Diamonds in the Rough: A Review of Tiffany v. Costco and a ...

Upload

mines-and-moneyCategory

view

2.447download

1

Private and confidential

Global Diversified Mining

Diamonds in the rough

Source: Lucara Diamond finds 1,111 ct stone, the second largest since the Cullinan diamond (3207 cts) in 1905

Tim Clark

+27 11 415 4295

11Diamonds in the rough

2013-14 was a strong period for diamonds, with prices +12%, though volumes declined

marginally. There was great hope that this was early signs of industry prosperity.

Rising debt pressures (financing, bankruptcies) and slower demand pushed polished

inventories into surplus in late 2014. Since then, miners first cut prices (-7% in 1H15), then

volumes (De Beers sold 3m cts in 3Q15, versus a run rate of 7.5m cts per quarter).

Polished prices recently ticked up, and we believe that inventories are clearing. The US

selling season (Thanksgiving to New Year) will determine if markets recover in 2016 or 2017.

We foresee a 2Q16 recovery.

We estimate that De Beers will increase diamond stocks from 3 to 7 months (mostly in

Debswana) by FY15e, and that Alrosa (Not covered) will increase from 5 to 10 months. If the

US selling season is good, inventories are likely to be drawn down through 2016e; if the

season is weak, we would expect a 30-50% production guidance decline in the short term.

Diamond markets are

highly consolidated

and the product is

relatively scarce

(limited long term

growth potential).

A series of factors has

resulted in high

polished inventories.

As a result prices fell

7% in 1H15, now

volumes have been

held back by the

miners. This is one of

the few markets with

producers exercising

supply constraint.

The US selling season

will set the scene for

2016.

Key points

22

Diamonds were formed 990-3.2bn years ago, 100-200kms below the earth’s

surface at 900-1300 degrees Celsius and at pressures of 45-60 kilobars

Udachnaya

Yubileynaya

Mir

Kokchetav

Western Gneiss

Region

AkluilãkLac de Gras

Snap Lake

Erzgebirge

Guaniamo

Kankan

C.A.R.

(Carbonado)

Dabie

Sulawesi

North Qaidam

Majhgawan

Wajrakarur

Junia

(São Luiz)

Poxoréu

(Carbonado)São

Francisco

Orapa

Jwaneng

Venetia

Monastery

Kimberley

Koffiefontein

Jagersfontein

Premier

Argyle

Orrorroo

New South

WalesArchon

Proton

Tecton

Source for all charts: Geological Survey of India; SBG Securities analysis

33Rough and polished market update

De Beers cut

prices 7% in

1H15, volumes

are now being

‘deferred’

Rough prices

remain above

polished and the

pipeline is in a

tough place. The

miners would

prefer to starve

inventory and

stem a polished

recovery. The

traders are

happy with a

rough price

rebase.

There is some

evidence of

polished prices

ticking up

recently.

Rough and polished pricesDe Beers prices and volumesKey points

Sample of rough diamond prices2015, sample of rough diamond prices

Source for all charts: Bloomberg, Datastream, company data, SBG Securities analysis & estimates

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Price change (est) Production/ sales (where known)

0

50

100

150

200

250

300

Rough Polished

70

80

90

100

110

120

130

140

150

Diamonds-1 Carat G VS2 Diamonds-0.3 Carat G VS2

Diamonds-3 Carat D Flawless Diamonds-0.5 Carat G VS2

Average

0

50

100

150

200

250

300

350

400

450

Diamonds-1 Carat G VS2 Diamonds-0.3 Carat G VS2

Diamonds-3 Carat D Flawless Diamonds-1 Carat H VS2

Diamonds-0.5 Carat G VS2 Average

44Themes that have led to the current conditions

Debt

Governance

requirements

Certification delays

Bankruptcies in

India, released

inventories

Chinese anti-

corruption

campaign

Low oil prices

affecting mid East /

Russian demand

Lack of advertising

to millennials

Inventories are

building

Oil prices, 1980 to present, real and nominalCertification timing has increased fourfoldKey points

De Beers and Alrosa, inventories (theoretic for

De Beers), production and sales

Millennials views on life goals

importance

Source for all charts: www.whitehouse.gov, Bain & Company, Datastream, company data, SBG Securities analysis

Certification times

0

40

80

120

160

US$

/bbl

Real prices derived using the US CPI rebased (1980- 1981 = 0)

