforms in Lithuania or in another EEA country is non-taxable, provided that the amount does not exceed EUR 500 per calendar year;

Capital gains from sale of private real property 24. Income from the sale of housing (including land)

located in a European Economic Area (EEA) member state, if the individual’s place of residence was declared there during the last two years prior to the sale. If the place of residence was declared for a shorter period but income received from such sale was invested into the acquisition of another housing located in one of the EEA member states in one year

after the sale and the place of residence is declared there accordingly, such income would also be treated as non-taxable;

25. Income from the sale of immovable property that is located in Lithuania or within an EEA member state, if the property was acquired more than 10 years prior to its sale;

Capital gains from sale of movable property, which is subject to legal registration 26. Income from the sale or other transfer of movable

property that is legally registered in Lithuania or within an EEA member state if the property was acquired more than three years prior to its sale;

Other non-taxable income 27. Life insurance benefits paid under life insurance

agreements, if certain conditions are met;

28. Pension benefits received from a pension fund if certain conditions are met;

29. Income received as a gift from spouses, children (adopted children), parents (adoptive parents), brothers, sisters, grandchildren and grandparents; as well as the amount (value) of income received as a gift from other individuals during the tax period, which does not exceed the amount of EUR 2,500;

30. Awards, sport contest prizes, and lottery winnings herein the value of which does not exceed EUR 200 provided such prizes are received from the same person not more than 6 times during the tax period;

31. Certain other income listed in the Law on Personal Income Tax.

Husband and wife 33. Income derived by a husband and wife is taxed

separately.

Family Allowances 34. For all children the Lithuanian local municipal offices

pay EUR 50 per month from birth to 18 years of age or older, if they study according to a general curriculum until they reach the age of 21 (individuals entitled to receive children allowances in Lithuania should meet certain conditions).

35. There are also additional allowances possible for children if families qualify for certain conditions.

Global Mobility Country Guide (Folio) 9

Family Allowances 36. The following expenses incurred by Lithuanian tax

residents over the tax period are tax deductible (certain additional conditions apply):

– Housing loan interest if the credit granted before 2009;

– Fees for initial higher education or vocational training;

– Contributions for/to (the total amount up to EUR 2,000):

• Life insurance contributions paid for one’s own benefit or for the benefit of a spouse, minor children, or disabled children;

• Pension contributions paid into the third tier pension funds for one’s own benefit or for the benefit of a spouse, minor children, or disabled children;

• Pension contributions paid into the second tier pension fund, provided that such contributions exceed 3% of the individual’s income on which social security contributions are calculated;

– Expenses incurred for one's own or spouse’s benefit for building finish and any type of its repair (except for apartment building renovation), car repair, and childcare services for children until 18 years, if the service provider is/should be registered as a Lithuanian taxpayer. The total annual amount of such expenses should not exceed EUR 2,000. The relief is temporary and will be applied to 2019, 2020, and 2021 calendar years.

Tax deductible expenses for tax residents 37. Income earned and taxed in countries that belong to

the EU or have signed a double taxation avoidance treaty with Lithuania is tax-exempt in Lithuania. This rule does not, however, apply to dividends, interest and royalties received in the above-mentioned countries as well as to all income earned in other countries, for which a tax credit method should be applied (when income is received from target territories (the list of which is established in the Lithuanian legislation) such income would be fully taxable in Lithuania).

38. The taxpayer should provide supporting documents, which would prove the tax paid abroad.

Tax returns 39. After making payments attributable to Class A

income during the tax period, a tax withholder (e.g. the employer) shall declare the payments made, together with the amount of income tax withheld and paid into the budget, by filing monthly income tax returns.

40. At the close of the tax period, a Lithuanian tax resident, who received reportable income that is attributable to both Class A and Class B income during the tax period, is obliged to submit an annual income tax return for that tax period to the Tax Authorities and declare during therein the total income derived during the tax period and the amount of income tax computed thereon.

41. The annual personal income tax return by an individual (Lithuanian tax resident) has to be submitted and income tax paid by 1 May of the following year.

