GIIC 2016-Kishore Hota, Addl. General Manager, NTPC Ltd.

21

Gas / RLNG : Power Sector Perspective Kishore K. Hota Addl. GM (Corp. Fuel Mgmt.) NTPC Limited Gas Infrastructure India 2016 22 July, 2016, New Delhi

-

Upload

kuldeepprospur -

Category

Presentations & Public Speaking

-

view

124 -

download

0

Transcript of GIIC 2016-Kishore Hota, Addl. General Manager, NTPC Ltd.

Gas / RLNG :

Power Sector Perspective

Kishore K. Hota

Addl. GM (Corp. Fuel Mgmt.)

NTPC Limited

Gas Infrastructure India 2016

22 July, 2016, New Delhi

Sustainable in comparison to coal

Thermal Efficiencies ~ 50-55%, about 50% carbon emissions compared to coal

Less NOX / SOX emissions/ SPM levels, No ash issues

Lower capital cost

CCGT ~ 0.58 to 0.75 million USD/MW, Coal ~ 1 to 1.17 million USD /MW

Shorter gestation period

~ 24 to 30 months for CCGT commissioning as compared to ~ 40 to 45 months for coal based plant

Less land and water requirementWater requirement around 25% as compared to coal plant

Suitable for Peaking as well as Base load requirements

Ideal for Integration of Renewable power in the grid

Significant growth in Renewables (Wind & Solar) in the last decade in India

Natural Gas - Preferred Fuel Option for Power Generation

Source: IEO2016 Reference case , EIA

22%

29%

22%

28%

40%

29%

Growth Rate:

Renewables (non-hydro): 5.7%/year

Natural gas: 2.7%/year

Nuclear: 2.4%/year

Coal: 0.8%/year

World : Projected Share of Various Sources in Power Generation

EIA indicates that in spite of significant growth in Renewables, fossil fuels continue to play important

