Global Expansion Strategies - TAGLa · Global Expansion Strategies Greg Bryant, ... pays some...

36

Global Expansion Strategies Greg Bryant, Esq. Partner / International Tax Williams Mullen [email protected] +1 919.981.4001

Transcript of Global Expansion Strategies - TAGLa · Global Expansion Strategies Greg Bryant, ... pays some...

Global Expansion Strategies

Greg Bryant, Esq. Partner / International Tax Williams Mullen [email protected] +1 919.981.4001

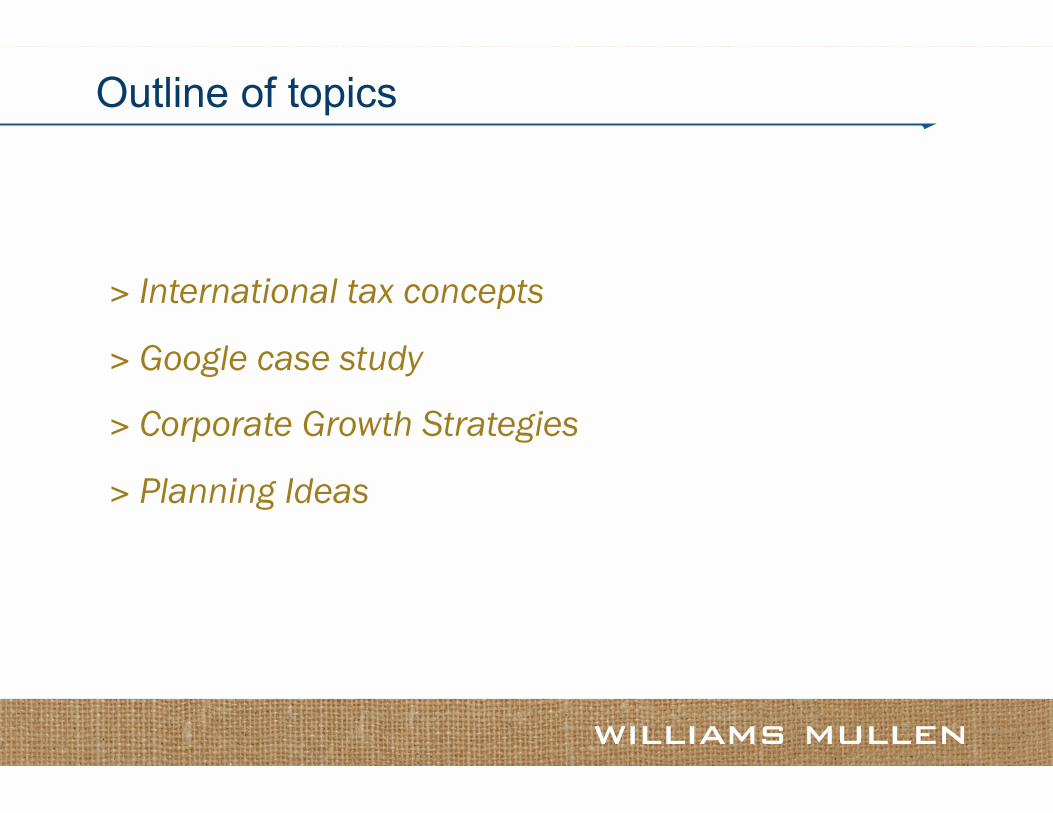

Outline of topics

> International tax concepts

> Google case study

> Corporate Growth Strategies

> Planning Ideas

International Tax Concepts

Concept Meaning Permanent Establishment Commonly used to define when a company has enough presence to

require it to file income tax returns

Transfer Pricing Required by law. The pricing of goods, services and intangibles that are transferred between related parties (more than 50% common ownership)

Indirect Tax Duties, and VAT that is included in the price of a product or service. VAT is generally "recoverable", meaning it can be charged through or refunded

DTA Double Tax Agreement: serves to reduce or eliminate source taxation

Character of Income The character of income often determines its taxation for withholding tax or other tax at source: Sale of goods Capital gain Service Rent or royalty