Nominal Brent Price Real Brent Price

Alrosa m cts notes De Beers m cts notes

01 Mar 15 15 31 Dec 15 8 3 months sales

2Q15 production 10 1H15 production 16

2Q15 sales -9 1H15 sales -14

3Q15 production 12 3Q15 production 6

3Q15 sales -5 SBGSe 3Q15 sales -3

4Q15e production 12 based on 3Q15 4Q15e production 7 based on guidance

4Q15e sales -5 based on 3Q15 4Q15e sales -3 base on sights

31 Dec 15 29 31 Dec 15 17

Months production 9.7 Months production 7.0

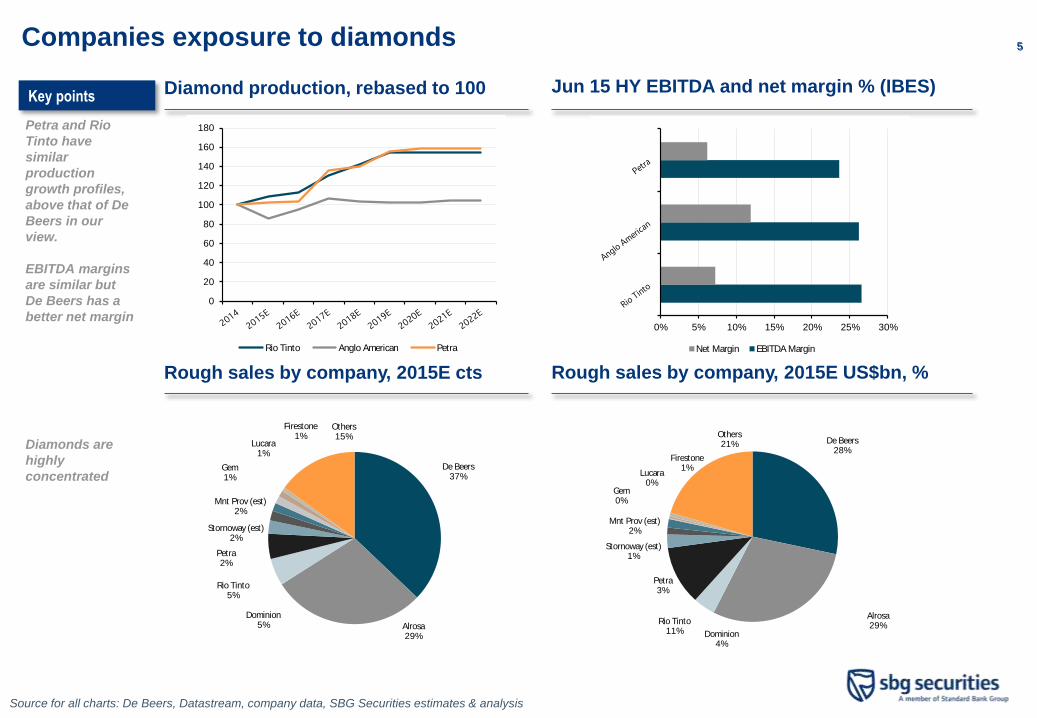

55Companies exposure to diamonds

Petra and Rio

Tinto have

similar

production

growth profiles,

above that of De

Beers in our

view.

EBITDA margins

are similar but

De Beers has a

better net margin

Diamonds are

highly

concentrated

Jun 15 HY EBITDA and net margin % (IBES)Diamond production, rebased to 100Key points

Rough sales by company, 2015E US$bn, %Rough sales by company, 2015E cts

Source for all charts: De Beers, Datastream, company data, SBG Securities estimates & analysis

0

20

40

60

80

100

120

140

160

180

Rio Tinto Anglo American Petra

0% 5% 10% 15% 20% 25% 30%

Net Margin EBITDA Margin

De Beers37%

Alrosa29%

Dominion5%

Rio Tinto5%

Petra2%

Stornoway (est)2%

Mnt Prov (est)2%

Gem1%

Lucara1%

Firestone1%

Others15% De Beers

28%

Alrosa29%

Dominion4%

Rio Tinto11%

Petra3%

Stornoway (est)1%

Mnt Prov (est)2%

Gem0%

Lucara0%

Firestone1%

Others21%

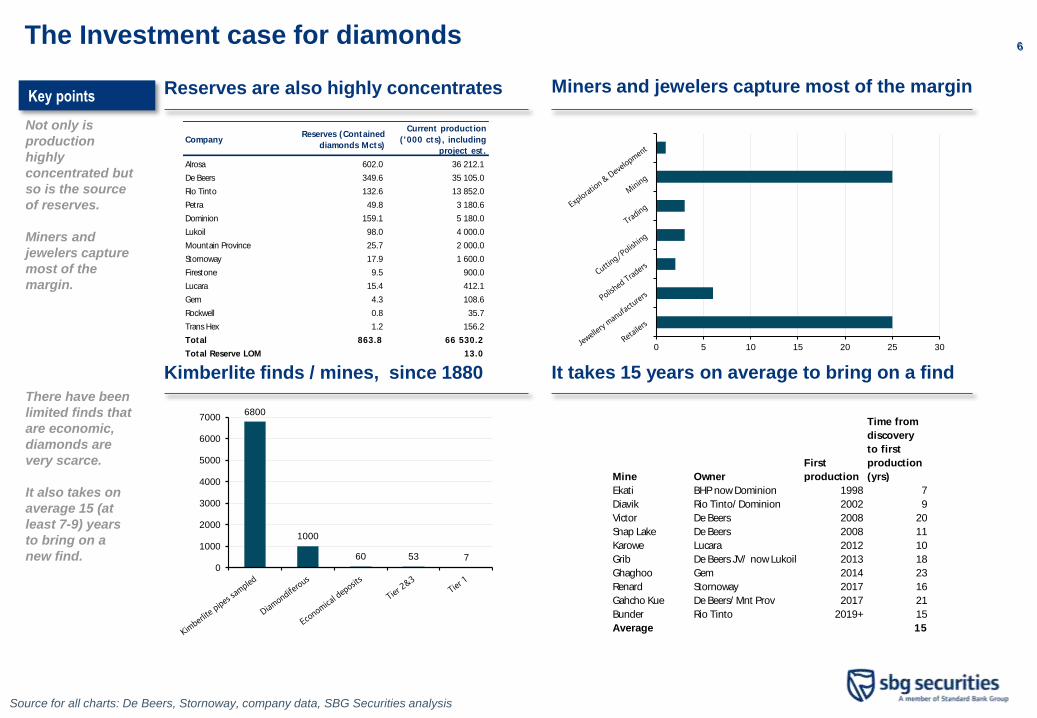

66The Investment case for diamonds

Not only is

production

highly

concentrated but

so is the source

of reserves.

