Global Marketing Industry M&A Report 2020 - Clarity › wp-content › uploads › 2020 › 01 ›...

14

Global Marketing Industry M&A Report 2020

Transcript of Global Marketing Industry M&A Report 2020 - Clarity › wp-content › uploads › 2020 › 01 ›...

Global Marketing Industry M&A Report 2020

5 things you need to know...

13 4 5

2The Marketing Services M&A market remains resilient, up by 2% in 2019 vs a decline of 6.9% across the broader Global M&A market.

Over 550 transactions were by ”non-traditional”marketing services buyers, representing 51% of all deals. Global networks contributed a record low of only 3%.

Strong buyer and investor interest in Continental Europe, in particular Germany, Benelux and Nordics which saw over 100 transactions completed across those geographies.

US market remains very active, with 459 completed in 2019. Buyers increasingly focusing on marketing businesses with tech-enabled capabilities and agencies providing e-commerce solutions.

Financial sponsors remain a key buyercategory, accounting for 14% of all transactions. Larger funds are building marketing agencies and platforms of scale through acquisition, for example, Dept, North Alliance and PIA in Europe and Tinuiti and Wpromote in North America.

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services space. *Mergermarket 2019 Global M&A Report

5 THINGS YOU NEED TO KNOW

13 4 5

2THE MARKETING SERVICES M&A MARKET REMAINS RESILIENT, UP BY 2% IN 2019 vs. a decline of 7%* across the broader Global M&A market

OVER 550 TRANSACTIONS WERE BY ”NON-TRADITIONAL” MARKETING SERVICES BUYERS, REPRESENTING 51% OF ALL DEALS. Global networks contributed a record low of only 3%

STRONG BUYER AND INVESTOR INTEREST IN CONTINENTAL EUROPE, IN PARTICULAR GERMANY, BENELUX AND NORDICS which saw over 100 transactions completed across those geographies

US MARKET REMAINS VERY ACTIVE, WITH 459 COMPLETED IN 2019. Buyers increasingly focusing on tech-enabled capabilities and e-commerce solutions

FINANCIAL SPONSORS REMAIN A KEY BUYER CATEGORY, ACCOUNTING FOR 14% OF ALLTRANSACTIONS. Large Private Equity funds arebuilding marketing agencies and platforms of scale through acquisition, for example, Dept, The North Alliance and PIA in Europe and Tinuiti and Wpromote in North America

We have analyzed

OVER 1,100 MARKETING SERVICES TRANSACTIONS IN 2019

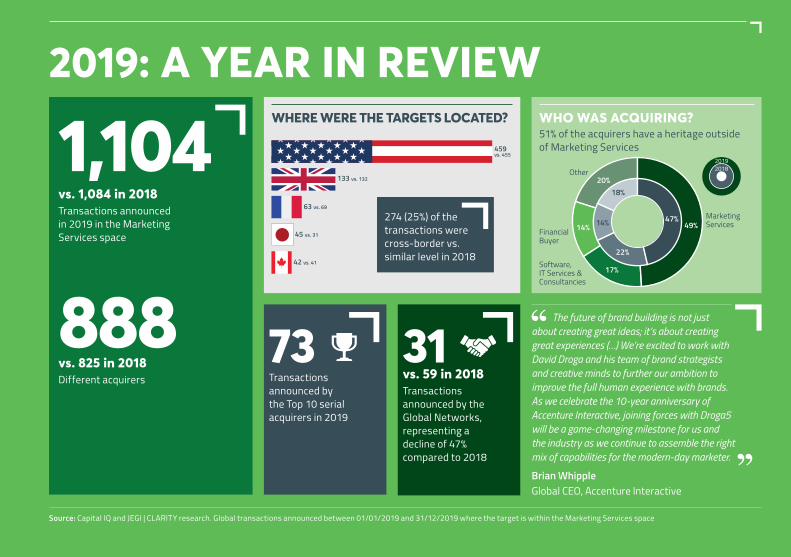

2019: A YEAR IN REVIEW

1,104vs. 1,084 in 2018Transactions announced in 2019 in the Marketing Services space

888vs. 825 in 2018Different acquirers

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services space

The future of brand building is not just about creating great ideas; it’s about creating great experiences (…) We’re excited to work with David Droga and his team of brand strategists and creative minds to further our ambition to improve the full human experience with brands. As we celebrate the 10-year anniversary of Accenture Interactive, joining forces with Droga5 will be a game-changing milestone for us and the industry as we continue to assemble the right mix of capabilities for the modern-day marketer.