International Tax Concepts

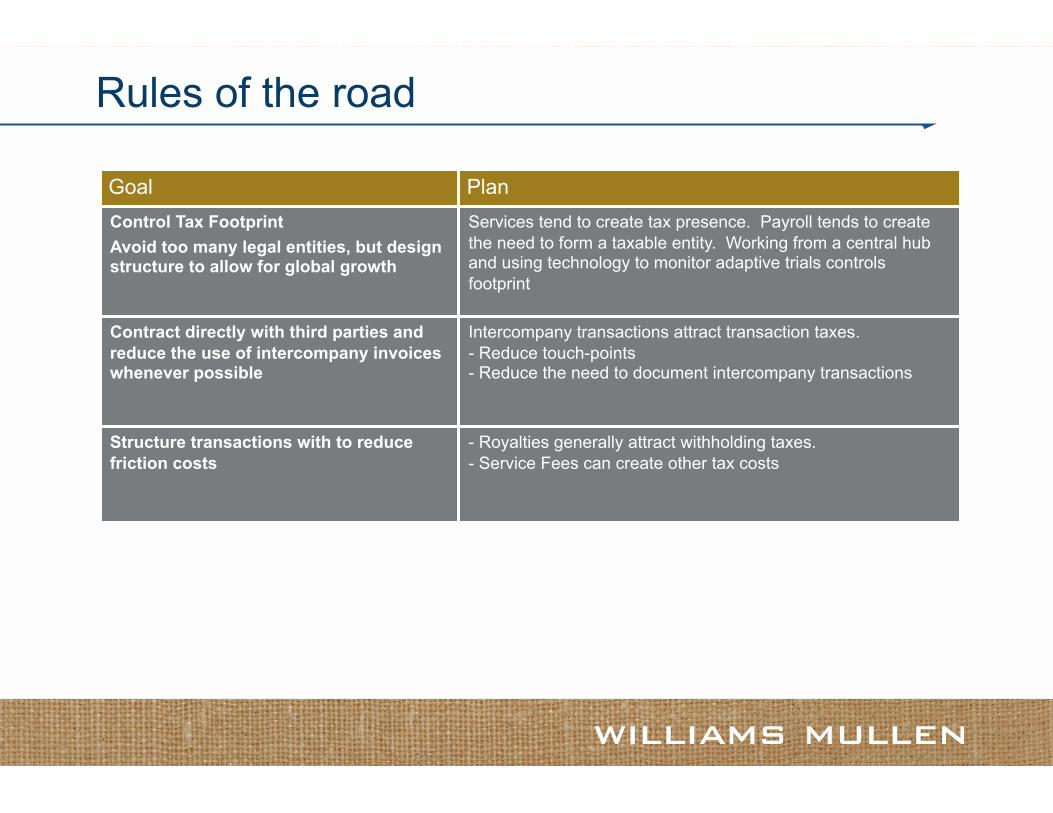

Goal Plan Control Tax Footprint Avoid too many legal entities, but design structure to allow for global growth

Services tend to create tax presence. Payroll tends to create the need to form a taxable entity. Working from a central hub and using technology to monitor adaptive trials controls footprint

Contract directly with third parties and reduce the use of intercompany invoices whenever possible

Intercompany transactions attract transaction taxes. - Reduce touch-points - Reduce the need to document intercompany transactions

Structure transactions with to reduce friction costs

- Royalties generally attract withholding taxes. - Service Fees can create other tax costs

Rules of the road

Factor Observations

Legal system Flexibility Exchange control Contract law Corporate governance Business model and path to market Business rules that favor international business

Costs Operational : location costs non-Operational: Tax and Money

Customer perception Cayman Islands and BVI can look bad

Stability Operational Infrastructure Tax rulings Tax system Political

Accessibility Aeropolis

Factors to consider

The facts Impact

Governments are broke They will shake every Euro out of the tree May create some protectionism More aggressive enforcement Base broadening Transfer pricing More indirect taxes

Unemployment is high Lets make a deal !!

More transparency in business Do not count on winning the audit lottery Be prepared to explain Transfer Pricing Accounting for income taxes requires more visibility

More need for operational efficiency Systems and processes now favor global hubs and centers of excellence

Structures can benefit from role specialization

Transfer pricing is viewed as a revenue raiser

Think proactively about transfer pricing

Current environment

Sept 19, 2012 - Senator Carl Levin (D-Mich), Senate Permanent Subcommittee on Investigations

"This isn’t just a wonky tax debate," ...."The tax moves employed by the two companies are especially relevant ..... as lawmakers engage in a heated debate over ways to close the budget deficit, and a possible overhaul of the tax code....." “We cannot close our budget gap without more revenue,”..... “The modern cause of this decline in corporate revenue is a plunge in corporate tax revenue.”..... "The high tech industry is probably the number one user of these offshore entities,” ..... “The tax practices and gimmicks range from egregious to dubious validity.”

Current trends

Bloomberg ... reports ... “about an elaborate tax scheme saving Google $3.1 billion. The company uses subsidiaries in Ireland, the Netherlands and Bermuda and, as a result, benefits from a stunningly low overseas tax rate of 2.4 percent. Considering the U.S. has a $1.4 trillion budget shortfall, havens like these threaten to tarnish Google's responsible corporate citizen image.”

Google Case Study

Google USA

Ireland Holdings

Ireland Services

/ /

Netherlands Regional Offices

Bermuda Owns IP for

Rest of World Customers /

Clients

Royalties & Advertising Revenue

90% paid as Royalty to NL

98% paid as Royalty to NL

Based on Bloomberg article by Jesse Drucker – Oct 21, 2010

Google Case Study

Customers pay Regional offices and Ireland directly

> Managing US Subpart F with check the box and look-thru treatment

Ireland pays royalties to Netherlands of 90% of profits

> Ireland taxation covered by advance ruling.

> Ireland Service company is paid Cost-Plus.

> Alternative structure would use a Non-Resident Ireland company.

