Global dairy market outlook - DairyNZ - DairyNZ · 12.40 12.40 6.80 5.80 0.80 1.20 7.80 8.80 9.00...

27

Recovery and lessons Global dairy market outlook Tim Hunt General Manager Rabobank Food & Agribusiness Research 17 th May 2016

-

Upload

nguyenthien -

Category

Documents

-

view

219 -

download

2

Transcript of Global dairy market outlook - DairyNZ - DairyNZ · 12.40 12.40 6.80 5.80 0.80 1.20 7.80 8.80 9.00...

12.40

6.80

5.80

0.80

1.20

7.80

8.80

9.00

0.20

0.20

12.40 7.90

7.50

Guides for gutter

8.40

Recovery and lessons

Global dairy market outlook

Tim Hunt General Manager Rabobank Food & Agribusiness Research 17th May 2016

2

Food & Agribusiness Research and Advisory

Rabobank’s unique global team of 87 analysts – supporting knowledge based banking

3

Why has this gone on so long?

When might things improve?

Section 1

Section 2

Section 3

Section 4

Is the medium term still attractive?

Lessons from the cycle

4

Dairy commodities remain depressed

Source: USDA, MDC, Rabobank analysis

1,000

2,000

3,000

4,000

5,000

6,000

USD

/tonne F

OB

WMP (fob Oceania)

13 months

4 months

21 months +

Months spent below USD 3000/t

5

Recapping the problem: a predictable downward cycle exacerbated by short term stocks

6

Milk supply taps have proved hard to turn off

-4%

-2%

0%

2%

4%

6%

8%

2008

2009

2010

2011

2012

2013

2014

2015

2016

Production growth in key export regions

Period average

Month

ly Y

OY

7

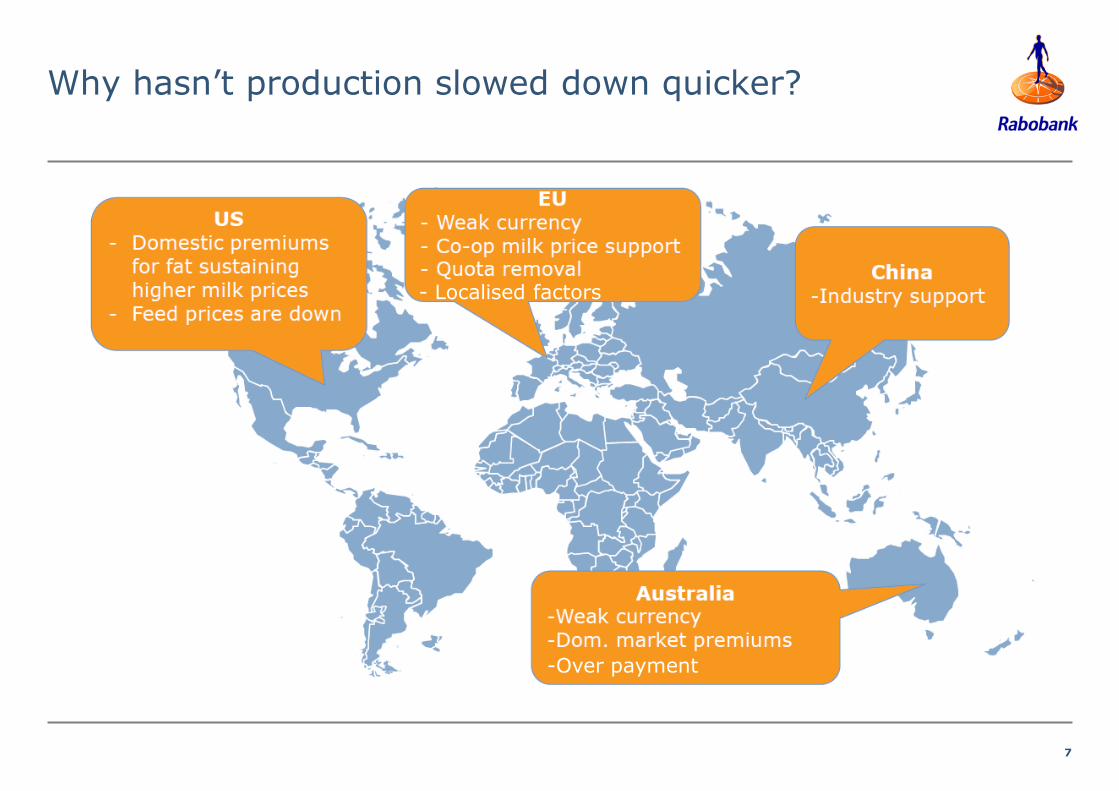

Why hasn’t production slowed down quicker?

