Global construction infrastructure market update 2016 Q4

28

Risk. Reinsurance. Human Resources. Construction & Infrastructure Market Update Aon Construction and Infrastructure Group Aon Risk Solutions 4th Quarter 2016

-

Upload

graeme-cross -

Category

Business

-

view

18 -

download

0

Transcript of Global construction infrastructure market update 2016 Q4

Risk. Reinsurance. Human Resources.

Construction & Infrastructure Market UpdateAon Construction and Infrastructure Group

Aon Risk Solutions

4th Quarter 2016

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Asia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Canada . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

EMEA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

Latin America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

United States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

Contacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

Table of Contents

Aon Risk Solutions 1

Executive summary

2016 will be remembered for many things. For those in construction, it will likely be recalled for both its opportunities and challenges. The market gained momentum in the first half only to falter in the second half, due to labor shortages and a tumultuous presidential election. After more than seven years of economic growth, some believe the economy is “overdue” for contraction. While the labor shortage could continue to plague the industry and construction material costs could continue to rise, innovative enhancements will help maintain confidence in the thriving construction market. With virtual reality technology, collaborative project delivery methods, future infrastructure spending boosts, and emerging foreign contractors the industry will continue moving into a more mature expansion phase.

Future investments in overseas construction projects will largely be directed towards Asia, Africa, and the Middle East, while the Mergers and Acquisitions activities will mainly be concentrated in U.S. and Europe. In Asia, projects placed on hold have finally reached financial close and are anticipated to kick off in 2017. The soft bearish cycle continues to drive aggressive pricing. Growth in Asia will outpace the rest of the world, setting development trends.

Canada is experiencing interest from both local and multinational contractors. The job sites are well-regulated, which make them attractive to overseas companies, including insurers. This creates an added level of competitiveness to the market. However, we should be apprehensive about mid-market insurance companies, as the amalgamation of insurers offers the possibility of retracted market capacity.

Australia is encountering pressure to either increase rates or limit the reductions that have been available for the past couple of years. The next few months will be critical in analyzing how insurers may attempt to balance a cautious market desperate to return to profitability with ever-increasing capital growth in the reinsurance capacity.

The rest of Europe and the Middle East continue to prevail as a buyers’ market, thru the global activity of European contractors. Although portfolios in the U.S. remain a challenge, the continued growing support for infrastructure and P3 projects has made the U.S. the world’s largest emerging P3 market. This is becoming evident through the initial rate stabilization being experienced as General Liability and Excess rates diminish. Yet even with all the growth and capital, New York Labor Law and meager automobile coverage will continue to deteriorate limits if competitive alternatives to companies with favorable loss history aren’t being pursued.

In 2016, Latin America experienced its hardest year in terms of construction. Between the decreases in oil and commodity prices and political corruption, we are optimistic that hesitancy and uncertainty will pass the wave of large P3 projects and pipeline development will create opportunities to re-engage competitive markets likely to offer increased capacity.

Outside of the U.S., we will likely see formal notification of the U.K.’s intent to exit in 2017. The unwinding of the territory and replacement of decades of policies will be further influenced by pending elections in France, Germany, and the Netherlands. It is anticipated that this uncertainty will continue to influence M&A activity playing out in 2017 and beyond.

Aon’s unparalleled insight into accessing risk capital allows us to implement truly innovative solutions. We pride ourselves in helping our clients make risk management a competitive advantage, no matter which markets they operate in. We are happy to share Aon’s 4th Quarter 2016 Global Market Update as a high-level view of these trends in the global market.

2 Aon Construction & Infrastructure Market Report | Q4 2016

Asia

Property | CAR, EAR

Going into 2017, the outlook for the construction industry is

positive, and it is anticipated that investment and growth in Asia

will outpace the rest of the world. This positive outlook stems

from a combination of domestic Asian-based developments and

an increase in the amount of Asian investment interests abroad.

The market is hopeful that projects on hold in recent years will

finally reach financial close and kick-off in 2017.

The soft bearish cycle is likely to continue, with markets

competing aggressively on pricing and coverage to secure market

share on developments scheduled to kick-off in 2017. In recent

months the Asian market has been pivotal in setting lead terms

and absorbing the majority of risks within the region.

One-off Contractor-controlled programs are still prominent within

Asia. Competitive tension has given rise to an increase in the need

for integrated / bespoke policies, a step away from the single risk

standard market form wordings Asia has previously accepted.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates ��� Rate Fluctuation: -10% to -15% Clients continue to benefit from soft market conditions and increasing market capacity both domestically and regionally. “Unproven” technology creates some concern and caution from markets in the first year of operations.

��� Expected Rate Fluctuation: -5% to -10% The market will continue to soften and cover is likely to broaden with a move toward Broker manuscript wordings.

Limits �� No material change. �� No material change is expected.

Deductibles/Retentions �� Most carriers have tried to maintain expiring

deductible structures; however, increased market competition has seen a reduction in MD and DSU deductibles.

�� This trend is anticipated to continue, but foresee some reluctance in terms of DSU Time Excess for unproven technology.

Coverage �� The market remained soft with broad coverage achievable. �� Increasing competition in a soft market will maintain

pressure on carriers to continue offering broad coverage where needed.