Netherlands on-pays 98%

> Back to Back royalty

Bermuda non taxable

Entity Income Portion paid on

Portion taxable

Tax rate ETR

Regional 100% 98% 2% 35% . 7 %

Ireland 98% 88% (90% on-pay)

10% 12.5% 1.2 %

Netherlands 88% 86% (98% on-pay)

2% 25% . 5 %

Bermuda 86% 0 86% Nil Nil

2.40 %

Tax Rate on Structure

Microsoft USA

Ireland Holdings

Ireland Services

/ /

Puerto Rico

Regional Offices

Bermuda Owns IP for

Rest of World Customers / Clients

Royalties & Advertising Revenue

90% paid as Royalty to NL

98% paid as Royalty to NL

Based on Bloomberg article by Jesse Drucker – Oct 21, 2010

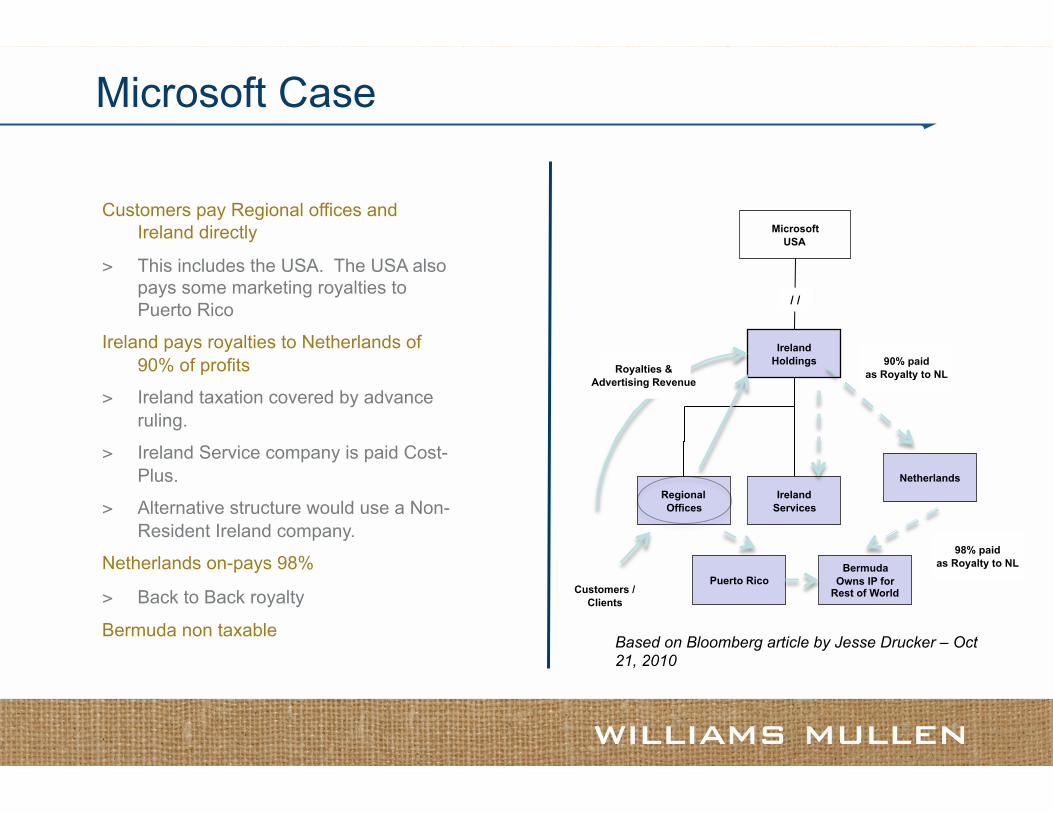

Microsoft Case

Customers pay Regional offices and Ireland directly

> This includes the USA. The USA also pays some marketing royalties to Puerto Rico

Ireland pays royalties to Netherlands of 90% of profits

> Ireland taxation covered by advance ruling.

> Ireland Service company is paid Cost-Plus.

> Alternative structure would use a Non-Resident Ireland company.