-Over payment

- Localised factors

8

Beneath the surface…. things are changing

9

China has rebalanced

1. Milk production has stagnated

2. Consumption is slowly rising

3. Stocks are significantly reduced

4. Imports are stable/rising

10

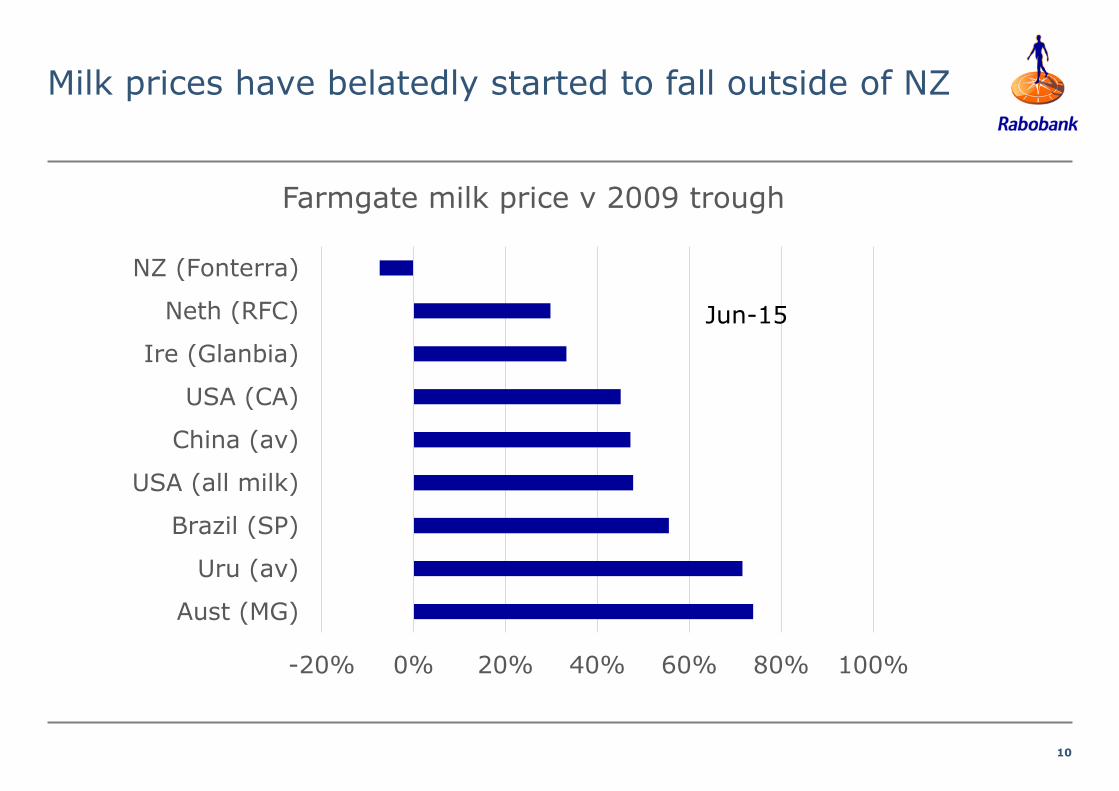

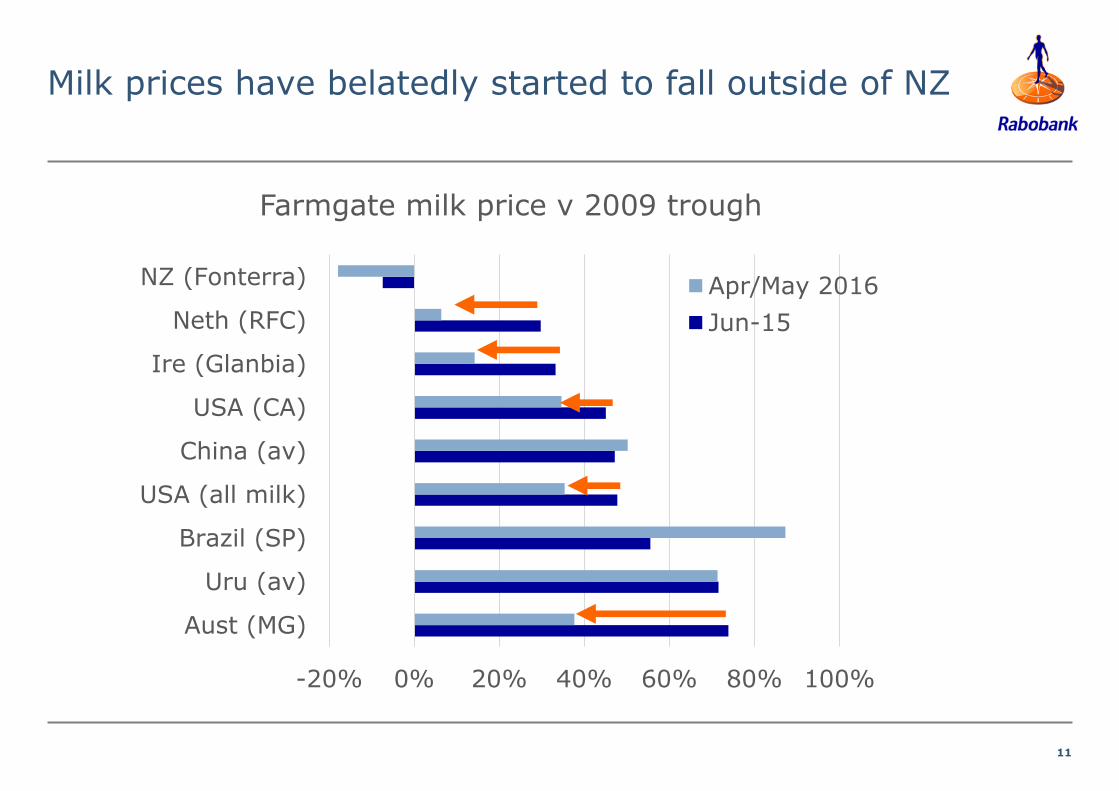

Milk prices have belatedly started to fall outside of NZ

-20% 0% 20% 40% 60% 80% 100%

Aust (MG)

Uru (av)

Brazil (SP)

USA (all milk)

China (av)

USA (CA)

Ire (Glanbia)

Neth (RFC)

NZ (Fonterra)

Farmgate milk price v 2009 trough

Jun-15

11

Milk prices have belatedly started to fall outside of NZ

-20% 0% 20% 40% 60% 80% 100%

Aust (MG)

Uru (av)

Brazil (SP)

USA (all milk)

China (av)

USA (CA)

Ire (Glanbia)

Neth (RFC)

NZ (Fonterra)