role in global power generation mix through to 2040

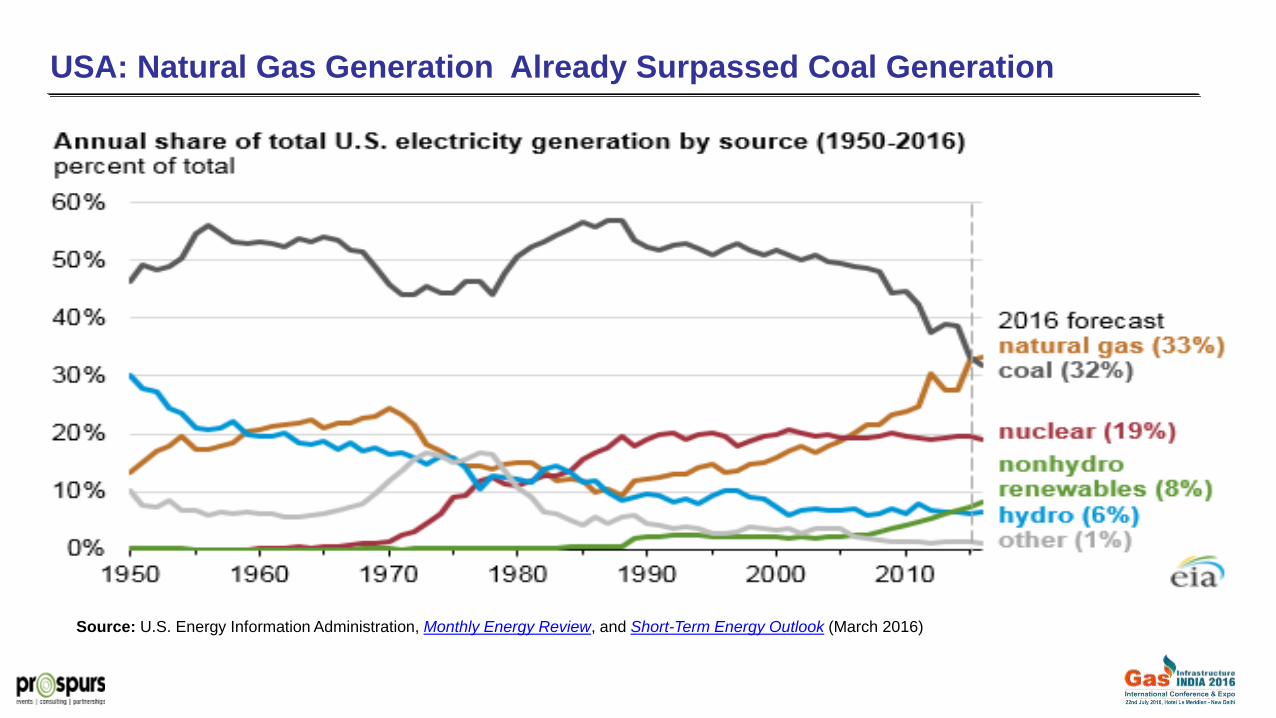

USA: Natural Gas Generation Already Surpassed Coal Generation

Source: U.S. Energy Information Administration, Monthly Energy Review, and Short-Term Energy Outlook (March 2016)

Source: U.S. Energy Information Administration, Monthly Energy Review, and Short-Term Energy Outlook (March 2016)

USA – Cost of Coal /Gas for Power Generation

Installed Capacity

Fuel MW %age

Total Thermal 210675 70.68

Coal 185173 62.13

Gas 24508 7.74

Diesel 993.5 0.33

Hydro (Renewable) 42783 16.03

Nuclear 5780 1.94

Renewable sources 38821.5 13.02

Total 298060 100.00

Installed Capacity as on 31st March, 2015

Source – CEA

Against installed Capacity of ~8%, share of Gas based electricity Generation in total

generation is less than 4%

Power Sector Overview in India

8.22%

0.33%

14.35%

1.94%

13.02%

62.13%

Coal

Gas

Diesel

Hydro

Nuclear

Renewable sources

IEO2016 Reference case- Net electricity generation in India increases @ 3.5%/year

INDIA : Projection of Electricity Generation Mix by 2040

INDIA : Projection of Electricity Generation Mix by 2040

Source: IEO2016 , EIA

Energy & Peak deficit which was more than 11% in financial year 2008-09 has dropped to

2.1% in 2015-16. 45,000 MW of conventional generation capacity added in last 2 years (22% growth)

Record 3019 MW Solar and 3300 MW Wind power capacity added in 2015-16. Fast

reduction in Renewable power tariffs

PLF of Coal stations in the country has fallen - significant URS power

CIL recorded a 6.9% increase in coal production in 2014-15 and 8.6% in 2015-16

Rationalisation/ Flexibility of linkages/ transportation of Coal

Reduction in Imported coal by 34.26 MT. Cost of Imported Coal significantly low globally

MoP’s UDAY Scheme – to improve the Discom’s financial health (Discoms losses: Rs. 60,000-

70,000 crore annually), Reduction in Cost of power generation

24x7 power and ATC reduction targets by 2022

Data source: CEA

India : Present Power Demand & Supply Position

India: Situation of Gas based Capacity in Jan 2015

Gas Requirement @70% PLF Gas Supply to Power Sector in 2014-15 (April- Jan)Gas

Shortage Commissioned

Ready for Commissioning

APM/PMT/NonAPM

KG D6Long Term

RLNGSpot RLNG Total

71.13 21.0414.58 0 1.42 0.38 16.38

75.80 (54.75 for existing +21.04 for new)Total 92.17

Gas based capacity

27,123 MW

21,874 MW

Commissioned5,349 MW

Ready for commissioning

Gas grid Connected

24,150 MW

Off - gas grid

2,774 MW Off - gas grid

200 MW

Stranded

14,305 MW

Domestic gas based

9,845 MW (32.2% PLF)

All CCGTs

Sharp Fall in Availability of Domestic gas

RLNG still not competitive in ‘Merit Order’ power generation – Take or Pay

(ToP) issues

Lack of availability of Infrastructure (Pipelines & Regas Terminals)