Netherlands on-pays 98%

> Back to Back royalty

Bermuda non taxable

Netherlands

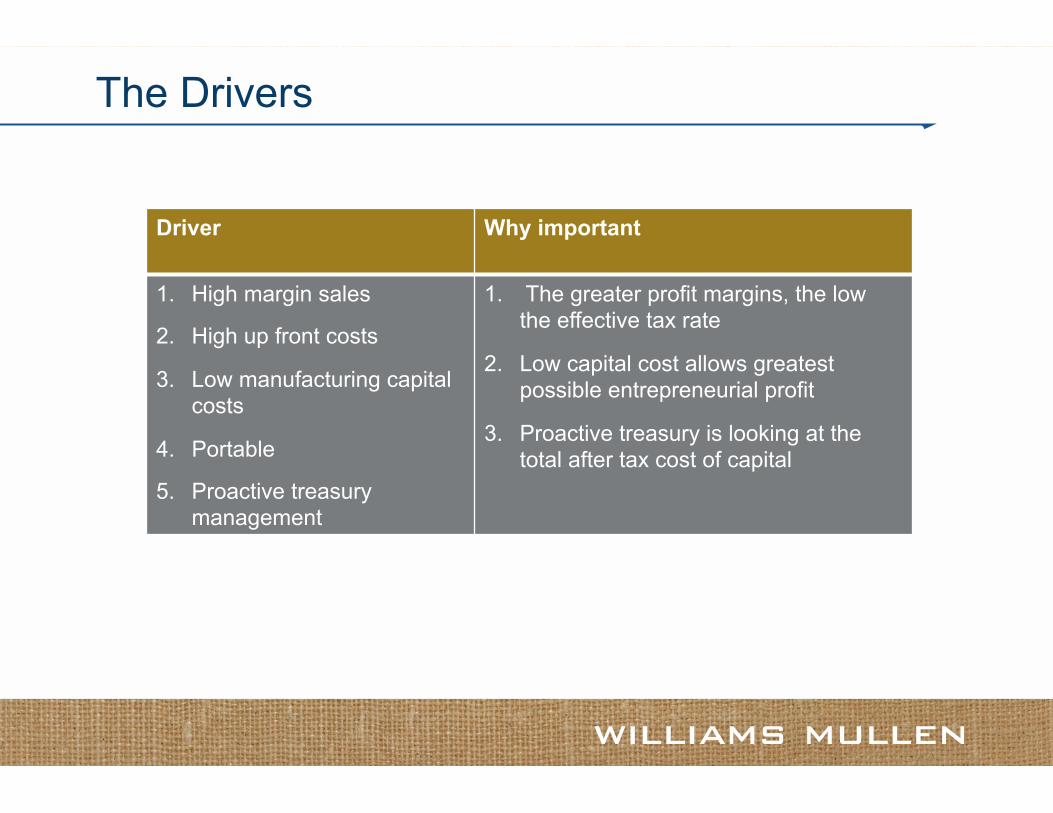

Driver Why important

1. High margin sales

2. High up front costs

3. Low manufacturing capital costs

4. Portable

5. Proactive treasury management

1. The greater profit margins, the low the effective tax rate

2. Low capital cost allows greatest possible entrepreneurial profit

3. Proactive treasury is looking at the total after tax cost of capital

The Drivers

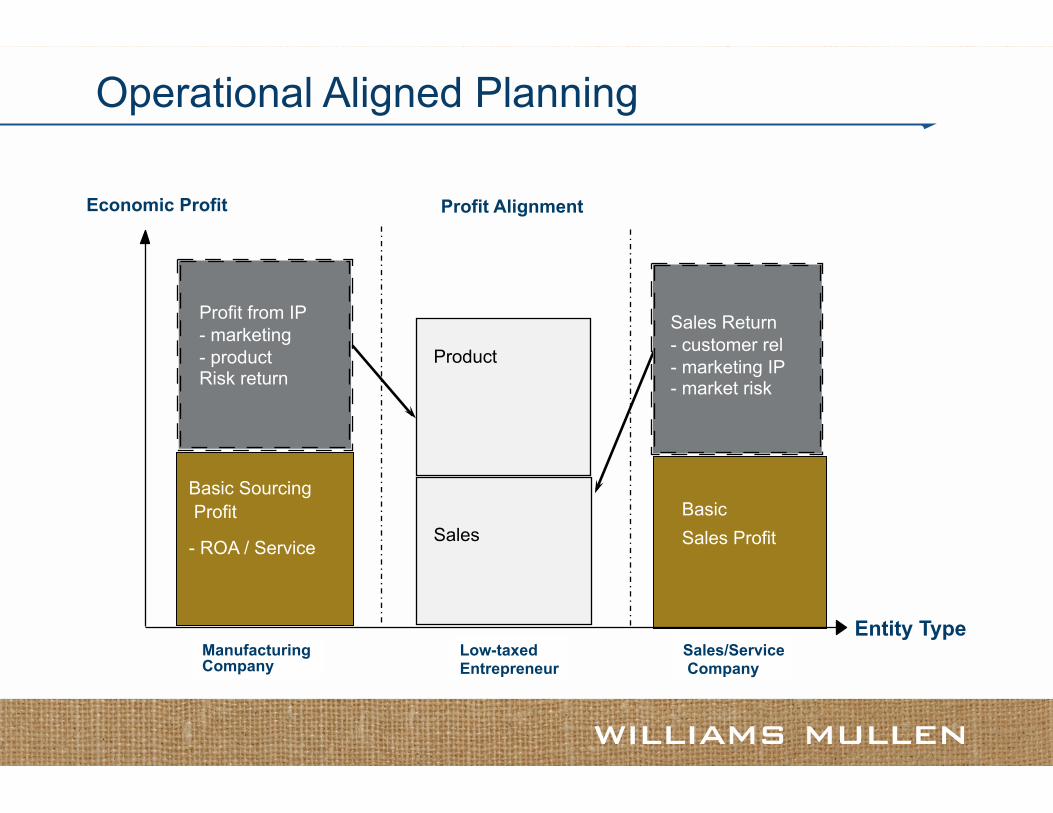

Manufacturing Company

Sales/Service Company

Entity Type

Economic Profit

Low-taxed Entrepreneur

Basic Sales Profit

Basic Sourcing Profit

- ROA / Service

Profit from IP - marketing - product Risk return

Sales Return - customer rel - marketing IP - market risk

Profit Alignment

Operational Aligned Planning

Entity Operations 35%

Trading Profit 5%

IP Profit 5%

Total Taxes

ETR

No Planning 100% 35

- - 100% 35 35%

Trading Profit and Risk

80% 28

20% 1

- 100% 29 29%

Trading and IP Alignment

60% 21

20% 1%

20% 1%

100% 22 22%

Comparison of structures

Current Profit Align Debt / Treasury Other

Foreign Taxes Element of Effective Tax Rate Effective Tax Rate Benchmarking

17 |

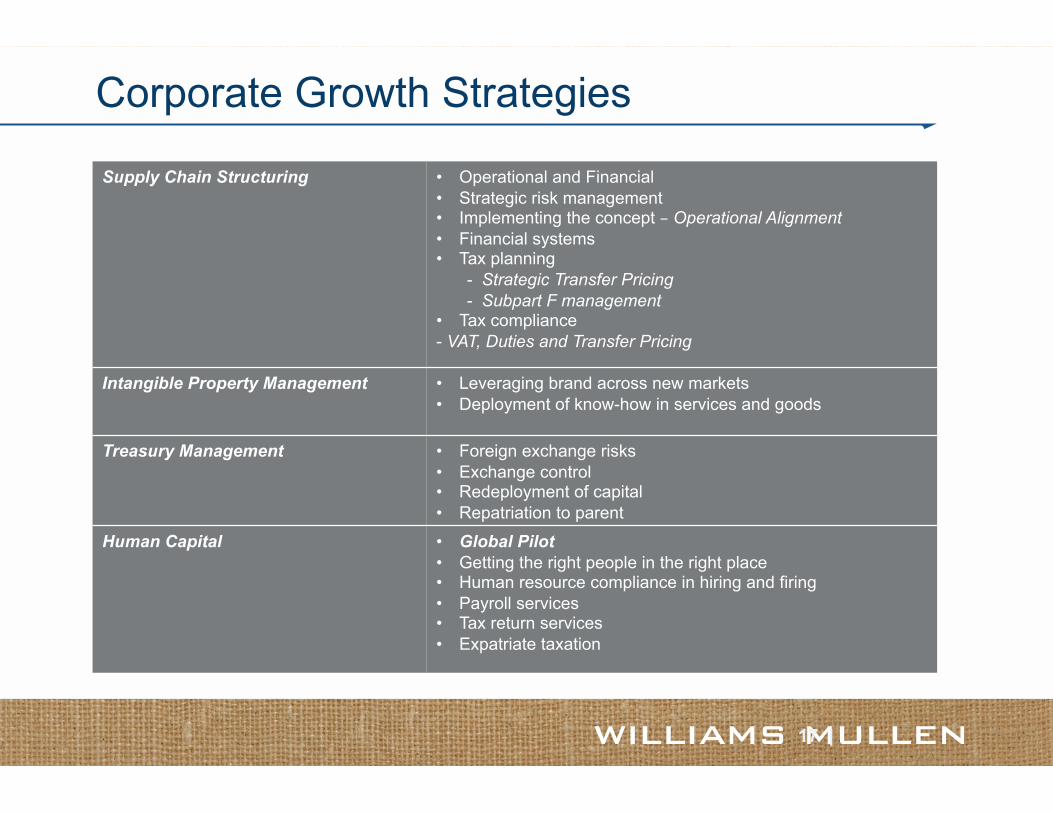

Supply Chain Structuring • Operational and Financial • Strategic risk management • Implementing the concept – Operational Alignment • Financial systems • Tax planning