Miners and

jewelers capture

most of the

margin.

There have been

limited finds that

are economic,

diamonds are

very scarce.

It also takes on

average 15 (at

least 7-9) years

to bring on a

new find.

Miners and jewelers capture most of the marginReserves are also highly concentratesKey points

It takes 15 years on average to bring on a findKimberlite finds / mines, since 1880

Source for all charts: De Beers, Stornoway, company data, SBG Securities analysis

Company Reserves (Contained

diamonds Mcts)

Current product ion

( '000 cts) , including

project est .

Alrosa 602.0 36 212.1

De Beers 349.6 35 105.0

Rio Tinto 132.6 13 852.0

Petra 49.8 3 180.6

Dominion 159.1 5 180.0

Lukoil 98.0 4 000.0

Mountain Province 25.7 2 000.0

Stornoway 17.9 1 600.0

Firestone 9.5 900.0

Lucara 15.4 412.1

Gem 4.3 108.6

Rockwell 0.8 35.7

Trans Hex 1.2 156.2

Total 863.8 66 530.2

Total Reserve LOM 13.0 0 5 10 15 20 25 30

6800

1000

60 53 70

1000

2000

3000

4000

5000

6000

7000

Mine Owner

First

production

Time from

discovery

to first

production

(yrs)

Ekati BHP now Dominion 1998 7

Diavik Rio Tinto/ Dominion 2002 9

Victor De Beers 2008 20

Snap Lake De Beers 2008 11

Karowe Lucara 2012 10

Grib De Beers JV/ now Lukoil 2013 18

Ghaghoo Gem 2014 23

Renard Stornoway 2017 16

Gahcho Kue De Beers/ Mnt Prov 2017 21

Bunder Rio Tinto 2019+ 15

Average 15

77The Investment case for diamonds

Diamond

producers are

more disciplined

because of the

concentration and

scarcity noted

previously.

The price/volume

balance tends to

be solved with

volume, where

other commodities

solve with price

De Beers sight values De Beers sight values Key points

Price variation for the precious metals and diamonds

Source for all charts: Datastream, company data, SBG Securities analysis

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Rough Diamonds Gold Platinum Copper Silver Iron ore

0

100

200

300

400

500

600

700

800

900

1000

2011 2012 2013

2014 2015 Average

0

100

200

300

400

500

600

700

800

900

1000

88Demand has held up reasonably

Polished demand

has been fairly

resilient. De Beers

estimates 7%

growth in the US in

2014, with Japan

and China slower

but positive.

We think that the

issues in diamonds

is over-supply /

release of

inventories more

than consumer

demand.

We remain

conservative given

thrifting into

synthetics and

other gems and re-

cycling on our

demand outlook, at

3% nominal.

Monthly US Jewellery sales (yoy%)Jewellery demand splitKey points

Japanese polished diamond imports (US$bn)

Chinese retail sales; gold, silver and

jewellery sales, CNY (Bn)

Source for all charts: Datastream, company data, SBG Securities analysis

US40%

China (incl HK, Macau)16%

India8%

Japan6%

Gulf8%

RoW22%

6.8%

-2.6%

3.9%

14.5%

1.2%

-0.9%

3.3%

1.7%

-1.4%

8.7%

5.3%

-4.3%

6.1%

3.2%

0.7%

2.1%

4.9%

2.0%

6.4%

3.7%

0.9%

-3.3%

-6.0% -5.9%-5.3%

-2.2%

5.2%

2.8%

-0.6%

-10%

-5%

0%

5%

10%

15%

0%

24%

40%

50%

42%

52%

28%23%

20%21%19%

0%

11%

-3%

-31%

-12%

2%

-10%

7%11%12%

5%6%0%

-4%

16%

8%11%

2%5%

2%

-1%

-40%

-20%

0%

20%

40%

60%

80% 1.45

1.05

1.291.2

0.97 0.94 0.97

1.18

1.051.01

0.88

0.77

0.620.69

0.810.9 0.87 0.89

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

US$

(b)

Japan's Polished Diamnonds Imports, (US$ b)

99Diamond demand is from middle and upper incomes

Demand for

diamonds is an

emotional and a

luxury purchase.

Diamonds are

unique and are not

thus a commodity.

Demand has been

created through

advertising and is

very middle/upper

income focused.

Recently branded

jewelry has become

ore prevalent.

Chinese income development over timeHistory of creating demand - De BeersKey points

Branded jewellery sales increasing over time

Source for all charts: G Securities analysis, McKinsey & Company, De Beers

101024m cts of growth are expected, excluding latent capacity

We have

reviewed the

project pipeline

and outline the

known projects

in detail.