Brian WhippleGlobal CEO, Accenture Interactive

WHERE WERE THE TARGETS LOCATED?

49%

20192018

47%

22%

14%

18%

14%

17%

20%

Marketing Services

Software, IT Services &Consultancies

Other

Financial Buyer

51% of the acquirers have a heritage outside of Marketing Services

WHO WAS ACQUIRING?

73Transactions announced by the Top 10 serial acquirers in 2019

31vs. 59 in 2018Transactions announced by the Global Networks, representing a decline of 47% compared to 2018

459 vs. 455

133 vs. 132

63 vs. 69

45 vs. 31

42 vs. 41

274 (25%) of the transactions were cross-border vs. similar level in 2018

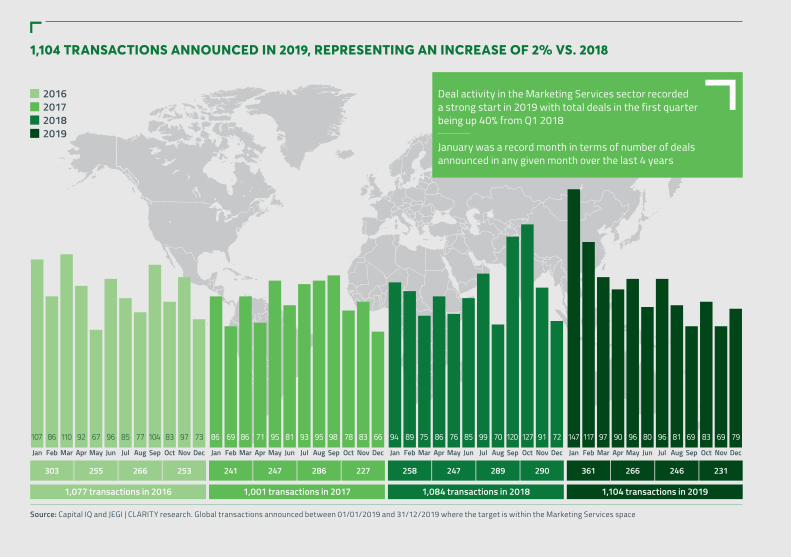

1,104 TRANSACTIONS ANNOUNCED IN 2019, REPRESENTING AN INCREASE OF 2% VS. 2018

Deal activity in the Marketing Services sector recorded a strong start in 2019 with total deals in the first quarter being up 40% from Q1 2018

January was a record month in terms of number of deals announced in any given month over the last 4 years

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services space

1,001 transactions in 2017

241 247 286 227

1,084 transactions in 2018

258 247 289 290

1,104 transactions in 2019

361 266 246 231

Jan

107 86 110 92 67 96 85 77 104 83 97 73

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

86 69 86 71 95 81 93 95 98 78 83 66

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

94 89 75 86 76 85 99 70 120 127 91 72

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

147 117 97 90 96 80 96 81 69 83 69 79

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016201720182019

1,077 transactions in 2016

303 255 266 253

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services space

NORTH AMERICAN AND EUROPEAN MARKETS REMAIN VERY ACTIVE

Top target locations:

Transactions by target location

45%vs. 46%

4%vs. 3%

34%vs. 38%

2%vs. 2%

13%vs. 10%

2%vs. 1%

Europe

Latin America

Asia

Africa and Middle East

501vs. 496 in 2018

40vs. 38 in 2018

379vs. 408 in 2018

19vs. 17 in 2018

138vs. 112 in 2018

27vs. 13 in 2018

North America

Australasia

459vs. 455in 2018

133vs. 132 in 2018

63vs. 69 in 2018

45vs. 31 in 2018

42vs. 41 in 2018

38vs. 47 in 2018

32vs. 33 in 2018

27vs. 19 in 2018

23vs. 11 in 2018

22vs. 22 in 2018

North America continued to be the largest region by deal volume in 2019

The total number of deals within Continental Europe and North America stayed relatively flat in 2019 with a moderate decline in France and Germany, of 6 and 9 deals respectively