Integrated All Risk policies are likely to take traction as we move away from transactional one-off placements

Capacity/Appetite ��� Capacity and Appetite domestically and

internationally continued to increase through 2016 as competitive tension and growth requirements increased

��� We expect further pressure from established markets as well as those not currently represented in Asia as they look to the region for growth opportunities

Losses �� The market continued to weather the claims experience in the Asian market with, for the most part, no significant impact on overall profitability

�� No material change is expected. Insured losses are not anticipated to change current market conditionsv

Aon Risk Solutions 3

Liability | Professional

The professional liability market for construction risks remains

stable and competitive for annual practice and project-specific

policies. In Asia, the growing demand for Owner Controlled

policies, particularly for large complex projects involving

international lenders and financiers, is a significant development.

The third quarter has seen increased activity as more of dormant

projects were revitalized. Buying behavior in Asia is still largely

predicated on contractual requirements. However, contracts

involving joint ventures or consortia with a combination of local

and international contractors tend to buy Professional Indemnity,

irrespective of the requirements.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates ��� Rate change:

Primary: -5% to -10% due to increased primary capacity.

Excess: -5% to -15% due to an abundance of capacity.

� Expected rate change: -5% to -15%

Pricing is expected to further soften as capacity is at an all-time high. Competition will result in favorable rates for many Insureds.

Limits �� Clients are maintaining limits purchased. � Many clients are considering increasing their limits due to capacity available at attractive terms.

Deductibles/Retentions �� Most clients have maintained their

deductible/retention levels. �� No material change is expected.

Coverage �� No material change. ��� Competition has caused insurers to explore coverage enhancements in order to differentiate their offerings and not compete exclusively on price.

Capacity/Appetite � Primary entrants like Chubb (ACE) are

creating greater pricing pressure. Excess professional liability insurers offered an abundance of capacity, often in excess of $250 million.

� Due to the entry of new professional liability insurers in the U.S. and London markets, capacity is expected to increase further for primary layers.

Losses ��� Claims activity in the Construction sector was fairly constant, but claims severity increased.

��� This trend is expected to continue.

Asia

4 Aon Construction & Infrastructure Market Report | Q4 2016

Australia

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change: No material change.

Pricing discounts are still available; however clients need to consider the value of existing insurer relationships versus a more competitive alternative.

�� Expect to see insurers taking a rollover position on renewal with some carriers pushing for rate increases.

Limits �� Insurers continue to offer higher than required limits; however, most clients chose to maintain their limits.

�� No material changes are expected.

While we expect insurers will continue offering increased limits, we do not foresee a catalyst for clients to materially change their program limits at this time.

Deductibles/Retentions �� Given the soft market conditions, there are

no material benefits for clients taking higher retentions.

�� No material changes are expected.

Coverage � Insurers continue to offer coverage enhancements. We have seen the development of annual DSU arrangements and some typical DSU extensions being included in the stand-alone MD Policy.

� We expect this trend to continue.

Capacity/Appetite �� While there continues to be an oversupply

of capacity, some insurers are retracting capacity where they believe pricing and coverage is unsustainable.

�� This trend is anticipated to continue.

We would expect more insurers to retract capacity; however, new entrants from other regions are still trying to enter the Australian Market for Construction Risks.

Losses � The second half of 2016 saw a number of large claim notifications hit the market from major projects.

� We would expect to see some new notifications hit the market as a number of LNG and Infrastructure projects head towards Practical Completion.

Property | CAR, EAR

The second half of 2016 saw another subtle shift in the property

market for construction risks. The introduction of a Multi-Speed

Market took effect. A number of carriers reviewed their pricing

strategies to return their portfolios to profitable levels, while

other insurers continued to aggressively target new business.

This does not mean that clients were experiencing pricing

increases; however, it did create a dilemma for those that

needed to weigh insurer relationships against alternative pricing

structures. Additional innovative coverages are still readily

available for all major projects, and annual policies as insurers

continue to try and differentiate from price.

Aon Risk Solutions 5

Liability | Primary Casualty

The second half 2016 had a “steady as she goes” approach in

the casualty market for construction risks. With an abundance

of capacity, certain carriers were still prepared to discount,

although the value of discounts diminished, particularly on

historical claims. We started to see a number of historical claims

make their mark, creating underwriter movement, which can

signal some market uncertainty for 2017.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change: There has been no material change; however, large discounts are becoming less available as pricing reaches minimum levels.

Clients are still able to achieve minor discounts if they are willing to remarket their accounts.

�� While we do not anticipate pricing increases, we do expect to see pricing decreases diminish further.

Limits � With an increase in market capacity, higher limits are easily attainable and competitively priced.

�� No material change is expected.

Deductibles/Retentions �� Given the soft market conditions, there are

no material benefits for clients taking higher retentions; however, clients with multiple Worker-to-Worker claims are considering higher deductibles for this cover.

�� No material change is expected.

Coverage � A number of insurers are considering innovative coverages within the liability policy to differentiate themselves from the competition. Extensions for Environmental Liability and Professional Indemnity are available under certain circumstances.

� This trend is expected to continue.

Capacity/Appetite � There continued to be an oversupply of

capacity in the market. �� No material change is expected.

Losses � A number of completed works claims were notified to the market. This resulted from the broadening of policy triggers over the last few years.

� No material change is expected.