Diamond projectsKey points

Source for all charts: Company reports, Bain & Company, McKinsey & Company, De Beers; SBG

Securities analysis

Notes 2015E

2016E

2017E

2018E

2019E

2020E

2021E

Tota

l

Alrosa Group Various projects to expand production 1.0 1.0 1.0 1.0 1.0 1.0 6.0

Bunder (Rio Tinto) Rio Tinto project in India with potential production of

2.5m cts pa

1.0 1.5 2.5

Gaghoo (Gem) Ghagoo is Botswana's first UG diamond mine. Gem

Diamonds is developing Ghaghoo in a phased approach.

0.1 0.1 0.2

Gahcho Kue (De Beers 51/ Mnt Prov 49) Gahcho Kue is a new mine in Canada, with an 11-13 year

life and producing 4-5.5m cts pa.

- 0.2 3.5 1.2 0.6 5.5

Grib (Lukoil) Lukoil has constructed the mine which has 98m cts of

reserves and will gorw incrementally towards 4.5m cts pa

production

1.0 2.0 0.5 3.5

Krone Endora Venetia alluvials (Diamcor) This is an alluvial deposit previously owned by De Beers

and adjacent to the Venetia diamond mine.

0.2 0.2

Lace (DiamondCorp) Lace is the restart of an old mine near Kroonstad in South

Africa, with potential production of 300k cts

0.3 0.3

Lerala (Kimberley Diamonds) The Lerala Mine, situated in north-east Botswana,

comprises a cluster of five diamondiferous kimberlite

pipes totalling 6.7 hectares in size, together with a 230

tonnes per hour processing and recovery facility. Lerala

will target a production rate of approximately 400 k ct pa.

0.2 0.2 0.4

Merlin (Merlin Diamonds Limited) Merlin Diamonds is an Australian kimberlite developer 0.1 0.2 0.3

Petra various Various projects to extend caves to new levels and

construct a new plant at Cullinan

0.1 0.0 1.0 0.1 0.5 0.1 1.8

Renard (Stornoway) Storoway project for the first diamond mine in Quebec,

production est of 1.6mcts pa from 2H16

- 0.3 0.9 0.4 1.6

Star Orion South (Shore Gold) Kimberlite near Saskatchewan, Canada, FS indicates 34mc

reserve, 20yr LOM, $1.9bn investment

0.8 0.9 1.7

Total 1.7 3.6 7.6 2.7 3.1 3.4 1.9 24.0

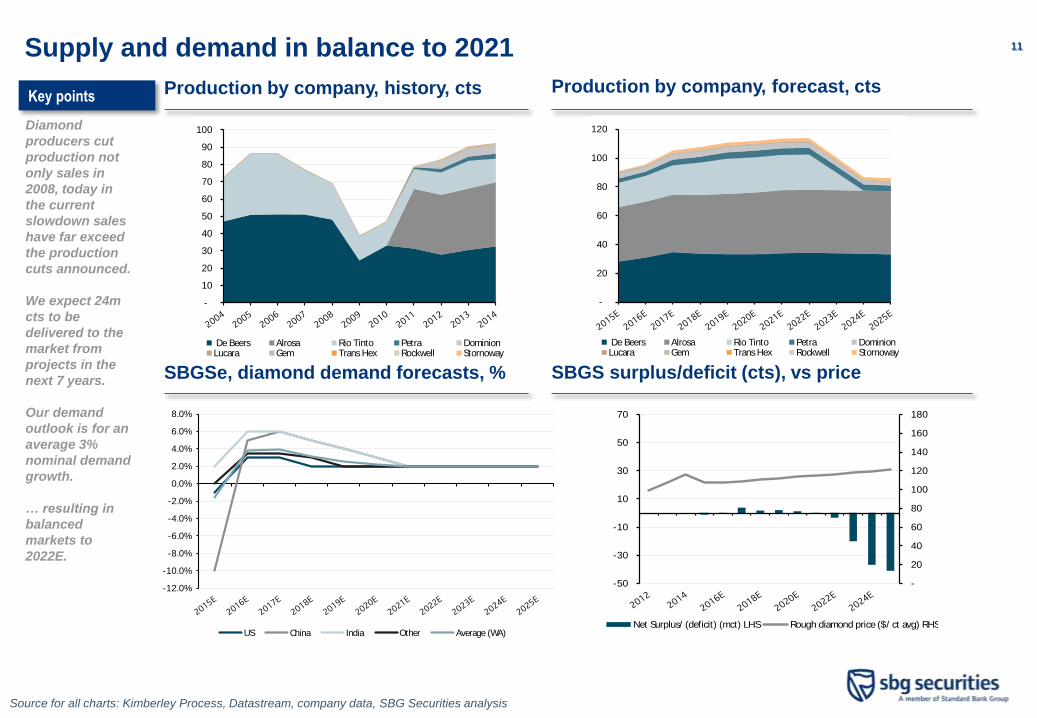

1111Supply and demand in balance to 2021

Diamond

producers cut

production not

only sales in

2008, today in

the current

slowdown sales

have far exceed

the production

cuts announced.

We expect 24m

cts to be

delivered to the

market from

projects in the

next 7 years.

Our demand

outlook is for an

average 3%

nominal demand

growth.