- Strategic Transfer Pricing - Subpart F management

• Tax compliance - VAT, Duties and Transfer Pricing

Intangible Property Management • Leveraging brand across new markets • Deployment of know-how in services and goods

Treasury Management • Foreign exchange risks • Exchange control • Redeployment of capital • Repatriation to parent

Human Capital • Global Pilot • Getting the right people in the right place • Human resource compliance in hiring and firing • Payroll services • Tax return services • Expatriate taxation

Corporate Growth Strategies

Flexibility > Treasury management > Contract structuring > Business model and path to market

Simplicity > Less entities > Control tax footprint

Scalability > Managing IP to leverage into new markets > Ability to redeploy capital

Efficiency > Operational > Structural > Treasury > Tax > Legal – business rules that favor international business

Compliant > Legally > Tax and transfer pricing

Overriding - Goals

Value Drivers Goals

• Simplify structure

• Simplify transfer pricing model

• Reduce FX risk management

• Improve visibility over transfer pricing

• Reduce uncertain tax positions

• Manage cash tax liabilities

• Flexible and tax-efficient framework for redeployment of foreign cash and future acquisitions

• Tax efficient repatriation

• Optimize foreign tax credit position

• Maintain APB 23 assertion on earnings where APB 23 is currently asserted (a US GAAP concept)