Regulatory issues

Issues with Taxes/ duties

Major Issues Of Concern

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17*

Net Domestic Gas

production 126.92 108.91 94.72 89.57 85.08 65.55

RLNG import 42.11 39.57 48.57 50.78 58.22 69.24

Total 169.03 148.48 143.29 140.35 143.3 134.79

*upto May, 2016

Source: PPAC

Supply Trend of Domestic Gas & RLNG

MMSCMD

13.27

7.436.84

6.255.58 5.81

6.37 6.6

11.03

6.74 6.3 5.865.37 5.54 5.96 6.12

0

2

4

6

8

10

12

14

2016 2016 2016 2016 2016

Dec, 2015 Jan, 2016 Feb, 2016 March, April, May, June, July,

0

2

4

6

8

10

12

14

16

18

20

LT RLNG Basic price Variable Cost

Vari

ab

le C

ost

of

po

wer

in

UP

Gas p

lan

t (R

s/u

nit

)

PL

L L

T R

LN

G B

asic

Pri

ce*

(US

$/M

MB

tu)

Price Trend of RLNG and Cost of Power Generation

*Forex component

Contributions/ Sacrifices by Stakeholders

Making “e-Bid RLNG”

affordable

GoI waivers- Customs duty

- Service tax on Transptn

& Regasification

- CTU charges and losses

- Provision of Commingling

and Swapping

State Govt waivers- VAT/CST/Entry tax

- STU charges and losses

Stranded DevelopersCapping of Fixed cost

with No Return on Equity

Transporters50% discount on

Transportation

Gas Seller (GAIL)75% discount on

Marketing Margin

Regasifiers- 50% discount on

Regas Charges

GoI Financial Supportfrom

PSDF Fund

Banks-Restructuring of Loans

-Support for WC

MoP Scheme on ‘e-Bid RLNG’ : Making RLNG Affordable for Power Generation

Reverse e-bidding Process: Boundary Conditions

Reverse Bidding

Target Price*

Set by EPMC

Target PLFSet by EPMC

Ceiling for Bidding

Set by EPMC

RLNG qty.As per

Regasification Capacity & Target PLF

PSDF supportFixed by GoI:

FY 2016 :Rs 3500 Cr

FY 2017: Rs 4000 Cr

Bidders to be ranked in the order of minimum PSDF support on ascending order basis

*Target Price : Max. Net Purchase Price for Discom

Transaction Structure (DGP category)

Gas Based Plant

(DGP category)

MoP

Pool Operator (GAIL)

DISCOM

PSDF Support

Agreement

e-BID RLNG

Sales Agreement

PPA

Gas supply/

Payment

PSDF Support (Y)

Trust & Retention A/c

(TRA)

Net Price to Discom (X) +

PSDF Support (Y)

X+Y = Fuel

cost

Impact /Issues of e-Bid RLNG Scheme

11,717 MW of Gas projects have started generating power in 2015-16

3 Phases of Bidding completed successfully.

4th Phase (last phase) Bidding likely in Aug-Sept, 2016

Amendment in Section 3 of CST Act, 1956 done thru Finance Bill, 2016,

will result in increased gas supplies through swapping, reduced tax

implications and legitimacy of inter-State CST sale of comingled gas

Issues of VAT, Entry tax exemptions in certain States to be addressed

Issue of Base PLF for DGP category plants need to be addressed

Target Price: may be reduced in view of reduction in cost of power

generation in the grid

Target PLF : may be increased in view of the increase in Regas capacity

The Scheme may be extended beyond March, 2017 as this will help utilisation of the

stranded capacity and benefit the Grid while balancing the Renewable power

Taxes/ duties

Customs Duty (CD) exemption is still not available for LT LNG imported by M/s PLL

Present VAT varies across States (0% in Delhi to 26% in UP) & has significant impact on cost of Power

Regulations

Reasonable Transportation Tariff – to promote Swapping of gas, uniform Gas grid

Reasonable Regasification charges, Transparent Third party/Open access in Regas terminals