42. Individuals may choose not to file an annual income tax return, if:

– They do not wish to take the advantage of deductions, and

– The only income they derived in the tax period is attributed to Class A (when personal income tax was withheld correctly) and

– TEA does not have to be recalculated at the end of the tax period

Double taxation avoidance agreements 43. Lithuanian Law on Personal Income Tax is overruled

by international agreements ratified by the Lithuanian Parliament. Lithuania has concluded double taxation avoidance agreements with 55 foreign countries. The effective agreements are listed in Appendix B to this document.

44. There is no special tax relief for short-term foreign employment.

Social security contributions 45. The following income is subject to social security

contributions (only the main types of income are commented):

– Income derived under employment agreements;

– Income from distributed profits and other remuneration received by the members of the Board or Supervisory Board;

People and Organisation 10

– Income received from individual activities and derived under business certificates;

– Income derived from sports activities, performers’ activities and under copyright agreements, etc.

46. Income derived under employment agreements: Social security contributions at 1.45% to 2.71% (for time limited employment agreements at 2.17% to 3.43%) are applied to employers up to the income of EUR 136,344 per calendar year, and social security contributions at 19.5% are withheld from employees up to the same threshold. A 6.98% rate (health insurance contribution) applies above this threshold, payable by the employee. This threshold is foreseen to be reduced in 2020 and 2021. Employers (with certain exceptions) also pay an additional contribution to the Guarantee Fund amounting to 0.16% and to the Long-term Employment Fund amounting to 0.16% on employee remuneration.

47. The lower limit for social security contributions is applied for employers meaning that social security contributions must be paid on the official minimum monthly salary amount in force (i.e. currently, EUR 555 per month) regardless of the fact that employee receives lower salary (not applicable when an individual is employed in another company, receives an old age pension benefit, is not older than 24 years).

48. Shares received under stock option plans not earlier than after a three-year period following the day on which the right to receive such shares was granted to employees are not the subject to social security contributions.

49. Income from distributed profits and other remuneration received by the members of the Board or Supervisory Board are subject to social security contributions at 15.7% up to income of EUR 136,344 and 6.98% (health insurance contribution) above this threshold.

50. Social security rate for self-employed individuals is 19.5% (includes 6.98% of health insurance). The tax base is limited to 90% of taxable income from individual activities derived in the tax period and cannot exceed EUR 48,856.60 per year.

51. Different social security rates apply to other types of income, e.g. income from sporting and performing activities, etc.

52. Individuals are also able to choose to additionally contribute for pension to the second tier pension fund. Individuals under 40 years old who were

included in the Register of insured individuals on 1 January 2019 were automatically involved in the participation in such pension accumulation system (such involvement will be performed each 3 years); however, they are allowed to choose whether to participate or not. Individuals over 40 years old are able to choose such a participation voluntarily.

53. Individuals who contributed to these funds additionally until 2019 (i.e. paid 2% in addition to their standard social security contributions rate) are required to pay an additional contribution of 3%, if they choose to remain in pension accumulation. The state also transfers an additional 1.5% on the state average remuneration amount to such individual's fund.

54. Individuals who did not historically participate in this pension accumulation system are able to start contributing from the lowest contribution rate amounting to 1.8%, which will gradually increase up to 3% within five years. The state respectively adds the contribution of 0.3% on the state average remuneration amount, which will gradually increase up to 1.5% within five years. Such individuals are also able to choose to contribute at the highest rate of 3% (with a subsidy of the state at 1.5%) from the beginning of enrolment to such system.

55. There is also an option to pay higher contributions (above 3%) either by individuals themselves or their employers.

56. Social security returns should be submitted by employers on a monthly basis by the 15th day of the following month, and the contributions should be paid on a monthly basis by the 15th day of the following month. The social security returns must be submitted electronically.

57. Social security contributions paid by employees both to the local or foreign social security systems are not deductible against personal income for taxation purposes.

Social security treaties 58. The Lithuanian legislation on social security has

been harmonised with the EU regulations. Foreign employees seconded to Lithuania from the European Economic Area or Switzerland and their employers are not required to pay social security contributions in Lithuania if A1 certificate is obtained.