Australia

6 Aon Construction & Infrastructure Market Report | Q4 2016

Liability | Excess Casualty

Similar to the first half of 2016, the current excess casualty markets capacity remains at an all-time high,

leaving little more room for rate compression.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate change: No material change; excess casualty premiums are at minimum treaty levels.

�� Rate change: No material changes are expected.

Limits � With an increase in market capacity, higher limits are easily attainable and competitively priced.

�� No material change is expected.

Deductibles/Retentions �� No material change. �� No material change is expected.

Coverage �� No material change as excess capacity is pure follow-form. �� No material change is expected.

Capacity/Appetite � There continued to be an oversupply of

capacity in the market. � We expect this trend to continue.

Losses �� No material change. �� No material change is expected.

Australia

Aon Risk Solutions 7

Liability | Professional

The professional liability market for construction risks saw a shift

in the latter half of 2016. As in the case of the property market,

a Multi-Speed Market took effect. A number of annual programs

obtained rate stabilization or increases, while project-specific

placements achieved low pricing and increased capacity with a

continuing competitive market.

In an effort to gain a competitive advantage, insurers are

innovating on project-specific coverages with a number of

enhancements, including tailored related parties coverage. The

challenge for 2017 is in ensuring enough capacity to provide

excess cover for long-term policies with broad cover.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate change: Annual programs saw rate stabilization or minor pricing increases where claims have been notified.

The premium levels on Project-Specific covers continue to be extremely competitive.

�� We expect this trend to continue.

Limits � A number of large infrastructure contracts are requiring higher limits as more parties are included to the contract.

� We expect this trend to continue.

Deductibles/Retentions �� No material change. �� No material changes are expected.

Coverage � A number of enhancements are still available, including tailored related parties coverages.

� We expect this trend to continue.

Capacity/Appetite � We saw London Capacity change their

appetite for Construction Projects and provide valuable competition for clients.

� We expect this trend to continue.

Losses � A number of historical notifications are starting to realize, as claims as the large infrastructure and LNG projects reach practical completion.

�� We expect this trend to continue.

Australia

8 Aon Construction & Infrastructure Market Report | Q4 2016

Canada

Property | Builders Risk, CAR, EAR

There is keen interest in large and complex projects from

both local and multinational contractors. Canadian work sites

are well regulated; for this reason, Canada is an attractive

business environment for overseas companies, including

Insurers. This environment enables an added level of

competitiveness to the market, especially with respect to

CAR, EAR, and Builders Risk coverages.

Insurers continue to pay close attention to projects located in

natural catastrophe zones as well as potential water damage

exposure. Underwriters are also beginning to question rate

adequacy, referencing underperforming lines of coverage.

The mid-market anticipates a stable environment from the

Property (COC) and Liability perspective for the coming quarter.

However, we should be apprehensive of key markets, such as

Zurich, which suggested last quarter that they were lowering

their new rate guidelines. Another issue impacting mid-market

is the amalgamation of markets, such as Liberty and Ironshore,

which can retract market capacity, as Ironshore has supported us

with property placements.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change:

Large Market: No material change.

Mid-Market: No material change.

�� Expected Rate Change: No material rate change is expected; should remain as competitive as ever with underwriters competing with London and European markets.

Limits �� Large Market: No material change. The majority of clients continue to purchase limits according to a project’s Total Insured Value and Probably Maximum Loss, factoring in natural catastrophe exposure.

Mid-Market: No material change.

�� No material change is expected.

Deductibles/Retentions ��� Large Market: No material change; specific peril

deductible levels, e.g. natural catastrophe, are set by project type and location. Water damage exposure attracts higher deductibles.

Middle Market: No material change.

�� No material change is expected.

Coverage �� Large Market: No material change; forms are almost exclusively manuscript.

Delay in start-up, soft costs, and consequential covers provided by DE / LEG language continue to garner attention.

Mid-Market: Due to the highly competitive market, mid-market placements are increasingly written on manuscript forms, allowing for broader cover than the general marketplace.

�� No material change is expected.

Natural catastrophe and water damage exposure will continue to be a focus for underwriters.

Capacity/Appetite �� No material change. Mega-projects are attracting

capacity with careful consideration for natural catastrophe exposures.

�� No material change is expected.

Losses � Certain large CAR losses have not fully materialized; however, projects (e.g. frame) are beginning to be priced close to technical terms.

Rulings / decisions have been made by the supreme court of Canada and the Appeal Court in certain Provinces regarding DE5 coverage and the broad interpretation of the coverage grant. Underwriters have taken notice but not yet reacted. Time will tell if they do.

�� No material change is expected for Q1 2017.

Aon Risk Solutions 9

Liability | Primary Casualty

Canadian work sites are well regulated; for this reason, Canada

is an attractive business environment for overseas companies,

including Insurers. This business environment enables an added

level of competitiveness to the market, especially in Wrap Up

coverage. However, there are local markets that compete with

London on certain projects.

A number of local underwriters continue to struggle to compete

with the U.K. & Lloyd’s insurers; however, some local underwriters

have had success: Berkshire, Ironshore, Northbridge, and AIG.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change: No material change. �� Expected Rate Change: No material change is expected.

Limits �� No material change. �� No material change is expected.

Deductibles/Retentions �� No material change. �� No material change is expected.

Coverage �� No material change; coverage remains broad with no restrictions. �� No material change is expected.