Treasury Management

Risk managed Efficient

Cash Management

Tax Attribute Management

Profit Alignment

Foreign Tax Credit Utilization

Maximize Benefits of Foreign Losses

Tax Efficient Financing of Foreign Operations

Reduced Cash Taxes and Sustainable Effective Tax Rate

Manage Deferral Positions and Maximize Benefits of APB 23

Tax Efficient Repatriation

Tax Efficient Use of Intellectual Property

Satisfy US and Foreign Tax Requirements

Tax Efficient Cash Management and Redeployment

Overview – Integrated Treasury and Operational Structure

Service Offering Responsibility Specifics

Treasury Management

1. Broker all Group Financing 2. Manage all treasury risks 3. Asset Transfer 4. Manage Group Risks

1. Company negotiates and manages all movement of working and structural capital

2. Cash Pooling 3. All management reporting and

information management 4. Manage to predetermined

leverage and capital goals, pooling excess liquidity for efficient redeployment

Integrated Treasury

Service Offering Business Function Specifics

Cash Pooling 1. Use Intercompany Bank 2. Sweep cash 3. Can use outside bank to

manage sweep 4. FX management 5. Real time accounting for

cash and foreign exchange

1. Set up in Luxembourg 2. Larger companies use Swiss

or Swiss Dubai structures 3. Can outsource functions

Cash Pooling

Benefits Challenges

Simplifies movement of capital Getting into this high efficiency structure is usually a major transformation event. Requires: - High level buy-in - Usually an operations or strategic realignment to market

Creates debt in high tax locations that enables movement of funds

Centralization of key back office functions can create matrix reporting, which can be difficult to manage in the long term

Harvest foreign tax credits now - Can harvest high tax before low tax

This requires a clear plan and flawless execution

Improves visibility on working capital, and transfer pricing and provides better treasury controls on management of foreign exchange

Foreign tax credits can be managed to create high and low tax pools

Improves after-tax cash flow by improving the management of IP and by making the movement of product and services more efficient.

Consider structures to improve supply chain management

The Good and the Bad

Factor Observations

Legal system • Must be in the EU to get license to import • Exchange control • Contract law • Corporate governance • Business model and path to market • Business rules that favor international business

Costs • Operational: location costs • Non-Operational: tax and money

Customer perception • Cayman Islands and BVI can look bad • Dubai for the Middle East • EU for imports into Europe

Stability • Operational • Infrastructure • Tax rulings • Tax system • Political

Accessibility • Access to good 3PLs and other service providers - Operational support - Back office

Factors to Consider

Planning Illustrations

Netherlands / Swiss

PARENT

Suppliers Unrelated CUSTOMERS

//

Flow of Services

Contract Flow

US

ROW

Netherlands or Swiss/Dubai Principal ZERO TAX: Corporate and Individual > Stable > Works with US non-Corporate structures > Excellent for ME, India and Russia > Can benefit from Dutch / Swiss double tax treaties (over 70) > Netherlands is a member of EU > Excellent platform for EU holding company and financing

structure to non-EU based borrowers > Can get rulings to reduce taxation on relocated staff > Dividends to the Netherlands / Switzerland qualify for the

participation exemption as long as there are real activities in Dubai

> -- Personnel > -- doing something: logistics, sales, risk management,

inventory management, regional management. > Can combine with Luxembourg and get a Zero Rate (like

notional branch illustration) – Not easy to staff – must bring in expats – Far from SE Asia and South America

Considerations > Requires substance in Dubai

– 1 Full Time Equivalent (FTE) at least – Consider time centric / travel access for on site visits

> If US is a S Corp or LLC (transparent) the withholding tax from the Netherlands to the US would likely be 15%. Swiss is a similar net effect, but requires withholding and refund.

> --- CONSIDER USING HOLDING CO OR CV ABOVE STRUCTURE IF US REPATRIATION IS IMPORTANT.

> Rulings recommended

GLOBAL OR REGIONAL TRADING\

DUBAI

Sales / Brokering

Customers Customers

OTHER FOREIGN COMPANIES

NEW MARKETS

Liux / CV

CUSTOMERS

Entity Income Portion paid on

Portion taxable

tax rate ETR

Supplier 100% 98% 2% 35% . 65 %

Dubai Global 98% 98% Nil Nil %

Netherlands 98% 0% 25% Nil

.65 %

Tax Rate on Structure

REGIONAL HQ and PRINCIPAL

Suppliers

//

Flow of Services

Contract Flow

US

ROW

Singapore Principal Location and stable > Excellent for SE Asia, China, India and Russia > Can benefit from Singapore double tax treaties (over

70) > Can get rulings to reduce taxation on relocated staff > Dividends paid by Singapore principal remain exempt

from withholding under Singapore local law (no treaty required)

> Generally not hard to staff – Not as tax advantaged as Lux / Dubai

Corporate tax rate is 17% in Singapore > Can negotiate tax holiday for IP company > Ruling is based on job creation and IP ownership

• Certainty • Requires physical presence in Singapore and

headcount in Singapore • SEDB will be advocate for company

> Can benefit from Singapore double tax treaties > Singapore is an excellent HQ location for SE Asia,

including Malaysia, Indonesia, Vietnam and Australia > Avoids use of a tax haven jurisdiction > Can get rulings to reduce taxation on relocated staff > No withholding tax on Dividends Considerations > Requires substance in Singapore to get any tax

advantaged ruling > 10 to 25 local employees (10-15 FTE)

Service Sales / Brokering

PARENT

Customers Suppliers

Suppliers

CHINA and OTHER ASIA

Entity Income Portion paid on

Portion taxable

tax rate ETR

Supplier 100% 98% 2% 35% . 65 %

Singapore 98% 98% 15% 14.7 %

15.35 %

Tax Rate on Structure

Structure: > Works well for Franchise / Service related

business models

> Parent (limited partner) and LLC (general partner) establish a NL limited partnership (CV).