… resulting in

balanced

markets to

2022E.

Production by company, forecast, ctsProduction by company, history, ctsKey points

SBGS surplus/deficit (cts), vs priceSBGSe, diamond demand forecasts, %

Source for all charts: Kimberley Process, Datastream, company data, SBG Securities analysis

-

10

20

30

40

50

60

70

80

90

100

De Beers Alrosa Rio Tinto Petra DominionLucara Gem Trans Hex Rockwell Stornoway

-

20

40

60

80

100

120

De Beers Alrosa Rio Tinto Petra DominionLucara Gem Trans Hex Rockwell Stornoway

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

US China India Other Average (WA)

-

20

40

60

80

100

120

140

160

180

-50

-30

-10

10

30

50

70

Net Surplus/ (deficit) (mct) LHS Rough diamond price ($/ ct avg) RHS

1212

The diamond pipeline, it

takes 6-9 months to

restock

Phase

Dia

mon

d ty

pe

Nat

ure

Value

(US$

bn SB

GSe

)

Cash

mar

gin (SB

GSe

)

Finan

cing

Note

s

Ro

ug

h

EXPLORATION

&

DISCOVERY

So urce: B o tswana D iamo nds

Fragmented, 100s of participants 1.0 na Equity

De Beers and Alrosa remain the main

exploration companies. Rio Tinto continues

developing Bunder. There are numerous

exploration companies, mostly listed on the

TSX.

MINING

So urce: D o minio n D iamo nds

Highly concentrated. De Beers and

Alrosa have a combined 70% share of

the market in terms of volume and 85%

in terms of value (SBGSe). 10s

15.0 20-30% Equity and senior LT debt

Largest mining companies include:

• De Beers

• Alrosa

• Rio Tinto

• Petra

• Dominion

• Endiama (Angola state)

TRADING

So urce: Lucara D iamo nds

Moderately concentrated, 120 known

buyers for the five major producers,

100s

15.0 1-5%

Historically 90% financed,

now 50-70% as a result of

the lower profuitability of

trading, the increased

capital regulation on banks

and bankruptcies in recnt

years.

Please refer to the table of traders and

sightholders for the 5 of the largest mining

companies. More recently there is pressure

for the traders to provide IFRS accounts,

comply with liquidity levels and to have

audited accounts.

CUTTERS

&

POLISHERS

So urce: D e B eers Insight

Highly fragmented, in India in particular.

1000s17.0 1-5%

Similar to trading, with

smaller cutters in cash on a

rolling basis, with limited

inventory

We estimate that there are arouns 200-250

polishers in SA, 1000 in Botswana, 800,000

In India

POLISHED TRADERS

So urce: GIA

Well fragmented, though not as highly

as cutting, 100s18.0 1-3% Similar to trading

Diamonds are acquired from smaller cutting

centres and sold by polished traders where

the producer and consumer are not vertically

integrated.

JEWELLERY

MANUFACTURERS

So urce: F o revermark

Very fragmented, 10,000s 35.0 5-12% Corporate debt and equity

Manufacturers include:

• Contracted specialists

• Luxury brands (LVMH, Richemont etc.)

• Independent designers

RETAILERS

So urce: R apapo rt news

Extremely fragmented. 250,000s 60.0 10-100% Corporate debt and equity

Channels include:

• Catalogue/ TV (QVC)

• Internet (Blue Nile)

• Department Stores (Macys)

• Discounters (Walmart)

• Jewellery Chains (Tiffany’s)

• Independent Jewellers (De Beers)

CONSUMERS

So urce: D e B eers Insight

Co

nsu

mers

Middle to upper income earners globally.

1,000,000s

Bain & Company estimate what Chinese

middel class households will increase

from 116m in 2013 to 282m by 2024E, a

CAGR increase of 8.4%. Indian middel class

households will increase from 39m in 2013

to 109m by 2024E, a CAGR increase of 9.9%.

Ro

ug

hP

oli

sh

ed

Jew

ell

ers

Lucara finds a 1,111 carat stone,

the second-largest ever after the

3107ct Cullinan Diamond was

found in 1905

Source for all charts: SBG Securities analysis, Lucara, Bain &

Company, Mckinsey & Company

1313Conclusion

Source for all charts: SBG Securities analysis

Diamond markets are among the most consolidated, the material is most scarce and the market

participants are the most rational

A number of events has caused excess polished inventories, including: large sales levels in 1H14,

financing constraints, cutting/polishing bankruptcies, oil price declines, China’s anti-corruption campaign

and a lack of advertising to millennials. Most of these events are pipeline issues not long term demand.

… the miners have reacted. Supply has been withheld, destocking is taking effect. There are two ways to

solve the puzzle, hold back supply and drive polished prices or cut rough prices. The miners have chosen

the former, rational given margin levels

We think that diamonds have fallen deeper and faster than other commodities but will recover

sooner.

Private and confidential

Disclosures

15Disclosures

SBG Securities (Pty) Limited is the name provided to the Institutional Stock broking entity of The Standard Bank of South

Africa Limited. The following analyst/s: Heidi Sternberg, Tim Clark certify, with respect to the companies or securities under

analysis, that (1) the views expressed in this report accurately reflect their personal views about all of the subject companies

and securities and (2) no part of their compensation was, is or will be directly or indirectly related to the specific

recommendations or views expressed in this report. SBG Securities (Pty) Limited Research Analyst receive compensation

that is based, in part, on the overall firm revenues, which include investment banking revenues.