Capacity/Appetite �� No material change. �� No material change is expected.

Losses �� No material change. �� No material change is expected.

Canada

10 Aon Construction Market Report | Q2 2016

Liability | Excess Casualty

There is increased appetite for Canadian umbrella / excess risk,

accompanied by rate compression. Fixed premium-per-million

on excess placements can still be negotiated.

Depending on the risk, there are certain thresholds (minimum

premium-per-million) below which underwriters will not reduce

their pricing.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change: No material change.

Excess capacity is available at historically low rates. London insurers are leading the market in pricing.

�� Expected Rate Change: No material change is expected.

Limits �� No material change. �� No material change is expected.

Deductibles/Retentions �� No material change. �� No material change is expected.

Coverage �� No material change. �� No material change is expected.

Capacity/Appetite �� No material change. �� No material change is expected.

Losses �� No material change. �� No material change is expected.

Canada

Aon Risk Solutions 11

Liability | Professional

Competitive pricing and generally broad coverage continues

to be available on annual practice programs. Despite the

Canadian government’s large financial commitment to

infrastructure spending, the market for project-specific

placements has decelerated. 2015 was a blockbuster year for

project-specific activity, but current conditions are more in

line with activity from previous years. New entrant insurers are

seeking to strengthen their positions and create opportunities

through quick response time, lower underwriting requirements,

and more competitive premiums.

Clients operating in Western Canada, particularly Alberta,

continue to be impacted by the weaker economic environment.

These clients are trying to soften the blow through cost-cutting

options, including the cost of their professional insurance.

This has resulted in the increased marketing of programs. The

number of smaller regional firms ceasing operations altogether

has slowed significantly.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change: No material change.

In general, clients with moderate growth and a favorable loss experience achieved a rate reduction. However, insurers were reluctant to offer significant savings where premium levels have decreased.

�� Expected Rate Change: No material change is expected.

Economic challenges for Western-focused clients have resulted in the increased marketing of risks.

Limits �� No material change, barring a material change in a contractor’s business. �� No material change is expected,

except where compelled by contract.

Deductibles/Retentions �� No material change.

Retentions have largely remained constant, as the benefit of assuming more risk is negligible for most clients. However, clients based in the Prairies are exploring alternate deductible and retention structures in an effort to reduce their premium spend in a challenging economic environment.

�� No material change is expected.

Coverage ��� Coverage broadened as a result of expanding client contractual requirements, pressure from brokers, and increased insurer competition.

�� No material change is expected.

Capacity/Appetite ��� In order to overcome their historic high pricing models

and restrictive coverage, U.S.-led insurer entrants into the Canadian market are embarking on more internal evaluation to find their niche. This change in approach is driven by infrastructure spending anticipated to start in 2017.

London insurers are taking small steps to increase their visibility in the Canadian market. More autonomous domestic markets have taken advantage of the retrenchment of the more established markets. This continues to keep the market softer than expected for certain risks.

London insurers continue to provide solutions and innovations for proven and preferred clients on annual placements; however, they are more selective in how they deploy their capital and their enhanced cover. While some markets have limited their capacity (ex QBE), there continues to be enough market appetite to meet overall requests through excess layers or a quota share approach.

�� No material change is expected.

Losses �� Given the maturity of the projects, professional liability claims are more prevalent, regardless of delivery model. �� We expect this trend to continue.

Canada

12 Aon Construction & Infrastructure Market Report | Q4 2016

EMEA

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change: No material change.

Smaller pool of construction premium continues to drive competition.

� Expected Rate Change: 0% to -5%.

Flat to moderate rate reductions are expected throughout the balance of the year.

Limits �� No material change.

Construction projects continued to benefit from limits that reflect the full contract value. Inner sub-limits for certain policy extensions remain high.

�� No material change is expected.

Deductibles/Retentions �� Deductible levels have stabilized but remain at

historical lows. �� No material change is expected.

Coverage � In general, broad policy coverage remains available as insurers seek to maintain share. �� No material change is expected.

Clients continue to be well-positioned to push for broader coverage.

Capacity/Appetite � Market capacity remains at record high levels. This

competition continues to drive appetite. �� No material change is expected.

Losses �� No material change.

Moderate attritional losses continued, but no major losses threaten to impact market conditions.

�� No material change is expected.

Property | CAR, EAR

A buyer’s market continues to prevail. The activity of European

contractors has become truly global. The European insurance

market has endeavored to “follow” this business to maintain

premium levels that reflect lower domestic activity. The market

remains highly-competitive with no imminent sign of change.

Aon Risk Solutions 13

Liability | Professional

The professional market is split into three sectors in EMEA:

United Kingdom and Ireland, Continental Europe, and Middle

East and North Africa. Below are two tables, one for the U.K. and

Continental Europe, and another for the Middle East. The trends

for all regions are predominately the same, with small- and

medium-sized firms benefitting from rate compression.

Rates for large firms are flat or are increasing where significant

claims have been experienced. While insurer mergers have

reduced capacity to a degree, this has been more than offset

by new insurer entrants. This is expected to continue into 2017.

The top-tier London brokers have shown a broader utilization of

programs and facilities for small- to mid-market business.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � Rate Change: -1% to -5%

Generally, rates have decreased in absence of significant claims experience.

