Global Entertainment and Media Outlook 2018-2022 · TV advertising Video games and e-sports Virtual...

21

Global Entertainment and Media Outlook 2018-2022 www.pwc.com/outlook

Transcript of Global Entertainment and Media Outlook 2018-2022 · TV advertising Video games and e-sports Virtual...

Global Entertainment and Media Outlook 2018-2022

www.pwc.com/outlook

PwC’s Digital Services 2

$Consumer/end-user & advertising spending

5 Year historical & 5 Year forecast data 53 Countries 15 Segments

www.pwc.com/outlook

Books

Business-to-business

Cinema

Internet access

Internet advertising

Magazines

Music, radio and podcast

Newspaper

OTT video

Out-of-home advertising

Traditional TV and home video

TV advertising

Video games and e-sports

Virtual reality

Data consumption

PwC’s Digital Services 3

What are the Global Trends?

PwC’s Digital Services

Expected global growth in E&M expenditures of 4.3%

4

BRIC: 7.5 %

Mature: 3.1 %

Scandinavia3.3 %

Russia8.8 %

UK 3.2 %

France 2.2 %

Germany 2.0 %

US3.5 %

Brazil5.3 %

India11.6 %

China7.2 %

Japan2.3 %

Global4.3 %

PwC’s Digital Services

Internet advertising and internet access are expected to lead growth across media segments in the Scandinavian E&M market towards 2022

5

Internet access

Books

Newspaper

-0.3%

-2.2%

-4.6%

Magazines

Music, radio and podcasts

Traditional TV and home video

TV advertising

Business-to-business

Video games and e-sports

Internet advertising

2.3%

8.2%

2.8%

8.2%

2.5%

1.5%

2.4%

5.3%

6.8%

0.9%

Cinema

Out-of-home

OTT video

Scandinavian growth by segment 2017-2022F

PwC’s Digital Services

Smart Speaker market will grow by more than 20% per year due to broad personal and commercial adoption

6

Smart Speaker Market size is projected to exceed $30 billion in 2024, with a cumulative annual growth rate of more than 20%

>20%

High growth expectations

>26%The growth in commercial applications is projected to be even higher, with an estimated cumulative annual growth rate of more than 26%

>4.5The current size of the Smart Speaker Market is more than $4.5 billion, according to Global Market Insights

Source: Global Smart Speaker Market Size worth over $30bn by 2024 (2018) Global Market Insights, Inc.

Customer demand due to improved quality and personlisation will overtake the productivity gains

PwC’s Digital Services

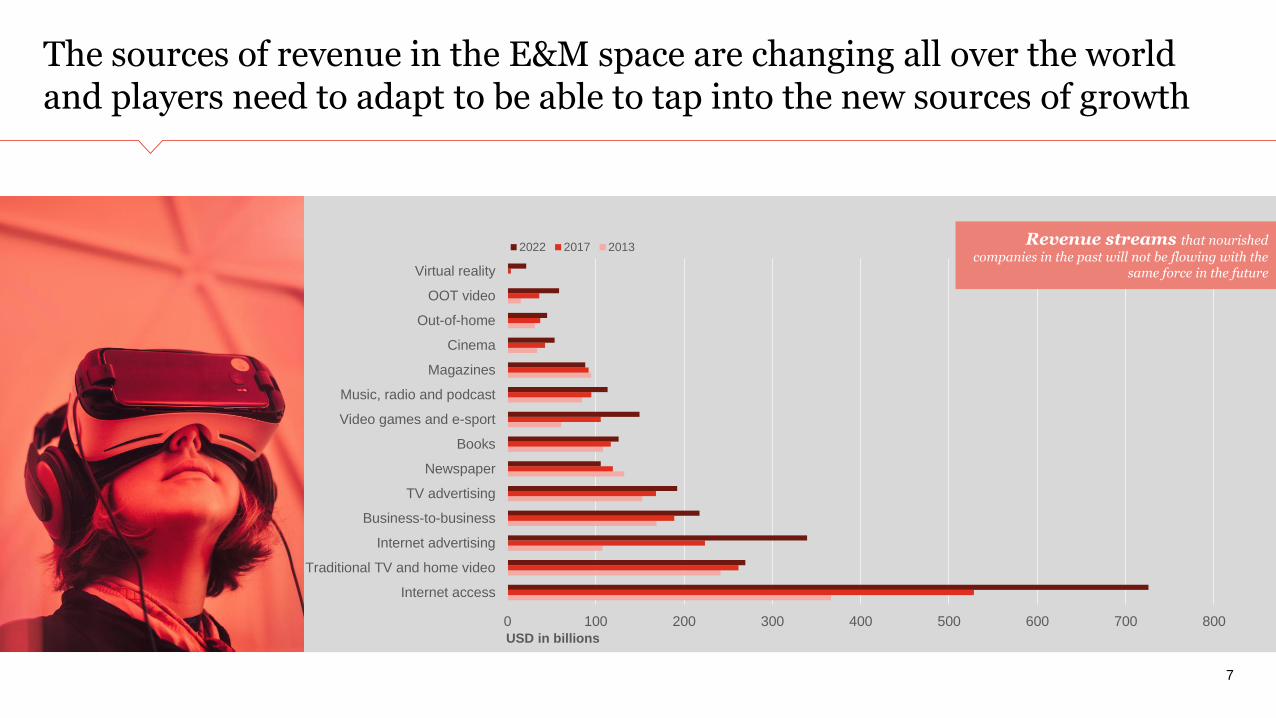

The sources of revenue in the E&M space are changing all over the worldand players need to adapt to be able to tap into the new sources of growth