The Netherlands, Italy and Finland, on the other side, recorded sharp increases, including the Carlyle acquisition of the leading Dutch agency Dept, on which JEGI | CLARITY advised

Asia recorded a strong increase of 23% in 2019 driven by Japan and India

Includes Media, Publishing, Telecoms, amongst others buyer types. Very strategic acquisitions that improve acquirer’s overall marketing/sales function

Financial buyers maintained a similar share of total acquisitions in 2019. Alpine and LDC were amongst the most acquisitive financial buyers

Accenture continued its strong activity in the space with the acquisition of creative agency Droga5 – understood to be AI’s biggest transaction since its founding

The Global Networks continued to represent a smaller proportion of total deals in 2019 (3% compared to 5% in 2018)

Increase in proportion of deals by Marketing Services buyers driven by both established groups (Next15, Finn Partners and Altavia) and more recently formed ones (S4, DEPT and Heroiks)

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services space

HALF OF THE ACQUIRERS WERE FROM A NON-TRADITIONAL MARKETING SERVICES BACKGROUND

Transactions by acquirer type

45%

7%

13%

14%

21%

2016 2017

1,077 1,001

41%

5%

22%

14%

18%

2018

1,084

46%

3%

17%

14%

20%

2019

1,104

50%

9%

12%

11%

18% Other

Financial Buyers

IT Services, Softwareand Consultancies

Global Networks

Marketing Services

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services space

25% OF ALL TRANSACTIONS WERE CROSS-BORDER

EuropeIn: 59

Out: 65

Africa and ME

In: 15Out: 4

AsiaIn: 23Out: 9

AustralasiaIn: 15Out: 6

Latin America

In: 5Out: 3

Split of cross-border transactions

TARGET LOCATION

UKEurope (excl. UK)

US RoW

BU

YER

LO

CA

TIO

N

UK 86 12 18 13

Europe (excl. UK)

24 198 18 16

US 18 32 401 36

RoW 5 4 22 201

Total 133 246 459 266

North American companies acquiring in Europe represented the largest proportion of cross-border transactions, 54, followed by European companies acquiring into North America, 36 (of which 18 had UK-based acquirers)

430

22

14

0

In/Out deals from region Transactions with target and acquirer in the same country within region

Transactions with target and acquirer from different countries within regionXX X

X

246

74

12

0

25

0

103

12

North America

In: 49Out: 79

54

11

2

2

7

10

9

7

5

1

1

1

2

11

1

24

5

36

3

1

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services space

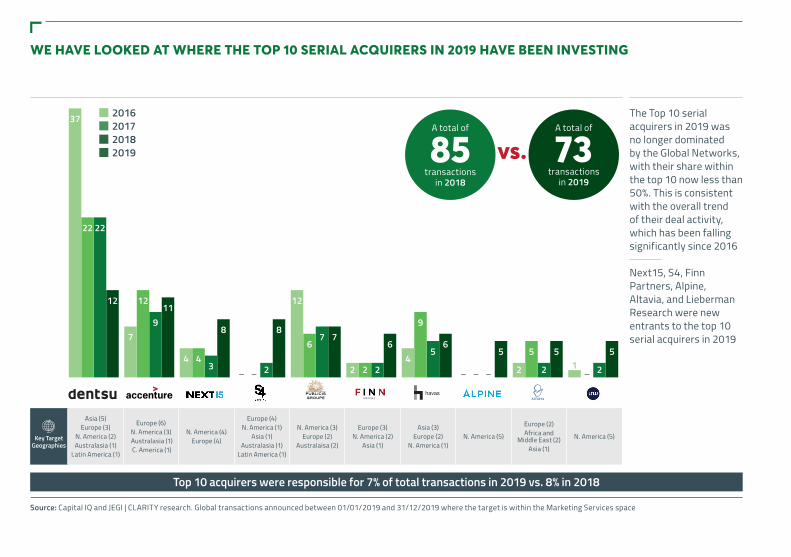

WE HAVE LOOKED AT WHERE THE TOP 10 SERIAL ACQUIRERS IN 2019 HAVE BEEN INVESTING

37

22 22

12

7

12

911

4 43

8

– – 2

8

12

67 7

2 2 2

64

9

56

– – –

5

2

5

2

51

– 2

5

The Top 10 serial acquirers in 2019 was no longer dominated by the Global Networks, with their share within the top 10 now less than 50%. This is consistent with the overall trend of their deal activity, which has been falling significantly since 2016