��� Expected Rate Change: 0% to -5%

Market sentiment suggests that overall loss ratios are deteriorating on historic years. This may result in a stabilization of rates.

Limits ��� Owners and contractors are seeking higher indemnity limits on large projects. �� Funders are driving indemnity limit requirements and

usurping Owners’ / Employers’ requirements.

Deductibles/Retentions �� Except where there are claims, retentions

have largely remained constant, as the benefit of assuming more risk is negligible for most clients.

��� Insurers are analyzing the effect of claims inflation on deductible/retention levels particularly in certain sectors.

Coverage �� Coverage is extremely broad. �� No material change is expected, other than Insured vs. Insured clauses, which are being scrutinized by insurers.

New insurers are still entering the market which will have an impact on capacity.

Capacity/Appetite ��� There is a surplus of capacity, particularly for

smaller firms, and an abundance of capacity from excess of loss insurers.

��� New insurers are still entering the market which will have an impact on capacity.

Losses ��� Increased claims due the size of projects. �� No material change is expected.

EMEA

EMEA ex Middle East

14 Aon Construction & Infrastructure Market Report | Q4 2016

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � Rate Change: -10% to -15%

Generally, rates have decreased in absence of significant claims experience and the continuing appetite of both local and regional Re/Insurers.

� Expected Rate Change: -20% to -50%

Increased appetite of local and regional Re/Insurers has further pushed the continued downward pressure on rates. International Reinsurers are to win large projects but happy to “wait it out’.

Limits ��� Owners and contractors appear to be asking for more informed SPPI insurance terms and conditions. Limits still vary.

�� Generally, there is a lack of understanding on sensible limits to purchase. Limits purchased are typically driven by contractual conditions.

Deductibles/Retentions �� There is continued pressure to have the lowest Retention

possible. ��� Re/Insurers are continually pressurized to offer lower Retentions while reducing premiums at the same time.

Coverage �� Coverage ranges from local basic average to extremely broad and is dependent on the Client and their purchasing mentality.

�� While some Owners are becoming more educated, the general understanding still allows for “basic” cover to be the norm. Local Re/Insurers are starting to offer London-based annual wordings for SPPI placements.

Capacity/Appetite ��� There is a surplus of capacity, particularly for smaller

firms, and an abundance of capacity from excess of loss insurers. However, due to aggregation squeeze / lack of capacity, small side contracts of large mega projects in region are seeing an inability to obtain even small limits.

��� No new Re/Insurers are expected with plenty of capacity available due to many projects being placed on hold or cancelled.

Losses ��� Still minimal in region. �� No material change is expected.

Middle East

EMEA

Aon Risk Solutions 15

Latin America

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � Rate Change: -1% to -5%

Lower anticipated investment in infrastructure projects has increased competition among insurers for a fewer number of projects.

� Expected Rate Change: -1% to -5%

Moderate rate reductions are expected throughout 2016.

Limits �� No material change. �� No material change is expected.

Deductibles/Retentions � While some insurers previously set retentions as a

percentage of loss with a minimum value, there has been a growing trend to apply a flat rate.

� We expect this trend to continue.

Coverage � LEG 3 is becoming more commonplace for certain types of construction. � We expect this trend to continue.

Capacity/Appetite � There is an abundance of capacity in the Latin

American market This is due to new insurer entrants and foreign capacity deployed on LatAm risks where there is a foreign contractor performing the work.

� We expect this trend to continue.

Losses �� No material change.

While not significant enough to impact the market, there were unexpected losses in wind farms related to windstorms that had not previously experienced with this type of construction.

�� No material change is expected.

Property | Builders Risk, CAR, EAR

2016 was the hardest year for the construction industry in recent

years for the Latam region. Negative factors, including oil and

commodity prices, the political environment and corruption,

all contributed to a decrease in investment for infrastructure

projects across the region. Brazil experienced corruption

scandals, which are affecting other countries at a regional level.

This includes the bribery scandal of Odebrecht, which admitted

to a U.S. court that it paid bribes in 12 countries across the

region. The consequences are still under analysis in each country.

On the other hand, according to industry sources, in 2016,

Colombia and the U.S. were the world’s most active P3 markets.

We expect to have the major investments on construction,

focused on power systems, located in Argentina, Central

America, Mexico, Peru and Chile. But the level of uncertainty

remains high for the main economics of the region.

The risk capital from local and international insurers continues

to be competitive and abundant. This means a soft market with

competitive rates and excellent terms and conditions.

16 Aon Construction & Infrastructure Market Report | Q4 2016

Liability | Primary Casualty

Latin American countries are not considered litigious. Thus,

limits for casualty insurance are moderate compared to other

geographies. The largest and most complex projects are analyzed

on a case-by-case basis. International lenders are also monitoring

the liability exposures and policies, which may translate to

higher limits of liability in the future. Given the compressed rate

environment, we believe there is room for higher casualty limits

on future projects.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � Rate Change: -5% to -10%

The number of new projects is shrinking, leading to market competition and rate reduction.

� Expected Rate Change: -5% to -10%

This trend is expected to continue

Limits � Given the soft market conditions, clients are increasingly considering purchasing higher limits.

� We expect this trend to continue.

Deductibles/Retentions �� No material change. �� No material change is expected.

Coverage �� No material change. �� No material change is expected.

Capacity/Appetite � Available capacity expanded due to new

entrants at local and regional levels. � We expect this trend to continue.