Global Mobility Country Guide (Folio) 11

59. The reciprocal social security agreements exist between Lithuania and the following countries:

– Belarus

– Ukraine

– Russia

– Canada

– USA

– Netherlands

– Moldova

– Czech Republic

– Estonia

– Latvia.

60. The agreements with Belarus, Ukraine, Canada and Moldova regulate the payment of social security contributions, therefore, foreign employees seconded from the aforementioned countries to Lithuania who obtain relevant certificates on social security coverage in their home countries are also not required to pay social security contributions in Lithuania.

61. Employees temporarily seconded to Lithuania from the third countries, with which Lithuania has no reciprocal social security agreements, are not required to pay the Lithuanian social security contributions as well, unless their permanent place of employment becomes Lithuania or the secondment exceeds one year.

Social security treaties 62. Individuals who contribute to the Lithuanian social

security system, depending on their form of activity and the types of contributions paid, are entitled to receive sickness allowances, free healthcare from public healthcare service providers, maternity/paternity and children allowances, unemployment benefits, benefits for accidents at work and occupational diseases, old age, disability and widows’/widower’s/orphans’ pensions

People and Organisation 12

Step 3 What to do before you arrive in Lithuania Visa requirements and work permit 63. EU citizens and their family members are free to stay

and work in Lithuania.

64. A non-EU citizen needs a visa to enter Lithuania or residence permit, unless a visa-free regime is applied.

65. At present Lithuania does not require a visa from citizens of EU member states and countries listed in Appendix C for a stay not exceeding 90 days in any 180-day period.

66. International assignees from non-EU/EEU country are allowed to come to Lithuania for temporary employment only if they have been granted a work permit or an Employment Service decision by the Employment Service and permission for temporary residence or national visa D. With certain exceptions, Lithuanian employers may not employ international assignees who do not have these permits

Work permits or Employment Service decisions 67. Currently general rule is that work permits or

Employment Service decisions are required for all non-EU nationals who wish to work in Lithuania. However, some exemptions from the requirement to obtain a work permit or an Employment Service decision may be applied in case of international assignments, for example:

– when an international assignee stays in Lithuania for up to 3 months to negotiate a contract or the terms of its implementation or to train personnel or to undertake commercial activities or to install equipment;

– when a profession of international assignee is included into the list of professions under demand in the Lithuanian Labour market;

– when international assignee arrives to work in the Lithuanian company as a shareholder (who invested EUR 14,000) or a CEO, if the equity capital of the Lithuanian company is greater than EUR 28,000;

– an international assignee is permanently employed in the company established in any EEA member state, provided that the international assignee keeps social security in his/her home country for the whole period of posting to Lithuania etc.

68. In order to employ a non-EU citizen, Lithuanian employers are required:

– to submit diploma(s) of an international assignee to the Centre of Quality Assessment in Higher Education for recommendations regarding professional qualification or recognition of professional qualification (if applicable);

– to apply to the Employment Service and register a vacancy;

– to receive a decision that the employment of a highly skilled international assignee meets the requirements of the Lithuanian labour market (might be required in case of highly skilled assignees);

– to obtain the work permit before an international assignee arrives to Lithuania or Employment Service decision that the employment of an international assignee meets the requirements of the Lithuanian labour market from the Employment Service.

69. Work permit and Employment Service decision are issued up to 2 years, but no longer than the term of the assignment of the international assignee.

EU Blue Card 70. EU blue card may be granted for those international

assignees having tertiary education or those, who have professional experience of at least 5 years in a specific field and such experience is acknowledged as tertiary education by the Lithuanian authorities.

Global Mobility Country Guide (Folio) 13

71. There is no requirement to obtain the above-mentioned decision from the Employment Service and register a vacancy and search for employees in the Lithuanian and EU labour markets, if the international assignee:

– is employed for more than 1 year and salary proposed to him/ her is greater than 3 national average monthly wages (approx. EUR 3,756 gross in total);

– has been employed in Lithuania for 2 years as a highly skilled employee and he/she applies for the renewal of the EU Blue Card;

– is employed for more than 1 year and the salary proposed is greater than 1.5 national average monthly wage (approx. EUR 1,878 gross in total) and his/her profession is included into the list of professions under demand in the Lithuanian labour market.