> Parent equity funds CV and elects to treat CV as a foreign corporation. CV is flow-through for NL tax (reverse hybrid).

> CV holds the shares in a NL holding (BV or Coöp) and funds NL Holding with a loan

> NL Holding holds foreign subsidiaries and funds foreign subsidiaries with loans

> Works best with Debt Pushdowns and Licensing of IP (Software or Product IP).

> Under Dutch law there is no withholding tax on interest on loans from CV and from Royalty Income.

CV

PARENT CO

Netherlands Treasury

Center

Disregarded Entity

For US Tax

Disregarded Entity

For US Tax

Disregarded Entity

For US Tax

LLC General Partner

Loan License

Loan License /

Franchise

Dutch Finance Structure with a CV – Debt Pushdowns /Royalty Strip

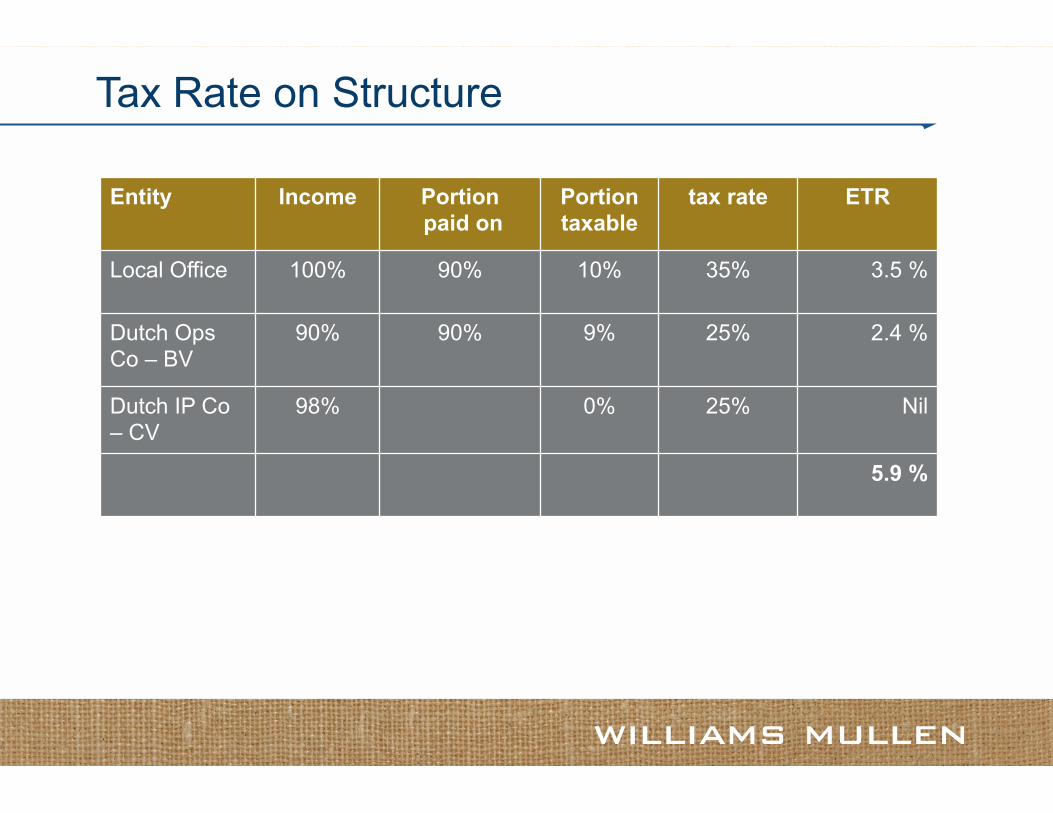

BV

Service Franchise

Entity Income Portion paid on

Portion taxable

tax rate ETR

Local Office 100% 90% 10% 35% 3.5 %

Dutch Ops Co – BV

90% 90% 9% 25% 2.4 %

Dutch IP Co – CV

98% 0% 25% Nil

5.9 %

Tax Rate on Structure

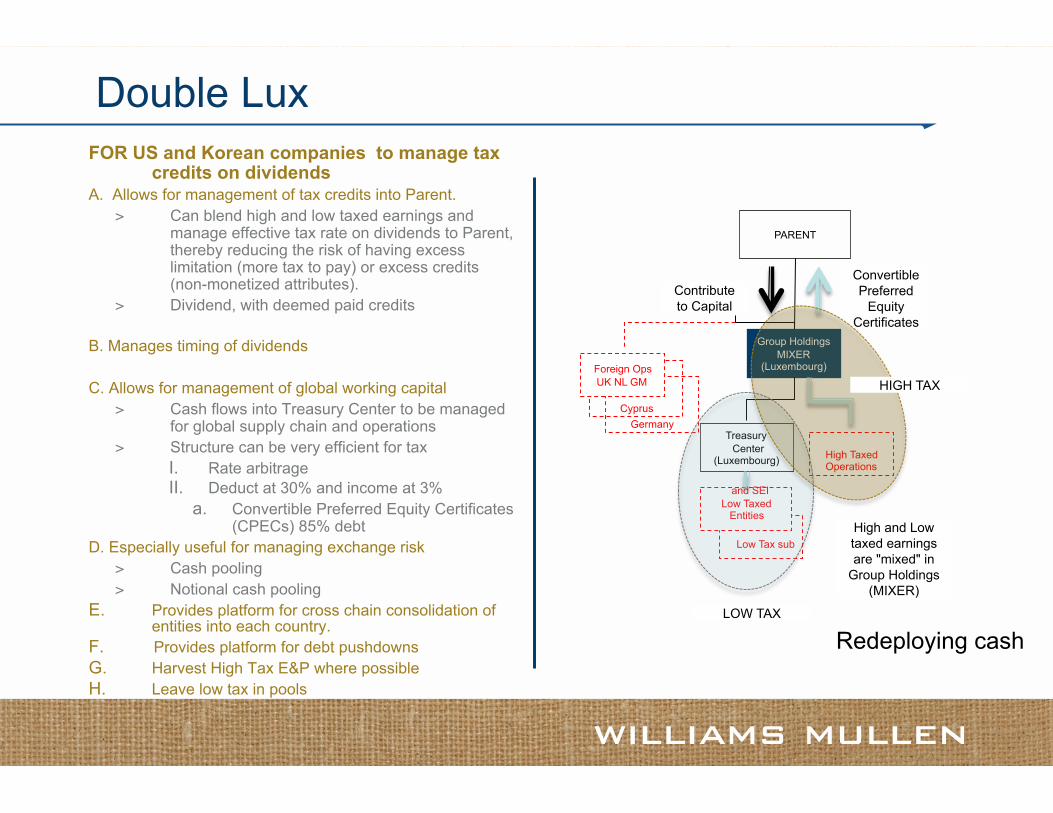

FOR US and Korean companies to manage tax credits on dividends

A. Allows for management of tax credits into Parent. > Can blend high and low taxed earnings and

manage effective tax rate on dividends to Parent, thereby reducing the risk of having excess limitation (more tax to pay) or excess credits (non-monetized attributes).

> Dividend, with deemed paid credits

B. Manages timing of dividends

C. Allows for management of global working capital > Cash flows into Treasury Center to be managed

for global supply chain and operations > Structure can be very efficient for tax

I. Rate arbitrage II. Deduct at 30% and income at 3%

a. Convertible Preferred Equity Certificates (CPECs) 85% debt

D. Especially useful for managing exchange risk > Cash pooling > Notional cash pooling

E. Provides platform for cross chain consolidation of entities into each country.

F. Provides platform for debt pushdowns G. Harvest High Tax E&P where possible H. Leave low tax in pools

CFC

Germany

Low Tax sub

CFC

Cyprus

PARENT

Group Holdings MIXER

(Luxembourg)

Contribute to Capital

Treasury Center

(Luxembourg)

Convertible Preferred

Equity Certificates

Foreign Ops UK NL GM

High Taxed Operations

High and Low taxed earnings are "mixed" in

Group Holdings (MIXER)

and SEI Low Taxed Entities

LOW TAX

HIGH TAX

Double Lux

Redeploying cash