Losses �� No material change. �� No material change is expected.

Latin America

Aon Risk Solutions 17

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � Rate Change: -1% to -5% � Expected Rate Change: -1% to -5%

New insurer entrants should result in further rate compression.

Limits � Owners, employers, and lenders are all seeking higher indemnity limits on large projects.

� We expect this trend to continue.

Deductibles/Retentions �� No material change. �� No material change is expected.

Coverage �� Coverage is already very broad. �� No material change is expected.

Capacity/Appetite � Capacity was abundant as new insurer

entrants continued to add capacity to the market.

� We expect this trend to continue.

Losses � Claims have increased along with the growing size and complexity of projects. � No material change is expected.

Liability | Professional

Latin America

18 Aon Construction & Infrastructure Market Report | Q4 2016

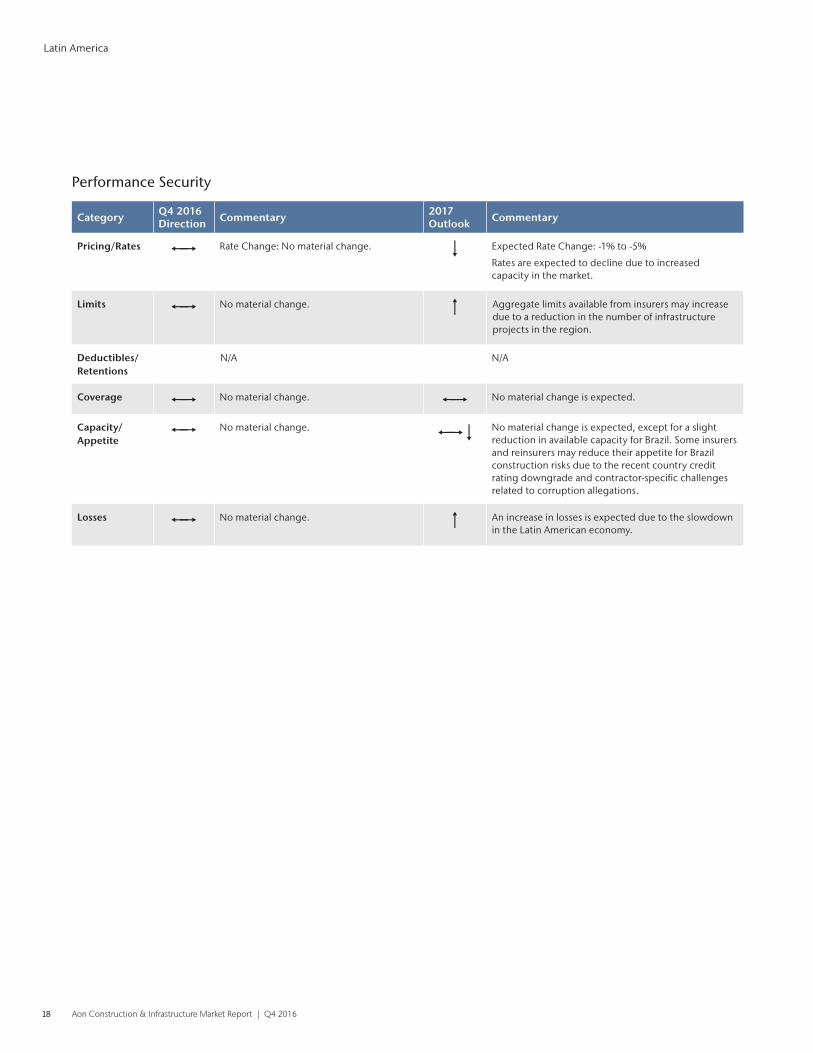

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates �� Rate Change: No material change. � Expected Rate Change: -1% to -5%

Rates are expected to decline due to increased capacity in the market.

Limits �� No material change. � Aggregate limits available from insurers may increase due to a reduction in the number of infrastructure projects in the region.

Deductibles/Retentions

N/A N/A

Coverage �� No material change. �� No material change is expected.

Capacity/Appetite �� No material change. ��� No material change is expected, except for a slight

reduction in available capacity for Brazil. Some insurers and reinsurers may reduce their appetite for Brazil construction risks due to the recent country credit rating downgrade and contractor-specific challenges related to corruption allegations.

Losses �� No material change. � An increase in losses is expected due to the slowdown in the Latin American economy.

Performance Security

Latin America

Aon Risk Solutions 19

United States

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates ��� Rate Change:

Primary: -1% to -5% due to insurer competition.

Excess: -5% to -10% due to an abundance of capacity.

� Expected Rate Change:

Primary: -1% to -5% due to insurer competition.

Excess: -1% to -5% with greater reductions possible in upper layers.

Data indicates a continued return to favorable market conditions with rate compression. The Residential Excess and Surplus Lines marketplace is softening, but admitted insurers continue to avoid this segment.

Limits �� Clients are maintaining limits purchased. �� The majority of clients are expected to maintain their

excess casualty limits.

Deductibles/Retentions �� Most clients have maintained their

deductible/retention levels as insurers have remained firm on retention levels.

�� Most clients are expected to maintain their deductible levels; however, clients with poor loss experience or low deductibles relative to the exposure continue to feel pressure from insurers to increase retentions. Lead umbrella insurers are also exerting pressure on the attachment point for clients with significant fleets or with poor loss experience.