72. The EU Blue Card is issued for 3 years or, in case the term of the employment contract is shorter - for the term of the employment contract plus 3 months.

Start-ups 73. If an international assignee is a shareholder of the

new start-up, he/she may be granted a temporary residence permit for up to 1 year provided that an authorized institution confirms all the following facts:

– the planned activities are related to creating of new technologies or other innovations important for the economic and social development of Lithuania;

– the international assignee has all necessary qualifications, financing and business plan;

– International assignee’s presence in Lithuania is necessary for the Lithuanian start-up.

74. In above-mentioned case the international assignee is also exempted from the obligation to obtain a work permit or an Employment Service decision.

People and Organisation 14

Step 4 What to do when you arrive in Lithuania 75. In case EU citizens and their family members intend

to stay in Lithuania for a period exceeding 3 months within half a year, they must obtain a certificate of temporary residence in the Republic of Lithuania allowing for EU citizen to temporarily live in Lithuania (issued by the Migration Authorities) and declare a place of residence in Lithuania.

76. Non-EU citizens, who obtained residence permits, also must declare a place of residence in Lithuania.

77. When a certificate of temporary residence or a residence permit is issued, individual is registered in the Population Register of the Republic of Lithuania

and Lithuanian personal identification code, which is also Lithuanian taxpayer’s identification code, is granted for him/her. No addition registering in the Register of Taxpayer’s is required.

78. In other cases, if individual has an obligation to file Lithuanian tax return (e.g. Lithuanian tax non-resident, who receives employment-related income for the work actually performed in Lithuania from the foreign employer without a permanent establishment in Lithuania), he/she has to register in the Register of Taxpayers (within the Lithuanian Tax Authorities) in order to obtain a Lithuanian taxpayer’s identification code.

Global Mobility Country Guide (Folio) 15

Step 5 What to do when you leave Lithuania 79. When individual had a declared place of residence in

Lithuania is leaving Lithuania, he/she must notify the Municipality of residence of the change of address no more than 7 days before the departure from Lithuania.

80. On the termination of employment contract concluded with the employee, having a valid work permit or Employment Service decision, a written notification must be submitted within 3 business days to the Employment Service. In addition, when the employee also has a valid residence permit or national visa, an employer must provide a notice to the Migration Authorities within 7 days.

81. Individuals, who are permanently departing from Lithuania, must submit the Lithuanian final departure personal income tax return and pay personal income tax (if any) before the date of departure.

82. Individuals, who were historically considered as the Lithuanian tax residents for no less than three years and are finally departing from Lithuania after spending less than 183 days in Lithuania during the year of departure until its date, are considered as tax residents until the departure date only, therefore, the annual Lithuanian personal income tax return for the year of departure is not required.

83. In other case (i.e. when individuals, who were historically considered as the Lithuanian tax residents for less than three years, or when individuals, who were historically considered as the Lithuanian tax residents for no less than three years and are finally departing from Lithuania after spending more than 183 days in Lithuania during the year of departure until its date) in addition to the Lithuanian final departure tax return, an annual Lithuanian personal income tax return has to be filed by the 1 May of the following year.

People and Organisation 16

Step 6 Other matters requiring consideration Import duties 84. Most recent Council Regulation (EC) No 1186/2009

setting up a Community system of relieves from customs duty applies. According to these regulations, personal property imported by individuals moving from their normal place of residence from a third country to the customs territory of the European Union shall be admitted free of import duties.

85. Personal property means any property intended for the personal use or for meeting their household needs, in particular:

– Household effects:

– Personal effects;

– Household linen;

– Furnishings;

– Equipment intended for the personal use of the persons concerned or for meeting their household needs;

– Cycles and motor cycles, private motor vehicles and their trailers, camping caravans, pleasure craft and private airplanes;

– Household provisions appropriate to normal family requirements;

– Household pets and saddle animals;

– Portable instruments of the applied or liberal arts, required by the person concerned for the pursuit of his trade or profession.