Next15, S4, Finn Partners, Alpine, Altavia, and Lieberman Research were new entrants to the top 10 serial acquirers in 2019

Top 10 acquirers were responsible for 7% of total transactions in 2019 vs. 8% in 2018

Key Target Geographies

Asia (5)Europe (3)

N. America (2)Australasia (1)

Latin America (1)

Europe (6)N. America (3)◦Australasia (1)◦C. America (1)

N. America (4)Europe (4)

Europe (4)N. America (1)

Asia (1)Australasia (1)

Latin America (1)

N. America (3)Europe (2)

Australaisa (2)

Europe (3)N. America (2)

Asia (1)

Asia (3)Europe (2)

N. America (1)N. America (5)

Europe (2)Africa and

Middle East (2)Asia (1)

N. America (5)

85transactions

in 2018

vs. 73transactions

in 2019

A total of A total of2016201720182019

Source: Capital IQ and JEGI | CLARITY research. Global transactions announced between 01/01/2019 and 31/12/2019 where the target is within the Marketing Services spaceNotes: 1 Value denotes the Implied Enterprise Value of the target; Converted into USD at announced date

NOTABLE TRANSACTIONS ANNOUNCED IN 2019

Some of the largest transactions in 2019 were…

ANN. DATE TARGET TARGET DESCRIPTION ACQUIRER VALUE1

($M)

Mar-19 Tranzact US-based end-to-end customer acquisition solutions provider

Willis Towers Watson 1,335

Apr-19 Droga5 US-based creative and strategic agency Accenture n.a.

Apr-19 Epsilon US-based data driven marketing company Publicis 4,400

Jun-19 Tableau US-based business analytics software provider Salesforce 16,322

Jul-19 Kantar US-based data, insights and consulting company Bain Capital 4,000

51% of deals involved non-traditional Marketing Services acquirers

ANN. DATE TARGET TARGET DESCRIPTION ACQUIRER VALUE1

($M)

Mar-19 Dynamic Yield US-based UX personalization platform McDonald’s 300

May-19 Pervorm NL-based digital marketing agency Deloitte n.a.

May-19 Sizmek(Ad server & DCO)

US-based ad server and dynamic creative optimization technologies

of SizmekAmazon n.a.

Oct-19 DataXu US-based demand-side-platform Roku 149

Dec-19 Exozet DE-based digital agency Endava n.a.

14% of the deals were led by financial investors

ANN. DATE TARGET TARGET DESCRIPTION ACQUIRER VALUE1

($M)

Jun-19 Teneo US-based communication advisory firm

CVC Capital Partners n.a.

Jul-19 Vungle US-based performance marketing platform Blackstone n.a.

Sep-19 Acquia US-based digital experience cloud-based platform

Vista EquityPartners 1,000

Oct-19 Cision US-based PR and Marketing communications software

Platinum Equity 2,783

Dec-19 Dept NL-based digital agency Carlyle n.a.

Other notable transactions

ANN. DATE TARGET TARGET DESCRIPTION ACQUIRER VALUE1

($M)

Jan-19 Trendkite US-based PR software Cision 224

Mar-19 Hjaltelin Stahl DK-based multi-channel marketing agency Accenture n.a.

Mar-19 Brainlabs UK-based technology-led digital marketing agency Livingbridge n.a.

Sep-19 Crossix US-based data analytics platform Veeva 432

Nov-19 Jellyfish UK-based digital agency Fimalac n.a.