Coverage ��� Coverage and program design enhancements were available. ��� We expect reasonable coverage and program design

enhancements to be available as insurers put a greater emphasis on managing their risk aggregation on a potential single loss scenario.

Capacity/Appetite ��� Excess casualty capacity remains at

record levels. ��� We expect this trend to continue. Capacity for lead excess layers is expected to increase.

Losses �� No material change. �� No material change is expected.

Many insurers are experiencing deterioration in their Auto Liability underwriting results. This may push rates higher in the future.

Liability | Primary, Excess & Auto

Overall, the U .S . market for construction remains competitive . We are starting to experience initial signs of some rate stabilization and while the market competition and capacity remain abundant, the deterioration of underwriting results is indisputable . Insurers with challenged portfolios continue to rebalance their business mix through coverage, deductible, premium and risk selection strategies understanding there are competitive alternatives for most insureds that demonstrate favorable loss histories . Poor underwriting performance in

automobile coverage is a notable macro trend across the general U .S . insurance marketplace . Most portfolios are realizing loss pressure, and larger fleets will likely impact both primary and excess programs . It is estimated the spike in losses comes from a host of interrelated issues, including increased mileage due to lower fuel cost, continued use of communication devices (notably texting), rising healthcare costs, and the cost to repair vehicles with increasingly sophisticated electronic components .

20 Aon Construction Market Report | Q2 2016

Liability | Professional

The professional liability market for construction risks remains

generally stable and competitive for both annual practice

and project-specific policies. Insurance capacity is at an all-

time high with an unprecedented number of insurers and

programs active in the market. Despite a moderate slowing

in the U.S. economy, construction activity is still strong across

most sectors and regions with design and construction firms

typically reporting increased revenues. Even with these revenue

increases, the market has surplus capacity, and yielding some

of the softest market conditions in recent history. The resulting

overabundance of capacity is good for buyers. However,

insurers are facing a fundamentally difficult landscape due to a

pronounced and increasing in the frequency of large claims and

the cost of defense (especially on large construction defect-

related claims). This situation, coupled with strong competition,

is hampering their attempts to lift pricing in response to higher

claims costs. It has also led to at least one insurer temporarily

suspending acceptance of new primary business until pricing

begins to improve.

Use of alternative project delivery methods, particularly

design-build, is rapidly increasing. For example, the majority of

large, non-residential public projects are now being delivered

on a design-build basis. This trend is closing the gap between

the U.S. and other regions where such delivery methods are

more common.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � Expected Rate Change: -1% to -5% due to continuing abundance of capacity � Expected Rate Change: -1% to -5% due to abundance

of capacity

Limits �� Clients are maintaining limits purchased. � Many clients are considering increasing their limits due to capacity available at attractive terms.

Deductibles/Retentions �� Most clients have maintained their

deductible/retention levels. �� No material change is expected.

Coverage ��� No material change. ��� Competition has caused insurers to explore coverage enhancements in order to differentiate their offerings and not compete exclusively on price.

Capacity/Appetite � Excess professional liability insurers offered

an abundance of capacity, often in excess of $250 million.

� Capacity is expected to increase due to the entry of several new professional liability insurers in the U.S. and London markets.

Losses ��� Claims activity in the Construction sector was fairly constant, but claims severity increased.

��� We expect this trend to continue.

United States

Aon Risk Solutions 21

Property

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � Rate Change: -1% to -5%

Larger and more complex client risks experienced a rate decrease for the quarter.

� Expected Rate Change: -5% to -10%

We expect high single- to double-digit rate decreases driven by oversupply, significant sign-downs, and a lack of catastrophic loss activity.

Limits ��� Nearly 95% of risks purchased the same or higher limits. ��� The abundance of supply coupled with the downward

pressure on price could make higher limits more attainable.

Deductibles/Retentions ��� Over 90% of risks purchased the same or

lower deductible/retention levels. �� No material change is expected.

Coverage �� No material changes in property coverage were seen as broad property coverage is readily available in the market.

�� No material change is expected. Flood and contingent business interruption continue to be carefully underwritten by most insurers.

Capacity/Appetite �� Most insurers offered similar line sizes. ��� Capacity is expected to be more than adequate to meet

buyer demand.

Losses �� No material change. �� No material change is expected.

United States

22 Aon Construction Market Report | Q2 2016

Property | Builders Risk

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates ��� Rate Change: -1% to -5%

Clients largely saw flat to declining rates due to high levels of capacity and competition among insurers; however, frame building contractors have continued to experience a hard market due to recent losses.

��� Expected Rate Change: -1% to -5%

National contractors with non-catastrophic exposures are expected to continue to see flat and declining rates in the absence of a large catastrophic event that would decrease available capacity.

Limits �� No material change. �� No material change is expected.

Deductibles/Retentions �� Most insurers have maintained deductibles,

although we have seen increased deductibles and retentions for prototypical equipment and testing.

�� This trend is expected to continue with increased capacity driving insurers to maintain deductibles. In areas highly susceptible to catastrophic events, deductibles are remaining constant, the main driver being percentage of value at risk at time of loss.

Coverage �� The market remained soft with broad coverage grants achievable as insurers felt pressure to retain business.