Flexibilities in GTAs/ GSAs – Firm and Interruptible transportation, Model agreements

Need for aligning the regulations of CERC & PNGRB – Gas / Transportation scheduling revision issue

Timely implementation of Trunk pipelines

Transparent implementation of Open Access and Affiliate Code of Conduct Regulations

Strengthening the PNGRB Act

DC requirement of 85% for Gas power plants needs to be lowered

Regulation / Taxation Issues

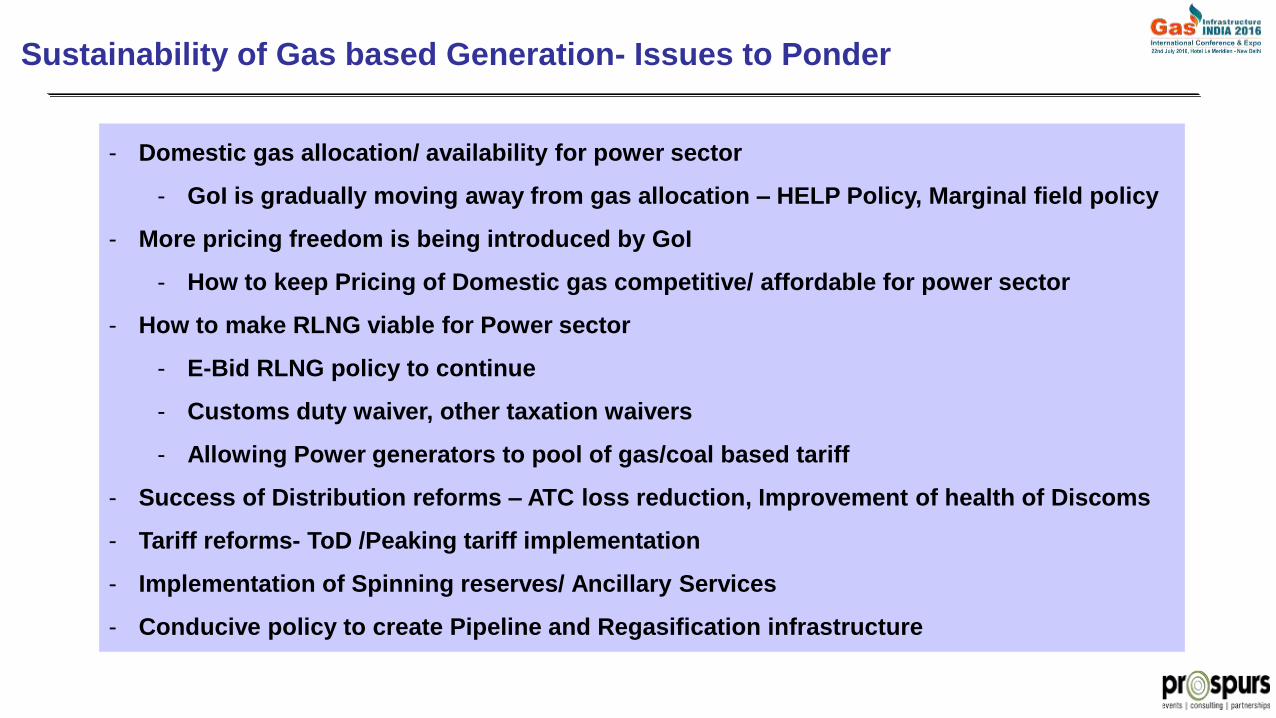

Sustainability of Gas based Generation- Issues to Ponder

- Domestic gas allocation/ availability for power sector

- GoI is gradually moving away from gas allocation – HELP Policy, Marginal field policy

- More pricing freedom is being introduced by GoI

- How to keep Pricing of Domestic gas competitive/ affordable for power sector

- How to make RLNG viable for Power sector

- E-Bid RLNG policy to continue

- Customs duty waiver, other taxation waivers

- Allowing Power generators to pool of gas/coal based tariff

- Success of Distribution reforms – ATC loss reduction, Improvement of health of Discoms