Farmgate milk price v 2009 trough

Apr/May 2016

Jun-15

12

Pain is now being shared

13

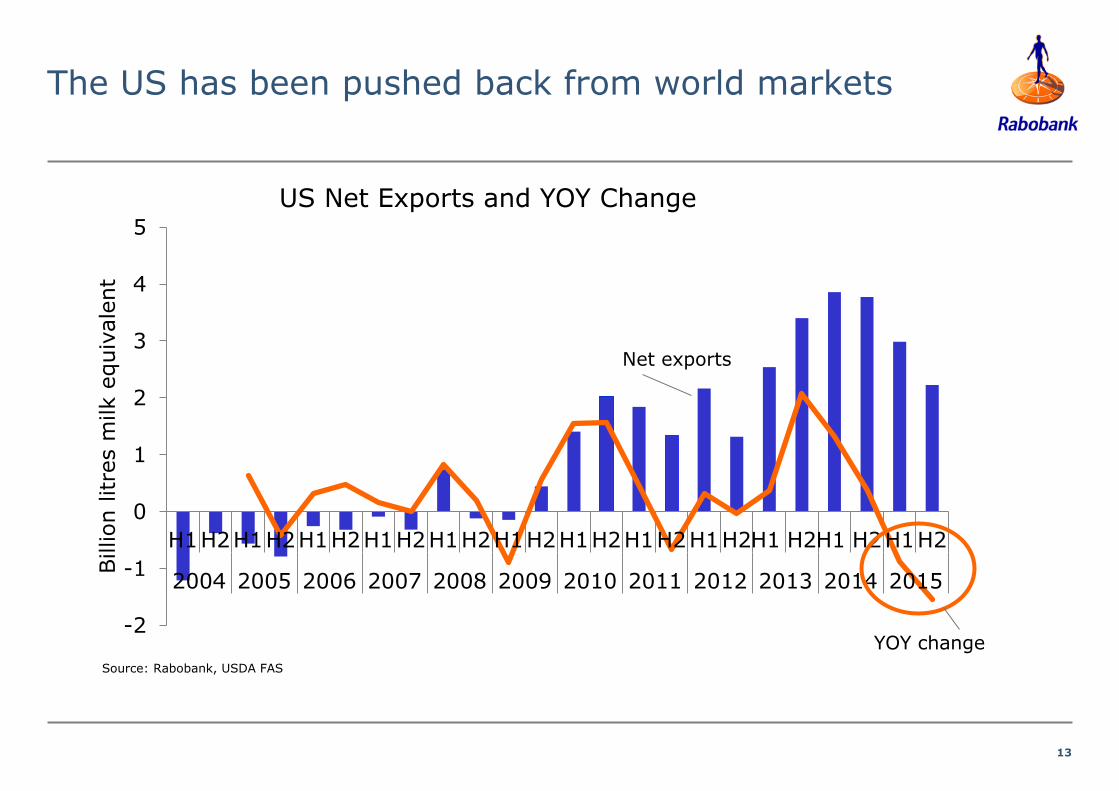

The US has been pushed back from world markets

-2

-1

0

1

2

3

4

5

H1H2H1H2H1H2H1H2H1H2H1H2H1H2H1H2H1H2H1 H2H1 H2H1H2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Billion litre

s m

ilk e

quiv

ale

nt

US Net Exports and YOY Change

Source: Rabobank, USDA FAS

Net exports

YOY change

14

Why has this gone on so long?

When might things improve?

Section 1

Section 2

Section 3

Section 4

Is the medium term still attractive?