Disclosure Appendix

Important Global Disclosures

Companies Mentioned (Price as of 1 December 2014)

Anglo American plc (AAL.L, p1,304, HOLD, TP p1,480)

BHP Billiton plc (BLT.L, p1,457, BUY, TP p1,900)

Glencore plc (GLEN.L, p317, BUY, TP p390)

Merafe Resources (MRFJ.J, R0.91, BUY, TP R1.90)

Rio Tinto plc (RIO.L, p2,956, BUY, TP p3,300)

African Rainbow Minerals (ARIJ.J, R126.53, BUY, TP R155.00)

Exxaro Resources Ltd (EXXJ.J, R106.74, HOLD, TP R150.00)

Kumba Iron Ore (KIOJ.J, R250.50, BUY, TP R255.00)

16Disclosures

SBG Securities’ distribution of stock ratings is:

SBG Securities (Pty) Limited is the name provided to the Institutional Stock broking entity of The Standard Bank of South Africa Limited. The following analyst/s: Heidi Sternberg, Tim Clark certify, with respect to the companies or securities under analysis, that (1) the views expressed in

this report accurately reflect their personal views about all of the subject companies and securities and (2) no part of their compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report. SBG Securities (Pty) Limited Research

Analyst receive compensation that is based, in part, on the overall firm revenues, which include investment banking revenues.

For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of BUY, HOLD, and SELL most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock

ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individual factors.

SBG Securities’ policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

SBG Securities’ policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please contact the Legal and Compliance Division of SBG Securities’ and request their Policies for Managing

Conflicts of Interest in connection with Investment Research.

SBG Securities does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Price Target: (12 months) for (AAL.L)

Methods: We value Anglo using a DCF valuation for operating assets, and over the life of mine, assuming a USD WACC of 9.5% (equity risk premium (ERP) 4.5%, Beta 1.25, long bond 5.0%, cost of equity 10.6%, and long-term gearing (excluding

marketing short-term debt) of 20% debt/equity %). We value non-core assets at a market price (PE and EV/EBITDA blend) and the listed holding in Exxaro at current market value. We DCF our cash flows on a 12-month forward rolling basis and include

the dividend yield in our one-year forward target price.

Risks: Risks to our target price, valuation and earnings include higher or lower commodity prices and exchange rates than we are forecasting. Risks also include delivery of ongoing production where unforeseen mining, logistics and labour issues may

impact our estimates. Project delivery and capex is a risk in the sector with projects coming in over budget and late at times in the cycle or if underestimated by management.

Price Target: (12 months) for (BLT.L)

Methods: We value BHP using a DCF valuation for operating assets over the LoM and assuming a USD WACC of 9.5% (equity risk premium (ERP) 4.5%, Beta 1.25, long bond 5.0%, cost of equity 10.6%, and long-term gearing of 20% debt/debt+equity).

We value petroleum exploration at the cost incurred given historical successes. We DCF our cash flows on a 12-month forward rolling basis and include the dividend yield in our one-year forward target price.

Risks: Risks to our target price, valuation and earnings include higher or lower commodity prices and exchange rates than we are forecasting. Risks also include delivery of ongoing production where unforeseen mining, logistics and labour issues may

impact our estimates. Project delivery and capex is a risk in the sector with projects coming in over budget and late at times in the cycle or if underestimated by management.

Price Target: (12 months) for (GLEN.L)

Methods: We value Glencore using a DCF valuation for operating assets and marketing activities over the LoM and assuming a USD WACC of 9.5% (equity risk premium (ERP) 4.5%, Beta 1.25, long bond 5.0%, cost of equity 10.6%, and long-term

gearing (excluding marketing short-term debt) of 20% debt/equity%). We value the unlisted assets at market value. We DCF our cash flows on a 12-month rolling forward basis, and include the dividend yield in our one-year forward target price.

Risks: Risks to our target price, valuation and earnings include higher or lower commodity prices and exchange rates than we are forecasting. Risks also include delivery of ongoing production where unforeseen mining, logistics and labour issues may

impact our estimates. Project delivery and capex is a risk in the sector with projects coming in over budget and late at times in the cycle or if underestimated by management.

Price Target: (12 months) for (MRFJ.J)

Methods: We value Merafe using a DCF valuation for operating assets over the life of mine and assuming a ZAR WACC of 12.5% (Equity Risk Premium (ERP) 4.5%, Beta 1.25, Long bond 8.5%, Cost of Equity 14.1%, and long-term gearing (excluding

marketing short term debt) of 30% Debt/Debt+Equity). We DCF our cash flows on a 12-month forward rolling basis and include the dividend yield in our one-year forward price target.

Risks: Risks to our target price, valuation and earnings include higher or lower commodity prices and exchange rates than we are forecasting. Risks also include delivery of ongoing production where unforeseen mining, logistics and labour issues may

impact our estimates. Project delivery and capex is a risk in the sector with projects coming in over budget and late at times in the cycle or if underestimated by management.