86. The above mentioned things are not considered as personal property if by their nature and quantity they are imported for commercial reasons.

87. Goods contained in traveler's personal luggage shall be admitted free of import duties if they are of a non-commercial nature and not exceeding certain value thresholds. Imports of a non-commercial nature are imports which are of an occasional nature, and consist exclusively of goods intended for the personal use of the travelers or their families or of goods intended for presents. The nature and quantity of imported goods should provide no doubts about their non-commerciality

Global Mobility Country Guide (Folio) 17

Appendix A Typical tax computation

Typical tax computation for a resident individual for 2019

Tax computation EUR EUR

Income

1. Salary income 36,000

2. Foreign income for work performed in Lithuania 10,000

3. Income from sale of property 20,000

4. Dividends received 1,000

5. Total income 67,000

Less — specific deductions:

6. Annual tax-exempt amount 0

7. Acquisition value of property sold (18,000)

8. Life insurance premiums paid (1,000)

9. Total deductions (19,000)

Income/deductions calculations:

10. Income subject to 20% rate (line 1 + line 2) 46,000

11. Income subject to 15% rate (line 3 – line 7 + line 4) 3,000

12. Amount of life insurance expenses deductible from income taxable at 20% rate (line 8 x line10/(line10 + line11))

939

13. Amount of life insurance expenses deductible from income taxable at 15% rate (line 8 x (line 11/(line 10 + line 11))

61

Taxes:

14. Personal income tax from salary income ((line 10 – line 6 x (line 10 / (line 10 + line 11)) – line 12) x 20%)1

9,012

15. Social insurance contributions paid by the employee (line 10 x 19.5%) 8,970

16. Personal income tax on the sale of property2 (((line 3 – line 7 – line 6 x ((line 3 – line 7) / (line 10 + line 11)) – line 13 x ((line 3 – line 7) / line 11)) x 15%)3

294

17. Personal income tax on dividends (line 4 – line 6 x (line 4 / (line 10 + line 11)) – line 13 x (line 4 / line 11)) x 15%)

147

18. Total personal income taxes (line 14 + line 16 + line 17) 9,453

19. Total social insurance contributions (line 15 ) 8,970

Total Net Income (line 5 – line 18 – line 19) 48,577

1 The tax rate of 20% has been applied as the income amount does not exceed EUR 136,344 per calendar year in 2019. 2 If certain conditions are met, income from the sale of immovable property is non-taxable. For this calculation, it was treated that income derived

from the sale of property is taxable. 3 The tax rate of 15% has been applied as the income amount does not exceed EUR 136,344 per calendar year in 2019.