Lessons from the cycle

15

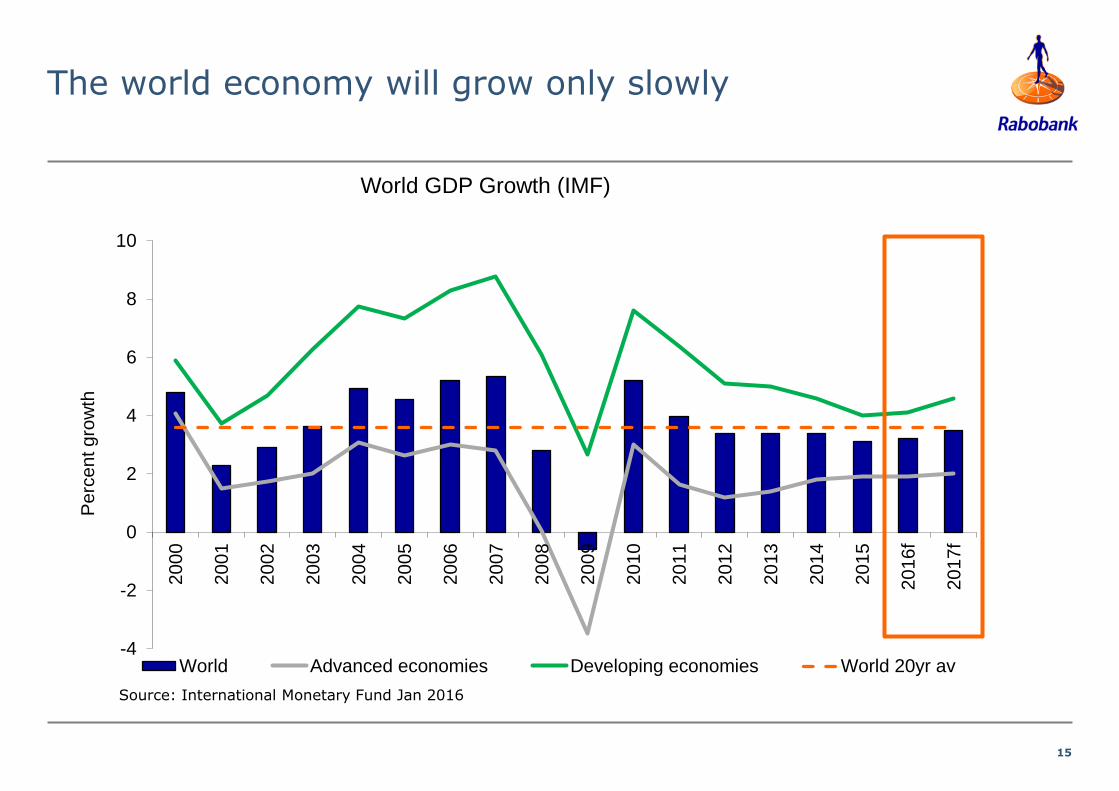

The world economy will grow only slowly

-4

-2

0

2

4

6

8

10

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

2016f

2017f

Pe

rce

nt g

row

th

World GDP Growth (IMF)

World Advanced economies Developing economies World 20yr av

Source: International Monetary Fund Jan 2016

16

Commodity feed will remain cheap

17

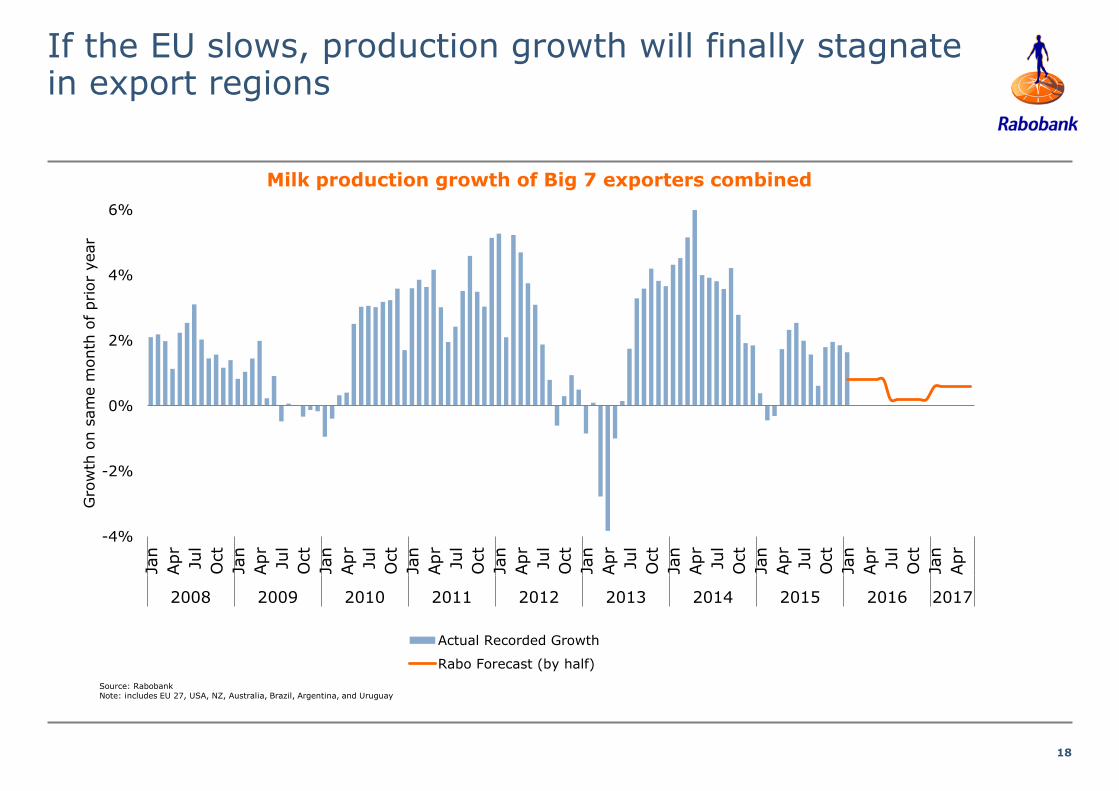

EU production will likely slow

From May we start to overlap the post quota period

Milk prices have now fallen below cash costs in many regions

Dutch no longer face a ‘phosphate incentive’ to hold cows

Ireland will remain an exception

18

-4%

-2%

0%

2%

4%

6%

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Gro

wth

on s

am

e m

onth

of prior

year

Actual Recorded Growth

Rabo Forecast (by half)