Price Target: (12 months) for (RIO.L)

Methods: We value Rio Tinto using a DCF valuation for operating assets over the life of mine and assuming a USD WACC of 9.5% (equity risk premium (ERP) 4.5%, Beta 1.25, long bond 5.0%, cost of equity 10.6% and long-term gearing of 20%

debt/debt+equity). We DCF our cash flows on a 12-month forward rolling basis and include the dividend yield in our one-year forward target price.

Risks: Risks to our target price, valuation and earnings include higher or lower commodity prices and exchange rates than we are forecasting. Risks also include delivery of ongoing production where unforeseen mining, logistics and labour issues may

impact our estimates. Project delivery and capex is a risk in the sector with projects coming in over budget and late at times in the cycle or if underestimated by management.

See the Companies Mentioned section for full company names.

17Disclosures

Important Standard Bank DisclosuresPotential Conflicts

A: The analyst is an officer, board member, or director of the Company

B: The company beneficially owns 5% or more of the equity shares of Standard Bank Group as at Jan 2012

C: Standard CIB beneficially owns 1% or more of the equity shares of the company

D: Standard CIB may beneficially hold a significant financial interest of the debt of this company where the aggregate of this debt is more than US$ 15 million

E: The Company is a client of Standard CIB

F: Standard CIB has lead managed or co-lead managed a public offering of the securities of the company in the last 12 months

G: Standard CIB has received compensation for investment banking services from the company within the last 12 months

H: Standard CIB expects to receive, or intends to seek, compensation for investment banking services from the company during the next 3 months

I: SBG Securities (Pty) Ltd has sent extracts of this research report to the subject company prior to publication for the purpose of verifying factual accuracy. Based on information provided by the subject company, factual changes have been

made as a result.

J: Analyst or a member of their household holds long or short personal positions in a class of common equity securities of this company

K: Standard CIB is a market maker or liquidity provider in the financial instruments of the relevant issuer

* Disclosures are correct as of 13 October 2014

For purposes of the NYSE and NASD, in connection to the distribution of SBG Securities research, Standard Bank Group must disclose certain material conflicts of interest. Standard Bank Group

expects to receive or intends to seek investment banking related compensation from the subject company Resources Strategy within the next 3 months.

This report may include references to Standard Bank Group Limited’s research recommendations. For further information and for published Standard Bank reports in their entirety, please visit the website at www.standardbank.co.za/research.

For SBG Securities’ disclosure information on other companies mentioned in this report, please visit the website at www.SBG Securities-sa.com/researchdisclosures.

Disclaimers continue on next page

.

Company Disclosure

Anglo American plc D J

BHP Billiton plc D F G J

Glencore plc D

Merafe Resources D G

Rio Tinto plc D

This report covers Metals and Mining. All other companies were used for illustrative purposes only. We are not commenting on the investment merit of the securities of these companies

Singapore recipients should contact a Singapore financial adviser for any matters arising from this research report.

The analyst(s) involved in the preparation of this report have not visited the material operations of the subject company () within the past 12 months. Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting

shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares. Individuals receiving this report from a Canadian investment dealer that is n ot affiliated with SBG Securities (Proprietary) Limited ( “ SBG Securities”) should be advised that this

report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

As of the date of this report, SBG Securities does not act as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

Taiwanese Disclosures: This research report is for reference only. Investors should carefully consider their own investment risk. Investment results are the responsibility of the individual investor. Reports may not be reprinted without permission of SBG

Securities. Reports written by Taiwan-based analysts on non-Taiwan listed companies are not considered recommendations to buy or sell securities under

Taiwan Stock Exchange Operational Regulations Governing Securities Firms Recommending Trades in Securities to Customers. To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following

are important disclosures regarding any non-U.S. analyst contributors:

The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of SNYS and therefore may not be subject to the NASD Rule

2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Heidi Sternberg, Tim Clark, Non-U.S. Analyst(s) is a (are) research analyst(s) employed by SBG Securities.(Proprietary) Limited (“SBG Securities”).

Important Regional Disclosures

18DisclaimerSBG Securities (Proprietary) Limited (“SBG Sec”) is the name of the Equities Trading Division of the Standard Bank Group (“SB”) operating under its Corporate and Investment banking Division (“CIB”).

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary

to law or regulation or which would subject SBG Sec to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to SBG Sec. None of the material, nor

its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of SBG Sec. All trademarks, service marks and logos used in this report are trademarks or

service marks or registered trademarks or service marks of SBG Sec or its affiliates.

The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial

instruments. SBG Sec may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. SBG Sec will not treat recipients as its customers by virtue of their receiving the report. The investments or

services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes

investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation to you. SBG Sec does not offer advice on the

tax consequences of investment and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change.

SBG Sec believes the information and opinions in the Disclosure Appendix of this report are accurate and complete. Information and opinions presented in the other sections of the report were obtained or derived from sources SBG Sec believes are

reliable, but SBG Sec makes no representations as to their accuracy or completeness. Additional information is available upon request. SBG Sec accepts no liability for loss arising from the use of the material presented in this report, except that this

exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to SBG Sec. This report is not to be relied upon in substitution for the exercise of independent judgment. SBG Sec may have issued, and

may in the future issue, a trading call regarding this security. In addition, SBG Sec may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those

reports reflect the different assumptions, views and analytical methods of the analysts who prepared them and SBG Sec is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. SBG Sec is

involved in many businesses that relate to companies mentioned in this report.