�� Increasing competition in a soft market will maintain pressure on insurers to hold broad coverage terms while preserving flat rates.

Capacity/Appetite ��� With all risk placements, we have seen

increased capacity in the market estimated at $3.5 billion U.S.D. Catastrophic-related capacity in high aggregation zones, such as Miami / Houston wind and California quake, is demonstrating moderation and less concern by the markets.

��� Capacity will remain flat or slightly up for non-catastrophic risks, while aggregation will continue to be an issue in high risk areas as the market has approximately $1.5 billion U.S.D in catastrophic capacity and construction continues to grow.

Losses �� No material change. �� No material change is expected.

United States

Aon Risk Solutions 23

Subcontractor Default Insurance | SDI

While SDI carrier appetite has stabilized around the risks they will

consider writing, expect a persistence of the hard market that

has been underway since 2015. General contractors renewing

SDI programs continue to assess options of increased retentions,

premiums, and coverage preferences. Each SDI insurance carrier

offers unique coverage considerations which must be evaluated

alongside the insured’s current and longer term market segment

and geographic goals.

The introduction of a fourth SDI insurance carrier, Cove

Programs, has provided some relief to U.S. market capacity

concerns; however, only Zurich and XL Catlin currently offer

Canadian based SDI programs. Larger scale construction projects

with higher value and longer-duration subcontractor packages

will continue to challenge existing SDI capacity.

With intent on obtaining the broadest of available SDI terms in a

more restrictive underwriting market, general contractors should

continue to allow additional time for marketing, underwriting,

negotiation and renewal of their existing programs and any

referral submissions.

Category Q4 2016 Direction Commentary 2017

Outlook Commentary

Pricing/Rates � In general, rates continued to rise, but were driven on a case-by-case basis with retention levels playing a major role.

� No change. Clients seeking as expiring or a reduction in existing rates will continue to consider increased retentions, as well as reductions in the completed operations period coverage and optional per-loss sub-limits.

Limits �� No material change. Clients are maintaining limits. �� No material change is expected.

Deductibles/Retentions � Clients have elected to increase retentions

to ease the pressure of the rate increase. Those with poor loss experience or low deductibles relative to the exposure are seeing fewer retention options.

� No material changes are expected.

Coverage � More narrow coverage with emphasis on aversion to “for sale” residential portfolios, Florida, offshore fabricated components, and longer coverage durations. Coverage restrictions apply to certain trade classes.

� This trend is anticipated to continue, along with expected reductions in exposure to certain third-party claim support expenses.

Capacity/Appetite �� While overall capacity has increased with

a fourth SDI insurance insurer option, insurance carrier risk appetite continues to be a challenge. Capacity for project-specific policies and subcontractor aggregation (large trade contacts) are already a significant challenge in Canada.

� Insurance carrier risk appetite will continue to challenge insureds with project-specific, residential, and large subcontractor enrollment projects. Insurance carrier aversion to significant subcontractor risk aggregation is reflected in referral submission non-approvals. Expect increased interest in dual insurance programs, excess, and quota share.

Losses �� While claim frequency has stabilized, claim severity continues to be a market-specific trend with some markets continuing to incur noteworthy claims.

�� Claim frequency and severity trends generally show signs of retraction.

United States

24 Aon Construction & Infrastructure Market Report | Q4 2016

Contacts

Global

Nate EspeChicago, [email protected]

Geoffrey HeekinChicago, [email protected]

Michael HerrodHouston, [email protected]

Henry LombardiNew York, [email protected]

Tariq TaherbhaiChicago, [email protected]

Africa

Darlington MunhuwaniJohannesburg, South [email protected]

Justin RussellJohannesburg, South [email protected]

Michiel Ebeling KoningAmsterdam, [email protected]

Sebastian KorczStuttgart, [email protected]

James MacNealLondon, [email protected]

Olof MångsStockholm, [email protected]

Francesco PeriniMilan, [email protected]

Latin America

Clemens FreitagSao Paulo, [email protected]

Alexander RianoMiami, [email protected]

Milena Milani SoaresMiami, [email protected]

Mariano VialeMiami, [email protected]

Asia & Pacific

Alister BurleyMelbourne, [email protected]

Mark ChanShanghai, [email protected]

Junko KunimitsuTokyo, [email protected]

Nicki TilneySingapore, [email protected]

Europe & Middle East

Steffen AabelOslo, [email protected]

Jean-David BenatarParis, [email protected]

Alfonso Garcia LarriuMadrid, [email protected]

Karl HennessyLondon, [email protected]

Robert HumphreysLondon, [email protected]

North America

David BowcottToronto, [email protected]

Galen BrislanePembroke, [email protected]

Doug CorreaVancouver, [email protected]

Allan HetzToronto, [email protected]

Scott TretheweyMiami, [email protected]

Matt WalshChicago, [email protected]

Kevin WhiteBoston, [email protected]

About Aon Aon plc (NYSE:AON) is a leading global provider of risk management, insurance brokerage and reinsurance brokerage, and human resources solutions and outsourcing services. Through its more than 72,000 colleagues worldwide, Aon unites to empower results for clients in over 120 countries via innovative risk and people solutions. For further information on our capabilities and to learn how we empower results for clients, please visit: http://aon.mediaroom.com.

© Aon plc 2017 . All rights reserved .The information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Risk . Reinsurance . Human Resources .