People and Organisation 18

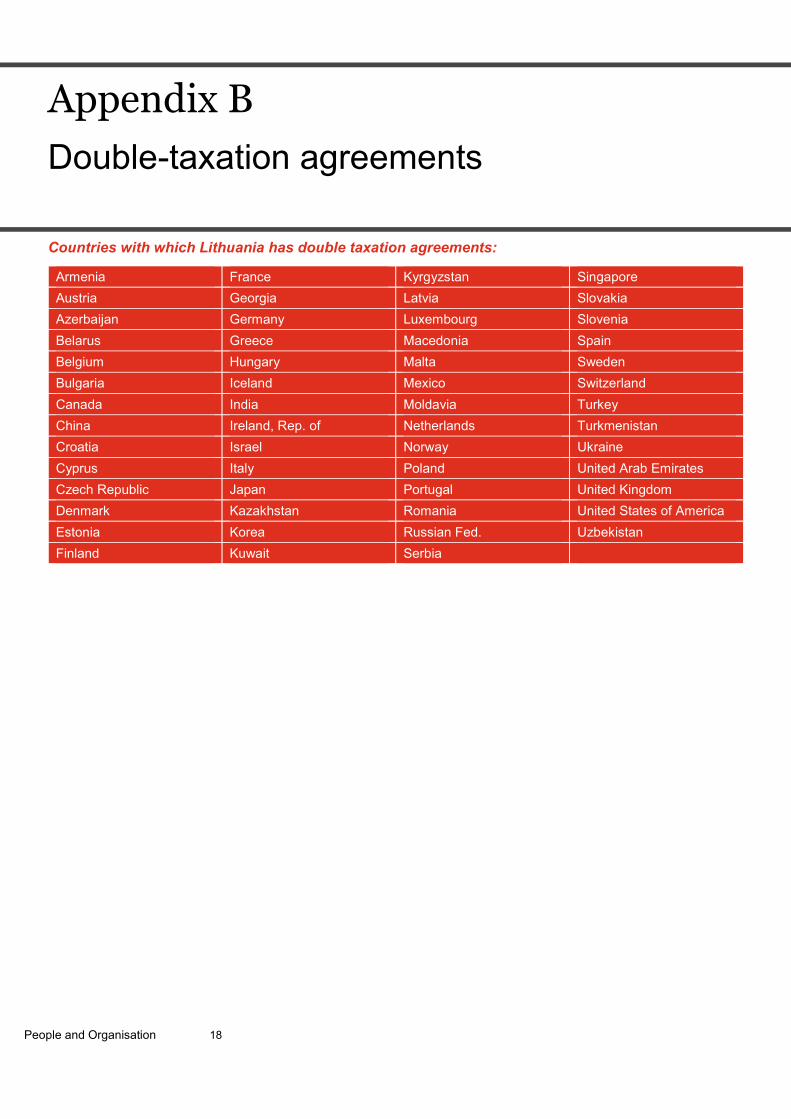

Appendix B Double-taxation agreements

Countries with which Lithuania has double taxation agreements:

Armenia France Kyrgyzstan Singapore Austria Georgia Latvia Slovakia Azerbaijan Germany Luxembourg Slovenia Belarus Greece Macedonia Spain Belgium Hungary Malta Sweden Bulgaria Iceland Mexico Switzerland Canada India Moldavia Turkey China Ireland, Rep. of Netherlands Turkmenistan Croatia Israel Norway Ukraine Cyprus Italy Poland United Arab Emirates Czech Republic Japan Portugal United Kingdom Denmark Kazakhstan Romania United States of America Estonia Korea Russian Fed. Uzbekistan Finland Kuwait Serbia