JEGI | CLARITY transactions in 2019

A seamless combination of

KNOWLEDGE, INSIGHT AND EXPERTISE

JEGI | CLARITY – THE LEADING M&A ADVISORY FIRM FOR THE GLOBAL MEDIA, INFORMATION AND MARKETING, SOFTWARE AND TECH-ENABLED SERVICES SECTORS

Mobile & Internet

Data & Analytics

Cont

ent &

Info

rmat

ion

Cloud & SaaS

B2B &

B2C

MED

IA

& EV

ENTS

& TECH-ENABLED

SERVICES

SOFTWARE

MAR

KETING SERVICES

& TE

CHNOLOGYINFORMATION

BUSINESS

& INTELLIGENCE

HU

MA

N C

APITALM

AN

AGEM

ENT

I am super happy we chose JEGI | CLARITY to advise. Going into a process I wasn’t sure what the difference or value add would be; on the other side I can confidently say that they were the difference between a good and an exceptional outcome. At the same time as driving a fantastic process, they also represented us in a way that reflected our business culture. I would recommend them in a heartbeat!

Daniel GilbertChief Executive Officer, Brainlabs

This is the second time we have worked with the team and put simply we would never do another deal without them by our side.

Wesley ter Haar and Victor KnaapCo-Founders, MediaMonks

Working with entrepreneurs, founders, private equity firms, and global corporations

Over 60 people across London, New York, Boston and Sydney

Deep sector knowledge, providing out-of-market opportunities and outcomes

Track record of surpassing client expectations

Note: Selected JEGI | CLARITY transactions

WE REMAIN INCREDIBLY ACTIVE ADVISING RIGHT ACROSS THE MARKETING LANDSCAPE

HAS BEEN SOLD TO

A PORTFOLIO COMPANY OF

The Monkeys and Maud are leading Australian agencies.

Framestore is a leading VFX studio servicing the global featured film, advertising, and content markets.

FuseFX is a leading independent visual effects studio providing services for episodic television, feature films, commercials, and VR productions.

Accordant is a leading data-driven, full-service programmatic advertising company and technology solution provider.

A PORTFOLIO COMPANY OF

TO

HAS SOLD

Resource/Ammirati is a leading, US-based digital marketing and creative agency.

Selligent is an international SaaS platform delivering omnichannel audience engagement.

RKG is a leading tech-enabled search and digital marketing agency.

adam&eve is a leading creative advertising agency.

HAS BEEN SOLD TO

A CONSORTIUM OF CHINESE INVESTORS

HAS SOLD A 75% STAKE TO

LED BY

Brand Learning is a leading marketing and sales capability consultancy.

True Clarity is a leading ecommerce and experience platform services provider.

Webcollage is a leading product content management SaaS platform for global brands and retailers.

Blue 449 is a leading UK media agency.

ProSites is a leading provider of subscription-based digital marketing solutions for local community professionals.

JKR is a leading design-led creative agency.

TOPO is a leading research and advisory firm.

Hjaltelin Stahl is a leading Danish multi-channel experience agency.

SmartBrief is a leading digital media publisher of targeted business news and information by industry.

MERGE is a leading integrated healthcare and technology deployment agency.

Brainlabs is a leading technology-led digital marketing agency.

MediaMonks is a leading global creative production platform.

T3 is a leading CRM and digital design/innovation agency.

MeritDirect is a leading provider of multi-channel B2B database products and services solutions.

OPEN Health is a leading multi-disciplinary health communications and market access group.

DEPT is a leading independent digital agency.

HAS BEEN SOLD TO

A SUBSIDIARY OF

HAS BEEN SOLD TO

HAS MERGED WITH

S4 CAPITAL

HAS BEEN SOLD TO

A SUBSIDIARY OF

A PORTFOLIO COMPANY OF

HAS BEEN SOLD TO

HAVE BEEN SOLD TO

HAS BEEN SOLD TO HAS BEEN

SOLD TO

LONDON90 Long Acre London WC2E 9RA +44 20 3402 4900

SYDNEYL35, Tower One International Towers 100 Barangaroo Avenue Sydney, NSW 2000 +61 2 8046 6840

NEW YORK 150 East 52nd Street 18th Floor New York, NY 10022 +1 212 754 0710

BOSTON One Liberty Square 11th Floor Boston, MA 02109 +1 617 294 6555