Entity Income Portion Paid On

Portion Taxable

Tax Rate ETR

Local Ops Co 100% 98% 2% 35% . 65 %

Lux Treasury 98% 85% from CPEC

13% 29% 3.77 %

4.42 %

Tax Rate on Structure

Country Observations

Hong Kong + Can achieve low tax rate: 8.25% + Friendly business environment + Excellent launch-point for China

- Not as good as Singapore for other SE Asia

Switzerland + Can achieve very low tax rates if company puts in large head-count – 75 to 100 people

+ Good location for coordinating EMEA

- Expensive, even by comparison to HK and Singapore - Was Hot, but after UBS it is getting cooler

Other Options

This presentation is for discussion purposes only.

Questions?

Thank you!

This presentation is for discussion purposes only.

The opinions and conclusions contained in this memorandum are based in part on the completeness and accuracy of the above-stated facts and assumptions. If any of these facts and assumptions are not complete and accurate, please notify us immediately as we may have to materially modify the opinions and conclusions of this memorandum. We are relying upon the relevant provisions of the Internal Revenue Code of 1986, the regulations thereunder, and judicial and administrative interpretations thereof, which exist as of the date of this opinion. These provisions are subject to change or modifications by subsequent legislative, regulatory, administrative, or judicial actions or decisions. Any such changes could have a material effect on the opinions and conclusions of this memorandum. Unless specifically requested, we will not update our advice for subsequent changes to the law and/or regulations or the judicial and administrative interpretations thereof. The use of this memorandum is strictly limited to the management of the party for which it is intended.

U.S. Treasury Department Circular 230 Disclosure: In accordance with applicable professional regulations, please understand that, unless specifically stated otherwise, any written advice contained in, forwarded with, or attached to this communication is not a tax opinion and is not intended or written to be used, and cannot be used, by any person for the purpose of (i) avoiding any penalties that may be imposed under the Internal Revenue code or applicable state or local law provisions or (ii) promoting, marketing or recommending to another party any tax-related matters addressed herein.