Global Mobility Country Guide (Folio) 19

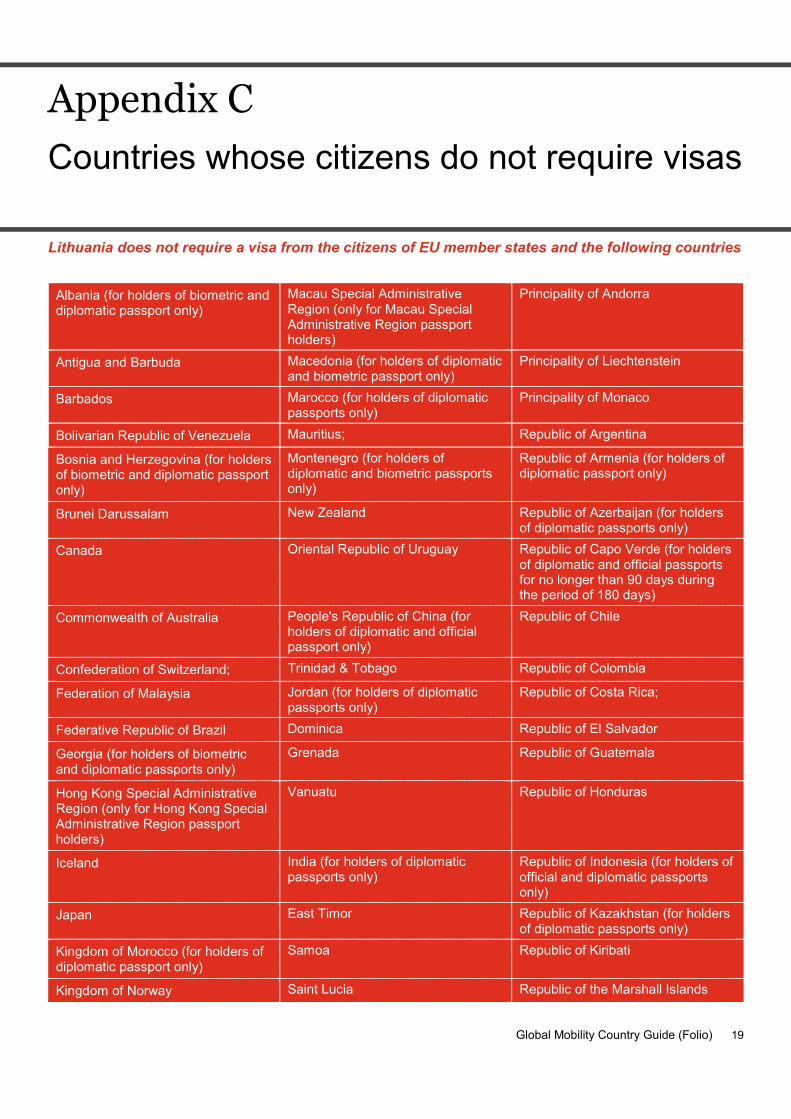

Appendix C Countries whose citizens do not require visas

Lithuania does not require a visa from the citizens of EU member states and the following countries

Albania (for holders of biometric and diplomatic passport only)

Macau Special Administrative Region (only for Macau Special Administrative Region passport holders)

Principality of Andorra

Antigua and Barbuda Macedonia (for holders of diplomatic and biometric passport only)

Principality of Liechtenstein

Barbados Marocco (for holders of diplomatic passports only)

Principality of Monaco

Bolivarian Republic of Venezuela Mauritius; Republic of Argentina

Bosnia and Herzegovina (for holders of biometric and diplomatic passport only)

Montenegro (for holders of diplomatic and biometric passports only)

Republic of Armenia (for holders of diplomatic passport only)

Brunei Darussalam New Zealand Republic of Azerbaijan (for holders of diplomatic passports only)

Canada Oriental Republic of Uruguay Republic of Capo Verde (for holders of diplomatic and official passports for no longer than 90 days during the period of 180 days)

Commonwealth of Australia People's Republic of China (for holders of diplomatic and official passport only)

Republic of Chile

Confederation of Switzerland; Trinidad & Tobago Republic of Colombia

Federation of Malaysia Jordan (for holders of diplomatic passports only)

Republic of Costa Rica;

Federative Republic of Brazil Dominica Republic of El Salvador

Georgia (for holders of biometric and diplomatic passports only)

Grenada Republic of Guatemala

Hong Kong Special Administrative Region (only for Hong Kong Special Administrative Region passport holders)

Vanuatu Republic of Honduras

Iceland India (for holders of diplomatic passports only)

Republic of Indonesia (for holders of official and diplomatic passports only)

Japan East Timor Republic of Kazakhstan (for holders of diplomatic passports only)

Kingdom of Morocco (for holders of diplomatic passport only)