7

0 100 200 300 400 500 600 700 800

Internet access

Traditional TV and home video

Internet advertising

Business-to-business

TV advertising

Newspaper

Books

Video games and e-sport

Music, radio and podcast

Magazines

Cinema

Out-of-home

OOT video

Virtual reality

2022 2017 2013Revenue streams that nourished

companies in the past will not be flowing with the same force in the future

USD in billions

PwC’s Digital Services 8

The distinctions among varieties of media are collapsing

PwC’s Digital Services

Announced deal values increased by 197% in the first half of 2018, fueled by megadeal activity

Internet & Information

Telecommunications

Cable

Broadcasting

Recreation & leisure

Film & Content

Advertising & Marketing

Publishing

Music

9

97

41

5

26

30

33

143

54

7

Deal volume Deal value ($M)

H1 2018 US announced deal volume and value by subsector

30 673

29 255

10 522

5 514

2 320

1 707

1 361

1 057

14

Source: PwC Deals US Technology Deals insights Q2 2018

§26.8billion USD

Largest mergers

PwC’s Digital Services

The forces driving convergence will lead to emergence of supercompetitors

A group of global supercompetitors that are involved in most, if not every, segment of E&M

10

Convergence towards similar business models will unite content, commerce, advertising, communications and deep financial resources

Supercompetitors can buy content, invest in startups and serve as buyers for maturing businesses

..combined hold a share of 57% of digital advertising revenue in the US

..deliver 25% of all the packages in the US..

..and it is expected to be 50% in 2020

PwC’s Digital Services 11

Reinventing Media Business Models and the Revenue Stream Revolution

PwC’s Digital Services

The global video game industry is projected to grow by 28 percent between 2018 and 2022

12

-

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F

US

D i

n m

illi

on

s

Global video games

Video games advertising

7.3 %

Social/casual vide gaming 9.2 %

Traditional video gaming 4.7 %

2017 – 2022F CAGR

7.1%

PwC’s Digital Services

-

500

1 000

1 500

2 000

2 500

3 000

2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F

US

D i

n m

illi

on

s

Scandinavian filmed entertainment revenues

On demand video services are expected to drive the growth of the Scandinavian filmed entertainment market

13

2017 – 2022F CAGR

4.2 %

Cinema tickets 2.6 %

OTT video 6.8 %

Electronic home video 3.7 %

Physical home video -8.2 %

PwC’s Digital Services

-

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F

US

D i

n m

illi

on

s

Linear and online TV advertising in Scandinavia

Online TV advertising is expected grow rapidly towards 2022

14

2017 – 2022F CAGR

2.4 %

Online TV 14.6 %

Linear TV 1.2 %

PwC’s Digital Services

-

1 000

2 000

3 000

4 000

5 000

6 000

2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F

US

D i

n m

illi

on

s

Scandinavian Newspaper Market

Newspapers succeed by encouraging a membership mind-set

15

2017 – 2022F CAGR

-4.6 %

Print advertising -8.8 %

Digital advertising 3.7 %

Print circulation -6.5 %

Digital Circulation 13.8 %

PwC’s Digital Services

-

100 000

200 000

300 000

400 000

500 000

600 000

700 000

2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F

Da

ta c

on

su

mp

tio

n in

mil

lio

n G

Bs

Global data consumption

16

The amount of data consumed globally is expected to grow annually by more than 25%

2017 – 2022F CAGR

Fixed broadband 18.8 %

Other portable 21.8 %

Tablet 25.9 %

Non-smartphone 12.4 %

Smartphone 33.3 %

25.1 %

PwC’s Digital Services 17

TRUST

PwC’s Digital Services

74%

57%

The rising importance of data is pushing trust to an even more central position

18

Is your content trustworthy?

Is your audience who you say it is?

Are you taking proper care of the data?

Are your investments paying off?

Is your company good for society?

Five vital dimensions of trust 76% of CEOs said

potential for biases and lack of transparency were impeding AI adoption in their enterprises

PwC CEO Pulse Survey 2017

PwC’s Digital Services

E&M CEOs remain optimistic about

longer term prospects, but are more concerned

about digital disruption than CEOs across all industries

19

of E&M CEOs are confident about their companies revenue

growth over the next 3 years

94 %

of E&M CEOs said changes in consumer behaviour would be

«somewhat or extremely disruptive»

86 %

of E&M CEOs said changes in distribution

channels would be «somewhat or

extremely disruptive»

69 %

of E&M CEOs are extremely concerned

about over-regulation

34 %

of E&M CEOs are confident about their companies revenue

growth over the next 3 years

81 %

20

PwC’s Digital Services

Contact us!

Eivind Nilsen

Partner

952 60 832

Øystein B. Sandvik

Director

952 60 415

21