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect

a judgement at its original date of publication by SBG Sec and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities

and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADRs, the values of which are influenced by

currency volatility, effectively assume this risk.

Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security

may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer.

Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase.

Some investments discussed in this report have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment.

Indeed, in the case of some investments the potential losses may exceed the amount of initial investment, in such circumstances you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in

consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain

reliable information about the value, or risks, to which such an investment is exposed.

SBG Sec maintains information barriers between its Research Analysts and the rest of its and its shareholders business divisions, more specifically the Investment Banking business. SBG Sec’ analysts’, strategists’ and economists’ compensation is not

linked to Investment Banking or Capital Markets transactions performed by SBG Sec or its shareholders. Facts and views presented in SBG Sec’ research have not been reviewed by, and may not reflect information known to, professionals in other SBG

Sec or Standard Bank business areas, including investment banking personnel.This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of SBG Sec and SB, SBG Sec

has not reviewed the linked site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to SBG Sec or SB’s own website material) is provided solely for your convenience and

information and the content of the linked site does not in any way form part of this document. Accessing such website or following such link through this report shall be at your own risk.

This report is issued and distributed in Europe Standard Bank PLC. 20 Gresham Street, London EC2V 7JE which is authorised by the Prudential Regulation Authority (“PRA”) and regulated by the Prudential Regulation Authority (PRA “) and the

Financial Conduct Authority (“FCA”) This report is being distributed in the United States by Standard New York Securities (USA) LLC; in Kenya by CfC Stanbic Bank Limited; in Nigeria by Stanbic IBTC; in Angola by Standard Bank de Angola S.A.; in

Brazil by Banco Standard de Investimentos S.A.; in China by Standard Resources (China) Limited; in Botswana by Stanbic Bank Botswana Limited; in Democratic Republic of Congo by Stanbic Bank Congo s.a.r.l.; in Ghana by Stanbic Bank Ghana

Limited; in Isle of Man by Standard Bank Isle of Man Limited; in Jersey by Standard Bank Jersey Limited; in Madagascar by Union Commercial Bank S.A.; in Mozambique by Standard Bank s.a.r.l.; in Malawi by Standard Bank Limited; in Namibia by

Standard Bank Namibia Limited; in Mauritius by Standard Bank (Mauritius) Limited; in Taiwan by The Standard Bank of South Africa; in Tanzania by Stanbic Bank Tanzania Limited; in Singapore by Standard Merchant Bank (Asia) Limited; in Swaziland

by Standard Bank Swaziland Limited; in Zambia by Stanbic Bank Zambia Limited; in Zimbabwe by Stanbic Bank Zimbabwe Limited; in UAE by Standard Bank Plc – Dubai branch

In jurisdictions where SBG Sec is not already registered or licensed to trade in securities, transactions will only be effected in accordance with applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade

be made in accordance with applicable exemptions from registration or licensing requirements.

All rights reserved. Any unauthorized use, duplication, redistribution or disclosure of this report (the “Product”), including, but not limited to, redistribution of the Product by electronic mail, posting of the Product on a website or page, and/or providing to a

third party a link to the Product, is prohibited by law and will result in prosecution. The information contained in the Product is intended solely for the recipient and may not be further distributed by the recipient to any third party. Where included in this

report, MSCI sourced information is the exclusive property of Morgan Stanley Capital International Inc. (MSCI). Without prior written permission of MSCI, this information and any other MSCI intellectual property may not be reproduced, redisseminated

or used to create any financial products, including any indices. This information is provided on an "as is" basis. The user assumes the entire risk of any use made of this information. MSCI, its affiliates and any third party involved in, or related to,

computing or compiling the information hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of this information. Without limiting any of the foregoing, in no

event shall MSCI, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind. MSCI, Morgan Stanley Capital International and the MSCI indexes are services marks

of MSCI and its affiliates. SBG Securities Proprietary Limited (“SBG Sec”) accepts no liability whatsoever for the actions of third parties. The document may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the

document refers to website material of SBG Sec, SBG Sec has not reviewed the linked site. Equally, except to the extent to which the document refers to website material of SBG Sec, SBG Sec takes no responsibility for, and makes no representations

or warranties whatsoever as to, the data and information contained therein. Such address or hyperlink (including addresses or hyperlinks to website material of SBG Sec) is provided solely for your convenience and information and the content of the

linked site does not in anyway form part of this document. Accessing such website or following such link through the document or the website of SBG Sec shall be at your own risk and SBG Sec shall have no liability arising out of, or in connection with,

any such referenced website.

Please note that this report was originally prepared by SBG Sec for distribution to SBG Sec and SB market professionals and institutional investor customers. Recipients who are not market professionals or institutional investor customers of these firms

should seek the advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. This research may relate to investments or services of a person outside of the UK

or to other matters which are not regulated by the PRA or in respect of which the protections of the PRA for private customers and/or the UK compensation scheme may not be available, and further details as to where this may be the case are available

upon request in respect of this report.

Additional information is available upon request.

SBG Sec is a member of the JSE Limited.

Copyright 2014 SBG Sec. All rights reserved..