Samoa Republic of Kiribati

Kingdom of Norway Saint Lucia Republic of the Marshall Islands

People and Organisation 20

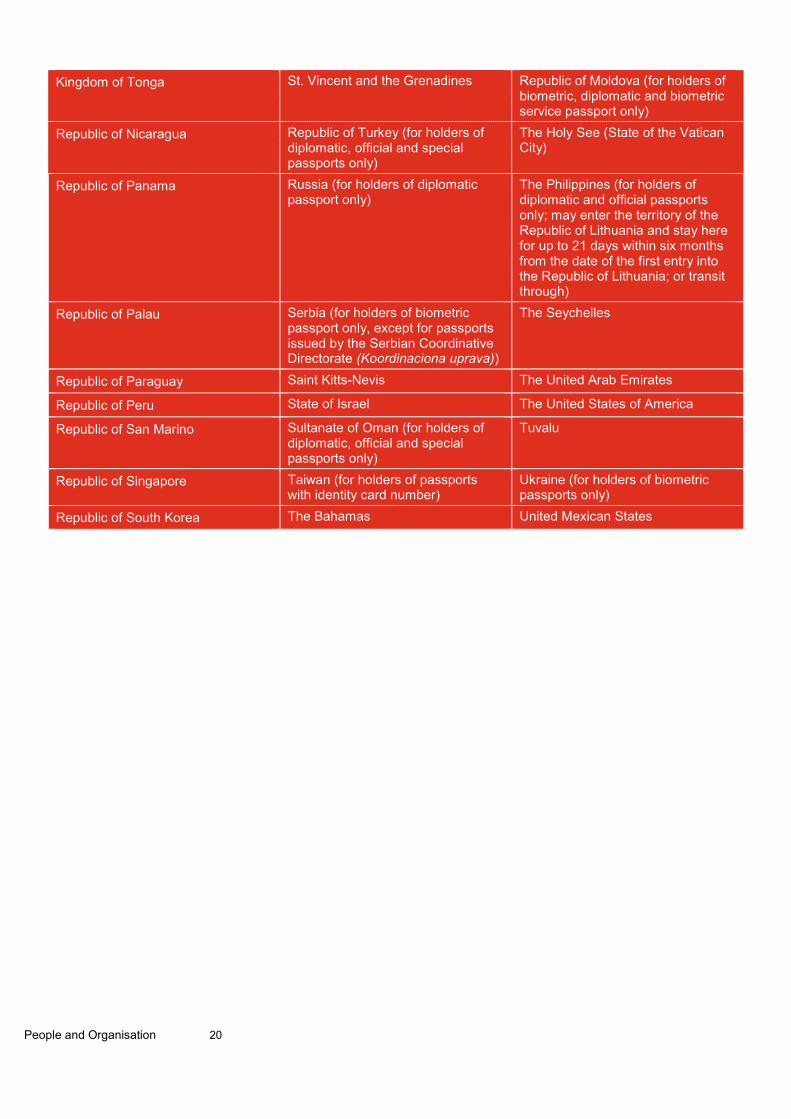

Kingdom of Tonga St. Vincent and the Grenadines Republic of Moldova (for holders of biometric, diplomatic and biometric service passport only)

Republic of Nicaragua Republic of Turkey (for holders of diplomatic, official and special passports only)

The Holy See (State of the Vatican City)

Republic of Panama Russia (for holders of diplomatic passport only)

The Philippines (for holders of diplomatic and official passports only; may enter the territory of the Republic of Lithuania and stay here for up to 21 days within six months from the date of the first entry into the Republic of Lithuania; or transit through)

Republic of Palau Serbia (for holders of biometric passport only, except for passports issued by the Serbian Coordinative Directorate (Koordinaciona uprava))

The Seychelles

Republic of Paraguay Saint Kitts-Nevis The United Arab Emirates

Republic of Peru State of Israel The United States of America

Republic of San Marino Sultanate of Oman (for holders of diplomatic, official and special passports only)

Tuvalu

Republic of Singapore Taiwan (for holders of passports with identity card number)

Ukraine (for holders of biometric passports only)

Republic of South Korea The Bahamas United Mexican States

Global Mobility Country Guide (Folio) 21

Appendix D Lithuania contacts and offices

Contacts

Vilnius office Vilnius office

Rasa Valatkevičiūtė Brigita Trakimavičienė

Tel: [370] (5) 239 2300 Tel: [370] (5) 239 2300

Email: [email protected] Email: [email protected]

Office

Vilnius office

PricewaterhouseCoopers UAB

J. Jasinskio st. 16B, Vilnius

LT-03163 Lithuania

Tel: [370] (5) 239 2300

© 2019 PricewaterhouseCoopers LLP. All rights reserved. "PricewaterhouseCoopers" refers to PricewaterhouseCoopers LLP (a Delaware limited liability partnership) or, as the context requires, the PricewaterhouseCoopers global network or other member firms of the network, each of which is a separate and independent legal entity. “PricewaterhouseCoopers” and “PwC” may also refer to one or more member firms of the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), each of which is a separate legal entity. PricewaterhouseCoopers does not act as agent of PwCIL or any other member firm nor can it control the exercise of another member firm’s professional judgement or bind another firm or PwCIL in any way.