If the EU slows, production growth will finally stagnate in export regions

Milk production growth of Big 7 exporters combined

Source: Rabobank Note: includes EU 27, USA, NZ, Australia, Brazil, Argentina, and Uruguay

19

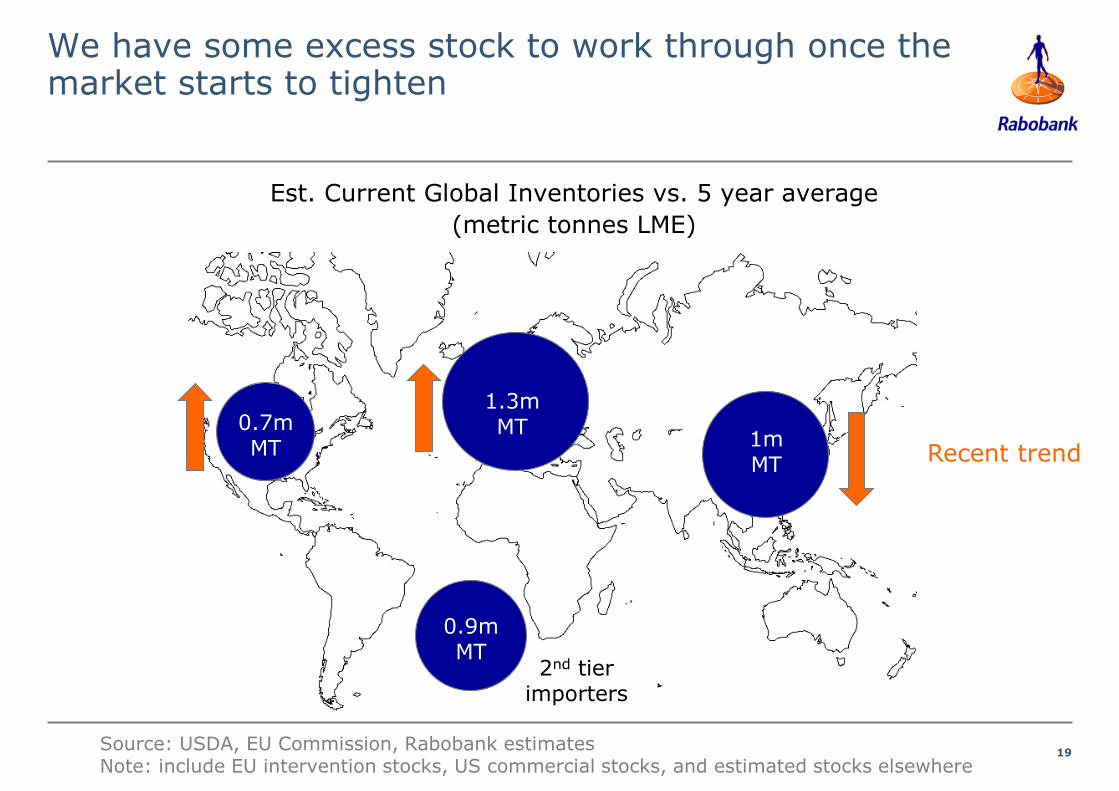

We have some excess stock to work through once the market starts to tighten

Source: USDA, EU Commission, Rabobank estimates Note: include EU intervention stocks, US commercial stocks, and estimated stocks elsewhere

0.9m MT

2nd tier importers

Est. Current Global Inventories vs. 5 year average

(metric tonnes LME)