- Tariff reforms- ToD /Peaking tariff implementation

- Implementation of Spinning reserves/ Ancillary Services

- Conducive policy to create Pipeline and Regasification infrastructure

Thank YouDisclaimer

The views expressed in this presentation are solely are of the presenter, and may not necessarily represent views of NTPC Limited

E mail : [email protected] [email protected]: +91 9650991215

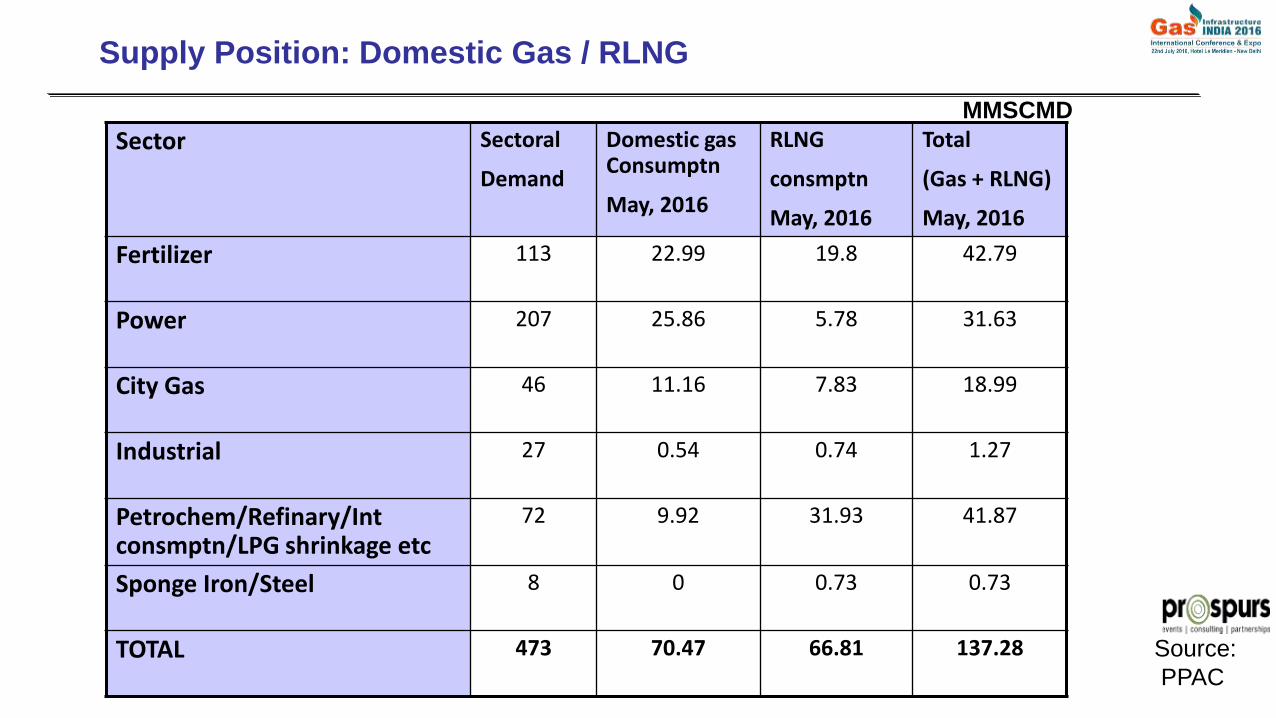

Sector Sectoral

Demand

Domestic gas Consumptn

May, 2016

RLNG

consmptn

May, 2016

Total

(Gas + RLNG)

May, 2016

Fertilizer 113 22.99 19.8 42.79

Power 207 25.86 5.78 31.63

City Gas 46 11.16 7.83 18.99

Industrial 27 0.54 0.74 1.27

Petrochem/Refinary/Int consmptn/LPG shrinkage etc

72 9.92 31.93 41.87

Sponge Iron/Steel 8 0 0.73 0.73

TOTAL 473 70.47 66.81 137.28

Supply Position: Domestic Gas / RLNG

Source:

PPAC

MMSCMD