0.7m MT

1.3m MT

1m MT

Recent trend

20

-

1,000

2,000

3,000

4,000

5,000

6,000Ja

n 2

006

Aug 2

006

Mar

2007

Oct

2007

May 2

008

Dec 2

008

Jul 2009

Feb 2

010

Sep 2

010

Apr

2011

Nov 2

011

Jun 2

012

Jan 2

013

Aug 2

013

Mar

2014

Oct

2014

May 2

015

Dec 2

015

Jul 2016

Feb 2

017

WMP Forecast

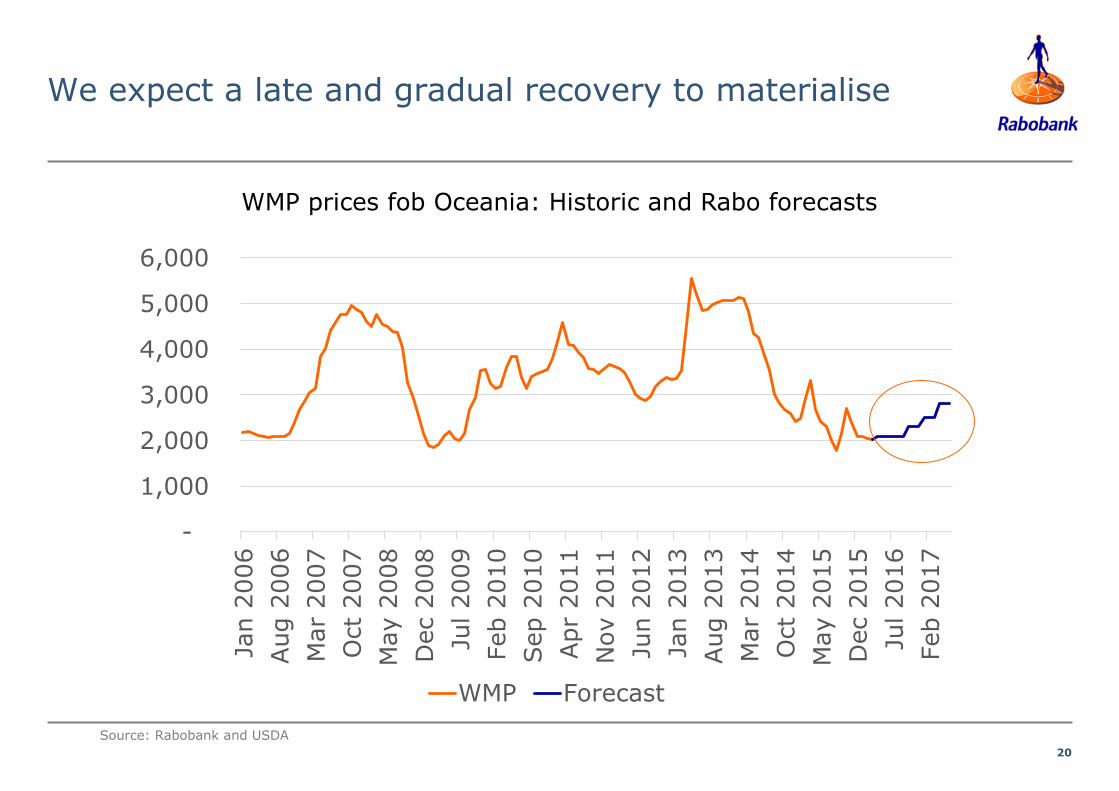

We expect a late and gradual recovery to materialise

Source: Rabobank and USDA

WMP prices fob Oceania: Historic and Rabo forecasts

21

Upside and downside dairy price risks exist

Russia reentering the market

Weather/disease

Further EU growth

USD appreciation

Upside Risk

Downside Risk

22

Why has this gone on so long?

When might things improve?

Section 1

Section 2

Section 3

Section 4

Is the medium term still attractive?

Lessons from the cycle

23

Medium term expectations

Demand for milk will continue to grow (led by emerging markets)

Emerging markets will look to surplus regions for more exports

EU production growth will normalize as post quota wave subsides

Prices will push above costs of production to encourage investment

NZ pasture based dairying likely to remain competitive

24

Why has this gone on so long?

When might things improve?

Section 1

Section 2

Section 3

Section 4

Is the medium term still attractive?

Lessons from the cycle

25

What have we learned from this latest downturn?

1. Economics are not everything in the short term

2. FTAs can only do so much

3. Sometimes its not enough to be the lowest cost producer

4. We probably carried too much debt/costs into this downturn (again)

26

Conclusions

We amidst a distressing ‘super cycle’: EU production now main concern

The protracted downturn looks likely to extend into 2016/17 season

Pricing will get substantially better in the medium term

This is our third major downturn since 2008: we will see them again

Its important we all learn what we can from this one

27

Contact details

Tim Hunt General Manager Food & Agribusiness Research and Advisory Australia and New Zealand [email protected]

“The financial link in the

global food chain”™